Analyzing AASB 16's Effects on CSR Limited's Financial Performance

VerifiedAdded on 2023/06/03

|10

|2137

|338

Report

AI Summary

This report examines the impact of AASB 16 on CSR Limited, an ASX-listed Australian industrial firm. It analyzes the types of lease agreements used by CSR Limited, provides an overview of AASB 16 compared to AASB 117 from the lessee's perspective, and evaluates the impact of AASB 16 on the financial performance and position of the organization. The report also offers recommendations to assist CSR Limited in applying the new standard, highlighting potential changes in financial statements, management burden, and brand image. The analysis concludes that while the management burden may increase, CSR Limited can build a favorable brand image with stakeholders through proper implementation of AASB 16.

Running head: ACCOUNTING FOR LEASES

Accounting for Leases

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Leases

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR LEASES

Executive Summary:

The organisation selected for meeting the goal of this paper is CSR Limited, which is listed in

ASX having adequate compliance with IFRS and AASB standards. The financial statements of

CSR Limited would undergo various changes owing to the implementation of AASB 16. The

management of the organisation is required preparing the financial reports on balance sheet for

lease assets as well as lease liabilities and it is estimated that the amounts of both the items

would increase. However, the management burden could rise. Finally, it has been analysed that

CSR Limited would be able to form a favourable brand image in the eyes of its stakeholders.

Executive Summary:

The organisation selected for meeting the goal of this paper is CSR Limited, which is listed in

ASX having adequate compliance with IFRS and AASB standards. The financial statements of

CSR Limited would undergo various changes owing to the implementation of AASB 16. The

management of the organisation is required preparing the financial reports on balance sheet for

lease assets as well as lease liabilities and it is estimated that the amounts of both the items

would increase. However, the management burden could rise. Finally, it has been analysed that

CSR Limited would be able to form a favourable brand image in the eyes of its stakeholders.

2ACCOUNTING FOR LEASES

Table of Contents

Introduction:....................................................................................................................................3

a. Description of leases of CSR Limited and overview of the new rules, AASB 16:.....................3

b. Analysis of the potential effects of AASB 16 on financial position and performance of CSR

Limited:............................................................................................................................................4

c. Assessment of whether AASB 16/IFRS 16 improves financial reporting:..................................5

d. Conclusion and recommendations:..............................................................................................6

References:......................................................................................................................................7

Appendix:........................................................................................................................................9

Table of Contents

Introduction:....................................................................................................................................3

a. Description of leases of CSR Limited and overview of the new rules, AASB 16:.....................3

b. Analysis of the potential effects of AASB 16 on financial position and performance of CSR

Limited:............................................................................................................................................4

c. Assessment of whether AASB 16/IFRS 16 improves financial reporting:..................................5

d. Conclusion and recommendations:..............................................................................................6

References:......................................................................................................................................7

Appendix:........................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR LEASES

Introduction:

AASB 116 is a new lease standard issued and formulated by the “Australian Accounting

Standards Board (AASB)’ and it is necessary for all the Australian firms to adhere to this

standard initiating from the start of the year 2019. The company selected for meeting the goal of

this paper is CSR Limited, which is listed in ASX having adequate compliance with IFRS and

AASB standards. CSR Limited is one of the leading Australian industrial firms manufacturing

building products with an employee base of 3,600 (Csr.com.au 2018). The report would analyse

the different types of lease agreements used by CSR Limited along with an overview of AASB

16 compared to AASB 117 from lessee’s perspective. Moreover, AASB 16 would be evaluated

critically to find out its impact on the financial performance and position of the concerned

organisation. Lastly, this report would shed light on providing recommendations for exploring

the ways that would assist CSR Limited in applying this new standard.

a. Description of leases of CSR Limited and overview of the new rules, AASB 16:

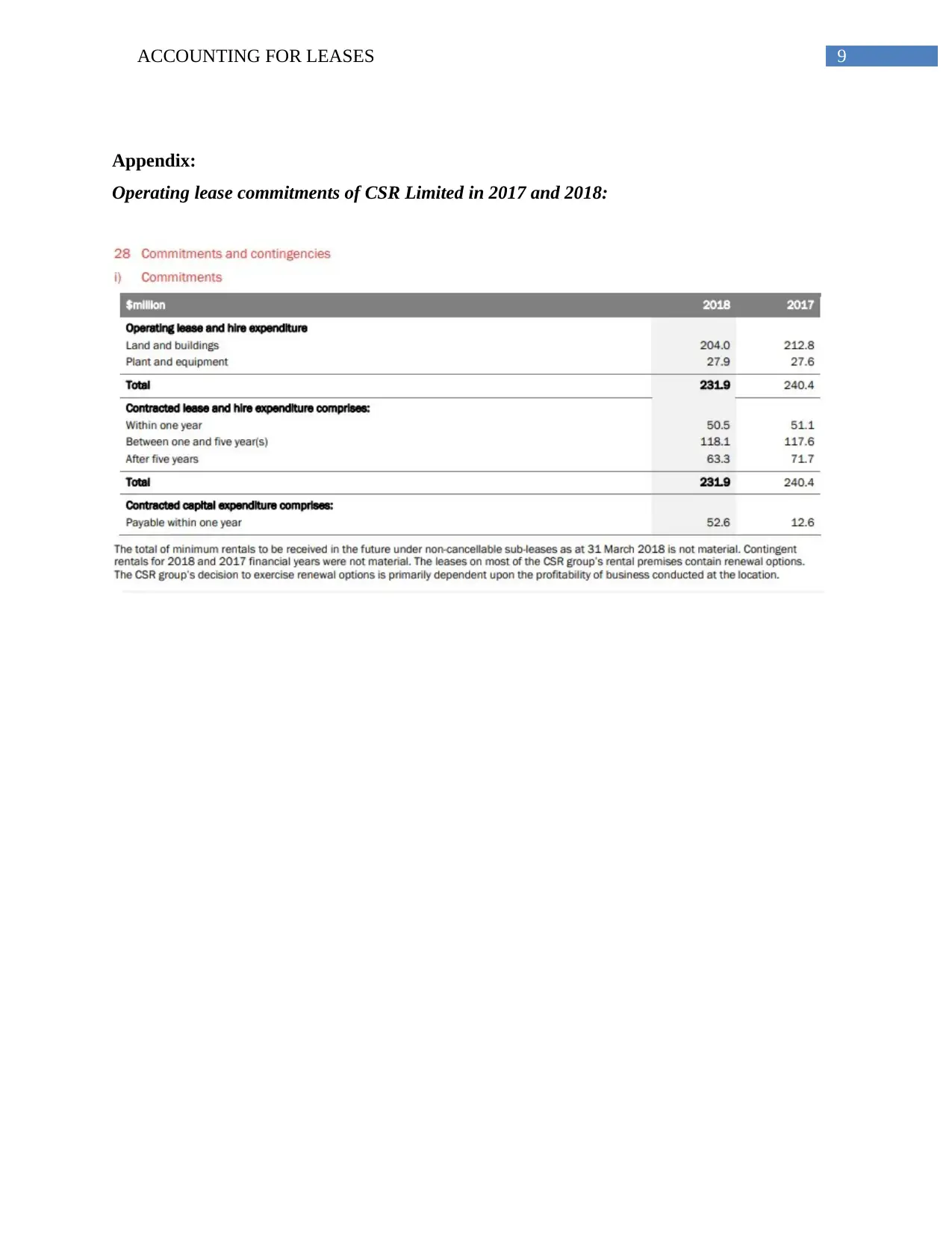

CSR Limited is observed to use a combination of finance lease and operating lease.

According to Dakis (2016), finance lease denotes a lease where risks and rewards are passed

over substantially incidental to the ownership of asset irrespective of the eventual transfer of the

asset title. In accordance with the 2018 annual report of CSR Limited, no evidence of finance

lease could be found, as it has settled its finance lease payments. Operating lease uses the

straight-line method to realise it in the form of an expense over the lease period. The operating

lease and hire expenditure commitments have been $231.9 million in 2018 compared to $240.4

million in 2017 (Csr.com.au 2018). Presently, CSR Limited is involved in utilising AASB 117 in

order to develop accounting for lease with no intention of changing the model. The reason is that

certain issues are inherent in AASB 16 along with increased cost and administrative

accountabilities on the management from which no benefit would be made (Henderson et al.

2015). The detailed picture of operating lease commitments of CSR Limited is represented in

Appendix.

All organisations need to identify each lease as operating lease or finance lease, as

mandatory under AASB 117 (Aasb.gov.au 2018). This creates a situation, in which the users

Introduction:

AASB 116 is a new lease standard issued and formulated by the “Australian Accounting

Standards Board (AASB)’ and it is necessary for all the Australian firms to adhere to this

standard initiating from the start of the year 2019. The company selected for meeting the goal of

this paper is CSR Limited, which is listed in ASX having adequate compliance with IFRS and

AASB standards. CSR Limited is one of the leading Australian industrial firms manufacturing

building products with an employee base of 3,600 (Csr.com.au 2018). The report would analyse

the different types of lease agreements used by CSR Limited along with an overview of AASB

16 compared to AASB 117 from lessee’s perspective. Moreover, AASB 16 would be evaluated

critically to find out its impact on the financial performance and position of the concerned

organisation. Lastly, this report would shed light on providing recommendations for exploring

the ways that would assist CSR Limited in applying this new standard.

a. Description of leases of CSR Limited and overview of the new rules, AASB 16:

CSR Limited is observed to use a combination of finance lease and operating lease.

According to Dakis (2016), finance lease denotes a lease where risks and rewards are passed

over substantially incidental to the ownership of asset irrespective of the eventual transfer of the

asset title. In accordance with the 2018 annual report of CSR Limited, no evidence of finance

lease could be found, as it has settled its finance lease payments. Operating lease uses the

straight-line method to realise it in the form of an expense over the lease period. The operating

lease and hire expenditure commitments have been $231.9 million in 2018 compared to $240.4

million in 2017 (Csr.com.au 2018). Presently, CSR Limited is involved in utilising AASB 117 in

order to develop accounting for lease with no intention of changing the model. The reason is that

certain issues are inherent in AASB 16 along with increased cost and administrative

accountabilities on the management from which no benefit would be made (Henderson et al.

2015). The detailed picture of operating lease commitments of CSR Limited is represented in

Appendix.

All organisations need to identify each lease as operating lease or finance lease, as

mandatory under AASB 117 (Aasb.gov.au 2018). This creates a situation, in which the users

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR LEASES

might be misguided while carrying out financial analysis of the organisation. Along with this,

this standard does not fulfil the user expectations, since it would provide a faithful depiction of

lease transactions. Since lease assets and lease liabilities are not appreciated on the balance sheet

statement owing to off-balance sheet leases, the accountants find it easy to hide and manipulate

financial information. This would assist in representing favourable financial condition of the

organisation in order to attract new investors for drawing adequate funds.

On the other hand, AASB would help in bringing certain changes that would reflect exact

representation of the financial position of the entity by applying on-balance sheet leases. The

realisation of lease assets and lease liabilities on the statement of financial position measured

initially utilising the present value of unavoidable future payments of leases, lease depreciation

and interest is to be represented on the income statement of the firm over the lease term

(Aasb.gov.au 2018). In addition, it is necessary to segregate the cash payment into a principal

amount based on the financial cash flows. Therefore, this new standard is bound to bring certain

changes in the financial statements of CSR Limited.

It is necessary for the lessees to reveal information by complying with AASB 16. When

the financial statements are prepared, the lessees are needed to use their own judgements. This

would help in segregating between the types of information required so that the goals of the

financial statement users could be fulfilled. Hence, the users could begin evaluating the effect of

lease on the financial reports of the organisation.

b. Analysis of the potential effects of AASB 16 on financial position and performance of

CSR Limited:

Effect on balance sheet statement:

The financial statements of CSR Limited would undergo various changes owing to the

implementation of AASB 16. The management of the organisation is required preparing the

financial reports on balance sheet for lease assets as well as lease liabilities and it is estimated

that the amounts of both the items would increase. The reason is that the recognition of assets,

which are not recognised previously, would raise the lease amount of the asset definitely and for

lease liabilities, the situation would be identical as well. In addition, AASB 16 does not segregate

might be misguided while carrying out financial analysis of the organisation. Along with this,

this standard does not fulfil the user expectations, since it would provide a faithful depiction of

lease transactions. Since lease assets and lease liabilities are not appreciated on the balance sheet

statement owing to off-balance sheet leases, the accountants find it easy to hide and manipulate

financial information. This would assist in representing favourable financial condition of the

organisation in order to attract new investors for drawing adequate funds.

On the other hand, AASB would help in bringing certain changes that would reflect exact

representation of the financial position of the entity by applying on-balance sheet leases. The

realisation of lease assets and lease liabilities on the statement of financial position measured

initially utilising the present value of unavoidable future payments of leases, lease depreciation

and interest is to be represented on the income statement of the firm over the lease term

(Aasb.gov.au 2018). In addition, it is necessary to segregate the cash payment into a principal

amount based on the financial cash flows. Therefore, this new standard is bound to bring certain

changes in the financial statements of CSR Limited.

It is necessary for the lessees to reveal information by complying with AASB 16. When

the financial statements are prepared, the lessees are needed to use their own judgements. This

would help in segregating between the types of information required so that the goals of the

financial statement users could be fulfilled. Hence, the users could begin evaluating the effect of

lease on the financial reports of the organisation.

b. Analysis of the potential effects of AASB 16 on financial position and performance of

CSR Limited:

Effect on balance sheet statement:

The financial statements of CSR Limited would undergo various changes owing to the

implementation of AASB 16. The management of the organisation is required preparing the

financial reports on balance sheet for lease assets as well as lease liabilities and it is estimated

that the amounts of both the items would increase. The reason is that the recognition of assets,

which are not recognised previously, would raise the lease amount of the asset definitely and for

lease liabilities, the situation would be identical as well. In addition, AASB 16 does not segregate

5ACCOUNTING FOR LEASES

lease assets and lease liabilities. Furthermore, the lessees could bring right-of-use asset and the

balance sheet statement would disclose lease liability in relation to all leases.

At present, CSR Limited has operating lease commitments valued $231.9 million

disclosed in its annual report and it is reported by fully conforming to AASB 117 guidelines.

Hence, the balance sheet statement of the organisation is not affected by this amount, since

income statement is used for adjusting lease-related transactions (Joubert, Garvie and Parle

2017). However, AASB 16 requires CSR Limited to capitalise operating lease commitments on

the statement of financial position of the firm. Another considerable effect would be inherent, in

which the liabilities and assets of the organisation would rise and the balance sheet statement

might reflect impact on covenants associated with debt-to-equity ratio.

Effect on the income statement:

The guidelines mentioned in AASB 16 would impact the income statement of CSR

Limited in the following ways:

Expense would be recognised belonging to portfolio lease and individual lease

Reflection of lease expense

Other effects

Since CSR Limited is deemed to contain off-balance sheet lease, this would lead to increase

in operating income of the organisation due to the implementation of AASB 16. The reason is

that when the standard is applied, the lease payment implicit interest would be represented for

the prior off-balance sheet lease as finance costs or interest expense (Tan‐Kantor, Abbott and

Jubb 2017). However, as per AASB 117, the off-balance sheet expenses are used to be included

as operating expense in the income statement. Hence, in accordance with AASB 16, the

operating margin ratio is estimated to rise, as operating income would increase significantly.

c. Assessment of whether AASB 16/IFRS 16 improves financial reporting:

By introducing AASB 16, all firms are required to include the cost of using lease assets

as well as balance sheet benefits. Therefore, correct representation of the financial position could

be disclosed because all liabilities are disclosed accordingly. With the help of such disclosures,

the investors could accumulate crucial information about the firms. In addition, the standard is

lease assets and lease liabilities. Furthermore, the lessees could bring right-of-use asset and the

balance sheet statement would disclose lease liability in relation to all leases.

At present, CSR Limited has operating lease commitments valued $231.9 million

disclosed in its annual report and it is reported by fully conforming to AASB 117 guidelines.

Hence, the balance sheet statement of the organisation is not affected by this amount, since

income statement is used for adjusting lease-related transactions (Joubert, Garvie and Parle

2017). However, AASB 16 requires CSR Limited to capitalise operating lease commitments on

the statement of financial position of the firm. Another considerable effect would be inherent, in

which the liabilities and assets of the organisation would rise and the balance sheet statement

might reflect impact on covenants associated with debt-to-equity ratio.

Effect on the income statement:

The guidelines mentioned in AASB 16 would impact the income statement of CSR

Limited in the following ways:

Expense would be recognised belonging to portfolio lease and individual lease

Reflection of lease expense

Other effects

Since CSR Limited is deemed to contain off-balance sheet lease, this would lead to increase

in operating income of the organisation due to the implementation of AASB 16. The reason is

that when the standard is applied, the lease payment implicit interest would be represented for

the prior off-balance sheet lease as finance costs or interest expense (Tan‐Kantor, Abbott and

Jubb 2017). However, as per AASB 117, the off-balance sheet expenses are used to be included

as operating expense in the income statement. Hence, in accordance with AASB 16, the

operating margin ratio is estimated to rise, as operating income would increase significantly.

c. Assessment of whether AASB 16/IFRS 16 improves financial reporting:

By introducing AASB 16, all firms are required to include the cost of using lease assets

as well as balance sheet benefits. Therefore, correct representation of the financial position could

be disclosed because all liabilities are disclosed accordingly. With the help of such disclosures,

the investors could accumulate crucial information about the firms. In addition, the standard is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR LEASES

estimated to raise integration among the various business departments related to lease contracts

(Wong and Joshi 2015). According to the GPFR objective, crucial information need to be

provided to the investors to assist in decision-making and this objective could be fulfilled with

the help of AASB 16, since it would disclose lease commitments appropriately to the investors.

In addition, the financial statements should be relevant and faithful, which are identified as two

qualitative characteristics of financial reporting. By including the relevant lease-related

information for the investors, the financial reporting quality could be improved. Furthermore,

CSR Limited could depict its lease commitments faithfully by using AASB 16 (Xu, Davidson

and Cheong 2017).

d. Conclusion and recommendations:

Based on the above discussion, some suggestions are provided to CSR Limited, which

would assist in preparation for adoption of AASB 16 and they are summarised as follows:

CSR Limited is required to gather available information so that the disclosure

requirements of the new standard could be met.

The existing systems of lease might not be able to collect the required data for the new

standard. Hence, a new system is to be in place so that the requirements of the new

standard could be fulfilled.

All the possible consequences are to be considered due to changes in balance sheet

statement and income statement such as modifications in significant ratios as well as

profits.

The leases and their associated terms and conditions are to be evaluated to obtain a closer

overview.

Hence, the new standard would result in significant change in the method of lease

accounting. However, the management burden could rise. Finally, it has been analysed that CSR

Limited would be able to form a favourable brand image in the eyes of its stakeholders.

estimated to raise integration among the various business departments related to lease contracts

(Wong and Joshi 2015). According to the GPFR objective, crucial information need to be

provided to the investors to assist in decision-making and this objective could be fulfilled with

the help of AASB 16, since it would disclose lease commitments appropriately to the investors.

In addition, the financial statements should be relevant and faithful, which are identified as two

qualitative characteristics of financial reporting. By including the relevant lease-related

information for the investors, the financial reporting quality could be improved. Furthermore,

CSR Limited could depict its lease commitments faithfully by using AASB 16 (Xu, Davidson

and Cheong 2017).

d. Conclusion and recommendations:

Based on the above discussion, some suggestions are provided to CSR Limited, which

would assist in preparation for adoption of AASB 16 and they are summarised as follows:

CSR Limited is required to gather available information so that the disclosure

requirements of the new standard could be met.

The existing systems of lease might not be able to collect the required data for the new

standard. Hence, a new system is to be in place so that the requirements of the new

standard could be fulfilled.

All the possible consequences are to be considered due to changes in balance sheet

statement and income statement such as modifications in significant ratios as well as

profits.

The leases and their associated terms and conditions are to be evaluated to obtain a closer

overview.

Hence, the new standard would result in significant change in the method of lease

accounting. However, the management burden could rise. Finally, it has been analysed that CSR

Limited would be able to form a favourable brand image in the eyes of its stakeholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR LEASES

References:

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf [Accessed 13 Oct.

2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 13 Oct. 2018].

Csr.com.au., 2018. About Us | CSR . [online] Available at: https://www.csr.com.au/about-us

[Accessed 13 Oct. 2018].

Csr.com.au., 2018. Annual Meetings and Reports. [online] Available at:

https://www.csr.com.au/investor-relations-and-news/annual-meetings-and-reports [Accessed 13

Oct. 2018].

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas & Trends, 15(2), pp.302-315.

Tan‐Kantor, A., Abbott, M. and Jubb, C., 2017. Accounting Choice and Theory in Crisis: The

Case of the Victorian Desalination Plant. Australian Accounting Review, 27(3), pp.273-284.

References:

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf [Accessed 13 Oct.

2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 13 Oct. 2018].

Csr.com.au., 2018. About Us | CSR . [online] Available at: https://www.csr.com.au/about-us

[Accessed 13 Oct. 2018].

Csr.com.au., 2018. Annual Meetings and Reports. [online] Available at:

https://www.csr.com.au/investor-relations-and-news/annual-meetings-and-reports [Accessed 13

Oct. 2018].

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas & Trends, 15(2), pp.302-315.

Tan‐Kantor, A., Abbott, M. and Jubb, C., 2017. Accounting Choice and Theory in Crisis: The

Case of the Victorian Desalination Plant. Australian Accounting Review, 27(3), pp.273-284.

8ACCOUNTING FOR LEASES

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating to

capitalised leases. Pacific Accounting Review, 29(1), pp.34-54.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating to

capitalised leases. Pacific Accounting Review, 29(1), pp.34-54.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR LEASES

Appendix:

Operating lease commitments of CSR Limited in 2017 and 2018:

Appendix:

Operating lease commitments of CSR Limited in 2017 and 2018:

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.