CO5123 Assignment: Analysis of AASB (IFRS 16) and Lease Accounting

VerifiedAdded on 2023/01/17

|8

|2957

|94

Essay

AI Summary

This essay delves into the implications of the new accounting standard for leases, AASB (IFRS) 16, examining its impact on companies and their financial performance. The paper focuses on the elimination of the distinction between financing and operating leases, leading to increased financial liabilities and changes in key financial metrics. The analysis uses JB Hi-Fi, an Australian home entertainment retailer, as a case study. The discussion covers the implementation of AASB 16, including the recognition of lease liabilities and right-of-use assets, and the impact on cash flows. The essay highlights the challenges in data collection, discount rate refinement, and transition methods. It also explores the effects on financial ratios, such as debt-to-equity and return on assets, and discusses the impact on the retail industry, including the importance of renewal options and potential business impacts like share-based payments and debt covenants. The essay concludes that the new standard enhances financial statement transparency but may negatively affect certain key ratios.

Running head: ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Accounting for leases- The impact of AASB (IFRS 16)

Name of the student

Name of the university

Student ID

Author note

Accounting for leases- The impact of AASB (IFRS 16)

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Introduction:

The current paper elucidates the understanding of the new accounting standard for

lease and examines the impact of the new lease standard on the company and its financial

performance. The new lease standard is introduced to essentially eliminate the accounting

distinction between financing and operating lease. With this, there will be increased financial

liabilities sans leased assets on the balance sheet of lessee. Accordingly, there will be

significant impacts on the key financial metrics for the companies having material off balance

sheet lease commitments. Although, there will not be any increase in the value of equity,

there will be increase in the enterprise value of the companies. For the analysis purpose, one

of the companies has been chosen from the ASX named JB Hi-Fi which is the largest home

entertainment retailer based in Australia. The company is engaged in selling wide variety of

entertainment products such as mobile phones, wireless speakers, headphones, and laptop and

game consoles.

Discussion:

The new accounting standard on lease has come in effect for the period beginning

after 1st January or on the given date. JB Hi-Fi has pointed out their annual report published

for the year ending 30th June, 2018 that the AASB 16 will be effective in the financial

statement of the group for the year ending June 30, 2020 (jbhifi.com.au 2019). A

comprehensive model has been introduced by AASB 16 for the identifying the lease

arrangements and accounting treatment for both lessees and lessors. The current guidance on

lease will be superseded by AASB 16 along with all the related interpretations. The

distinction between the service and lease contracts is created by AASB 16 on the basis of

whether the customer controls the identified assets. In addition to this, the lease accounting

does not identify differences between the operating and financing lease. A model under the

new lease standard has replaced the existing model and the new model where the recognition

for the corresponding liability and right for used assets for all the leases have to be

recognized by lessees on their balance sheet. However, such recognition will not include

leases for low value and short term leases. For the remeasuremnt of lease liability, the

measurement of the right of use assets is done at cost and subsequently, the measurement is

done at the cost less impairment losses and accumulated depreciation. At the initial level, the

leased liabilities are measured at the value of lease payments that are not being paid at the

Introduction:

The current paper elucidates the understanding of the new accounting standard for

lease and examines the impact of the new lease standard on the company and its financial

performance. The new lease standard is introduced to essentially eliminate the accounting

distinction between financing and operating lease. With this, there will be increased financial

liabilities sans leased assets on the balance sheet of lessee. Accordingly, there will be

significant impacts on the key financial metrics for the companies having material off balance

sheet lease commitments. Although, there will not be any increase in the value of equity,

there will be increase in the enterprise value of the companies. For the analysis purpose, one

of the companies has been chosen from the ASX named JB Hi-Fi which is the largest home

entertainment retailer based in Australia. The company is engaged in selling wide variety of

entertainment products such as mobile phones, wireless speakers, headphones, and laptop and

game consoles.

Discussion:

The new accounting standard on lease has come in effect for the period beginning

after 1st January or on the given date. JB Hi-Fi has pointed out their annual report published

for the year ending 30th June, 2018 that the AASB 16 will be effective in the financial

statement of the group for the year ending June 30, 2020 (jbhifi.com.au 2019). A

comprehensive model has been introduced by AASB 16 for the identifying the lease

arrangements and accounting treatment for both lessees and lessors. The current guidance on

lease will be superseded by AASB 16 along with all the related interpretations. The

distinction between the service and lease contracts is created by AASB 16 on the basis of

whether the customer controls the identified assets. In addition to this, the lease accounting

does not identify differences between the operating and financing lease. A model under the

new lease standard has replaced the existing model and the new model where the recognition

for the corresponding liability and right for used assets for all the leases have to be

recognized by lessees on their balance sheet. However, such recognition will not include

leases for low value and short term leases. For the remeasuremnt of lease liability, the

measurement of the right of use assets is done at cost and subsequently, the measurement is

done at the cost less impairment losses and accumulated depreciation. At the initial level, the

leased liabilities are measured at the value of lease payments that are not being paid at the

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

date of lease agreement. The leased liability is adjusted for lease payments and interest

subsequently along with the impact of modification of lease (Guermazi & Khamoussi, 2018).

It is expected that the requirements of the new lease standard to recognize the related

lease liability and right of asset use is expected to create considerable impact on the amounts

that is recognized on the consolidated financial statements of the group. There will be impact

on the classification of cash flows because under AASB 117, the payments concerning

operating lease are presented as operating cash flow. On other hand, under the AASB 16, the

payment of lease will be split into an interest payment and principal that will be represented

as operating and financial cash flow respectively (Hladika & Valenta, 2018). Moreover, the

new lease accounting standard requires the reporting entity to make extensive disclosures.

From the analysis of the financial report of JB Hi-Fi, it has been ascertained that the

company has made progress in preparing the implementation of the new standard in number

of areas during the financial year 2018. Such areas include identifying necessary changes to

the processes and system that required accounting treatment and reporting the facts in

accordance with the new standard. Efforts were put in collation of data for the calculation to

assess the impact of new standard and identifying areas of judgment and complexities that are

relevant to the group (Chu et al., 2019). In addition to this, the initial estimates for identifying

the discount rates were also developed. There are a number of unresolved areas on which the

reliable estimate of the financial impact on the on the consolidated results of the group is

dependent. Such areas involve conclusion of data collection, refining the approach of

discount rate, transition method choice and approach refinement to discount rate.

In relation to the some minor operating lease and lease concerning with stores, the

group has entered into some operating lease agreement. Stores have been taken on lease for a

term of between 5 to 15 years with an option to extent the period in some case. In the event of

the group exercising the option to renew, there are few clauses that are contained in the

market review clauses. Regarding the lease term and arrangement, the company opt for the

short term leased where appropriate which is considered as one of the strategies opted by

organization to drive growth. The leasehold improvement is stated at the cost that is less of

impairment and accumulated depreciation (Agyei, 2017). In addition to this, the provision of

lease by the group is their best estimate of the amount that is required to return the lease

premises to the original condition. Such estimation is done by considering the best estimate

of onerous lease obligations and past history of vacating stores. Costs comprised of

date of lease agreement. The leased liability is adjusted for lease payments and interest

subsequently along with the impact of modification of lease (Guermazi & Khamoussi, 2018).

It is expected that the requirements of the new lease standard to recognize the related

lease liability and right of asset use is expected to create considerable impact on the amounts

that is recognized on the consolidated financial statements of the group. There will be impact

on the classification of cash flows because under AASB 117, the payments concerning

operating lease are presented as operating cash flow. On other hand, under the AASB 16, the

payment of lease will be split into an interest payment and principal that will be represented

as operating and financial cash flow respectively (Hladika & Valenta, 2018). Moreover, the

new lease accounting standard requires the reporting entity to make extensive disclosures.

From the analysis of the financial report of JB Hi-Fi, it has been ascertained that the

company has made progress in preparing the implementation of the new standard in number

of areas during the financial year 2018. Such areas include identifying necessary changes to

the processes and system that required accounting treatment and reporting the facts in

accordance with the new standard. Efforts were put in collation of data for the calculation to

assess the impact of new standard and identifying areas of judgment and complexities that are

relevant to the group (Chu et al., 2019). In addition to this, the initial estimates for identifying

the discount rates were also developed. There are a number of unresolved areas on which the

reliable estimate of the financial impact on the on the consolidated results of the group is

dependent. Such areas involve conclusion of data collection, refining the approach of

discount rate, transition method choice and approach refinement to discount rate.

In relation to the some minor operating lease and lease concerning with stores, the

group has entered into some operating lease agreement. Stores have been taken on lease for a

term of between 5 to 15 years with an option to extent the period in some case. In the event of

the group exercising the option to renew, there are few clauses that are contained in the

market review clauses. Regarding the lease term and arrangement, the company opt for the

short term leased where appropriate which is considered as one of the strategies opted by

organization to drive growth. The leasehold improvement is stated at the cost that is less of

impairment and accumulated depreciation (Agyei, 2017). In addition to this, the provision of

lease by the group is their best estimate of the amount that is required to return the lease

premises to the original condition. Such estimation is done by considering the best estimate

of onerous lease obligations and past history of vacating stores. Costs comprised of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

expenditure that are attributable directly to the item of acquisition. It can be seen that JB Hi-

Fi does not have any onerous provision for lease and under the new standard; it is not

required by the company to obtain the information about original lease payments and lease

term for such leases.

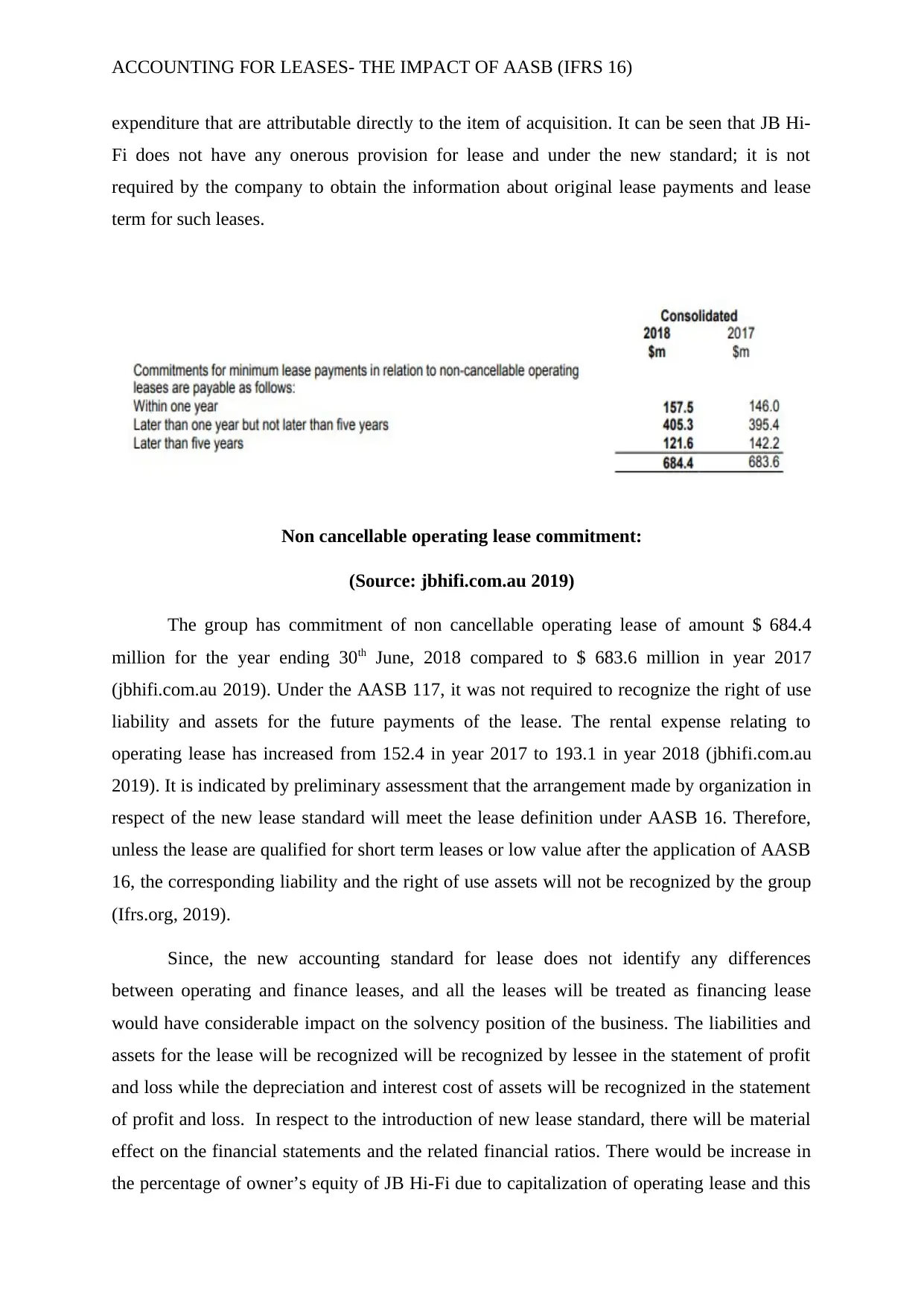

Non cancellable operating lease commitment:

(Source: jbhifi.com.au 2019)

The group has commitment of non cancellable operating lease of amount $ 684.4

million for the year ending 30th June, 2018 compared to $ 683.6 million in year 2017

(jbhifi.com.au 2019). Under the AASB 117, it was not required to recognize the right of use

liability and assets for the future payments of the lease. The rental expense relating to

operating lease has increased from 152.4 in year 2017 to 193.1 in year 2018 (jbhifi.com.au

2019). It is indicated by preliminary assessment that the arrangement made by organization in

respect of the new lease standard will meet the lease definition under AASB 16. Therefore,

unless the lease are qualified for short term leases or low value after the application of AASB

16, the corresponding liability and the right of use assets will not be recognized by the group

(Ifrs.org, 2019).

Since, the new accounting standard for lease does not identify any differences

between operating and finance leases, and all the leases will be treated as financing lease

would have considerable impact on the solvency position of the business. The liabilities and

assets for the lease will be recognized will be recognized by lessee in the statement of profit

and loss while the depreciation and interest cost of assets will be recognized in the statement

of profit and loss. In respect to the introduction of new lease standard, there will be material

effect on the financial statements and the related financial ratios. There would be increase in

the percentage of owner’s equity of JB Hi-Fi due to capitalization of operating lease and this

expenditure that are attributable directly to the item of acquisition. It can be seen that JB Hi-

Fi does not have any onerous provision for lease and under the new standard; it is not

required by the company to obtain the information about original lease payments and lease

term for such leases.

Non cancellable operating lease commitment:

(Source: jbhifi.com.au 2019)

The group has commitment of non cancellable operating lease of amount $ 684.4

million for the year ending 30th June, 2018 compared to $ 683.6 million in year 2017

(jbhifi.com.au 2019). Under the AASB 117, it was not required to recognize the right of use

liability and assets for the future payments of the lease. The rental expense relating to

operating lease has increased from 152.4 in year 2017 to 193.1 in year 2018 (jbhifi.com.au

2019). It is indicated by preliminary assessment that the arrangement made by organization in

respect of the new lease standard will meet the lease definition under AASB 16. Therefore,

unless the lease are qualified for short term leases or low value after the application of AASB

16, the corresponding liability and the right of use assets will not be recognized by the group

(Ifrs.org, 2019).

Since, the new accounting standard for lease does not identify any differences

between operating and finance leases, and all the leases will be treated as financing lease

would have considerable impact on the solvency position of the business. The liabilities and

assets for the lease will be recognized will be recognized by lessee in the statement of profit

and loss while the depreciation and interest cost of assets will be recognized in the statement

of profit and loss. In respect to the introduction of new lease standard, there will be material

effect on the financial statements and the related financial ratios. There would be increase in

the percentage of owner’s equity of JB Hi-Fi due to capitalization of operating lease and this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

would have an impact on debt to equity ratio and debt to assets ratio (Hilliard &

Neidermeyer, 2018). Since the rent expense would disappear and will be replaced by interest

expense for lease liability the depreciation expense for the right of use under the new

standard. This would have an impact on decreasing the operating expense and thereby

increasing the income before tax and interest. At the same time, due to the recognition of

interest expense on lease liability, there will be an increased expense for the company.

There will be increased amount of debt and it is indicated by many research that the

combined net debt of the company has grown by some Euro 45 billion. Therefore, it is

expected that the financial metric indicating the total debt of JB Hi-Fi would increase after

the new lease standard becomes effective. Since the majority of the rental expenses will be

reflected in the depreciation, an increase in earnings before profit tax and depreciation will

also increase, however the increase will not be substantial (Joubert et al., 2017). There would

be lower return on capital invested for JB Hi-Fi because of higher investment in capital for

lessee.

Since the lease will be in balance sheet, the transparency of the financial statements

would be enhanced. However, the company would be negative impact because of adverse

affect on some key ratios such as return on assets, debt to equity and debt to assets.

Therefore, from the analysis, it can be inferred that the leverage and gearing ratios will

increase along with the additional liabilities brought into the element of debt into the

calculations. The computations for return on capital employed will reduce because an

increase in the operating profit is not proportionate to the increment in capital employed

(Oppong & Aga, 2019). In addition to this, the cash flow statement of the company will not

be fundamentally impacted by the new lease standard. However, there would be an impact on

the valuation of the items in the cash flow statement.

JB Hi-Fi is an organization operating in the retail industry and this particular industry

and the likelihood of the impact of this particular standard is considerably high given the

significant usage of rented premises for the stores hired by them. It is indicated by the Pwc

global lease capitalization that there would be an increase in the median debt of 98% for the

retailers (Ward & Lowe, 2017). Much of the leases for the retailers are in the form of medium

term leases, whether in shopping centers and premium location and with such leases offering

renewal options in the form of variable rentals. The variation in the rentals is because of

existence of contingent rentals in some locations where the property owner has vested interest

would have an impact on debt to equity ratio and debt to assets ratio (Hilliard &

Neidermeyer, 2018). Since the rent expense would disappear and will be replaced by interest

expense for lease liability the depreciation expense for the right of use under the new

standard. This would have an impact on decreasing the operating expense and thereby

increasing the income before tax and interest. At the same time, due to the recognition of

interest expense on lease liability, there will be an increased expense for the company.

There will be increased amount of debt and it is indicated by many research that the

combined net debt of the company has grown by some Euro 45 billion. Therefore, it is

expected that the financial metric indicating the total debt of JB Hi-Fi would increase after

the new lease standard becomes effective. Since the majority of the rental expenses will be

reflected in the depreciation, an increase in earnings before profit tax and depreciation will

also increase, however the increase will not be substantial (Joubert et al., 2017). There would

be lower return on capital invested for JB Hi-Fi because of higher investment in capital for

lessee.

Since the lease will be in balance sheet, the transparency of the financial statements

would be enhanced. However, the company would be negative impact because of adverse

affect on some key ratios such as return on assets, debt to equity and debt to assets.

Therefore, from the analysis, it can be inferred that the leverage and gearing ratios will

increase along with the additional liabilities brought into the element of debt into the

calculations. The computations for return on capital employed will reduce because an

increase in the operating profit is not proportionate to the increment in capital employed

(Oppong & Aga, 2019). In addition to this, the cash flow statement of the company will not

be fundamentally impacted by the new lease standard. However, there would be an impact on

the valuation of the items in the cash flow statement.

JB Hi-Fi is an organization operating in the retail industry and this particular industry

and the likelihood of the impact of this particular standard is considerably high given the

significant usage of rented premises for the stores hired by them. It is indicated by the Pwc

global lease capitalization that there would be an increase in the median debt of 98% for the

retailers (Ward & Lowe, 2017). Much of the leases for the retailers are in the form of medium

term leases, whether in shopping centers and premium location and with such leases offering

renewal options in the form of variable rentals. The variation in the rentals is because of

existence of contingent rentals in some locations where the property owner has vested interest

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

in business performance and adjustment in inflation. The right to control assets in the retail

industry will be impacted by number of factors such as control over physical access over the

goods sold, physical access to space and tenant controlling the shop design along with

unrestricted use of defined retail space (Warren, 2016). Renting of the retail space under the

new standard would provide economic benefits those results from selling the products with

the objective of earning profit. Nonetheless, the retailers are required to consider the

potentially critical element of renewal option that are market priced but can be exercised only

when there is a significant economic incentive for the tenant to renew the lease (pwc.com.au,

2019). In such event when it is required to calculate the lease liability, it is required to include

the payment during the extended period of lease. Furthermore, the wider potential business

impact due to the interdiction of the AASB 16 on the retail industry could be identified in a

number of areas. Such areas include share based payment, debt covenants, lease negotiations

and dividend payment policy.

The operating lease by many lessees are currently managed though the accounts

payable system or on the spreadsheets. It is therefore required by them to conduct a

reassessment of index based payments and lease terms at each reporting date that now

requires capturing of extensive data (Stancheva & Velinova, 2019). Moreover, it might be

required by lessees to modify their process, information system and internal control for

complying with the standard.

Conclusion:

The analysis of the impact of the new lease standard that is AASB 16 have been

ascertained which views that the financial statement of the retail industry will be considerably

impacted due to the abolishment of differences between operating and financing lease. From

the analysis of the annual report of JB Hi-Fi, it has been found that the company is making

progress in a number of areas for the effective implementation of the AASB 16. Furthermore,

the financial metrics such as return on assets, debt ratio, debt covenants and earning before

inters, tax and depreciation would increased due to inclusion of operating lease on the

balance sheet. The accounting treatment for the leases would change considerably with

deterioration in the calculations of gearing ratios. Moreover, it has been evaluated that the

most sizeable impact of the new lease standard will be on the retail industry.

in business performance and adjustment in inflation. The right to control assets in the retail

industry will be impacted by number of factors such as control over physical access over the

goods sold, physical access to space and tenant controlling the shop design along with

unrestricted use of defined retail space (Warren, 2016). Renting of the retail space under the

new standard would provide economic benefits those results from selling the products with

the objective of earning profit. Nonetheless, the retailers are required to consider the

potentially critical element of renewal option that are market priced but can be exercised only

when there is a significant economic incentive for the tenant to renew the lease (pwc.com.au,

2019). In such event when it is required to calculate the lease liability, it is required to include

the payment during the extended period of lease. Furthermore, the wider potential business

impact due to the interdiction of the AASB 16 on the retail industry could be identified in a

number of areas. Such areas include share based payment, debt covenants, lease negotiations

and dividend payment policy.

The operating lease by many lessees are currently managed though the accounts

payable system or on the spreadsheets. It is therefore required by them to conduct a

reassessment of index based payments and lease terms at each reporting date that now

requires capturing of extensive data (Stancheva & Velinova, 2019). Moreover, it might be

required by lessees to modify their process, information system and internal control for

complying with the standard.

Conclusion:

The analysis of the impact of the new lease standard that is AASB 16 have been

ascertained which views that the financial statement of the retail industry will be considerably

impacted due to the abolishment of differences between operating and financing lease. From

the analysis of the annual report of JB Hi-Fi, it has been found that the company is making

progress in a number of areas for the effective implementation of the AASB 16. Furthermore,

the financial metrics such as return on assets, debt ratio, debt covenants and earning before

inters, tax and depreciation would increased due to inclusion of operating lease on the

balance sheet. The accounting treatment for the leases would change considerably with

deterioration in the calculations of gearing ratios. Moreover, it has been evaluated that the

most sizeable impact of the new lease standard will be on the retail industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

References list:

Agyei-Mensah, B. K. (2017). The relationship between corporate governance mechanisms

and IFRS 7 compliance: evidence from an emerging market. Corporate Governance:

The International Journal of Business in Society, 17(3), 446-465.

Chu, J., Heo, K., & Pae, J. (2019). Does a Firm’s Corporate Governance Enhance the

Beneficial Effect of IFRS Adoption?. Sustainability, 11(3), 885.

De Luca, F., & Prather-Kinsey, J. (2018). Legitimacy theory may explain the failure of global

adoption of IFRS: the case of Europe and the US. Journal of Management and

Governance, 22(3), 501-534.

Guermazi, W., & Khamoussi, H. (2018). Mandatory IFRS adoption in Europe: effect on the

conservative financial reporting. Journal of Financial Reporting and

Accounting, 16(4), 543-563.

Hilliard, T., & Neidermeyer, P. (2018). Market reaction to the transitory effects of IFRS: an

examination of disaggregated measures. International Journal of Accounting &

Information Management, 26(1), 2-37.

Hladika, M., & Valenta, I. (2018). Analysis of the effects of applying the new IFRS 16

Leases on the financial statements. Economic and Social Development: Book of

Proceedings, 255-263.

Ifrs.org. (2019). Retrieved 17 May 2019, from

https://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf

JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer. Jbhifi.com.au.

(2019). Retrieved 17 May 2019, from https://www.jbhifi.com.au/?q=annual%20report

%202018

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), 1-11.

Oppong, C., & Aga, M. (2019). Economic growth in European Union: does IFRS mandatory

adoption matter?. International Journal of Emerging Markets.

References list:

Agyei-Mensah, B. K. (2017). The relationship between corporate governance mechanisms

and IFRS 7 compliance: evidence from an emerging market. Corporate Governance:

The International Journal of Business in Society, 17(3), 446-465.

Chu, J., Heo, K., & Pae, J. (2019). Does a Firm’s Corporate Governance Enhance the

Beneficial Effect of IFRS Adoption?. Sustainability, 11(3), 885.

De Luca, F., & Prather-Kinsey, J. (2018). Legitimacy theory may explain the failure of global

adoption of IFRS: the case of Europe and the US. Journal of Management and

Governance, 22(3), 501-534.

Guermazi, W., & Khamoussi, H. (2018). Mandatory IFRS adoption in Europe: effect on the

conservative financial reporting. Journal of Financial Reporting and

Accounting, 16(4), 543-563.

Hilliard, T., & Neidermeyer, P. (2018). Market reaction to the transitory effects of IFRS: an

examination of disaggregated measures. International Journal of Accounting &

Information Management, 26(1), 2-37.

Hladika, M., & Valenta, I. (2018). Analysis of the effects of applying the new IFRS 16

Leases on the financial statements. Economic and Social Development: Book of

Proceedings, 255-263.

Ifrs.org. (2019). Retrieved 17 May 2019, from

https://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf

JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer. Jbhifi.com.au.

(2019). Retrieved 17 May 2019, from https://www.jbhifi.com.au/?q=annual%20report

%202018

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), 1-11.

Oppong, C., & Aga, M. (2019). Economic growth in European Union: does IFRS mandatory

adoption matter?. International Journal of Emerging Markets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Retail and consumer - an industry focus on the impact of IFRS 16. (2019). PwC. Retrieved 17

May 2019, from https://www.pwc.com.au/ifrs/retail-and-consumer-an-industry-focus-

on-the-impact-of-ifrs16.html

Stancheva-Todorova, E., & Velinova-Sokolova, N. (2019). IFRS 16 Leases and Its Impact on

Company’s Financial Reporting, Financial Ratios and Performance

Metrics. Economic Alternatives, (1), 44-62.

Ward, C. L., & Lowe, S. K. (2017). CULTURAL IMPACT OF INTERNATIONAL

FINANCIAL REPORTING STANDARDS ON THE COMPARABILITY OF

FINANCIAL STATEMENTS. International Journal of Business, Accounting, &

Finance, 11(1).

Warren, C. M. (2016). The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property

Management, 34(3).

Whittington, G. (2015). Fair value and IFRS. In The Routledge companion to financial

accounting theory (pp. 237-255). Routledge.

Www2.deloitte.com. (2019). Retrieved 17 May 2019, from

https://www2.deloitte.com/content/dam/Deloitte/nl/Documents/mergers-acquisitions/

deloitte-nl-ma-ifrs16-impactonbusinessvaluation1.pdf

Retail and consumer - an industry focus on the impact of IFRS 16. (2019). PwC. Retrieved 17

May 2019, from https://www.pwc.com.au/ifrs/retail-and-consumer-an-industry-focus-

on-the-impact-of-ifrs16.html

Stancheva-Todorova, E., & Velinova-Sokolova, N. (2019). IFRS 16 Leases and Its Impact on

Company’s Financial Reporting, Financial Ratios and Performance

Metrics. Economic Alternatives, (1), 44-62.

Ward, C. L., & Lowe, S. K. (2017). CULTURAL IMPACT OF INTERNATIONAL

FINANCIAL REPORTING STANDARDS ON THE COMPARABILITY OF

FINANCIAL STATEMENTS. International Journal of Business, Accounting, &

Finance, 11(1).

Warren, C. M. (2016). The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property

Management, 34(3).

Whittington, G. (2015). Fair value and IFRS. In The Routledge companion to financial

accounting theory (pp. 237-255). Routledge.

Www2.deloitte.com. (2019). Retrieved 17 May 2019, from

https://www2.deloitte.com/content/dam/Deloitte/nl/Documents/mergers-acquisitions/

deloitte-nl-ma-ifrs16-impactonbusinessvaluation1.pdf

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.