Accounting for Leases: Reviewing Financial Impacts and Regulations

VerifiedAdded on 2023/06/06

|9

|2179

|109

Essay

AI Summary

This essay provides a comprehensive overview of accounting for leases, distinguishing between financial and operating leases and examining their implications for financial reporting. It references articles by Ellwood and Newberry, as well as Jacobs and Jones, to highlight the importance of accounting standards and parliamentary oversight in Australia. The analysis covers the role of government in lease accounting, the impact on accountants in Australian companies concerning depreciation, interest expenses, and future lease payment liabilities, and the implications for accounting regulators in ensuring faithful presentation and preventing manipulation of leasing transactions. The essay concludes that accounting for leases is crucial for understanding the financial and economic value of a firm, affecting its auditing and financial activities and significantly impacting external stakeholders.

Accounting for Leases

Name:

Student ID.:

Date of submission:

Word count: 1500 words

0 | a g eP

Name:

Student ID.:

Date of submission:

Word count: 1500 words

0 | a g eP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

he lease is the process of contact that is provided by a party to the other party for utilizing theirT

asset in return of asset or money n the accounting process there is two type of leases and they. I ,

are operating along with the fi nancing lease within the fi eld he transfer of the risk along with the. T

reward of the asset within the market can be effectively needed to develop the operating lease that

is considered to be zero percent and the fi nance lease is considered to be the percent he100 . T

article of llwood and ewberry and the article of acobs and ones effectively provides the view onE N J J

the value of accounting system within the fi eld.

1 | a g eP

he lease is the process of contact that is provided by a party to the other party for utilizing theirT

asset in return of asset or money n the accounting process there is two type of leases and they. I ,

are operating along with the fi nancing lease within the fi eld he transfer of the risk along with the. T

reward of the asset within the market can be effectively needed to develop the operating lease that

is considered to be zero percent and the fi nance lease is considered to be the percent he100 . T

article of llwood and ewberry and the article of acobs and ones effectively provides the view onE N J J

the value of accounting system within the fi eld.

1 | a g eP

Table of Contents

ntroductionI ...................................................................................................................................................3

Main conte tx ...............................................................................................................................................3

Conclusion...................................................................................................................................................6

References...................................................................................................................................................7

2 | a g eP

ntroductionI ...................................................................................................................................................3

Main conte tx ...............................................................................................................................................3

Conclusion...................................................................................................................................................6

References...................................................................................................................................................7

2 | a g eP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ntroductionI

ease accounting is the process where the direct fi nancing lease along with the sales type lease isL - -

being recognized in the market he lease needs to be accounted for the development of the. T

process within the process to perform the direct fi nancing lease for the fi rm Acito ogan and- ( , H ,

Mergenthaler, 2017). he lease accounting is also required to provide effective view on theT

agreement that has been formed for the accounting process llwood and ewberry(E , N , 2007) he. T

primary purpose of the paper is to provide an effective view of the accounting for lease or. F

providing the clear view on the process two valuable article on the accounting for lease is being

selected hese article help to understand the process and the need for accounting within the fi rm. T

and also the value for the development of numerous actions in the fi eld of the fi nancial and

economic condition he paper also provides the view of the effective working process of the fi rm. T

within the market.

Main conte tx

eases are generally known as the contracts or the agreements which the asset owners allowL

other people to use their property in e change for other asset or money audot herex (B , 2014). T

is two type of lease that is a fi nancial lease and the operating lease n the fi nancial lease the risk. I ,

along with the reward inherent are transferred to the lessee n the other hand in the operating. O

lease the risk as well as the reward inherent are not being transferred he accounting for lease, , , . T

generally depends on the terms as well as the condition for the lease ackling owieson and(J , H ,

atoli he article that is being selected for understanding the accounting for lease are theN , 2012). T

article by llwood and ewberry on public sector accrual accounting and the second one is byE N

acobs and ones on the legitimacy and parliamentary oversight in Australia hese articles provideJ J . T

the effective view of the accounting for lease within the country.

he articles provide the clear view on the accounting for lease within the country and theT

importance for the system in the accounting process he article by llwood and ewberry clearly. T E N

provides the view on the purpose to understand regarding the role of the public sector accrual

or the agreement accounting for the implementation of the neoliberal form he article eventually. T

provides the view on the accounting process and provides the primary question regarding the

3 | a g eP

ease accounting is the process where the direct fi nancing lease along with the sales type lease isL - -

being recognized in the market he lease needs to be accounted for the development of the. T

process within the process to perform the direct fi nancing lease for the fi rm Acito ogan and- ( , H ,

Mergenthaler, 2017). he lease accounting is also required to provide effective view on theT

agreement that has been formed for the accounting process llwood and ewberry(E , N , 2007) he. T

primary purpose of the paper is to provide an effective view of the accounting for lease or. F

providing the clear view on the process two valuable article on the accounting for lease is being

selected hese article help to understand the process and the need for accounting within the fi rm. T

and also the value for the development of numerous actions in the fi eld of the fi nancial and

economic condition he paper also provides the view of the effective working process of the fi rm. T

within the market.

Main conte tx

eases are generally known as the contracts or the agreements which the asset owners allowL

other people to use their property in e change for other asset or money audot herex (B , 2014). T

is two type of lease that is a fi nancial lease and the operating lease n the fi nancial lease the risk. I ,

along with the reward inherent are transferred to the lessee n the other hand in the operating. O

lease the risk as well as the reward inherent are not being transferred he accounting for lease, , , . T

generally depends on the terms as well as the condition for the lease ackling owieson and(J , H ,

atoli he article that is being selected for understanding the accounting for lease are theN , 2012). T

article by llwood and ewberry on public sector accrual accounting and the second one is byE N

acobs and ones on the legitimacy and parliamentary oversight in Australia hese articles provideJ J . T

the effective view of the accounting for lease within the country.

he articles provide the clear view on the accounting for lease within the country and theT

importance for the system in the accounting process he article by llwood and ewberry clearly. T E N

provides the view on the purpose to understand regarding the role of the public sector accrual

or the agreement accounting for the implementation of the neoliberal form he article eventually. T

provides the view on the accounting process and provides the primary question regarding the

3 | a g eP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activity of the agreement for the accountants llwood and ewberry t is the primary(E , N , 2007). I

process for the development of numerous activity within the fi eld and also for the development of

valuable accounting form in the market Another article by acobs and ones provides the primary. J J

purpose of the research is to provide an effective understanding of the accounting legitimacy along

with the parliamentary activity in Australia t is highly essential for understanding the need for. I

appropriate accounting process within the fi eld for the betterment of working function within the

market acobs and ones t is the general fact where the accountant can effectively(J , J , 2009). I

perform their activity in term of the lease with the help of proper legitimacy along with the

parliamentary activity he primary concern of the project is to deliver valuable and suitable. T

concern for performing accounting for the leases process.

he similarities within both the article are that both of them provide an effective view of theT

accounting process and also the need of accounting for the lease or the agreement t can be seen. I

from both the article that the government plays the vital role in the development of accounting in

term of the lease within the fi eld his is the mere fact where the government performs their. T

activity and the trade liberalisation process within the fi eld he process for the accounting for lease. T

have a vital activity in the fi eld of auditing and accounting for delivering the effective knowledge on the

agreement process Duff he fi nancial lease along with the operating lease is also( , 2017). T

proclaimed within the article for gathering the information regarding the working function of these

process in the fi eld he accounting for leases directly implied action in the fi eld of accounting and. T

auditing.

he difference within both the article can be seen that there is a various gap within the fi nding ofT

the process he article by llwood and ewberry provides the view that the development of. T E N

accrual accounting the government role of procurer gets reduced n another article by acobs and. I J

ones it can be seen that the accounting generally focuses on the development process of a jointJ ,

committee of the public accounts oth the article has a different view on the accounting process for. B

the lease to maintain the activity in the accounting fi eld n the case of the lease it can be seen that. I ,

accounting help to understand the facts and the business process to maintain the activity

rvinen he fi nding is also effective for maintaining the view of the development of(Jä , 2016). T

4 | a g eP

process for the development of numerous activity within the fi eld and also for the development of

valuable accounting form in the market Another article by acobs and ones provides the primary. J J

purpose of the research is to provide an effective understanding of the accounting legitimacy along

with the parliamentary activity in Australia t is highly essential for understanding the need for. I

appropriate accounting process within the fi eld for the betterment of working function within the

market acobs and ones t is the general fact where the accountant can effectively(J , J , 2009). I

perform their activity in term of the lease with the help of proper legitimacy along with the

parliamentary activity he primary concern of the project is to deliver valuable and suitable. T

concern for performing accounting for the leases process.

he similarities within both the article are that both of them provide an effective view of theT

accounting process and also the need of accounting for the lease or the agreement t can be seen. I

from both the article that the government plays the vital role in the development of accounting in

term of the lease within the fi eld his is the mere fact where the government performs their. T

activity and the trade liberalisation process within the fi eld he process for the accounting for lease. T

have a vital activity in the fi eld of auditing and accounting for delivering the effective knowledge on the

agreement process Duff he fi nancial lease along with the operating lease is also( , 2017). T

proclaimed within the article for gathering the information regarding the working function of these

process in the fi eld he accounting for leases directly implied action in the fi eld of accounting and. T

auditing.

he difference within both the article can be seen that there is a various gap within the fi nding ofT

the process he article by llwood and ewberry provides the view that the development of. T E N

accrual accounting the government role of procurer gets reduced n another article by acobs and. I J

ones it can be seen that the accounting generally focuses on the development process of a jointJ ,

committee of the public accounts oth the article has a different view on the accounting process for. B

the lease to maintain the activity in the accounting fi eld n the case of the lease it can be seen that. I ,

accounting help to understand the facts and the business process to maintain the activity

rvinen he fi nding is also effective for maintaining the view of the development of(Jä , 2016). T

4 | a g eP

valuable process to maintain their activity with the help of legitimate purpose n the other hand. O ,

the article shows that neo liberal principles are having the effective view within the fi eld- .

he accounting for lease has the major implication on the accountants of the AustralianT

companies in various aspect t can be seen that companies are generally associated with. I

numerous leases or the agreement which needs effective accounting process for maintaining the

system in the market Accountant in this process help to develop the view and the various.

working function for the development of numerous documents regarding the cases oitash and(H ,

oitash he major implication that is being faced by the accountants in the fi eld ofH , 2017). T

accounting for leases is regarding the depreciation and the interest e pense Another implicationx .

for the accountants is the value that is being utilised for the future lease payment as the liability.

his is the primary activity that needs to be performed by the accountants of the AustralianT

companies to maintain the value of the fi rm he agreement needs to be adjusted with effective. T

accounting process to understand the e pense along with the income and the liabilities that arex

associated with the company imbar ansen and zlanski he implication clearly(G , H , O , 2016). T

provides the effective development process for the fi rm.

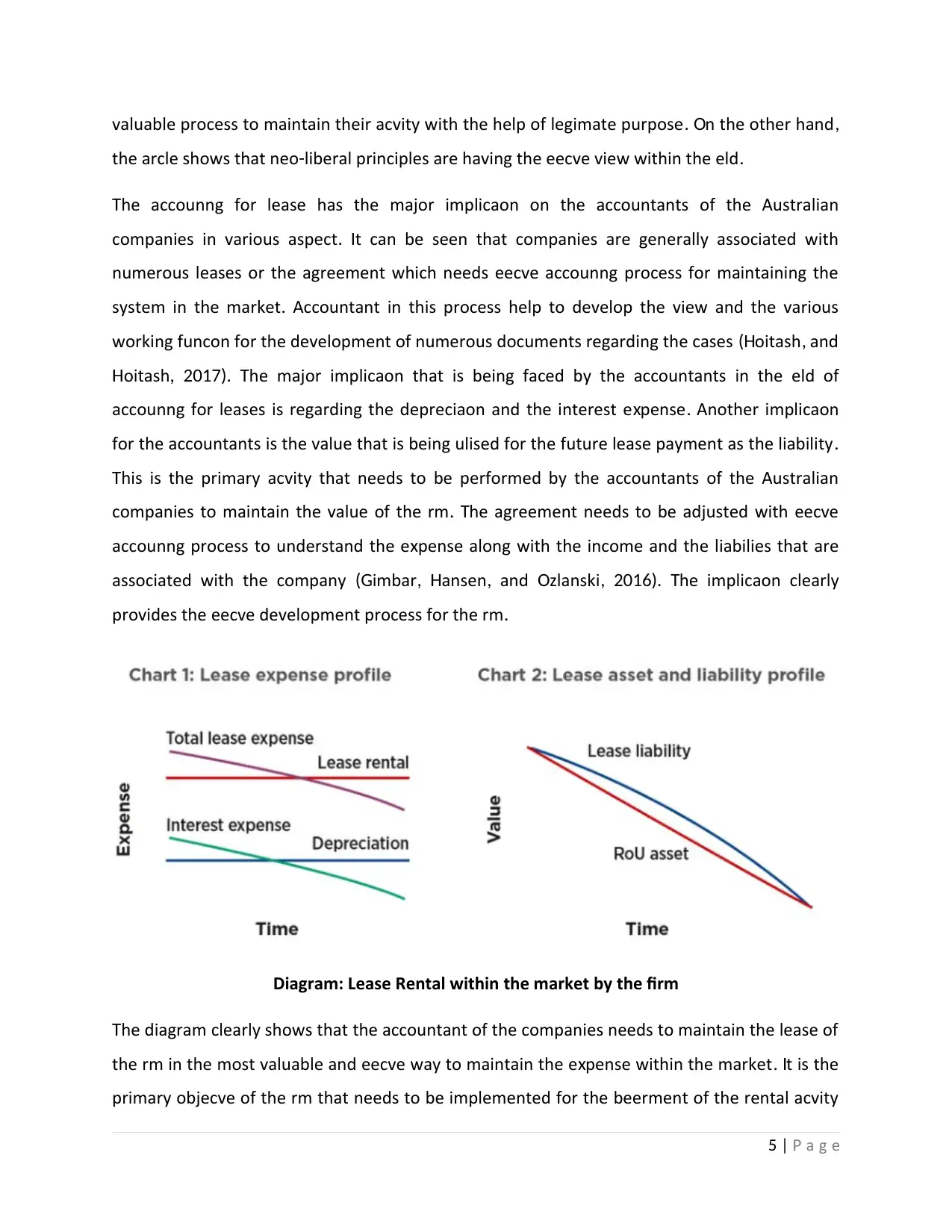

Diagram: Lease Rental within the market by the firm

he diagram clearly shows that the accountant of the companies needs to maintain the lease ofT

the fi rm in the most valuable and effective way to maintain the e pense within the market t is thex . I

primary objective of the fi rm that needs to be implemented for the betterment of the rental activity

5 | a g eP

the article shows that neo liberal principles are having the effective view within the fi eld- .

he accounting for lease has the major implication on the accountants of the AustralianT

companies in various aspect t can be seen that companies are generally associated with. I

numerous leases or the agreement which needs effective accounting process for maintaining the

system in the market Accountant in this process help to develop the view and the various.

working function for the development of numerous documents regarding the cases oitash and(H ,

oitash he major implication that is being faced by the accountants in the fi eld ofH , 2017). T

accounting for leases is regarding the depreciation and the interest e pense Another implicationx .

for the accountants is the value that is being utilised for the future lease payment as the liability.

his is the primary activity that needs to be performed by the accountants of the AustralianT

companies to maintain the value of the fi rm he agreement needs to be adjusted with effective. T

accounting process to understand the e pense along with the income and the liabilities that arex

associated with the company imbar ansen and zlanski he implication clearly(G , H , O , 2016). T

provides the effective development process for the fi rm.

Diagram: Lease Rental within the market by the firm

he diagram clearly shows that the accountant of the companies needs to maintain the lease ofT

the fi rm in the most valuable and effective way to maintain the e pense within the market t is thex . I

primary objective of the fi rm that needs to be implemented for the betterment of the rental activity

5 | a g eP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and the agreement performed by the organisation Robinson Stomberg and owery he( , , T , 2015). T

diagram effectively provides the view on lease rental as well as the depreciation of the fi rm within

the market t can be seen that the entire working function is being developed for the value of the. I

fi

rm.

Accounting regulators provide the effective view of the development process of accounting within

the fi eld an and ow Accounting for lease is the vital aspect for the accounting regulators(T , L , 2017).

and this has the huge implication on the process he two major implication of the accounting. T

regulator is the faithful presentation of the obligation arising from the leases or the agreements in

the fi eld Another implication is the decreasing opportunity for the fi rm to framework the leasing.

transaction in the market oth this effectively creates implication for the accounting process that is. B

being formed in the accounting system.

he fi nancial report is being used by the various stakeholder within the fi rm and it allows them toT

understand the business process and the development value of the fi rm within the market he. T

implication of the stakeholders regarding the accounting process within the fi rm to develop the

accounting report for the fi rm Abbott and an( , T ‐ antor he primary implication is on the yearK , 2018). T -

end balance sheet of the fi rm along with the fi nancial reporting for the fi rm t allows the. I

stakeholders to analyze the process and understand the fi nancial as well as the economic

condition of the fi rm in the market.

Conclusion

he paper eventually concludes the fact that the accounting for lease is the valuable process forT

developing the concept of fi nancial and the economic value of the fi rm he paper also concludes. T

the facts that the accounting process for the lease affect the auditing and the fi nancial activity of the

fi

rm within the market he paper also concludes that the accounting process for the lease or the. T

agreement has a great impact on the e ternal stakeholders of the fi rm to maintain their workingx

function in the market t is one of the most effective and the valuable process for building the. I

accounting report of the fi rm.

6 | a g eP

diagram effectively provides the view on lease rental as well as the depreciation of the fi rm within

the market t can be seen that the entire working function is being developed for the value of the. I

fi

rm.

Accounting regulators provide the effective view of the development process of accounting within

the fi eld an and ow Accounting for lease is the vital aspect for the accounting regulators(T , L , 2017).

and this has the huge implication on the process he two major implication of the accounting. T

regulator is the faithful presentation of the obligation arising from the leases or the agreements in

the fi eld Another implication is the decreasing opportunity for the fi rm to framework the leasing.

transaction in the market oth this effectively creates implication for the accounting process that is. B

being formed in the accounting system.

he fi nancial report is being used by the various stakeholder within the fi rm and it allows them toT

understand the business process and the development value of the fi rm within the market he. T

implication of the stakeholders regarding the accounting process within the fi rm to develop the

accounting report for the fi rm Abbott and an( , T ‐ antor he primary implication is on the yearK , 2018). T -

end balance sheet of the fi rm along with the fi nancial reporting for the fi rm t allows the. I

stakeholders to analyze the process and understand the fi nancial as well as the economic

condition of the fi rm in the market.

Conclusion

he paper eventually concludes the fact that the accounting for lease is the valuable process forT

developing the concept of fi nancial and the economic value of the fi rm he paper also concludes. T

the facts that the accounting process for the lease affect the auditing and the fi nancial activity of the

fi

rm within the market he paper also concludes that the accounting process for the lease or the. T

agreement has a great impact on the e ternal stakeholders of the fi rm to maintain their workingx

function in the market t is one of the most effective and the valuable process for building the. I

accounting report of the fi rm.

6 | a g eP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Abbott M and an, . T ‐ antor A air Value Measurement and Mandated Accounting ChangesK , ., 2018. F :

he Case of the Victorian Rail rack CorporationT T . ustralian ccounting evieA A R w, 28 pp(2), .266-278.

Acito A A ogan C and Mergenthaler R D he effects of CA inspections on, . ., H , .E. , . ., 2017. T P OB

auditor client relationships- . he ccounting evieT A R w, 93 pp(2), .1-35.

audot AA convergence or convergence ap unfolding ten years of accountingB , L., 2014. G P G :

change. ccounting uditing ccounta ility ournalA , A & A b J , 27 pp(6), .956-994.

Duff A Social mobility and air Access to the accountancy profession in the vidence, ., 2017. F UK: E

from ig our and mid ti er fi rmsB F - . ccounting uditing ccounta ility ournalA , A & A b J , 30 pp(5), .1082-1110.

llwood S and ewberry S ublic sector accrual accounting institutionalising neo liberalE , . N , ., 2007. P : -

principles?. ccounting uditing ccounta ility ournalA , A & A b J , 20 pp(4), .549-573.

imbar C ansen and zlanski M he effects of critical audit matter paragraphs andG , ., H , B. O , .E., 2016. T

accounting standard precision on auditor liability. he ccounting evieT A R w, 91 pp(6), .1629-1646.

oitash R and oitash Measuring accounting reporting comple ity with RH , . H , U., 2017. x XB L. heT

ccounting evieA R w, 93 pp(1), .259-287.

ackling owieson and atoli R Some implications of RS adoption for accountingJ , B., H , B. N , ., 2012. IF

education. ustralian ccounting evieA A R w, 22 pp(4), .331-340.

acobs and ones egitimacy and parliamentary oversight in Australia he rise andJ , K. J , K., 2009. L : T

fall of two public accounts committees. ccounting uditing ccounta ility ournalA , A & A b J , 22 pp(1), .13-

34.

rvinen Role of management accounting in applying new institutional logics AJä , J.T., 2016. :

comparative case study in the non profit sector- . ccounting uditing ccounta ility ournalA , A & A b J , 29(5),

pp.861-886.

7 | a g eP

Abbott M and an, . T ‐ antor A air Value Measurement and Mandated Accounting ChangesK , ., 2018. F :

he Case of the Victorian Rail rack CorporationT T . ustralian ccounting evieA A R w, 28 pp(2), .266-278.

Acito A A ogan C and Mergenthaler R D he effects of CA inspections on, . ., H , .E. , . ., 2017. T P OB

auditor client relationships- . he ccounting evieT A R w, 93 pp(2), .1-35.

audot AA convergence or convergence ap unfolding ten years of accountingB , L., 2014. G P G :

change. ccounting uditing ccounta ility ournalA , A & A b J , 27 pp(6), .956-994.

Duff A Social mobility and air Access to the accountancy profession in the vidence, ., 2017. F UK: E

from ig our and mid ti er fi rmsB F - . ccounting uditing ccounta ility ournalA , A & A b J , 30 pp(5), .1082-1110.

llwood S and ewberry S ublic sector accrual accounting institutionalising neo liberalE , . N , ., 2007. P : -

principles?. ccounting uditing ccounta ility ournalA , A & A b J , 20 pp(4), .549-573.

imbar C ansen and zlanski M he effects of critical audit matter paragraphs andG , ., H , B. O , .E., 2016. T

accounting standard precision on auditor liability. he ccounting evieT A R w, 91 pp(6), .1629-1646.

oitash R and oitash Measuring accounting reporting comple ity with RH , . H , U., 2017. x XB L. heT

ccounting evieA R w, 93 pp(1), .259-287.

ackling owieson and atoli R Some implications of RS adoption for accountingJ , B., H , B. N , ., 2012. IF

education. ustralian ccounting evieA A R w, 22 pp(4), .331-340.

acobs and ones egitimacy and parliamentary oversight in Australia he rise andJ , K. J , K., 2009. L : T

fall of two public accounts committees. ccounting uditing ccounta ility ournalA , A & A b J , 22 pp(1), .13-

34.

rvinen Role of management accounting in applying new institutional logics AJä , J.T., 2016. :

comparative case study in the non profit sector- . ccounting uditing ccounta ility ournalA , A & A b J , 29(5),

pp.861-886.

7 | a g eP

Robinson A Stomberg and owery M ne size does not fi t all ow the uniform, L. ., , B. T , E. ., 2015. O : H

rules of affect the relevance of income ta accountingFIN 48 x . he ccounting evieT A R w, 91(4),

pp.1195-1217.

an S and ow itcoin its economics for fi nancial reportingT , B. . L , K.Y., 2017. B – . ustralian ccountingA A

evieR w, 27 pp(2), .220-227.

8 | a g eP

rules of affect the relevance of income ta accountingFIN 48 x . he ccounting evieT A R w, 91(4),

pp.1195-1217.

an S and ow itcoin its economics for fi nancial reportingT , B. . L , K.Y., 2017. B – . ustralian ccountingA A

evieR w, 27 pp(2), .220-227.

8 | a g eP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.