Accounting for Management: Budgeting and Cost Allocation Methods

VerifiedAdded on 2022/11/12

|10

|1405

|330

AI Summary

This document discusses budgeting and sensitivity analysis, indirect cost allocation methods, and activity-based costing. It includes schedules, an email to T & K, and a report to T & K.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING FOR MANAGEMENT

ACCOUNTING FOR MANAGEMENT

Name of the Student:

Name of the University:

Author Note

ACCOUNTING FOR MANAGEMENT

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING FOR MANAGEMENT

Table of Contents

Task A........................................................................................................................................2

Budgeting and Sensitivity analysis............................................................................................2

Schedule 1..............................................................................................................................2

Schedule 2..............................................................................................................................2

Email to T & K.......................................................................................................................3

Task B........................................................................................................................................5

Indirect Cost allocation Method.................................................................................................5

Schedule 3..............................................................................................................................5

Report to T & K.....................................................................................................................6

Introduction........................................................................................................................6

Discussion..........................................................................................................................6

Conclusion..........................................................................................................................7

Reference and Bibliography.......................................................................................................8

Table of Contents

Task A........................................................................................................................................2

Budgeting and Sensitivity analysis............................................................................................2

Schedule 1..............................................................................................................................2

Schedule 2..............................................................................................................................2

Email to T & K.......................................................................................................................3

Task B........................................................................................................................................5

Indirect Cost allocation Method.................................................................................................5

Schedule 3..............................................................................................................................5

Report to T & K.....................................................................................................................6

Introduction........................................................................................................................6

Discussion..........................................................................................................................6

Conclusion..........................................................................................................................7

Reference and Bibliography.......................................................................................................8

2ACCOUNTING FOR MANAGEMENT

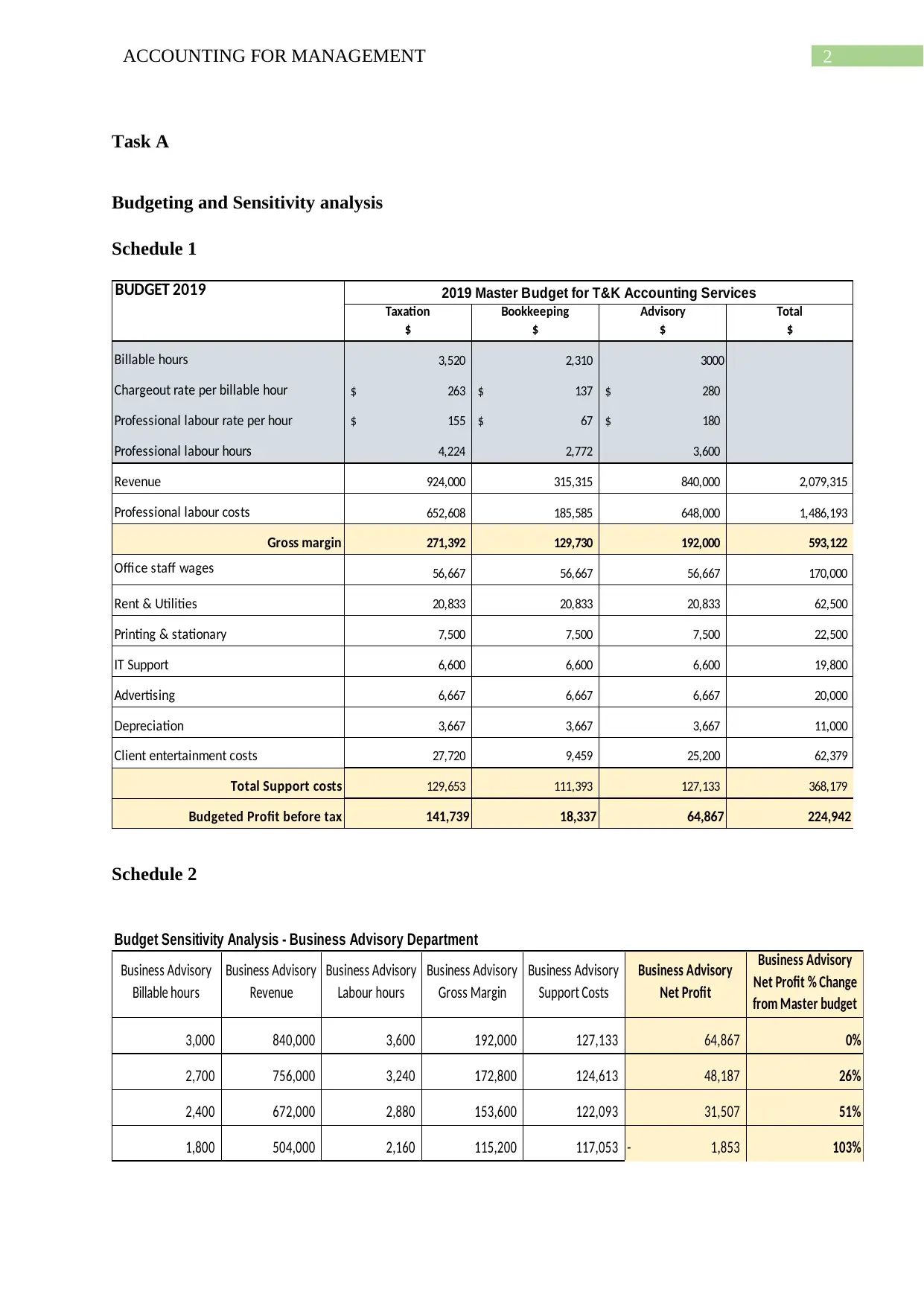

Task A

Budgeting and Sensitivity analysis

Schedule 1

BUDGET 2019

Taxation Bookkeeping Advisory Total

$ $ $ $

Billable hours 3,520 2,310 3000

Chargeout rate per billable hour 263$ 137$ 280$

Professional labour rate per hour 155$ 67$ 180$

Professional labour hours 4,224 2,772 3,600

Revenue 924,000 315,315 840,000 2,079,315

Professional labour costs 652,608 185,585 648,000 1,486,193

Gross margin 271,392 129,730 192,000 593,122

Office staff wages 56,667 56,667 56,667 170,000

Rent & Utilities 20,833 20,833 20,833 62,500

Printing & stationary 7,500 7,500 7,500 22,500

IT Support 6,600 6,600 6,600 19,800

Advertising 6,667 6,667 6,667 20,000

Depreciation 3,667 3,667 3,667 11,000

Client entertainment costs 27,720 9,459 25,200 62,379

Total Support costs 129,653 111,393 127,133 368,179

Budgeted Profit before tax 141,739 18,337 64,867 224,942

2019 Master Budget for T&K Accounting Services

Schedule 2

Budget Sensitivity Analysis - Business Advisory Department

Business Advisory

Billable hours

Business Advisory

Revenue

Business Advisory

Labour hours

Business Advisory

Gross Margin

Business Advisory

Support Costs

Business Advisory

Net Profit

Business Advisory

Net Profit % Change

from Master budget

3,000 840,000 3,600 192,000 127,133 64,867 0%

2,700 756,000 3,240 172,800 124,613 48,187 26%

2,400 672,000 2,880 153,600 122,093 31,507 51%

1,800 504,000 2,160 115,200 117,053 1,853- 103%

Task A

Budgeting and Sensitivity analysis

Schedule 1

BUDGET 2019

Taxation Bookkeeping Advisory Total

$ $ $ $

Billable hours 3,520 2,310 3000

Chargeout rate per billable hour 263$ 137$ 280$

Professional labour rate per hour 155$ 67$ 180$

Professional labour hours 4,224 2,772 3,600

Revenue 924,000 315,315 840,000 2,079,315

Professional labour costs 652,608 185,585 648,000 1,486,193

Gross margin 271,392 129,730 192,000 593,122

Office staff wages 56,667 56,667 56,667 170,000

Rent & Utilities 20,833 20,833 20,833 62,500

Printing & stationary 7,500 7,500 7,500 22,500

IT Support 6,600 6,600 6,600 19,800

Advertising 6,667 6,667 6,667 20,000

Depreciation 3,667 3,667 3,667 11,000

Client entertainment costs 27,720 9,459 25,200 62,379

Total Support costs 129,653 111,393 127,133 368,179

Budgeted Profit before tax 141,739 18,337 64,867 224,942

2019 Master Budget for T&K Accounting Services

Schedule 2

Budget Sensitivity Analysis - Business Advisory Department

Business Advisory

Billable hours

Business Advisory

Revenue

Business Advisory

Labour hours

Business Advisory

Gross Margin

Business Advisory

Support Costs

Business Advisory

Net Profit

Business Advisory

Net Profit % Change

from Master budget

3,000 840,000 3,600 192,000 127,133 64,867 0%

2,700 756,000 3,240 172,800 124,613 48,187 26%

2,400 672,000 2,880 153,600 122,093 31,507 51%

1,800 504,000 2,160 115,200 117,053 1,853- 103%

3ACCOUNTING FOR MANAGEMENT

Email to T & K

To,

Mr Thompson and Mr Chua

T & K Accounting Services

Brisbane,

Australia

To Whom It May Concern

This letter is to notify you that I has completed my research as you have asked for to review

and analyse the budget along with that I have also performed the sensitivity analysis of the

prepare budget. As per your requirement, this analysis is prepared to provide the

recommendation about the inclusion of the advisory department in the firm. This letter also

provide the details of the necessary actions, which can be taken by the firm in respect of the

inclusion of the advisory department in the firm. This recommendation and the suggested

steps are developed in the basis of the calculation and the analysis of the calculation done by

me. Here, I have calculated the budget for the advisory department in the basis of the budget

for the existing department and the estimated budget of the new advisory department.

The proper and the extensive calculation regarding the budget of the new department helps to

understand the situation in a better way. To analyse the any project the value comparison is

also a better way to proceed and this help to understand the value of the new project that is an

advisory department here. As per the value of the budget that is calculated to understand the

project, this is observed that the company earned the profit of $ 160,120 before implementing

the advisory department and cost of the profit for the company has around $ 223,380. Here,

Email to T & K

To,

Mr Thompson and Mr Chua

T & K Accounting Services

Brisbane,

Australia

To Whom It May Concern

This letter is to notify you that I has completed my research as you have asked for to review

and analyse the budget along with that I have also performed the sensitivity analysis of the

prepare budget. As per your requirement, this analysis is prepared to provide the

recommendation about the inclusion of the advisory department in the firm. This letter also

provide the details of the necessary actions, which can be taken by the firm in respect of the

inclusion of the advisory department in the firm. This recommendation and the suggested

steps are developed in the basis of the calculation and the analysis of the calculation done by

me. Here, I have calculated the budget for the advisory department in the basis of the budget

for the existing department and the estimated budget of the new advisory department.

The proper and the extensive calculation regarding the budget of the new department helps to

understand the situation in a better way. To analyse the any project the value comparison is

also a better way to proceed and this help to understand the value of the new project that is an

advisory department here. As per the value of the budget that is calculated to understand the

project, this is observed that the company earned the profit of $ 160,120 before implementing

the advisory department and cost of the profit for the company has around $ 223,380. Here,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING FOR MANAGEMENT

the profit margin for the company has been moderate and the cost for the profit is also under

the limit of the company.

Further, the calculated budget shows that the estimated profit of the firm after implementing

the new advisory department, will be increased to $ 224,942 and the cost for this profit

increase to the $ 368,179. This comparison of the value states that the profit of the firm will

increase and even the cost of the company to generating such profit will increase too.

Although, the percentage of the change is very minor.

Hence, this analysis and the calculation of the budget shows that the profitability of the firm

will increase by implementing the advisory department in the company as the profit before

tax of the company estimated to be more compared to the before implementing the

department in the firm. This implementation will also help the other department of the firm to

perform well as this department reduce the work- load of the other department too. Even this

help to reduce the requirement of the resources of the other department. Hence, it has been

suggested to the firm to imply the new advisory department in the firm as it is beneficial for

the company and will help the company to increase the efficiency and the performance of the

company as well. This letter also provides the detailed calculation herewith, kindly go throw

that to take the further require actions regarding the implication of the advisory department in

the firm.

Thanks and Regards,

Tony John

Date: - 24th May 2019

the profit margin for the company has been moderate and the cost for the profit is also under

the limit of the company.

Further, the calculated budget shows that the estimated profit of the firm after implementing

the new advisory department, will be increased to $ 224,942 and the cost for this profit

increase to the $ 368,179. This comparison of the value states that the profit of the firm will

increase and even the cost of the company to generating such profit will increase too.

Although, the percentage of the change is very minor.

Hence, this analysis and the calculation of the budget shows that the profitability of the firm

will increase by implementing the advisory department in the company as the profit before

tax of the company estimated to be more compared to the before implementing the

department in the firm. This implementation will also help the other department of the firm to

perform well as this department reduce the work- load of the other department too. Even this

help to reduce the requirement of the resources of the other department. Hence, it has been

suggested to the firm to imply the new advisory department in the firm as it is beneficial for

the company and will help the company to increase the efficiency and the performance of the

company as well. This letter also provides the detailed calculation herewith, kindly go throw

that to take the further require actions regarding the implication of the advisory department in

the firm.

Thanks and Regards,

Tony John

Date: - 24th May 2019

5ACCOUNTING FOR MANAGEMENT

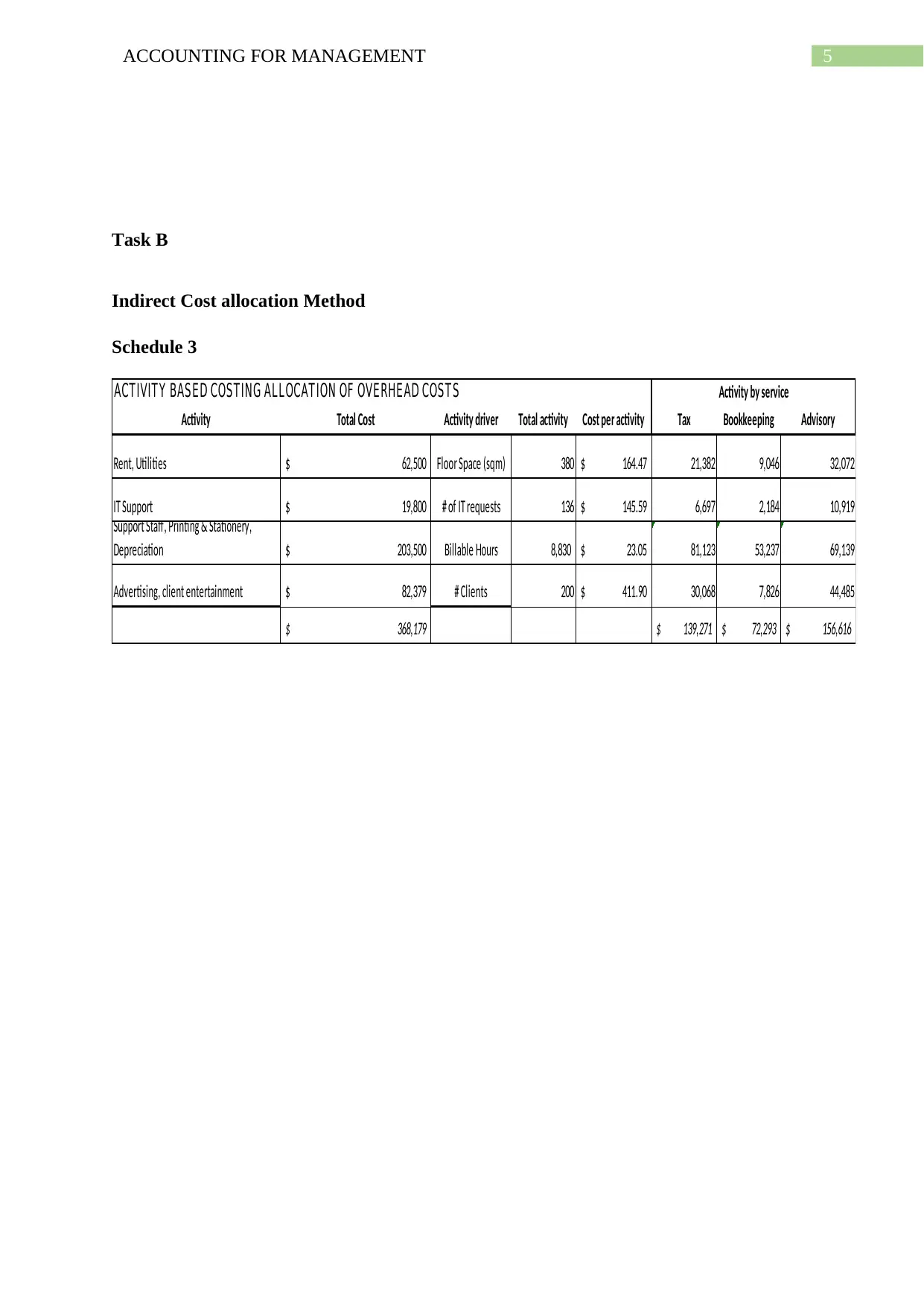

Task B

Indirect Cost allocation Method

Schedule 3

ACT IVIT Y BAS E D COS T ING AL L OCAT ION OF OVE RHE AD COS T S

Activity Total Cost Activity driver Total activity Cost per activity Tax Bookkeeping Advisory

Rent, Utilities 62,500$ Floor Space (sqm) 380 164.47$ 21,382 9,046 32,072

IT Support 19,800$ # of IT requests 136 145.59$ 6,697 2,184 10,919

Support Staff, Printing & Stationery,

Depreciation 203,500$ Billable Hours 8,830 23.05$ 81,123 53,237 69,139

Advertising, client entertainment 82,379$ # Clients 200 411.90$ 30,068 7,826 44,485

368,179$ 139,271$ 72,293$ 156,616$

Activity by service

Task B

Indirect Cost allocation Method

Schedule 3

ACT IVIT Y BAS E D COS T ING AL L OCAT ION OF OVE RHE AD COS T S

Activity Total Cost Activity driver Total activity Cost per activity Tax Bookkeeping Advisory

Rent, Utilities 62,500$ Floor Space (sqm) 380 164.47$ 21,382 9,046 32,072

IT Support 19,800$ # of IT requests 136 145.59$ 6,697 2,184 10,919

Support Staff, Printing & Stationery,

Depreciation 203,500$ Billable Hours 8,830 23.05$ 81,123 53,237 69,139

Advertising, client entertainment 82,379$ # Clients 200 411.90$ 30,068 7,826 44,485

368,179$ 139,271$ 72,293$ 156,616$

Activity by service

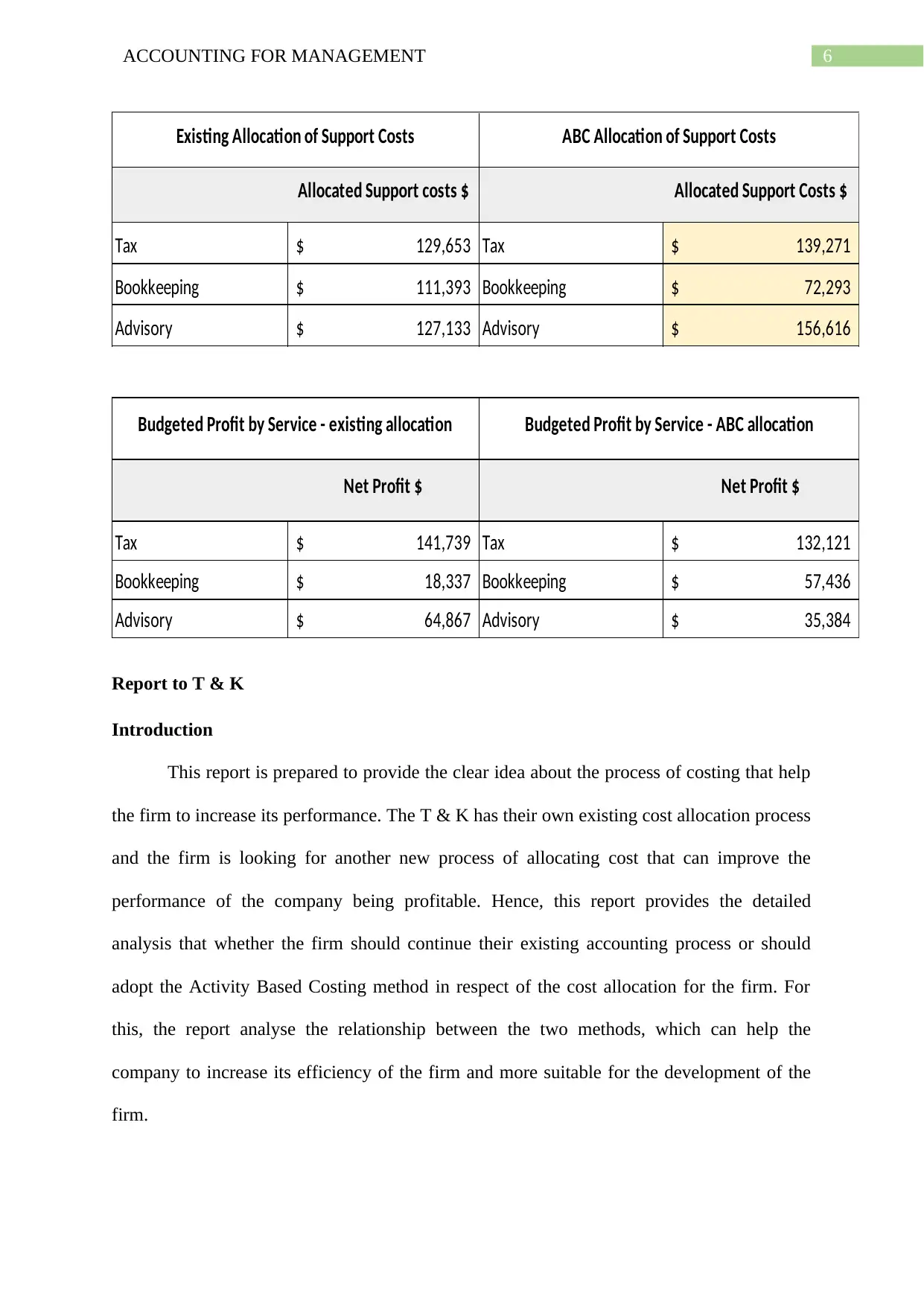

6ACCOUNTING FOR MANAGEMENT

Allocated Support costs $ Allocated Support Costs $

Tax 129,653$ Tax 139,271$

Bookkeeping 111,393$ Bookkeeping 72,293$

Advisory 127,133$ Advisory 156,616$

Net Profit $ Net Profit $

Tax 141,739$ Tax 132,121$

Bookkeeping 18,337$ Bookkeeping 57,436$

Advisory 64,867$ Advisory 35,384$

Existing Allocation of Support Costs ABC Allocation of Support Costs

Budgeted Profit by Service - existing allocation Budgeted Profit by Service - ABC allocation

Report to T & K

Introduction

This report is prepared to provide the clear idea about the process of costing that help

the firm to increase its performance. The T & K has their own existing cost allocation process

and the firm is looking for another new process of allocating cost that can improve the

performance of the company being profitable. Hence, this report provides the detailed

analysis that whether the firm should continue their existing accounting process or should

adopt the Activity Based Costing method in respect of the cost allocation for the firm. For

this, the report analyse the relationship between the two methods, which can help the

company to increase its efficiency of the firm and more suitable for the development of the

firm.

Allocated Support costs $ Allocated Support Costs $

Tax 129,653$ Tax 139,271$

Bookkeeping 111,393$ Bookkeeping 72,293$

Advisory 127,133$ Advisory 156,616$

Net Profit $ Net Profit $

Tax 141,739$ Tax 132,121$

Bookkeeping 18,337$ Bookkeeping 57,436$

Advisory 64,867$ Advisory 35,384$

Existing Allocation of Support Costs ABC Allocation of Support Costs

Budgeted Profit by Service - existing allocation Budgeted Profit by Service - ABC allocation

Report to T & K

Introduction

This report is prepared to provide the clear idea about the process of costing that help

the firm to increase its performance. The T & K has their own existing cost allocation process

and the firm is looking for another new process of allocating cost that can improve the

performance of the company being profitable. Hence, this report provides the detailed

analysis that whether the firm should continue their existing accounting process or should

adopt the Activity Based Costing method in respect of the cost allocation for the firm. For

this, the report analyse the relationship between the two methods, which can help the

company to increase its efficiency of the firm and more suitable for the development of the

firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGEMENT

Discussion

The Activity Based Costing is a new tool that allocates the direct cost of production to

the products in a prescribed manner. This tool allocates the cost of production in the basis of

the dependent hours of the product (Childress et al, 2015). The activity based costing initially

allocates the production cost to the operations as the operations of the company is the main

reason behind the production cost. The activity cost of the firm is allocated to the products in

the basis of the level of demand made by the product for the activity process. Currently, the

firm is using the conventional costing process in production process. The comparison of the

current cost of production for the firm and the profit in existing cost process and the

estimated cost of production and the profit under the activity based costing. This comparison

will help the company to understand that whether the existing costing method is profitable or

the activity based costing is more profitable for the firm (Iswahyudi, Azis & Santosa, 2017).

In the existing method of the costing, the firm incurred the $ 129,653, $ 111,293 and $

127,133 for three departments and profit of the same departments was $ 141,739, $ 18,337

and $ 64,867. On other hand, it is estimated that the cost of the company will become $

139,271, $ 72,293 and $ 156,616 and the profit of the department will increase to $ 132,121,

$ 57,436 and $ 35,384 for the three department in the activity based accounting.

In the basis of the above comprising, this report recommends the firm to adopt the

activity based costing to allocate the cost of the production among the products. As in this

process the cost of the production will decreased and the profit of the firm will increase as per

the expected value.

Conclusion

The report concludes that the T & K firm follows the conventional method for

allocating the cost of production among the products and looking for the new efficient

method of allocating the cost that can increase the performance of the firm. This report

Discussion

The Activity Based Costing is a new tool that allocates the direct cost of production to

the products in a prescribed manner. This tool allocates the cost of production in the basis of

the dependent hours of the product (Childress et al, 2015). The activity based costing initially

allocates the production cost to the operations as the operations of the company is the main

reason behind the production cost. The activity cost of the firm is allocated to the products in

the basis of the level of demand made by the product for the activity process. Currently, the

firm is using the conventional costing process in production process. The comparison of the

current cost of production for the firm and the profit in existing cost process and the

estimated cost of production and the profit under the activity based costing. This comparison

will help the company to understand that whether the existing costing method is profitable or

the activity based costing is more profitable for the firm (Iswahyudi, Azis & Santosa, 2017).

In the existing method of the costing, the firm incurred the $ 129,653, $ 111,293 and $

127,133 for three departments and profit of the same departments was $ 141,739, $ 18,337

and $ 64,867. On other hand, it is estimated that the cost of the company will become $

139,271, $ 72,293 and $ 156,616 and the profit of the department will increase to $ 132,121,

$ 57,436 and $ 35,384 for the three department in the activity based accounting.

In the basis of the above comprising, this report recommends the firm to adopt the

activity based costing to allocate the cost of the production among the products. As in this

process the cost of the production will decreased and the profit of the firm will increase as per

the expected value.

Conclusion

The report concludes that the T & K firm follows the conventional method for

allocating the cost of production among the products and looking for the new efficient

method of allocating the cost that can increase the performance of the firm. This report

8ACCOUNTING FOR MANAGEMENT

compare the cost of production under the existing method of the firm and the cost and profit

of the firm under activity based costing to recommend the best method of the costing to the

firm. Lastly, this report recommends the activity based costing to the T & K as in this process

the profit of the firm is more than the existing method of costing.

compare the cost of production under the existing method of the firm and the cost and profit

of the firm under activity based costing to recommend the best method of the costing to the

firm. Lastly, this report recommends the activity based costing to the T & K as in this process

the profit of the firm is more than the existing method of costing.

9ACCOUNTING FOR MANAGEMENT

Reference and Bibliography

Holzer, M., Mullins, L. B., Ferreira, M., & Hoontis, P. (2016). Implementing performance

budgeting at the state level: Lessons learned from New Jersey. International Journal

of Public Administration, 39(2), 95-106.

Henttu-Aho, T. (2016). Enabling characteristics of new budgeting practice and the role of

controller. Qualitative Research in Accounting & Management, 13(1), 31-56.

Childress, S., Nichols, B., Charlton, B., & Coe, S. (2015). Using an activity-based model to

explore the potential impacts of automated vehicles. Transportation Research

Record, 2493(1), 99-106

Iswahyudi, B. E., Azis, S., & Santosa, A. A. (2017). Analysis of Contruction Cost Efficiency

Between Precast Method and Conventional Method in Building Project. International

Journal of Technology and Sciences, 1(1).

Reference and Bibliography

Holzer, M., Mullins, L. B., Ferreira, M., & Hoontis, P. (2016). Implementing performance

budgeting at the state level: Lessons learned from New Jersey. International Journal

of Public Administration, 39(2), 95-106.

Henttu-Aho, T. (2016). Enabling characteristics of new budgeting practice and the role of

controller. Qualitative Research in Accounting & Management, 13(1), 31-56.

Childress, S., Nichols, B., Charlton, B., & Coe, S. (2015). Using an activity-based model to

explore the potential impacts of automated vehicles. Transportation Research

Record, 2493(1), 99-106

Iswahyudi, B. E., Azis, S., & Santosa, A. A. (2017). Analysis of Contruction Cost Efficiency

Between Precast Method and Conventional Method in Building Project. International

Journal of Technology and Sciences, 1(1).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.