The Impact of AASB 16 on Lease Accounting for Woolworths Group Limited

VerifiedAdded on 2023/04/20

|12

|3173

|122

Essay

AI Summary

This essay provides a comprehensive analysis of the impact of AASB 16 (IFRS 16) on Woolworths Group Limited's lease accounting practices. It begins with an abstract and an introduction to the new leasing standard, contrasting operating and finance leases under AASB 117 and AASB 16. The essay details the changes in lease accounting, including the requirement to recognize lease liabilities and right-of-use assets on the balance sheet, with exemptions for low-value and short-term leases. It then provides an overview of Woolworths Group Limited, discussing its lease commitments and how the new standard will affect its financial statements. The essay examines the short-term and long-term impacts on the balance sheet, income statement, and cash flow statement, highlighting changes in asset and liability values, expense recognition, and cash flow presentation. Finally, the essay discusses the implications for the Australian retail sector and the lifecycle of leases, concluding with the effect of AASB 16 on different industrial sectors. The essay emphasizes the enhanced transparency and faithful representation of financial statements resulting from the new standard.

Running head: ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

Accounting for Leases- The Impact of AASB (IFRS) 16

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Leases- The Impact of AASB (IFRS) 16

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

Abstract:

The essay provides a brief overview of the new leasing standard, AASB 16 and its potential effects on the practices

of Woolworths Group Limited, which is one of the leading retailers in Australia. With the help of AASB 16, it

becomes easy to enhance transparency and ensure faithful depiction of the financial statement of the lessees, as

leasing is a financing tool developing obligations. This standard needs the organisation to analyse leasing

agreements intensively, since it holds a considerable amount of operating leases, which would bring drastic

variations in the preparation of financial statements. Hence, Woolworths needs to start analysing the probable effects

of AASB 16 by accumulating data and preparing for new procedures to adhere to the standard along with

minimising the unanticipated effects.

Abstract:

The essay provides a brief overview of the new leasing standard, AASB 16 and its potential effects on the practices

of Woolworths Group Limited, which is one of the leading retailers in Australia. With the help of AASB 16, it

becomes easy to enhance transparency and ensure faithful depiction of the financial statement of the lessees, as

leasing is a financing tool developing obligations. This standard needs the organisation to analyse leasing

agreements intensively, since it holds a considerable amount of operating leases, which would bring drastic

variations in the preparation of financial statements. Hence, Woolworths needs to start analysing the probable effects

of AASB 16 by accumulating data and preparing for new procedures to adhere to the standard along with

minimising the unanticipated effects.

2ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

Introduction:

The “Australian Accounting Standards Board (AASB)” has developed and issued AASB 16, which is a

new accounting standard for leases and it is mandatory for all the listed Australian organisations to adhere to the

same initiating from January 1, 2019. The paper would provide an overview of the different kinds of lease

agreements with special emphasis on the differences between operating lease and financial lease. In particular, the

essay would intend to analyse the different kinds of lease agreements in relation to Woolworths Group Limited,

which is a giant retailer in Australia after Wesfarmers Limited. In addition, a discussion regarding the value of

leases in the annual report of the organisation would be made in this paper as well. Along with this, the evaluation of

the new leasing standard, AASB 16 would be taken into consideration and it would be contrasted with the previous

leasing standards, AASB 17 to gain an overview of the probable effects of the accounting rules of leases on

Woolworths. Finally, the essay would shed light on gaining an insight of the lease agreements in the context of the

Australian retail sector along with lifecycle and stage of the lease.

Understanding of lease agreements, their impact on financial reports and comparison between operating and

financial leases:

In accordance with AASB 117, leases are of two types, which include operating lease and finance lease.

This model needs reporting of lease liabilities and assets on balance sheet only for finance lease. However, in case of

operating lease, AASB 117 needs the organisation in disclosing important information (Aasb.gov.au, 2018). In case

of operating lease, the asset ownership stays with the lessor for the overall lease term, while for finance lease, the

transfer of ownership after the end of the lease term stays with the lessee. However, AASB 117 does not fulfil the

needs of the users at the time of undertaking decisions from the financial statements, as the material amount related

to operating leases are not represented on the balance sheet statement. Hence, IASB has issued IFRS 16 Leases, after

which AASB has issued AASB 16 Leases.

Numerous changes are made from AASB 117 to AASB 16. However, there would be no change in lease

accounting for the lessors. In case of lessees, the significant change is the eradication of two lease categorisations,

which imply the new rule develops a single model of lease accounting. The contracts containing leases or are leased,

are categorised in the form of leases (Aasb.gov.au, 2018). All lessees need to realise all leases as present value of

lease liability and right-of-use asset in the balance sheet statement except leased assets having lower values and

short-term leases. Accordingly, there would be depreciation in right-of-use assets in compliance with “AASB 116

Property, Plant and Equipment” or there would be testing of the same with adherence to “AASB 136 Impairment of

Assets” or interest would be recognised on lease liability with conformance to “AASB 140 Investment Property”.

According to the new lease standard, the lessors and lessees are needed to fulfil the objective of disclosure,

instead of stringent checklists. The lessees need to present right-of-use assets distinctively from other assets and the

case would be similar in case of lease liabilities as well in the balance sheet statement or they need to be published

Introduction:

The “Australian Accounting Standards Board (AASB)” has developed and issued AASB 16, which is a

new accounting standard for leases and it is mandatory for all the listed Australian organisations to adhere to the

same initiating from January 1, 2019. The paper would provide an overview of the different kinds of lease

agreements with special emphasis on the differences between operating lease and financial lease. In particular, the

essay would intend to analyse the different kinds of lease agreements in relation to Woolworths Group Limited,

which is a giant retailer in Australia after Wesfarmers Limited. In addition, a discussion regarding the value of

leases in the annual report of the organisation would be made in this paper as well. Along with this, the evaluation of

the new leasing standard, AASB 16 would be taken into consideration and it would be contrasted with the previous

leasing standards, AASB 17 to gain an overview of the probable effects of the accounting rules of leases on

Woolworths. Finally, the essay would shed light on gaining an insight of the lease agreements in the context of the

Australian retail sector along with lifecycle and stage of the lease.

Understanding of lease agreements, their impact on financial reports and comparison between operating and

financial leases:

In accordance with AASB 117, leases are of two types, which include operating lease and finance lease.

This model needs reporting of lease liabilities and assets on balance sheet only for finance lease. However, in case of

operating lease, AASB 117 needs the organisation in disclosing important information (Aasb.gov.au, 2018). In case

of operating lease, the asset ownership stays with the lessor for the overall lease term, while for finance lease, the

transfer of ownership after the end of the lease term stays with the lessee. However, AASB 117 does not fulfil the

needs of the users at the time of undertaking decisions from the financial statements, as the material amount related

to operating leases are not represented on the balance sheet statement. Hence, IASB has issued IFRS 16 Leases, after

which AASB has issued AASB 16 Leases.

Numerous changes are made from AASB 117 to AASB 16. However, there would be no change in lease

accounting for the lessors. In case of lessees, the significant change is the eradication of two lease categorisations,

which imply the new rule develops a single model of lease accounting. The contracts containing leases or are leased,

are categorised in the form of leases (Aasb.gov.au, 2018). All lessees need to realise all leases as present value of

lease liability and right-of-use asset in the balance sheet statement except leased assets having lower values and

short-term leases. Accordingly, there would be depreciation in right-of-use assets in compliance with “AASB 116

Property, Plant and Equipment” or there would be testing of the same with adherence to “AASB 136 Impairment of

Assets” or interest would be recognised on lease liability with conformance to “AASB 140 Investment Property”.

According to the new lease standard, the lessors and lessees are needed to fulfil the objective of disclosure,

instead of stringent checklists. The lessees need to present right-of-use assets distinctively from other assets and the

case would be similar in case of lease liabilities as well in the balance sheet statement or they need to be published

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

distinctively as notes to financial statements (Ahmed & Ali, 2015). There needs to be segregation of depreciation

expense and interest expense in the profit and loss statement and it is necessary for the lessees to categorise the

below-stated payments in the cash flow statement:

Cash payments on lease liabilities under financing activities

Payments from lower leased asset values and short-term leases

Compliance of interest payments related to leased liabilities with “AASB 107 Statement of Cash Flows for

interest paid”

The above changes have assisted in enhancing financial reporting quality and thus, faithful representation is

ensured in terms of timing, amount and correct presentation of cash flow activity for leases. Moreover, the users

could contrast the financial statements of the organisations without spending time on adjustments. Finally, AASB 16

would enable in developing increased transparency of the financial leverage level of the lessees (Beckman, 2016).

Overview of Woolworths Group Limited and the value of leases disclosed in its latest annual report:

Woolworths Group Limited is the leading Australian retailer placed after Wesfarmers Limited in Australia

and New Zealand. It is involved in operating through Australian Food, New Zealand Food, Big W, Endeavour

Drinks and other segments. Moreover, the organisation has 1,008 metro stores and supermarkets and 1,545 liquor

stores. It has been established in 1924 with workforce around 201,522 employees (Woolworthsgroup.com.au, 2018).

The organisation leases properties that include warehouses and retail premises and it is responsible for

expenses associated with leased assets like insurance, maintenance and taxes. Woolworths is involved in using both

finance lease and operating lease. Finance lease passes over the rewards and risks related to ownership of assets

even if there is mutual transfer of titles of the assets (Dagwell, Wines & Lambert, 2015). The non-current, unsecured

finance lease of the organisation has been nil in 2018, which was $2 million in 2017. However, it has no current,

unsecured finance lease in both the years. However, there is difference between the two types of leases in that it is

realised in the form of expense based on straight-line method over the term of the lease. In 2018, the commitments

of operating lease of Woolworths have been $22,904 million compared to $24,439 million in 2017. It has recognised

operating lease obligations for onerous lease in the balance sheet statement in “Note 3.9 of the latest annual report”.

In addition, the firm has lease commitments on its leased premises, which are calculated in the form of turnover

percentage of the store dwelling in the premises (Woolworthsgroup.com.au, 2018).

At present, Woolworths is following AASB 117 in order to prepare lease accounting, as the new standard

has additional cost, complexities and administrative abilities on the management in the absence of benefits.

Impact of the accounting rules of leases on Woolworths Group Limited:

The new lease standard, AASB 16 would affect the consolidated financial statements of Woolworths that

takes into account discontinued operations as well.

distinctively as notes to financial statements (Ahmed & Ali, 2015). There needs to be segregation of depreciation

expense and interest expense in the profit and loss statement and it is necessary for the lessees to categorise the

below-stated payments in the cash flow statement:

Cash payments on lease liabilities under financing activities

Payments from lower leased asset values and short-term leases

Compliance of interest payments related to leased liabilities with “AASB 107 Statement of Cash Flows for

interest paid”

The above changes have assisted in enhancing financial reporting quality and thus, faithful representation is

ensured in terms of timing, amount and correct presentation of cash flow activity for leases. Moreover, the users

could contrast the financial statements of the organisations without spending time on adjustments. Finally, AASB 16

would enable in developing increased transparency of the financial leverage level of the lessees (Beckman, 2016).

Overview of Woolworths Group Limited and the value of leases disclosed in its latest annual report:

Woolworths Group Limited is the leading Australian retailer placed after Wesfarmers Limited in Australia

and New Zealand. It is involved in operating through Australian Food, New Zealand Food, Big W, Endeavour

Drinks and other segments. Moreover, the organisation has 1,008 metro stores and supermarkets and 1,545 liquor

stores. It has been established in 1924 with workforce around 201,522 employees (Woolworthsgroup.com.au, 2018).

The organisation leases properties that include warehouses and retail premises and it is responsible for

expenses associated with leased assets like insurance, maintenance and taxes. Woolworths is involved in using both

finance lease and operating lease. Finance lease passes over the rewards and risks related to ownership of assets

even if there is mutual transfer of titles of the assets (Dagwell, Wines & Lambert, 2015). The non-current, unsecured

finance lease of the organisation has been nil in 2018, which was $2 million in 2017. However, it has no current,

unsecured finance lease in both the years. However, there is difference between the two types of leases in that it is

realised in the form of expense based on straight-line method over the term of the lease. In 2018, the commitments

of operating lease of Woolworths have been $22,904 million compared to $24,439 million in 2017. It has recognised

operating lease obligations for onerous lease in the balance sheet statement in “Note 3.9 of the latest annual report”.

In addition, the firm has lease commitments on its leased premises, which are calculated in the form of turnover

percentage of the store dwelling in the premises (Woolworthsgroup.com.au, 2018).

At present, Woolworths is following AASB 117 in order to prepare lease accounting, as the new standard

has additional cost, complexities and administrative abilities on the management in the absence of benefits.

Impact of the accounting rules of leases on Woolworths Group Limited:

The new lease standard, AASB 16 would affect the consolidated financial statements of Woolworths that

takes into account discontinued operations as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

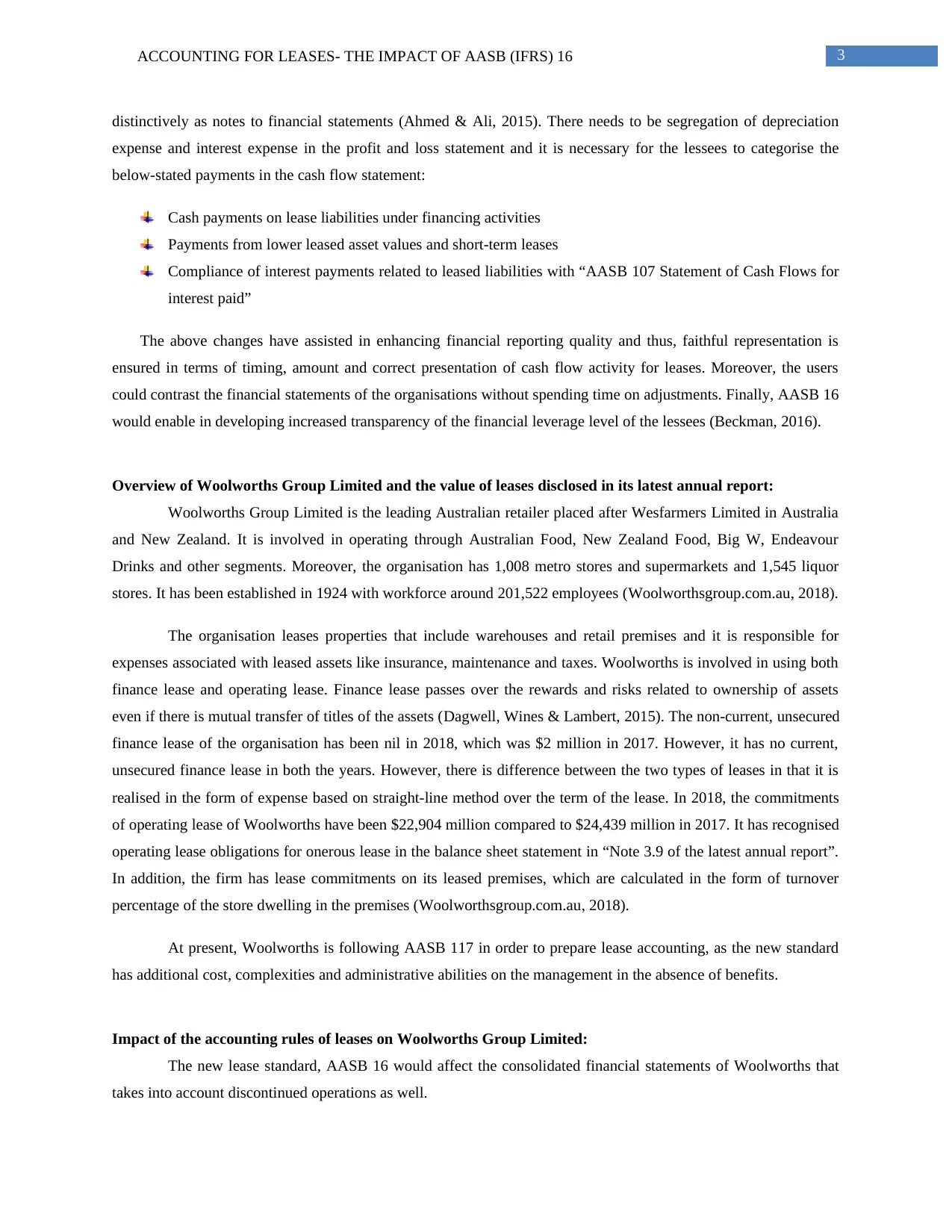

The net impact of new lease liabilities as well as right-of-use assets adjusted in relation to deferred tax and

reversing the current straight-line lease and incentive liability of $260 million mentioned in “Note 3.10 of the annual

report” would be realised against retained earnings. The effect would be predominant on the property leases of the

organisation for warehousing facilities, support offices, retail premises and distribution centres (Dakis, 2016). The

actual effect of applying AASB 16 on the financial reports would rely on economic conditions in future including

the following:

The borrowing rate of the organisation at July 1, 2019

The composition of lease portfolio

The degree to which choice is made in using recognition exemptions as well as practical expedients

The revised accounting policies subject to change before the organisation publishes its financial reports

including the initial application date

Summary of the short-term and long-term impacts of the changes to reporting for leases:

Impact on the balance sheet statement of Woolworths:

There would be changes in the financial statements of the concerned organisation owing the

implementation of AASB 16. It is required to prepare the financial report on the statement of financial position in

relation to lease assets and lease liabilities and the amounts of both items are expected to rise over time (Holland,

2016). The reason is that when these assets are recognised, which are not required under AASB 117, both lease asset

and lease liability amounts would increase as well. Along with this, no segregation would be made in AASB 16

between lease liabilities and lease assets. Furthermore, it becomes possible for the lessees to bring right-of-use asset

and lease liability would be disclosed in the balance sheet statement for each type of lease (Joubert, Garvie & Parle,

2017).

At present, the operating lease commitments of Woolworths have been $22,904 million and disclosure is

made by adhering to AASB 117. Hence, the balance sheet statement would not be affected by these lease

commitments, since they are adjusted in profit and loss statement. In accordance with AASB 16, it is necessary for

Woolworths to capitalise commitments related to operating lease on the statement of financial position of the

organisation. Another considerable effect would be observed by increased values of assets and liabilities and the

statement of financial position of Woolworths might represent impact on covenants associated with debt-to-equity

ratio (Kabir & Rahman, 2018).

Impact on the income statement of Woolworths:

The net impact of new lease liabilities as well as right-of-use assets adjusted in relation to deferred tax and

reversing the current straight-line lease and incentive liability of $260 million mentioned in “Note 3.10 of the annual

report” would be realised against retained earnings. The effect would be predominant on the property leases of the

organisation for warehousing facilities, support offices, retail premises and distribution centres (Dakis, 2016). The

actual effect of applying AASB 16 on the financial reports would rely on economic conditions in future including

the following:

The borrowing rate of the organisation at July 1, 2019

The composition of lease portfolio

The degree to which choice is made in using recognition exemptions as well as practical expedients

The revised accounting policies subject to change before the organisation publishes its financial reports

including the initial application date

Summary of the short-term and long-term impacts of the changes to reporting for leases:

Impact on the balance sheet statement of Woolworths:

There would be changes in the financial statements of the concerned organisation owing the

implementation of AASB 16. It is required to prepare the financial report on the statement of financial position in

relation to lease assets and lease liabilities and the amounts of both items are expected to rise over time (Holland,

2016). The reason is that when these assets are recognised, which are not required under AASB 117, both lease asset

and lease liability amounts would increase as well. Along with this, no segregation would be made in AASB 16

between lease liabilities and lease assets. Furthermore, it becomes possible for the lessees to bring right-of-use asset

and lease liability would be disclosed in the balance sheet statement for each type of lease (Joubert, Garvie & Parle,

2017).

At present, the operating lease commitments of Woolworths have been $22,904 million and disclosure is

made by adhering to AASB 117. Hence, the balance sheet statement would not be affected by these lease

commitments, since they are adjusted in profit and loss statement. In accordance with AASB 16, it is necessary for

Woolworths to capitalise commitments related to operating lease on the statement of financial position of the

organisation. Another considerable effect would be observed by increased values of assets and liabilities and the

statement of financial position of Woolworths might represent impact on covenants associated with debt-to-equity

ratio (Kabir & Rahman, 2018).

Impact on the income statement of Woolworths:

5ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

When the new leasing standard AASB 16 would be implemented, it is deemed to have the following effects

on the profit and loss statement of Woolworths Group Limited:

Representation of lease-related expense

Recognition of expenses associated with individual lease and lease in relation to a portfolio (Spencer &

Webb, 2015)

Other impacts

AASB 16 is estimated to increase the operating income of the organisation, since it contains off-balance sheet

leases. The reason is that when it would be applied, the implicit interest associated with lease payments would be

depicted for past off-balance sheet leases as finance costs or interest expense (Warren, 2016). On the other hand, in

accordance with AASB 117, the off-balance sheet expenditures would be taken into consideration as operating

expenses. Hence, when AASB 16 is applied, operating margin ratio is expected to rise due to rise in operating

income.

Impact on the cash flow statement of Woolworths:

The new leasing standard, AASB 16, would not have any effect on the cash flow statement, as the changes

needed do not exercise any influence on cash-in-cash-out between the two parties in the lease contracts. However,

there would be an effect on the depiction of cash-in-cash-out to past balance sheet leases. In order to ensure the

linkage between the financial statements, AASB 16 requires the organisation to categorise the payments for the main

portion of lease liabilities under financing activities and the case would be similar in case of interest portion of lease

liabilities based on the requirements in relation to payment of other interest (Wilkins, 2015).

Understanding of lease agreements for the Australian retail sector and the lifecycle and stage of the lease:

There are a number of industries having considerable operating lease amounts like telecommunication and

airlines, which would be impacted by AASB 16. Similarly, the Australian retail companies like Woolworths would

be affected significantly owing to the considerable amount of renting premises for their warehouses, distribution

centres and stores.

When the new leasing standard AASB 16 would be implemented, it is deemed to have the following effects

on the profit and loss statement of Woolworths Group Limited:

Representation of lease-related expense

Recognition of expenses associated with individual lease and lease in relation to a portfolio (Spencer &

Webb, 2015)

Other impacts

AASB 16 is estimated to increase the operating income of the organisation, since it contains off-balance sheet

leases. The reason is that when it would be applied, the implicit interest associated with lease payments would be

depicted for past off-balance sheet leases as finance costs or interest expense (Warren, 2016). On the other hand, in

accordance with AASB 117, the off-balance sheet expenditures would be taken into consideration as operating

expenses. Hence, when AASB 16 is applied, operating margin ratio is expected to rise due to rise in operating

income.

Impact on the cash flow statement of Woolworths:

The new leasing standard, AASB 16, would not have any effect on the cash flow statement, as the changes

needed do not exercise any influence on cash-in-cash-out between the two parties in the lease contracts. However,

there would be an effect on the depiction of cash-in-cash-out to past balance sheet leases. In order to ensure the

linkage between the financial statements, AASB 16 requires the organisation to categorise the payments for the main

portion of lease liabilities under financing activities and the case would be similar in case of interest portion of lease

liabilities based on the requirements in relation to payment of other interest (Wilkins, 2015).

Understanding of lease agreements for the Australian retail sector and the lifecycle and stage of the lease:

There are a number of industries having considerable operating lease amounts like telecommunication and

airlines, which would be impacted by AASB 16. Similarly, the Australian retail companies like Woolworths would

be affected significantly owing to the considerable amount of renting premises for their warehouses, distribution

centres and stores.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

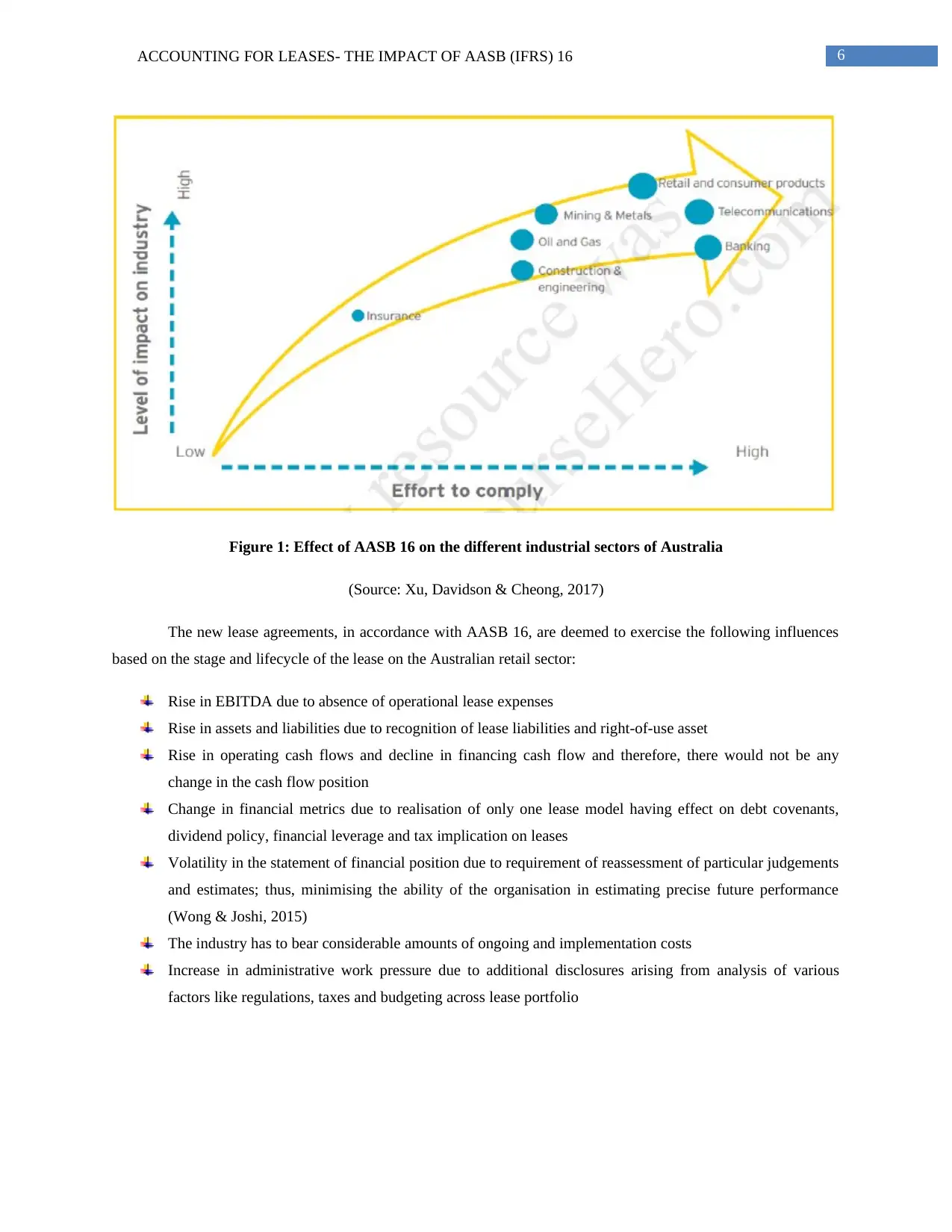

Figure 1: Effect of AASB 16 on the different industrial sectors of Australia

(Source: Xu, Davidson & Cheong, 2017)

The new lease agreements, in accordance with AASB 16, are deemed to exercise the following influences

based on the stage and lifecycle of the lease on the Australian retail sector:

Rise in EBITDA due to absence of operational lease expenses

Rise in assets and liabilities due to recognition of lease liabilities and right-of-use asset

Rise in operating cash flows and decline in financing cash flow and therefore, there would not be any

change in the cash flow position

Change in financial metrics due to realisation of only one lease model having effect on debt covenants,

dividend policy, financial leverage and tax implication on leases

Volatility in the statement of financial position due to requirement of reassessment of particular judgements

and estimates; thus, minimising the ability of the organisation in estimating precise future performance

(Wong & Joshi, 2015)

The industry has to bear considerable amounts of ongoing and implementation costs

Increase in administrative work pressure due to additional disclosures arising from analysis of various

factors like regulations, taxes and budgeting across lease portfolio

Figure 1: Effect of AASB 16 on the different industrial sectors of Australia

(Source: Xu, Davidson & Cheong, 2017)

The new lease agreements, in accordance with AASB 16, are deemed to exercise the following influences

based on the stage and lifecycle of the lease on the Australian retail sector:

Rise in EBITDA due to absence of operational lease expenses

Rise in assets and liabilities due to recognition of lease liabilities and right-of-use asset

Rise in operating cash flows and decline in financing cash flow and therefore, there would not be any

change in the cash flow position

Change in financial metrics due to realisation of only one lease model having effect on debt covenants,

dividend policy, financial leverage and tax implication on leases

Volatility in the statement of financial position due to requirement of reassessment of particular judgements

and estimates; thus, minimising the ability of the organisation in estimating precise future performance

(Wong & Joshi, 2015)

The industry has to bear considerable amounts of ongoing and implementation costs

Increase in administrative work pressure due to additional disclosures arising from analysis of various

factors like regulations, taxes and budgeting across lease portfolio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

Conclusion:

After assessment of the changes in AASB 16, there would be considerable impact on a number of business

areas like additional disclosures, recognition of new leases, portfolio of leases and others. The Australian retail

sector is expected to be impacted considerably and thus, there arises need for consideration of different areas

through which benefits could be gained. These areas constitute of lease incentive, lease terms and staff bonus policy.

As the new leasing standard would be effective from 2019, it is advised to Woolworths to initiate accumulating data

along with preparing for new procedures to conform to AASB 16 and the managers from various departments are

needed to plan and cooperate regarding future lease arrangements.

Conclusion:

After assessment of the changes in AASB 16, there would be considerable impact on a number of business

areas like additional disclosures, recognition of new leases, portfolio of leases and others. The Australian retail

sector is expected to be impacted considerably and thus, there arises need for consideration of different areas

through which benefits could be gained. These areas constitute of lease incentive, lease terms and staff bonus policy.

As the new leasing standard would be effective from 2019, it is advised to Woolworths to initiate accumulating data

along with preparing for new procedures to conform to AASB 16 and the managers from various departments are

needed to plan and cooperate regarding future lease arrangements.

8ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

References:

Aasb.gov.au. (2018). Retrieved 23 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf

Aasb.gov.au. (2018). Retrieved 23 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf

Ahmed, K., & Ali, M. J. (2015). Has the harmonisation of accounting practices improved? Evidence from South

Asia. International Journal of Accounting & Information Management, 23(4), 327-348.

Beckman, J. K. (2016). FASB and IASB diverging perspectives on the new lessee accounting: Implications for

international managerial decision-making. International Journal of Managerial Finance, 12(2), 161-176.

Dagwell, R., Wines, G., & Lambert, C. (2015). Corporate accounting in Australia. Pearson Higher Education AU.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance Directions, 68(2), 99.

Holland, D. (2016). Simplifying income recognition for not-for-profit entities. Governance Directions, 68(11), 666.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas &

Trends, 15(2), 113-119.

Kabir, H., & Rahman, A. (2018). How Does the IASB Use the Conceptual Framework in Developing IFRSs? An

Examination of the Development of IFRS 16 Leases. Journal of Financial Reporting, 27(9), 310-342.

Spencer, A. W., & Webb, T. Z. (2015). Leases: A review of contemporary academic literature relating to

lessees. Accounting Horizons, 29(4), 997-1023.

Warren, C. M. (2016). The impact of International Accounting Standards Board (IASB)/International Financial

Reporting Standard 16 (IFRS 16). Property Management, 34(3), 91-110.

Wilkins, T. A. (2015). Accounting for Leases Standards. Wiley Encyclopedia of Management, 18(7), 1-4.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key ratios: Evidence

from Australia. Australasian Accounting, Business and Finance Journal, 9(3), 27-44.

Woolworthsgroup.com.au. (2018). Retrieved 23 December 2018, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Woolworthsgroup.com.au. (2018). Woolworths Group: Quality Brands and Trusted Retailing. Retrieved 23

December 2018, from https://www.woolworthsgroup.com.au/

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating to capitalised

leases. Pacific Accounting Review, 29(1), 34-54.

References:

Aasb.gov.au. (2018). Retrieved 23 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf

Aasb.gov.au. (2018). Retrieved 23 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf

Ahmed, K., & Ali, M. J. (2015). Has the harmonisation of accounting practices improved? Evidence from South

Asia. International Journal of Accounting & Information Management, 23(4), 327-348.

Beckman, J. K. (2016). FASB and IASB diverging perspectives on the new lessee accounting: Implications for

international managerial decision-making. International Journal of Managerial Finance, 12(2), 161-176.

Dagwell, R., Wines, G., & Lambert, C. (2015). Corporate accounting in Australia. Pearson Higher Education AU.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance Directions, 68(2), 99.

Holland, D. (2016). Simplifying income recognition for not-for-profit entities. Governance Directions, 68(11), 666.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas &

Trends, 15(2), 113-119.

Kabir, H., & Rahman, A. (2018). How Does the IASB Use the Conceptual Framework in Developing IFRSs? An

Examination of the Development of IFRS 16 Leases. Journal of Financial Reporting, 27(9), 310-342.

Spencer, A. W., & Webb, T. Z. (2015). Leases: A review of contemporary academic literature relating to

lessees. Accounting Horizons, 29(4), 997-1023.

Warren, C. M. (2016). The impact of International Accounting Standards Board (IASB)/International Financial

Reporting Standard 16 (IFRS 16). Property Management, 34(3), 91-110.

Wilkins, T. A. (2015). Accounting for Leases Standards. Wiley Encyclopedia of Management, 18(7), 1-4.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key ratios: Evidence

from Australia. Australasian Accounting, Business and Finance Journal, 9(3), 27-44.

Woolworthsgroup.com.au. (2018). Retrieved 23 December 2018, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Woolworthsgroup.com.au. (2018). Woolworths Group: Quality Brands and Trusted Retailing. Retrieved 23

December 2018, from https://www.woolworthsgroup.com.au/

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating to capitalised

leases. Pacific Accounting Review, 29(1), 34-54.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

Appendices:

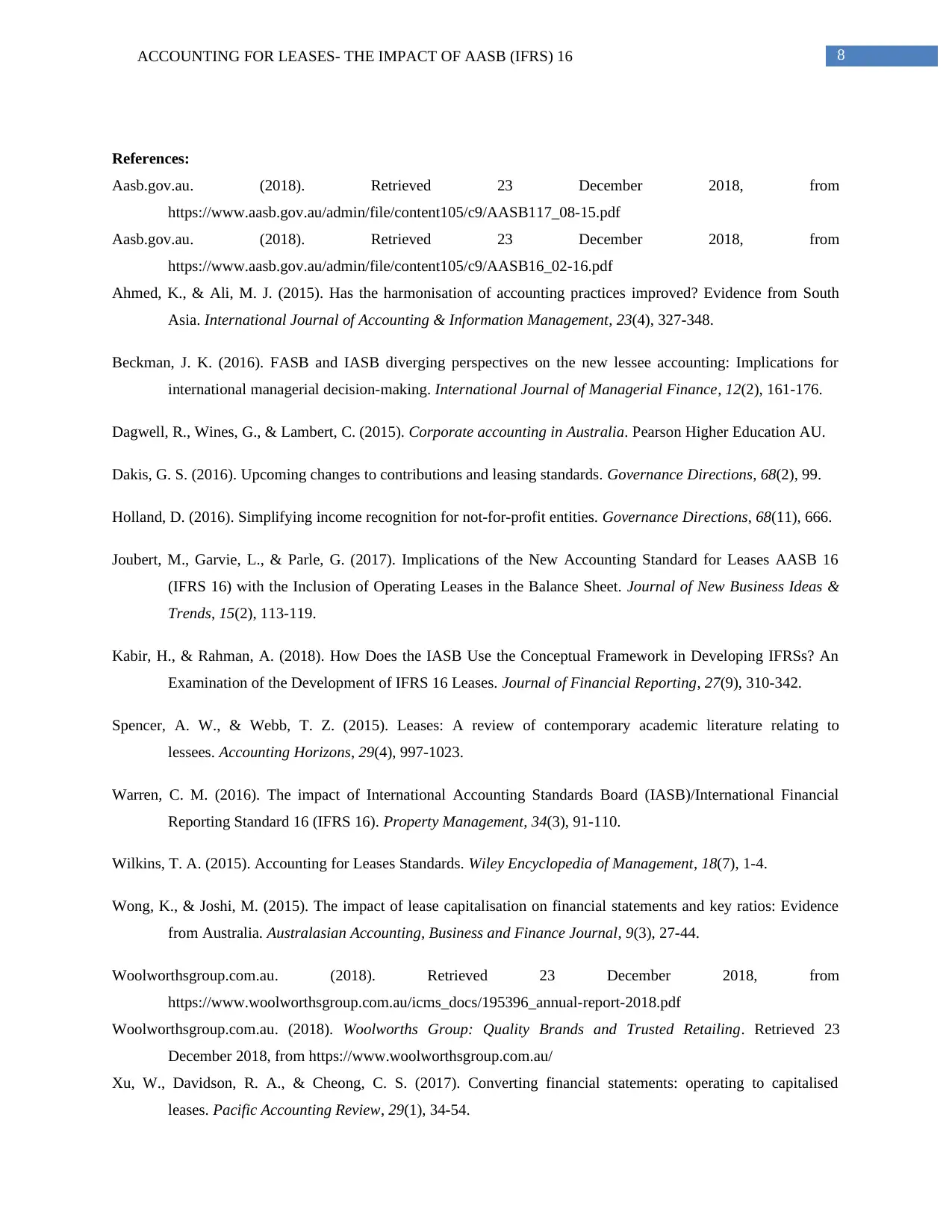

Appendix 1: Finance lease of Woolworths Group Limited for the years 2017 and 2018

Appendices:

Appendix 1: Finance lease of Woolworths Group Limited for the years 2017 and 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

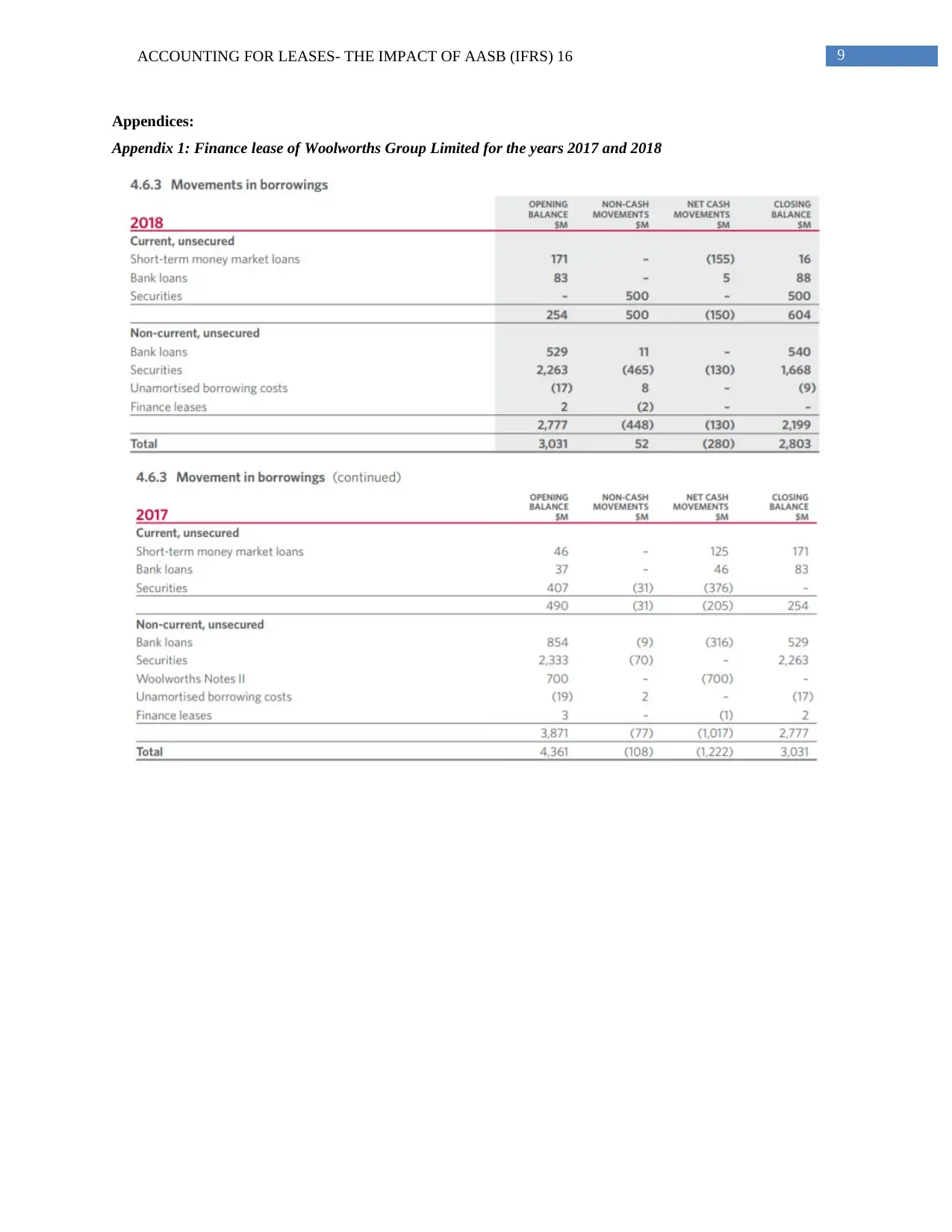

Appendix 2: Operating lease commitments of Woolworths Group Limited for the years 2017 and 2018

Appendix 2: Operating lease commitments of Woolworths Group Limited for the years 2017 and 2018

11ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS) 16

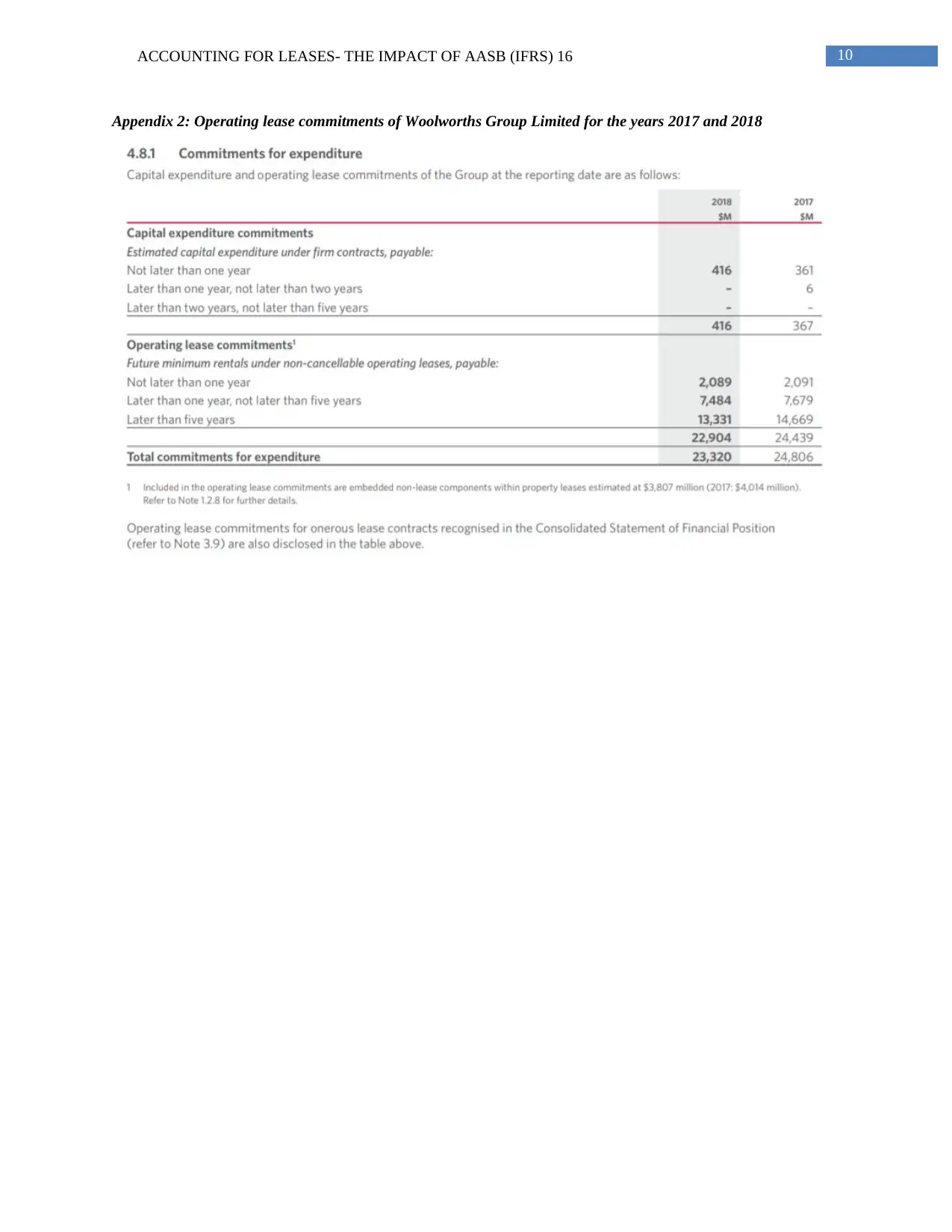

Appendix 3: Estimated effect of the impleemntation of AASB 16 on Woolworths Group Limited

Appendix 3: Estimated effect of the impleemntation of AASB 16 on Woolworths Group Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.