Grafton Pty Ltd Financial Analysis - ACC00724 Assignment

VerifiedAdded on 2022/08/20

|7

|1182

|285

Homework Assignment

AI Summary

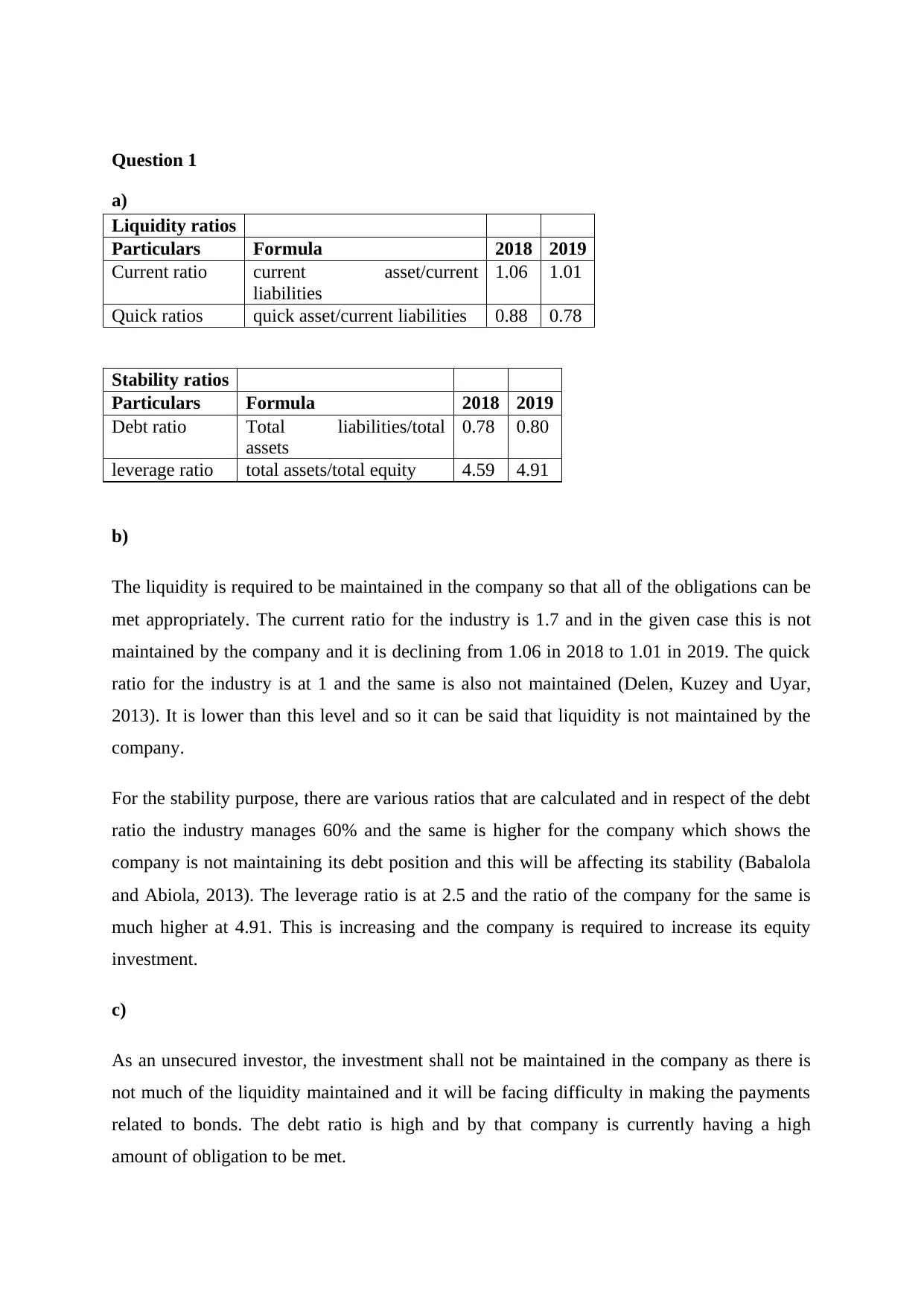

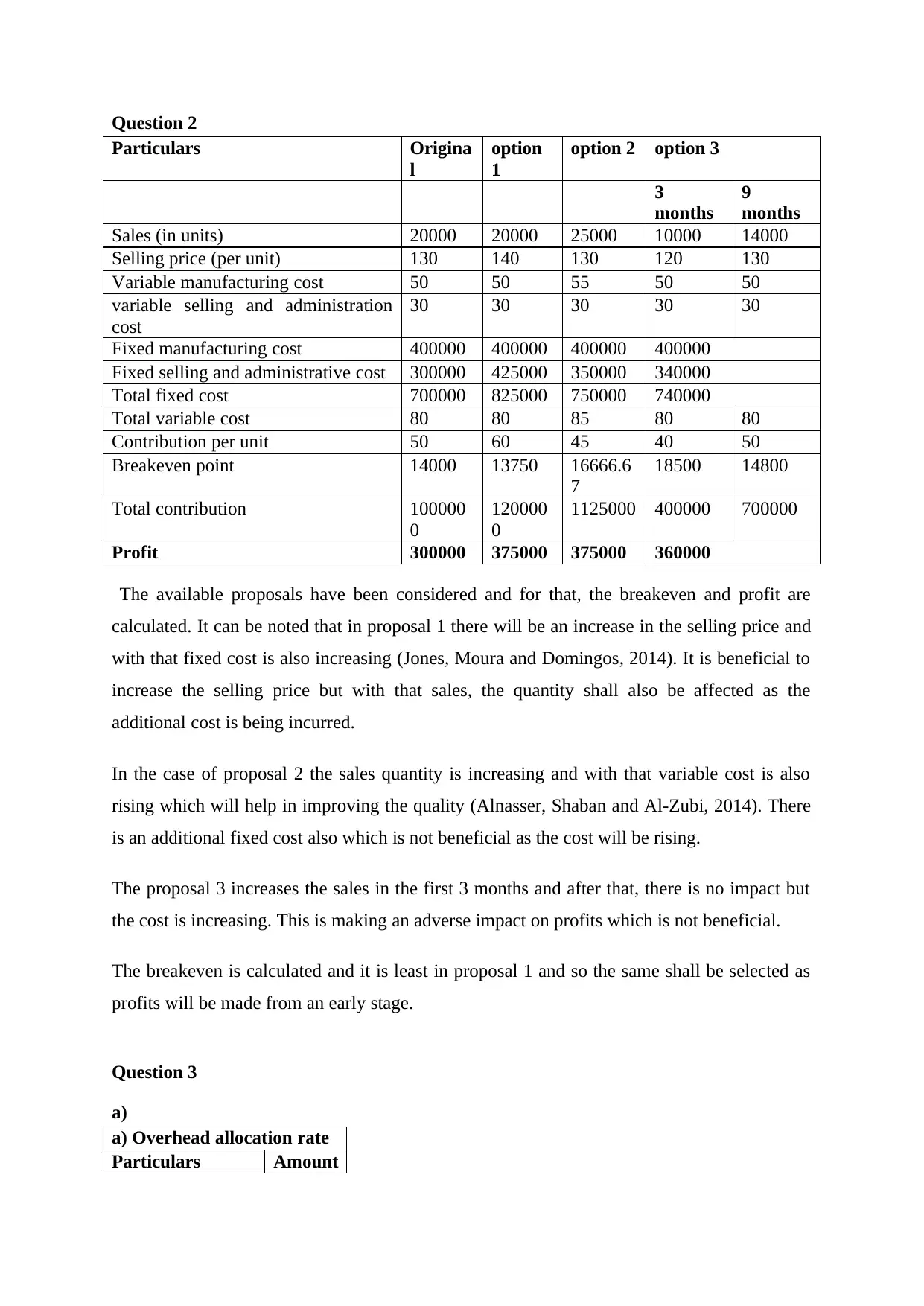

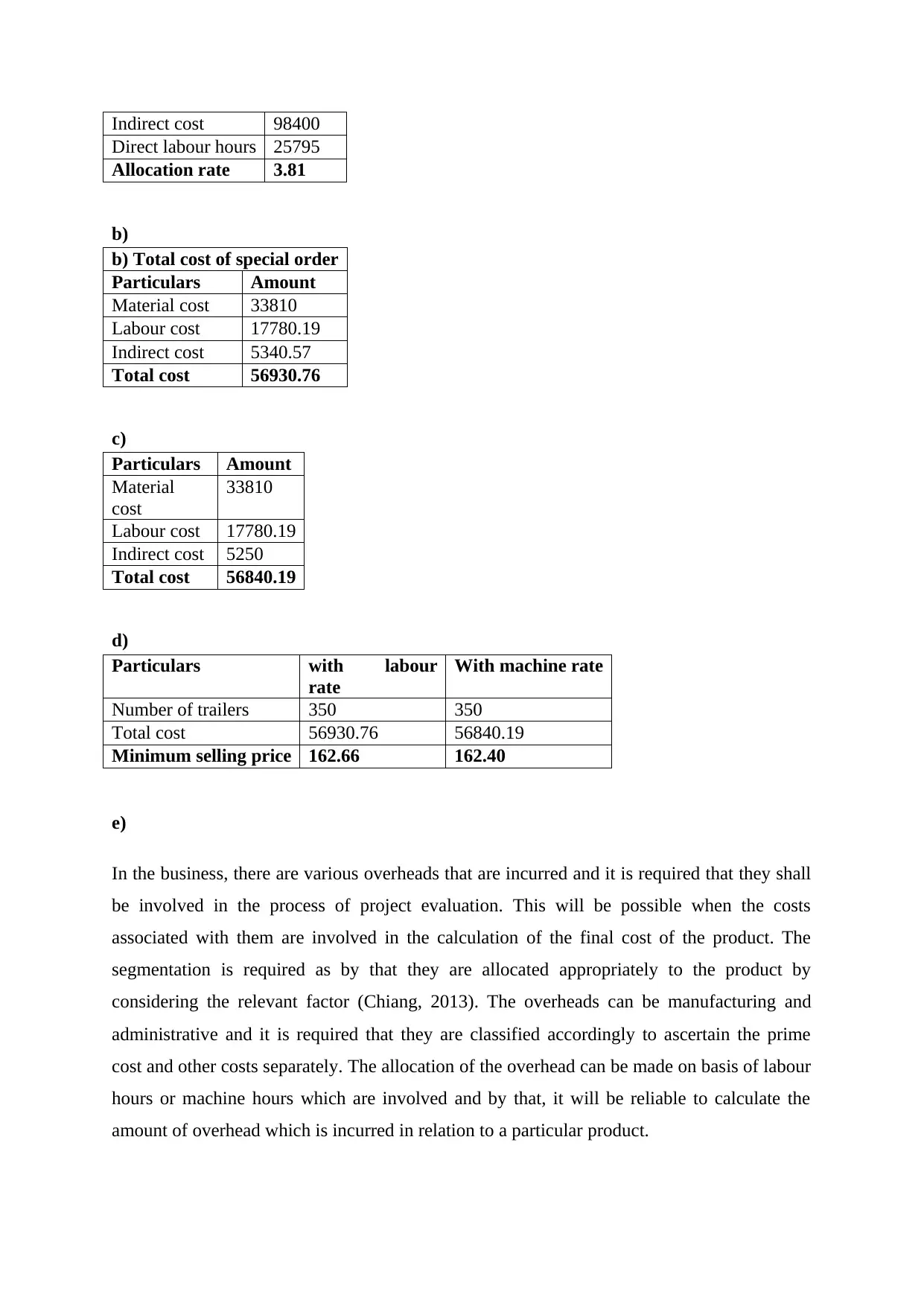

This assignment analyzes the financial performance of Grafton Pty Ltd using financial ratios. It begins with calculating liquidity and stability ratios for 2018 and 2019, including current, quick, debt, and leverage ratios, and evaluates their implications. The analysis then explores different business proposals, calculating breakeven points and profits to determine the most favorable option. Finally, it delves into overhead allocation, calculating the overhead allocation rate and total cost for a special order using both labor and machine hour allocation methods, and discusses the importance of segmentation in overhead allocation for improved decision-making. The assignment provides a comprehensive overview of financial statement analysis and its practical application in managerial accounting.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.