Finance Report: Accounting for Decision Making and Control Analysis

VerifiedAdded on 2022/08/11

|17

|3336

|33

Report

AI Summary

This report analyzes accounting for decision making and control, addressing cost allocation, revenue reconciliation, and financial performance. It begins with a cost analysis of support services, comparing traditional and activity-based costing methods, and evaluates the profitability of telephone support and on-site services. The report then applies DuPont analysis to assess and compare the financial performance of two companies, evaluating their profitability, asset turnover, and return on equity. Finally, it examines revenue budgeting, reconciliation, and performance evaluation, considering factors such as student numbers, course fees, and feedback scores. The analysis includes a revenue reconciliation statement, and assesses the performance of marketing, program administration, and faculty.

Running head: ACCOUNTING FOR DECISION MAKING AND CONTROL

Accounting for Decision Making and Control

Name of the Student:

Name of the University:

Author’s Note:

Accounting for Decision Making and Control

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR DECISION MAKING AND CONTROL

Table of Contents

Answer to question 1:......................................................................................................................2

Part a:...........................................................................................................................................2

Part b:...........................................................................................................................................2

Part c:...........................................................................................................................................3

Part d:...........................................................................................................................................3

Part e:...........................................................................................................................................4

Part f:...........................................................................................................................................4

Answer to question 2:......................................................................................................................5

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................6

Answer to question 3:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................8

Part c:...........................................................................................................................................9

Answer to question 4:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................11

Answer to question 5:....................................................................................................................11

Part a:.........................................................................................................................................11

Table of Contents

Answer to question 1:......................................................................................................................2

Part a:...........................................................................................................................................2

Part b:...........................................................................................................................................2

Part c:...........................................................................................................................................3

Part d:...........................................................................................................................................3

Part e:...........................................................................................................................................4

Part f:...........................................................................................................................................4

Answer to question 2:......................................................................................................................5

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................6

Answer to question 3:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................8

Part c:...........................................................................................................................................9

Answer to question 4:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................11

Answer to question 5:....................................................................................................................11

Part a:.........................................................................................................................................11

2ACCOUNTING FOR DECISION MAKING AND CONTROL

Part b:.........................................................................................................................................11

Part c:.........................................................................................................................................12

Part d:.........................................................................................................................................12

Part e:.........................................................................................................................................12

Bibliography:.................................................................................................................................14

Part b:.........................................................................................................................................11

Part c:.........................................................................................................................................12

Part d:.........................................................................................................................................12

Part e:.........................................................................................................................................12

Bibliography:.................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR DECISION MAKING AND CONTROL

Answer to question 1:

Part a:

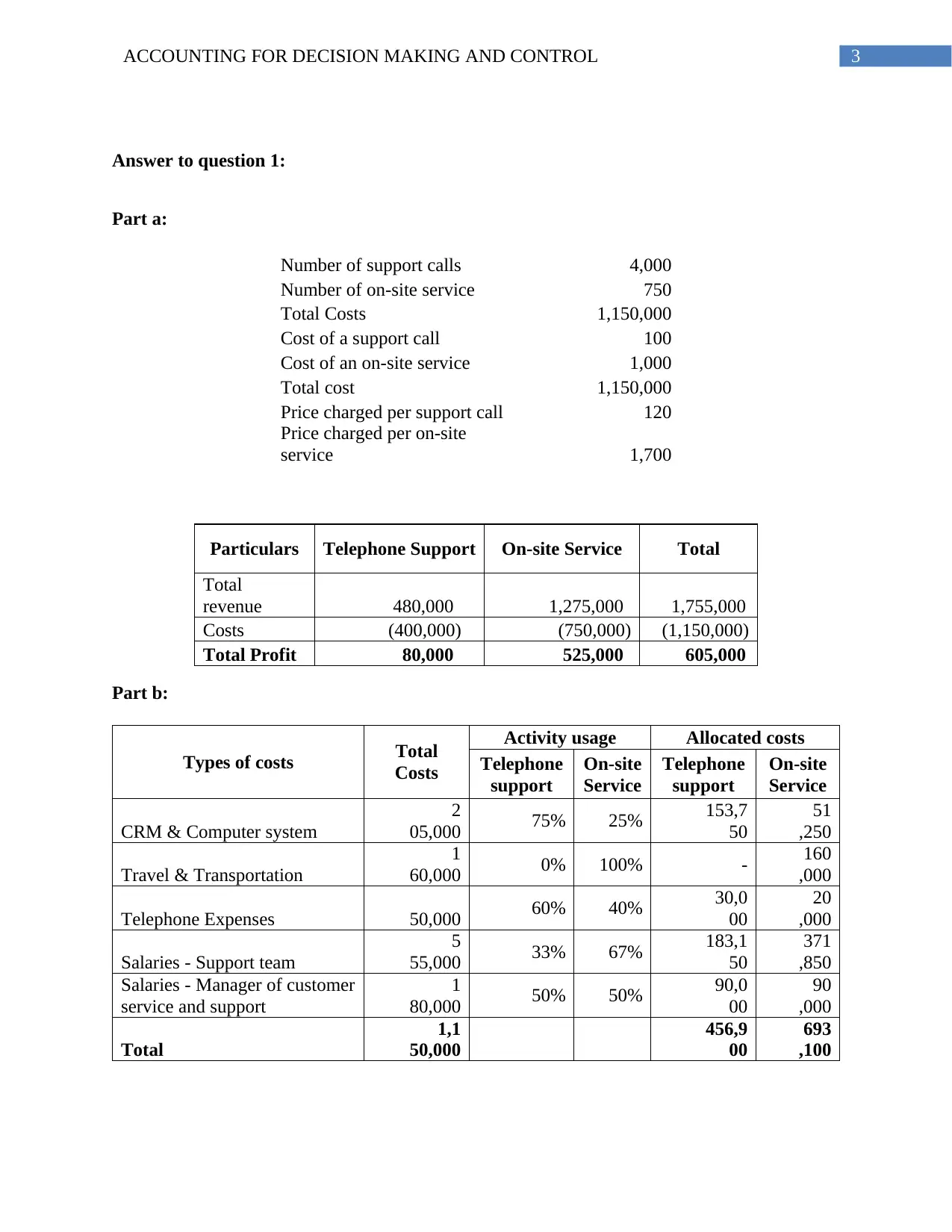

Number of support calls 4,000

Number of on-site service 750

Total Costs 1,150,000

Cost of a support call 100

Cost of an on-site service 1,000

Total cost 1,150,000

Price charged per support call 120

Price charged per on-site

service 1,700

Particulars Telephone Support On-site Service Total

Total

revenue 480,000 1,275,000 1,755,000

Costs (400,000) (750,000) (1,150,000)

Total Profit 80,000 525,000 605,000

Part b:

Types of costs Total

Costs

Activity usage Allocated costs

Telephone

support

On-site

Service

Telephone

support

On-site

Service

CRM & Computer system

2

05,000 75% 25% 153,7

50

51

,250

Travel & Transportation

1

60,000 0% 100% - 160

,000

Telephone Expenses 50,000 60% 40% 30,0

00

20

,000

Salaries - Support team

5

55,000 33% 67% 183,1

50

371

,850

Salaries - Manager of customer

service and support

1

80,000 50% 50% 90,0

00

90

,000

Total

1,1

50,000

456,9

00

693

,100

Answer to question 1:

Part a:

Number of support calls 4,000

Number of on-site service 750

Total Costs 1,150,000

Cost of a support call 100

Cost of an on-site service 1,000

Total cost 1,150,000

Price charged per support call 120

Price charged per on-site

service 1,700

Particulars Telephone Support On-site Service Total

Total

revenue 480,000 1,275,000 1,755,000

Costs (400,000) (750,000) (1,150,000)

Total Profit 80,000 525,000 605,000

Part b:

Types of costs Total

Costs

Activity usage Allocated costs

Telephone

support

On-site

Service

Telephone

support

On-site

Service

CRM & Computer system

2

05,000 75% 25% 153,7

50

51

,250

Travel & Transportation

1

60,000 0% 100% - 160

,000

Telephone Expenses 50,000 60% 40% 30,0

00

20

,000

Salaries - Support team

5

55,000 33% 67% 183,1

50

371

,850

Salaries - Manager of customer

service and support

1

80,000 50% 50% 90,0

00

90

,000

Total

1,1

50,000

456,9

00

693

,100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR DECISION MAKING AND CONTROL

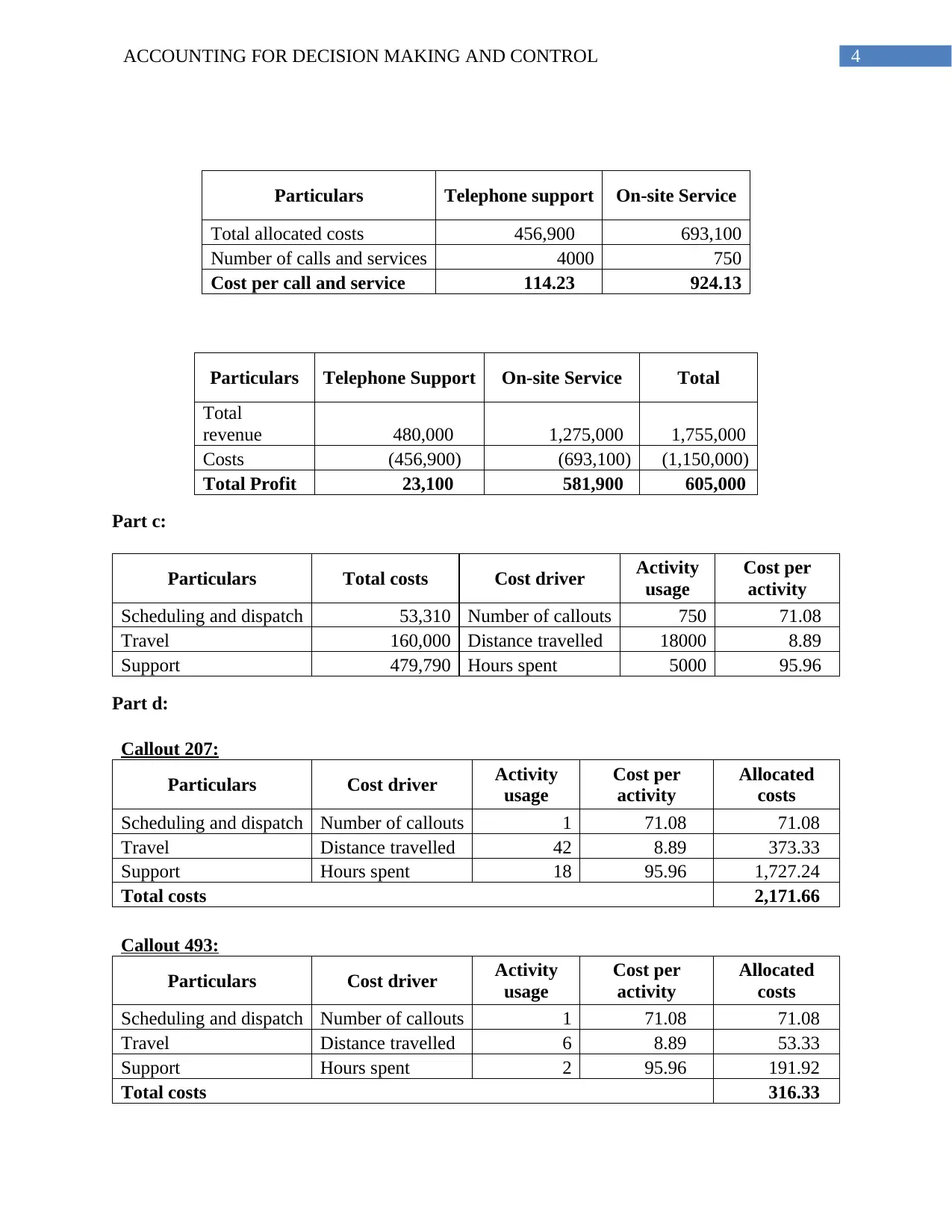

Particulars Telephone support On-site Service

Total allocated costs 456,900 693,100

Number of calls and services 4000 750

Cost per call and service 114.23 924.13

Particulars Telephone Support On-site Service Total

Total

revenue 480,000 1,275,000 1,755,000

Costs (456,900) (693,100) (1,150,000)

Total Profit 23,100 581,900 605,000

Part c:

Particulars Total costs Cost driver Activity

usage

Cost per

activity

Scheduling and dispatch 53,310 Number of callouts 750 71.08

Travel 160,000 Distance travelled 18000 8.89

Support 479,790 Hours spent 5000 95.96

Part d:

Callout 207:

Particulars Cost driver Activity

usage

Cost per

activity

Allocated

costs

Scheduling and dispatch Number of callouts 1 71.08 71.08

Travel Distance travelled 42 8.89 373.33

Support Hours spent 18 95.96 1,727.24

Total costs 2,171.66

Callout 493:

Particulars Cost driver Activity

usage

Cost per

activity

Allocated

costs

Scheduling and dispatch Number of callouts 1 71.08 71.08

Travel Distance travelled 6 8.89 53.33

Support Hours spent 2 95.96 191.92

Total costs 316.33

Particulars Telephone support On-site Service

Total allocated costs 456,900 693,100

Number of calls and services 4000 750

Cost per call and service 114.23 924.13

Particulars Telephone Support On-site Service Total

Total

revenue 480,000 1,275,000 1,755,000

Costs (456,900) (693,100) (1,150,000)

Total Profit 23,100 581,900 605,000

Part c:

Particulars Total costs Cost driver Activity

usage

Cost per

activity

Scheduling and dispatch 53,310 Number of callouts 750 71.08

Travel 160,000 Distance travelled 18000 8.89

Support 479,790 Hours spent 5000 95.96

Part d:

Callout 207:

Particulars Cost driver Activity

usage

Cost per

activity

Allocated

costs

Scheduling and dispatch Number of callouts 1 71.08 71.08

Travel Distance travelled 42 8.89 373.33

Support Hours spent 18 95.96 1,727.24

Total costs 2,171.66

Callout 493:

Particulars Cost driver Activity

usage

Cost per

activity

Allocated

costs

Scheduling and dispatch Number of callouts 1 71.08 71.08

Travel Distance travelled 6 8.89 53.33

Support Hours spent 2 95.96 191.92

Total costs 316.33

5ACCOUNTING FOR DECISION MAKING AND CONTROL

Part e:

There are various methods that can be used for ascertainment and allocation of costs.

Under traditional method or the volume based costing method, costs are ascertained and

allocated based on a single costs driver or base. It might not be always true that all the segments

or departments are always consuming the services or using the facilities at the same rate. Hence,

it would not be always fair to allocate the cost at the same predetermined allocation rate. In the

given case study, the cost has been allocated to the telephone support and on-site support at a

predetermined rate. It can be observed that, when the actual costs are allocated to number of calls

and on-site support, the cost per telephone support and on-site support becomes much higher that

the predetermined costs. Hence, it is better to use the revised costs as determined in the second

part.

Activity costing system is the most scientific and rational method of allocation of costs to

various departments and product or service units based on the consumption and utilization of

various individual service r facilities. It allocates the costs to the departments, product or service

units on a more rational and scientific way. Hence, it can be recommended to the company to use

the activity based costing system to ascertain and allocate costs per telephone support or on-site

support.

Part f:

It can be observed that in the first of this case study, the costs have been allocated on a

predetermined rate. In the second part, costs have been classified to the telephone support service

and on-site support service based on the utilization of the services, still it might not be a rational

Part e:

There are various methods that can be used for ascertainment and allocation of costs.

Under traditional method or the volume based costing method, costs are ascertained and

allocated based on a single costs driver or base. It might not be always true that all the segments

or departments are always consuming the services or using the facilities at the same rate. Hence,

it would not be always fair to allocate the cost at the same predetermined allocation rate. In the

given case study, the cost has been allocated to the telephone support and on-site support at a

predetermined rate. It can be observed that, when the actual costs are allocated to number of calls

and on-site support, the cost per telephone support and on-site support becomes much higher that

the predetermined costs. Hence, it is better to use the revised costs as determined in the second

part.

Activity costing system is the most scientific and rational method of allocation of costs to

various departments and product or service units based on the consumption and utilization of

various individual service r facilities. It allocates the costs to the departments, product or service

units on a more rational and scientific way. Hence, it can be recommended to the company to use

the activity based costing system to ascertain and allocate costs per telephone support or on-site

support.

Part f:

It can be observed that in the first of this case study, the costs have been allocated on a

predetermined rate. In the second part, costs have been classified to the telephone support service

and on-site support service based on the utilization of the services, still it might not be a rational

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR DECISION MAKING AND CONTROL

way of allocating costs to the telephone support and on-site service, as the time consumption for

the each of the individual telephone call and on-site support may be different. Therefore, an

activity based costing system for allocation and ascertainment of costs for each of the telephone

support and on-site service should be applied. It can be observed that, in the last part of the case

study, only a few activities have been identified for the on-site support service. There might be

other activities also which can be considered as the costs drivers and based on that costs can be

allocated further in more rational and efficient way. Moreover, for the on-site service only the

activities have been identified, though it can be identified and implemented for the telephone

support service also.

Answer to question 2:

Part a:

DuPont analysis is a method of evaluation of the financial performance and financial

strength of a company based on the return on equity calculated from various other performance

measurement ratios. In DuPont analysis the return on equity is calculated as the product of

profitability, assets turnover and the equity multiplier or the leverage of the company. In the

given case study, information related to the financial performance and financial position of the

Nimble Ned Pty Ltd and the Agile Andrea Pty Ltd have been given. The non-current liabilities of

both the companies have been computed as the balancing figure of current liabilities and equity

from the total assets. The net profit margin has been calculated from the profit after interest.

Following calculations shows the parameters of the DuPont analysis and the return on equity

under the DuPont analysis.

way of allocating costs to the telephone support and on-site service, as the time consumption for

the each of the individual telephone call and on-site support may be different. Therefore, an

activity based costing system for allocation and ascertainment of costs for each of the telephone

support and on-site service should be applied. It can be observed that, in the last part of the case

study, only a few activities have been identified for the on-site support service. There might be

other activities also which can be considered as the costs drivers and based on that costs can be

allocated further in more rational and efficient way. Moreover, for the on-site service only the

activities have been identified, though it can be identified and implemented for the telephone

support service also.

Answer to question 2:

Part a:

DuPont analysis is a method of evaluation of the financial performance and financial

strength of a company based on the return on equity calculated from various other performance

measurement ratios. In DuPont analysis the return on equity is calculated as the product of

profitability, assets turnover and the equity multiplier or the leverage of the company. In the

given case study, information related to the financial performance and financial position of the

Nimble Ned Pty Ltd and the Agile Andrea Pty Ltd have been given. The non-current liabilities of

both the companies have been computed as the balancing figure of current liabilities and equity

from the total assets. The net profit margin has been calculated from the profit after interest.

Following calculations shows the parameters of the DuPont analysis and the return on equity

under the DuPont analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR DECISION MAKING AND CONTROL

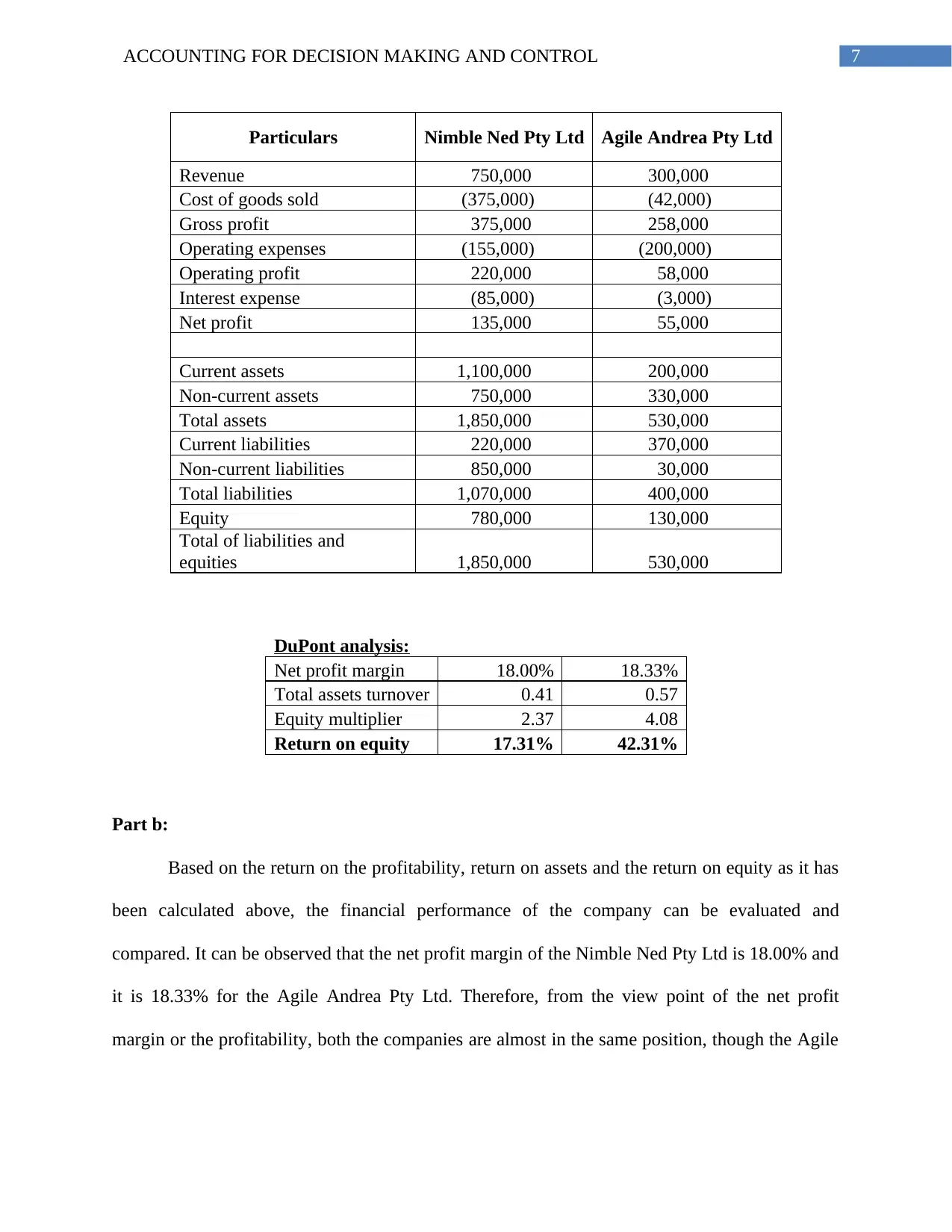

Particulars Nimble Ned Pty Ltd Agile Andrea Pty Ltd

Revenue 750,000 300,000

Cost of goods sold (375,000) (42,000)

Gross profit 375,000 258,000

Operating expenses (155,000) (200,000)

Operating profit 220,000 58,000

Interest expense (85,000) (3,000)

Net profit 135,000 55,000

Current assets 1,100,000 200,000

Non-current assets 750,000 330,000

Total assets 1,850,000 530,000

Current liabilities 220,000 370,000

Non-current liabilities 850,000 30,000

Total liabilities 1,070,000 400,000

Equity 780,000 130,000

Total of liabilities and

equities 1,850,000 530,000

DuPont analysis:

Net profit margin 18.00% 18.33%

Total assets turnover 0.41 0.57

Equity multiplier 2.37 4.08

Return on equity 17.31% 42.31%

Part b:

Based on the return on the profitability, return on assets and the return on equity as it has

been calculated above, the financial performance of the company can be evaluated and

compared. It can be observed that the net profit margin of the Nimble Ned Pty Ltd is 18.00% and

it is 18.33% for the Agile Andrea Pty Ltd. Therefore, from the view point of the net profit

margin or the profitability, both the companies are almost in the same position, though the Agile

Particulars Nimble Ned Pty Ltd Agile Andrea Pty Ltd

Revenue 750,000 300,000

Cost of goods sold (375,000) (42,000)

Gross profit 375,000 258,000

Operating expenses (155,000) (200,000)

Operating profit 220,000 58,000

Interest expense (85,000) (3,000)

Net profit 135,000 55,000

Current assets 1,100,000 200,000

Non-current assets 750,000 330,000

Total assets 1,850,000 530,000

Current liabilities 220,000 370,000

Non-current liabilities 850,000 30,000

Total liabilities 1,070,000 400,000

Equity 780,000 130,000

Total of liabilities and

equities 1,850,000 530,000

DuPont analysis:

Net profit margin 18.00% 18.33%

Total assets turnover 0.41 0.57

Equity multiplier 2.37 4.08

Return on equity 17.31% 42.31%

Part b:

Based on the return on the profitability, return on assets and the return on equity as it has

been calculated above, the financial performance of the company can be evaluated and

compared. It can be observed that the net profit margin of the Nimble Ned Pty Ltd is 18.00% and

it is 18.33% for the Agile Andrea Pty Ltd. Therefore, from the view point of the net profit

margin or the profitability, both the companies are almost in the same position, though the Agile

8ACCOUNTING FOR DECISION MAKING AND CONTROL

Andrea Pty Ltd is having a slightly higher net profit margin. A net profit margin of around 18%

can be considered as a good profitability for a company.

Assets turnover is the ratio of total assets to the total turnover of the company. It can be

observed from the above analysis that the Nimble Ned Pty Ltd is 0.41 while the assets turnover is

0.57 for the Agile Andrea Pty Ltd. It can be observed that the assets turnover ratio is higher for

the Agile Andrea Pty Ltd as compared to the Nimble Ned Pty Ltd. Hence, from the view point of

the assets turnover, the Agile Andrea Pty Ltd is in a better position. Assets turnover ratio implies

the efficiency in utilization of assets of the company to generate revenue and to earn a significant

amount of profit. It can also be used as a measure of the management efficiency of the company.

Hence, it can be concluded that the Agile Andrea Pty Ltd is much more efficient than the Nimble

Ned Pty Ltd in managing and utilizing their assets towards generation of revenue and profit.

Following bar chart can be used for comparison of profitability and financial performance of two

of the companies for better analysis.

Net profit margin Total assets turnover Return on equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

DuPont Analysis Comparison

Nimble Ned Pty Ltd Agile Andrea Pty Ltd

Andrea Pty Ltd is having a slightly higher net profit margin. A net profit margin of around 18%

can be considered as a good profitability for a company.

Assets turnover is the ratio of total assets to the total turnover of the company. It can be

observed from the above analysis that the Nimble Ned Pty Ltd is 0.41 while the assets turnover is

0.57 for the Agile Andrea Pty Ltd. It can be observed that the assets turnover ratio is higher for

the Agile Andrea Pty Ltd as compared to the Nimble Ned Pty Ltd. Hence, from the view point of

the assets turnover, the Agile Andrea Pty Ltd is in a better position. Assets turnover ratio implies

the efficiency in utilization of assets of the company to generate revenue and to earn a significant

amount of profit. It can also be used as a measure of the management efficiency of the company.

Hence, it can be concluded that the Agile Andrea Pty Ltd is much more efficient than the Nimble

Ned Pty Ltd in managing and utilizing their assets towards generation of revenue and profit.

Following bar chart can be used for comparison of profitability and financial performance of two

of the companies for better analysis.

Net profit margin Total assets turnover Return on equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

DuPont Analysis Comparison

Nimble Ned Pty Ltd Agile Andrea Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR DECISION MAKING AND CONTROL

Return on equity is another measure of the profitability and management efficiency of the

company. It can be observed that the return on equity for the Nimble Ned Pty Ltd is 17.31%,

while the return on equity is 42.31% for the Agile Andrea Pty Ltd. Therefor it can be concluded

that with the higher profit margin, assets turnover and equity multiplier, the Agile Andrea Pty

Ltd is having better financial performance and financial position as compared to the financial

performance and financial position of Nimble Ned Pty Ltd.

Answer to question 3:

Part a:

Based on the given information related to the number of courses offered, expected

number of students and feedback score, the revenue budget can be prepared as follows.

Expected number of student 50

Number of courses per student 16

Upfront fee per course 2,000

End of course fee multiplier 550

Average feedback score 7

Revenue Budget:

Upfront fees 1,600,000

End of course fees 3,080,000

Total Revenue 4,680,000

Part b:

Based on the actual number of students, actual number of courses offered and actual

average feedback score, the actual amount of revenue can be computed as follows and a revenue

reconciliation statement has been prepared to reconcile the budgeted revenue to the actual

revenue.

Return on equity is another measure of the profitability and management efficiency of the

company. It can be observed that the return on equity for the Nimble Ned Pty Ltd is 17.31%,

while the return on equity is 42.31% for the Agile Andrea Pty Ltd. Therefor it can be concluded

that with the higher profit margin, assets turnover and equity multiplier, the Agile Andrea Pty

Ltd is having better financial performance and financial position as compared to the financial

performance and financial position of Nimble Ned Pty Ltd.

Answer to question 3:

Part a:

Based on the given information related to the number of courses offered, expected

number of students and feedback score, the revenue budget can be prepared as follows.

Expected number of student 50

Number of courses per student 16

Upfront fee per course 2,000

End of course fee multiplier 550

Average feedback score 7

Revenue Budget:

Upfront fees 1,600,000

End of course fees 3,080,000

Total Revenue 4,680,000

Part b:

Based on the actual number of students, actual number of courses offered and actual

average feedback score, the actual amount of revenue can be computed as follows and a revenue

reconciliation statement has been prepared to reconcile the budgeted revenue to the actual

revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR DECISION MAKING AND CONTROL

Actual number of student 46

Number of courses per student 17

Upfront fee per course 1,900

End of course fee multiplier 550

Average feedback score 7.90

Upfront fees 1,485,800

End of course fees 3,397,790

Total Actual Revenue 4,883,590

Revenue reconciliation of budgeted revenue to actual revenue:

Budgeted revenue 4,680,000

Decrease in upfront fees due to number of students (128,000)

Decrease in upfront fees due to discount (73,600)

Increase in upfront revenue due to number of courses 87,400

Decrease in end of course revenue due to number of students (246,400)

Increase in end of course revenue due to higher feedback score 364,320

Increase in end of course revenue due to number of courses 199870

Actual revenue 4,883,590

Part c:

It can be observed that the actual number of student is 46 while the budget was for 50

students. Hence, the marketing and admission team has been performed well but they failed to

achieve the budgeted and target number of students. Therefore, the marketing and admission

team has been performed significantly well but somehow fail to achieve the target. It can further

be observed that the base upfront fees payment was 2,000, while they have to reduce it down to

1,900 due to completion in the market. It caused a significant amount of revenue loss due to a

higher amount of discount.

Actual number of student 46

Number of courses per student 17

Upfront fee per course 1,900

End of course fee multiplier 550

Average feedback score 7.90

Upfront fees 1,485,800

End of course fees 3,397,790

Total Actual Revenue 4,883,590

Revenue reconciliation of budgeted revenue to actual revenue:

Budgeted revenue 4,680,000

Decrease in upfront fees due to number of students (128,000)

Decrease in upfront fees due to discount (73,600)

Increase in upfront revenue due to number of courses 87,400

Decrease in end of course revenue due to number of students (246,400)

Increase in end of course revenue due to higher feedback score 364,320

Increase in end of course revenue due to number of courses 199870

Actual revenue 4,883,590

Part c:

It can be observed that the actual number of student is 46 while the budget was for 50

students. Hence, the marketing and admission team has been performed well but they failed to

achieve the budgeted and target number of students. Therefore, the marketing and admission

team has been performed significantly well but somehow fail to achieve the target. It can further

be observed that the base upfront fees payment was 2,000, while they have to reduce it down to

1,900 due to completion in the market. It caused a significant amount of revenue loss due to a

higher amount of discount.

11ACCOUNTING FOR DECISION MAKING AND CONTROL

The programme admin is responsible for the course structure and conducting the courses

successfully. It can be observed that, while there was a budget for 16 number of courses, they

managed to offer 17 number of courses actually, which implies a better performance of the

programme admin. Moreover, it has been estimated that there would be an average feedback

score of 7, while the actual average feedback score is 7.9. It contributed significantly to the total

revenue of the organization, as the end of course fee depends on the feedback score. Therefore, it

can be concluded that the programme admin performed very well.

Faculties of the organization are responsible for the efficient delivery of the course and

successful completion of the course. Based on the average feedback score of the students, it can

be concluded that the faculties of the organization have performed very well though there are

still ample scope of improvement of the service leading to a full satisfaction and higher feedback

score.

Answer to question 4:

Part a:

Strategies are the set of alternative plans for an organization which are built up for

achieving the mission and vision or overall objectives of the organization. It always have

different alternatives and changing plans for different and changing situations. Execution or

implementation of the strategies at the management level and at the ground level of an

organization is the way in which the organization can achieve their mission and vision.

Performance measure of the organization as well as the employees are important for

evaluating the performance of the organization and to find out any discrepancies and to take

The programme admin is responsible for the course structure and conducting the courses

successfully. It can be observed that, while there was a budget for 16 number of courses, they

managed to offer 17 number of courses actually, which implies a better performance of the

programme admin. Moreover, it has been estimated that there would be an average feedback

score of 7, while the actual average feedback score is 7.9. It contributed significantly to the total

revenue of the organization, as the end of course fee depends on the feedback score. Therefore, it

can be concluded that the programme admin performed very well.

Faculties of the organization are responsible for the efficient delivery of the course and

successful completion of the course. Based on the average feedback score of the students, it can

be concluded that the faculties of the organization have performed very well though there are

still ample scope of improvement of the service leading to a full satisfaction and higher feedback

score.

Answer to question 4:

Part a:

Strategies are the set of alternative plans for an organization which are built up for

achieving the mission and vision or overall objectives of the organization. It always have

different alternatives and changing plans for different and changing situations. Execution or

implementation of the strategies at the management level and at the ground level of an

organization is the way in which the organization can achieve their mission and vision.

Performance measure of the organization as well as the employees are important for

evaluating the performance of the organization and to find out any discrepancies and to take

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.