Accounting for Business: Financial Statement Analysis & Investment

VerifiedAdded on 2023/06/14

|10

|1574

|298

Report

AI Summary

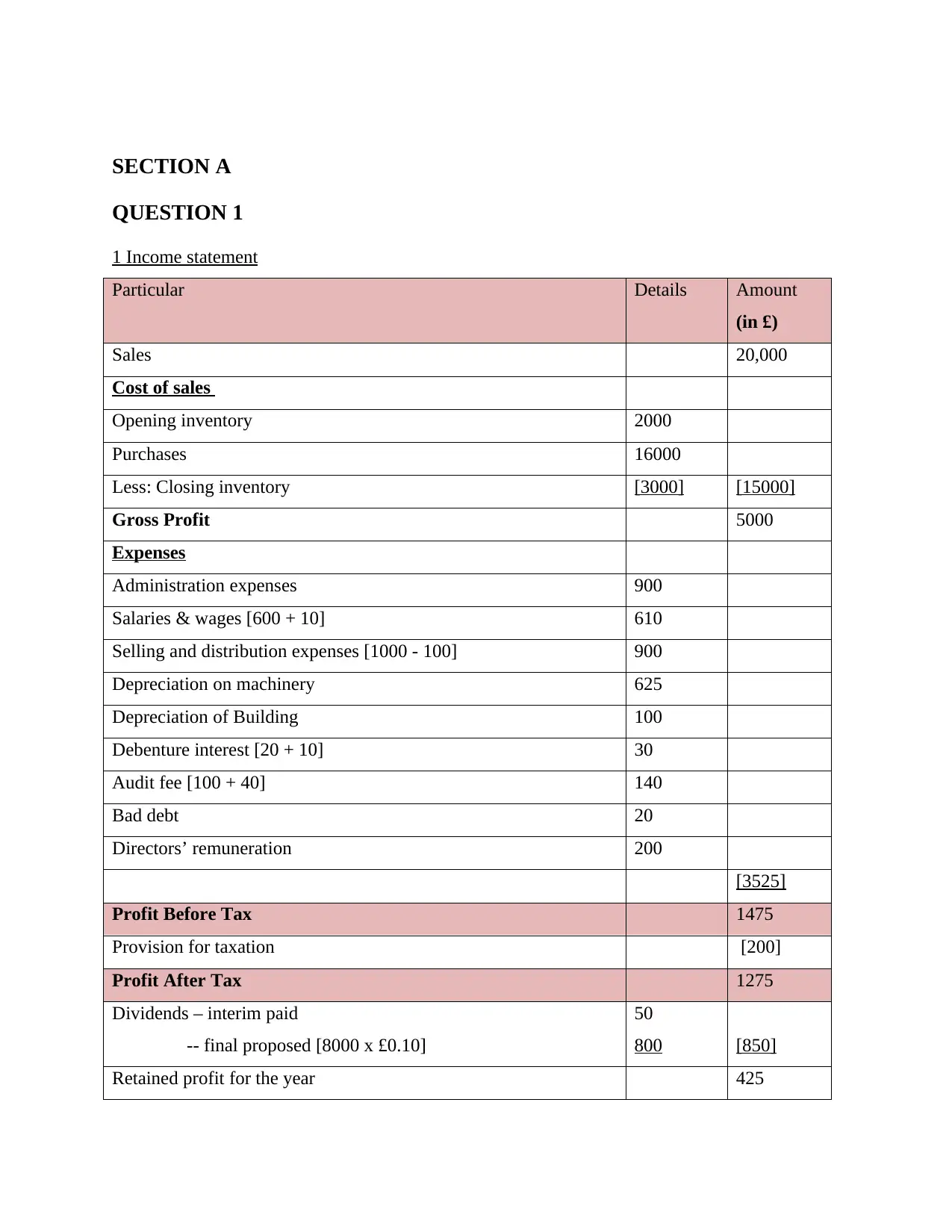

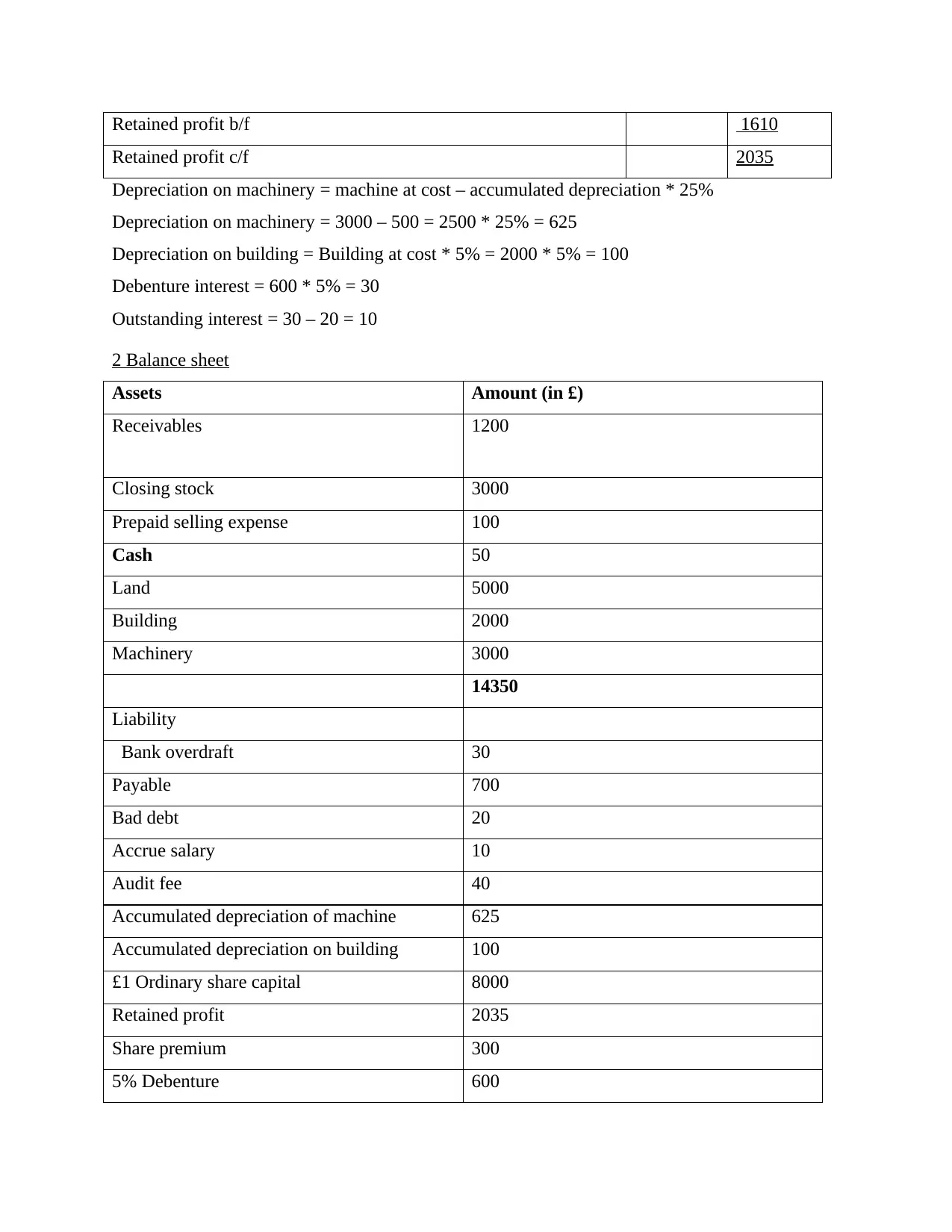

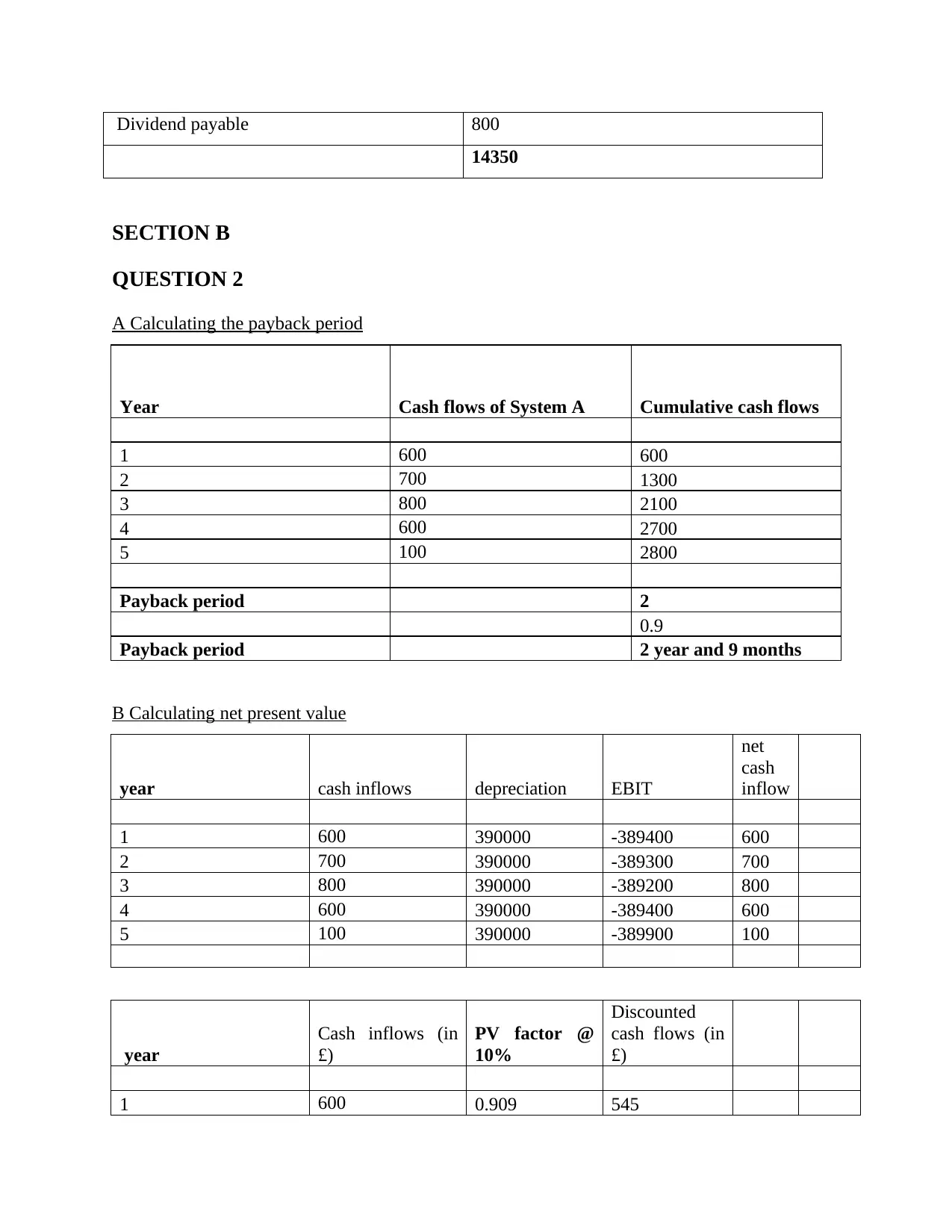

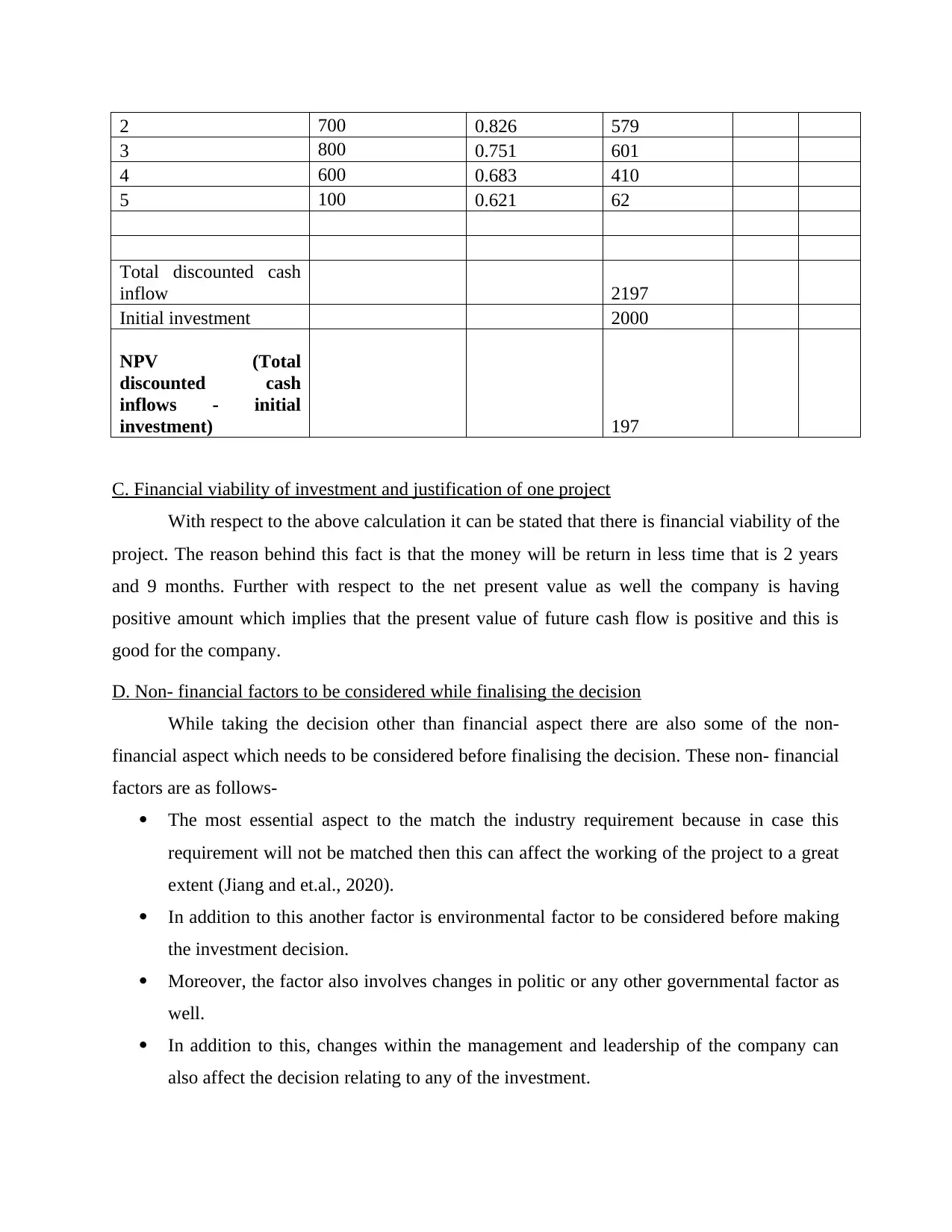

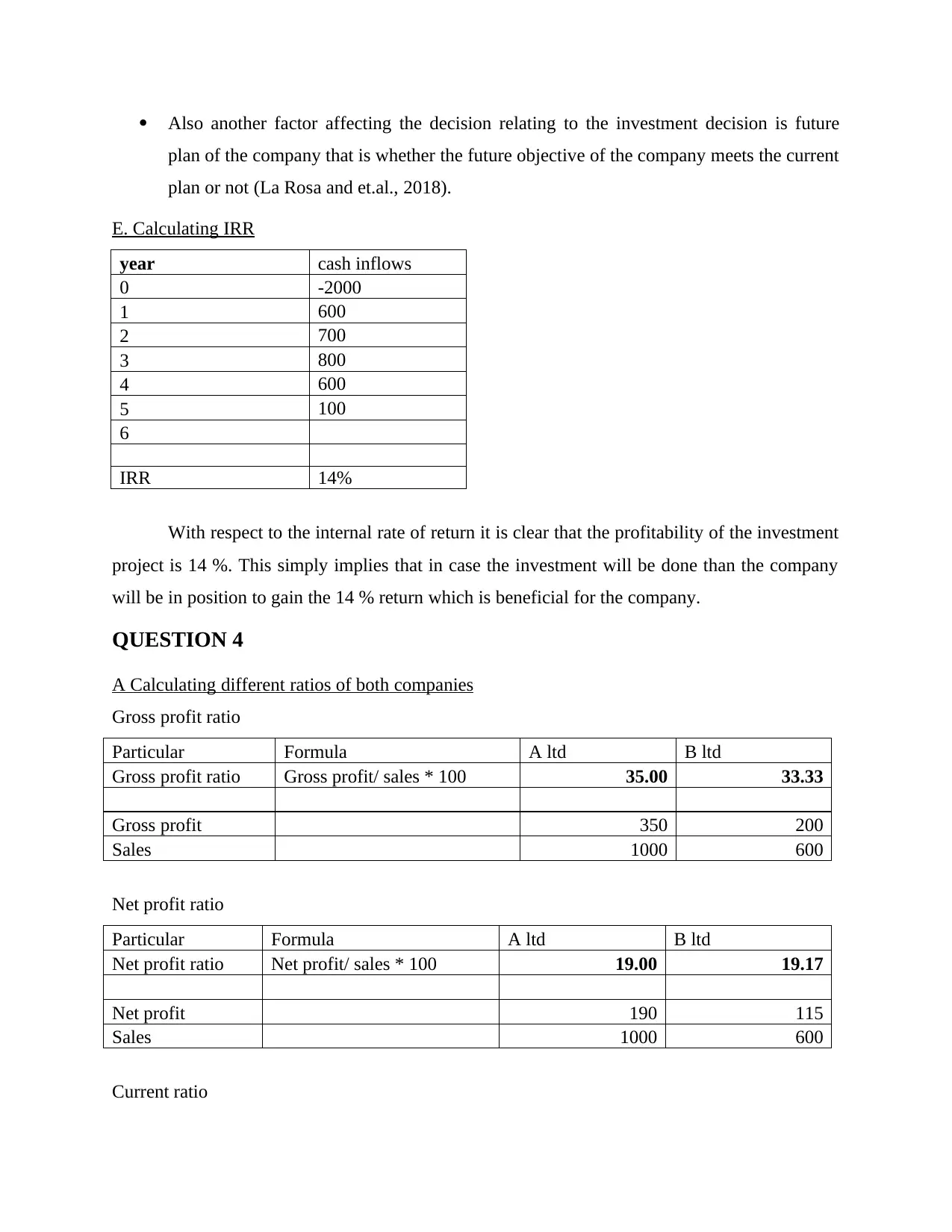

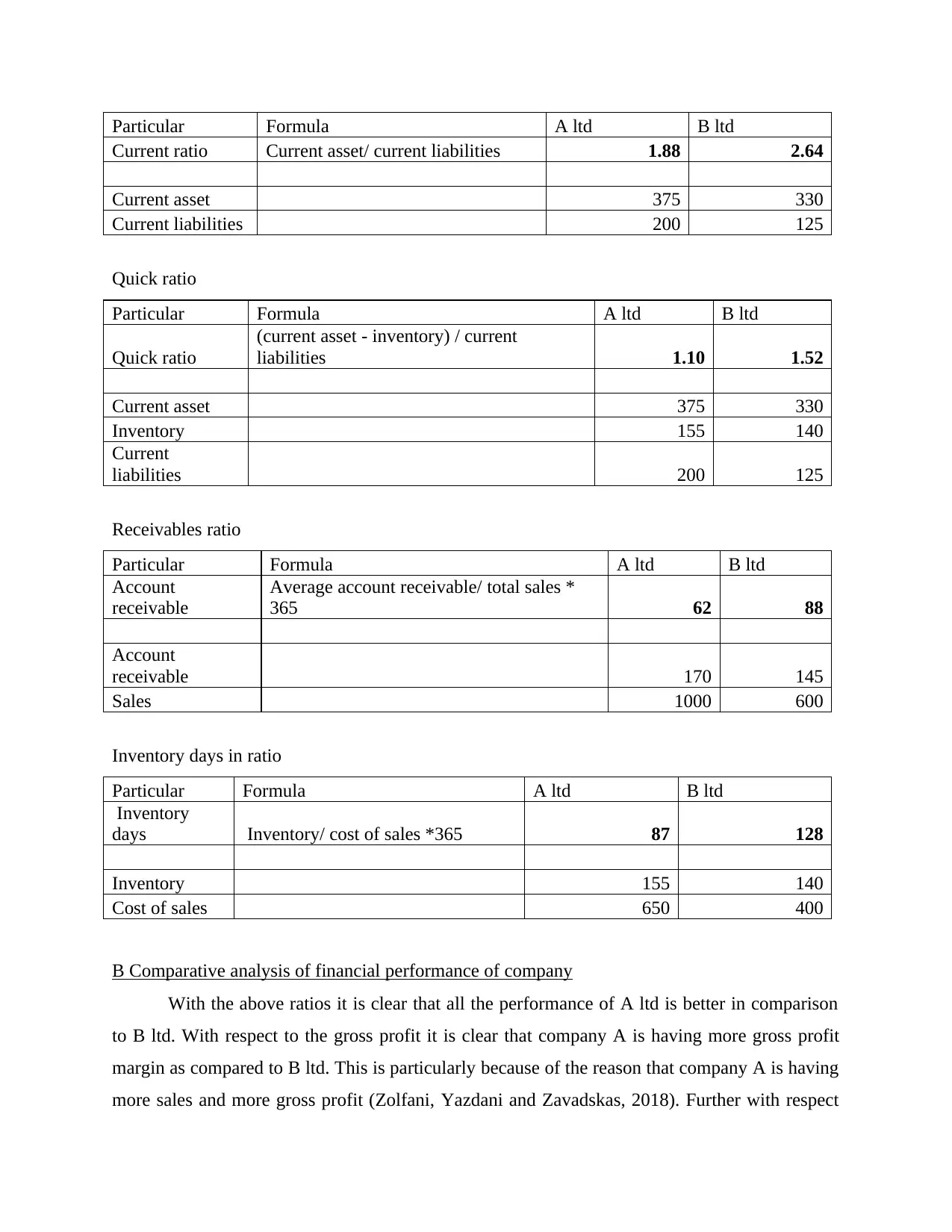

This report provides a comprehensive analysis of accounting for business, covering key areas such as financial statement analysis, investment appraisal, and ratio analysis. The income statement and balance sheet are presented, followed by an investment appraisal using methods like payback period, net present value (NPV), and internal rate of return (IRR). Non-financial factors affecting investment decisions are also discussed. Furthermore, a comparative financial performance analysis of two companies (A Ltd and B Ltd) is conducted using various financial ratios, including gross profit ratio, net profit ratio, current ratio, quick ratio, receivables ratio, and inventory days ratio, highlighting the strengths and weaknesses of each company. Desklib provides access to similar solved assignments and study resources for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.