ACC00724 - Financial Performance Evaluation of JB Hi-Fi

VerifiedAdded on 2021/12/29

|14

|1742

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING FOR MANAGERS

JB Hi-Fi

STUDENT ID:

[Pick the date]

JB Hi-Fi

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

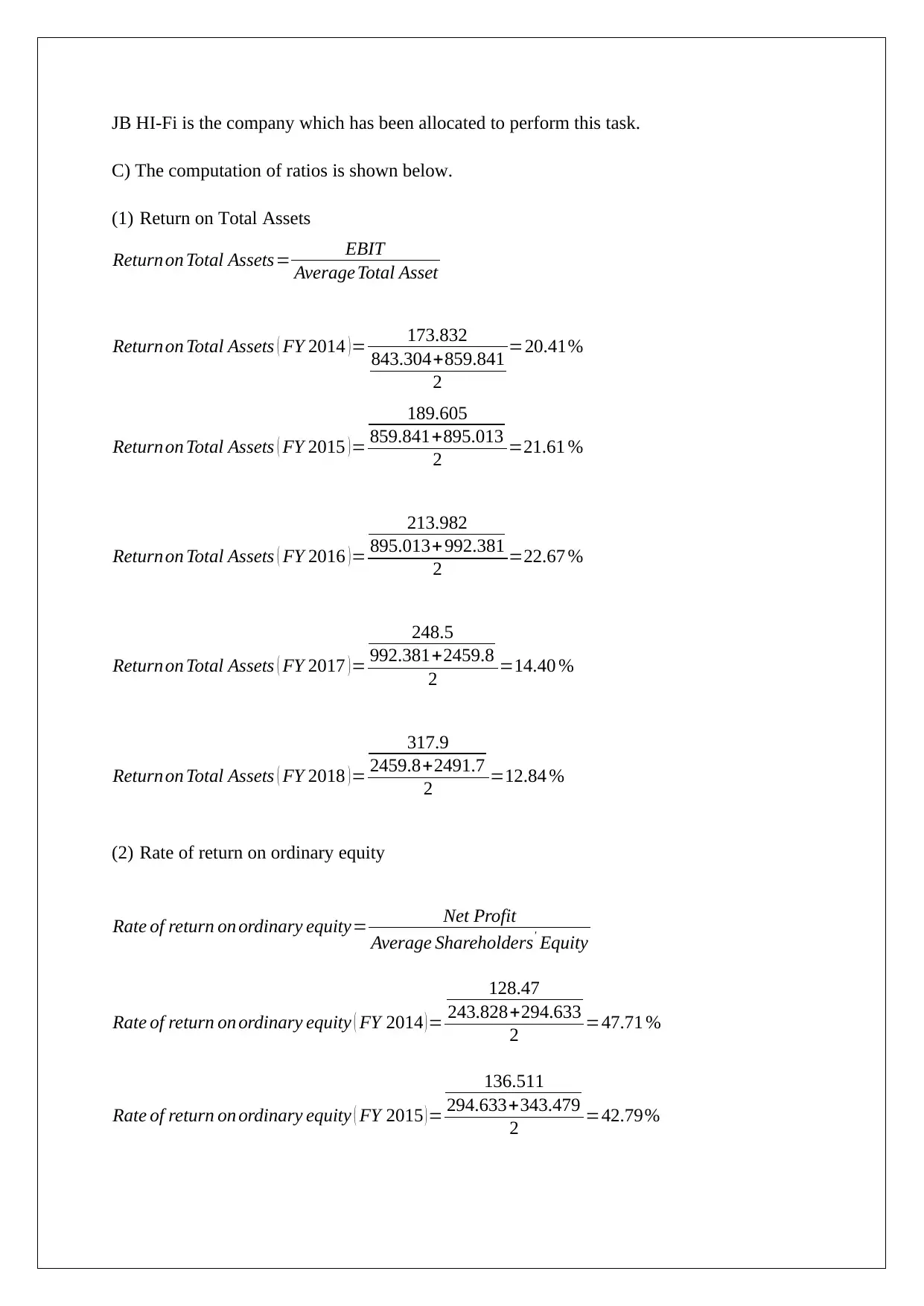

JB HI-Fi is the company which has been allocated to perform this task.

C) The computation of ratios is shown below.

(1) Return on Total Assets

Returnon Total Assets= EBIT

Average Total Asset

Returnon Total Assets ( FY 2014 ) = 173.832

843.304+859.841

2

=20.41%

Returnon Total Assets ( FY 2015 )=

189.605

859.841+895.013

2 =21.61 %

Returnon Total Assets ( FY 2016 ) =

213.982

895.013+ 992.381

2 =22.67 %

Returnon Total Assets ( FY 2017 )=

248.5

992.381+2459.8

2 =14.40 %

Returnon Total Assets ( FY 2018 )=

317.9

2459.8+2491.7

2 =12.84 %

(2) Rate of return on ordinary equity

Rate of return on ordinary equity= Net Profit

Average Shareholders' Equity

Rate of return on ordinary equity ( FY 2014 )=

128.47

243.828+294.633

2 =47.71 %

Rate of return on ordinary equity ( FY 2015 )=

136.511

294.633+343.479

2 =42.79%

C) The computation of ratios is shown below.

(1) Return on Total Assets

Returnon Total Assets= EBIT

Average Total Asset

Returnon Total Assets ( FY 2014 ) = 173.832

843.304+859.841

2

=20.41%

Returnon Total Assets ( FY 2015 )=

189.605

859.841+895.013

2 =21.61 %

Returnon Total Assets ( FY 2016 ) =

213.982

895.013+ 992.381

2 =22.67 %

Returnon Total Assets ( FY 2017 )=

248.5

992.381+2459.8

2 =14.40 %

Returnon Total Assets ( FY 2018 )=

317.9

2459.8+2491.7

2 =12.84 %

(2) Rate of return on ordinary equity

Rate of return on ordinary equity= Net Profit

Average Shareholders' Equity

Rate of return on ordinary equity ( FY 2014 )=

128.47

243.828+294.633

2 =47.71 %

Rate of return on ordinary equity ( FY 2015 )=

136.511

294.633+343.479

2 =42.79%

Rate of return on ordinary equity ( FY 2016 )=

152.181

343.479+ 404.702

2 =40.68 %

Rate of return on ordinary equity ( FY 2017 ) =

172.4

404.702+853.5

2 =27.40 %

Rate of return on ordinary equity ( FY 2018 )= 233.2

853.5+947.6 =25.90 %

(3) Operating profit margin

Operating profit margin= Operating profit

Sales Revenue

Operating profit margin ( FY 2014 ) = 173.832

3483.775 =4.99 %

Operating profit margin ( FY 2015 ) = 189.605

3652.14 =5.19 %

Operating profit margin ( FY 2016 )= 213.982

3954.47 =5.41 %

Operating profit margin ( FY 2017 )= 248.5

5628 =4.42%

Operating profit margin ( FY 2018 )= 317.9

6864.3 =4.63 %

(4) Gross profit margin

Gross profit margin= Gross Profit

Sales Revenue

152.181

343.479+ 404.702

2 =40.68 %

Rate of return on ordinary equity ( FY 2017 ) =

172.4

404.702+853.5

2 =27.40 %

Rate of return on ordinary equity ( FY 2018 )= 233.2

853.5+947.6 =25.90 %

(3) Operating profit margin

Operating profit margin= Operating profit

Sales Revenue

Operating profit margin ( FY 2014 ) = 173.832

3483.775 =4.99 %

Operating profit margin ( FY 2015 ) = 189.605

3652.14 =5.19 %

Operating profit margin ( FY 2016 )= 213.982

3954.47 =5.41 %

Operating profit margin ( FY 2017 )= 248.5

5628 =4.42%

Operating profit margin ( FY 2018 )= 317.9

6864.3 =4.63 %

(4) Gross profit margin

Gross profit margin= Gross Profit

Sales Revenue

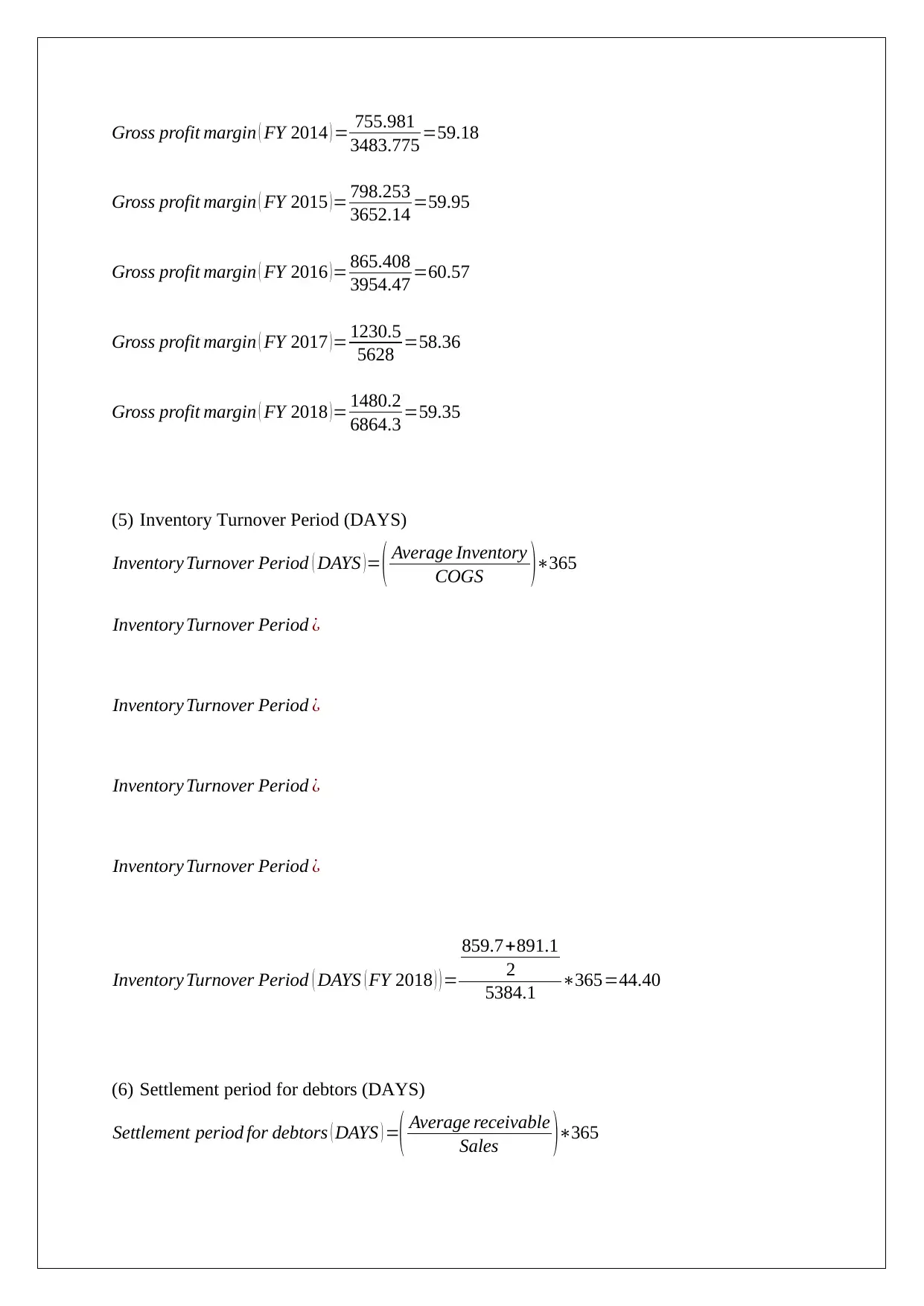

Gross profit margin ( FY 2014 ) = 755.981

3483.775 =59.18

Gross profit margin ( FY 2015 )= 798.253

3652.14 =59.95

Gross profit margin ( FY 2016 )= 865.408

3954.47 =60.57

Gross profit margin ( FY 2017 )= 1230.5

5628 =58.36

Gross profit margin ( FY 2018 )= 1480.2

6864.3 =59.35

(5) Inventory Turnover Period (DAYS)

Inventory Turnover Period ( DAYS )= ( Average Inventory

COGS )∗365

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ( DAYS ( FY 2018 ) ) =

859.7+891.1

2

5384.1 ∗365=44.40

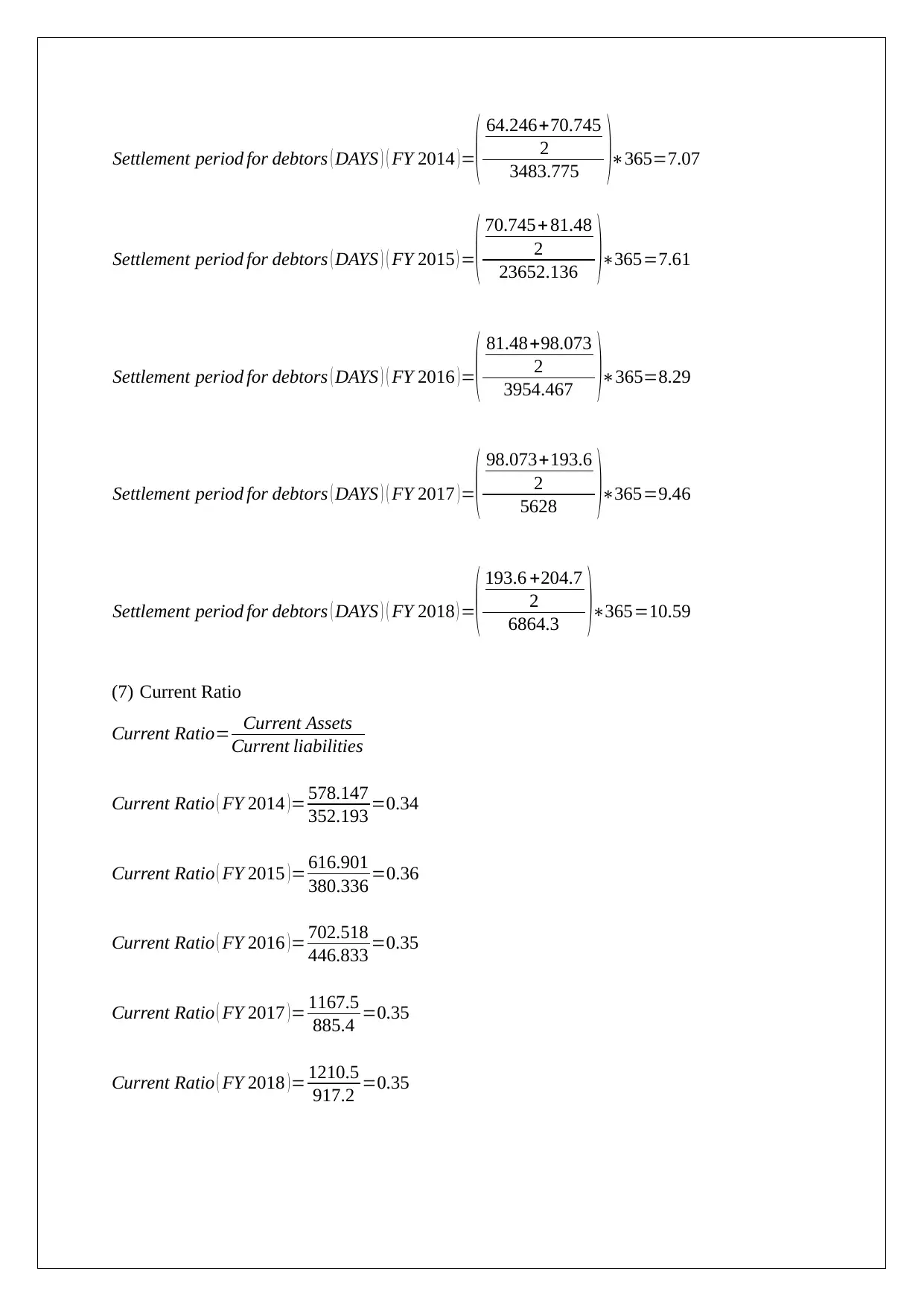

(6) Settlement period for debtors (DAYS)

Settlement period for debtors ( DAYS ) =( Average receivable

Sales )∗365

3483.775 =59.18

Gross profit margin ( FY 2015 )= 798.253

3652.14 =59.95

Gross profit margin ( FY 2016 )= 865.408

3954.47 =60.57

Gross profit margin ( FY 2017 )= 1230.5

5628 =58.36

Gross profit margin ( FY 2018 )= 1480.2

6864.3 =59.35

(5) Inventory Turnover Period (DAYS)

Inventory Turnover Period ( DAYS )= ( Average Inventory

COGS )∗365

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ¿

Inventory Turnover Period ( DAYS ( FY 2018 ) ) =

859.7+891.1

2

5384.1 ∗365=44.40

(6) Settlement period for debtors (DAYS)

Settlement period for debtors ( DAYS ) =( Average receivable

Sales )∗365

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Settlement period for debtors ( DAYS ) ( FY 2014 )=( 64.246+70.745

2

3483.775 )∗365=7.07

Settlement period for debtors ( DAYS ) ( FY 2015 ) =( 70.745+ 81.48

2

23652.136 )∗365=7.61

Settlement period for debtors ( DAYS ) ( FY 2016 )=( 81.48+98.073

2

3954.467 )∗365=8.29

Settlement period for debtors ( DAYS ) ( FY 2017 ) =( 98.073+193.6

2

5628 )∗365=9.46

Settlement period for debtors ( DAYS ) ( FY 2018 ) =( 193.6 +204.7

2

6864.3 )∗365=10.59

(7) Current Ratio

Current Ratio= Current Assets

Current liabilities

Current Ratio ( FY 2014 )= 578.147

352.193 =0.34

Current Ratio ( FY 2015 ) = 616.901

380.336 =0.36

Current Ratio ( FY 2016 )= 702.518

446.833 =0.35

Current Ratio ( FY 2017 )= 1167.5

885.4 =0.35

Current Ratio ( FY 2018 )= 1210.5

917.2 =0.35

2

3483.775 )∗365=7.07

Settlement period for debtors ( DAYS ) ( FY 2015 ) =( 70.745+ 81.48

2

23652.136 )∗365=7.61

Settlement period for debtors ( DAYS ) ( FY 2016 )=( 81.48+98.073

2

3954.467 )∗365=8.29

Settlement period for debtors ( DAYS ) ( FY 2017 ) =( 98.073+193.6

2

5628 )∗365=9.46

Settlement period for debtors ( DAYS ) ( FY 2018 ) =( 193.6 +204.7

2

6864.3 )∗365=10.59

(7) Current Ratio

Current Ratio= Current Assets

Current liabilities

Current Ratio ( FY 2014 )= 578.147

352.193 =0.34

Current Ratio ( FY 2015 ) = 616.901

380.336 =0.36

Current Ratio ( FY 2016 )= 702.518

446.833 =0.35

Current Ratio ( FY 2017 )= 1167.5

885.4 =0.35

Current Ratio ( FY 2018 )= 1210.5

917.2 =0.35

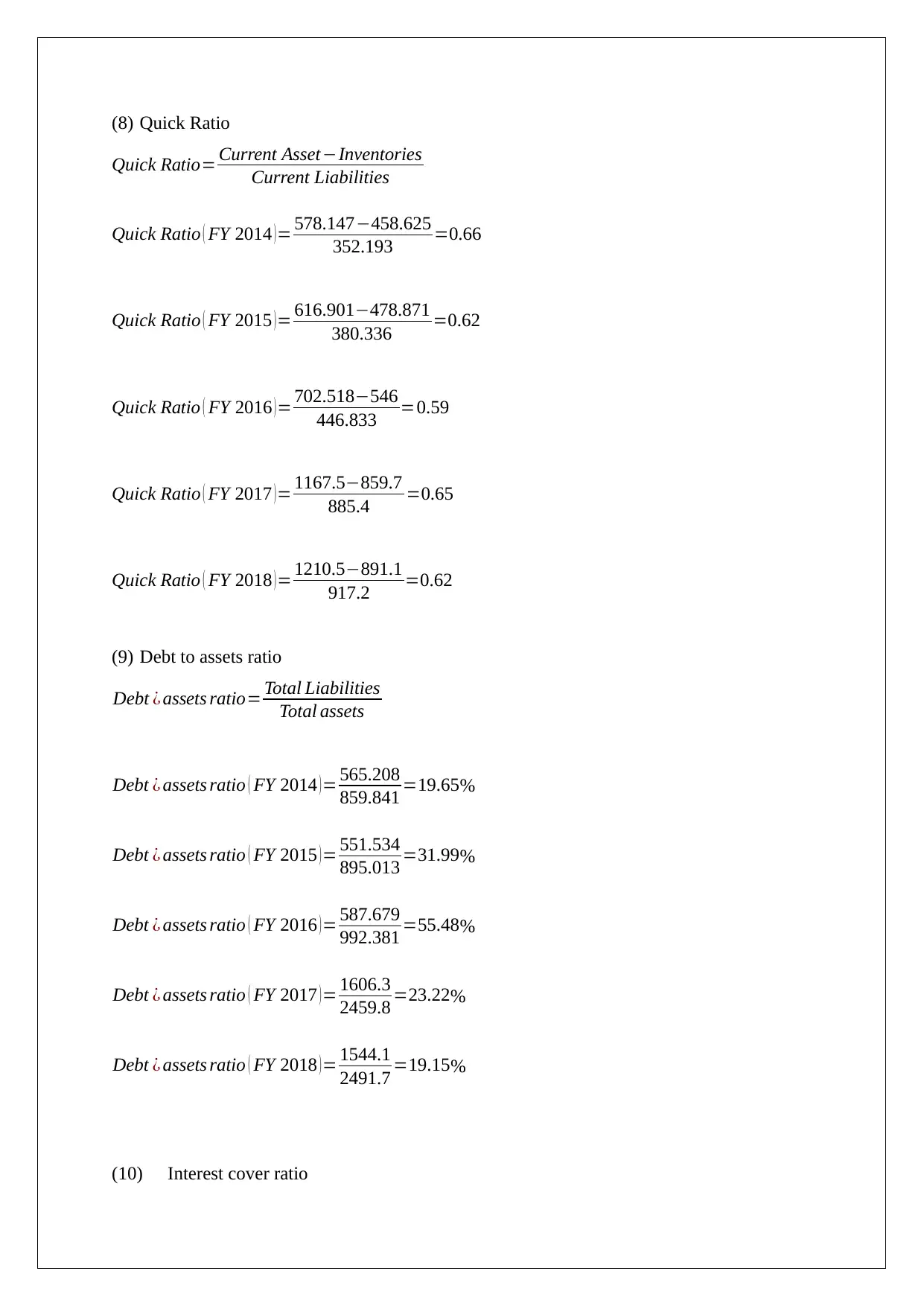

(8) Quick Ratio

Quick Ratio= Current Asset−Inventories

Current Liabilities

Quick Ratio ( FY 2014 )= 578.147−458.625

352.193 =0.66

Quick Ratio ( FY 2015 )= 616.901−478.871

380.336 =0.62

Quick Ratio ( FY 2016 ) = 702.518−546

446.833 =0.59

Quick Ratio ( FY 2017 )= 1167.5−859.7

885.4 =0.65

Quick Ratio ( FY 2018 ) = 1210.5−891.1

917.2 =0.62

(9) Debt to assets ratio

Debt ¿ assets ratio= Total Liabilities

Total assets

Debt ¿ assets ratio ( FY 2014 )= 565.208

859.841 =19.65%

Debt ¿ assets ratio ( FY 2015 )= 551.534

895.013 =31.99%

Debt ¿ assets ratio ( FY 2016 )= 587.679

992.381 =55.48%

Debt ¿ assets ratio ( FY 2017 )= 1606.3

2459.8 =23.22%

Debt ¿ assets ratio ( FY 2018 )= 1544.1

2491.7 =19.15%

(10) Interest cover ratio

Quick Ratio= Current Asset−Inventories

Current Liabilities

Quick Ratio ( FY 2014 )= 578.147−458.625

352.193 =0.66

Quick Ratio ( FY 2015 )= 616.901−478.871

380.336 =0.62

Quick Ratio ( FY 2016 ) = 702.518−546

446.833 =0.59

Quick Ratio ( FY 2017 )= 1167.5−859.7

885.4 =0.65

Quick Ratio ( FY 2018 ) = 1210.5−891.1

917.2 =0.62

(9) Debt to assets ratio

Debt ¿ assets ratio= Total Liabilities

Total assets

Debt ¿ assets ratio ( FY 2014 )= 565.208

859.841 =19.65%

Debt ¿ assets ratio ( FY 2015 )= 551.534

895.013 =31.99%

Debt ¿ assets ratio ( FY 2016 )= 587.679

992.381 =55.48%

Debt ¿ assets ratio ( FY 2017 )= 1606.3

2459.8 =23.22%

Debt ¿ assets ratio ( FY 2018 )= 1544.1

2491.7 =19.15%

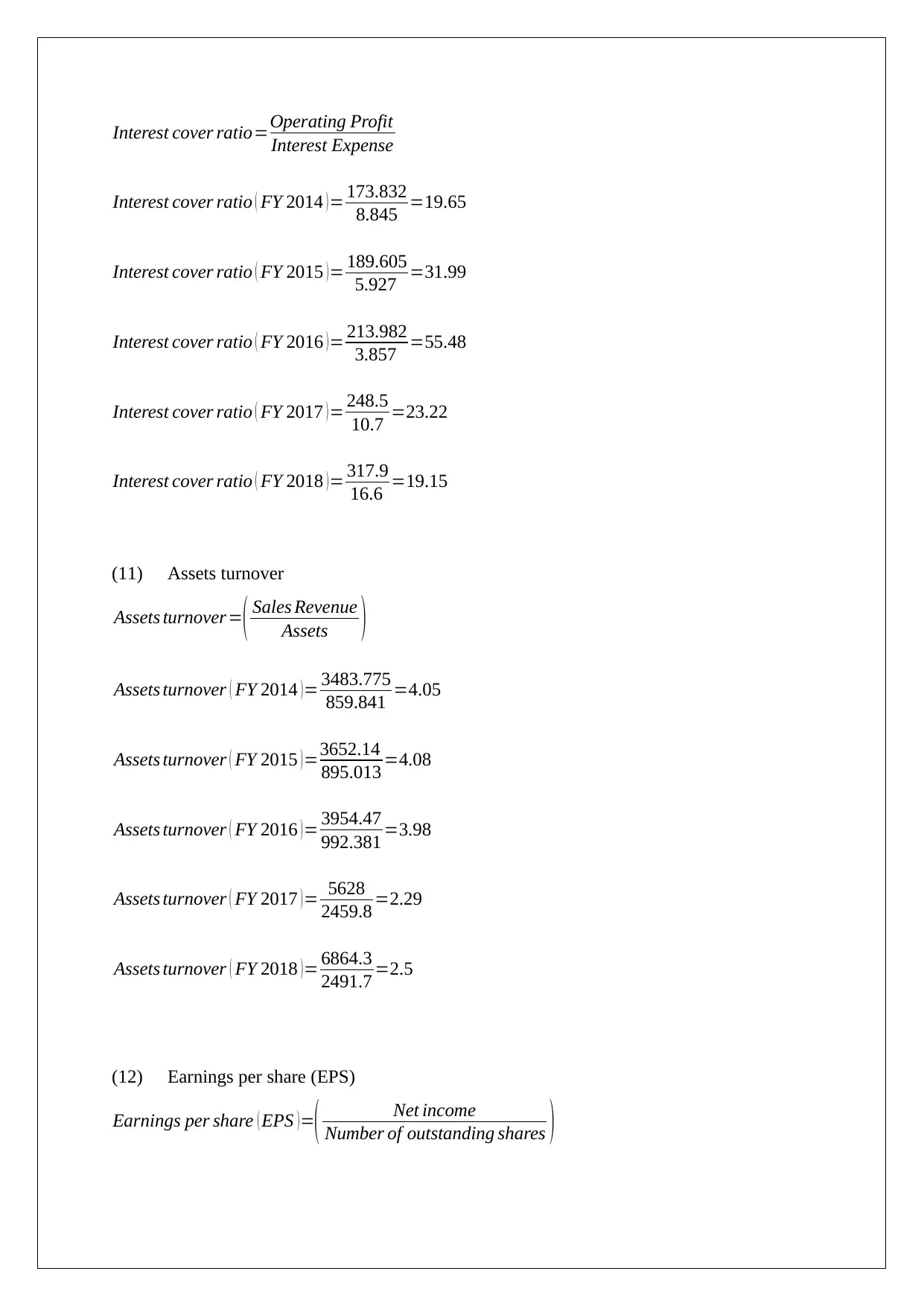

(10) Interest cover ratio

Interest cover ratio=Operating Profit

Interest Expense

Interest cover ratio ( FY 2014 )= 173.832

8.845 =19.65

Interest cover ratio ( FY 2015 ) = 189.605

5.927 =31.99

Interest cover ratio ( FY 2016 ) = 213.982

3.857 =55.48

Interest cover ratio ( FY 2017 )= 248.5

10.7 =23.22

Interest cover ratio ( FY 2018 ) = 317.9

16.6 =19.15

(11) Assets turnover

Assets turnover=( Sales Revenue

Assets )

Assets turnover ( FY 2014 ) = 3483.775

859.841 =4.05

Assets turnover ( FY 2015 )=3652.14

895.013 =4.08

Assets turnover ( FY 2016 )= 3954.47

992.381 =3.98

Assets turnover ( FY 2017 )= 5628

2459.8 =2.29

Assets turnover ( FY 2018 ) = 6864.3

2491.7 =2.5

(12) Earnings per share (EPS)

Earnings per share ( EPS )=( Net income

Number of outstanding shares )

Interest Expense

Interest cover ratio ( FY 2014 )= 173.832

8.845 =19.65

Interest cover ratio ( FY 2015 ) = 189.605

5.927 =31.99

Interest cover ratio ( FY 2016 ) = 213.982

3.857 =55.48

Interest cover ratio ( FY 2017 )= 248.5

10.7 =23.22

Interest cover ratio ( FY 2018 ) = 317.9

16.6 =19.15

(11) Assets turnover

Assets turnover=( Sales Revenue

Assets )

Assets turnover ( FY 2014 ) = 3483.775

859.841 =4.05

Assets turnover ( FY 2015 )=3652.14

895.013 =4.08

Assets turnover ( FY 2016 )= 3954.47

992.381 =3.98

Assets turnover ( FY 2017 )= 5628

2459.8 =2.29

Assets turnover ( FY 2018 ) = 6864.3

2491.7 =2.5

(12) Earnings per share (EPS)

Earnings per share ( EPS )=( Net income

Number of outstanding shares )

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

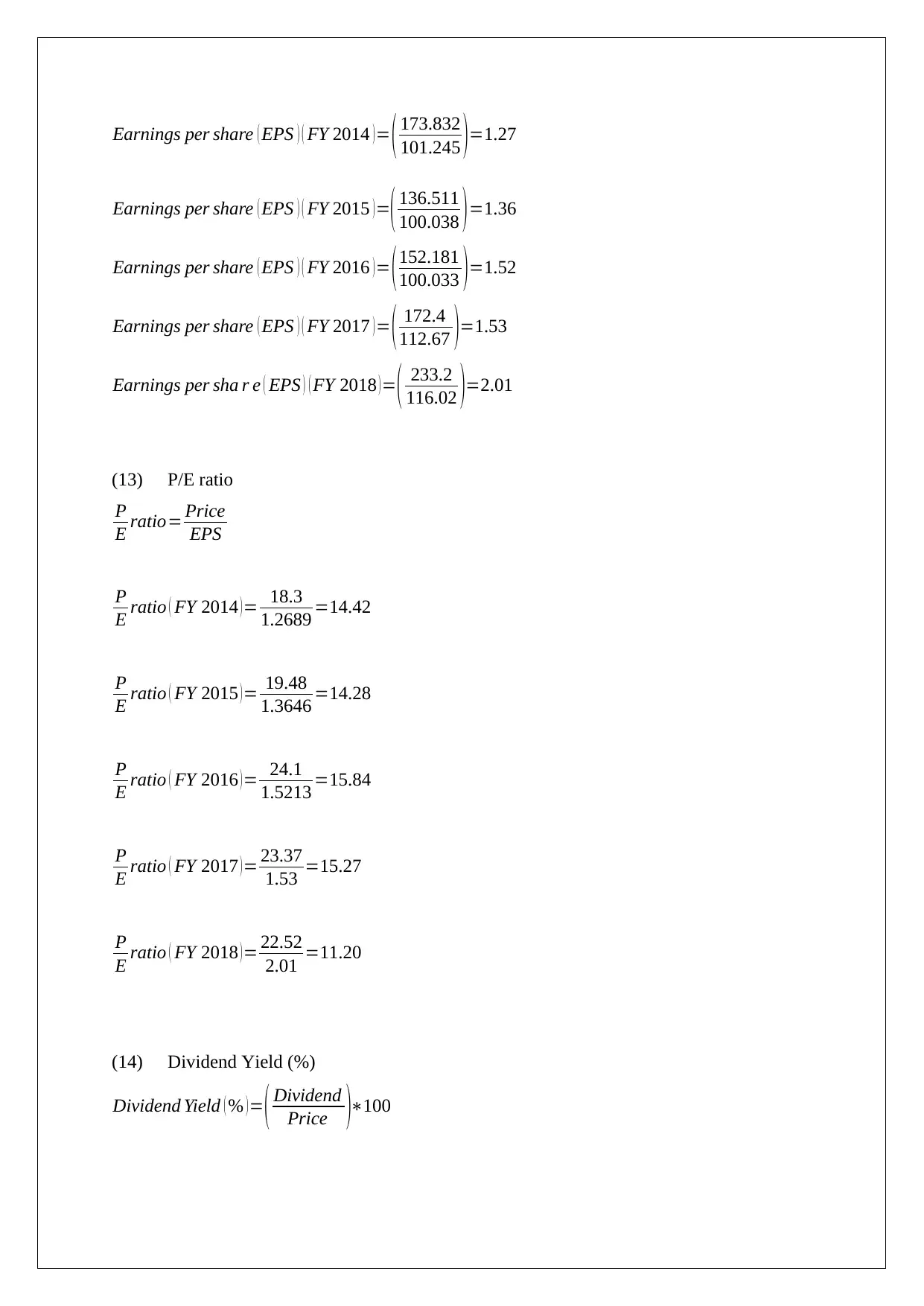

Earnings per share ( EPS ) ( FY 2014 )= ( 173.832

101.245 )=1.27

Earnings per share ( EPS ) ( FY 2015 )=( 136.511

100.038 )=1.36

Earnings per share ( EPS ) ( FY 2016 )= (152.181

100.033 )=1.52

Earnings per share ( EPS ) ( FY 2017 ) = ( 172.4

112.67 )=1.53

Earnings per sha r e ( EPS ) ( FY 2018 ) = ( 233.2

116.02 )=2.01

(13) P/E ratio

P

E ratio= Price

EPS

P

E ratio ( FY 2014 ) = 18.3

1.2689 =14.42

P

E ratio ( FY 2015 ) = 19.48

1.3646 =14.28

P

E ratio ( FY 2016 )= 24.1

1.5213 =15.84

P

E ratio ( FY 2017 )= 23.37

1.53 =15.27

P

E ratio ( FY 2018 )= 22.52

2.01 =11.20

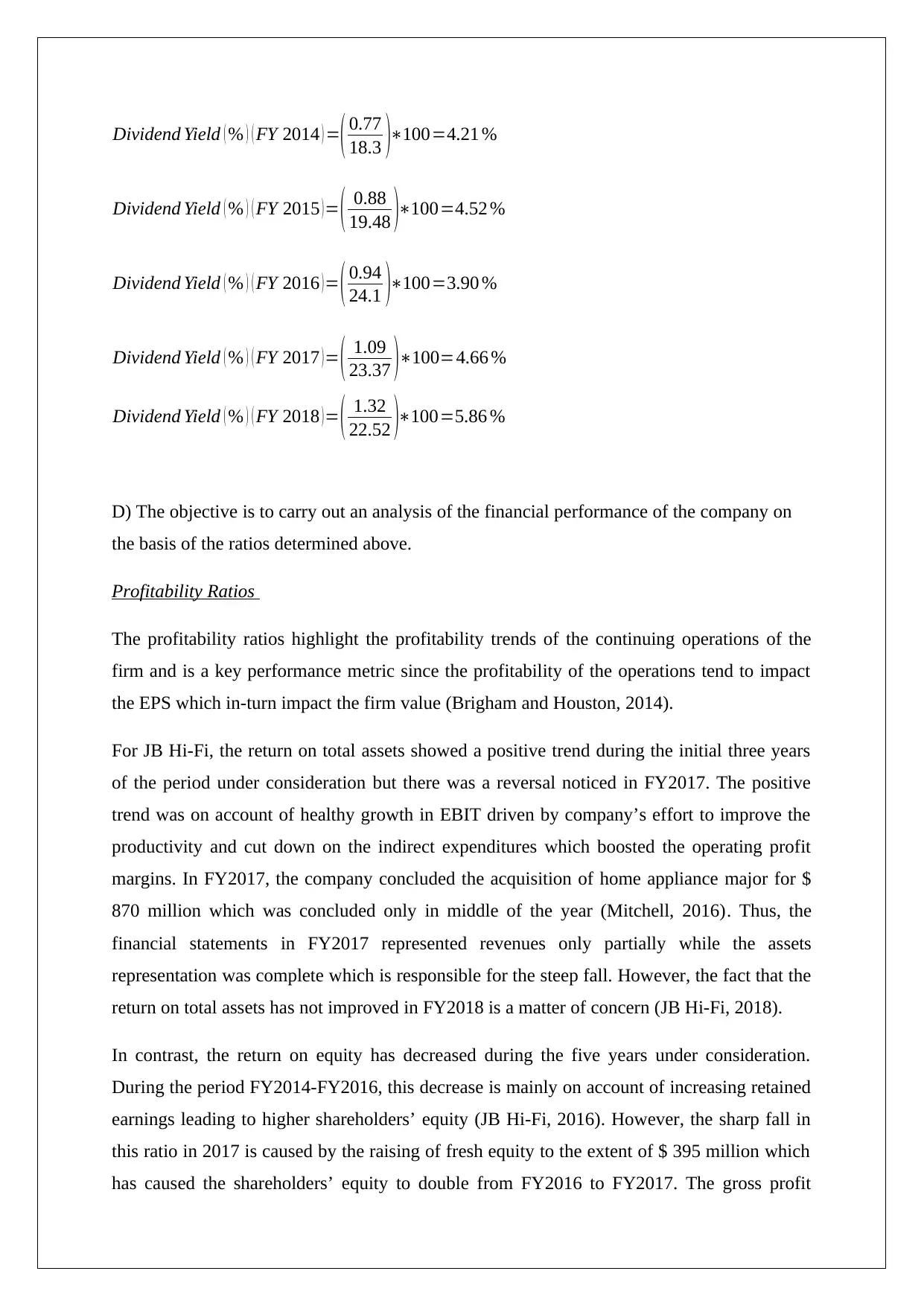

(14) Dividend Yield (%)

Dividend Yield ( % ) = ( Dividend

Price )∗100

101.245 )=1.27

Earnings per share ( EPS ) ( FY 2015 )=( 136.511

100.038 )=1.36

Earnings per share ( EPS ) ( FY 2016 )= (152.181

100.033 )=1.52

Earnings per share ( EPS ) ( FY 2017 ) = ( 172.4

112.67 )=1.53

Earnings per sha r e ( EPS ) ( FY 2018 ) = ( 233.2

116.02 )=2.01

(13) P/E ratio

P

E ratio= Price

EPS

P

E ratio ( FY 2014 ) = 18.3

1.2689 =14.42

P

E ratio ( FY 2015 ) = 19.48

1.3646 =14.28

P

E ratio ( FY 2016 )= 24.1

1.5213 =15.84

P

E ratio ( FY 2017 )= 23.37

1.53 =15.27

P

E ratio ( FY 2018 )= 22.52

2.01 =11.20

(14) Dividend Yield (%)

Dividend Yield ( % ) = ( Dividend

Price )∗100

Dividend Yield ( % ) ( FY 2014 ) =( 0.77

18.3 )∗100=4.21 %

Dividend Yield ( % ) ( FY 2015 ) = ( 0.88

19.48 )∗100=4.52 %

Dividend Yield ( % ) ( FY 2016 )= ( 0.94

24.1 )∗100=3.90 %

Dividend Yield ( % ) ( FY 2017 )= ( 1.09

23.37 )∗100=4.66 %

Dividend Yield ( % ) ( FY 2018 )= ( 1.32

22.52 )∗100=5.86 %

D) The objective is to carry out an analysis of the financial performance of the company on

the basis of the ratios determined above.

Profitability Ratios

The profitability ratios highlight the profitability trends of the continuing operations of the

firm and is a key performance metric since the profitability of the operations tend to impact

the EPS which in-turn impact the firm value (Brigham and Houston, 2014).

For JB Hi-Fi, the return on total assets showed a positive trend during the initial three years

of the period under consideration but there was a reversal noticed in FY2017. The positive

trend was on account of healthy growth in EBIT driven by company’s effort to improve the

productivity and cut down on the indirect expenditures which boosted the operating profit

margins. In FY2017, the company concluded the acquisition of home appliance major for $

870 million which was concluded only in middle of the year (Mitchell, 2016). Thus, the

financial statements in FY2017 represented revenues only partially while the assets

representation was complete which is responsible for the steep fall. However, the fact that the

return on total assets has not improved in FY2018 is a matter of concern (JB Hi-Fi, 2018).

In contrast, the return on equity has decreased during the five years under consideration.

During the period FY2014-FY2016, this decrease is mainly on account of increasing retained

earnings leading to higher shareholders’ equity (JB Hi-Fi, 2016). However, the sharp fall in

this ratio in 2017 is caused by the raising of fresh equity to the extent of $ 395 million which

has caused the shareholders’ equity to double from FY2016 to FY2017. The gross profit

18.3 )∗100=4.21 %

Dividend Yield ( % ) ( FY 2015 ) = ( 0.88

19.48 )∗100=4.52 %

Dividend Yield ( % ) ( FY 2016 )= ( 0.94

24.1 )∗100=3.90 %

Dividend Yield ( % ) ( FY 2017 )= ( 1.09

23.37 )∗100=4.66 %

Dividend Yield ( % ) ( FY 2018 )= ( 1.32

22.52 )∗100=5.86 %

D) The objective is to carry out an analysis of the financial performance of the company on

the basis of the ratios determined above.

Profitability Ratios

The profitability ratios highlight the profitability trends of the continuing operations of the

firm and is a key performance metric since the profitability of the operations tend to impact

the EPS which in-turn impact the firm value (Brigham and Houston, 2014).

For JB Hi-Fi, the return on total assets showed a positive trend during the initial three years

of the period under consideration but there was a reversal noticed in FY2017. The positive

trend was on account of healthy growth in EBIT driven by company’s effort to improve the

productivity and cut down on the indirect expenditures which boosted the operating profit

margins. In FY2017, the company concluded the acquisition of home appliance major for $

870 million which was concluded only in middle of the year (Mitchell, 2016). Thus, the

financial statements in FY2017 represented revenues only partially while the assets

representation was complete which is responsible for the steep fall. However, the fact that the

return on total assets has not improved in FY2018 is a matter of concern (JB Hi-Fi, 2018).

In contrast, the return on equity has decreased during the five years under consideration.

During the period FY2014-FY2016, this decrease is mainly on account of increasing retained

earnings leading to higher shareholders’ equity (JB Hi-Fi, 2016). However, the sharp fall in

this ratio in 2017 is caused by the raising of fresh equity to the extent of $ 395 million which

has caused the shareholders’ equity to double from FY2016 to FY2017. The gross profit

margins and net profit margins of the company both showed positive trend during FY2014-

FY2016 but have reversed in FY2017 since the profitability margins for the acquired

business (i.e. “The Good Guys”) is lower in comparison to JB Hi-Fi (JB Hi-Fi, 2018).

Efficiency Ratios

Efficiency ratios provide a measure of the underlying operational and asset usage efficiency

of the company. The first key measure is inventory turnover period which has shown

miniscule fluctuation in the five year period. Hence, there has been no improvement in this

regards. Any improvement in this aspect would be captured by the decrease in inventory

turnover period which would imply lower time for conversion of inventory into sales

(Damodaran, 2014).

The second key measure is settlement period for debtor which has been on rise during the

five year period. This is not in the best interest of the company considering that a longer

settlement period would imply a longer cash cycle which would automatically lead to higher

working capital requirement (Gitman, Juchaou and Flanagan, 2017). On the asset turnover

front, during the initial three years, there was only a slight deterioration but it has been

significant in FY2017. This can be explained by the acquisition happening in the middle of

the financial year owing to which only part of the revenues of the acquitted entity were

reflected in FY2017 income statement (JB Hi-Fi, 2018).

Liquidity Ratios

Liquidity ratios assume importance especially for creditors as these highlight the ease with

which the short term obligations would be met by the company (Brigham and Houston,

2014). Two key ratios in this regards are current ratio and quick ratio. The current ratio in the

five year period under consideration is on the decline but has witnessed a significant

reduction only in FY2017 which is on account of the acquired entity having lower liquidity

ratios in comparison to JB Hi-Fi. A silver lining in regards to current ratio is that there is no

decline in FY2018. In regards to quick ratio, no major changes have occurred during the five

year period and stability is maintained which is reflective of the fact that major fluctuations in

current asset was experienced owing to inventory ((JB Hi-Fi, 2018; 2016; 2014).

Financial Gearing Ratios

FY2016 but have reversed in FY2017 since the profitability margins for the acquired

business (i.e. “The Good Guys”) is lower in comparison to JB Hi-Fi (JB Hi-Fi, 2018).

Efficiency Ratios

Efficiency ratios provide a measure of the underlying operational and asset usage efficiency

of the company. The first key measure is inventory turnover period which has shown

miniscule fluctuation in the five year period. Hence, there has been no improvement in this

regards. Any improvement in this aspect would be captured by the decrease in inventory

turnover period which would imply lower time for conversion of inventory into sales

(Damodaran, 2014).

The second key measure is settlement period for debtor which has been on rise during the

five year period. This is not in the best interest of the company considering that a longer

settlement period would imply a longer cash cycle which would automatically lead to higher

working capital requirement (Gitman, Juchaou and Flanagan, 2017). On the asset turnover

front, during the initial three years, there was only a slight deterioration but it has been

significant in FY2017. This can be explained by the acquisition happening in the middle of

the financial year owing to which only part of the revenues of the acquitted entity were

reflected in FY2017 income statement (JB Hi-Fi, 2018).

Liquidity Ratios

Liquidity ratios assume importance especially for creditors as these highlight the ease with

which the short term obligations would be met by the company (Brigham and Houston,

2014). Two key ratios in this regards are current ratio and quick ratio. The current ratio in the

five year period under consideration is on the decline but has witnessed a significant

reduction only in FY2017 which is on account of the acquired entity having lower liquidity

ratios in comparison to JB Hi-Fi. A silver lining in regards to current ratio is that there is no

decline in FY2018. In regards to quick ratio, no major changes have occurred during the five

year period and stability is maintained which is reflective of the fact that major fluctuations in

current asset was experienced owing to inventory ((JB Hi-Fi, 2018; 2016; 2014).

Financial Gearing Ratios

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

These ratios tend to signify the ease with which the company can fulfil long term

commitments (Damodaran, 2014). There is a positive trend in regards to debt to assets ratio

which has reached the lowest point at the end of FY2016. This highlights the minimum

leveraging of the balance sheet was achieved at the end of FY2016 (JB Hi-Fi, 2016).

However, in FY2017, there is a sudden jump which does not come as a surprise considering

that company raised debt to the tune of $ 500 million to fund the acquisition. A positive

observation is the return of thee trend of lowering debt to assets ratio in FY2018 which

highlights management commitment to lowering the debt on the books (JB Hi-Fi, 2018).

The peaking of the interest cover also happens in FY2016 since the interest cost was at the

lowest point and operating profit at a high point. However, in FY2017 there is a decline in

this regards as the interest expense has shot up in a disproportionate manner as compared to

operating profit. Despite the decline in interest cover in FY2017 and FY2018, the company is

able to provide enough cover to meet the interest obligations (JB Hi-Fi, 2018).

Investment Ratios

The EPS of the company has witnessed a strong growth in the five years under consideration

but majority of this growth has been achieved in FY2018. The key contribution of this growth

is not the superior performance of the company but the acquisition of another entity with

significant profits and complementary product line of home appliances. The P/E ratio also is

indicative of lacklustre organic growth of business owing to which there has not been any P/E

expansion and in the recent times it has contracted on account of the acquisition and the

related risks assumed. From an investor perspective, the healthy divided yield is a significant

positive for the stock (Gitman, Juchaou and Flanagan, 2017).

E) To compare the cash flow statements for the year ending June 30, 2017 and June 30, 2018,

the three key aspects of the statement have been compared with each other.

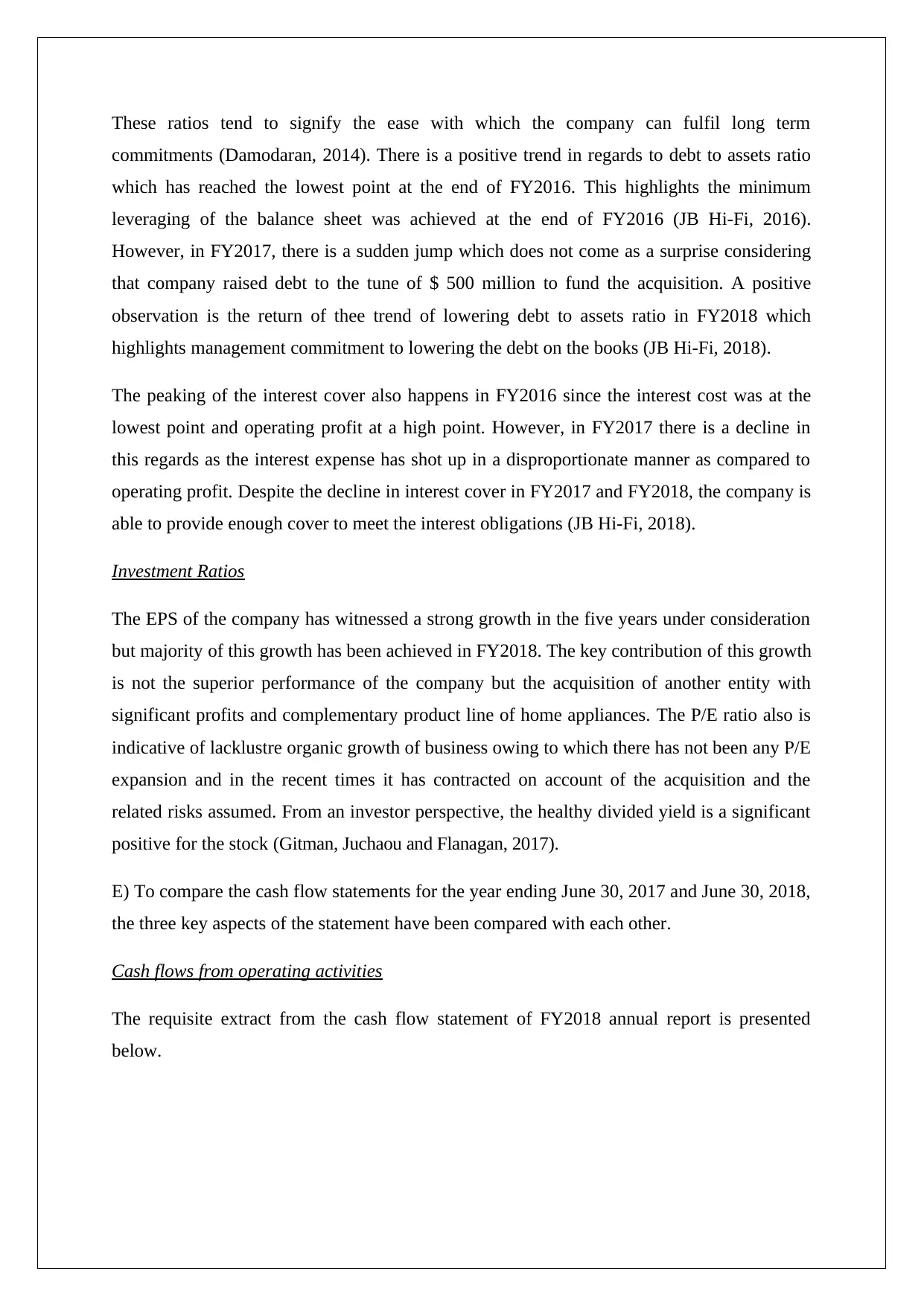

Cash flows from operating activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

commitments (Damodaran, 2014). There is a positive trend in regards to debt to assets ratio

which has reached the lowest point at the end of FY2016. This highlights the minimum

leveraging of the balance sheet was achieved at the end of FY2016 (JB Hi-Fi, 2016).

However, in FY2017, there is a sudden jump which does not come as a surprise considering

that company raised debt to the tune of $ 500 million to fund the acquisition. A positive

observation is the return of thee trend of lowering debt to assets ratio in FY2018 which

highlights management commitment to lowering the debt on the books (JB Hi-Fi, 2018).

The peaking of the interest cover also happens in FY2016 since the interest cost was at the

lowest point and operating profit at a high point. However, in FY2017 there is a decline in

this regards as the interest expense has shot up in a disproportionate manner as compared to

operating profit. Despite the decline in interest cover in FY2017 and FY2018, the company is

able to provide enough cover to meet the interest obligations (JB Hi-Fi, 2018).

Investment Ratios

The EPS of the company has witnessed a strong growth in the five years under consideration

but majority of this growth has been achieved in FY2018. The key contribution of this growth

is not the superior performance of the company but the acquisition of another entity with

significant profits and complementary product line of home appliances. The P/E ratio also is

indicative of lacklustre organic growth of business owing to which there has not been any P/E

expansion and in the recent times it has contracted on account of the acquisition and the

related risks assumed. From an investor perspective, the healthy divided yield is a significant

positive for the stock (Gitman, Juchaou and Flanagan, 2017).

E) To compare the cash flow statements for the year ending June 30, 2017 and June 30, 2018,

the three key aspects of the statement have been compared with each other.

Cash flows from operating activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

The cash receipts from customers have shown a significant jump for FY2018 when compared

with the previous year. However, most of these gains are neutralised by the corresponding

rise in cash outflows to customers and suppliers in FY2018. The finance and interest related

outflow have increased in FY2018 to $ 15 million as compared to corresponding value of

$9.3 million in FY2017. Further, on account of increased profits, the tax outflow has been

higher in FY2018 when compared to the previous year. Overall, cash generated from

operating activities has shown increase of $ 101.5 million in FY2018 which is positive for the

company (JB Hi-Fi, 2018).

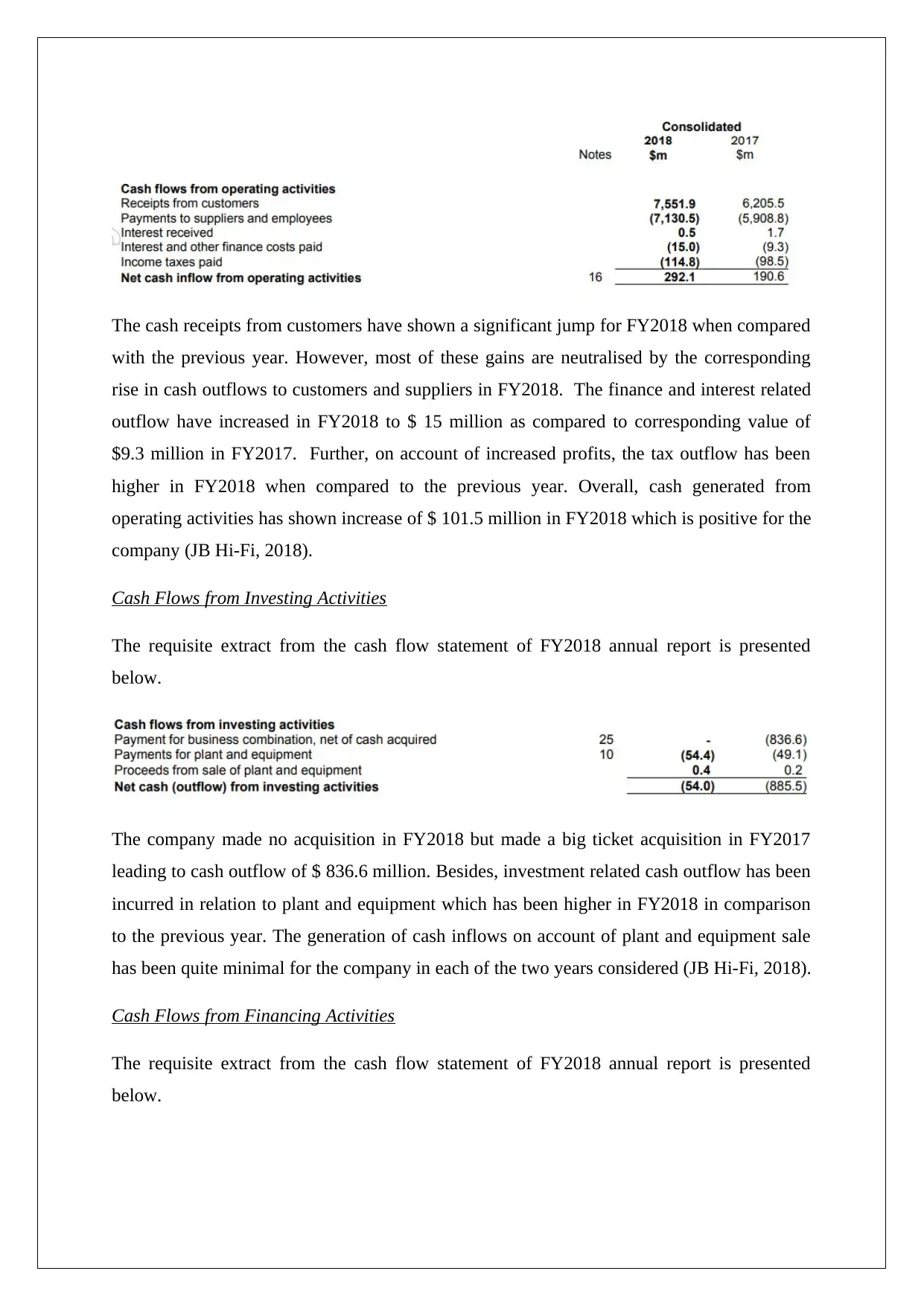

Cash Flows from Investing Activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

The company made no acquisition in FY2018 but made a big ticket acquisition in FY2017

leading to cash outflow of $ 836.6 million. Besides, investment related cash outflow has been

incurred in relation to plant and equipment which has been higher in FY2018 in comparison

to the previous year. The generation of cash inflows on account of plant and equipment sale

has been quite minimal for the company in each of the two years considered (JB Hi-Fi, 2018).

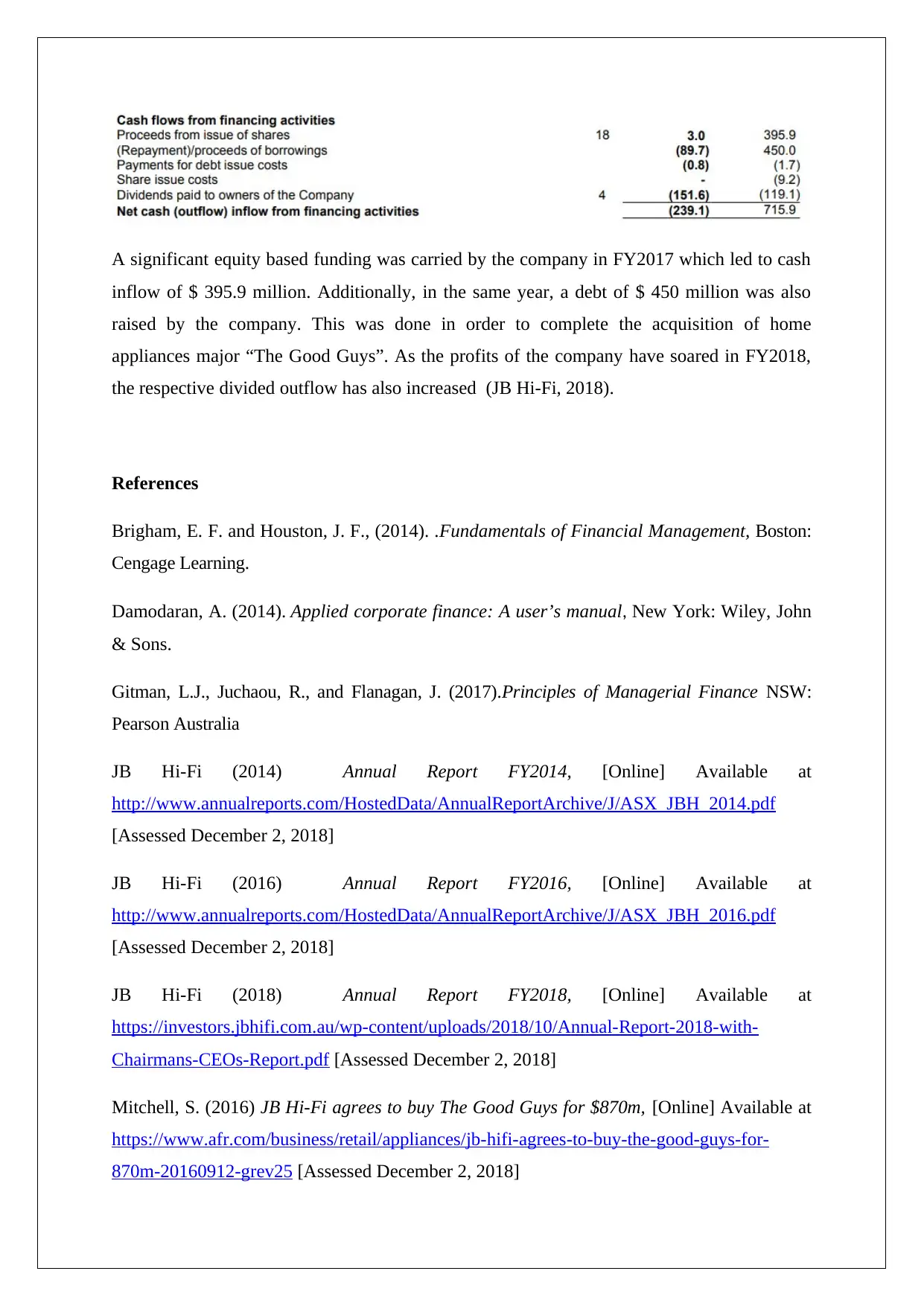

Cash Flows from Financing Activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

with the previous year. However, most of these gains are neutralised by the corresponding

rise in cash outflows to customers and suppliers in FY2018. The finance and interest related

outflow have increased in FY2018 to $ 15 million as compared to corresponding value of

$9.3 million in FY2017. Further, on account of increased profits, the tax outflow has been

higher in FY2018 when compared to the previous year. Overall, cash generated from

operating activities has shown increase of $ 101.5 million in FY2018 which is positive for the

company (JB Hi-Fi, 2018).

Cash Flows from Investing Activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

The company made no acquisition in FY2018 but made a big ticket acquisition in FY2017

leading to cash outflow of $ 836.6 million. Besides, investment related cash outflow has been

incurred in relation to plant and equipment which has been higher in FY2018 in comparison

to the previous year. The generation of cash inflows on account of plant and equipment sale

has been quite minimal for the company in each of the two years considered (JB Hi-Fi, 2018).

Cash Flows from Financing Activities

The requisite extract from the cash flow statement of FY2018 annual report is presented

below.

A significant equity based funding was carried by the company in FY2017 which led to cash

inflow of $ 395.9 million. Additionally, in the same year, a debt of $ 450 million was also

raised by the company. This was done in order to complete the acquisition of home

appliances major “The Good Guys”. As the profits of the company have soared in FY2018,

the respective divided outflow has also increased (JB Hi-Fi, 2018).

References

Brigham, E. F. and Houston, J. F., (2014). .Fundamentals of Financial Management, Boston:

Cengage Learning.

Damodaran, A. (2014). Applied corporate finance: A user’s manual, New York: Wiley, John

& Sons.

Gitman, L.J., Juchaou, R., and Flanagan, J. (2017).Principles of Managerial Finance NSW:

Pearson Australia

JB Hi-Fi (2014) Annual Report FY2014, [Online] Available at

http://www.annualreports.com/HostedData/AnnualReportArchive/J/ASX_JBH_2014.pdf

[Assessed December 2, 2018]

JB Hi-Fi (2016) Annual Report FY2016, [Online] Available at

http://www.annualreports.com/HostedData/AnnualReportArchive/J/ASX_JBH_2016.pdf

[Assessed December 2, 2018]

JB Hi-Fi (2018) Annual Report FY2018, [Online] Available at

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Assessed December 2, 2018]

Mitchell, S. (2016) JB Hi-Fi agrees to buy The Good Guys for $870m, [Online] Available at

https://www.afr.com/business/retail/appliances/jb-hifi-agrees-to-buy-the-good-guys-for-

870m-20160912-grev25 [Assessed December 2, 2018]

inflow of $ 395.9 million. Additionally, in the same year, a debt of $ 450 million was also

raised by the company. This was done in order to complete the acquisition of home

appliances major “The Good Guys”. As the profits of the company have soared in FY2018,

the respective divided outflow has also increased (JB Hi-Fi, 2018).

References

Brigham, E. F. and Houston, J. F., (2014). .Fundamentals of Financial Management, Boston:

Cengage Learning.

Damodaran, A. (2014). Applied corporate finance: A user’s manual, New York: Wiley, John

& Sons.

Gitman, L.J., Juchaou, R., and Flanagan, J. (2017).Principles of Managerial Finance NSW:

Pearson Australia

JB Hi-Fi (2014) Annual Report FY2014, [Online] Available at

http://www.annualreports.com/HostedData/AnnualReportArchive/J/ASX_JBH_2014.pdf

[Assessed December 2, 2018]

JB Hi-Fi (2016) Annual Report FY2016, [Online] Available at

http://www.annualreports.com/HostedData/AnnualReportArchive/J/ASX_JBH_2016.pdf

[Assessed December 2, 2018]

JB Hi-Fi (2018) Annual Report FY2018, [Online] Available at

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Assessed December 2, 2018]

Mitchell, S. (2016) JB Hi-Fi agrees to buy The Good Guys for $870m, [Online] Available at

https://www.afr.com/business/retail/appliances/jb-hifi-agrees-to-buy-the-good-guys-for-

870m-20160912-grev25 [Assessed December 2, 2018]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.