CSR Ltd & Boral Ltd: Detailed Financial Ratio Analysis Report

VerifiedAdded on 2023/03/31

|11

|1861

|104

Report

AI Summary

This report analyzes the financial performance of CSR Ltd, a major building products company, in comparison to its competitor, Boral Ltd, using key financial ratios. The analysis covers profitability, solvency, and liquidity, providing insights into the companies' operational efficiency and financial health from 2016 to 2018. CSR Ltd demonstrates strong asset turnover and profitability, but faces challenges in inventory management and cash cycle efficiency. Recommendations for CSR Ltd include cost reduction, improved inventory management, and shortening the cash cycle to enhance liquidity and overall performance. The report concludes that while CSR Ltd performs well in certain areas, implementing suggested improvements will further strengthen its business structure and competitive position.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

Name of the Student:

Name of the University:

Author’s Notes:

Accounting for Business

Name of the Student:

Name of the University:

Author’s Notes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction......................................................................................................................................2

Financial Ratio Analysis..................................................................................................................2

Recommendation.............................................................................................................................5

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................7

Appendix..........................................................................................................................................9

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction......................................................................................................................................2

Financial Ratio Analysis..................................................................................................................2

Recommendation.............................................................................................................................5

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................7

Appendix..........................................................................................................................................9

2

ACCOUNTING FOR BUSINESS

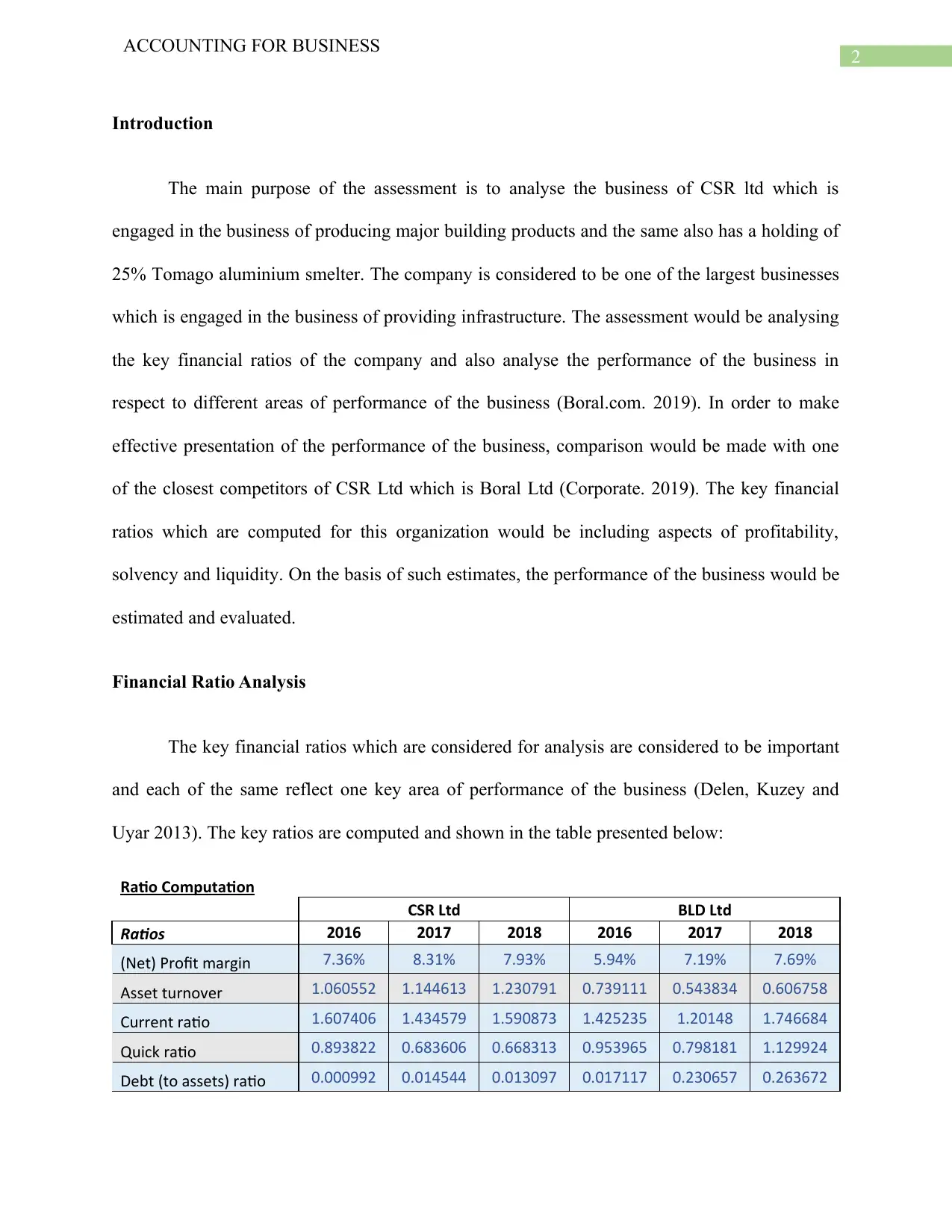

Introduction

The main purpose of the assessment is to analyse the business of CSR ltd which is

engaged in the business of producing major building products and the same also has a holding of

25% Tomago aluminium smelter. The company is considered to be one of the largest businesses

which is engaged in the business of providing infrastructure. The assessment would be analysing

the key financial ratios of the company and also analyse the performance of the business in

respect to different areas of performance of the business (Boral.com. 2019). In order to make

effective presentation of the performance of the business, comparison would be made with one

of the closest competitors of CSR Ltd which is Boral Ltd (Corporate. 2019). The key financial

ratios which are computed for this organization would be including aspects of profitability,

solvency and liquidity. On the basis of such estimates, the performance of the business would be

estimated and evaluated.

Financial Ratio Analysis

The key financial ratios which are considered for analysis are considered to be important

and each of the same reflect one key area of performance of the business (Delen, Kuzey and

Uyar 2013). The key ratios are computed and shown in the table presented below:

Ratio Computation

CSR Ltd BLD Ltd

Ratios 2016 2017 2018 2016 2017 2018

(Net) Profit margin 7.36% 8.31% 7.93% 5.94% 7.19% 7.69%

Asset turnover 1.060552 1.144613 1.230791 0.739111 0.543834 0.606758

Current ratio 1.607406 1.434579 1.590873 1.425235 1.20148 1.746684

Quick ratio 0.893822 0.683606 0.668313 0.953965 0.798181 1.129924

Debt (to assets) ratio 0.000992 0.014544 0.013097 0.017117 0.230657 0.263672

ACCOUNTING FOR BUSINESS

Introduction

The main purpose of the assessment is to analyse the business of CSR ltd which is

engaged in the business of producing major building products and the same also has a holding of

25% Tomago aluminium smelter. The company is considered to be one of the largest businesses

which is engaged in the business of providing infrastructure. The assessment would be analysing

the key financial ratios of the company and also analyse the performance of the business in

respect to different areas of performance of the business (Boral.com. 2019). In order to make

effective presentation of the performance of the business, comparison would be made with one

of the closest competitors of CSR Ltd which is Boral Ltd (Corporate. 2019). The key financial

ratios which are computed for this organization would be including aspects of profitability,

solvency and liquidity. On the basis of such estimates, the performance of the business would be

estimated and evaluated.

Financial Ratio Analysis

The key financial ratios which are considered for analysis are considered to be important

and each of the same reflect one key area of performance of the business (Delen, Kuzey and

Uyar 2013). The key ratios are computed and shown in the table presented below:

Ratio Computation

CSR Ltd BLD Ltd

Ratios 2016 2017 2018 2016 2017 2018

(Net) Profit margin 7.36% 8.31% 7.93% 5.94% 7.19% 7.69%

Asset turnover 1.060552 1.144613 1.230791 0.739111 0.543834 0.606758

Current ratio 1.607406 1.434579 1.590873 1.425235 1.20148 1.746684

Quick ratio 0.893822 0.683606 0.668313 0.953965 0.798181 1.129924

Debt (to assets) ratio 0.000992 0.014544 0.013097 0.017117 0.230657 0.263672

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FOR BUSINESS

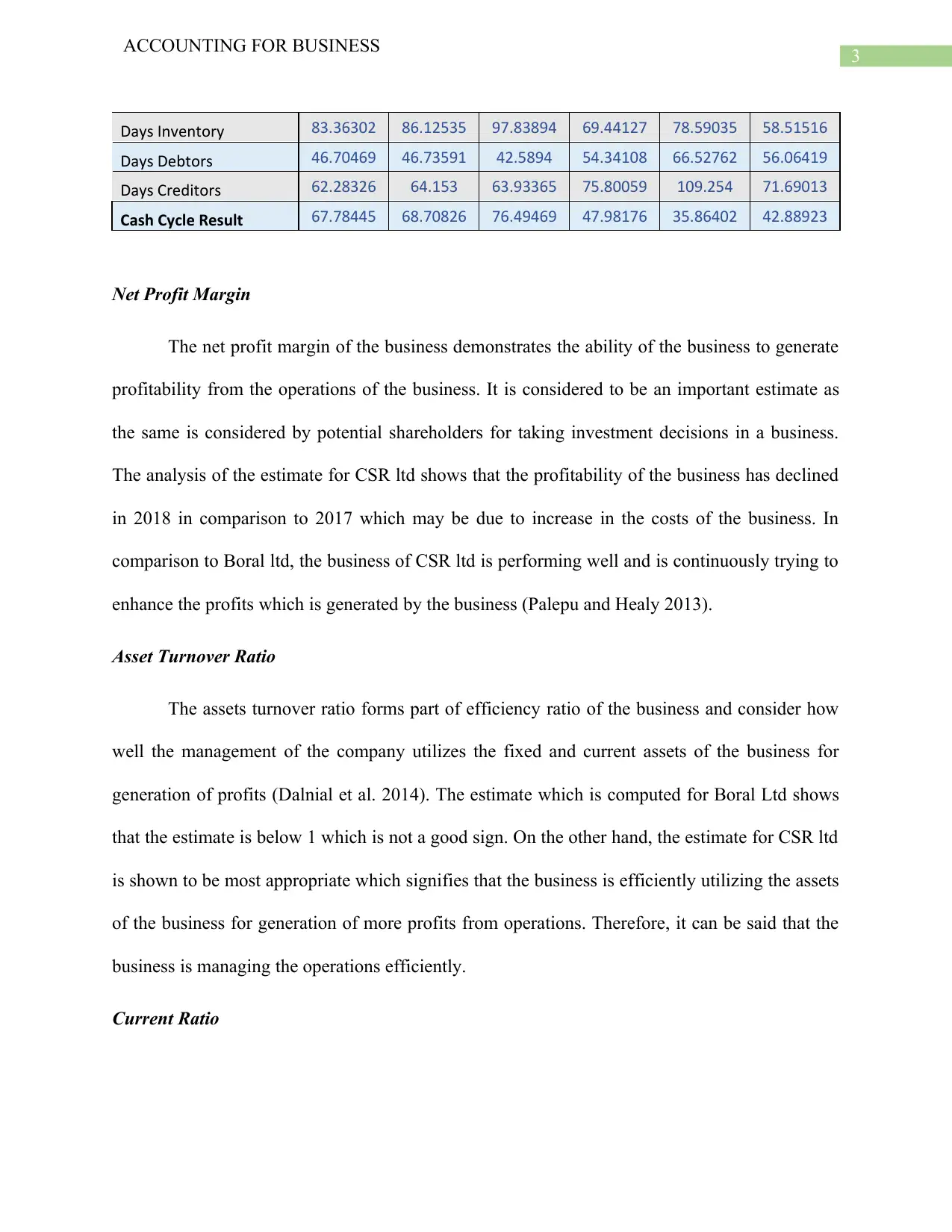

Days Inventory 83.36302 86.12535 97.83894 69.44127 78.59035 58.51516

Days Debtors 46.70469 46.73591 42.5894 54.34108 66.52762 56.06419

Days Creditors 62.28326 64.153 63.93365 75.80059 109.254 71.69013

Cash Cycle Result 67.78445 68.70826 76.49469 47.98176 35.86402 42.88923

Net Profit Margin

The net profit margin of the business demonstrates the ability of the business to generate

profitability from the operations of the business. It is considered to be an important estimate as

the same is considered by potential shareholders for taking investment decisions in a business.

The analysis of the estimate for CSR ltd shows that the profitability of the business has declined

in 2018 in comparison to 2017 which may be due to increase in the costs of the business. In

comparison to Boral ltd, the business of CSR ltd is performing well and is continuously trying to

enhance the profits which is generated by the business (Palepu and Healy 2013).

Asset Turnover Ratio

The assets turnover ratio forms part of efficiency ratio of the business and consider how

well the management of the company utilizes the fixed and current assets of the business for

generation of profits (Dalnial et al. 2014). The estimate which is computed for Boral Ltd shows

that the estimate is below 1 which is not a good sign. On the other hand, the estimate for CSR ltd

is shown to be most appropriate which signifies that the business is efficiently utilizing the assets

of the business for generation of more profits from operations. Therefore, it can be said that the

business is managing the operations efficiently.

Current Ratio

ACCOUNTING FOR BUSINESS

Days Inventory 83.36302 86.12535 97.83894 69.44127 78.59035 58.51516

Days Debtors 46.70469 46.73591 42.5894 54.34108 66.52762 56.06419

Days Creditors 62.28326 64.153 63.93365 75.80059 109.254 71.69013

Cash Cycle Result 67.78445 68.70826 76.49469 47.98176 35.86402 42.88923

Net Profit Margin

The net profit margin of the business demonstrates the ability of the business to generate

profitability from the operations of the business. It is considered to be an important estimate as

the same is considered by potential shareholders for taking investment decisions in a business.

The analysis of the estimate for CSR ltd shows that the profitability of the business has declined

in 2018 in comparison to 2017 which may be due to increase in the costs of the business. In

comparison to Boral ltd, the business of CSR ltd is performing well and is continuously trying to

enhance the profits which is generated by the business (Palepu and Healy 2013).

Asset Turnover Ratio

The assets turnover ratio forms part of efficiency ratio of the business and consider how

well the management of the company utilizes the fixed and current assets of the business for

generation of profits (Dalnial et al. 2014). The estimate which is computed for Boral Ltd shows

that the estimate is below 1 which is not a good sign. On the other hand, the estimate for CSR ltd

is shown to be most appropriate which signifies that the business is efficiently utilizing the assets

of the business for generation of more profits from operations. Therefore, it can be said that the

business is managing the operations efficiently.

Current Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FOR BUSINESS

The current ratio is considered to be one of the important estimates which signifies the

liquidity position of the business (Ehiedu 2014). The current ratio shows the ability of the

business to meet the current obligations of the business in an effective manner. The current ratio

for CSR ltd is shown to be 1.59 in 2018 which has improved in comparison to previous year

estimate which is a positive sign for the business (Ecer and Boyukaslan 2014). On the other

hand, the current ratio for Boral ltd is also shown to be on a rising trend and the same is shown to

be 1.74 in 2018 which is more than CSR ltd. This means that the business of Boral ltd enjoys

superior liquidity position.

Quick Ratio

The quick ratio is quite similar to current ratio and the same also depicts the liquidity

position of the business and the ability of the business to meet the current obligations of the

business. The quick ratio of the business of CSR ltd is also shown to be proper and similar the

estimate for Boral ltd is also shown to be proper. This shows that both the companies enjoy

liquidity superiority and effectively manages the operations of the business.

Debt to Asset Ratio

The debt to asset ratio forms part of leverage ratios and the same reflects the debt capital

which is used by the business for generating profits and also effectively utilizing the assets of the

business (Enekwe, Agu and Nnagbogu 2014). The utilization of debt in the business of CSR ltd

is shown to be low in comparison to Boral Ltd and the same suggest that both the businesses

effectively utilizes the assets of the business and also manages the debts of the business.

Day Inventory

ACCOUNTING FOR BUSINESS

The current ratio is considered to be one of the important estimates which signifies the

liquidity position of the business (Ehiedu 2014). The current ratio shows the ability of the

business to meet the current obligations of the business in an effective manner. The current ratio

for CSR ltd is shown to be 1.59 in 2018 which has improved in comparison to previous year

estimate which is a positive sign for the business (Ecer and Boyukaslan 2014). On the other

hand, the current ratio for Boral ltd is also shown to be on a rising trend and the same is shown to

be 1.74 in 2018 which is more than CSR ltd. This means that the business of Boral ltd enjoys

superior liquidity position.

Quick Ratio

The quick ratio is quite similar to current ratio and the same also depicts the liquidity

position of the business and the ability of the business to meet the current obligations of the

business. The quick ratio of the business of CSR ltd is also shown to be proper and similar the

estimate for Boral ltd is also shown to be proper. This shows that both the companies enjoy

liquidity superiority and effectively manages the operations of the business.

Debt to Asset Ratio

The debt to asset ratio forms part of leverage ratios and the same reflects the debt capital

which is used by the business for generating profits and also effectively utilizing the assets of the

business (Enekwe, Agu and Nnagbogu 2014). The utilization of debt in the business of CSR ltd

is shown to be low in comparison to Boral Ltd and the same suggest that both the businesses

effectively utilizes the assets of the business and also manages the debts of the business.

Day Inventory

5

ACCOUNTING FOR BUSINESS

The days inventory of the business reflects the efficiency of the business in managing the

inventory balance of the business. The management of a company would be trying to reduce the

period so that there is more cash cycle in the business. The estimate for Boral ltd is shown to be

much more favourable in comparison to other business which suggest that the business is

performing well in this area. In addition to this, the management of CSR ltd need to make

improvement in the inventory management plan of the business.

Days Receivable

The days receivable estimates of the business shows the efficiency of the business in

managing the debtors of the business and ensuring that the collection of cash can be done as

quickly as possible. The management of CSR ltd follows an appropriate policy in managing the

debtors of the business and ensuring that there is appropriate flow of cash in the business in

comparison to Boral Ltd.

Days Payable

The days payable estimate shows the efficiency of the business in managing the payable

balances of the business and it is considered that if the period is long than the same is more

beneficial for the business. The days payable period effectively shows that Boral ltd has a better

credit period than CSR ltd and this shows that the efficiency of the business is better than the

CSR ltd. The management of CSR ltd needs to make improvements in the same.

Cash Cycle

The cash cycle of the business shows the cash flow in the business and whether the

business would have appropriate cash for ensuring that it is able to meet the current obligations

ACCOUNTING FOR BUSINESS

The days inventory of the business reflects the efficiency of the business in managing the

inventory balance of the business. The management of a company would be trying to reduce the

period so that there is more cash cycle in the business. The estimate for Boral ltd is shown to be

much more favourable in comparison to other business which suggest that the business is

performing well in this area. In addition to this, the management of CSR ltd need to make

improvement in the inventory management plan of the business.

Days Receivable

The days receivable estimates of the business shows the efficiency of the business in

managing the debtors of the business and ensuring that the collection of cash can be done as

quickly as possible. The management of CSR ltd follows an appropriate policy in managing the

debtors of the business and ensuring that there is appropriate flow of cash in the business in

comparison to Boral Ltd.

Days Payable

The days payable estimate shows the efficiency of the business in managing the payable

balances of the business and it is considered that if the period is long than the same is more

beneficial for the business. The days payable period effectively shows that Boral ltd has a better

credit period than CSR ltd and this shows that the efficiency of the business is better than the

CSR ltd. The management of CSR ltd needs to make improvements in the same.

Cash Cycle

The cash cycle of the business shows the cash flow in the business and whether the

business would have appropriate cash for ensuring that it is able to meet the current obligations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FOR BUSINESS

of the business in an effective manner. The cash cycle is shown to be appropriate for both the

companies but the same would be requiring more improvements in the long run.

Recommendation

The management of CSR ltd needs to take the following steps for ensuring that the

business is able to meet the current obligations of the business and also improve the performance

of the business in different areas (Xu et al. 2014). On the basis of ratio analysis, the

recommendation which can be suggested to the management of CSR ltd are listed below in

details:

The management of the company needs to reduce the costs of the business so that the

profitability of the business can be improved.

In addition to this, the inventory management policy of the business needs to be revised

so that better control is maintained and the business is able to sell off the inventory in a

quicker time.

The management of the company also needs to reduce the cash cycle period which would

also improve the liquidity position of the business significantly.

Conclusion

The above discussion mainly relates to the interpretation of key financial ratios which is

computed and presented in the table above relating to both the companies which are considered.

The above analysis shows that the business of CSR ltd is performing well in certain areas but

there are still scope for further development. The discussion shows that the business of CSR ltd

is well ahead of Boral Ltd and the management needs to take steps for the purpose of

ACCOUNTING FOR BUSINESS

of the business in an effective manner. The cash cycle is shown to be appropriate for both the

companies but the same would be requiring more improvements in the long run.

Recommendation

The management of CSR ltd needs to take the following steps for ensuring that the

business is able to meet the current obligations of the business and also improve the performance

of the business in different areas (Xu et al. 2014). On the basis of ratio analysis, the

recommendation which can be suggested to the management of CSR ltd are listed below in

details:

The management of the company needs to reduce the costs of the business so that the

profitability of the business can be improved.

In addition to this, the inventory management policy of the business needs to be revised

so that better control is maintained and the business is able to sell off the inventory in a

quicker time.

The management of the company also needs to reduce the cash cycle period which would

also improve the liquidity position of the business significantly.

Conclusion

The above discussion mainly relates to the interpretation of key financial ratios which is

computed and presented in the table above relating to both the companies which are considered.

The above analysis shows that the business of CSR ltd is performing well in certain areas but

there are still scope for further development. The discussion shows that the business of CSR ltd

is well ahead of Boral Ltd and the management needs to take steps for the purpose of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FOR BUSINESS

maintaining the status. In addition to this, the management of the company also needs to

implement the measures which have been suggested so that improvement can be brought about

in the business structure of the company.

Reference

Boral.com. (2019). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 18 Aug. 2019].

Corporate. (2019). Annual Meetings and Reports. [online] Available at:

https://www.csr.com.au/investor-relations-and-news/annual-meetings-and-reports [Accessed 18

Aug. 2019].

Dalnial, H., Kamaluddin, A., Sanusi, Z.M. and Khairuddin, K.S., 2014. Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science Vol, 2(1).

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ecer, F. and Boyukaslan, A., 2014. Measuring performances of football clubs using financial

ratios: the gray relational analysis approach. American Journal of Economics, 4(1), pp.62-71.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

ACCOUNTING FOR BUSINESS

maintaining the status. In addition to this, the management of the company also needs to

implement the measures which have been suggested so that improvement can be brought about

in the business structure of the company.

Reference

Boral.com. (2019). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 18 Aug. 2019].

Corporate. (2019). Annual Meetings and Reports. [online] Available at:

https://www.csr.com.au/investor-relations-and-news/annual-meetings-and-reports [Accessed 18

Aug. 2019].

Dalnial, H., Kamaluddin, A., Sanusi, Z.M. and Khairuddin, K.S., 2014. Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science Vol, 2(1).

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ecer, F. and Boyukaslan, A., 2014. Measuring performances of football clubs using financial

ratios: the gray relational analysis approach. American Journal of Economics, 4(1), pp.62-71.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

8

ACCOUNTING FOR BUSINESS

Enekwe, C.I., Agu, C.I. and Nnagbogu, E.K., 2014. The effect of financial leverage on financial

performance: Evidence of quoted pharmaceutical companies in Nigeria. Journal of Economics

and Finance, 5(3), pp.17-25.

Palepu, K.G. and Healy, P.M., 2013. Business analysis and valuation: Using financial

statements, text and cases.

Xu, W., Xiao, Z., Dang, X., Yang, D. and Yang, X., 2014. Financial ratio selection for business

failure prediction using soft set theory. Knowledge-Based Systems, 63, pp.59-67.

ACCOUNTING FOR BUSINESS

Enekwe, C.I., Agu, C.I. and Nnagbogu, E.K., 2014. The effect of financial leverage on financial

performance: Evidence of quoted pharmaceutical companies in Nigeria. Journal of Economics

and Finance, 5(3), pp.17-25.

Palepu, K.G. and Healy, P.M., 2013. Business analysis and valuation: Using financial

statements, text and cases.

Xu, W., Xiao, Z., Dang, X., Yang, D. and Yang, X., 2014. Financial ratio selection for business

failure prediction using soft set theory. Knowledge-Based Systems, 63, pp.59-67.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FOR BUSINESS

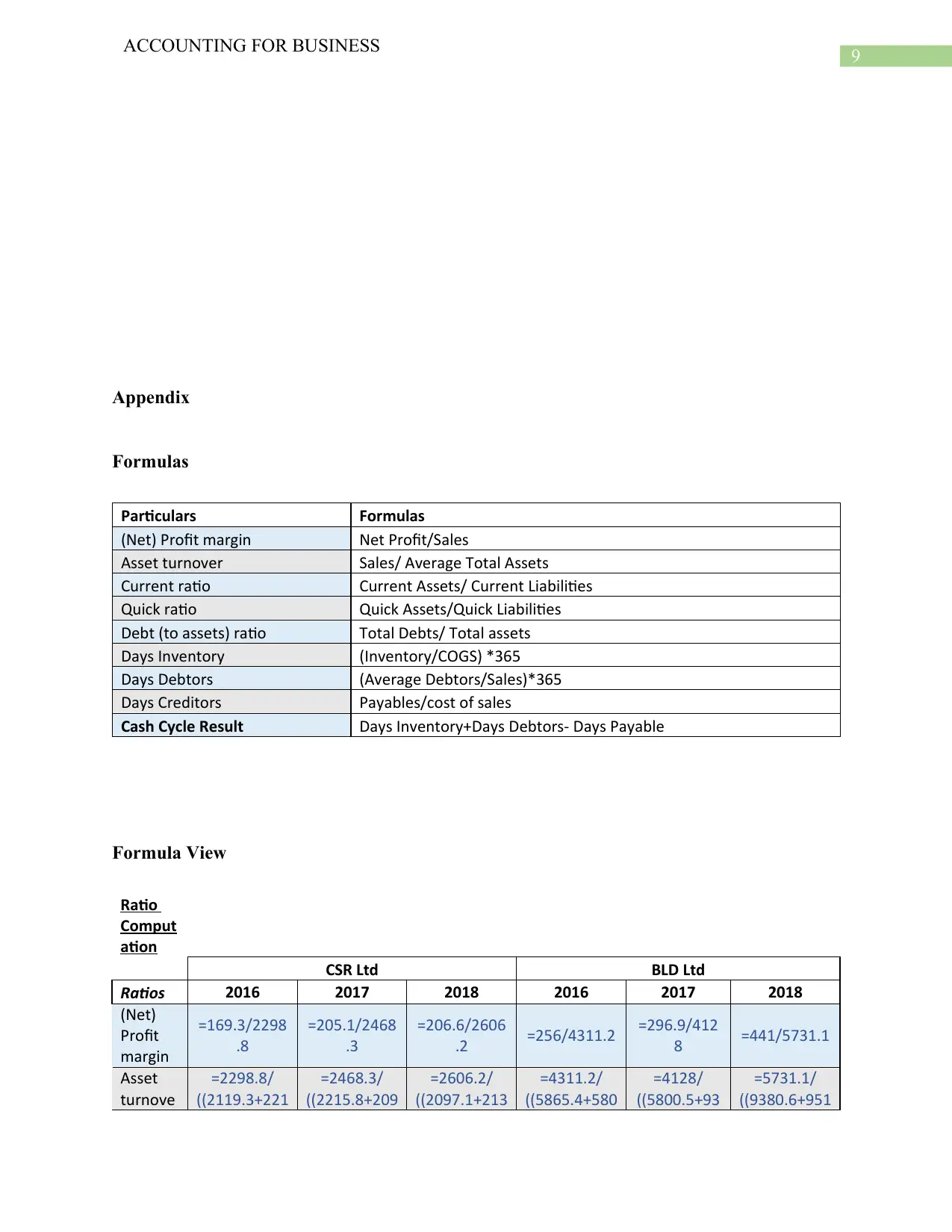

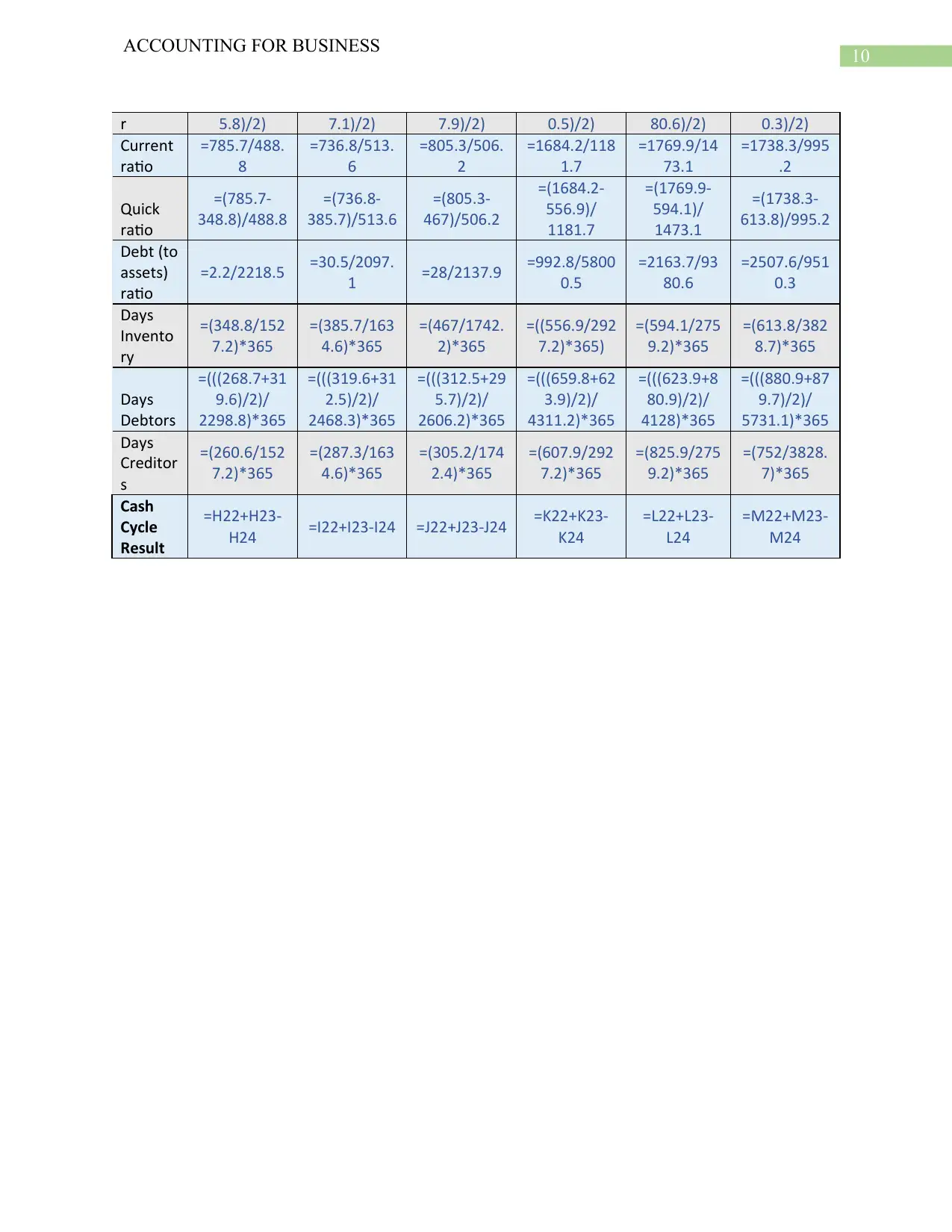

Appendix

Formulas

Particulars Formulas

(Net) Profit margin Net Profit/Sales

Asset turnover Sales/ Average Total Assets

Current ratio Current Assets/ Current Liabilities

Quick ratio Quick Assets/Quick Liabilities

Debt (to assets) ratio Total Debts/ Total assets

Days Inventory (Inventory/COGS) *365

Days Debtors (Average Debtors/Sales)*365

Days Creditors Payables/cost of sales

Cash Cycle Result Days Inventory+Days Debtors- Days Payable

Formula View

Ratio

Comput

ation

CSR Ltd BLD Ltd

Ratios 2016 2017 2018 2016 2017 2018

(Net)

Profit

margin

=169.3/2298

.8

=205.1/2468

.3

=206.6/2606

.2 =256/4311.2 =296.9/412

8 =441/5731.1

Asset

turnove

=2298.8/

((2119.3+221

=2468.3/

((2215.8+209

=2606.2/

((2097.1+213

=4311.2/

((5865.4+580

=4128/

((5800.5+93

=5731.1/

((9380.6+951

ACCOUNTING FOR BUSINESS

Appendix

Formulas

Particulars Formulas

(Net) Profit margin Net Profit/Sales

Asset turnover Sales/ Average Total Assets

Current ratio Current Assets/ Current Liabilities

Quick ratio Quick Assets/Quick Liabilities

Debt (to assets) ratio Total Debts/ Total assets

Days Inventory (Inventory/COGS) *365

Days Debtors (Average Debtors/Sales)*365

Days Creditors Payables/cost of sales

Cash Cycle Result Days Inventory+Days Debtors- Days Payable

Formula View

Ratio

Comput

ation

CSR Ltd BLD Ltd

Ratios 2016 2017 2018 2016 2017 2018

(Net)

Profit

margin

=169.3/2298

.8

=205.1/2468

.3

=206.6/2606

.2 =256/4311.2 =296.9/412

8 =441/5731.1

Asset

turnove

=2298.8/

((2119.3+221

=2468.3/

((2215.8+209

=2606.2/

((2097.1+213

=4311.2/

((5865.4+580

=4128/

((5800.5+93

=5731.1/

((9380.6+951

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FOR BUSINESS

r 5.8)/2) 7.1)/2) 7.9)/2) 0.5)/2) 80.6)/2) 0.3)/2)

Current

ratio

=785.7/488.

8

=736.8/513.

6

=805.3/506.

2

=1684.2/118

1.7

=1769.9/14

73.1

=1738.3/995

.2

Quick

ratio

=(785.7-

348.8)/488.8

=(736.8-

385.7)/513.6

=(805.3-

467)/506.2

=(1684.2-

556.9)/

1181.7

=(1769.9-

594.1)/

1473.1

=(1738.3-

613.8)/995.2

Debt (to

assets)

ratio

=2.2/2218.5 =30.5/2097.

1 =28/2137.9 =992.8/5800

0.5

=2163.7/93

80.6

=2507.6/951

0.3

Days

Invento

ry

=(348.8/152

7.2)*365

=(385.7/163

4.6)*365

=(467/1742.

2)*365

=((556.9/292

7.2)*365)

=(594.1/275

9.2)*365

=(613.8/382

8.7)*365

Days

Debtors

=(((268.7+31

9.6)/2)/

2298.8)*365

=(((319.6+31

2.5)/2)/

2468.3)*365

=(((312.5+29

5.7)/2)/

2606.2)*365

=(((659.8+62

3.9)/2)/

4311.2)*365

=(((623.9+8

80.9)/2)/

4128)*365

=(((880.9+87

9.7)/2)/

5731.1)*365

Days

Creditor

s

=(260.6/152

7.2)*365

=(287.3/163

4.6)*365

=(305.2/174

2.4)*365

=(607.9/292

7.2)*365

=(825.9/275

9.2)*365

=(752/3828.

7)*365

Cash

Cycle

Result

=H22+H23-

H24 =I22+I23-I24 =J22+J23-J24 =K22+K23-

K24

=L22+L23-

L24

=M22+M23-

M24

ACCOUNTING FOR BUSINESS

r 5.8)/2) 7.1)/2) 7.9)/2) 0.5)/2) 80.6)/2) 0.3)/2)

Current

ratio

=785.7/488.

8

=736.8/513.

6

=805.3/506.

2

=1684.2/118

1.7

=1769.9/14

73.1

=1738.3/995

.2

Quick

ratio

=(785.7-

348.8)/488.8

=(736.8-

385.7)/513.6

=(805.3-

467)/506.2

=(1684.2-

556.9)/

1181.7

=(1769.9-

594.1)/

1473.1

=(1738.3-

613.8)/995.2

Debt (to

assets)

ratio

=2.2/2218.5 =30.5/2097.

1 =28/2137.9 =992.8/5800

0.5

=2163.7/93

80.6

=2507.6/951

0.3

Days

Invento

ry

=(348.8/152

7.2)*365

=(385.7/163

4.6)*365

=(467/1742.

2)*365

=((556.9/292

7.2)*365)

=(594.1/275

9.2)*365

=(613.8/382

8.7)*365

Days

Debtors

=(((268.7+31

9.6)/2)/

2298.8)*365

=(((319.6+31

2.5)/2)/

2468.3)*365

=(((312.5+29

5.7)/2)/

2606.2)*365

=(((659.8+62

3.9)/2)/

4311.2)*365

=(((623.9+8

80.9)/2)/

4128)*365

=(((880.9+87

9.7)/2)/

5731.1)*365

Days

Creditor

s

=(260.6/152

7.2)*365

=(287.3/163

4.6)*365

=(305.2/174

2.4)*365

=(607.9/292

7.2)*365

=(825.9/275

9.2)*365

=(752/3828.

7)*365

Cash

Cycle

Result

=H22+H23-

H24 =I22+I23-I24 =J22+J23-J24 =K22+K23-

K24

=L22+L23-

L24

=M22+M23-

M24

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.