Financial Analysis and Performance Comparison: Santos Ltd and Woodside

VerifiedAdded on 2022/12/23

|9

|1786

|4

Report

AI Summary

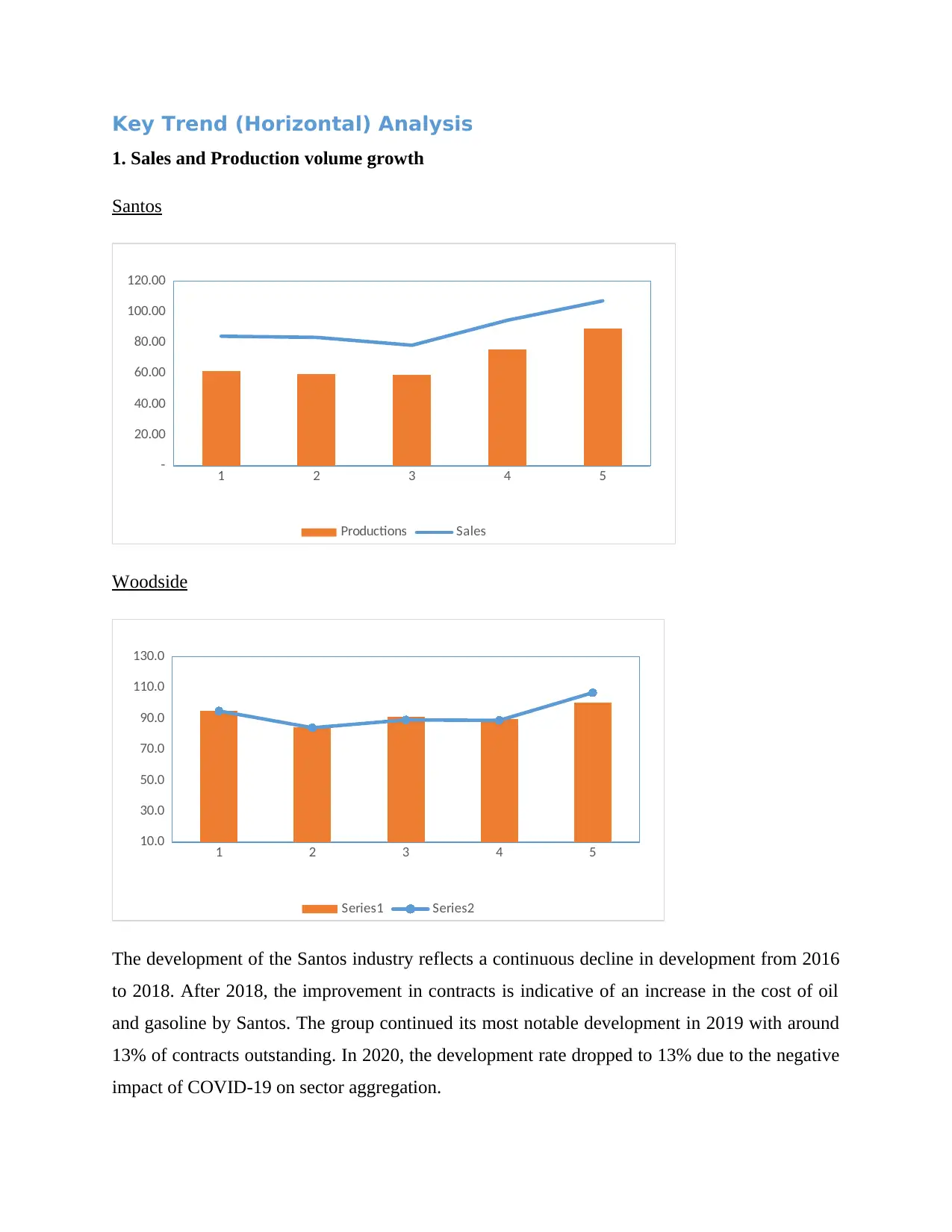

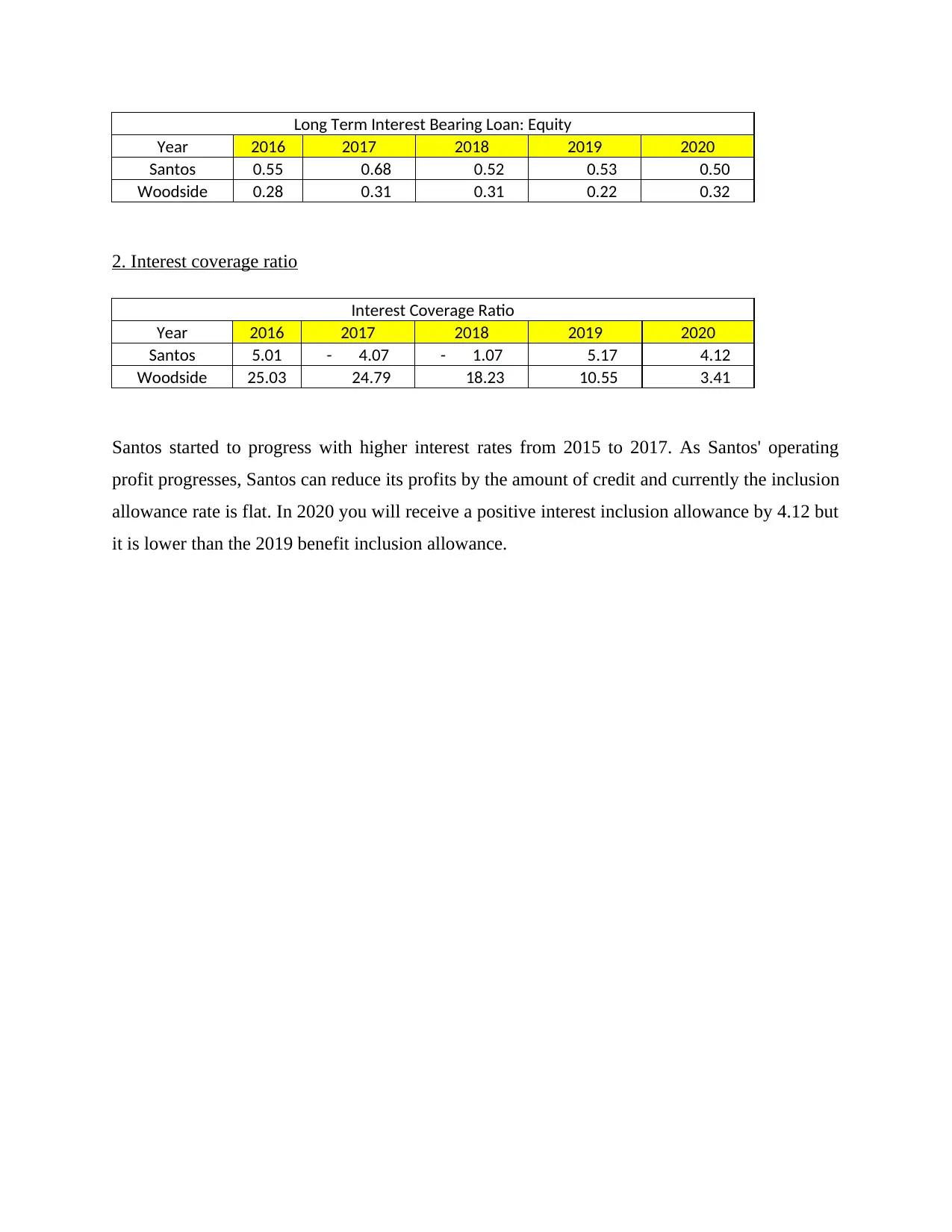

This report provides a comprehensive financial analysis comparing the performance of Santos Ltd and Woodside Petroleum. It begins with an introduction to both companies, highlighting their core activities and market positions. The analysis then delves into key financial aspects, including sales and production volume growth, income statement trends, and a detailed examination of key ratios such as the cash conversion cycle, profitability ratios (gross profit margin), liquidity ratios (current ratio), and financial leverage (long-term interest-bearing loan to equity, interest coverage ratio). The report utilizes horizontal (key trend) analysis and ratio analysis to evaluate the companies' financial health, efficiency, and risk profile over the period from 2016 to 2020, providing insights into their respective strengths and weaknesses and the impact of external factors like the COVID-19 pandemic. The report also includes a comparative assessment of dividend payout ratios and provides context for the financial data, discussing management strategies and external influences on performance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.