Advanced Accounting: Impact of AASB (IFRS) 16 on Lease Accounting

VerifiedAdded on 2023/03/17

|14

|3397

|34

Essay

AI Summary

This essay examines the impact of the new lease accounting standard, AASB 16 (IFRS 16), on financial reporting, using JB HI-FI as a case study. The essay begins with an overview of the changes introduced by AASB 16, which eliminates the classification of leases as operating or financial leases and introduces a single lessee accounting model. It discusses the recognition of right-of-use assets and lease liabilities, the measurement of these items, and the disclosure requirements. The essay then provides background on JB HI-FI, detailing the company's lease arrangements and the accounting rules applied. It analyzes JB HI-FI's financial statements, including minimum lease payments, leasehold improvements, and lease provisions. The essay explains the accounting treatment of lease accruals and incentives, and the company's non-cancellable operating leases. The essay also touches upon the life cycle and stages in lease, and the short-term and long-term impacts of the new standard. It highlights how AASB 16 affects the financial statements, including debt ratios and profit calculations. Overall, the essay provides a comprehensive analysis of AASB 16 and its practical implications for companies like JB HI-FI.

Accounting for Leases – the impact of

AASB (IFRS) 16

AASB (IFRS) 16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

The present report is related with the new model of the Lease standard, AASB 16. Since the

existing lease standard does not fulfill the requirements of the users of financial report, therefore

the necessary changes in incorporated in the new model. This standard removes the requirement

of the classification of the lease as operating lease or the financial lease. Further, additional

disclosure requirement is also incorporated in the new accounting standard.

The present report is related with the new model of the Lease standard, AASB 16. Since the

existing lease standard does not fulfill the requirements of the users of financial report, therefore

the necessary changes in incorporated in the new model. This standard removes the requirement

of the classification of the lease as operating lease or the financial lease. Further, additional

disclosure requirement is also incorporated in the new accounting standard.

Table of Contents

Lease arrangement and its effect on the financial statement...........................................................4

Backgroud of the company..............................................................................................................6

Value of Lease and Accounting rules for lease applied by the company........................................6

Accounting Rules applied by the company.....................................................................................6

Lease Accruals.............................................................................................................................8

Lease incentives...........................................................................................................................8

Non-cancellable operating leases................................................................................................8

Life Cycle and stages in Lease........................................................................................................9

Lease arrangement and its effect on the financial statement...........................................................4

Backgroud of the company..............................................................................................................6

Value of Lease and Accounting rules for lease applied by the company........................................6

Accounting Rules applied by the company.....................................................................................6

Lease Accruals.............................................................................................................................8

Lease incentives...........................................................................................................................8

Non-cancellable operating leases................................................................................................8

Life Cycle and stages in Lease........................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LEASE ARRANGEMENT AND ITS EFFECT ON THE FINANCIAL

STATEMENT

For several business organizations, leasing is considered as a significant activity. As per the

earlier accounting standard, the lease is classified into two aspects, such as financial lease and

operating lease. This model does not meet the prescribed user requirement and proper

presentation of lease activity in the financial accounts of the company. Therefore a latest

accounting standard is approved by the government (Cheng, 2015).

Australian Accounting Standard 16 deals with the Leasing accounting of the entity. As per this

accounting standard, a person has not to classify the lease in the financial lease or an operating

lease. It is based on the exercise of the control and documented as a right to use assets and

corresponding liability. This new model introduces a single model of accounting for the lessee.

All assets and liabilities are recognized by the lessee with a period of exceeding twelve months

(Chatfield, Chatfield, & Poon, 2017). However, if it is a low value, then it should not be

recognized. Moreover, the right of use of assets is measured just as a measurement of non-

financial assets and liability of lease is the same as other non-financial liabilities. Initially, the

assets and liabilities arising from the lease are measured on the basis of present value. Further,

in the measurement of liabilities and assets, non-cancellable lease payments and payment made

by lessee for exercise the option of extension is also considered (Comiran, & Graham, 2016). In

addition, the new model also described the disclosure requirement for lessees. Application of the

judgment for determination of the requirement of the user of financial statement should be

applied by lessee so that user can get the actual and reliable financial data from the financial

STATEMENT

For several business organizations, leasing is considered as a significant activity. As per the

earlier accounting standard, the lease is classified into two aspects, such as financial lease and

operating lease. This model does not meet the prescribed user requirement and proper

presentation of lease activity in the financial accounts of the company. Therefore a latest

accounting standard is approved by the government (Cheng, 2015).

Australian Accounting Standard 16 deals with the Leasing accounting of the entity. As per this

accounting standard, a person has not to classify the lease in the financial lease or an operating

lease. It is based on the exercise of the control and documented as a right to use assets and

corresponding liability. This new model introduces a single model of accounting for the lessee.

All assets and liabilities are recognized by the lessee with a period of exceeding twelve months

(Chatfield, Chatfield, & Poon, 2017). However, if it is a low value, then it should not be

recognized. Moreover, the right of use of assets is measured just as a measurement of non-

financial assets and liability of lease is the same as other non-financial liabilities. Initially, the

assets and liabilities arising from the lease are measured on the basis of present value. Further,

in the measurement of liabilities and assets, non-cancellable lease payments and payment made

by lessee for exercise the option of extension is also considered (Comiran, & Graham, 2016). In

addition, the new model also described the disclosure requirement for lessees. Application of the

judgment for determination of the requirement of the user of financial statement should be

applied by lessee so that user can get the actual and reliable financial data from the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounts of the company. Although, the effective date for the new accounting standard is on or

after the 1 January 2019.

Prior to this accounting standard, the lease is classified as an operating lease or financial lease

based on the risk and reward (Warren, 2016). If the all significant risk and rewards associated

with the underlying assets is transfer, then in such case it is considered as a financial lease. On

the other hand, if significant risk and rewards connected with underlying assets are not

transferred, then it is considered as an operating lease. It is not required as per the new model of

an accounting standard.

As per AASB 16, in the beginning, the lessee has to recognize a right of use and liability of

lease. It should be recognized at cost (Fafatas, & Fischer, 2016). Further, the lease liability

recognized at the present value of unpaid lease payment. Subsequently, the lessee can apply the

cost model or another measurement model for the recognition of the right to use assets. As per

the cost model, the cost of the right of use should be deducted by depreciation and impairment

loss (if any). With the aspect of another measurement model, the lessee can apply the fair value

model, if the definition given under the AASB 140, Investment property is satisfied. In case of

lease liability, subsequently, it is measured by enhancing the carrying amount to show the

interest on the lease liability, or decreasing the carrying amount to show the lease payment incur.

Further, lease liability is re-measured in case of any reassessment or any modification in lease.

Further, in the notes to account, lessee, must disclose the right to use assets and lease distinctly

from other assets, and other liability respectively (Hunt, 2017).

after the 1 January 2019.

Prior to this accounting standard, the lease is classified as an operating lease or financial lease

based on the risk and reward (Warren, 2016). If the all significant risk and rewards associated

with the underlying assets is transfer, then in such case it is considered as a financial lease. On

the other hand, if significant risk and rewards connected with underlying assets are not

transferred, then it is considered as an operating lease. It is not required as per the new model of

an accounting standard.

As per AASB 16, in the beginning, the lessee has to recognize a right of use and liability of

lease. It should be recognized at cost (Fafatas, & Fischer, 2016). Further, the lease liability

recognized at the present value of unpaid lease payment. Subsequently, the lessee can apply the

cost model or another measurement model for the recognition of the right to use assets. As per

the cost model, the cost of the right of use should be deducted by depreciation and impairment

loss (if any). With the aspect of another measurement model, the lessee can apply the fair value

model, if the definition given under the AASB 140, Investment property is satisfied. In case of

lease liability, subsequently, it is measured by enhancing the carrying amount to show the

interest on the lease liability, or decreasing the carrying amount to show the lease payment incur.

Further, lease liability is re-measured in case of any reassessment or any modification in lease.

Further, in the notes to account, lessee, must disclose the right to use assets and lease distinctly

from other assets, and other liability respectively (Hunt, 2017).

BACKGROUD OF THE COMPANY

The present report is related to JB HI-FI, which was incorporated in 1974. This company has

opened its stores at many locations expanded its operations throughout the world. It is mainly

engaged in providing the services of Computers, Cameras, Car Sound, Home Theatre, Hi-Fi,

Speakers, and Televisions. Along with this, it also provides the excellent range of game, TV

shows, recorded music, at the lowest price.

VALUE OF LEASE AND ACCOUNTING RULES FOR LEASE APPLIED

BY THE COMPANY

As per the Annual Report of the year ended 2018, the Board of directors has stated that company

has a proprietorship interest in shopping centres in each of the GPT Wholesale Shopping Centre

Fund, Vicinity Limited and Kiwi Property Group Limited, in which the company presently

leases stores. The company has documented in the profit and loss account of the year ended

2018, Minimum Lease payment of $193.1Million, it is in relation to the operating lease. Further,

the leasehold improvement in the Plant and equipment is realized by the company at the cost of $

188.1 Million, and depreciation is charged with $ 130.2 Million, and by this NetBook Amount of

$ 57.9 is reported in the financial statement.

ACCOUNTING RULES APPLIED BY THE COMPANY

Leasehold Improvement is stated in the financial statement by deduction of depreciation and

impairment loss from the cost of assets. Cost of the asset included any costs which are directly

connected with the acquisition of assets (Paik, van der Laan Smith, Lee, & Yoon, 2015).

Company has charged the depreciation on leasehold improvements. Further, it has applied the

The present report is related to JB HI-FI, which was incorporated in 1974. This company has

opened its stores at many locations expanded its operations throughout the world. It is mainly

engaged in providing the services of Computers, Cameras, Car Sound, Home Theatre, Hi-Fi,

Speakers, and Televisions. Along with this, it also provides the excellent range of game, TV

shows, recorded music, at the lowest price.

VALUE OF LEASE AND ACCOUNTING RULES FOR LEASE APPLIED

BY THE COMPANY

As per the Annual Report of the year ended 2018, the Board of directors has stated that company

has a proprietorship interest in shopping centres in each of the GPT Wholesale Shopping Centre

Fund, Vicinity Limited and Kiwi Property Group Limited, in which the company presently

leases stores. The company has documented in the profit and loss account of the year ended

2018, Minimum Lease payment of $193.1Million, it is in relation to the operating lease. Further,

the leasehold improvement in the Plant and equipment is realized by the company at the cost of $

188.1 Million, and depreciation is charged with $ 130.2 Million, and by this NetBook Amount of

$ 57.9 is reported in the financial statement.

ACCOUNTING RULES APPLIED BY THE COMPANY

Leasehold Improvement is stated in the financial statement by deduction of depreciation and

impairment loss from the cost of assets. Cost of the asset included any costs which are directly

connected with the acquisition of assets (Paik, van der Laan Smith, Lee, & Yoon, 2015).

Company has charged the depreciation on leasehold improvements. Further, it has applied the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

straight-line method for charging the depreciation, and the estimated life is used in the

computation of depreciation is 1 to 15 years. Moreover, any circumstance which gives any

indication regarding the non-recovery of carrying amount, then the company tested the leasehold

improvement for the impairment purpose. As per the Australian Accounting standard, an

impairment loss is recognized by the company if carrying amount of assets is more than its

recoverable amount (Osei, 2017).

Moreover, the company has realized the Lease provision in its current liabilities of $ 83.5

Million, and non-current liability of Lease provision of $ 5.2 Million. The provision is recorded

by the company if there is a current obligation either lawfully or constructive as an outcome of

the past events. Further, it is likely that the company will require settling the provision and a

reliable assumption of the amount incurred for settlement of liability can be made. The amount

of provision is determined on the basis of amounts which are required to settle the present

obligation at the date of reporting (Hussan, &Sulaiman, 2016). It considers the risk and

uncertainties connected with the obligations. The provision of the Lease consists of the best

estimate of Company related with the amount needed to return the leased property of Group to

their original condition, by considering the past history of the Group of vacating premises and

the best estimate of the group related with onerous lease obligations.

Further, in the other Liabilities of the company, it has realized the Lease accrual liability of $ 2.8

Million and leases incentives of $ 5.2 Million in current liability sections. Further, in the non-

current liability, the company has realized Lease accrual of $ 15 Million and Lease incentives of

$ 20.6 Million.

computation of depreciation is 1 to 15 years. Moreover, any circumstance which gives any

indication regarding the non-recovery of carrying amount, then the company tested the leasehold

improvement for the impairment purpose. As per the Australian Accounting standard, an

impairment loss is recognized by the company if carrying amount of assets is more than its

recoverable amount (Osei, 2017).

Moreover, the company has realized the Lease provision in its current liabilities of $ 83.5

Million, and non-current liability of Lease provision of $ 5.2 Million. The provision is recorded

by the company if there is a current obligation either lawfully or constructive as an outcome of

the past events. Further, it is likely that the company will require settling the provision and a

reliable assumption of the amount incurred for settlement of liability can be made. The amount

of provision is determined on the basis of amounts which are required to settle the present

obligation at the date of reporting (Hussan, &Sulaiman, 2016). It considers the risk and

uncertainties connected with the obligations. The provision of the Lease consists of the best

estimate of Company related with the amount needed to return the leased property of Group to

their original condition, by considering the past history of the Group of vacating premises and

the best estimate of the group related with onerous lease obligations.

Further, in the other Liabilities of the company, it has realized the Lease accrual liability of $ 2.8

Million and leases incentives of $ 5.2 Million in current liability sections. Further, in the non-

current liability, the company has realized Lease accrual of $ 15 Million and Lease incentives of

$ 20.6 Million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lease Accruals

If the major risk and rewards connected with the underlying assets are not transferred to the

company as the lessee are classified it as an operating Lease (James, 2016). Therefore, it can be

said that the company has adopted the classification of Lease as per the prescribed definition

criteria are given under the Australian Accounting standard. Payments made in connection with

the operating lease are recognized in the profit or loss statement of the financial accounts

(Joubert, Garvie, & Parle, 2017). However, if lessor provides any incentive related to this, then it

is not separately shown and recognized net of any incentive received by Lessor. Over the term

of lease period by the application of a straight-line basis, the payments are documented.

Differences in the expenses incurred and the payment made are represented by the Lease

accruals (Nuryani, Heng, &Juliesta, 2015).

Lease incentives

If the lease incentives are obtained for the entering into the operating lease, then Incentives are

recognized as liability. On the basis of the period of lease term, the total benefits of incentives

are recognized as a deduction of rental expenses. For this, the straight-line method is applied

(Wong, & Joshi, 2015).

Non-cancellable operating leases

The company has come into the operating lease arrangement in connection with its stores.

Further, in connection with its plant and equipment, it has entered into some minor operating

leases. Generally, the store's leases have a time period of five to fifteen years; however, the

company has an option to extend the term period in some exceptional cases. If the company

implement the option to extend the term, then operating lease contract possess the market review

If the major risk and rewards connected with the underlying assets are not transferred to the

company as the lessee are classified it as an operating Lease (James, 2016). Therefore, it can be

said that the company has adopted the classification of Lease as per the prescribed definition

criteria are given under the Australian Accounting standard. Payments made in connection with

the operating lease are recognized in the profit or loss statement of the financial accounts

(Joubert, Garvie, & Parle, 2017). However, if lessor provides any incentive related to this, then it

is not separately shown and recognized net of any incentive received by Lessor. Over the term

of lease period by the application of a straight-line basis, the payments are documented.

Differences in the expenses incurred and the payment made are represented by the Lease

accruals (Nuryani, Heng, &Juliesta, 2015).

Lease incentives

If the lease incentives are obtained for the entering into the operating lease, then Incentives are

recognized as liability. On the basis of the period of lease term, the total benefits of incentives

are recognized as a deduction of rental expenses. For this, the straight-line method is applied

(Wong, & Joshi, 2015).

Non-cancellable operating leases

The company has come into the operating lease arrangement in connection with its stores.

Further, in connection with its plant and equipment, it has entered into some minor operating

leases. Generally, the store's leases have a time period of five to fifteen years; however, the

company has an option to extend the term period in some exceptional cases. If the company

implement the option to extend the term, then operating lease contract possess the market review

clause. Moreover, after the expiry of the term period of the lease, there is no option available to

the company to buy the leased assets (Strauss, 2018).

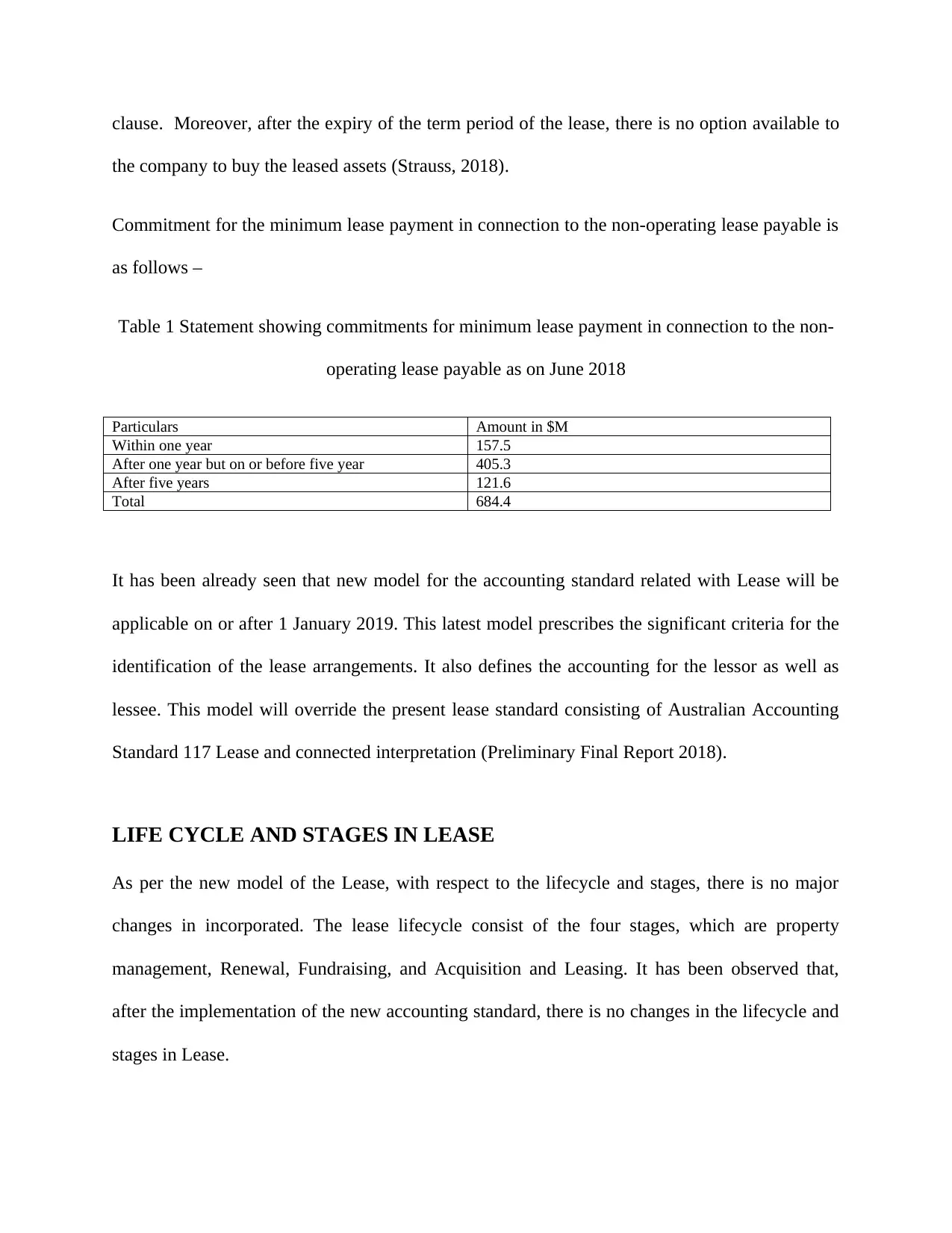

Commitment for the minimum lease payment in connection to the non-operating lease payable is

as follows –

Table 1 Statement showing commitments for minimum lease payment in connection to the non-

operating lease payable as on June 2018

Particulars Amount in $M

Within one year 157.5

After one year but on or before five year 405.3

After five years 121.6

Total 684.4

It has been already seen that new model for the accounting standard related with Lease will be

applicable on or after 1 January 2019. This latest model prescribes the significant criteria for the

identification of the lease arrangements. It also defines the accounting for the lessor as well as

lessee. This model will override the present lease standard consisting of Australian Accounting

Standard 117 Lease and connected interpretation (Preliminary Final Report 2018).

LIFE CYCLE AND STAGES IN LEASE

As per the new model of the Lease, with respect to the lifecycle and stages, there is no major

changes in incorporated. The lease lifecycle consist of the four stages, which are property

management, Renewal, Fundraising, and Acquisition and Leasing. It has been observed that,

after the implementation of the new accounting standard, there is no changes in the lifecycle and

stages in Lease.

the company to buy the leased assets (Strauss, 2018).

Commitment for the minimum lease payment in connection to the non-operating lease payable is

as follows –

Table 1 Statement showing commitments for minimum lease payment in connection to the non-

operating lease payable as on June 2018

Particulars Amount in $M

Within one year 157.5

After one year but on or before five year 405.3

After five years 121.6

Total 684.4

It has been already seen that new model for the accounting standard related with Lease will be

applicable on or after 1 January 2019. This latest model prescribes the significant criteria for the

identification of the lease arrangements. It also defines the accounting for the lessor as well as

lessee. This model will override the present lease standard consisting of Australian Accounting

Standard 117 Lease and connected interpretation (Preliminary Final Report 2018).

LIFE CYCLE AND STAGES IN LEASE

As per the new model of the Lease, with respect to the lifecycle and stages, there is no major

changes in incorporated. The lease lifecycle consist of the four stages, which are property

management, Renewal, Fundraising, and Acquisition and Leasing. It has been observed that,

after the implementation of the new accounting standard, there is no changes in the lifecycle and

stages in Lease.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Short Term and Long Term Impact

On the basis of implementation of the control exercised by the customer, this new standard

makes the differentiation in the lease and service contract on the identified assets (Folsom,

Hribar, Mergenthaler, & Peterson, 2016). The differences in the operating lease and the financial

lease have been removed from this standard. In the case of the lessee, for all leases, on the basis

of the right of use asset is recognized and a corresponding liability is recognized. It is not

applicable in the short term leases and the leases that have a minimum amount (Giner, &Pardo,

2017). Since, in the financial statement, the debt position will rise, therefore the Net Geraing to

Debt Ratio of the company will increase. Along with this, profits before interest, tax, and

depreciation will increase because the operating expenses will not considered in the profit and

loss account as per the new accounting standard.

As per the new standard, initially, right of use is recognized on the basis of cost, and after this, it

is recognized on the basis of cost less accumulated depreciation and impairment loss (if any).

For the reassessment of the liability of lease, it is further adjusted (Nichols, 2017). With the

aspect of ease liability, initially, it is recognized at the present value of the lease payments, which

are not paid up to this date. After this, the liability of lease is adjusted for the lease payment and

interest, along with the adjustment of effect of lease modification.

The new criteria of recognition of the right to use assets and its corresponding liability will make

a major effect on the amount recognized in the consolidated financial statement of the company.

Further, the classification of the cash flows of the company will also be impacted by the new

accounting standard. as in the old accounting standard payment made in relation with the

operating leases are shown as operating cash flows, on the other hand, as per AASB 16, lease

On the basis of implementation of the control exercised by the customer, this new standard

makes the differentiation in the lease and service contract on the identified assets (Folsom,

Hribar, Mergenthaler, & Peterson, 2016). The differences in the operating lease and the financial

lease have been removed from this standard. In the case of the lessee, for all leases, on the basis

of the right of use asset is recognized and a corresponding liability is recognized. It is not

applicable in the short term leases and the leases that have a minimum amount (Giner, &Pardo,

2017). Since, in the financial statement, the debt position will rise, therefore the Net Geraing to

Debt Ratio of the company will increase. Along with this, profits before interest, tax, and

depreciation will increase because the operating expenses will not considered in the profit and

loss account as per the new accounting standard.

As per the new standard, initially, right of use is recognized on the basis of cost, and after this, it

is recognized on the basis of cost less accumulated depreciation and impairment loss (if any).

For the reassessment of the liability of lease, it is further adjusted (Nichols, 2017). With the

aspect of ease liability, initially, it is recognized at the present value of the lease payments, which

are not paid up to this date. After this, the liability of lease is adjusted for the lease payment and

interest, along with the adjustment of effect of lease modification.

The new criteria of recognition of the right to use assets and its corresponding liability will make

a major effect on the amount recognized in the consolidated financial statement of the company.

Further, the classification of the cash flows of the company will also be impacted by the new

accounting standard. as in the old accounting standard payment made in relation with the

operating leases are shown as operating cash flows, on the other hand, as per AASB 16, lease

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payment should be bifurcated into the principal and the interest portion, which will be shown as

separately in the heading of operating cash flows and financing cash flows separately. In

addition, major disclosures are also required as per AASB 16.

In the financial report of JB – Hi-Fi Limited, year ended 2018; the company has reported that,

during this year, application of the latest accounting standard has been initiated in the number of

manners, which are described as below –

Assessment of leases and contract that could be included in the lease.

Collection of data related to a lease for the computation of impact assessment.

Complex areas and judgments have been identified.

For determination of discounts rates, initial estimates are made.

Identification of essential changes to the system and process needed to enable reporting

and accounting as per the new accounting standard.

At the end of 30 June 2018, the company has non-cancellable operating lease commitments of

amount $ 684.4 Million (Preliminary Final Report 2018). There is no requirement of recognition

of the right of use and corresponding liability as per the AASB 117. As per the preliminary

assessment, it has been identified that this arrangement will satisfy the definition of the lease as

per the AASB 16, and therefore the company will realize the right of use and corresponding

liability in relation withal these leases except if they are short term leases or low-value amount.

separately in the heading of operating cash flows and financing cash flows separately. In

addition, major disclosures are also required as per AASB 16.

In the financial report of JB – Hi-Fi Limited, year ended 2018; the company has reported that,

during this year, application of the latest accounting standard has been initiated in the number of

manners, which are described as below –

Assessment of leases and contract that could be included in the lease.

Collection of data related to a lease for the computation of impact assessment.

Complex areas and judgments have been identified.

For determination of discounts rates, initial estimates are made.

Identification of essential changes to the system and process needed to enable reporting

and accounting as per the new accounting standard.

At the end of 30 June 2018, the company has non-cancellable operating lease commitments of

amount $ 684.4 Million (Preliminary Final Report 2018). There is no requirement of recognition

of the right of use and corresponding liability as per the AASB 117. As per the preliminary

assessment, it has been identified that this arrangement will satisfy the definition of the lease as

per the AASB 16, and therefore the company will realize the right of use and corresponding

liability in relation withal these leases except if they are short term leases or low-value amount.

References

Books and Journals

Chatfield, H. K., Chatfield, R. E., & Poon, P. (2017). Is the Hospitality Industry Ready for the

New Lease Accounting Standards?. The Journal of Hospitality Financial

Management, 25(2), 101-111.

Cheng, J. (2015). Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting. Technology and Investment, 6(01), 71.

Comiran, F., & Graham, C. M. (2016). Comment letter activity: A response to proposed changes

in lease accounting. Research in Accounting Regulation, 28(2), 109-117.

Fafatas, S., & Fischer, D. (2016). The Effect of the New Lease Accounting Rules on Profitability

Analysis in the Retail Industry. Journal of Corporate Accounting & Finance, 28(1), 19-31.

Folsom, D., Hribar, P., Mergenthaler, R. D., & Peterson, K. (2016). Principles-based standards

and earnings attributes. Management Science, 63(8), 2592-2615.

Giner, B., &Pardo, F. (2017).Operating lease decision and the impact of capitalization in a bank-

oriented country. Applied Economics, 49(19), 1886-1900.

Hunt, K. G. (2017). BALANCING ACT: HOW THE FASB'S NEW LEASE ACCOUNTING

STANDARD COULD AFFECT BUSINESS PRACTICES. Journal of Property

Management, 82(6), 32-36.

Books and Journals

Chatfield, H. K., Chatfield, R. E., & Poon, P. (2017). Is the Hospitality Industry Ready for the

New Lease Accounting Standards?. The Journal of Hospitality Financial

Management, 25(2), 101-111.

Cheng, J. (2015). Small and Medium Sized Entities Management’s Perspective on Principles-

Based Accounting Standards on Lease Accounting. Technology and Investment, 6(01), 71.

Comiran, F., & Graham, C. M. (2016). Comment letter activity: A response to proposed changes

in lease accounting. Research in Accounting Regulation, 28(2), 109-117.

Fafatas, S., & Fischer, D. (2016). The Effect of the New Lease Accounting Rules on Profitability

Analysis in the Retail Industry. Journal of Corporate Accounting & Finance, 28(1), 19-31.

Folsom, D., Hribar, P., Mergenthaler, R. D., & Peterson, K. (2016). Principles-based standards

and earnings attributes. Management Science, 63(8), 2592-2615.

Giner, B., &Pardo, F. (2017).Operating lease decision and the impact of capitalization in a bank-

oriented country. Applied Economics, 49(19), 1886-1900.

Hunt, K. G. (2017). BALANCING ACT: HOW THE FASB'S NEW LEASE ACCOUNTING

STANDARD COULD AFFECT BUSINESS PRACTICES. Journal of Property

Management, 82(6), 32-36.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.