Accounting for Managers Assignment Solution: ACC00724 Analysis

VerifiedAdded on 2023/06/07

|10

|1338

|271

Homework Assignment

AI Summary

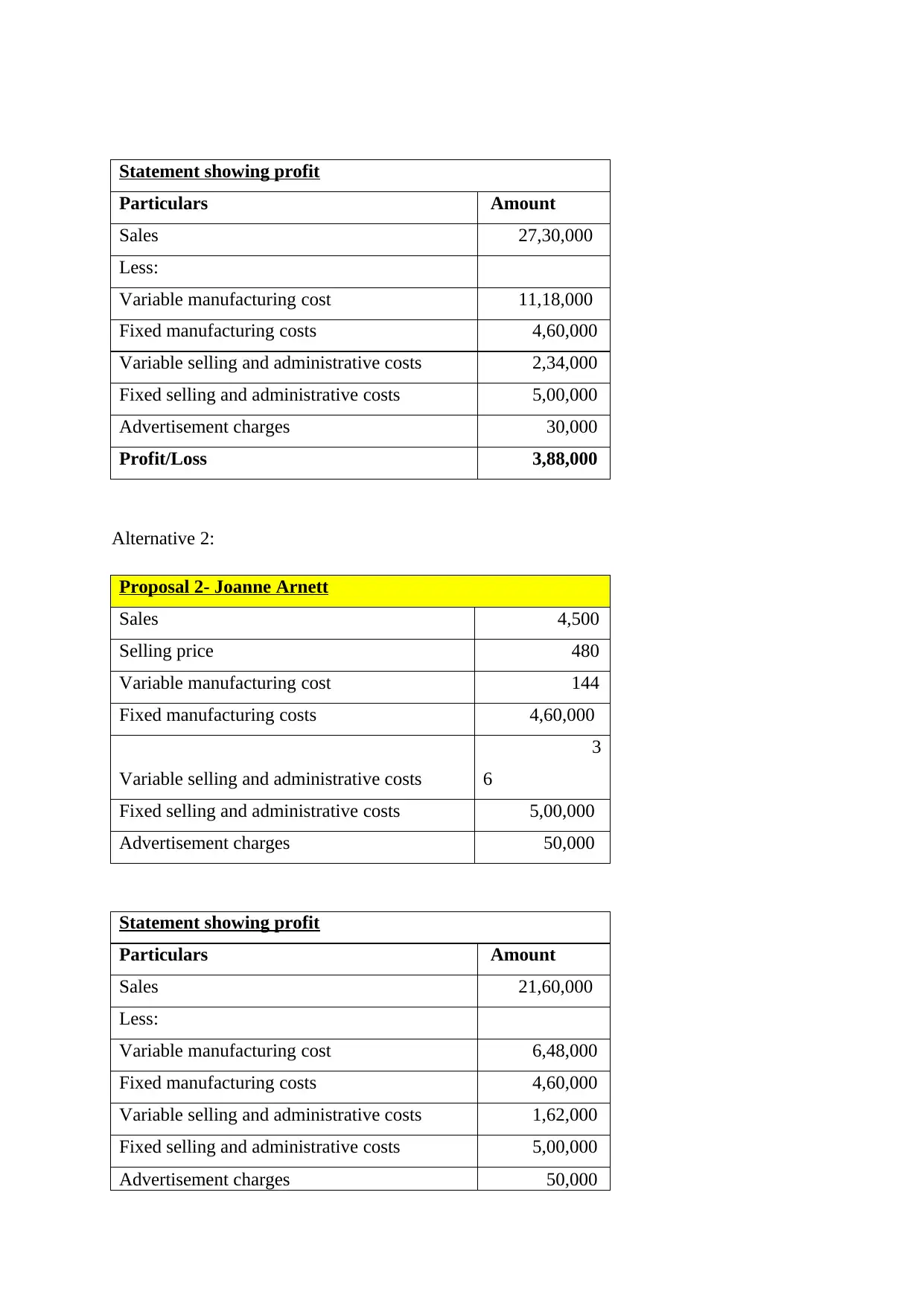

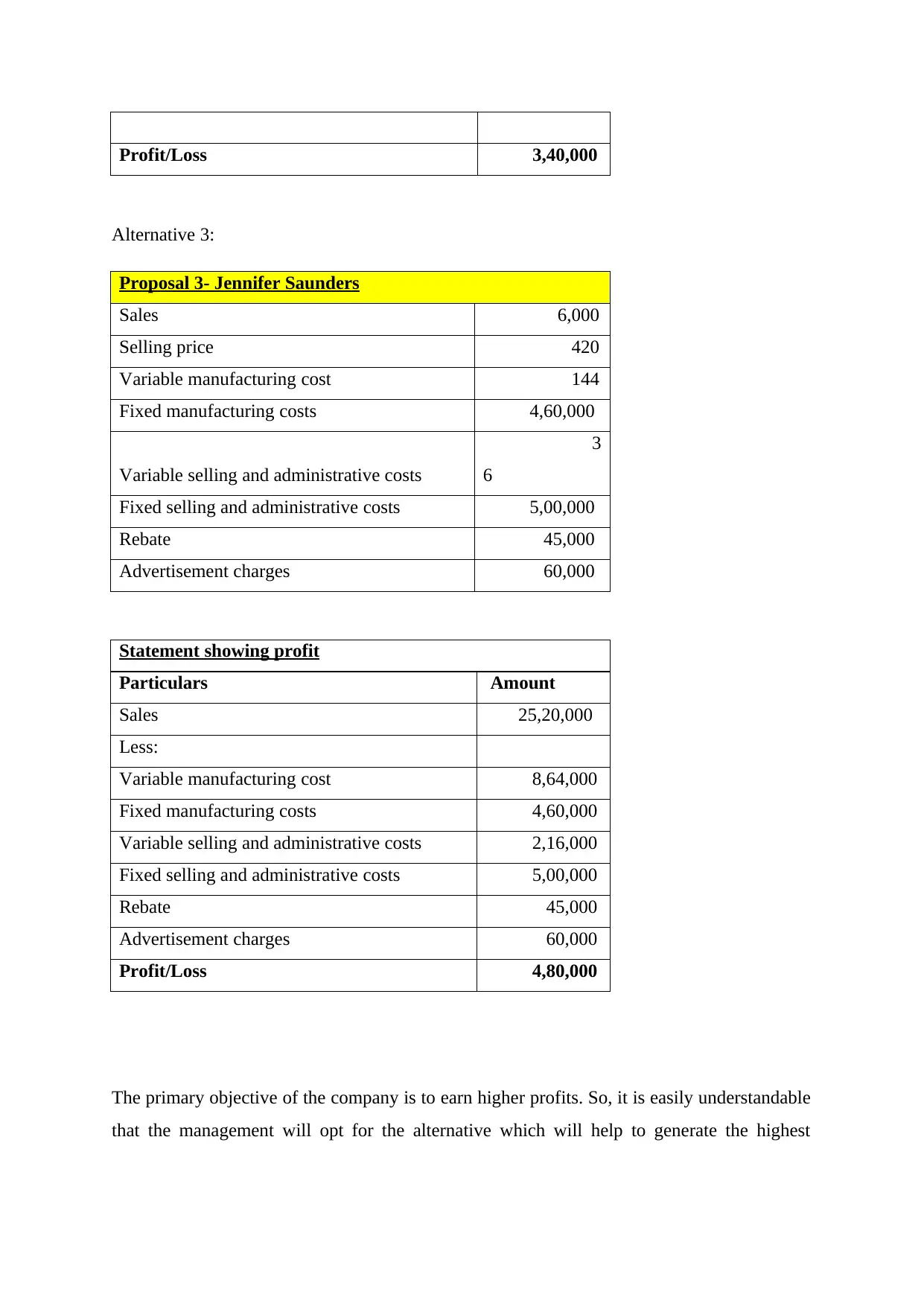

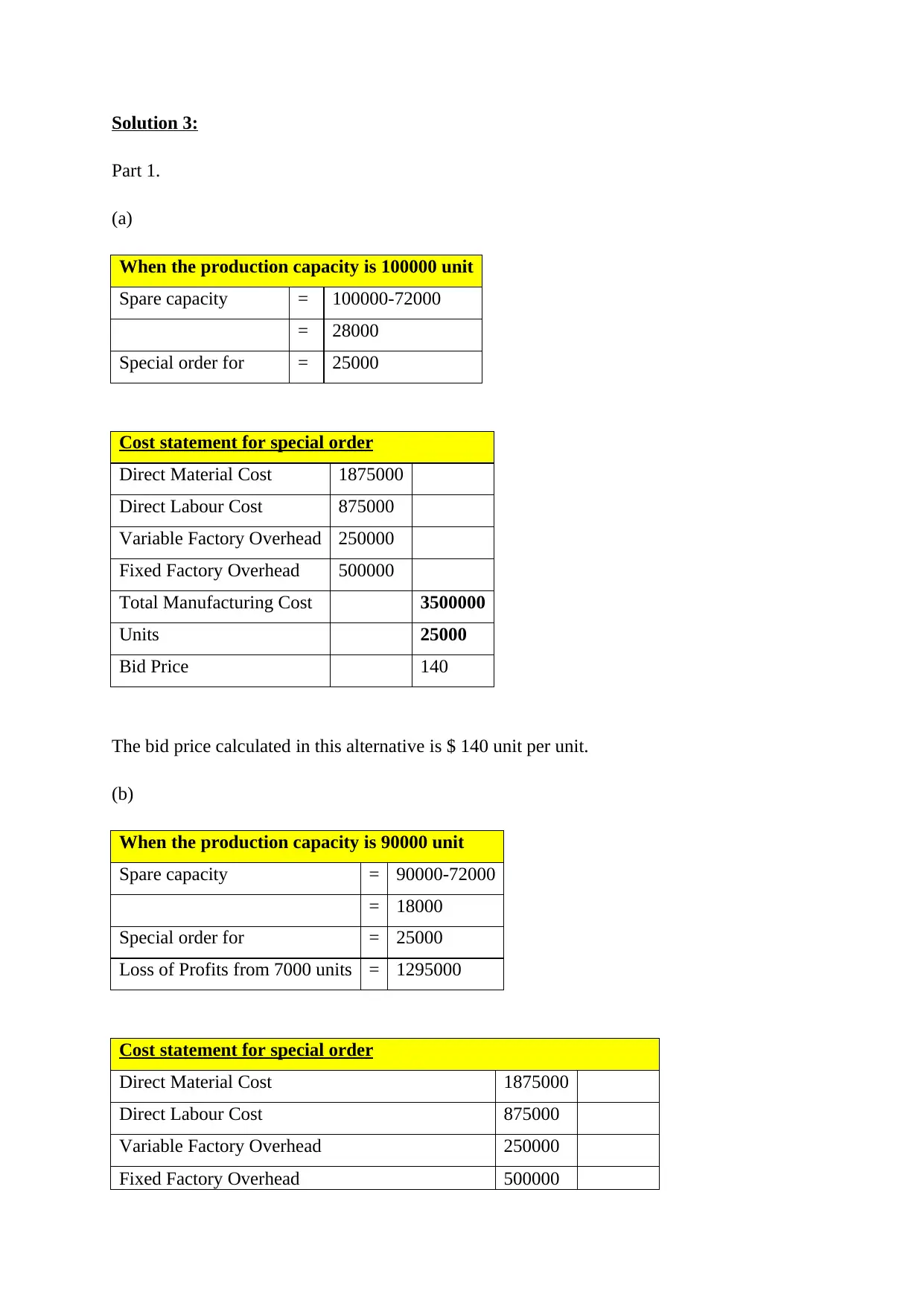

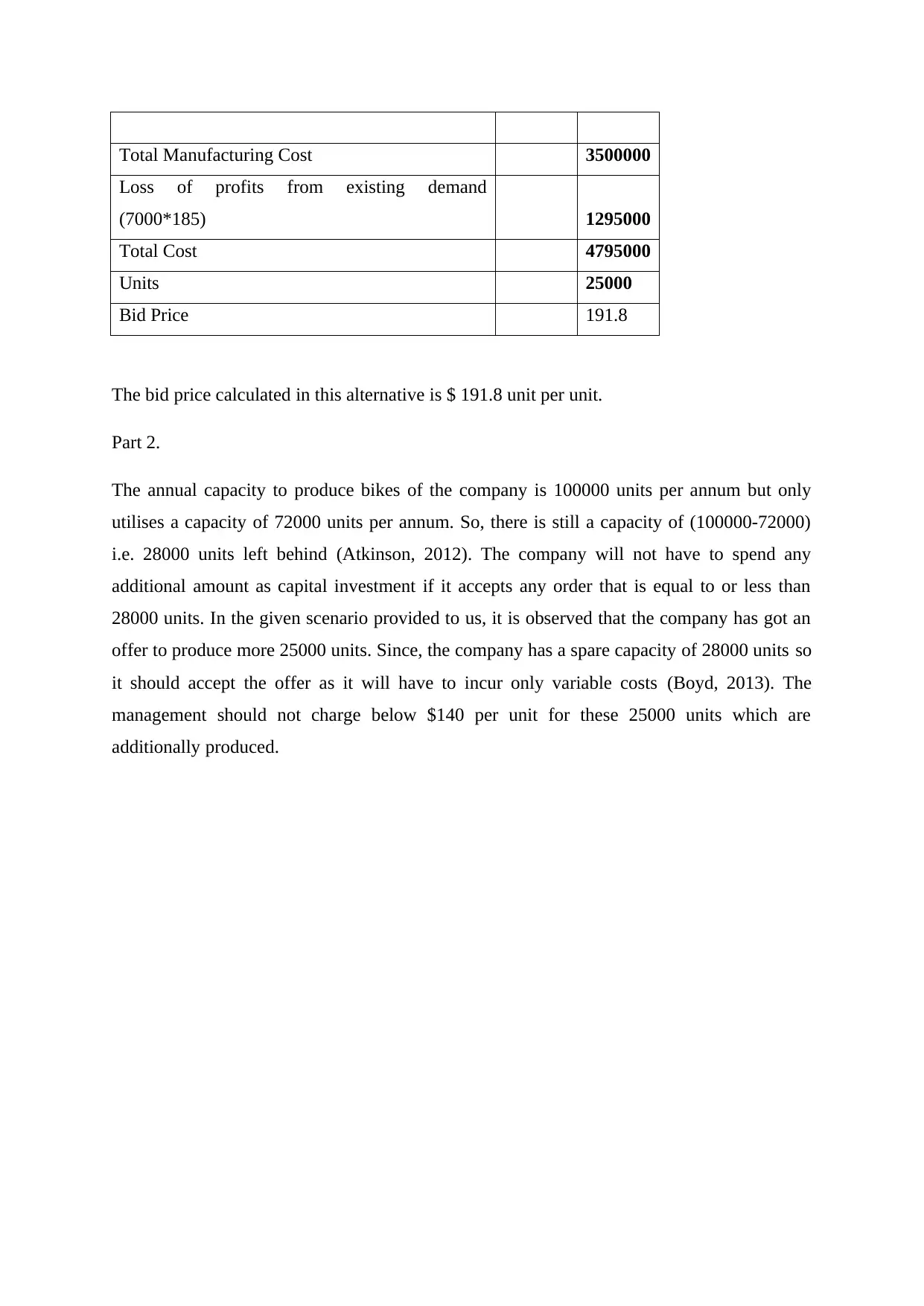

This assignment solution for Accounting for Managers (ACC00724) presents a comprehensive analysis of financial data and management accounting principles. The solution begins with a calculation of the cash cycle period for a company over a five-year period, followed by an evaluation of cash flow trends, particularly from operating activities, based on the Statement of Cash Flows. The assignment then delves into a case study involving Telesmart Ltd., a smartphone manufacturer, analyzing various proposals to improve profitability. The solution includes detailed calculations of profit/loss under different scenarios and recommends the optimal course of action based on quantitative and qualitative factors. Finally, the assignment addresses a special order decision, determining the bid price based on different production capacity scenarios and explaining the rationale for accepting the order. The solution incorporates relevant cost accounting concepts and provides a bibliography of supporting references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.