Preparation of Accounting Records using Spreadsheets

VerifiedAdded on 2023/04/21

|17

|4867

|127

AI Summary

This document provides a detailed explanation of how to prepare accounting records using spreadsheets. It includes examples of journal entries, ledger accounts, and adjusting entries. The document also discusses the types of adjusting entries and provides a worksheet, statement of profit/loss, balance sheet, and statement of changes in equity.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING FOR

MANAGERS

ASSIGNMENT

MANAGERS

ASSIGNMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Question 1: Preparation of accounting records – using spreadsheets.........................................................3

Question 2: History of accounting - essay..................................................................................................10

Question 3: ABC Learning Case Study........................................................................................................12

References.................................................................................................................................................15

2 | P a g e

Contents

Question 1: Preparation of accounting records – using spreadsheets.........................................................3

Question 2: History of accounting - essay..................................................................................................10

Question 3: ABC Learning Case Study........................................................................................................12

References.................................................................................................................................................15

2 | P a g e

3

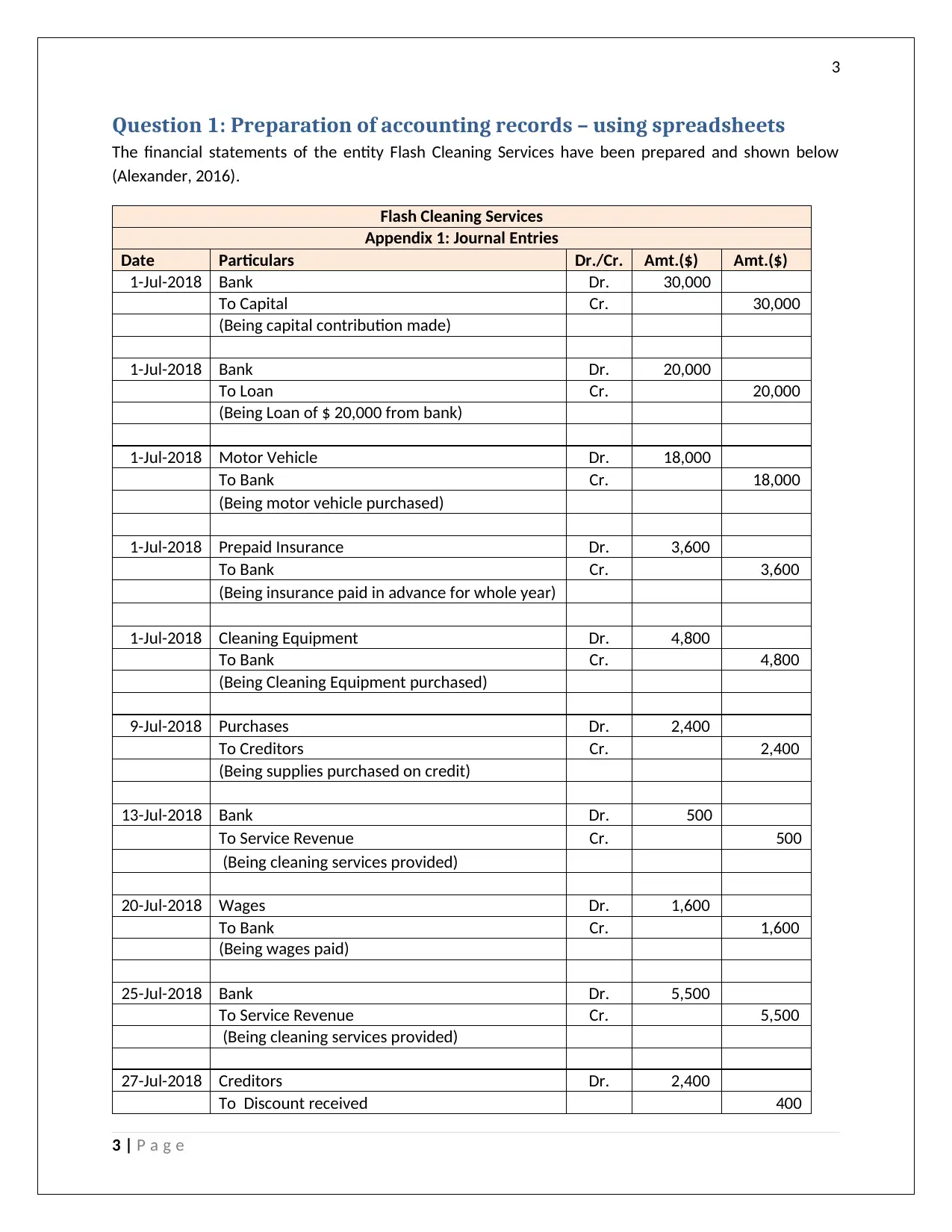

Question 1: Preparation of accounting records – using spreadsheets

The financial statements of the entity Flash Cleaning Services have been prepared and shown below

(Alexander, 2016).

Flash Cleaning Services

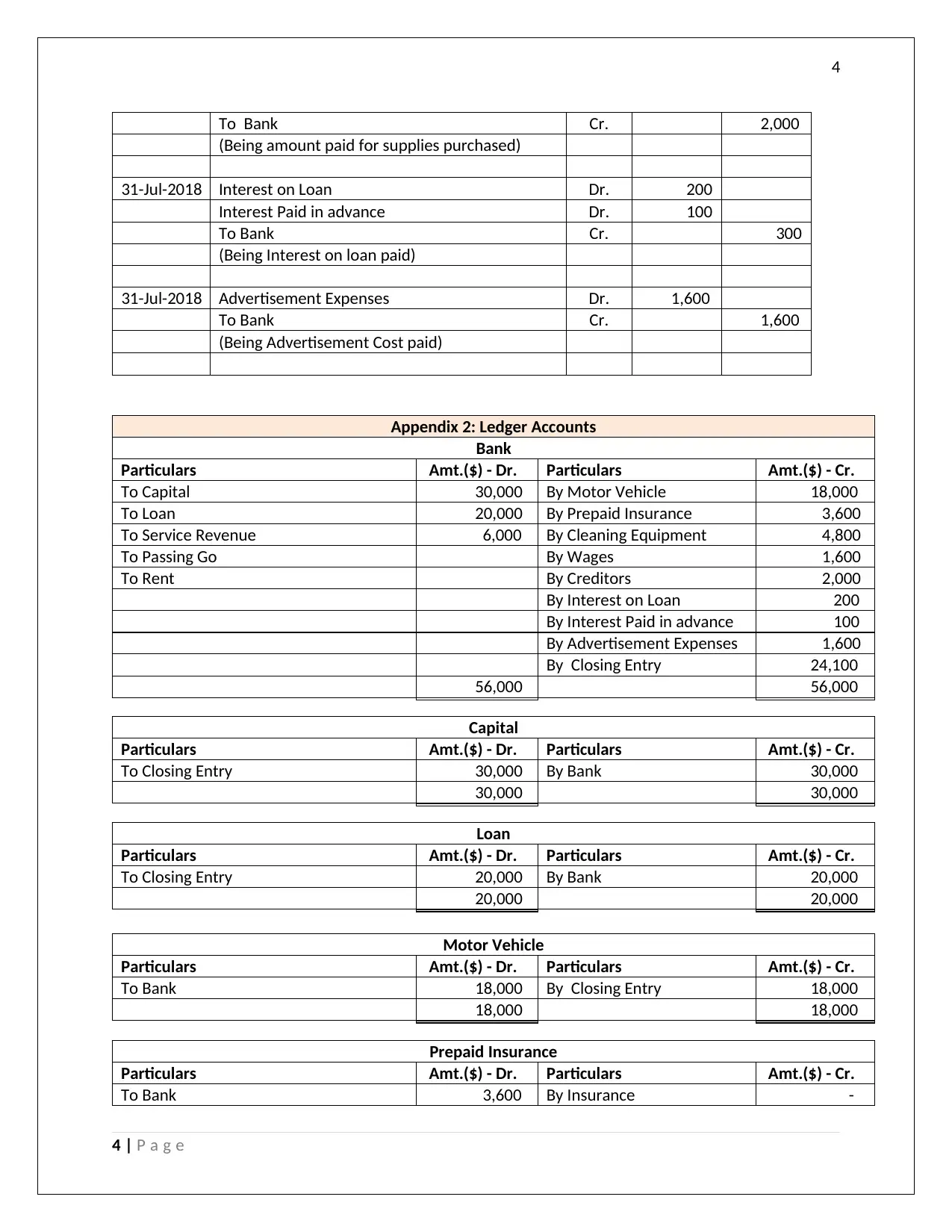

Appendix 1: Journal Entries

Date Particulars Dr./Cr. Amt.($) Amt.($)

1-Jul-2018 Bank Dr. 30,000

To Capital Cr. 30,000

(Being capital contribution made)

1-Jul-2018 Bank Dr. 20,000

To Loan Cr. 20,000

(Being Loan of $ 20,000 from bank)

1-Jul-2018 Motor Vehicle Dr. 18,000

To Bank Cr. 18,000

(Being motor vehicle purchased)

1-Jul-2018 Prepaid Insurance Dr. 3,600

To Bank Cr. 3,600

(Being insurance paid in advance for whole year)

1-Jul-2018 Cleaning Equipment Dr. 4,800

To Bank Cr. 4,800

(Being Cleaning Equipment purchased)

9-Jul-2018 Purchases Dr. 2,400

To Creditors Cr. 2,400

(Being supplies purchased on credit)

13-Jul-2018 Bank Dr. 500

To Service Revenue Cr. 500

(Being cleaning services provided)

20-Jul-2018 Wages Dr. 1,600

To Bank Cr. 1,600

(Being wages paid)

25-Jul-2018 Bank Dr. 5,500

To Service Revenue Cr. 5,500

(Being cleaning services provided)

27-Jul-2018 Creditors Dr. 2,400

To Discount received 400

3 | P a g e

Question 1: Preparation of accounting records – using spreadsheets

The financial statements of the entity Flash Cleaning Services have been prepared and shown below

(Alexander, 2016).

Flash Cleaning Services

Appendix 1: Journal Entries

Date Particulars Dr./Cr. Amt.($) Amt.($)

1-Jul-2018 Bank Dr. 30,000

To Capital Cr. 30,000

(Being capital contribution made)

1-Jul-2018 Bank Dr. 20,000

To Loan Cr. 20,000

(Being Loan of $ 20,000 from bank)

1-Jul-2018 Motor Vehicle Dr. 18,000

To Bank Cr. 18,000

(Being motor vehicle purchased)

1-Jul-2018 Prepaid Insurance Dr. 3,600

To Bank Cr. 3,600

(Being insurance paid in advance for whole year)

1-Jul-2018 Cleaning Equipment Dr. 4,800

To Bank Cr. 4,800

(Being Cleaning Equipment purchased)

9-Jul-2018 Purchases Dr. 2,400

To Creditors Cr. 2,400

(Being supplies purchased on credit)

13-Jul-2018 Bank Dr. 500

To Service Revenue Cr. 500

(Being cleaning services provided)

20-Jul-2018 Wages Dr. 1,600

To Bank Cr. 1,600

(Being wages paid)

25-Jul-2018 Bank Dr. 5,500

To Service Revenue Cr. 5,500

(Being cleaning services provided)

27-Jul-2018 Creditors Dr. 2,400

To Discount received 400

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

To Bank Cr. 2,000

(Being amount paid for supplies purchased)

31-Jul-2018 Interest on Loan Dr. 200

Interest Paid in advance Dr. 100

To Bank Cr. 300

(Being Interest on loan paid)

31-Jul-2018 Advertisement Expenses Dr. 1,600

To Bank Cr. 1,600

(Being Advertisement Cost paid)

Appendix 2: Ledger Accounts

Bank

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Capital 30,000 By Motor Vehicle 18,000

To Loan 20,000 By Prepaid Insurance 3,600

To Service Revenue 6,000 By Cleaning Equipment 4,800

To Passing Go By Wages 1,600

To Rent By Creditors 2,000

By Interest on Loan 200

By Interest Paid in advance 100

By Advertisement Expenses 1,600

By Closing Entry 24,100

56,000 56,000

Capital

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 30,000 By Bank 30,000

30,000 30,000

Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 20,000 By Bank 20,000

20,000 20,000

Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 18,000 By Closing Entry 18,000

18,000 18,000

Prepaid Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 3,600 By Insurance -

4 | P a g e

To Bank Cr. 2,000

(Being amount paid for supplies purchased)

31-Jul-2018 Interest on Loan Dr. 200

Interest Paid in advance Dr. 100

To Bank Cr. 300

(Being Interest on loan paid)

31-Jul-2018 Advertisement Expenses Dr. 1,600

To Bank Cr. 1,600

(Being Advertisement Cost paid)

Appendix 2: Ledger Accounts

Bank

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Capital 30,000 By Motor Vehicle 18,000

To Loan 20,000 By Prepaid Insurance 3,600

To Service Revenue 6,000 By Cleaning Equipment 4,800

To Passing Go By Wages 1,600

To Rent By Creditors 2,000

By Interest on Loan 200

By Interest Paid in advance 100

By Advertisement Expenses 1,600

By Closing Entry 24,100

56,000 56,000

Capital

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 30,000 By Bank 30,000

30,000 30,000

Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 20,000 By Bank 20,000

20,000 20,000

Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 18,000 By Closing Entry 18,000

18,000 18,000

Prepaid Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 3,600 By Insurance -

4 | P a g e

5

By Closing Entry 3,600

3,600 3,600

Cleaning Equipment

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 4,800 By Closing Entry 4,800

4,800 4,800

Purchase

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Creditors 2,400 By Closing Entry 2,400

2,400 2,400

Creditors

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Discount Received 400 By Purchase 2,400

To Bank 2,000

To Closing Entry -

2,400 2,400

Service Revenue

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To income received in advance - By Bank 6,000

To Closing Entry 6,000 By Accounts Receivable -

6,000 6,000

Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

To Outstanding Expenses -

1,600 1,600

Discount Received

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 400 By Creditors 400

400 400

Interest on Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 200 By Closing Entry 200

200 200

Interest Paid in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 100 By Closing Entry 100

100 100

5 | P a g e

By Closing Entry 3,600

3,600 3,600

Cleaning Equipment

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 4,800 By Closing Entry 4,800

4,800 4,800

Purchase

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Creditors 2,400 By Closing Entry 2,400

2,400 2,400

Creditors

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Discount Received 400 By Purchase 2,400

To Bank 2,000

To Closing Entry -

2,400 2,400

Service Revenue

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To income received in advance - By Bank 6,000

To Closing Entry 6,000 By Accounts Receivable -

6,000 6,000

Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

To Outstanding Expenses -

1,600 1,600

Discount Received

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 400 By Creditors 400

400 400

Interest on Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 200 By Closing Entry 200

200 200

Interest Paid in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 100 By Closing Entry 100

100 100

5 | P a g e

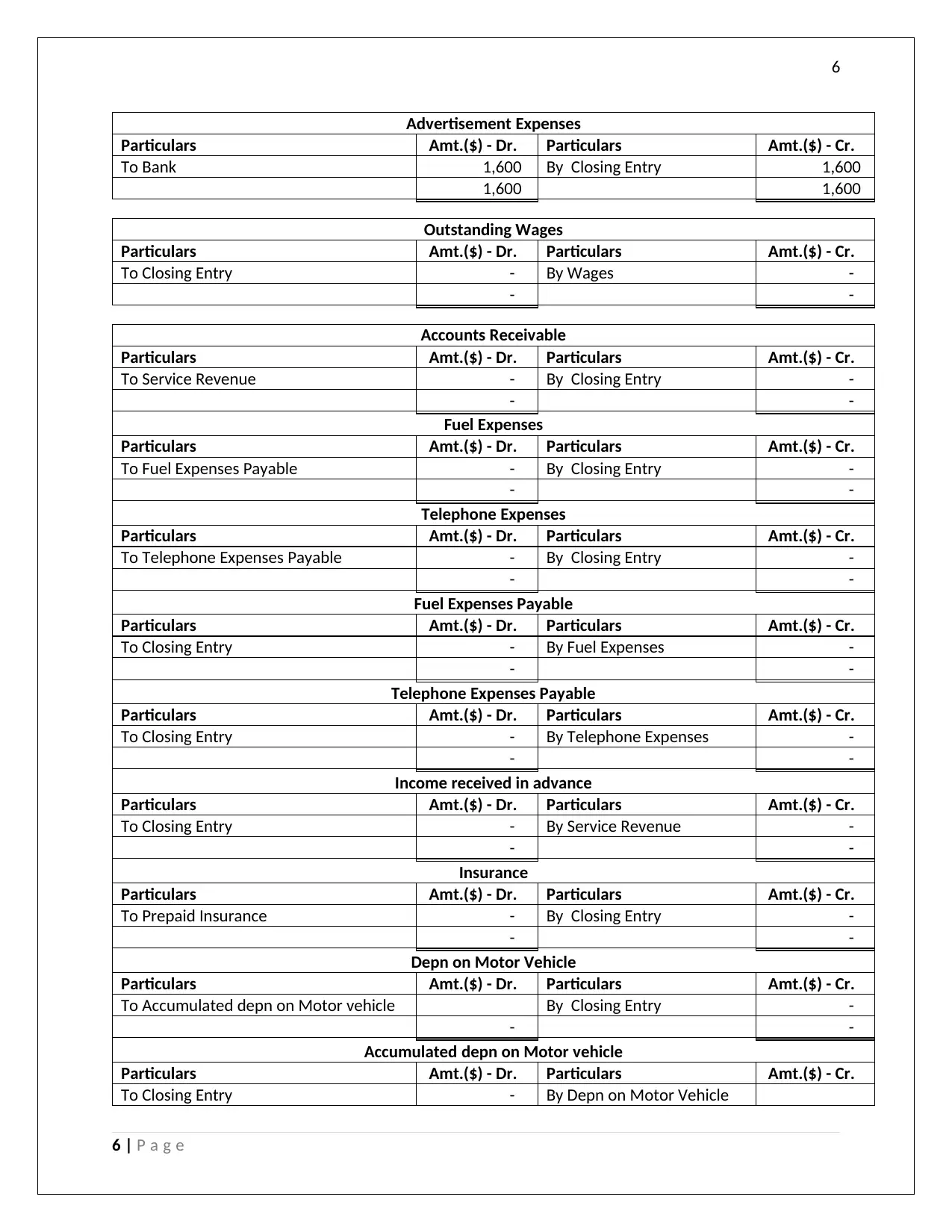

6

Advertisement Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

1,600 1,600

Outstanding Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Wages -

- -

Accounts Receivable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Service Revenue - By Closing Entry -

- -

Fuel Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Fuel Expenses Payable - By Closing Entry -

- -

Telephone Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Telephone Expenses Payable - By Closing Entry -

- -

Fuel Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Fuel Expenses -

- -

Telephone Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Telephone Expenses -

- -

Income received in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Service Revenue -

- -

Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Prepaid Insurance - By Closing Entry -

- -

Depn on Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Accumulated depn on Motor vehicle By Closing Entry -

- -

Accumulated depn on Motor vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Depn on Motor Vehicle

6 | P a g e

Advertisement Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

1,600 1,600

Outstanding Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Wages -

- -

Accounts Receivable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Service Revenue - By Closing Entry -

- -

Fuel Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Fuel Expenses Payable - By Closing Entry -

- -

Telephone Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Telephone Expenses Payable - By Closing Entry -

- -

Fuel Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Fuel Expenses -

- -

Telephone Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Telephone Expenses -

- -

Income received in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Service Revenue -

- -

Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Prepaid Insurance - By Closing Entry -

- -

Depn on Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Accumulated depn on Motor vehicle By Closing Entry -

- -

Accumulated depn on Motor vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Depn on Motor Vehicle

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

- -

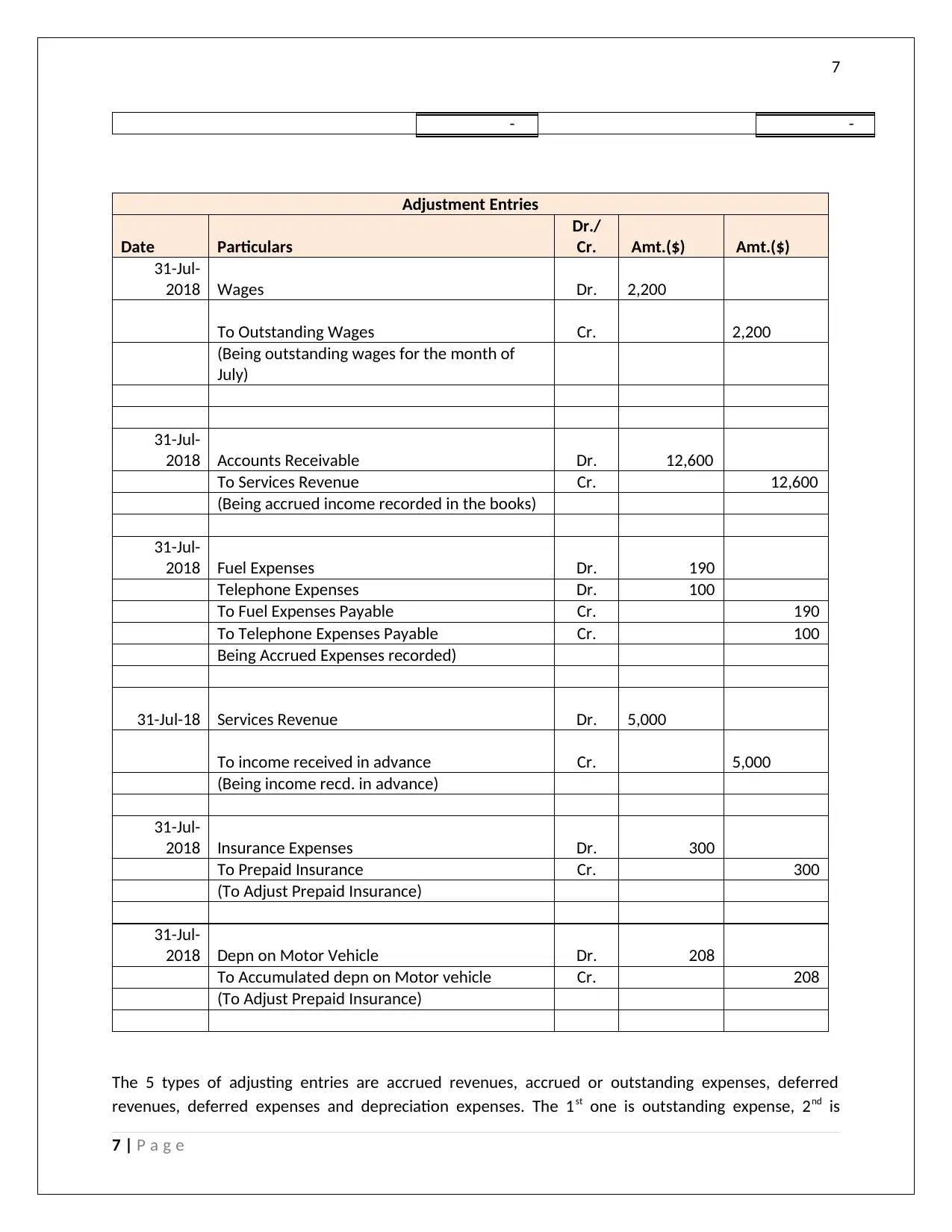

Adjustment Entries

Date Particulars

Dr./

Cr. Amt.($) Amt.($)

31-Jul-

2018 Wages Dr. 2,200

To Outstanding Wages Cr. 2,200

(Being outstanding wages for the month of

July)

31-Jul-

2018 Accounts Receivable Dr. 12,600

To Services Revenue Cr. 12,600

(Being accrued income recorded in the books)

31-Jul-

2018 Fuel Expenses Dr. 190

Telephone Expenses Dr. 100

To Fuel Expenses Payable Cr. 190

To Telephone Expenses Payable Cr. 100

Being Accrued Expenses recorded)

31-Jul-18 Services Revenue Dr. 5,000

To income received in advance Cr. 5,000

(Being income recd. in advance)

31-Jul-

2018 Insurance Expenses Dr. 300

To Prepaid Insurance Cr. 300

(To Adjust Prepaid Insurance)

31-Jul-

2018 Depn on Motor Vehicle Dr. 208

To Accumulated depn on Motor vehicle Cr. 208

(To Adjust Prepaid Insurance)

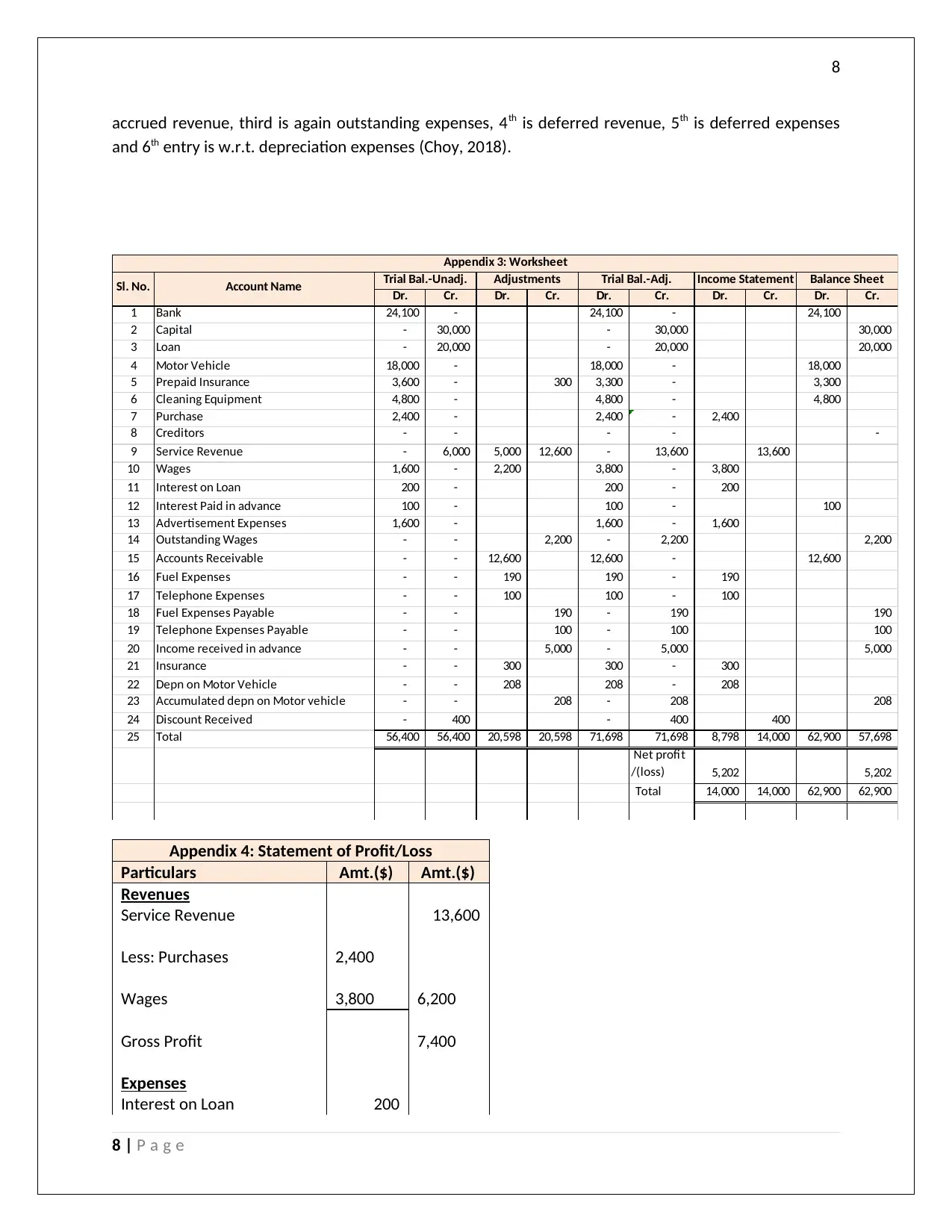

The 5 types of adjusting entries are accrued revenues, accrued or outstanding expenses, deferred

revenues, deferred expenses and depreciation expenses. The 1st one is outstanding expense, 2nd is

7 | P a g e

- -

Adjustment Entries

Date Particulars

Dr./

Cr. Amt.($) Amt.($)

31-Jul-

2018 Wages Dr. 2,200

To Outstanding Wages Cr. 2,200

(Being outstanding wages for the month of

July)

31-Jul-

2018 Accounts Receivable Dr. 12,600

To Services Revenue Cr. 12,600

(Being accrued income recorded in the books)

31-Jul-

2018 Fuel Expenses Dr. 190

Telephone Expenses Dr. 100

To Fuel Expenses Payable Cr. 190

To Telephone Expenses Payable Cr. 100

Being Accrued Expenses recorded)

31-Jul-18 Services Revenue Dr. 5,000

To income received in advance Cr. 5,000

(Being income recd. in advance)

31-Jul-

2018 Insurance Expenses Dr. 300

To Prepaid Insurance Cr. 300

(To Adjust Prepaid Insurance)

31-Jul-

2018 Depn on Motor Vehicle Dr. 208

To Accumulated depn on Motor vehicle Cr. 208

(To Adjust Prepaid Insurance)

The 5 types of adjusting entries are accrued revenues, accrued or outstanding expenses, deferred

revenues, deferred expenses and depreciation expenses. The 1st one is outstanding expense, 2nd is

7 | P a g e

8

accrued revenue, third is again outstanding expenses, 4th is deferred revenue, 5th is deferred expenses

and 6th entry is w.r.t. depreciation expenses (Choy, 2018).

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

1 Bank 24,100 - 24,100 - 24,100

2 Capital - 30,000 - 30,000 30,000

3 Loan - 20,000 - 20,000 20,000

4 Motor Vehicle 18,000 - 18,000 - 18,000

5 Prepaid Insurance 3,600 - 300 3,300 - 3,300

6 Cleaning Equipment 4,800 - 4,800 - 4,800

7 Purchase 2,400 - 2,400 - 2,400

8 Creditors - - - - -

9 Service Revenue - 6,000 5,000 12,600 - 13,600 13,600

10 Wages 1,600 - 2,200 3,800 - 3,800

11 Interest on Loan 200 - 200 - 200

12 Interest Paid in advance 100 - 100 - 100

13 Advertisement Expenses 1,600 - 1,600 - 1,600

14 Outstanding Wages - - 2,200 - 2,200 2,200

15 Accounts Receivable - - 12,600 12,600 - 12,600

16 Fuel Expenses - - 190 190 - 190

17 Telephone Expenses - - 100 100 - 100

18 Fuel Expenses Payable - - 190 - 190 190

19 Telephone Expenses Payable - - 100 - 100 100

20 Income received in advance - - 5,000 - 5,000 5,000

21 Insurance - - 300 300 - 300

22 Depn on Motor Vehicle - - 208 208 - 208

23 Accumulated depn on Motor vehicle - - 208 - 208 208

24 Discount Received - 400 - 400 400

25 Total 56,400 56,400 20,598 20,598 71,698 71,698 8,798 14,000 62,900 57,698

Net profit

/(loss) 5,202 5,202

Total 14,000 14,000 62,900 62,900

Account NameSl. No.

Appendix 3: Worksheet

Trial Bal.-Adj.Trial Bal.-Unadj. Adjustments Income Statement Balance Sheet

Appendix 4: Statement of Profit/Loss

Particulars Amt.($) Amt.($)

Revenues

Service Revenue 13,600

Less: Purchases 2,400

Wages 3,800 6,200

Gross Profit 7,400

Expenses

Interest on Loan 200

8 | P a g e

accrued revenue, third is again outstanding expenses, 4th is deferred revenue, 5th is deferred expenses

and 6th entry is w.r.t. depreciation expenses (Choy, 2018).

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

1 Bank 24,100 - 24,100 - 24,100

2 Capital - 30,000 - 30,000 30,000

3 Loan - 20,000 - 20,000 20,000

4 Motor Vehicle 18,000 - 18,000 - 18,000

5 Prepaid Insurance 3,600 - 300 3,300 - 3,300

6 Cleaning Equipment 4,800 - 4,800 - 4,800

7 Purchase 2,400 - 2,400 - 2,400

8 Creditors - - - - -

9 Service Revenue - 6,000 5,000 12,600 - 13,600 13,600

10 Wages 1,600 - 2,200 3,800 - 3,800

11 Interest on Loan 200 - 200 - 200

12 Interest Paid in advance 100 - 100 - 100

13 Advertisement Expenses 1,600 - 1,600 - 1,600

14 Outstanding Wages - - 2,200 - 2,200 2,200

15 Accounts Receivable - - 12,600 12,600 - 12,600

16 Fuel Expenses - - 190 190 - 190

17 Telephone Expenses - - 100 100 - 100

18 Fuel Expenses Payable - - 190 - 190 190

19 Telephone Expenses Payable - - 100 - 100 100

20 Income received in advance - - 5,000 - 5,000 5,000

21 Insurance - - 300 300 - 300

22 Depn on Motor Vehicle - - 208 208 - 208

23 Accumulated depn on Motor vehicle - - 208 - 208 208

24 Discount Received - 400 - 400 400

25 Total 56,400 56,400 20,598 20,598 71,698 71,698 8,798 14,000 62,900 57,698

Net profit

/(loss) 5,202 5,202

Total 14,000 14,000 62,900 62,900

Account NameSl. No.

Appendix 3: Worksheet

Trial Bal.-Adj.Trial Bal.-Unadj. Adjustments Income Statement Balance Sheet

Appendix 4: Statement of Profit/Loss

Particulars Amt.($) Amt.($)

Revenues

Service Revenue 13,600

Less: Purchases 2,400

Wages 3,800 6,200

Gross Profit 7,400

Expenses

Interest on Loan 200

8 | P a g e

9

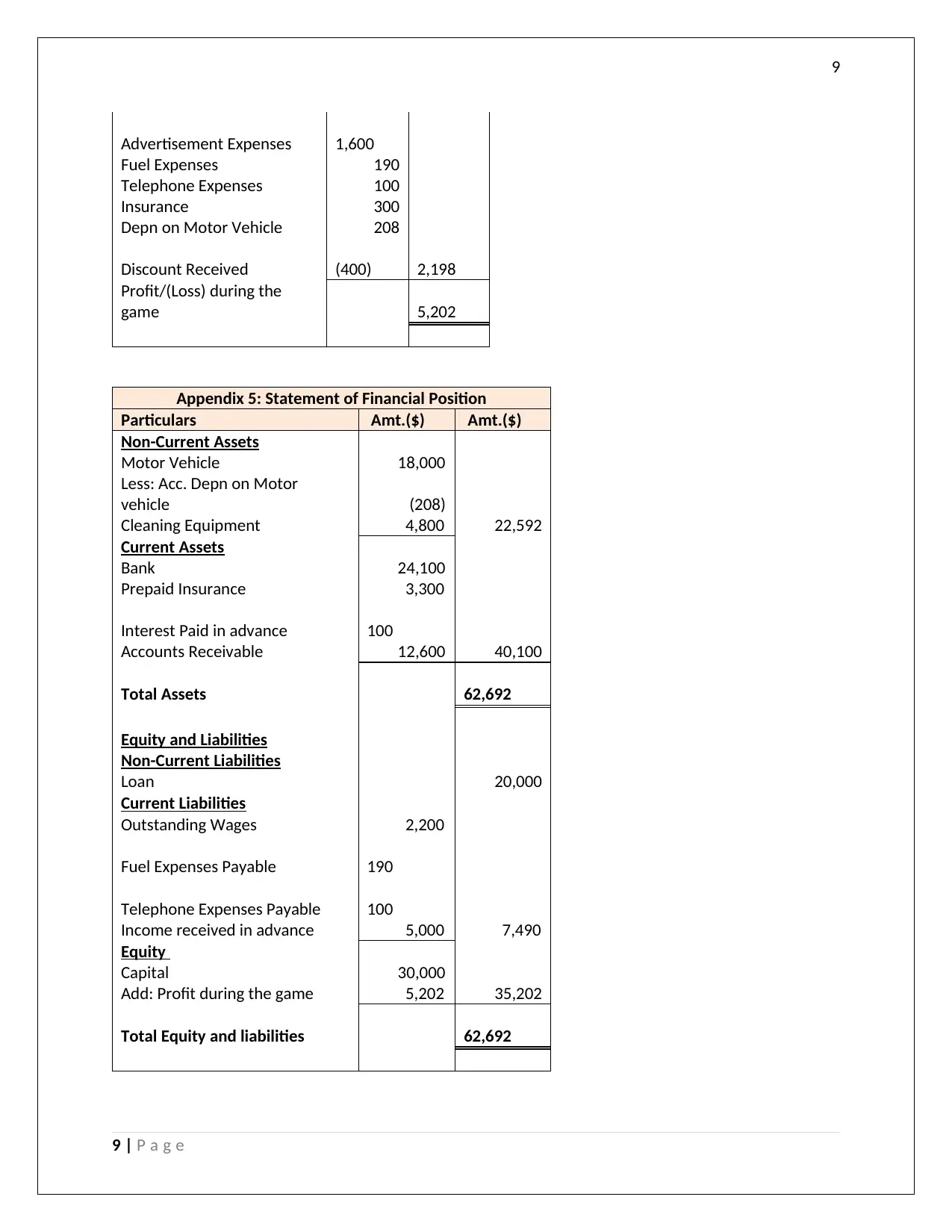

Advertisement Expenses 1,600

Fuel Expenses 190

Telephone Expenses 100

Insurance 300

Depn on Motor Vehicle 208

Discount Received (400) 2,198

Profit/(Loss) during the

game 5,202

Appendix 5: Statement of Financial Position

Particulars Amt.($) Amt.($)

Non-Current Assets

Motor Vehicle 18,000

Less: Acc. Depn on Motor

vehicle (208)

Cleaning Equipment 4,800 22,592

Current Assets

Bank 24,100

Prepaid Insurance 3,300

Interest Paid in advance 100

Accounts Receivable 12,600 40,100

Total Assets 62,692

Equity and Liabilities

Non-Current Liabilities

Loan 20,000

Current Liabilities

Outstanding Wages 2,200

Fuel Expenses Payable 190

Telephone Expenses Payable 100

Income received in advance 5,000 7,490

Equity

Capital 30,000

Add: Profit during the game 5,202 35,202

Total Equity and liabilities 62,692

9 | P a g e

Advertisement Expenses 1,600

Fuel Expenses 190

Telephone Expenses 100

Insurance 300

Depn on Motor Vehicle 208

Discount Received (400) 2,198

Profit/(Loss) during the

game 5,202

Appendix 5: Statement of Financial Position

Particulars Amt.($) Amt.($)

Non-Current Assets

Motor Vehicle 18,000

Less: Acc. Depn on Motor

vehicle (208)

Cleaning Equipment 4,800 22,592

Current Assets

Bank 24,100

Prepaid Insurance 3,300

Interest Paid in advance 100

Accounts Receivable 12,600 40,100

Total Assets 62,692

Equity and Liabilities

Non-Current Liabilities

Loan 20,000

Current Liabilities

Outstanding Wages 2,200

Fuel Expenses Payable 190

Telephone Expenses Payable 100

Income received in advance 5,000 7,490

Equity

Capital 30,000

Add: Profit during the game 5,202 35,202

Total Equity and liabilities 62,692

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

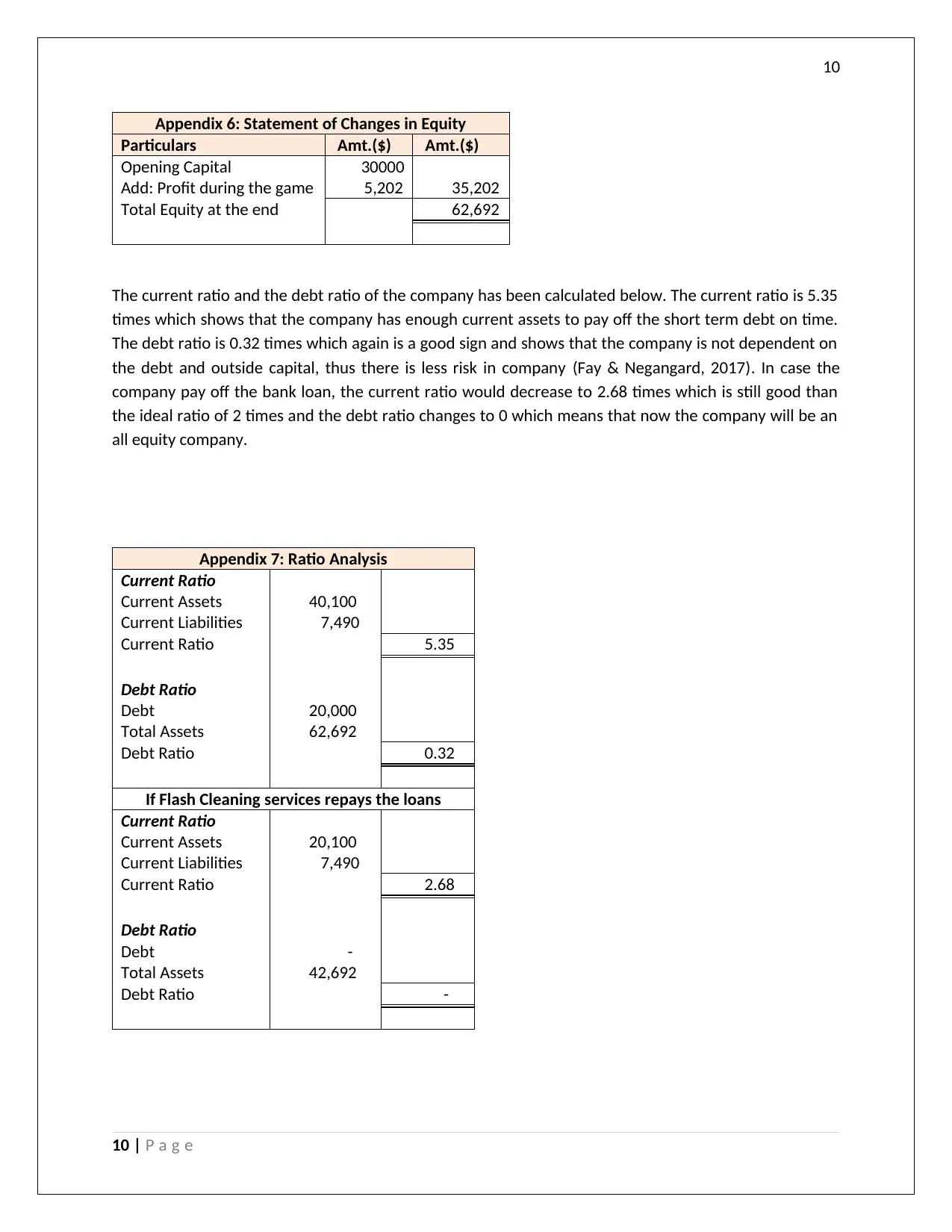

Appendix 6: Statement of Changes in Equity

Particulars Amt.($) Amt.($)

Opening Capital 30000

Add: Profit during the game 5,202 35,202

Total Equity at the end 62,692

The current ratio and the debt ratio of the company has been calculated below. The current ratio is 5.35

times which shows that the company has enough current assets to pay off the short term debt on time.

The debt ratio is 0.32 times which again is a good sign and shows that the company is not dependent on

the debt and outside capital, thus there is less risk in company (Fay & Negangard, 2017). In case the

company pay off the bank loan, the current ratio would decrease to 2.68 times which is still good than

the ideal ratio of 2 times and the debt ratio changes to 0 which means that now the company will be an

all equity company.

Appendix 7: Ratio Analysis

Current Ratio

Current Assets 40,100

Current Liabilities 7,490

Current Ratio 5.35

Debt Ratio

Debt 20,000

Total Assets 62,692

Debt Ratio 0.32

If Flash Cleaning services repays the loans

Current Ratio

Current Assets 20,100

Current Liabilities 7,490

Current Ratio 2.68

Debt Ratio

Debt -

Total Assets 42,692

Debt Ratio -

10 | P a g e

Appendix 6: Statement of Changes in Equity

Particulars Amt.($) Amt.($)

Opening Capital 30000

Add: Profit during the game 5,202 35,202

Total Equity at the end 62,692

The current ratio and the debt ratio of the company has been calculated below. The current ratio is 5.35

times which shows that the company has enough current assets to pay off the short term debt on time.

The debt ratio is 0.32 times which again is a good sign and shows that the company is not dependent on

the debt and outside capital, thus there is less risk in company (Fay & Negangard, 2017). In case the

company pay off the bank loan, the current ratio would decrease to 2.68 times which is still good than

the ideal ratio of 2 times and the debt ratio changes to 0 which means that now the company will be an

all equity company.

Appendix 7: Ratio Analysis

Current Ratio

Current Assets 40,100

Current Liabilities 7,490

Current Ratio 5.35

Debt Ratio

Debt 20,000

Total Assets 62,692

Debt Ratio 0.32

If Flash Cleaning services repays the loans

Current Ratio

Current Assets 20,100

Current Liabilities 7,490

Current Ratio 2.68

Debt Ratio

Debt -

Total Assets 42,692

Debt Ratio -

10 | P a g e

11

Question 2: History of accounting - essay

Double Entry bookkeeping is one of the concepts of recording the accounting transaction in the books of

accounts which has an impact on the two sides of company finances. It has two legs of the transaction,

which can be an asset, liability, income, expense or equity. For example, if the company sells the goods,

it has an impact on the revenue and also the cash account (Jefferson, 2017).

The Italian Luca Pacioli, who is considered to be the Father of Accounting and Bookkeeping was the first

person to introduce the concept of double entry book keeping and introduced it in Italy. In the 13 th

century, when medieval Europe moved towards the monetary transaction, most of the merchants were

dependent on the bookkeeping for effecting and recording the multiple transactions with the bank. It

was at that time that one of the most important breakthrough in the field of accounting took place and

double entry bookkeeping got introduced where each transaction had 2 legs namely debit and the credit

leg (Heminway, 2017). The words are derived from the Latin words debitum and creditum which means

“what is due” and “something entrusted to another or loan”. The double entry book keeping system

replaced the earlier used single entry book keeping system. It is believed that the double entry

bookkeeping was pioneered in the Jewish community and when the Italian merchants discussed on this

system with the Jewish counterparts, they implemented the same. The earliest evidence of the same is

found in Farolfi ledger in 1299-1300 period (Linden & Freeman, 2017). The oldest discovered record

which has been found on the given subject is Messari (Treasurer’s in Italian) accounts in Genoa city in

1340. It contains debits and credits being recorded in the bilateral form and the carry forward balances

from the previous year and hence the complete evidence of double entry system. Luca Pacioli's

renowned works namely Summa de Arithmetica, Geometria, Proportioni et Proportionalità (early Italian:

"Review of Arithmetic, Geometry, Ratio and Proportion") which were first printed and published in

Venice in 1494 are considered to be the first known printed material on bookkeeping rules and

regulations. Although he did not invent the double entry system but his 27 page work on bookkeeping,

"Particularis de Computis et Scripturis" (Latin: "Details of Calculation and Recording") is considered to

have laid foundation for what is being practiced today as double entry bookkeeping (Goldmann, 2016).

Off late the double entry system has become profoundly significant and important in the world of

accounting due to the complete cycle of transaction being recorded under this system. This is simple and

easy to understand and interpret. It has approaches namely traditional approach and the accounting

equation approach. The benefit with this system is that multiple debits and credits can be posted at the

same time such the sum total of all the debits and the credits is same. It thus also acts as a check of the

correct recording of the entries (Van Rinsum, 2018). Since both the debit and credit aspect of the entry

have the same date so the error if any can be identified quickly for both the legs of the transaction and

thus it also serves as the audit trail. The two approaches to accounting are mentioned below:

1. Traditional Approach: Also called as British Approach, it classifies all the accounts into real,

personal and nominal accounts and the following rule is used while accounting.

“Real account: Debit what comes in and credit what goes out.

Personal account: Debit the receiver and credit the giver.

Nominal account: Debit all expenses & losses and credit all incomes & gains”

11 | P a g e

Question 2: History of accounting - essay

Double Entry bookkeeping is one of the concepts of recording the accounting transaction in the books of

accounts which has an impact on the two sides of company finances. It has two legs of the transaction,

which can be an asset, liability, income, expense or equity. For example, if the company sells the goods,

it has an impact on the revenue and also the cash account (Jefferson, 2017).

The Italian Luca Pacioli, who is considered to be the Father of Accounting and Bookkeeping was the first

person to introduce the concept of double entry book keeping and introduced it in Italy. In the 13 th

century, when medieval Europe moved towards the monetary transaction, most of the merchants were

dependent on the bookkeeping for effecting and recording the multiple transactions with the bank. It

was at that time that one of the most important breakthrough in the field of accounting took place and

double entry bookkeeping got introduced where each transaction had 2 legs namely debit and the credit

leg (Heminway, 2017). The words are derived from the Latin words debitum and creditum which means

“what is due” and “something entrusted to another or loan”. The double entry book keeping system

replaced the earlier used single entry book keeping system. It is believed that the double entry

bookkeeping was pioneered in the Jewish community and when the Italian merchants discussed on this

system with the Jewish counterparts, they implemented the same. The earliest evidence of the same is

found in Farolfi ledger in 1299-1300 period (Linden & Freeman, 2017). The oldest discovered record

which has been found on the given subject is Messari (Treasurer’s in Italian) accounts in Genoa city in

1340. It contains debits and credits being recorded in the bilateral form and the carry forward balances

from the previous year and hence the complete evidence of double entry system. Luca Pacioli's

renowned works namely Summa de Arithmetica, Geometria, Proportioni et Proportionalità (early Italian:

"Review of Arithmetic, Geometry, Ratio and Proportion") which were first printed and published in

Venice in 1494 are considered to be the first known printed material on bookkeeping rules and

regulations. Although he did not invent the double entry system but his 27 page work on bookkeeping,

"Particularis de Computis et Scripturis" (Latin: "Details of Calculation and Recording") is considered to

have laid foundation for what is being practiced today as double entry bookkeeping (Goldmann, 2016).

Off late the double entry system has become profoundly significant and important in the world of

accounting due to the complete cycle of transaction being recorded under this system. This is simple and

easy to understand and interpret. It has approaches namely traditional approach and the accounting

equation approach. The benefit with this system is that multiple debits and credits can be posted at the

same time such the sum total of all the debits and the credits is same. It thus also acts as a check of the

correct recording of the entries (Van Rinsum, 2018). Since both the debit and credit aspect of the entry

have the same date so the error if any can be identified quickly for both the legs of the transaction and

thus it also serves as the audit trail. The two approaches to accounting are mentioned below:

1. Traditional Approach: Also called as British Approach, it classifies all the accounts into real,

personal and nominal accounts and the following rule is used while accounting.

“Real account: Debit what comes in and credit what goes out.

Personal account: Debit the receiver and credit the giver.

Nominal account: Debit all expenses & losses and credit all incomes & gains”

11 | P a g e

12

2. Accounting equation approach: Also known as the American Approach this is based on the rule

of Assets = Liabilities + capital. For the purpose of accounting, all the accounts are classified into

5 types namely assets, liabilities, revenues, expenses and capital gain or losses. The total of

debits should be equal to the total of credits. It works as per the below (Werner, 2017).

Again double entry system is important due to its wide use in maintaining the financial statements.

Since it has 2 aspects of recording any given transaction, therefore the chances of errors and mistakes

are lowered. It follows “T way” of recording transaction in ledger where there are 2 equal halves, left

being debit side and right being the credit side. It also helps in preparation of income and expense

statement and the balance sheet easily (Sithole, Chandler, Abeysekera, & Paas, 2017). It helps in

avoiding frauds as even a small change in the account can be caught and thus manipulation of accounts

is difficult. It thus helps in maintaining the accuracy of accounts. Since this is based on the matching

principle, it also helps in assessing the loss and the profit to company correctly. Finally, it enables the

comparable study as well amongst the different years for the purposes of decision making (Arnott,

Lizama, & Song, 2017).

Before double entry system, single entry system was being used, which used to record only one of the

aspects like if the customer pays cash, either debtor will be debited or the cash will be credited thus it

failed to track the asset and liability status which made it look like check book register. This shortcoming

is resolved by double entry system. The single entry system did not ensure a cross check as the

corresponding entry was not available and thus there were high chances of inaccuracy in that system

(Alieid, 2016). Single entry system cannot help in the preparation of the trial balance or even the other

financial statements like those of profit and loss account, the balance sheet, cash flow statement and

the statement of changes in equity which is enabled by double entry system. It was difficult for company

to ascertain the financial position under the single entry system as it did not follow the fundamental

system of accounting which was later on enabled by double entry system. This is how the double entry

system differs from the old bookkeeping methods.

Question 3: ABC Learning Case Study

12 | P a g e

2. Accounting equation approach: Also known as the American Approach this is based on the rule

of Assets = Liabilities + capital. For the purpose of accounting, all the accounts are classified into

5 types namely assets, liabilities, revenues, expenses and capital gain or losses. The total of

debits should be equal to the total of credits. It works as per the below (Werner, 2017).

Again double entry system is important due to its wide use in maintaining the financial statements.

Since it has 2 aspects of recording any given transaction, therefore the chances of errors and mistakes

are lowered. It follows “T way” of recording transaction in ledger where there are 2 equal halves, left

being debit side and right being the credit side. It also helps in preparation of income and expense

statement and the balance sheet easily (Sithole, Chandler, Abeysekera, & Paas, 2017). It helps in

avoiding frauds as even a small change in the account can be caught and thus manipulation of accounts

is difficult. It thus helps in maintaining the accuracy of accounts. Since this is based on the matching

principle, it also helps in assessing the loss and the profit to company correctly. Finally, it enables the

comparable study as well amongst the different years for the purposes of decision making (Arnott,

Lizama, & Song, 2017).

Before double entry system, single entry system was being used, which used to record only one of the

aspects like if the customer pays cash, either debtor will be debited or the cash will be credited thus it

failed to track the asset and liability status which made it look like check book register. This shortcoming

is resolved by double entry system. The single entry system did not ensure a cross check as the

corresponding entry was not available and thus there were high chances of inaccuracy in that system

(Alieid, 2016). Single entry system cannot help in the preparation of the trial balance or even the other

financial statements like those of profit and loss account, the balance sheet, cash flow statement and

the statement of changes in equity which is enabled by double entry system. It was difficult for company

to ascertain the financial position under the single entry system as it did not follow the fundamental

system of accounting which was later on enabled by double entry system. This is how the double entry

system differs from the old bookkeeping methods.

Question 3: ABC Learning Case Study

12 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

1. The company ABC learning had to liquidate due to its corrupt accounting practices and unethical

accounting practices which led to one of the downfall of one of Australia’s largest child care

corporation. Liquidation is a procedure by which the company decides to shut own all its

business operation and sell or redistribute all its properties and assets. There are so many

factors which are responsible for the liquidation of company. Sometime companies does it

voluntarily or in some cases it is ordered by the court to do the same. Liquidation is also known

as winding-up or dissolution and it impact the fundamental accounting assumption that is Going

Concern assumption of company as well as the investors and other stakeholders who are related

to the company (Knechel & Salterio, 2016). There are various rules and regulation made by the

court for the effective liquidation of the companies. For the successful administration of

liquidation process company need to appoint liquidator that will look over the entire liquidation

process. In case if company is not able to pay off all its dues sometimes the personal assets of

the management team may be attached to pay off all its liabilities. Similar was the case with ABC

Learning Company.

ABC learning has been popular for one of the famous child education providing companies in

Australia in the past (Fukukawa & Mock, 2011). The company had lots of educational centres

primary as well as secondary across Australia was earning huge amount of profit. In the year

2006 the company was listed on the Australian Stock exchange with the huge market

capitalization of 2.5 billion dollars. Regardless, in the coming year the company was found to be

involved in several illegal professional operations because of these unprofessional behaviour the

company had to liquidate and close down all its operations. The major reasons due to which

company had to liquidate were it had a huge amount of loans and borrowings and was not able

to pay within a given period of time (Marques, 2018). However, these are not only affected the

company but also the large number of investors. In the given case for all widespread loss the

auditors were held responsible for the acts of the company because they did not inform the

management so that the management can take serious steps within the time and hence the

company went into liquidation in 2008. In the year December 2009 the company was taken over

by one of the renewed company Goodyear Early Learning, which had a large number of centres

around 650 centres across Australia.

This was taken place as the company was not able to pay off its creditors on time and the

company went into voluntary liquidation since the auditor disagree to signing off the audit

report due to involvement of material misstatement in the financials of last few years so, the

auditors requirement restated financial statement without any misstatement. The childcare

come into existence in early 2000s and very soon it expanded rapidly to have a large number of

2300 centres all across Australia (Kuhn & Morris, 2016). It provides the company the

controllership not only in Australia but also acquiring 1% stake in the US market. In addition of

all these the company also involved in several acquisitions and all this considered for huge

profits for the company between 15-20% in 2004 – 2005. However, it all increasing the burden

of debt of the company, which company not able to pay and resultant in share prices of the

13 | P a g e

1. The company ABC learning had to liquidate due to its corrupt accounting practices and unethical

accounting practices which led to one of the downfall of one of Australia’s largest child care

corporation. Liquidation is a procedure by which the company decides to shut own all its

business operation and sell or redistribute all its properties and assets. There are so many

factors which are responsible for the liquidation of company. Sometime companies does it

voluntarily or in some cases it is ordered by the court to do the same. Liquidation is also known

as winding-up or dissolution and it impact the fundamental accounting assumption that is Going

Concern assumption of company as well as the investors and other stakeholders who are related

to the company (Knechel & Salterio, 2016). There are various rules and regulation made by the

court for the effective liquidation of the companies. For the successful administration of

liquidation process company need to appoint liquidator that will look over the entire liquidation

process. In case if company is not able to pay off all its dues sometimes the personal assets of

the management team may be attached to pay off all its liabilities. Similar was the case with ABC

Learning Company.

ABC learning has been popular for one of the famous child education providing companies in

Australia in the past (Fukukawa & Mock, 2011). The company had lots of educational centres

primary as well as secondary across Australia was earning huge amount of profit. In the year

2006 the company was listed on the Australian Stock exchange with the huge market

capitalization of 2.5 billion dollars. Regardless, in the coming year the company was found to be

involved in several illegal professional operations because of these unprofessional behaviour the

company had to liquidate and close down all its operations. The major reasons due to which

company had to liquidate were it had a huge amount of loans and borrowings and was not able

to pay within a given period of time (Marques, 2018). However, these are not only affected the

company but also the large number of investors. In the given case for all widespread loss the

auditors were held responsible for the acts of the company because they did not inform the

management so that the management can take serious steps within the time and hence the

company went into liquidation in 2008. In the year December 2009 the company was taken over

by one of the renewed company Goodyear Early Learning, which had a large number of centres

around 650 centres across Australia.

This was taken place as the company was not able to pay off its creditors on time and the

company went into voluntary liquidation since the auditor disagree to signing off the audit

report due to involvement of material misstatement in the financials of last few years so, the

auditors requirement restated financial statement without any misstatement. The childcare

come into existence in early 2000s and very soon it expanded rapidly to have a large number of

2300 centres all across Australia (Kuhn & Morris, 2016). It provides the company the

controllership not only in Australia but also acquiring 1% stake in the US market. In addition of

all these the company also involved in several acquisitions and all this considered for huge

profits for the company between 15-20% in 2004 – 2005. However, it all increasing the burden

of debt of the company, which company not able to pay and resultant in share prices of the

13 | P a g e

14

company reduced to more than 40% in 2007. The major impact of all these failure is S&P

delisted the company from the stock exchange and receivership being imposed on the company.

2. There were many ethical reasons involved for the failure of the company which was once in the

progressing stage of becoming the largest child care company in Australia. There are several

factor that can be attributed to the collapse of ABC learning liquidation but some of the primary

factors are :

a. Lack of corporate governance being followed at the organisation: The weak internal control

system and review technique of management proved that there is a lack of due diligence.

The company did not create an investment review committee who value the investment as

per the regulations. However, it had management group approval whose only work was

redundant stamping exercise (Raiborn, Butler, & Martin, 2016).

b. Unethical corporate behaviour and window dressing of the financial statements: the

company even convinced the then auditor about the anomalies in the financial statements

and the management did not bother to highlight the same to the shareholders. The weak

financial reviews system ultimately led the company to be in debt for huge amount and

thereby default in the payment of the same (Kachelmeier, Schmidt, & Valentine, 2018).

c. Incorrect valuation method which not discloses the price sensitive information to the

stakeholders and the person which influenced by those information. In the valuation

process of newly acquired entity there is a difference of multi million dollars with the actual

cost. All these things highlighted that acquisitions were never valued based on future

economic benefits rather than it was just a rubber and stamp activity for those charged with

governance. From the in depth study of report it is also highlighted from a report that one

company was acquired was disclosed at a value of $ 70 Mn instead of the actual $ 30 Mn,

which clearly reflects the overvaluation of the companies and making immoderate

payments (Bumgarner & Vasarhelyi, 2018).

There can be many reasons for the liquidation of the company. In case company is continuously

making loss, then to save the company from huge losses the directors of the company can

propose to end the existence of company and also can call for the liquidation of the company

(Dichev, 2017). Apart from this, the company might get liquidated due to working capital

position not being reasonable, business being done for wrong objective, location of the

company not being suitable for the operations of company, etc. However, in case of ABC

learning, there were several ethical reasons involved which have been explained in detail above.

14 | P a g e

company reduced to more than 40% in 2007. The major impact of all these failure is S&P

delisted the company from the stock exchange and receivership being imposed on the company.

2. There were many ethical reasons involved for the failure of the company which was once in the

progressing stage of becoming the largest child care company in Australia. There are several

factor that can be attributed to the collapse of ABC learning liquidation but some of the primary

factors are :

a. Lack of corporate governance being followed at the organisation: The weak internal control

system and review technique of management proved that there is a lack of due diligence.

The company did not create an investment review committee who value the investment as

per the regulations. However, it had management group approval whose only work was

redundant stamping exercise (Raiborn, Butler, & Martin, 2016).

b. Unethical corporate behaviour and window dressing of the financial statements: the

company even convinced the then auditor about the anomalies in the financial statements

and the management did not bother to highlight the same to the shareholders. The weak

financial reviews system ultimately led the company to be in debt for huge amount and

thereby default in the payment of the same (Kachelmeier, Schmidt, & Valentine, 2018).

c. Incorrect valuation method which not discloses the price sensitive information to the

stakeholders and the person which influenced by those information. In the valuation

process of newly acquired entity there is a difference of multi million dollars with the actual

cost. All these things highlighted that acquisitions were never valued based on future

economic benefits rather than it was just a rubber and stamp activity for those charged with

governance. From the in depth study of report it is also highlighted from a report that one

company was acquired was disclosed at a value of $ 70 Mn instead of the actual $ 30 Mn,

which clearly reflects the overvaluation of the companies and making immoderate

payments (Bumgarner & Vasarhelyi, 2018).

There can be many reasons for the liquidation of the company. In case company is continuously

making loss, then to save the company from huge losses the directors of the company can

propose to end the existence of company and also can call for the liquidation of the company

(Dichev, 2017). Apart from this, the company might get liquidated due to working capital

position not being reasonable, business being done for wrong objective, location of the

company not being suitable for the operations of company, etc. However, in case of ABC

learning, there were several ethical reasons involved which have been explained in detail above.

14 | P a g e

15

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 3(1), 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Fay, R., & Negangard, E. (2017). Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, 38, 37-49.

15 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 3(1), 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Fay, R., & Negangard, E. (2017). Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, 38, 37-49.

15 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), 1-39.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Van Rinsum, M. M. (2018). Disclosure Checklists and Auditors’ Judgments of Aggressive Accounting.

European Accounting Review, 27(2), 383-399.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

16 | P a g e

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), 1-39.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Van Rinsum, M. M. (2018). Disclosure Checklists and Auditors’ Judgments of Aggressive Accounting.

European Accounting Review, 27(2), 383-399.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

16 | P a g e

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.