Depreciation Methods: A Comparative Analysis of Qantas and Virgin Ltd

VerifiedAdded on 2023/06/13

|10

|2267

|412

Report

AI Summary

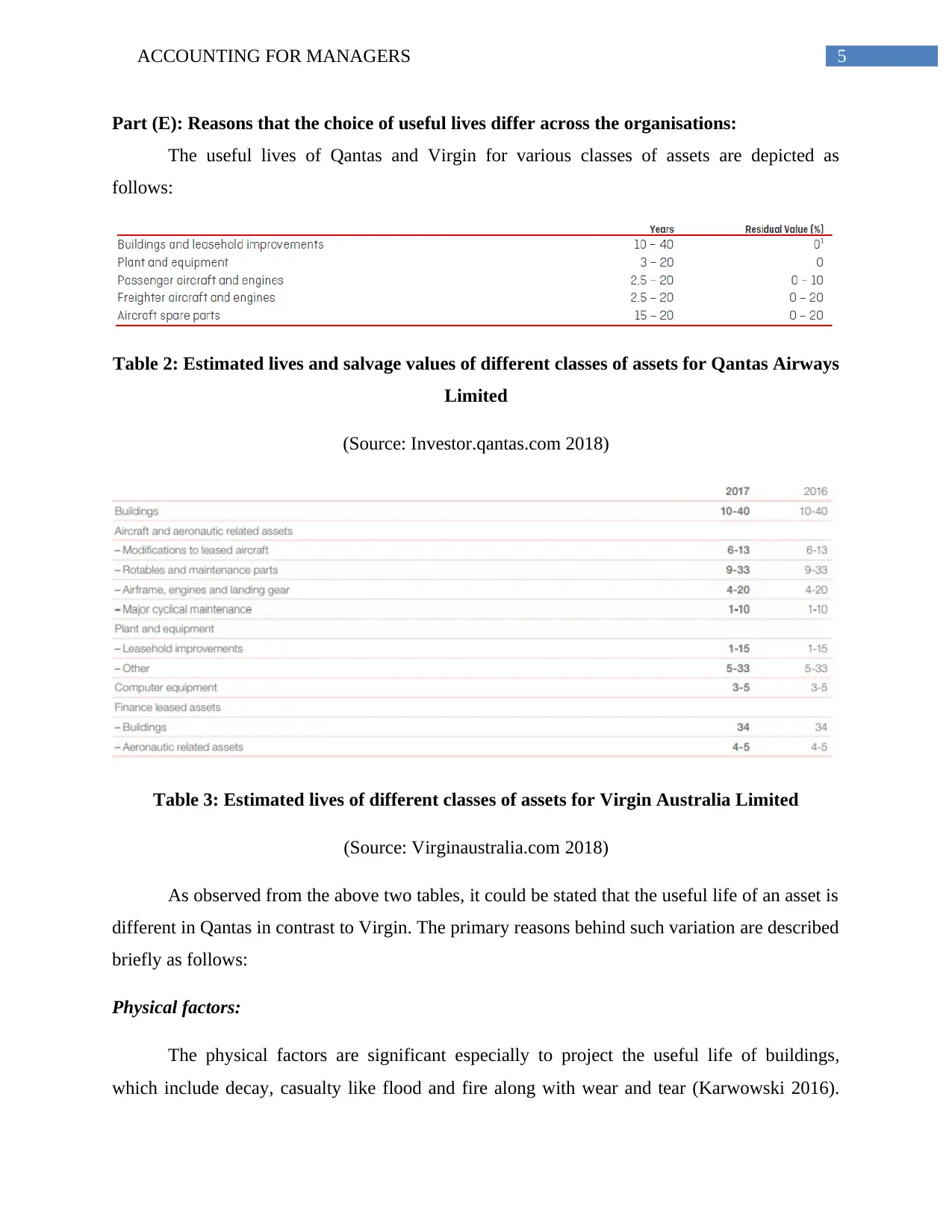

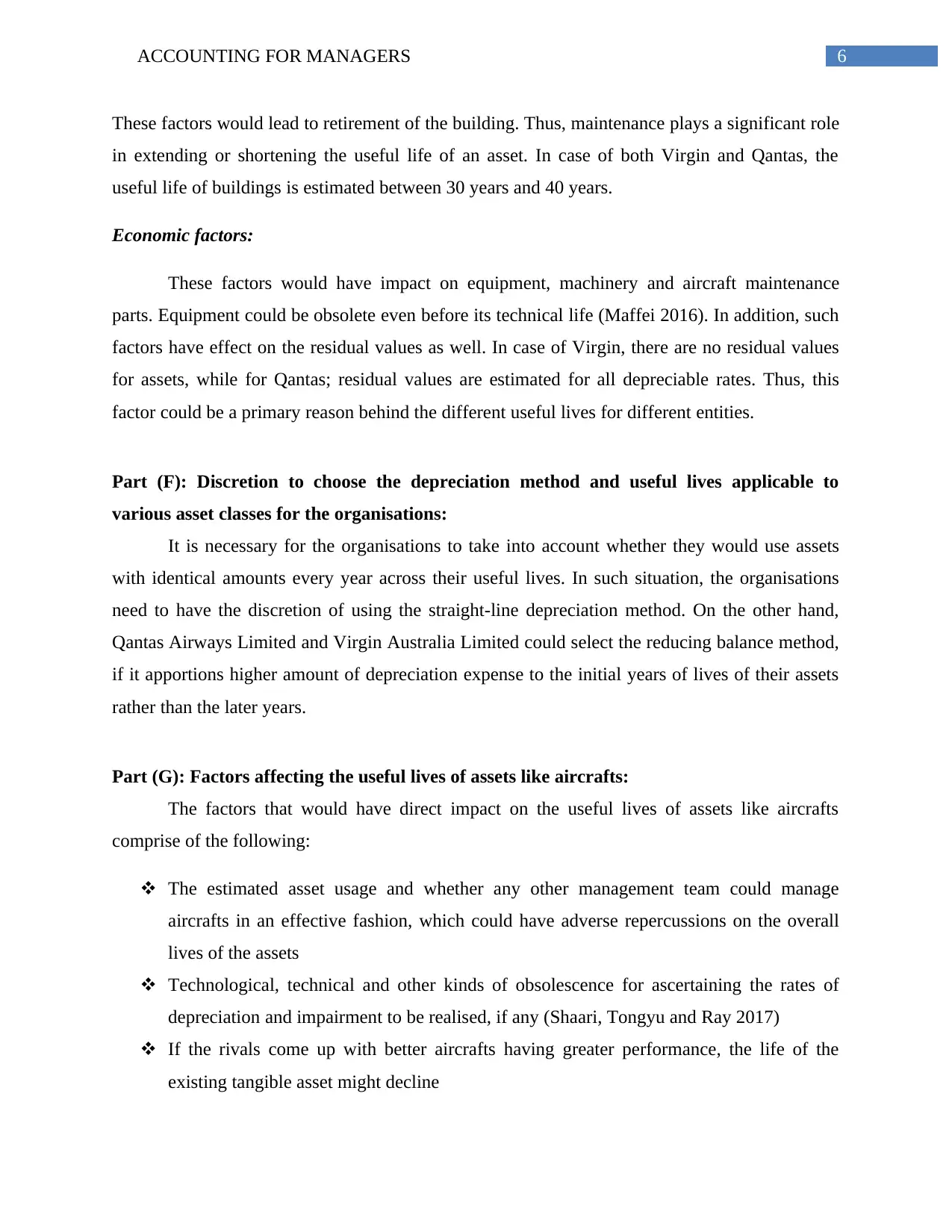

This report provides a detailed analysis of depreciation methods and impairment reporting as practiced by Qantas Airways Limited and Virgin Australia Limited. It begins by defining depreciation and outlining current reporting requirements based on accounting standards, including the cost and matching principles. The report then describes two common depreciation methods: straight-line and reducing balance, and analyzes the 2017 annual reports of Qantas and Virgin Australia to illustrate how depreciation and impairment are recorded. It comments on the effect of differing depreciation rates on the profits of both companies and suggests reasons for the variations in the useful lives of assets across the entities. The report also debates the discretion entities have in choosing depreciation methods and useful lives, identifies factors affecting the useful lives of assets like aircraft, and defines asset impairment, outlining the current reporting requirements in the context of Qantas and Virgin Australia. This comprehensive analysis offers valuable insights into the financial accounting practices of major airline companies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.