Accounting for Corporate Income Tax

VerifiedAdded on 2021/05/31

|13

|3343

|56

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:........................................................................................................................2

Part (i):.........................................................................................................................................2

Part (ii):........................................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Part (iii):.......................................................................................................................................5

Part (iv):.......................................................................................................................................5

Part (v):........................................................................................................................................6

Accounting for corporate income tax:.............................................................................................6

Part (vi):.......................................................................................................................................6

Part (vii):......................................................................................................................................7

Part (viii):.....................................................................................................................................8

Part (ix):.......................................................................................................................................8

Part (x):........................................................................................................................................9

Part (xi):.......................................................................................................................................9

References:....................................................................................................................................11

Table of Contents

Cash flow statement:........................................................................................................................2

Part (i):.........................................................................................................................................2

Part (ii):........................................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Part (iii):.......................................................................................................................................5

Part (iv):.......................................................................................................................................5

Part (v):........................................................................................................................................6

Accounting for corporate income tax:.............................................................................................6

Part (vi):.......................................................................................................................................6

Part (vii):......................................................................................................................................7

Part (viii):.....................................................................................................................................8

Part (ix):.......................................................................................................................................8

Part (x):........................................................................................................................................9

Part (xi):.......................................................................................................................................9

References:....................................................................................................................................11

2CORPORATE ACCOUNTING

Cash flow statement:

Part (i):

There are certain items listed in the cash flow statement of an organisation and for this

paper, Wesfarmers Limited is chosen as the organisation and the cash flow items are stated in its

context. The most significant items in operating activities include receipts from customers,

payments to suppliers, interest received, borrowing cost and others. The receipts from customers

are those amounts that the organisation has received for sales made on credit (Armstrong et al.

2015). In case of Wesfarmers, the receipts from customers have increased from $71,157 million

in 2016 to $74,042 million in 2017. On the other hand, the payments to suppliers imply those

amounts that Wesfarmers has purchased on credit and the trend is increasing like that of receipts

from customers due to higher purchases. Interest received is the amount obtained for using

money to be repaid at a particular time or on demand (Atanasov and Black 2016). In case of

Wesfarmers, there is fall in interest received from $131 million in 2016 to $83 million in 2017,

since a certain portion of the amount is written off as bad debt. Borrowing cost denotes the debt

obligation charge, which could comprise of financing fees and interest payments. For

Wesfarmers, decline could be observed in borrowing cost over the year due to the fall in market

interest rates.

The important items in investing activities of Wesfarmers Limited constitute of payments

for and proceedings from property, plant and equipment, proceeds from and investments in

associates and joint ventures, subsidiary acquisition and redemption of or investment in loan

notes. The payments for property, plant and equipment are the prices paid for acquiring the same,

which is essential to carry out the business operations (Benson et al. 2015). On the other hand,

Cash flow statement:

Part (i):

There are certain items listed in the cash flow statement of an organisation and for this

paper, Wesfarmers Limited is chosen as the organisation and the cash flow items are stated in its

context. The most significant items in operating activities include receipts from customers,

payments to suppliers, interest received, borrowing cost and others. The receipts from customers

are those amounts that the organisation has received for sales made on credit (Armstrong et al.

2015). In case of Wesfarmers, the receipts from customers have increased from $71,157 million

in 2016 to $74,042 million in 2017. On the other hand, the payments to suppliers imply those

amounts that Wesfarmers has purchased on credit and the trend is increasing like that of receipts

from customers due to higher purchases. Interest received is the amount obtained for using

money to be repaid at a particular time or on demand (Atanasov and Black 2016). In case of

Wesfarmers, there is fall in interest received from $131 million in 2016 to $83 million in 2017,

since a certain portion of the amount is written off as bad debt. Borrowing cost denotes the debt

obligation charge, which could comprise of financing fees and interest payments. For

Wesfarmers, decline could be observed in borrowing cost over the year due to the fall in market

interest rates.

The important items in investing activities of Wesfarmers Limited constitute of payments

for and proceedings from property, plant and equipment, proceeds from and investments in

associates and joint ventures, subsidiary acquisition and redemption of or investment in loan

notes. The payments for property, plant and equipment are the prices paid for acquiring the same,

which is essential to carry out the business operations (Benson et al. 2015). On the other hand,

3CORPORATE ACCOUNTING

these assets generate economic benefits for the organisation, which are termed as proceedings

from property, plant and equipment. It has been observed that Wesfarmers Limited has reduced

its investment in these assets in 2017; however, the proceeds have increased over the year due to

sale of a portion of these assets. When the long-term assets are sold or purchased, they are

realised as proceeds and investments respectively (Cheng, Ioannou and Serafeim 2014). In case

of Wesfarmers Limited, significant amount of proceedings has been generated from associates

and joint arrangements in 2017; however, the investment amount has remained the same in both

the years. A loan note could be defined as a financial instrument, which is a loan contract

specifying the time of repaying the loan along with interest payable. Wesfarmers has made

investment of $47 million in loan notes in 2016; however, it has sought redemption of $54

million in loan notes.

The significant items in financing activities constitute of proceeds and repayment of

borrowings and equity dividends paid to the shareholders of Wesfarmers Limited. Borrowings

denote the net amount that a lender disburses to the borrower under the loan agreement terms

(Christensen et al. 2015). In case of Wesfarmers, there is significant fall in the proceeds from

borrowings due to extension of the loan term to the debtors. On the other hand, greater amount is

paid to the banks in order to repay its loans. Equity dividend denotes the yearly cash flow, which

is provided to the equity stockholders of an organisation. In case of Wesfarmers, equity dividend

payment has been minimised in 2017, since it has focused on increasing its retained earnings

base.

Part (ii):

As observed above from the annual report of Wesfarmers Limited, three categories of

cash flows are inherent, which include operating activities, investing activities and financing

these assets generate economic benefits for the organisation, which are termed as proceedings

from property, plant and equipment. It has been observed that Wesfarmers Limited has reduced

its investment in these assets in 2017; however, the proceeds have increased over the year due to

sale of a portion of these assets. When the long-term assets are sold or purchased, they are

realised as proceeds and investments respectively (Cheng, Ioannou and Serafeim 2014). In case

of Wesfarmers Limited, significant amount of proceedings has been generated from associates

and joint arrangements in 2017; however, the investment amount has remained the same in both

the years. A loan note could be defined as a financial instrument, which is a loan contract

specifying the time of repaying the loan along with interest payable. Wesfarmers has made

investment of $47 million in loan notes in 2016; however, it has sought redemption of $54

million in loan notes.

The significant items in financing activities constitute of proceeds and repayment of

borrowings and equity dividends paid to the shareholders of Wesfarmers Limited. Borrowings

denote the net amount that a lender disburses to the borrower under the loan agreement terms

(Christensen et al. 2015). In case of Wesfarmers, there is significant fall in the proceeds from

borrowings due to extension of the loan term to the debtors. On the other hand, greater amount is

paid to the banks in order to repay its loans. Equity dividend denotes the yearly cash flow, which

is provided to the equity stockholders of an organisation. In case of Wesfarmers, equity dividend

payment has been minimised in 2017, since it has focused on increasing its retained earnings

base.

Part (ii):

As observed above from the annual report of Wesfarmers Limited, three categories of

cash flows are inherent, which include operating activities, investing activities and financing

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

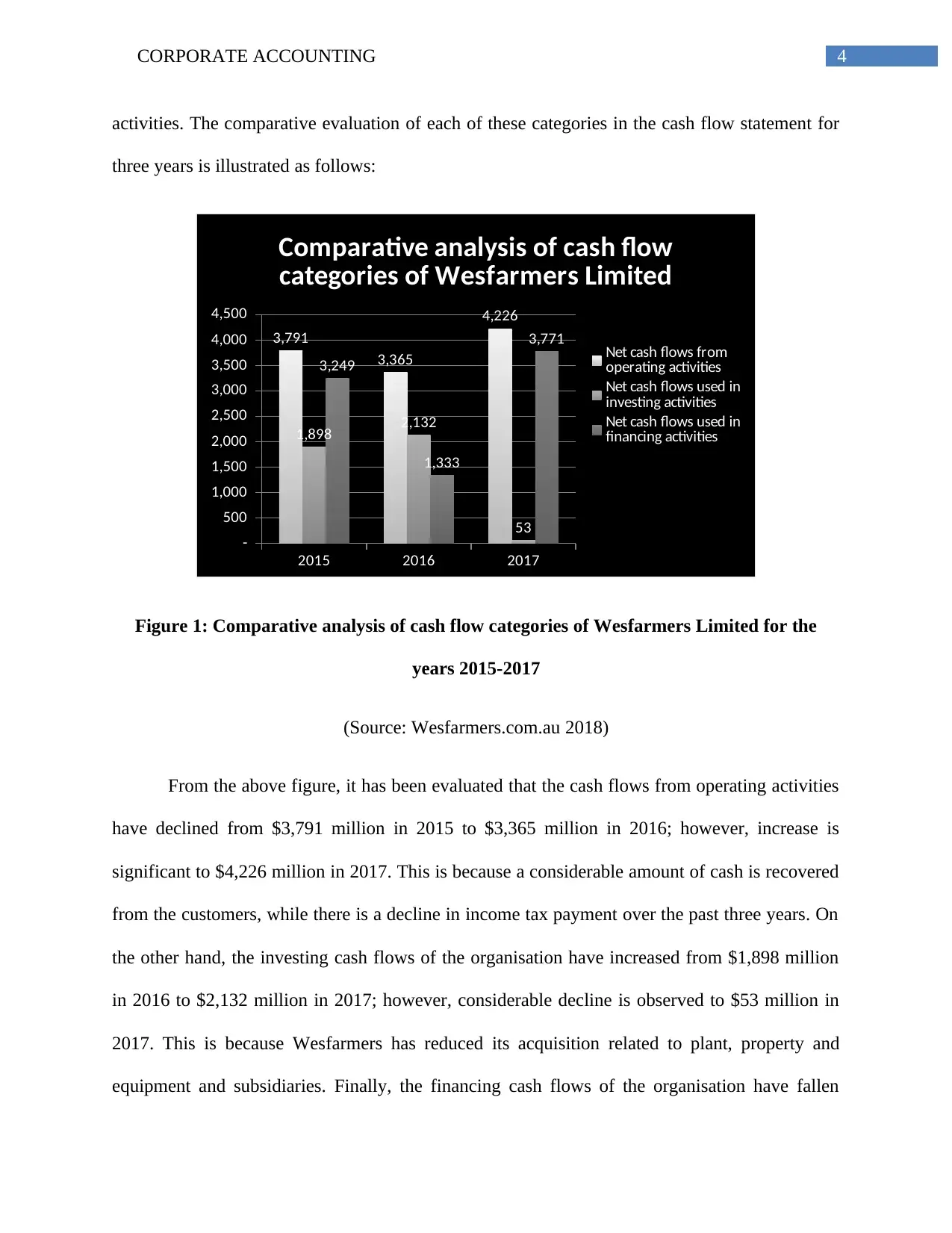

activities. The comparative evaluation of each of these categories in the cash flow statement for

three years is illustrated as follows:

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative analysis of cash flow

categories of Wesfarmers Limited

Net cash flows from

operating activities

Net cash flows used in

investing activities

Net cash flows used in

financing activities

Figure 1: Comparative analysis of cash flow categories of Wesfarmers Limited for the

years 2015-2017

(Source: Wesfarmers.com.au 2018)

From the above figure, it has been evaluated that the cash flows from operating activities

have declined from $3,791 million in 2015 to $3,365 million in 2016; however, increase is

significant to $4,226 million in 2017. This is because a considerable amount of cash is recovered

from the customers, while there is a decline in income tax payment over the past three years. On

the other hand, the investing cash flows of the organisation have increased from $1,898 million

in 2016 to $2,132 million in 2017; however, considerable decline is observed to $53 million in

2017. This is because Wesfarmers has reduced its acquisition related to plant, property and

equipment and subsidiaries. Finally, the financing cash flows of the organisation have fallen

activities. The comparative evaluation of each of these categories in the cash flow statement for

three years is illustrated as follows:

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative analysis of cash flow

categories of Wesfarmers Limited

Net cash flows from

operating activities

Net cash flows used in

investing activities

Net cash flows used in

financing activities

Figure 1: Comparative analysis of cash flow categories of Wesfarmers Limited for the

years 2015-2017

(Source: Wesfarmers.com.au 2018)

From the above figure, it has been evaluated that the cash flows from operating activities

have declined from $3,791 million in 2015 to $3,365 million in 2016; however, increase is

significant to $4,226 million in 2017. This is because a considerable amount of cash is recovered

from the customers, while there is a decline in income tax payment over the past three years. On

the other hand, the investing cash flows of the organisation have increased from $1,898 million

in 2016 to $2,132 million in 2017; however, considerable decline is observed to $53 million in

2017. This is because Wesfarmers has reduced its acquisition related to plant, property and

equipment and subsidiaries. Finally, the financing cash flows of the organisation have fallen

5CORPORATE ACCOUNTING

significantly from $3,249 million in 2015 to $1,333 million in 2016; however, the increase is

considerable to $3,771 million in 2017. The reason is that it has incurred a significant portion in

order to clear its bank loans in 2017. However, this increase is offset by significant rise in

operating cash flows, due to which the cash base at the end of the year 2017 has increased to

$1,013 million in 2017 from $611 million in 2016.

Other comprehensive income statement:

Part (iii):

The main items that are reported in the other comprehensive income statement of

Wesfarmers Limited include the following:

Foreign currency translation reserve

Cash flow hedge reserve

Retained earnings

Part (iv):

In the words of Damodaran (2016), foreign currency translation reserve is used for

converting the results of the foreign subsidiaries of the parent organisation to the reporting

currency. This is a major portion of the consolidation process of the financial statement, in which

the functional currency of the cross-border entity is ascertained initially. After this, the financial

statements of the foreign entity are remeasured into the reporting currency of the parent firm.

Finally, the profits and losses are recorded on the currency translation.

Cash flow hedge reserve is utilised at the time an organisation is planning to remove or

minimise the exposure arising from changes in cash flows of a financial liability or asset because

significantly from $3,249 million in 2015 to $1,333 million in 2016; however, the increase is

considerable to $3,771 million in 2017. The reason is that it has incurred a significant portion in

order to clear its bank loans in 2017. However, this increase is offset by significant rise in

operating cash flows, due to which the cash base at the end of the year 2017 has increased to

$1,013 million in 2017 from $611 million in 2016.

Other comprehensive income statement:

Part (iii):

The main items that are reported in the other comprehensive income statement of

Wesfarmers Limited include the following:

Foreign currency translation reserve

Cash flow hedge reserve

Retained earnings

Part (iv):

In the words of Damodaran (2016), foreign currency translation reserve is used for

converting the results of the foreign subsidiaries of the parent organisation to the reporting

currency. This is a major portion of the consolidation process of the financial statement, in which

the functional currency of the cross-border entity is ascertained initially. After this, the financial

statements of the foreign entity are remeasured into the reporting currency of the parent firm.

Finally, the profits and losses are recorded on the currency translation.

Cash flow hedge reserve is utilised at the time an organisation is planning to remove or

minimise the exposure arising from changes in cash flows of a financial liability or asset because

6CORPORATE ACCOUNTING

of changes in a specific risk like rate of interest on debt instrument of floating rate (Goh et al.

2016). On the other hand, retained earnings denote the portion of net earnings, which is not

distributed as dividends to the shareholders; instead, the organisation retains it for investing in

core business or paying debt.

Part (v):

As commented by Graham et al. (2017), other comprehensive income is seen as a

diversified view of net profit. In past times, the variations in the profits of an organisation

deemed to be external of its core operations or highly volatile were transferred to the

shareholders’ equity. However, Wesfarmers uses the other comprehensive income statement to

provide significant details on the figures of the above-stated items. Comprehensive income is the

mixture of other comprehensive income and standard net income. These items are reported in

other comprehensive income statement to provide holistic and comprehensive overview of the

drivers of business activities and operations, which could not be reported in the income

statement.

Accounting for corporate income tax:

Part (vi):

A business organisation often incurs various types of expenses like selling and

administrative expense, research and development costs and others, out of which tax expense is

one of them (Khan, Srinivasan and Tan 2016). Moreover, tax expense is taken into account as a

significant liability of the organisation due to the state, federal and municipal governments of the

nation. Tax expense is computed by multiplying the profit before tax with the tax rate applicable

after some significant items are factored such as tax assets and liabilities along with non-

of changes in a specific risk like rate of interest on debt instrument of floating rate (Goh et al.

2016). On the other hand, retained earnings denote the portion of net earnings, which is not

distributed as dividends to the shareholders; instead, the organisation retains it for investing in

core business or paying debt.

Part (v):

As commented by Graham et al. (2017), other comprehensive income is seen as a

diversified view of net profit. In past times, the variations in the profits of an organisation

deemed to be external of its core operations or highly volatile were transferred to the

shareholders’ equity. However, Wesfarmers uses the other comprehensive income statement to

provide significant details on the figures of the above-stated items. Comprehensive income is the

mixture of other comprehensive income and standard net income. These items are reported in

other comprehensive income statement to provide holistic and comprehensive overview of the

drivers of business activities and operations, which could not be reported in the income

statement.

Accounting for corporate income tax:

Part (vi):

A business organisation often incurs various types of expenses like selling and

administrative expense, research and development costs and others, out of which tax expense is

one of them (Khan, Srinivasan and Tan 2016). Moreover, tax expense is taken into account as a

significant liability of the organisation due to the state, federal and municipal governments of the

nation. Tax expense is computed by multiplying the profit before tax with the tax rate applicable

after some significant items are factored such as tax assets and liabilities along with non-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

y6deductible items. Wesfarmers is not exempted from taxation as well. The tax expense

incurred, as per the annual report, has been $1,265 million in 2017 and $631 million in 2016.

Moreover, the tax rate that Wesfarmers uses in accordance with its last published annual report is

30%. By using this rate, the tax expense of Wesfarmers in 2017 would have been $1,241.40

million ($4,138 million x 30%) and $311.40 million ($1,038 million x 30%) in 2016. Thus, it

could be observed that the major tax expenses of the organisation were the above-stated figures

because of the increase in income for the organisation.

Part (vii):

Based on the annual report of Wesfarmers Limited in 2017, the profit before income tax

of the organisation has been $4,138 million, which was $1,038 million in 2016. Moreover, the

tax rate that Wesfarmers uses in accordance with its last published annual report is 30%. By

using this rate, the tax expense of Wesfarmers in 2017 would have been $1,241.40 million

($4,138 million x 30%) and $311.40 million ($1,038 million x 30%) in 2016. However, the tax

expense incurred, as per the annual report, has been $1,265 million in 2017 and $631 million in

2016. Hence, the standard tax expense and the amount actually incurred do not resemble each

other (Grubert and Altshuler 2016). Wesfarmers has made the inclusion or exclusion of few

items in the overall tax expenses, which has lead to such difference in amount. One of these

items is the non-deductible expenses necessary to arrive at the taxable profit. The next item is the

charge of different tax rate for its subsidiaries. For instance, in Australia, the tax rate is 30%;

however, in New Zealand, the tax rate is 28%. Deferred tax asset is another item, from which

Wesfarmers Limited has obtained tax benefits. Finally, non-assessable income is another item

behind the varying tax rate of the organisation.

y6deductible items. Wesfarmers is not exempted from taxation as well. The tax expense

incurred, as per the annual report, has been $1,265 million in 2017 and $631 million in 2016.

Moreover, the tax rate that Wesfarmers uses in accordance with its last published annual report is

30%. By using this rate, the tax expense of Wesfarmers in 2017 would have been $1,241.40

million ($4,138 million x 30%) and $311.40 million ($1,038 million x 30%) in 2016. Thus, it

could be observed that the major tax expenses of the organisation were the above-stated figures

because of the increase in income for the organisation.

Part (vii):

Based on the annual report of Wesfarmers Limited in 2017, the profit before income tax

of the organisation has been $4,138 million, which was $1,038 million in 2016. Moreover, the

tax rate that Wesfarmers uses in accordance with its last published annual report is 30%. By

using this rate, the tax expense of Wesfarmers in 2017 would have been $1,241.40 million

($4,138 million x 30%) and $311.40 million ($1,038 million x 30%) in 2016. However, the tax

expense incurred, as per the annual report, has been $1,265 million in 2017 and $631 million in

2016. Hence, the standard tax expense and the amount actually incurred do not resemble each

other (Grubert and Altshuler 2016). Wesfarmers has made the inclusion or exclusion of few

items in the overall tax expenses, which has lead to such difference in amount. One of these

items is the non-deductible expenses necessary to arrive at the taxable profit. The next item is the

charge of different tax rate for its subsidiaries. For instance, in Australia, the tax rate is 30%;

however, in New Zealand, the tax rate is 28%. Deferred tax asset is another item, from which

Wesfarmers Limited has obtained tax benefits. Finally, non-assessable income is another item

behind the varying tax rate of the organisation.

8CORPORATE ACCOUNTING

Part (viii):

Deferred tax assets denote the situation, in which the organisations either pay higher

taxes or taxes are paid in advance on financial assets (Klassen, Lisowsky and Mescall 2015).

Deferred tax liabilities signify a situation, in which difference could be observed in profit and tax

carrying amount of the organisation (Liu et al. 2016). For Wesfarmers, deferred tax assets have

been $971 million in 2017, which was $1,042 million in 2016, while the deferred tax liabilities

have been $722 million in 2017, which was $611 million in 2016. The deferred tax assets are

realised because of additional depreciation payment due to the variation in taxable rate of

depreciation and depreciation amount. Deferred tax liabilities are recognised because of

temporary differences in business profits, in which lower taxes are paid in 2017.

Part (ix):

Income tax payable is a significant aspect for the business entities in Australia. The

annual report of Wesfarmers states that the income tax payable of the organisation is $292

million in 2017, which was $29 million in 2016. However, differences tend to exist between

income tax expense and income tax payable. The primary reason is deferred tax assets. Instances

are inherent when additional tax expenses are paid in contrast to the actual ones (Qamar, Khalil

and Akhtar 2016). The payment of additional tax amount results in the difference. The second

rule could be observed in the rules of financial accounting and tax accounting. In this aspect, it is

noteworthy to mention depreciation instance. As rates of depreciation vary, its treatment varies

in tax accounting and financial accounting (Ramanna 2014). Hence, the total depreciation

expenses could be raised or declined. These are the basic reasons that variations exist between

income tax expense and income tax payable.

Part (viii):

Deferred tax assets denote the situation, in which the organisations either pay higher

taxes or taxes are paid in advance on financial assets (Klassen, Lisowsky and Mescall 2015).

Deferred tax liabilities signify a situation, in which difference could be observed in profit and tax

carrying amount of the organisation (Liu et al. 2016). For Wesfarmers, deferred tax assets have

been $971 million in 2017, which was $1,042 million in 2016, while the deferred tax liabilities

have been $722 million in 2017, which was $611 million in 2016. The deferred tax assets are

realised because of additional depreciation payment due to the variation in taxable rate of

depreciation and depreciation amount. Deferred tax liabilities are recognised because of

temporary differences in business profits, in which lower taxes are paid in 2017.

Part (ix):

Income tax payable is a significant aspect for the business entities in Australia. The

annual report of Wesfarmers states that the income tax payable of the organisation is $292

million in 2017, which was $29 million in 2016. However, differences tend to exist between

income tax expense and income tax payable. The primary reason is deferred tax assets. Instances

are inherent when additional tax expenses are paid in contrast to the actual ones (Qamar, Khalil

and Akhtar 2016). The payment of additional tax amount results in the difference. The second

rule could be observed in the rules of financial accounting and tax accounting. In this aspect, it is

noteworthy to mention depreciation instance. As rates of depreciation vary, its treatment varies

in tax accounting and financial accounting (Ramanna 2014). Hence, the total depreciation

expenses could be raised or declined. These are the basic reasons that variations exist between

income tax expense and income tax payable.

9CORPORATE ACCOUNTING

Part (x):

Based on the annual report of Wesfarmers in 2017, it could be stated that Wesfarmers has

mentioned tax expenses in income statement as well as in its cash flow statement. However, the

two amounts do not match with each other in the financial statements. In the income statement,

tax expense incurred has been $1,265 million in 2017 and $631 million in 2016. However, in the

cash flow statement, the income tax paid has been $951 million in 2017 and $1,009 million in

2016. Some particular reasons could be identified for such difference. The tax expense in the

income statement is calculated by considering tax expense and other items. However, on the

other hand, in the cash flow statement, the tax expenses fall under the operating cash flows

(Schaltegger, Etxeberria and Ortas 2017). Wesfarmers considers income tax payment in the form

of current asset. However, in the cash flow statement, minimisation in the elements of income

tax expense has been brought denoting the use of cash. This signifies that it has eliminated some

tax expense elements before they are considered in the cash flow statement (Sikka 2017).

Part (xi):

Based on the evaluation of the tax treatment in Wesfarmers Limited, no surprising or

confusing elements could be observed. In other words, all the regulations of the Australian

Taxation Law are adhered to conduct the tax treatment of the organisation. Along with this, it has

provided necessary briefings to support the different factors of taxation that constitute of rate of

tax, income tax payable, current tax liabilities, deferred tax assets, deferred tax liabilities and

others. Out of them, the explanation of the difference between the overall tax expenses is the

most significant factor (Zeff 2016). Moreover, five significant influential dynamics accountable

for developing variation in tax expense could be observed.

Part (x):

Based on the annual report of Wesfarmers in 2017, it could be stated that Wesfarmers has

mentioned tax expenses in income statement as well as in its cash flow statement. However, the

two amounts do not match with each other in the financial statements. In the income statement,

tax expense incurred has been $1,265 million in 2017 and $631 million in 2016. However, in the

cash flow statement, the income tax paid has been $951 million in 2017 and $1,009 million in

2016. Some particular reasons could be identified for such difference. The tax expense in the

income statement is calculated by considering tax expense and other items. However, on the

other hand, in the cash flow statement, the tax expenses fall under the operating cash flows

(Schaltegger, Etxeberria and Ortas 2017). Wesfarmers considers income tax payment in the form

of current asset. However, in the cash flow statement, minimisation in the elements of income

tax expense has been brought denoting the use of cash. This signifies that it has eliminated some

tax expense elements before they are considered in the cash flow statement (Sikka 2017).

Part (xi):

Based on the evaluation of the tax treatment in Wesfarmers Limited, no surprising or

confusing elements could be observed. In other words, all the regulations of the Australian

Taxation Law are adhered to conduct the tax treatment of the organisation. Along with this, it has

provided necessary briefings to support the different factors of taxation that constitute of rate of

tax, income tax payable, current tax liabilities, deferred tax assets, deferred tax liabilities and

others. Out of them, the explanation of the difference between the overall tax expenses is the

most significant factor (Zeff 2016). Moreover, five significant influential dynamics accountable

for developing variation in tax expense could be observed.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE ACCOUNTING

All the necessary working notes to the financial statements are provided for supporting

the treatment of various items. The deferred tax assets are realised because of additional

depreciation payment due to the variation in taxable rate of depreciation and depreciation

amount. Deferred tax liabilities are recognised because of temporary differences in business

profits, in which lower taxes are paid in 2017. These interesting influential dynamics have helped

in improving the understanding and knowledge of business taxation. Hence, this evaluation

would help an individual in obtaining knowledge regarding the tax treatment of the

organisations.

All the necessary working notes to the financial statements are provided for supporting

the treatment of various items. The deferred tax assets are realised because of additional

depreciation payment due to the variation in taxable rate of depreciation and depreciation

amount. Deferred tax liabilities are recognised because of temporary differences in business

profits, in which lower taxes are paid in 2017. These interesting influential dynamics have helped

in improving the understanding and knowledge of business taxation. Hence, this evaluation

would help an individual in obtaining knowledge regarding the tax treatment of the

organisations.

11CORPORATE ACCOUNTING

References:

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F., 2015. Corporate governance,

incentives, and tax avoidance. Journal of Accounting and Economics, 60(1), pp.1-17.

Atanasov, V. and Black, B., 2016. Shock-based causal inference in corporate finance and

accounting research.

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal, 35(1), pp.1-23.

Christensen, D.M., Dhaliwal, D.S., Boivie, S. and Graffin, S.D., 2015. Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), pp.1918-1938.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Goh, B.W., Lee, J., Lim, C.Y. and Shevlin, T., 2016. The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), pp.1647-1670.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate Decision-

making. The Review of Financial Studies, 30(9), pp.3128-3175.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

References:

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F., 2015. Corporate governance,

incentives, and tax avoidance. Journal of Accounting and Economics, 60(1), pp.1-17.

Atanasov, V. and Black, B., 2016. Shock-based causal inference in corporate finance and

accounting research.

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal, 35(1), pp.1-23.

Christensen, D.M., Dhaliwal, D.S., Boivie, S. and Graffin, S.D., 2015. Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), pp.1918-1938.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Goh, B.W., Lee, J., Lim, C.Y. and Shevlin, T., 2016. The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), pp.1647-1670.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate Decision-

making. The Review of Financial Studies, 30(9), pp.3128-3175.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

12CORPORATE ACCOUNTING

Khan, M., Srinivasan, S. and Tan, L., 2016. Institutional ownership and corporate tax avoidance:

New evidence. The Accounting Review, 92(2), pp.101-122.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2015. The role of auditors, non-auditors, and

internal tax departments in corporate tax aggressiveness. The Accounting Review, 91(1), pp.179-

205.

Liu, Y., Li, X., Zeng, H. and An, Y., 2016. Political connections, auditor choice and corporate

accounting transparency: evidence from private sector firms in China. Accounting & Finance.

Qamar, M.A.J., Khalil, F. and Akhtar, W., 2016. Corporate Governance Culture Transmission in

Mutual Funds: Directors as Vector of Transmission. International Journal of Academic Research

in Accounting, Finance and Management Sciences, 6(2), pp.175-183.

Ramanna, K., 2014. Political standards: Accounting for legitimacy.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2), pp.113-

122.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Elsevier.

Wesfarmers.com.au., 2018., [online] Available at: https://www.wesfarmers.com.au/docs/default-

source/default-document-library/2017-annual-report.pdf?sfvrsn=0 [Accessed 6 May 2018].

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

Khan, M., Srinivasan, S. and Tan, L., 2016. Institutional ownership and corporate tax avoidance:

New evidence. The Accounting Review, 92(2), pp.101-122.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2015. The role of auditors, non-auditors, and

internal tax departments in corporate tax aggressiveness. The Accounting Review, 91(1), pp.179-

205.

Liu, Y., Li, X., Zeng, H. and An, Y., 2016. Political connections, auditor choice and corporate

accounting transparency: evidence from private sector firms in China. Accounting & Finance.

Qamar, M.A.J., Khalil, F. and Akhtar, W., 2016. Corporate Governance Culture Transmission in

Mutual Funds: Directors as Vector of Transmission. International Journal of Academic Research

in Accounting, Finance and Management Sciences, 6(2), pp.175-183.

Ramanna, K., 2014. Political standards: Accounting for legitimacy.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2), pp.113-

122.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Elsevier.

Wesfarmers.com.au., 2018., [online] Available at: https://www.wesfarmers.com.au/docs/default-

source/default-document-library/2017-annual-report.pdf?sfvrsn=0 [Accessed 6 May 2018].

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.