Accounting for Managers: Analyzing Nimbin's Financial Statements 2016

VerifiedAdded on 2020/07/23

|11

|2013

|30

Report

AI Summary

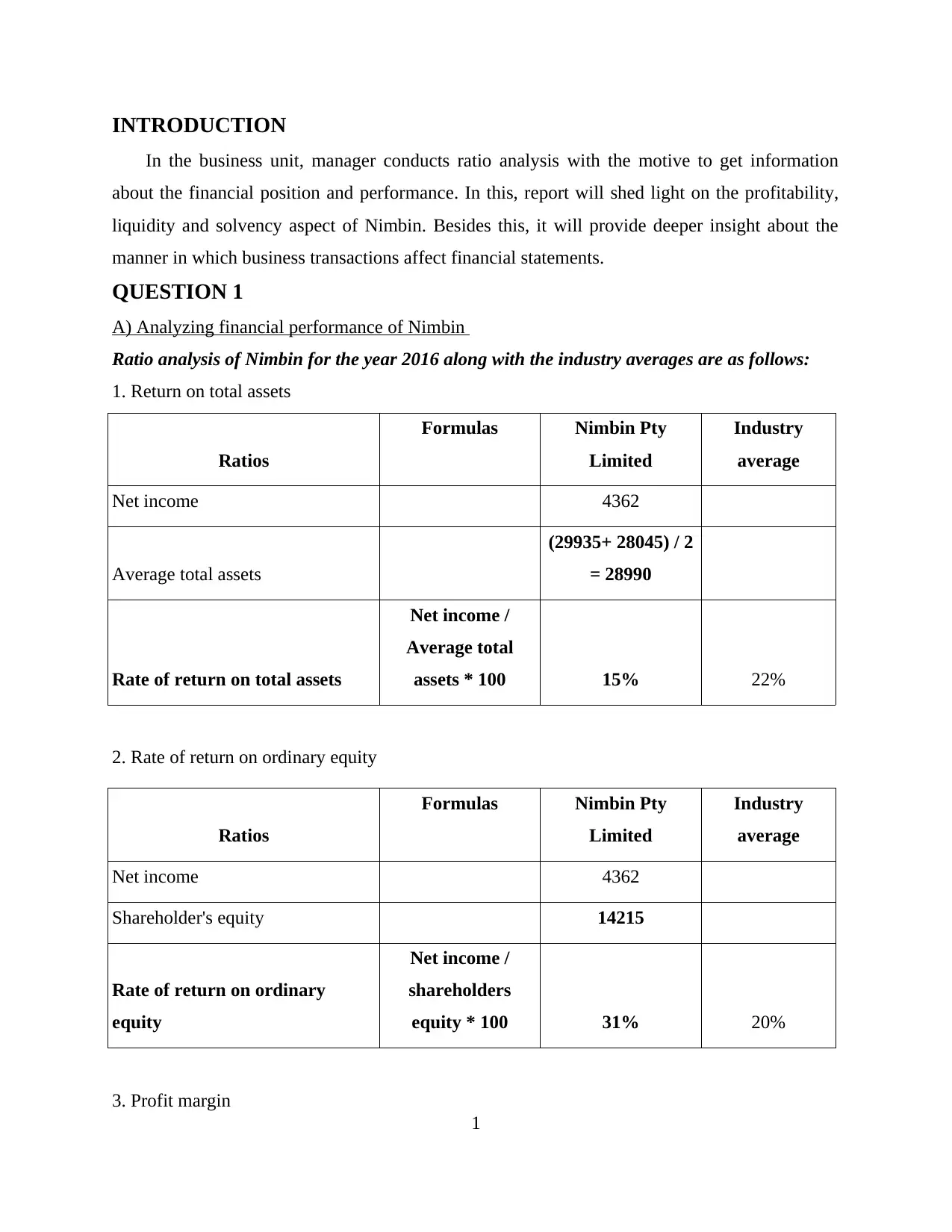

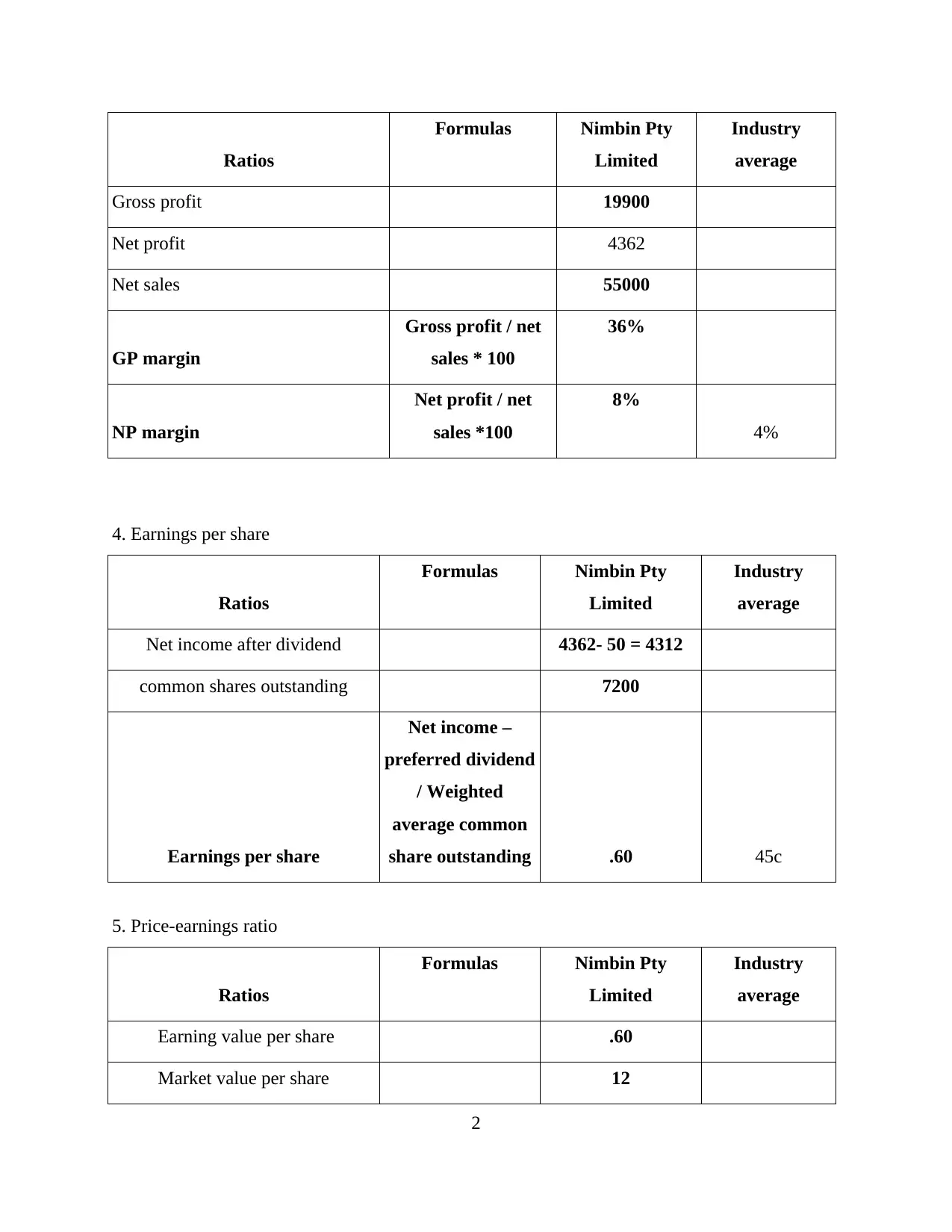

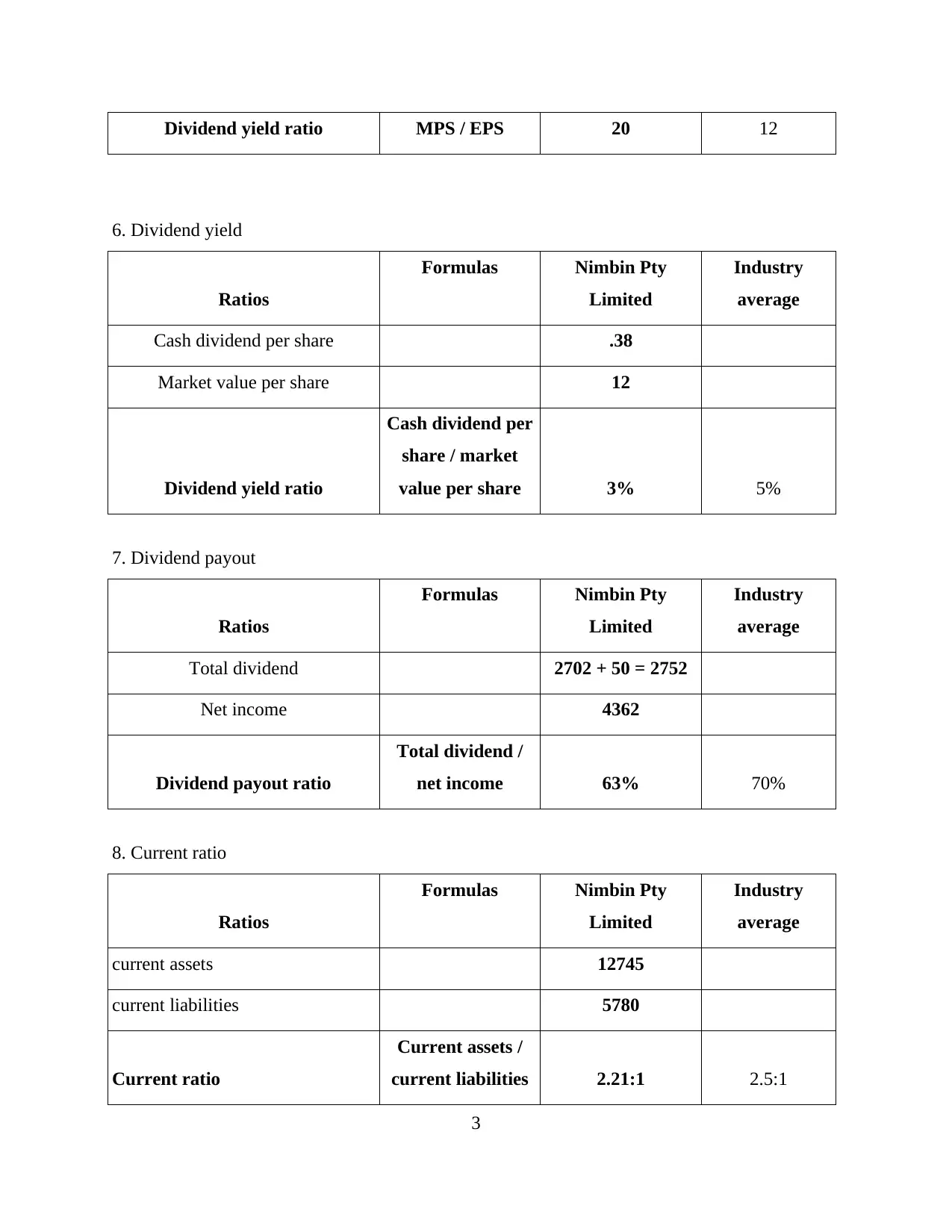

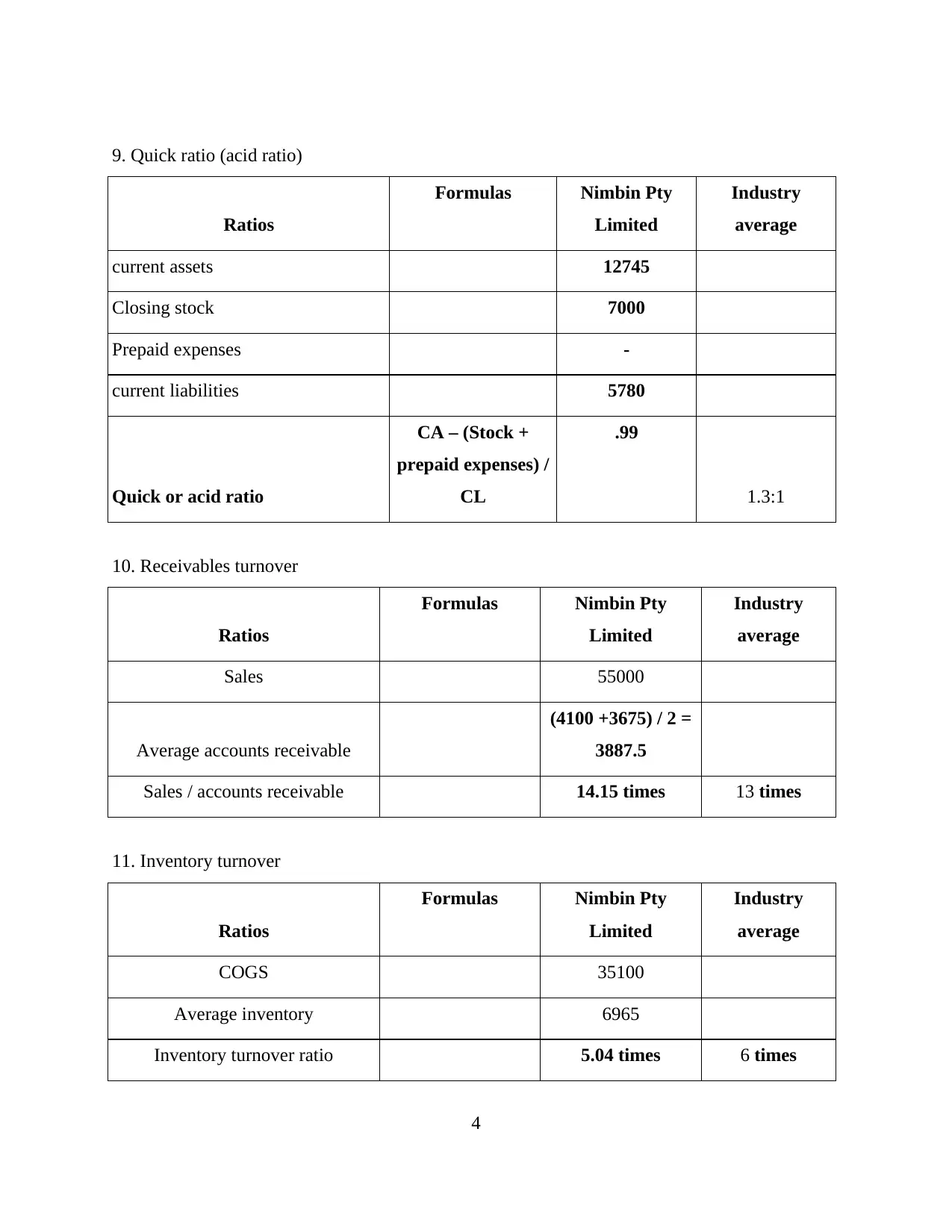

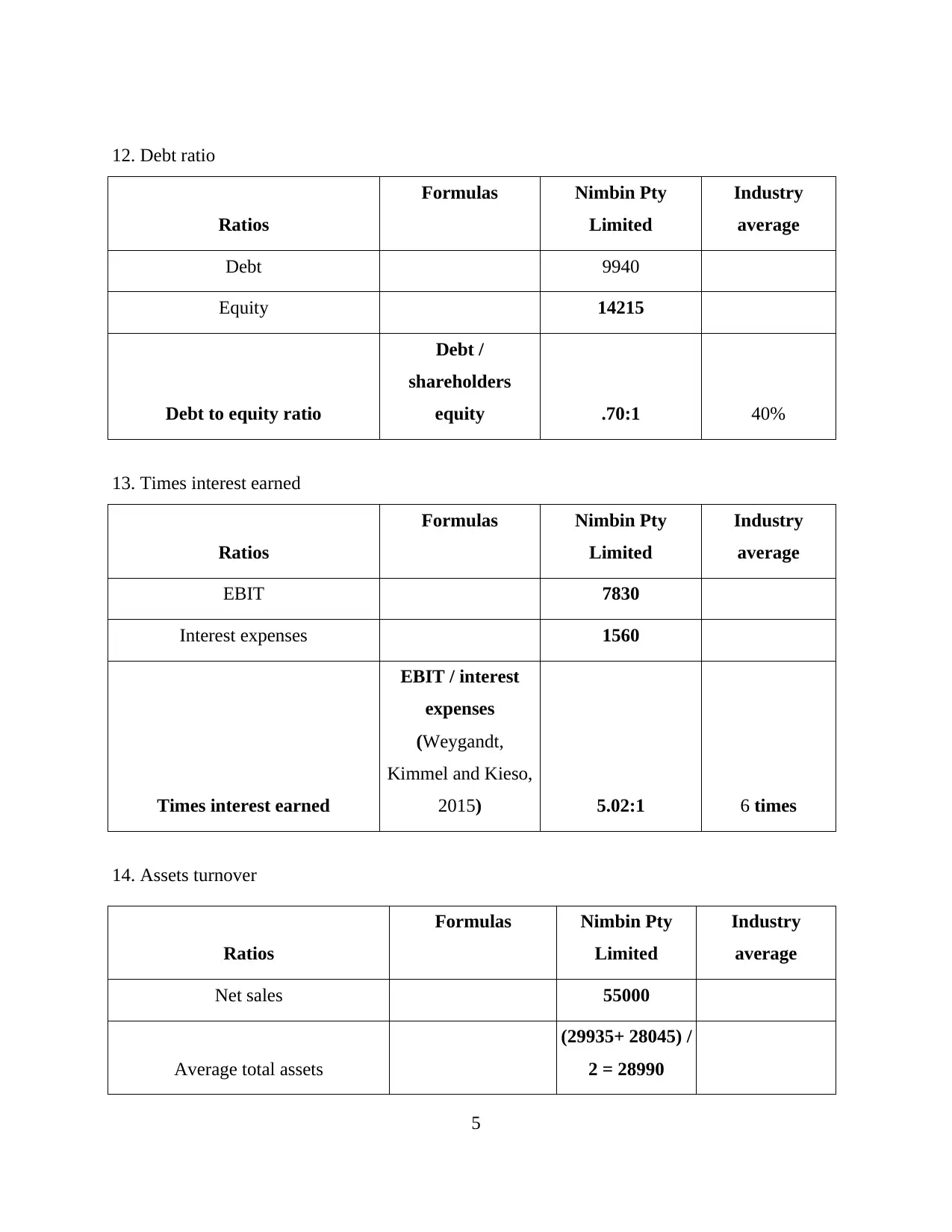

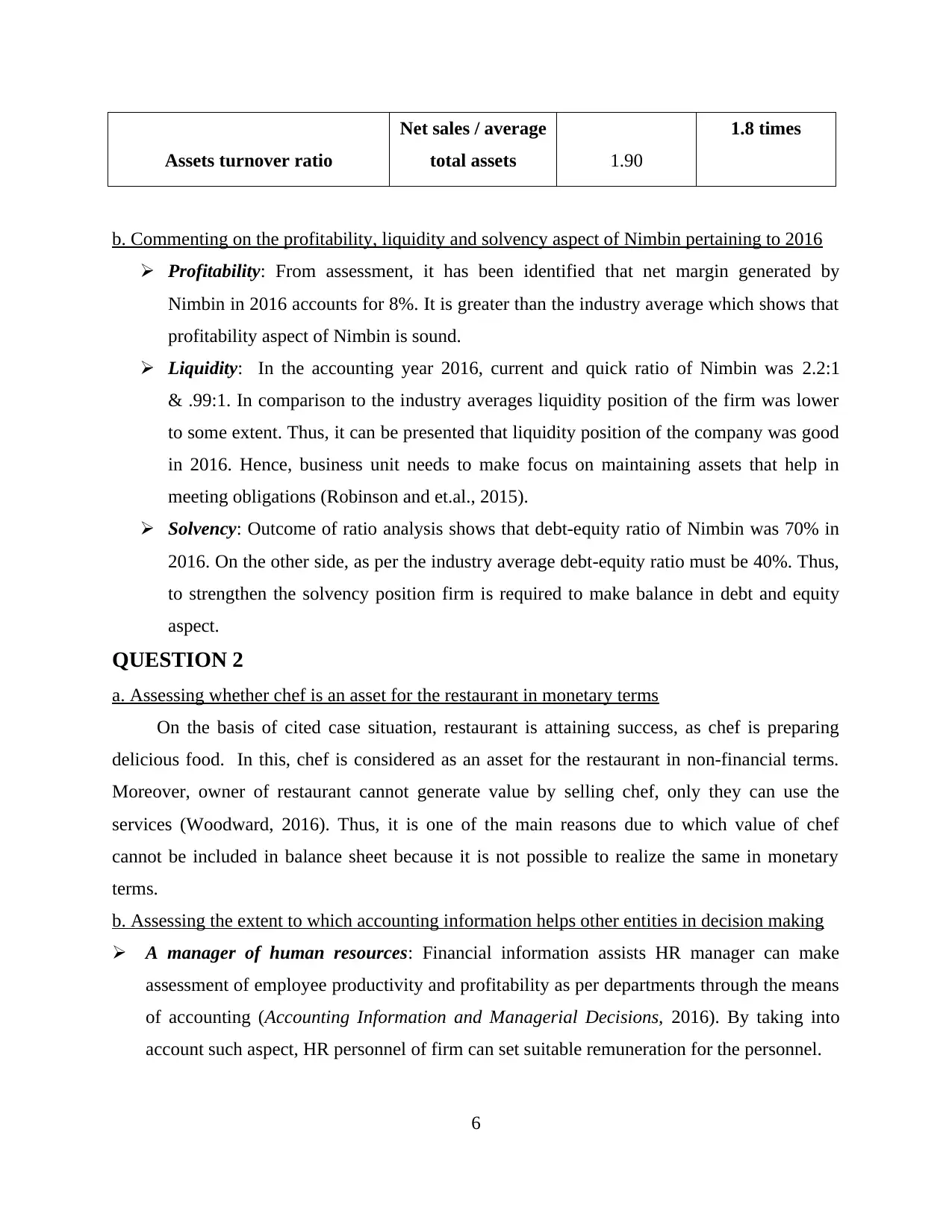

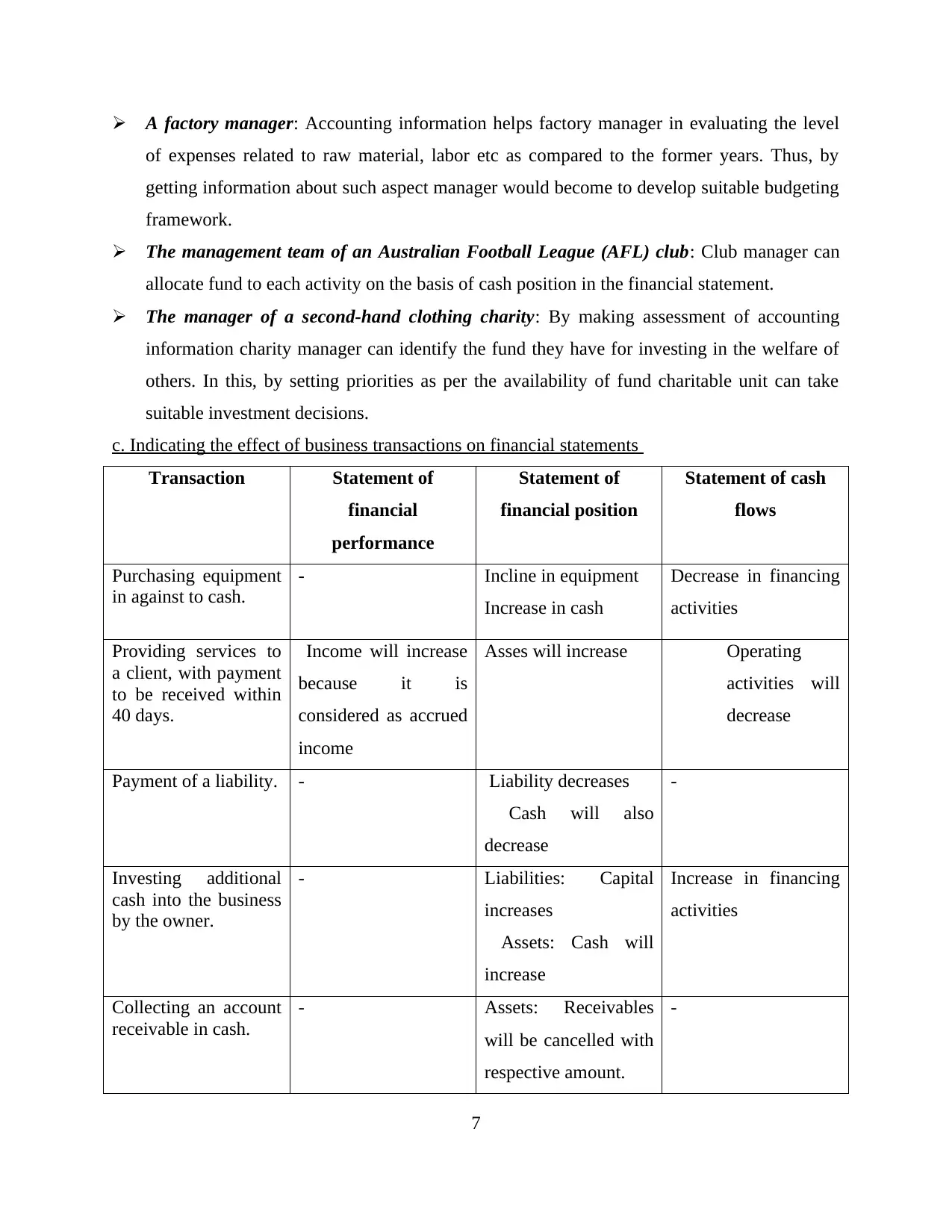

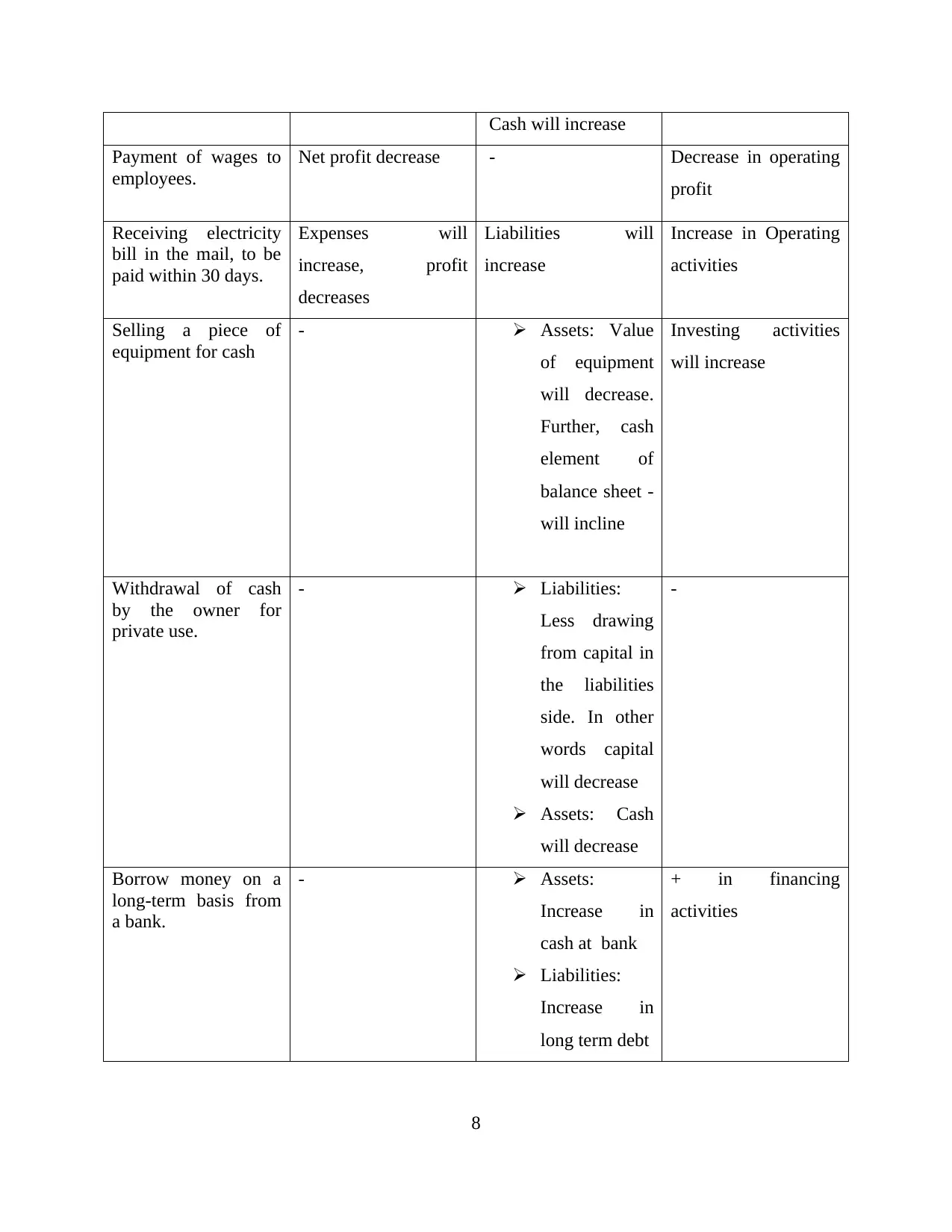

This report provides a comprehensive analysis of Nimbin Pty Ltd's financial performance in 2016, focusing on profitability, liquidity, and solvency. It employs ratio analysis to evaluate the company's financial health, comparing its performance to industry averages. The report examines key financial metrics, including return on assets, return on equity, profit margins, earnings per share, and various turnover ratios. Furthermore, it assesses the role of a chef as an asset and explores how accounting information supports decision-making for various entities, such as HR managers, factory managers, and AFL clubs. The report also details the impact of business transactions on financial statements, including the effects of purchasing equipment, providing services, paying liabilities, and collecting receivables. The conclusion highlights the importance of accounting in providing insights for sound economic decisions.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.