ACC00724 Accounting for Managers: A Financial Report on JB Hi-Fi

VerifiedAdded on 2023/06/09

|8

|1565

|231

Report

AI Summary

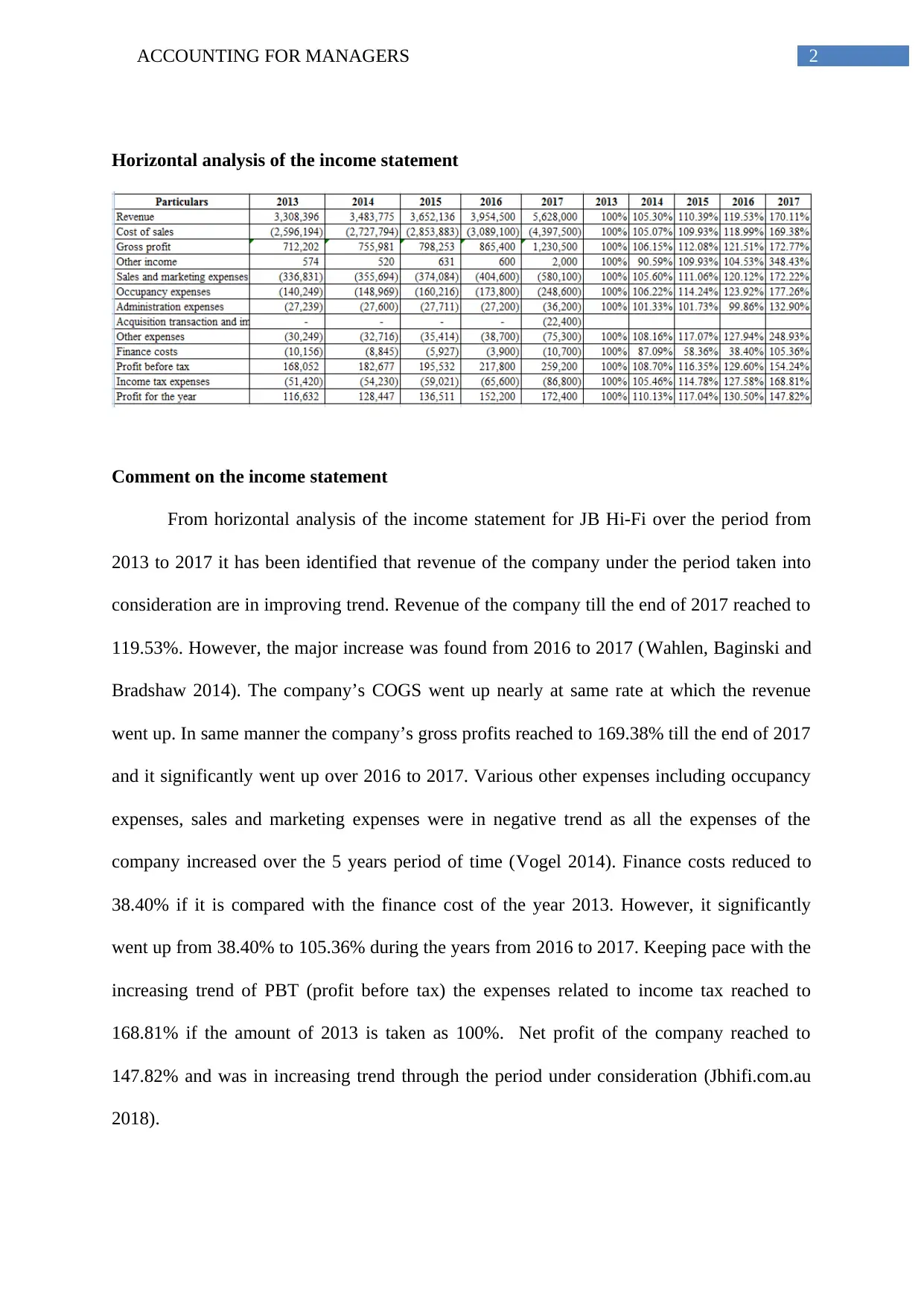

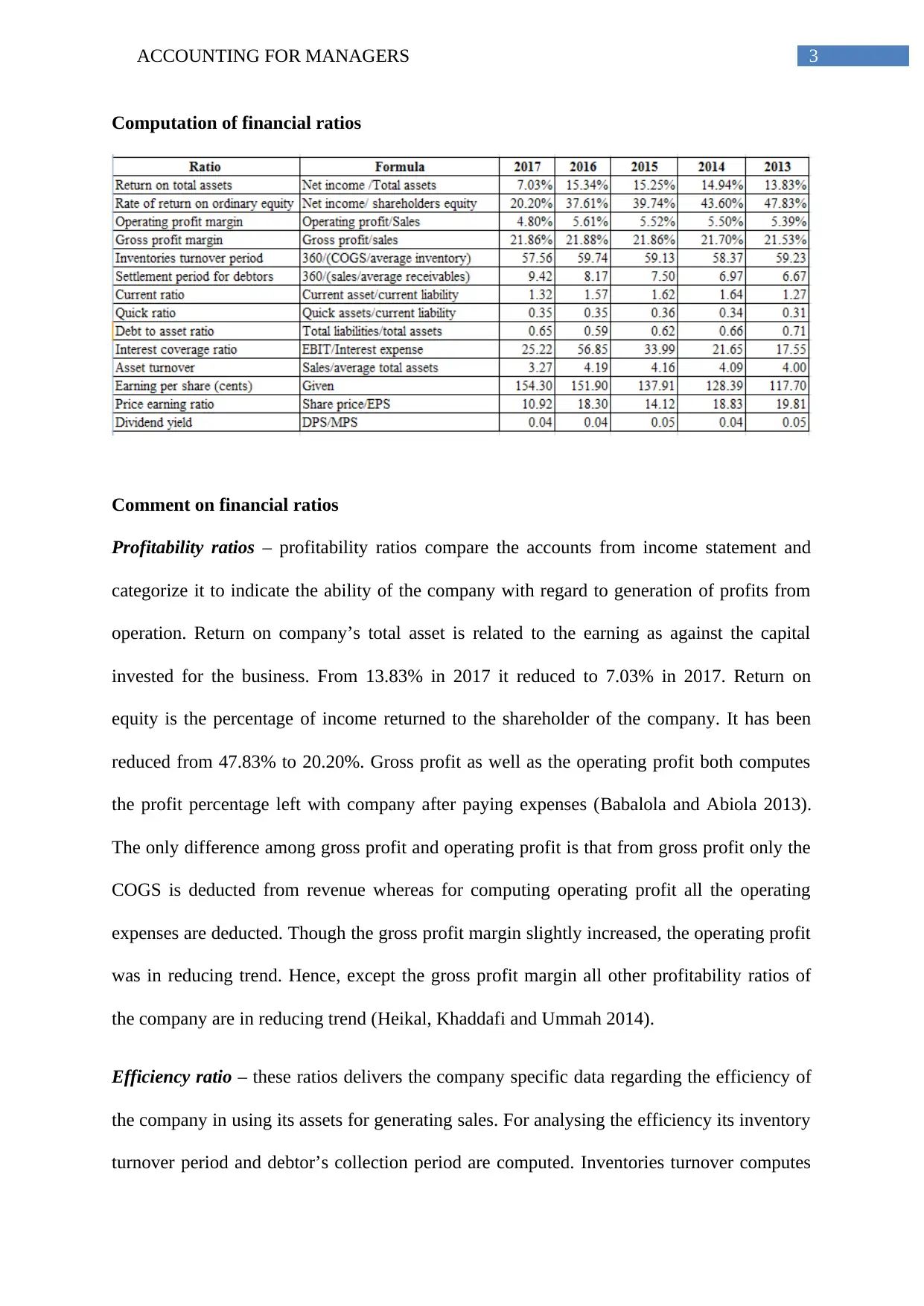

This report provides a comprehensive financial analysis of JB Hi-Fi Ltd from 2013 to 2017. It includes a horizontal analysis of the income statement, highlighting revenue growth and expense trends. Key financial ratios such as profitability, efficiency, liquidity, financial gearing, and investment ratios are computed and analyzed to assess the company's financial health and performance. The analysis covers return on assets, return on equity, gross profit margin, operating profit, inventory turnover, debtor's collection period, current ratio, quick ratio, debt to asset ratio, interest coverage ratio, assets turnover ratio, earnings per share, and dividend yield. The report concludes with an overall assessment of JB Hi-Fi's financial position and its ability to meet its obligations and generate returns for investors. Desklib offers more solved assignments and resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.