Individual Report: Accounting for Business Decisions - HC1010, T2 2019

VerifiedAdded on 2022/11/17

|8

|1450

|90

Report

AI Summary

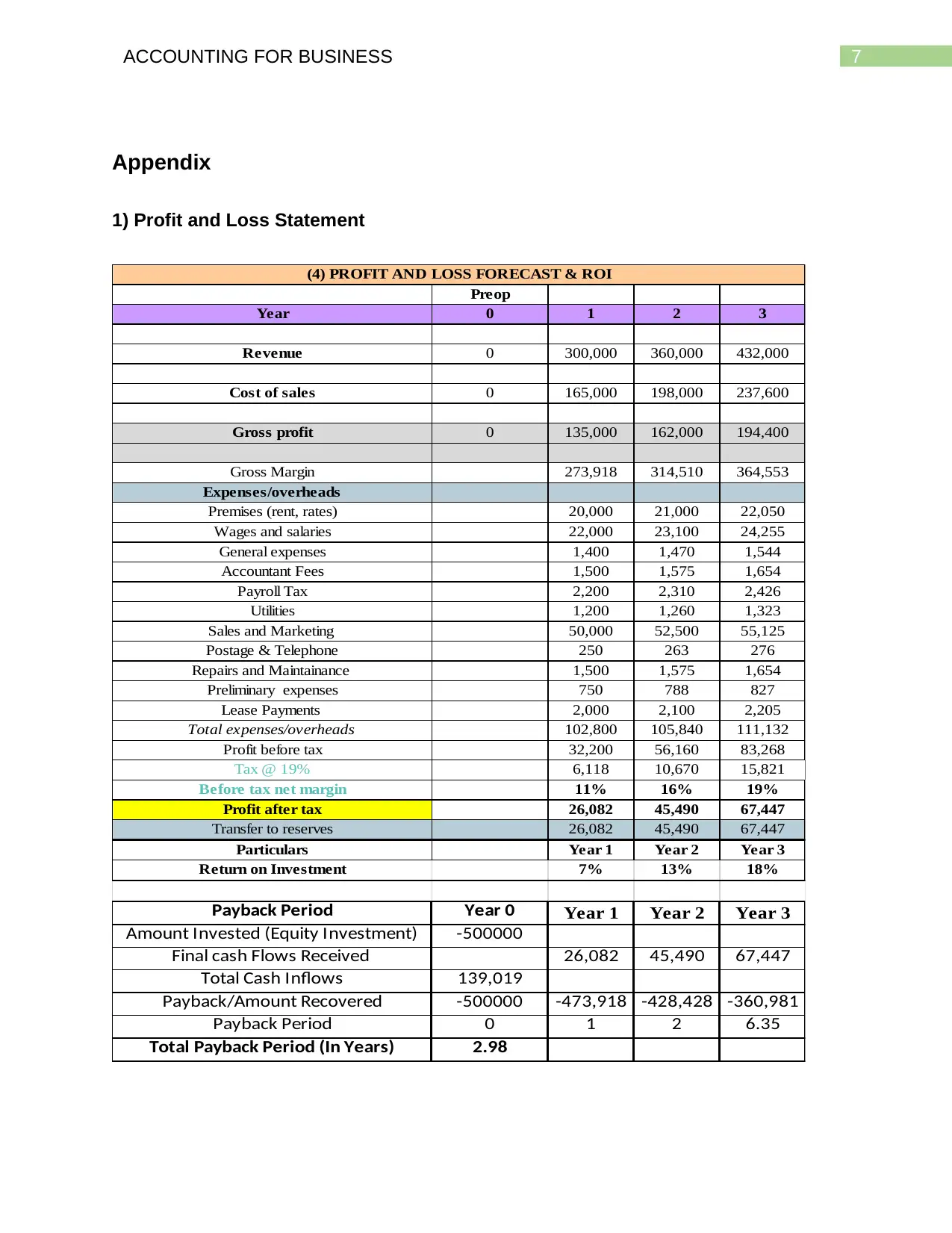

This report, prepared for the Holmes Institute's HC1010 unit on Accounting for Business, examines key aspects of business accounting. It begins by outlining different forms of business organization, including sole proprietorships, partnerships, and corporations, and discusses their respective advantages and disadvantages, particularly focusing on their implications for Tim's business. The report then delves into the availability of finance for each organizational form, exploring how different structures affect the ability to raise capital through equity shares, short-term borrowings, and personal investments. It also examines the significance of both accounting and non-financial information in making informed business decisions, with a focus on skills and accounting knowledge required for success. The report includes a profit and loss statement in the appendix and concludes by recommending the corporate form of business organization for Tim.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.