Detailed Analysis: Accounting for Income Tax - Finance Module

VerifiedAdded on 2020/03/02

|10

|824

|32

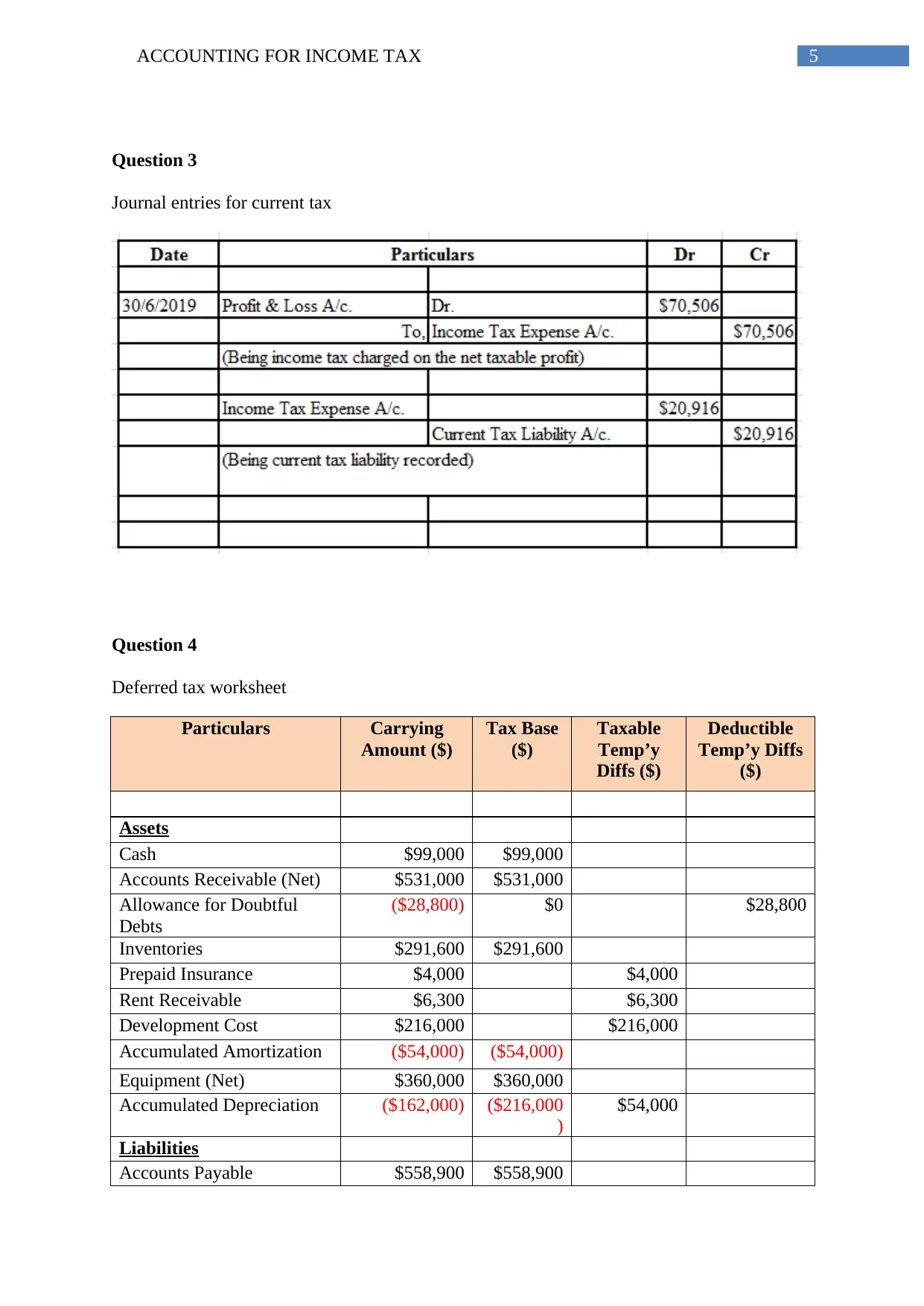

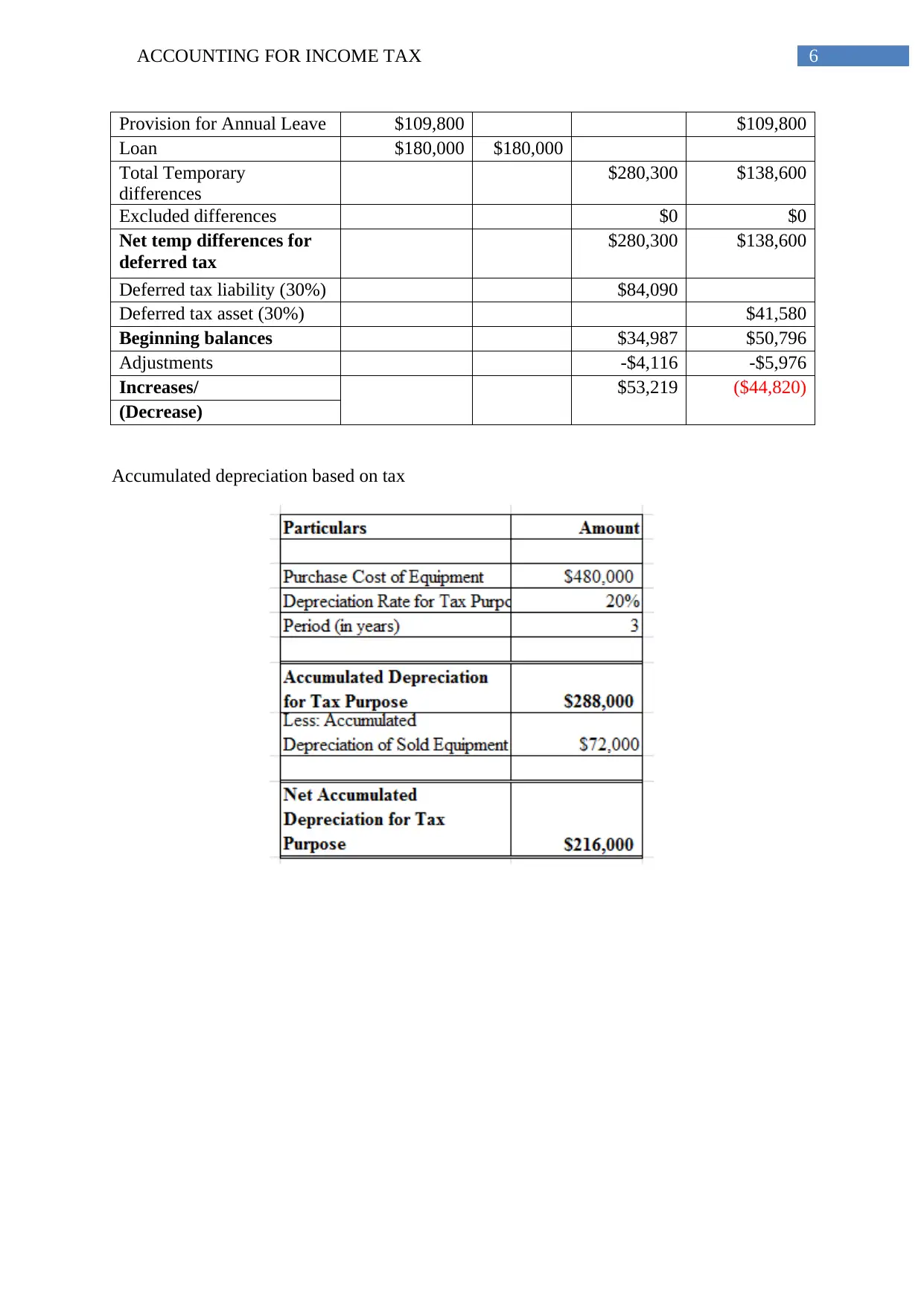

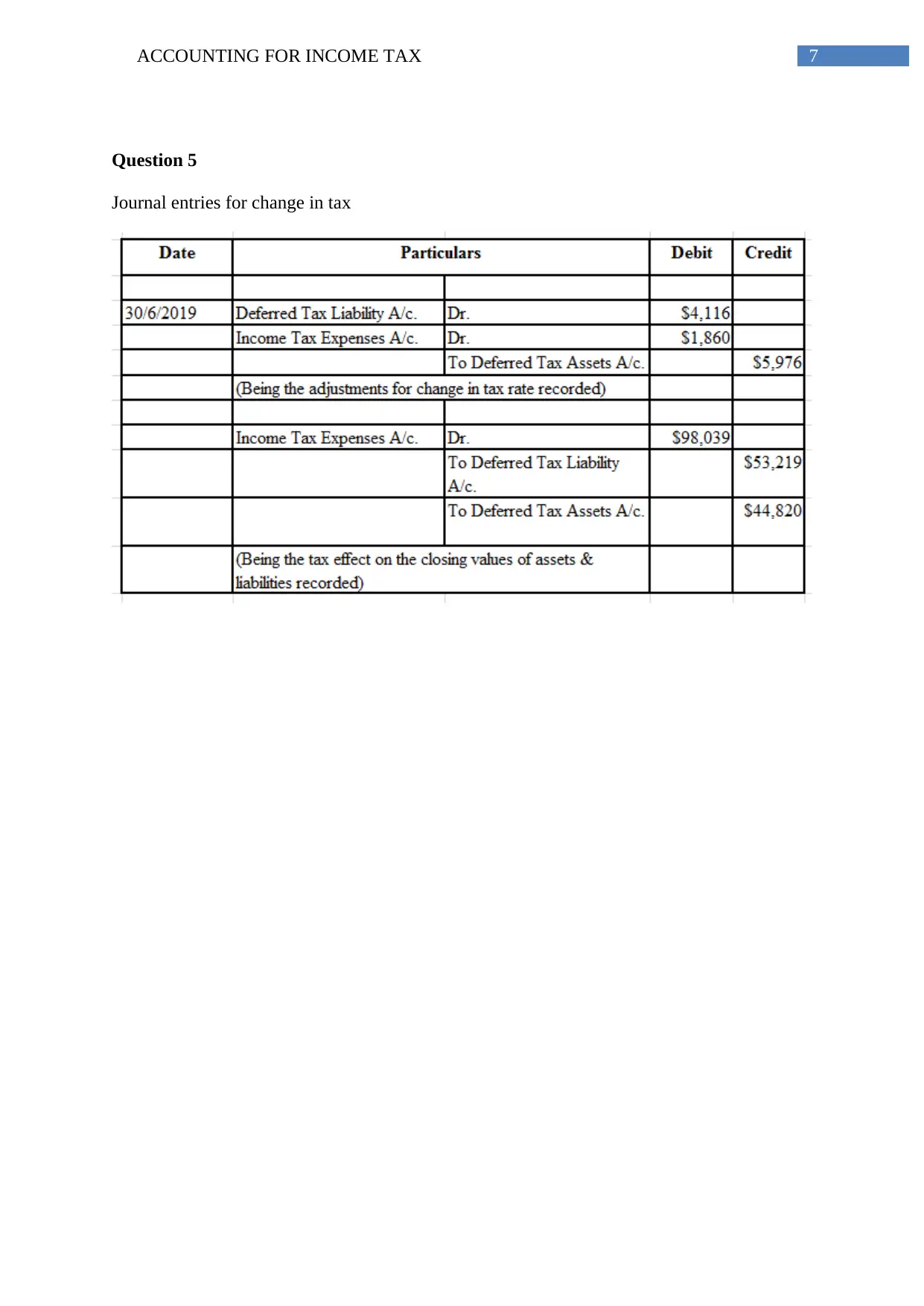

Homework Assignment

AI Summary

This assignment addresses the principles of accounting for income tax, focusing on Australian tax regulations. The solution begins by examining the treatment of various expenses like insurance and entertainment costs under current tax laws, including GST implications. It then presents a current tax worksheet detailing calculations to arrive at taxable income and current tax liability. The assignment includes journal entries for current tax and a comprehensive deferred tax worksheet, outlining temporary differences and the calculation of deferred tax assets and liabilities. Finally, the document provides journal entries related to changes in tax. The assignment covers key aspects of tax accounting, including the application of accounting principles to calculate income tax liabilities and assets.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.