A Detailed Report on Accounting for Forfeiture & Reissue

VerifiedAdded on 2024/06/04

|14

|2019

|69

Report

AI Summary

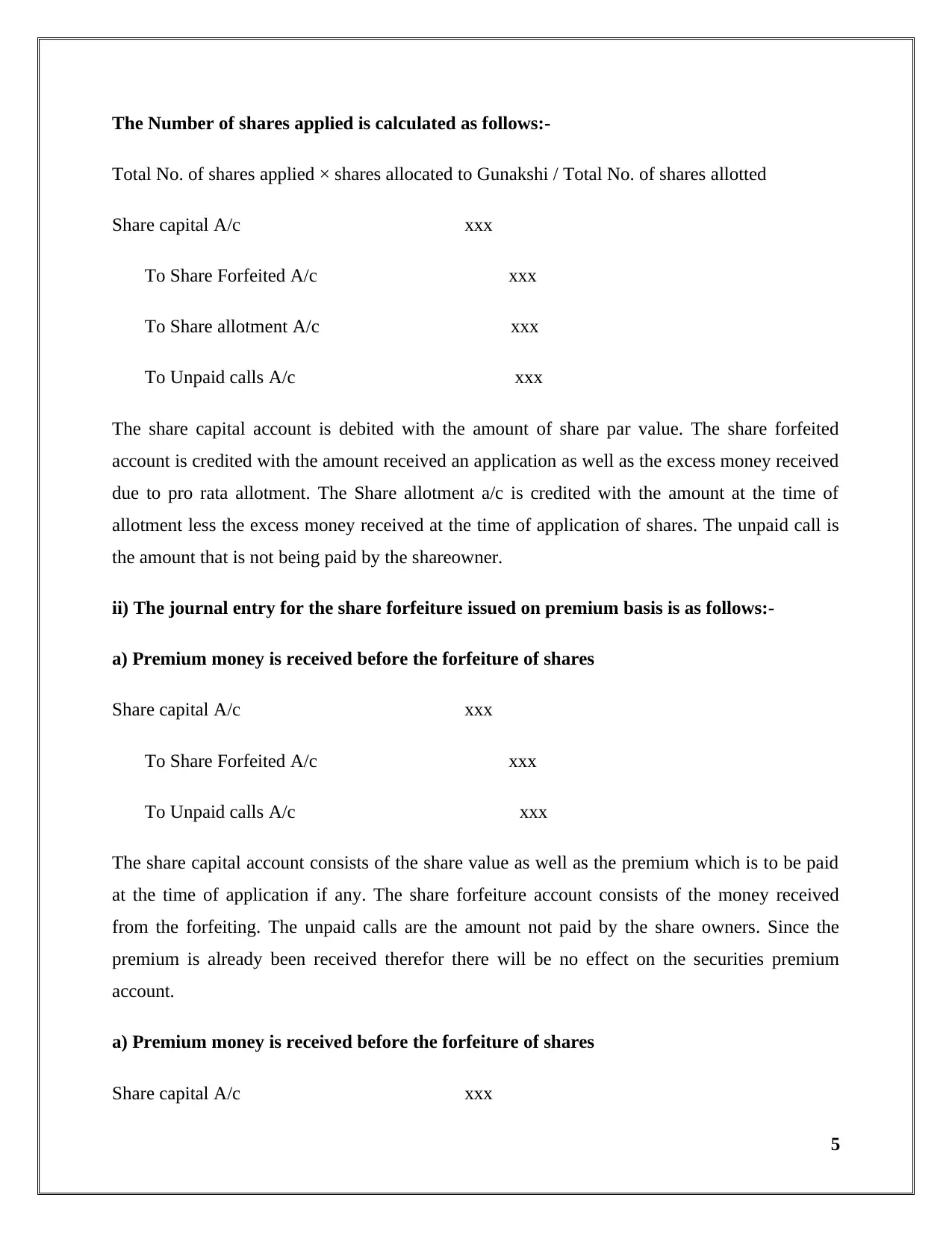

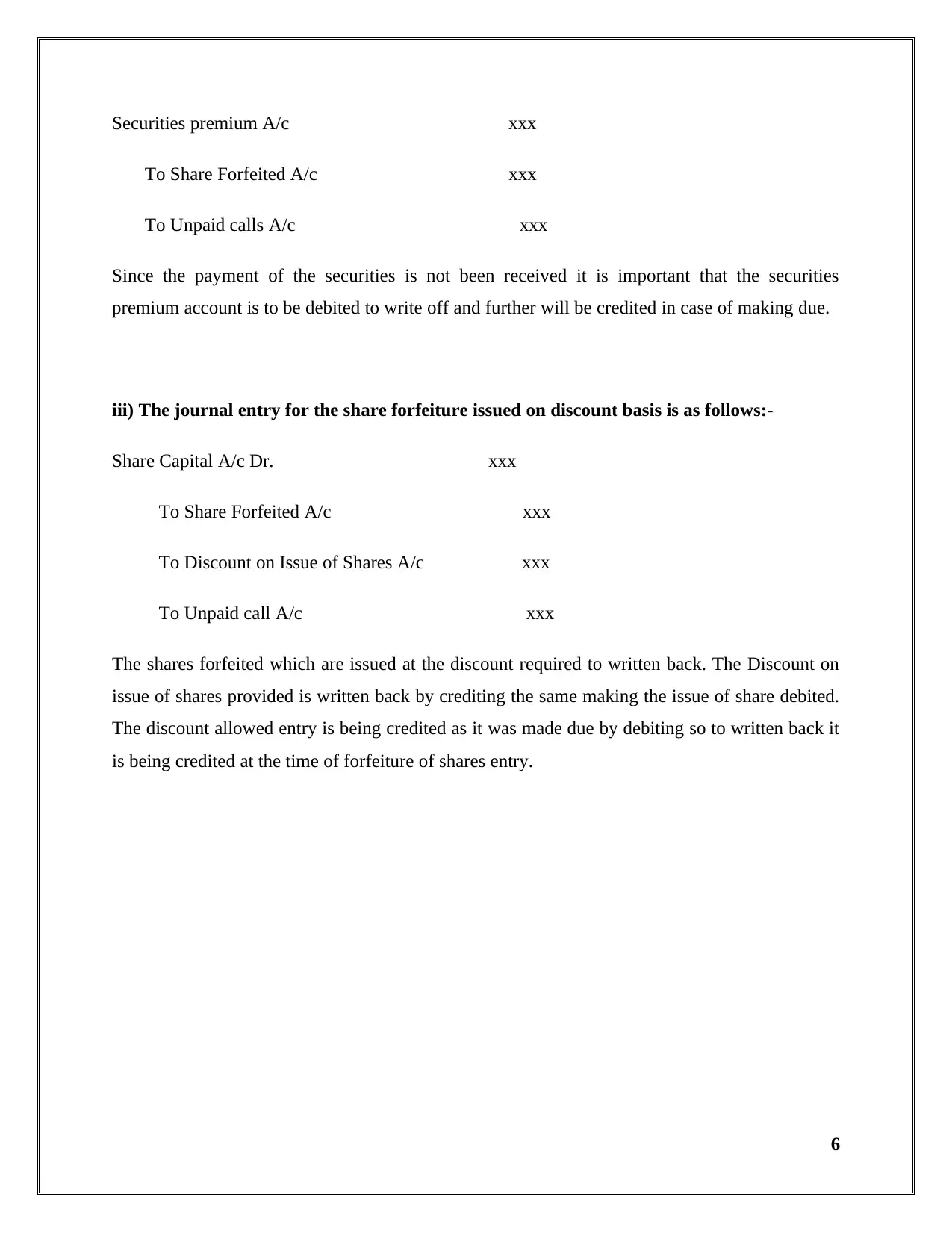

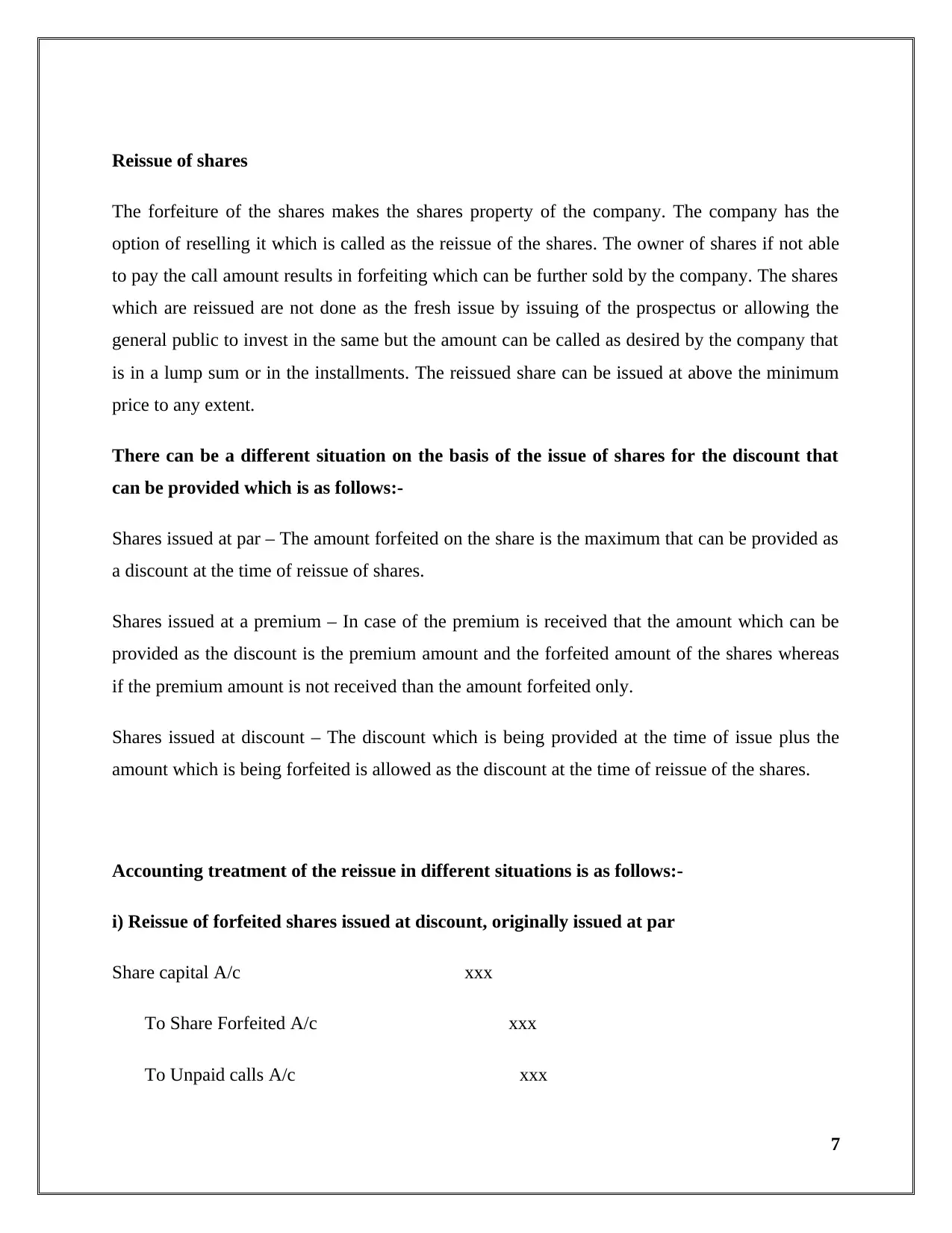

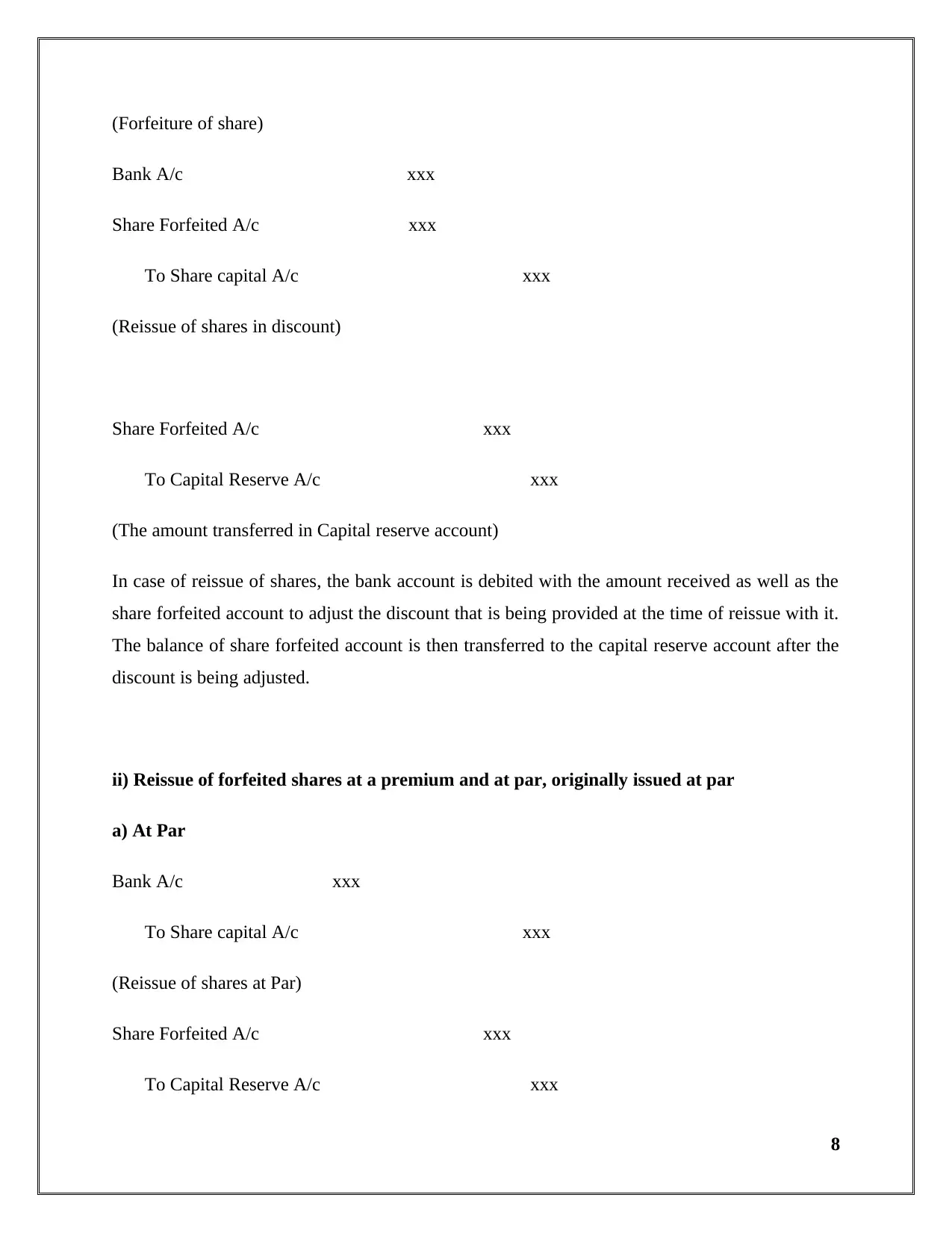

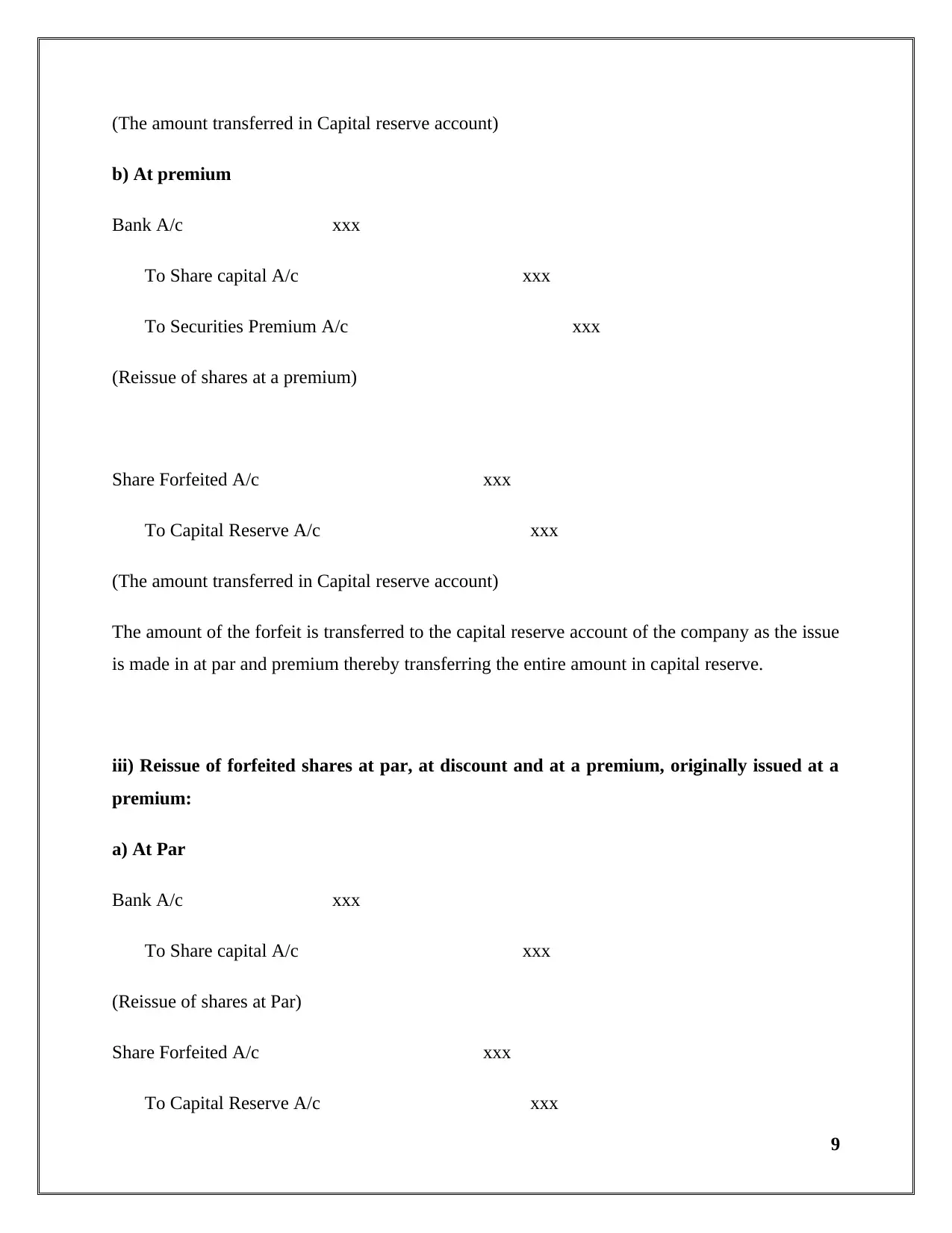

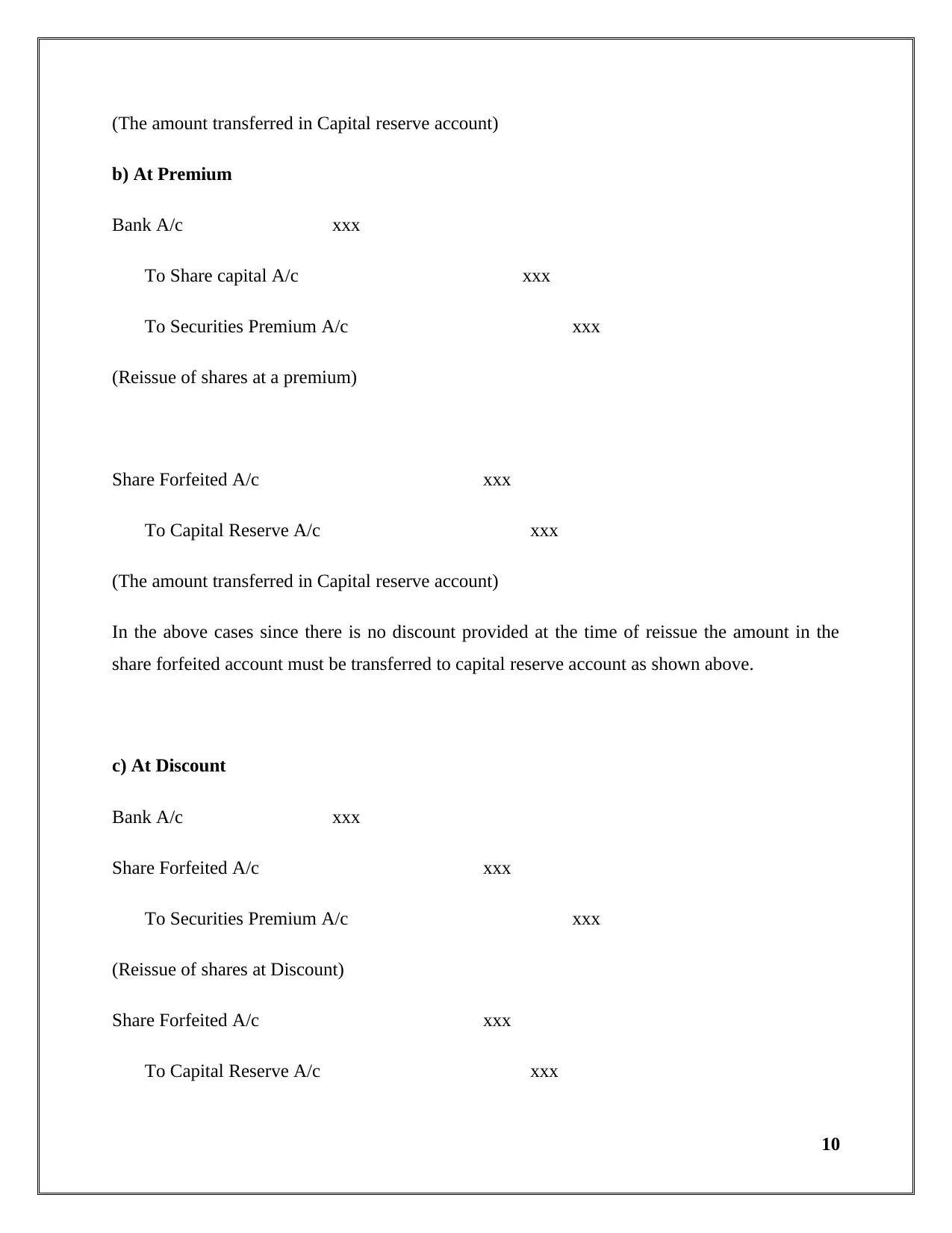

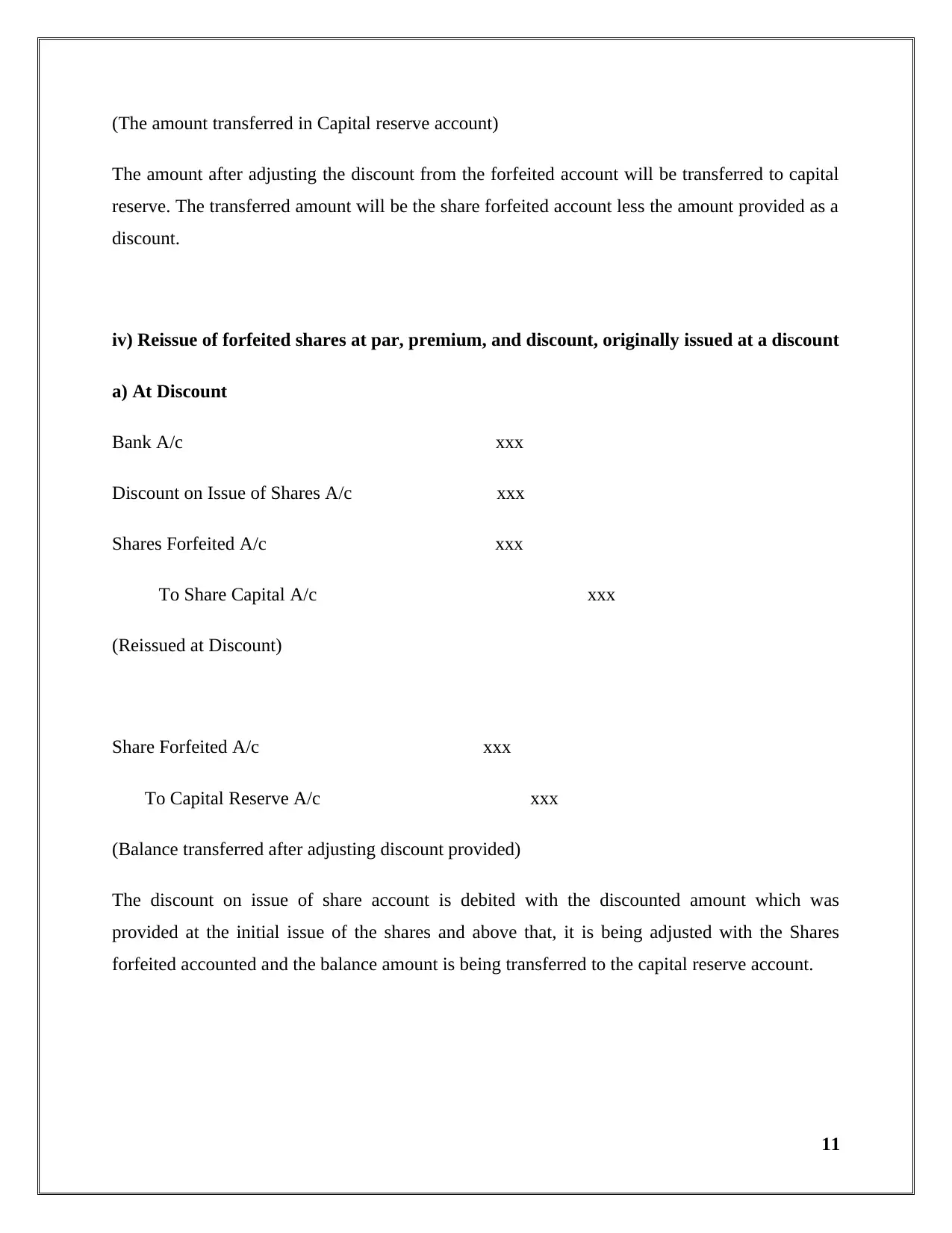

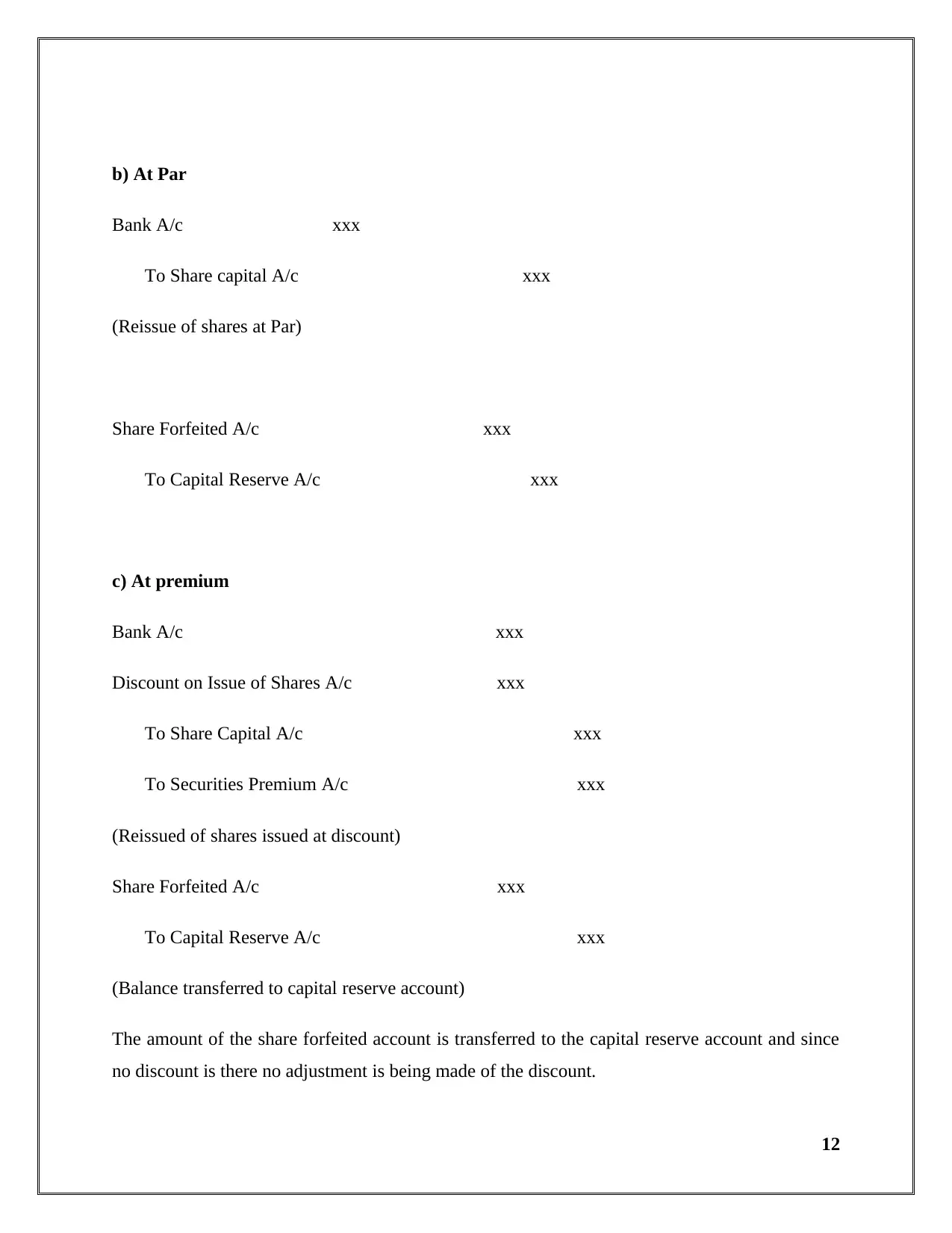

This report provides a detailed analysis of the accounting treatment for the forfeiture and reissue of shares. It covers various scenarios, including shares issued at par, premium, and discount. The report explains the cancellation of shares, the process of forfeiture due to non-payment of allotment or call money, and the subsequent reissue of these shares. It includes journal entries for different situations, such as forfeiture of shares issued at par, premium, or discount, and the corresponding accounting treatment for the reissue of forfeited shares. The report also addresses the treatment of securities premium and discounts on the issue of shares, along with the transfer of amounts to the capital reserve account. It references relevant sections of the Companies Act 2001 and other sources to support its analysis.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.