Accounting for Managers Assignment: Financial Ratio Analysis Report

VerifiedAdded on 2023/06/08

|10

|1921

|327

Report

AI Summary

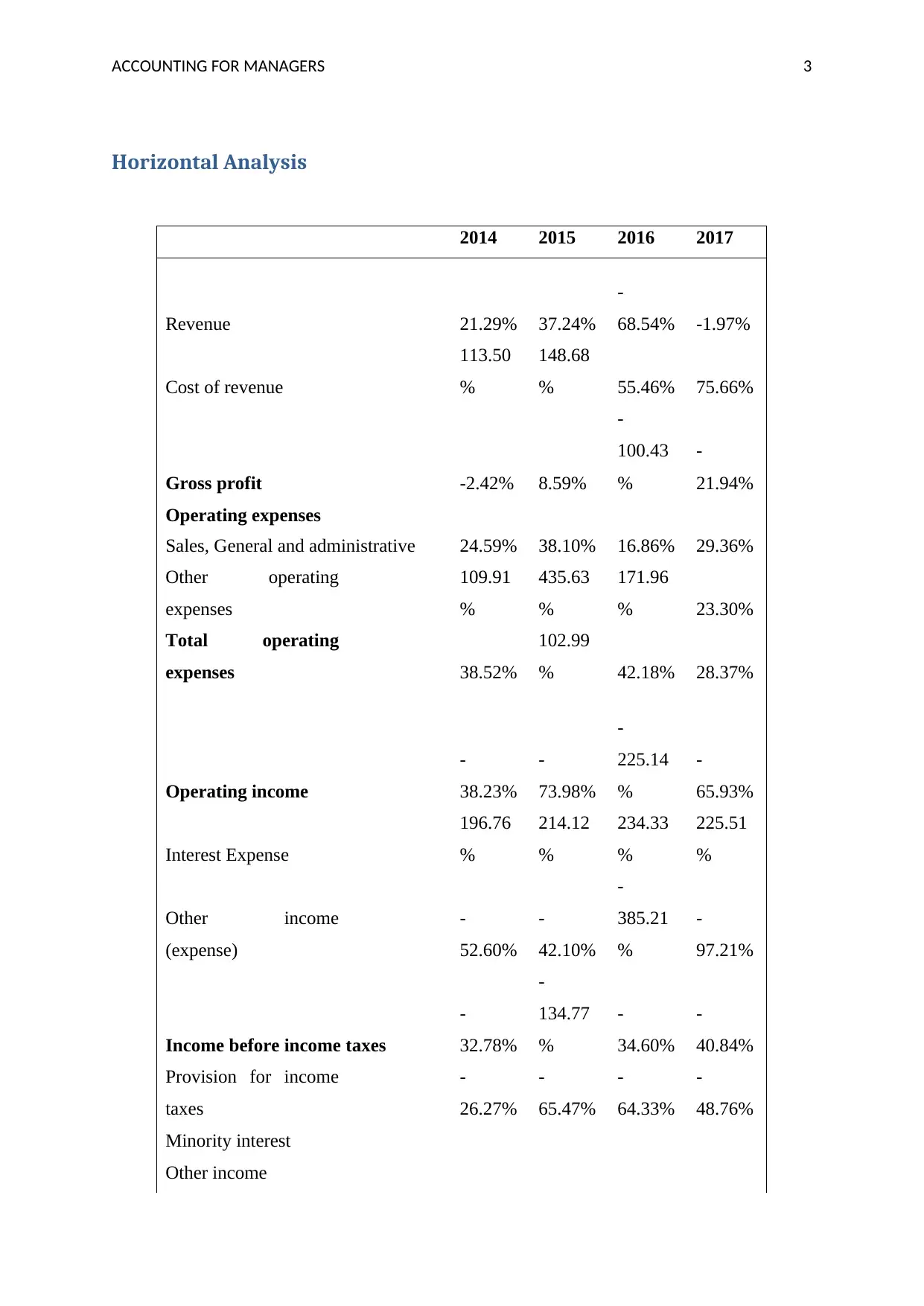

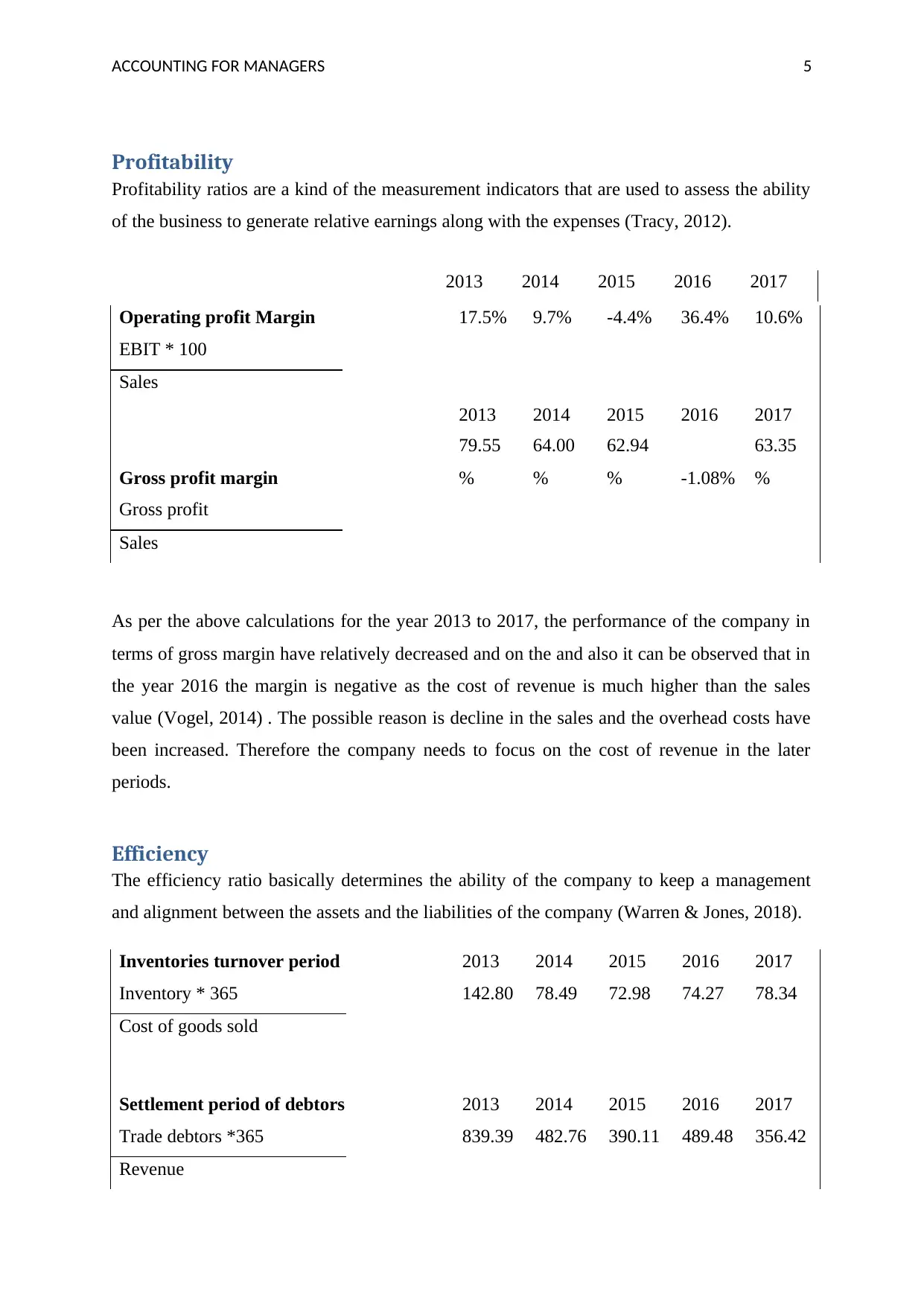

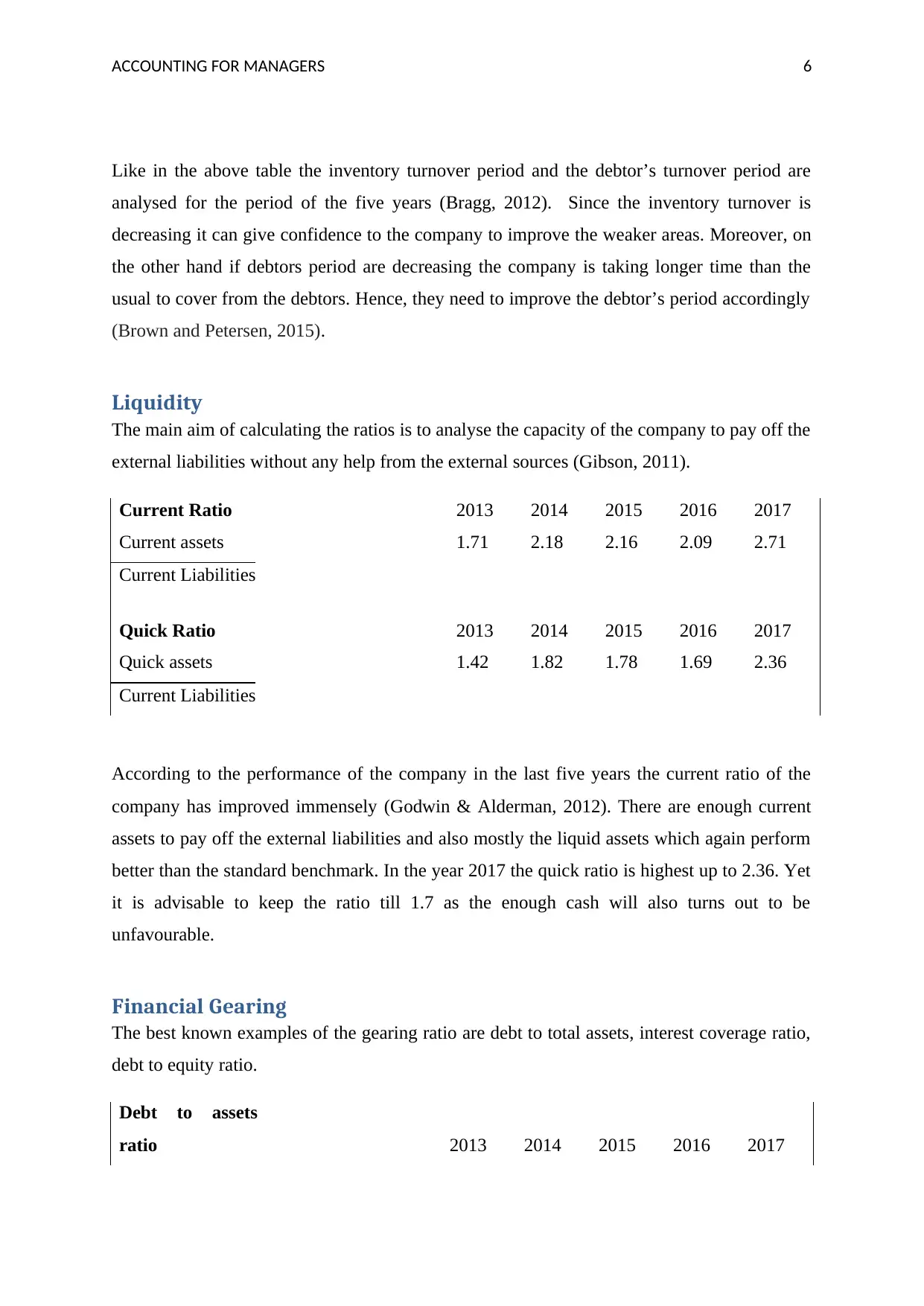

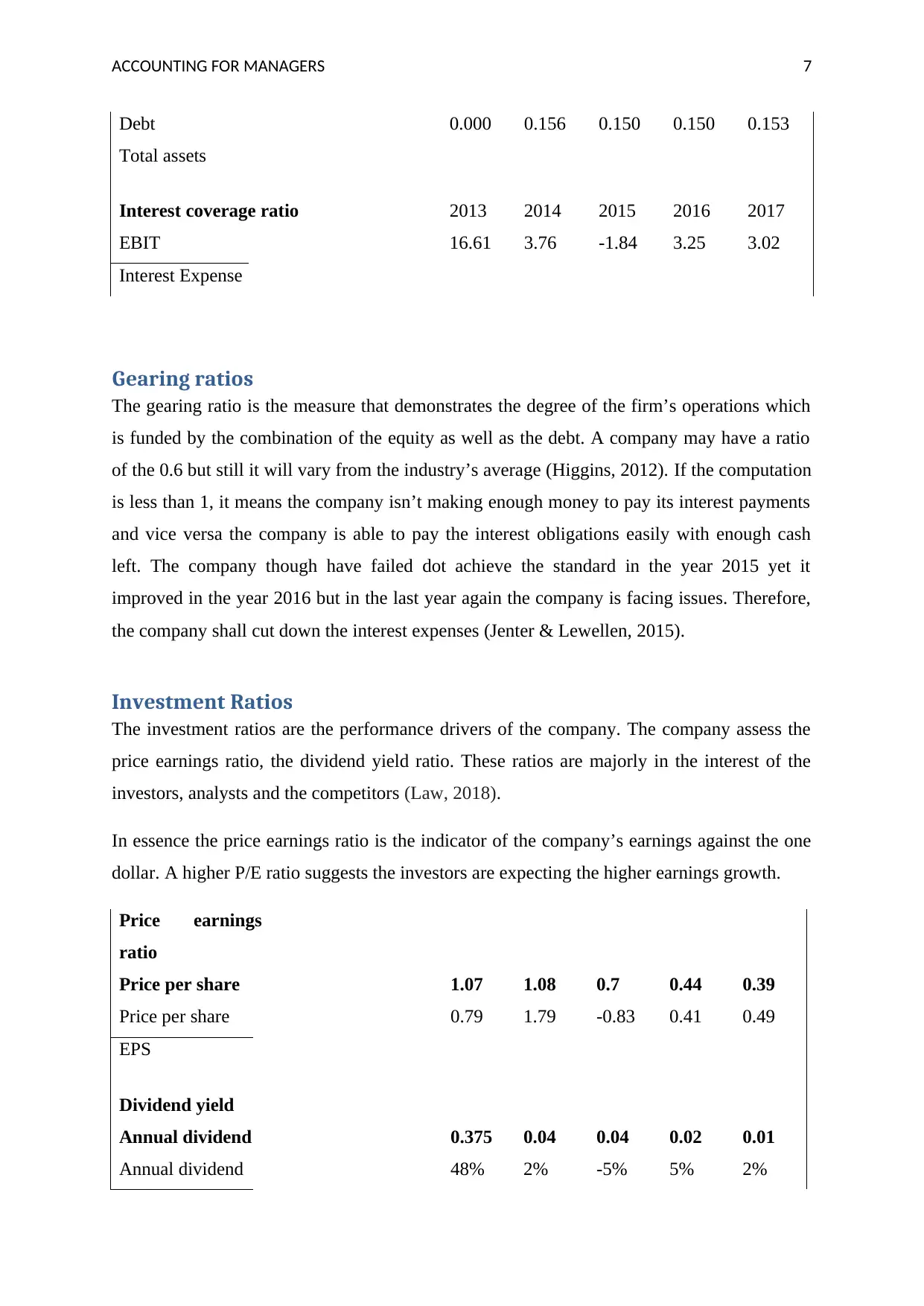

This report presents a comprehensive financial analysis of Cash Converters International Ltd (CCV), covering the period from 2013 to 2017. The analysis begins with a horizontal analysis of the income statement, examining revenue, cost of revenue, operating expenses, and net income trends to identify key changes and performance drivers. The report then delves into profitability ratios, including operating profit margin and gross profit margin, to assess CCV's ability to generate earnings relative to its expenses. Efficiency ratios, such as inventory turnover and debtor turnover periods, are calculated to evaluate the company's asset and liability management. Liquidity ratios, including the current and quick ratios, are used to assess CCV's ability to meet its short-term obligations. Financial gearing ratios, like debt to total assets and interest coverage ratio, are calculated to determine the extent to which CCV uses debt financing. Finally, investment ratios, including price-earnings ratio and dividend yield, are analyzed to evaluate the company's performance from an investor's perspective. The report uses data from CCV's annual reports and provides insights into the company's financial health and key performance indicators.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.