T1 2019 HC1010: Financial Statement Analysis Assignment

VerifiedAdded on 2022/11/24

|6

|1378

|174

Homework Assignment

AI Summary

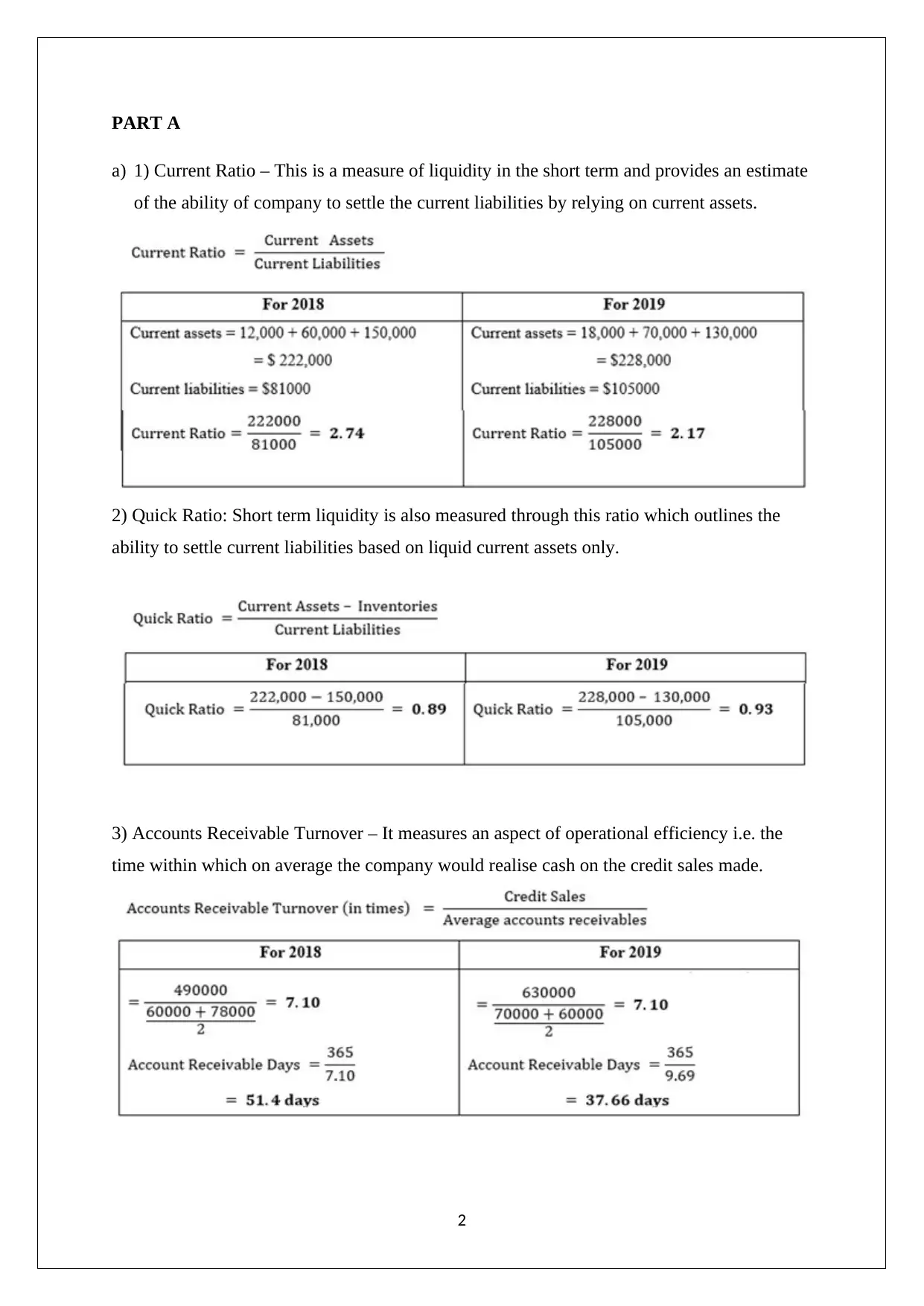

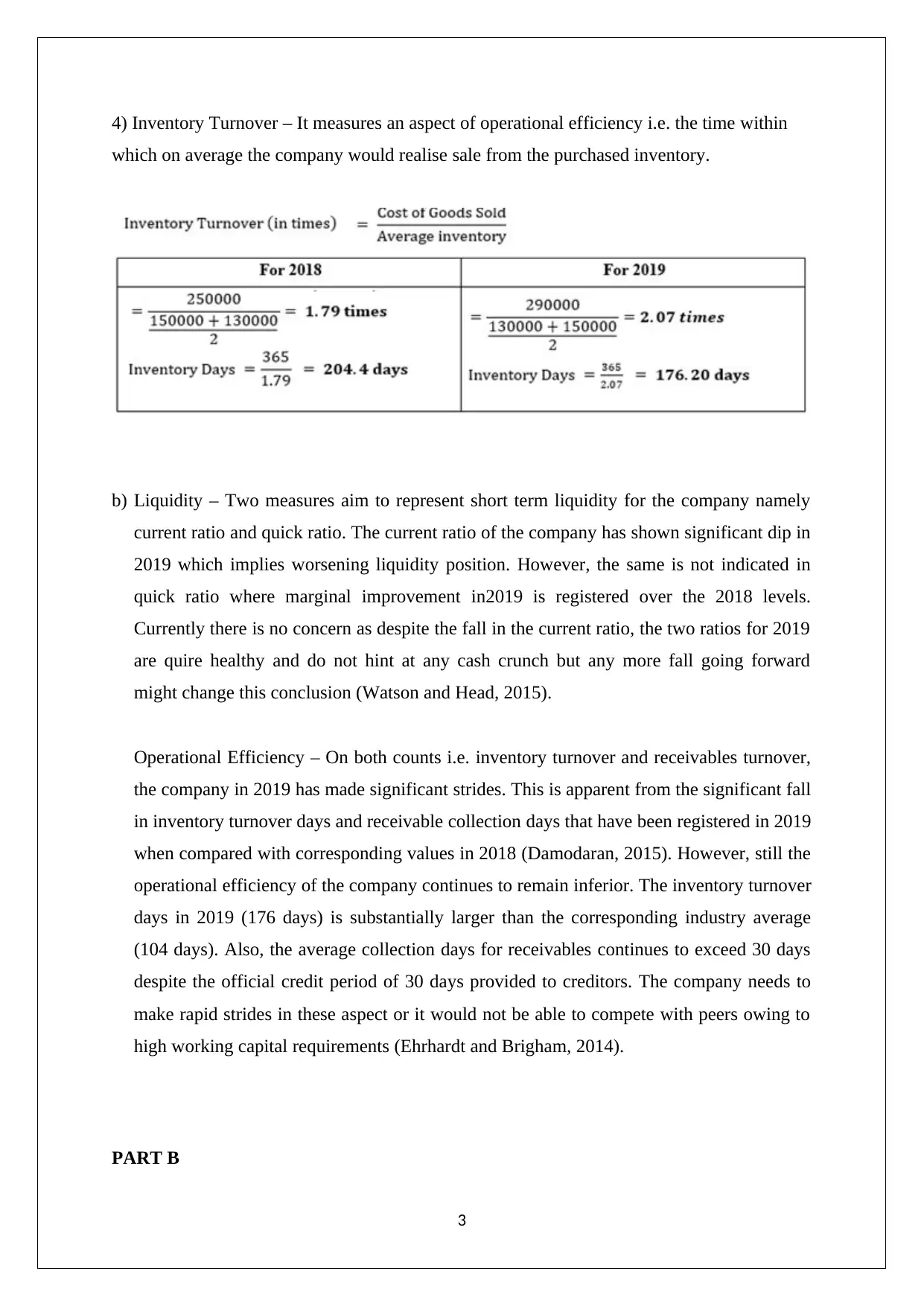

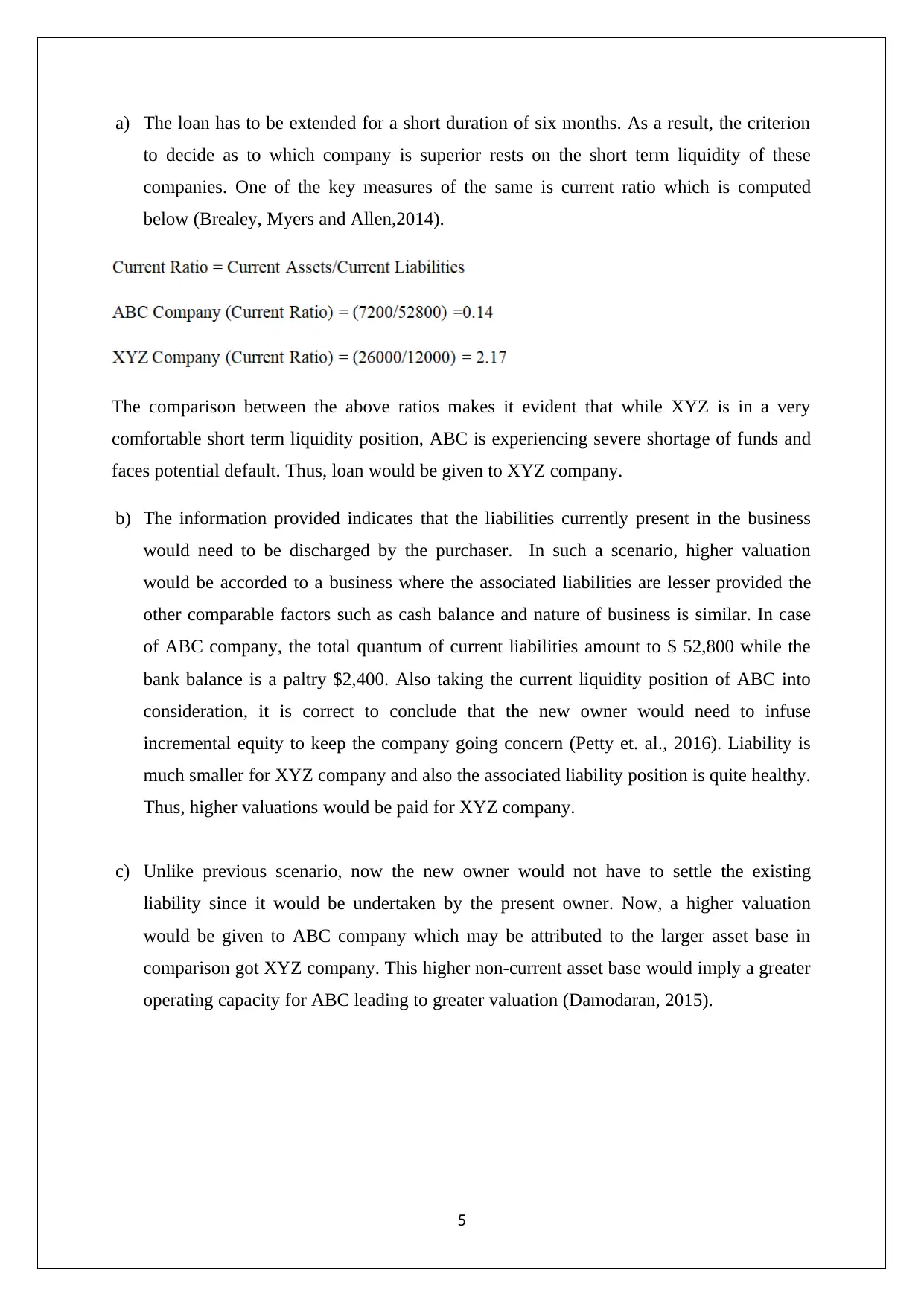

This accounting assignment provides a comprehensive analysis of financial statements, focusing on key aspects like liquidity and operational efficiency. Part A delves into the calculation and interpretation of ratios such as the current ratio, quick ratio, accounts receivable turnover, and inventory turnover, evaluating a company's short-term liquidity and operational performance. Part B examines the classification of financial items as either revenue or income, based on AASB 118, using examples like software sales, interest income, and discount settlements. Part C uses the understanding of financial ratios to evaluate two companies for a loan, emphasizing the importance of short-term liquidity and the impact of liabilities on valuation. The assignment demonstrates the application of accounting principles and provides insights into financial decision-making, supported by relevant references.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.