Accounting for Business: Financial Statement Analysis & Ratios

VerifiedAdded on 2023/06/04

|10

|1056

|476

Homework Assignment

AI Summary

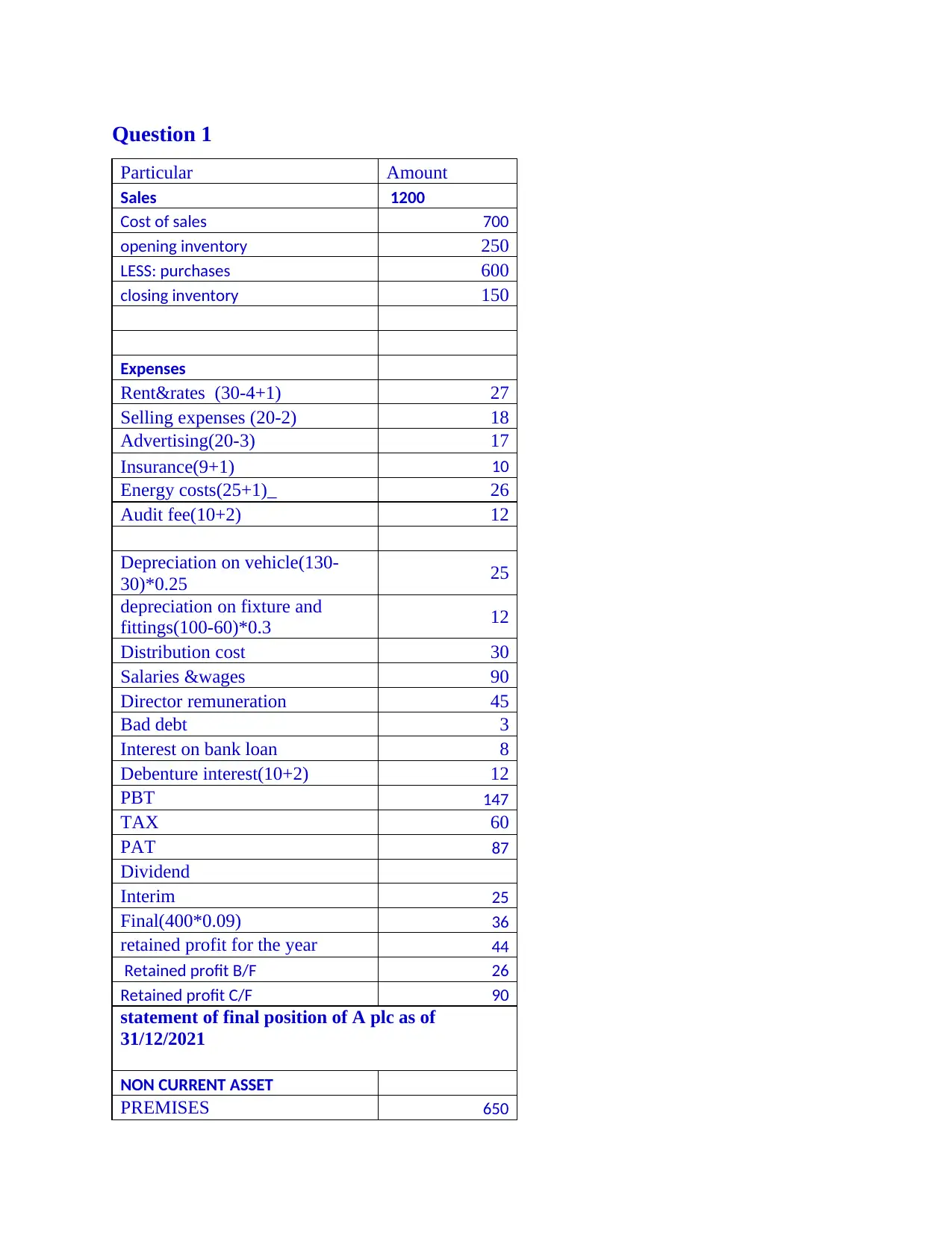

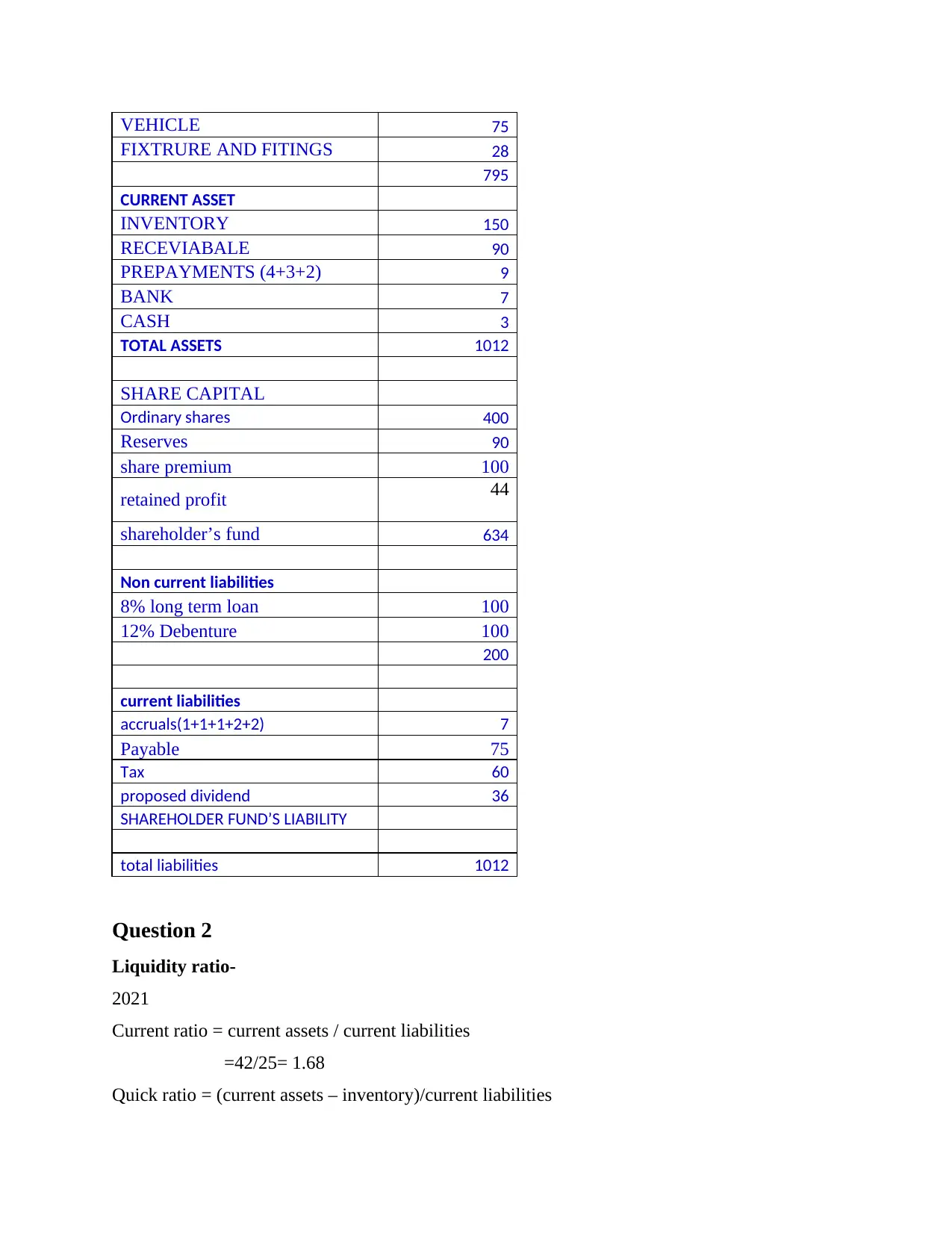

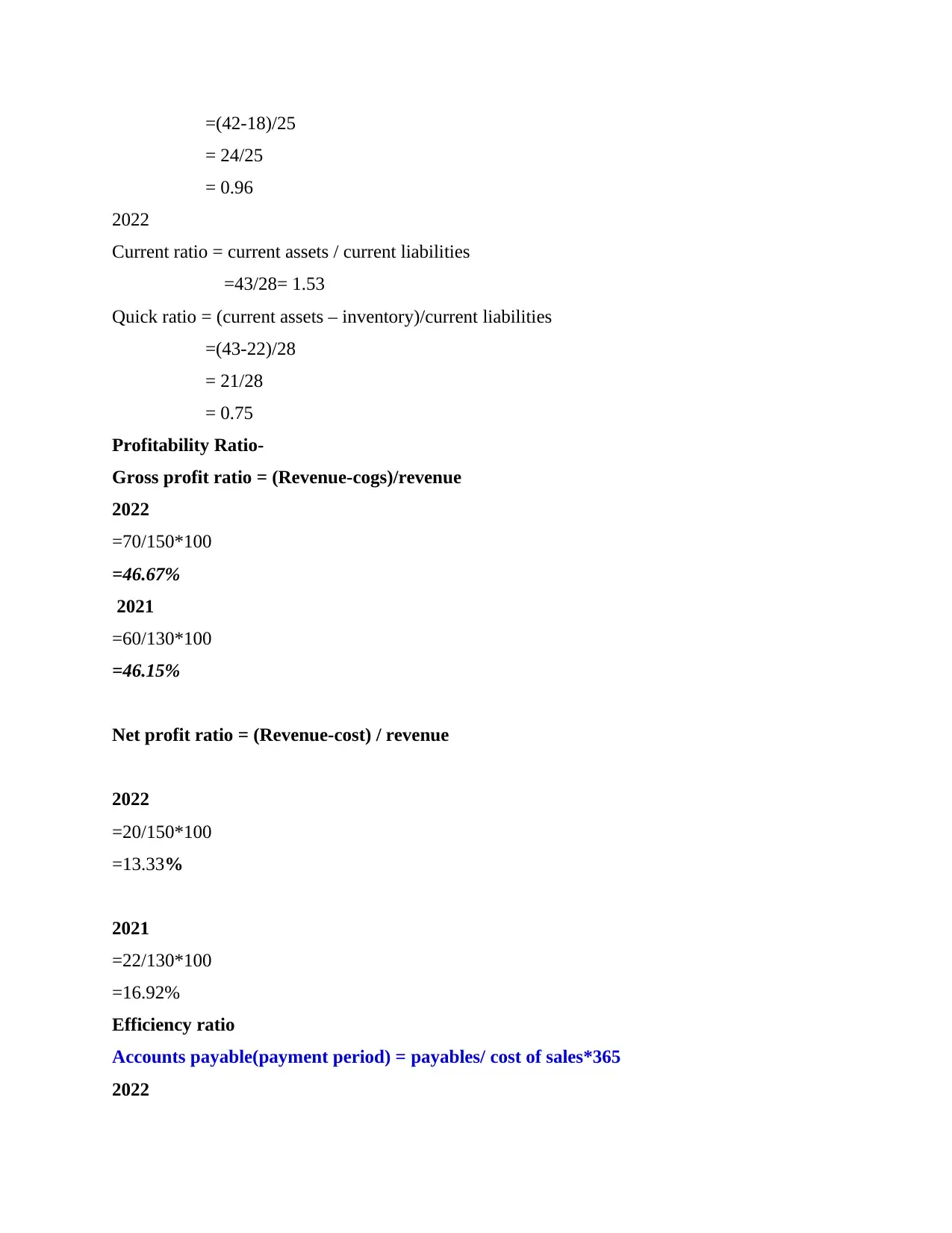

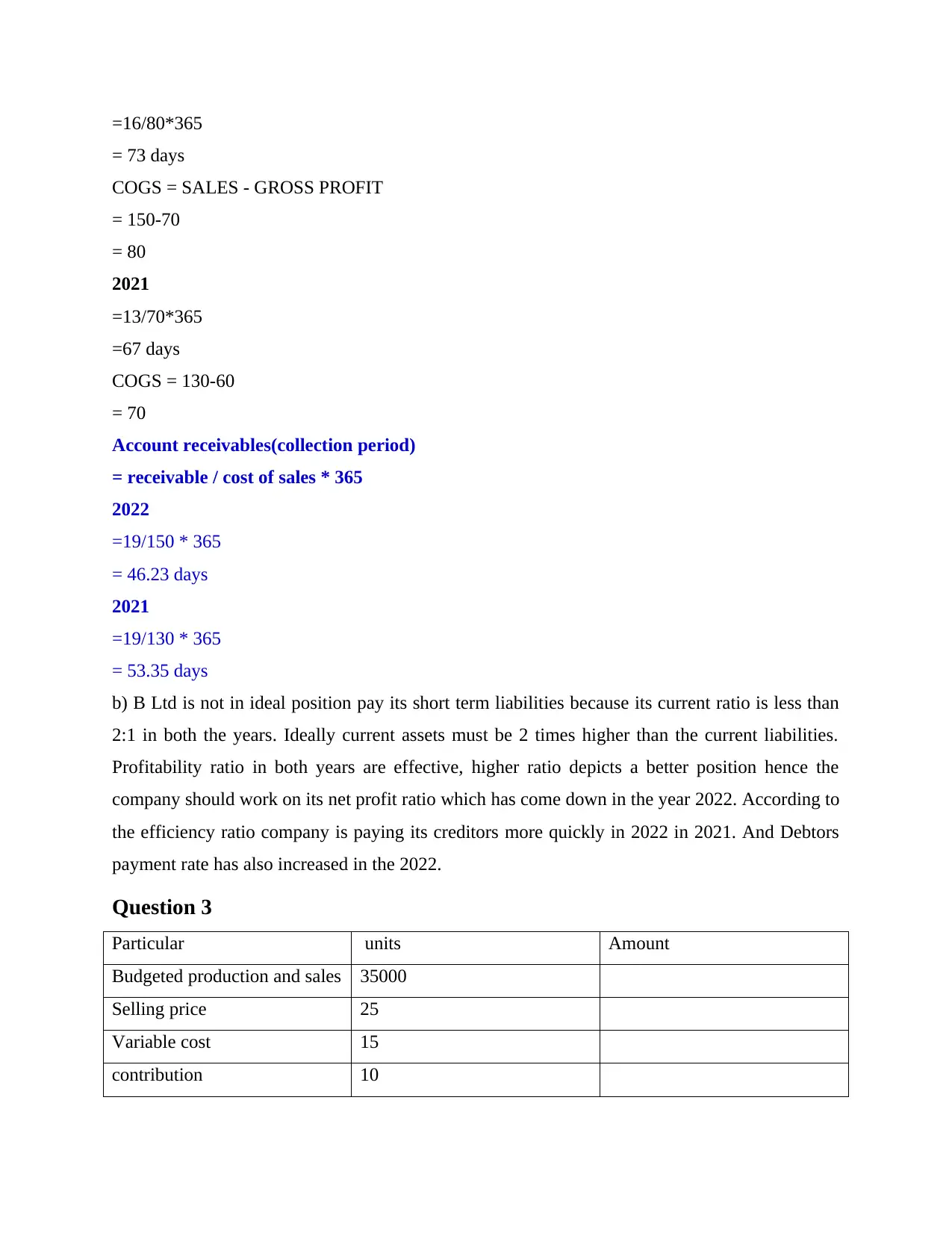

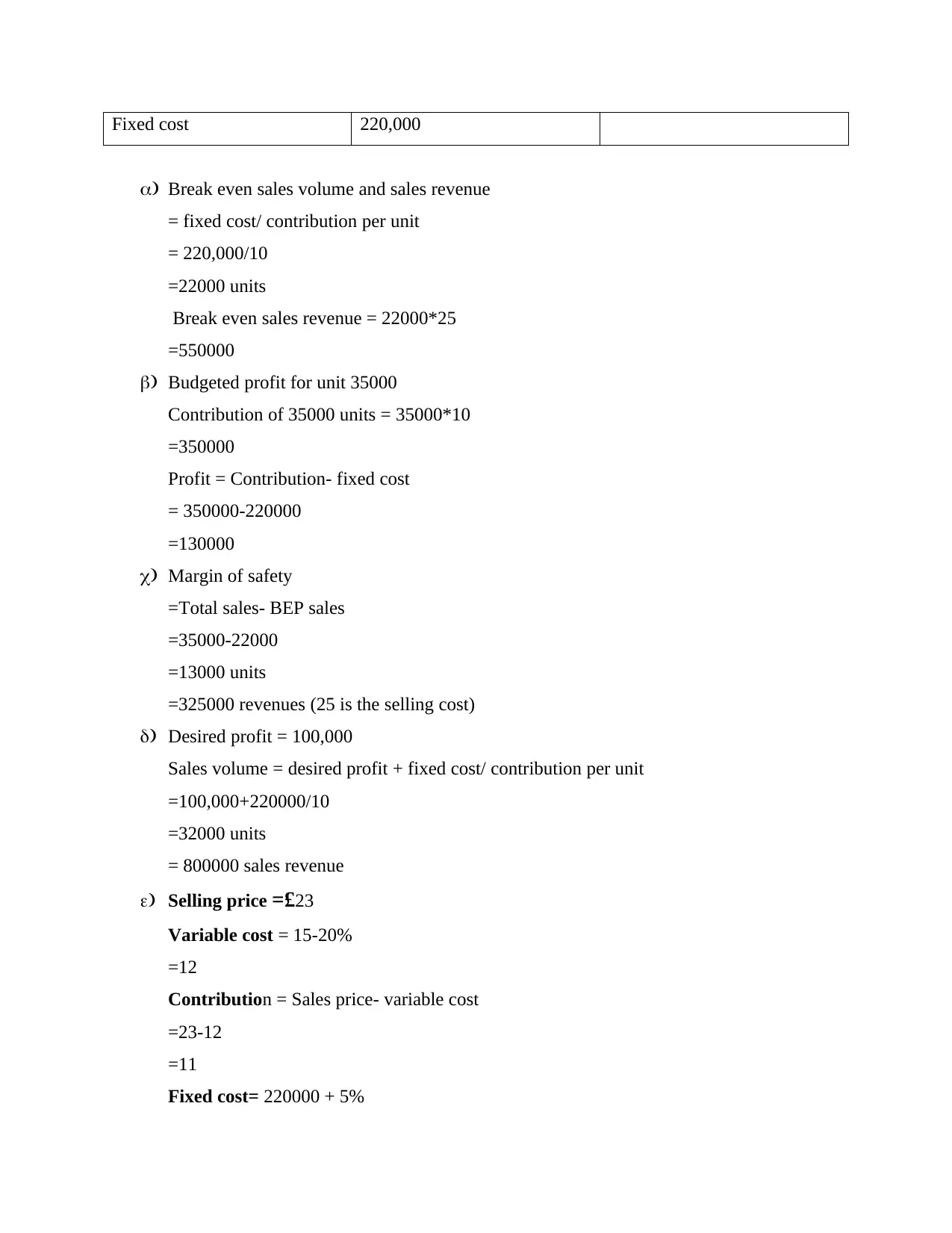

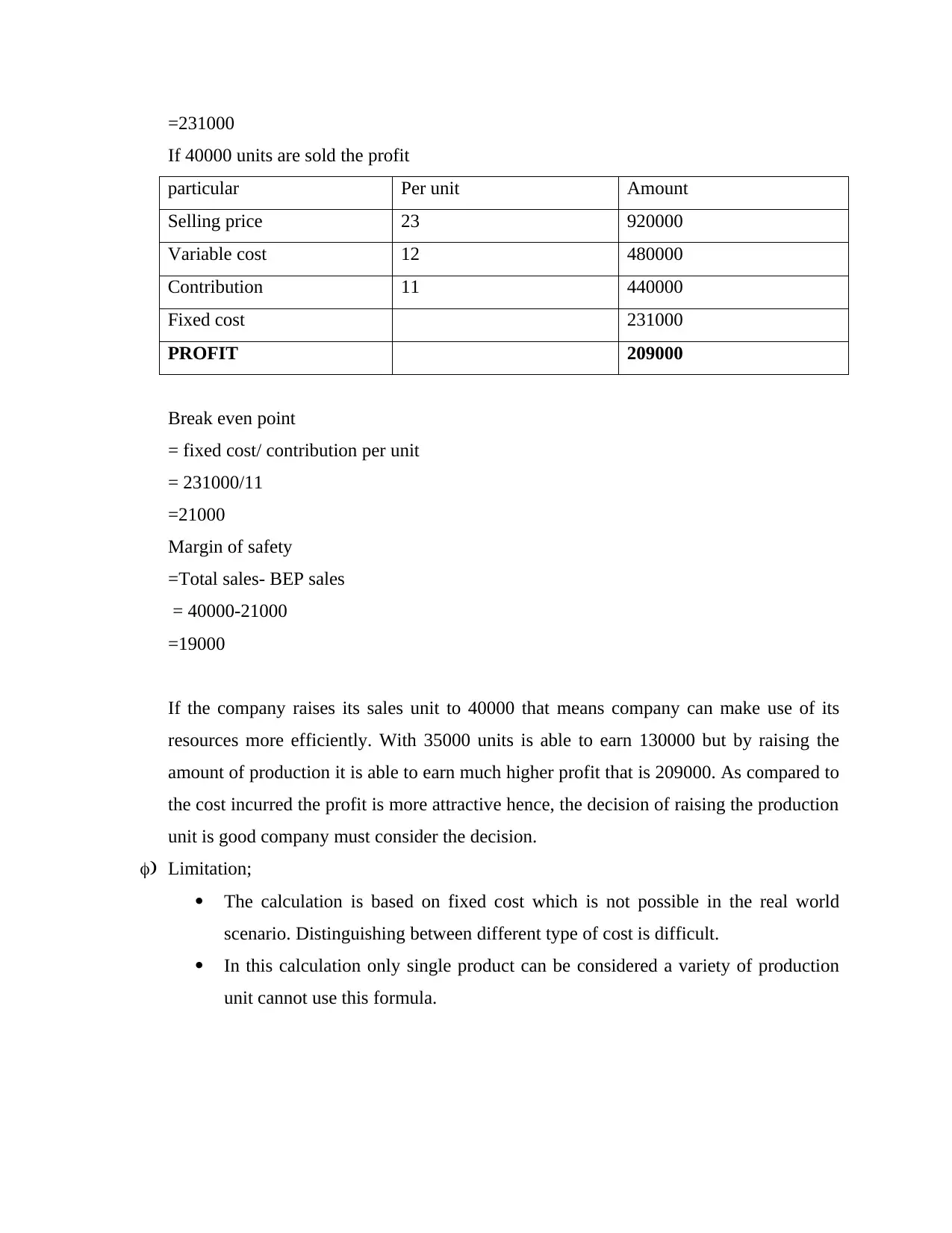

This assignment focuses on accounting for business, providing detailed solutions related to financial statement analysis. It includes calculations and interpretations of key financial metrics. The assignment begins with constructing financial statements, including income statements and balance sheets, based on provided data. It then delves into liquidity, profitability, and efficiency ratio analysis, comparing results between two years to assess a company's financial health and performance trends. Furthermore, the assignment covers break-even point analysis, budgeted profit calculations, margin of safety, and sales volume determination for desired profit levels. Finally, it evaluates the impact of changes in selling price and variable costs on profitability and recommends strategic decisions based on the analysis. Desklib provides a platform to access this and similar assignments.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.