Accounting Fundamentals 1

VerifiedAdded on 2023/01/09

|17

|4213

|27

AI Summary

This document provides study material and solved assignments for Accounting Fundamentals 1. It covers topics such as cost accounting, management accounting, and financial accounting. It explains the nature, purpose, characteristics, similarities, and differences between management and cost accounting. It also discusses the use of cost and management accounting in developing long and short strategies for organizations. Additionally, it outlines the responsibilities of management accountants.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING FUNDAMENTALS 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Task 2...............................................................................................................................................5

a) What is the nature and purpose of cost and management accounting and what are the

specific characteristics, similarities and differences between management and cost accounting

.....................................................................................................................................................5

b) Use of cost and management accounting in develop long and short strategies of

organizations..........................................................................................................................10

Task 3.............................................................................................................................................11

Task 4.............................................................................................................................................12

References......................................................................................................................................16

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Task 2...............................................................................................................................................5

a) What is the nature and purpose of cost and management accounting and what are the

specific characteristics, similarities and differences between management and cost accounting

.....................................................................................................................................................5

b) Use of cost and management accounting in develop long and short strategies of

organizations..........................................................................................................................10

Task 3.............................................................................................................................................11

Task 4.............................................................................................................................................12

References......................................................................................................................................16

Introduction

This project report consists of the concept of management accounting, cost accounting and

financial accounting. To know their uses and application; comparison have been done between

them in the form of similarities, differences and characteristics. Additional to this the role of

management accountant in achieving business goals have also been discussed.

This project report consists of the concept of management accounting, cost accounting and

financial accounting. To know their uses and application; comparison have been done between

them in the form of similarities, differences and characteristics. Additional to this the role of

management accountant in achieving business goals have also been discussed.

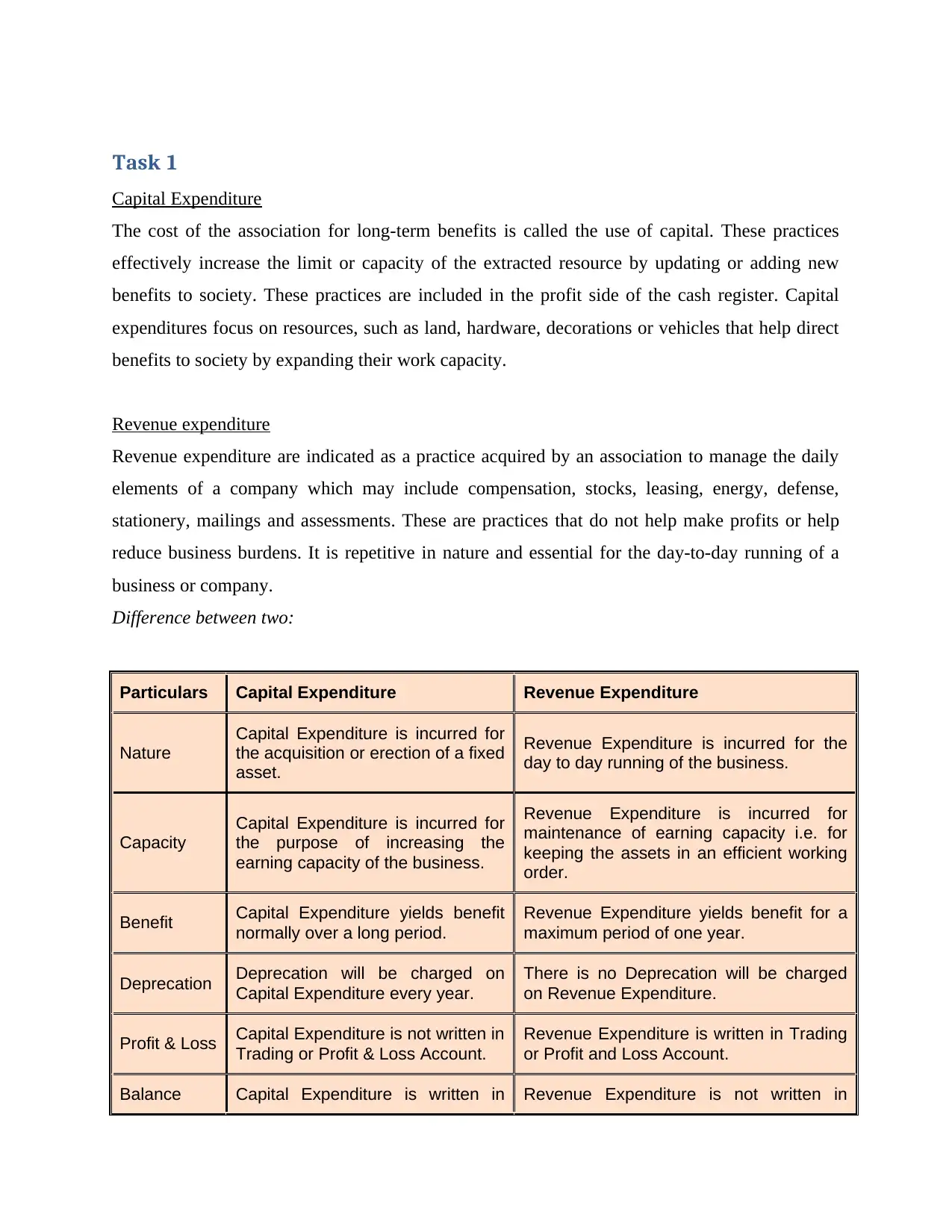

Task 1

Capital Expenditure

The cost of the association for long-term benefits is called the use of capital. These practices

effectively increase the limit or capacity of the extracted resource by updating or adding new

benefits to society. These practices are included in the profit side of the cash register. Capital

expenditures focus on resources, such as land, hardware, decorations or vehicles that help direct

benefits to society by expanding their work capacity.

Revenue expenditure

Revenue expenditure are indicated as a practice acquired by an association to manage the daily

elements of a company which may include compensation, stocks, leasing, energy, defense,

stationery, mailings and assessments. These are practices that do not help make profits or help

reduce business burdens. It is repetitive in nature and essential for the day-to-day running of a

business or company.

Difference between two:

Particulars Capital Expenditure Revenue Expenditure

Nature

Capital Expenditure is incurred for

the acquisition or erection of a fixed

asset.

Revenue Expenditure is incurred for the

day to day running of the business.

Capacity

Capital Expenditure is incurred for

the purpose of increasing the

earning capacity of the business.

Revenue Expenditure is incurred for

maintenance of earning capacity i.e. for

keeping the assets in an efficient working

order.

Benefit Capital Expenditure yields benefit

normally over a long period.

Revenue Expenditure yields benefit for a

maximum period of one year.

Deprecation Deprecation will be charged on

Capital Expenditure every year.

There is no Deprecation will be charged

on Revenue Expenditure.

Profit & Loss Capital Expenditure is not written in

Trading or Profit & Loss Account.

Revenue Expenditure is written in Trading

or Profit and Loss Account.

Balance Capital Expenditure is written in Revenue Expenditure is not written in

Capital Expenditure

The cost of the association for long-term benefits is called the use of capital. These practices

effectively increase the limit or capacity of the extracted resource by updating or adding new

benefits to society. These practices are included in the profit side of the cash register. Capital

expenditures focus on resources, such as land, hardware, decorations or vehicles that help direct

benefits to society by expanding their work capacity.

Revenue expenditure

Revenue expenditure are indicated as a practice acquired by an association to manage the daily

elements of a company which may include compensation, stocks, leasing, energy, defense,

stationery, mailings and assessments. These are practices that do not help make profits or help

reduce business burdens. It is repetitive in nature and essential for the day-to-day running of a

business or company.

Difference between two:

Particulars Capital Expenditure Revenue Expenditure

Nature

Capital Expenditure is incurred for

the acquisition or erection of a fixed

asset.

Revenue Expenditure is incurred for the

day to day running of the business.

Capacity

Capital Expenditure is incurred for

the purpose of increasing the

earning capacity of the business.

Revenue Expenditure is incurred for

maintenance of earning capacity i.e. for

keeping the assets in an efficient working

order.

Benefit Capital Expenditure yields benefit

normally over a long period.

Revenue Expenditure yields benefit for a

maximum period of one year.

Deprecation Deprecation will be charged on

Capital Expenditure every year.

There is no Deprecation will be charged

on Revenue Expenditure.

Profit & Loss Capital Expenditure is not written in

Trading or Profit & Loss Account.

Revenue Expenditure is written in Trading

or Profit and Loss Account.

Balance Capital Expenditure is written in Revenue Expenditure is not written in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sheet Balance Sheet under Fixed Assets. Balance Sheet, these effected profit & loss

account.

Task 2

a) What is the nature and purpose of cost and management accounting and

what are the specific characteristics, similarities and differences between

management and cost accounting

Cost accounting examines the cost structure of a company. It does this by collecting data on the

costs incurred by a group's businesses, assigning the selected costs to other items and

administrations and cost complaints and evaluating the feasibility of the costs.

Nature

Cost accounts concerned about cost assessment and control. The data that cost accounting

provides to management is useful for cost control and cost reduction through elements of

organization, dynamics and control. Initially, they limited themselves to determining the cost and

basically introduced the same to determine the cost of the item.

The guide to finding out creation costs. It is proven to be useful and not beneficial exercises.

They help the council to ignore unsuccessful exercises. Provides data for evaluations and

tenders. They reflect the misfortunes that occur such as idle time falling or rubbish and so on. It

also provides an infinite equality framework.

Purpose

It is part of the accounting through which the costs of products or administrations are learned and

controlled for a variety of purposes. It helps to find out the true cost of each action, through a

nearby clock, for example, a cost analysis and a bonus.

The main purpose for keeping cost books is:

Cost declaration:

account.

Task 2

a) What is the nature and purpose of cost and management accounting and

what are the specific characteristics, similarities and differences between

management and cost accounting

Cost accounting examines the cost structure of a company. It does this by collecting data on the

costs incurred by a group's businesses, assigning the selected costs to other items and

administrations and cost complaints and evaluating the feasibility of the costs.

Nature

Cost accounts concerned about cost assessment and control. The data that cost accounting

provides to management is useful for cost control and cost reduction through elements of

organization, dynamics and control. Initially, they limited themselves to determining the cost and

basically introduced the same to determine the cost of the item.

The guide to finding out creation costs. It is proven to be useful and not beneficial exercises.

They help the council to ignore unsuccessful exercises. Provides data for evaluations and

tenders. They reflect the misfortunes that occur such as idle time falling or rubbish and so on. It

also provides an infinite equality framework.

Purpose

It is part of the accounting through which the costs of products or administrations are learned and

controlled for a variety of purposes. It helps to find out the true cost of each action, through a

nearby clock, for example, a cost analysis and a bonus.

The main purpose for keeping cost books is:

Cost declaration:

The basic goal of cost records to determine the cost of any item, process, job, approval, and

administration or creation unit. It is done through a variety of strategies and techniques.

Cost control:

The essential ability for expense records to control costs. A study of actual costs with

instructions reveals inconsistencies (variances). The differences determine whether the cost is

under control or not. The corrective action is to control out-of-pocket expenses.

Cost reduction:

The reduction in costs refers to the effective permanent reduction in the unit cost of the

manufactured goods or the benefits provided without affecting the proposed use. It can be quite

complete with the help of strategies called budget control, routine costs, materials control, work

control and cost control.

Characteristics

Correctness

The cost accounting body should provide the correct data for both cost assessment and

introduction. Another thing, it misleads clients.

Ease

The cost accounting framework includes a point-by-point analysis of costs. In order to keep a

strategic distance from the difficulties in a cost assessment strategy, complex cost arrangements

need to be circumvented and care must be taken to keep it as simple as possible.

Elasticity

The cost accounting framework should be equipped to adapt to changes in business conditions.

Must be capable for expansion or modification based on company requirements.

Cost-effectiveness

The operating costs of the cost framework need to be practical and monetary. The benefits

should outweigh the costs.

administration or creation unit. It is done through a variety of strategies and techniques.

Cost control:

The essential ability for expense records to control costs. A study of actual costs with

instructions reveals inconsistencies (variances). The differences determine whether the cost is

under control or not. The corrective action is to control out-of-pocket expenses.

Cost reduction:

The reduction in costs refers to the effective permanent reduction in the unit cost of the

manufactured goods or the benefits provided without affecting the proposed use. It can be quite

complete with the help of strategies called budget control, routine costs, materials control, work

control and cost control.

Characteristics

Correctness

The cost accounting body should provide the correct data for both cost assessment and

introduction. Another thing, it misleads clients.

Ease

The cost accounting framework includes a point-by-point analysis of costs. In order to keep a

strategic distance from the difficulties in a cost assessment strategy, complex cost arrangements

need to be circumvented and care must be taken to keep it as simple as possible.

Elasticity

The cost accounting framework should be equipped to adapt to changes in business conditions.

Must be capable for expansion or modification based on company requirements.

Cost-effectiveness

The operating costs of the cost framework need to be practical and monetary. The benefits

should outweigh the costs.

Comparability

The records to be kept should be encouraged over time. The records need to be filled in as a basis

to make sure what comes next.

The term Management Accounting is made up of two words "Management” and “Accounting”.

It is a study of the administrative aspects of accounting. The tab property is a tool for dynamic

use. The emphasis of the board's accounting is to update the accounting in a useful way for the

administration in terms of circulation and performance control.

Nature

Despite the fact that Management Accounting is the most recent branch in the field of

accounting, it could be viewed as a science and incomplete as an art. It is a study of "Evaluation

and synthesis" and information on the conservation of "Deciphering" art books.

Management Accounts derives its findings through the mixing, preparation and targeted analysis

of information on the increased figure. It is therefore based on "Themes and increasing progress

and issues". From this point of view, the conservation of management books can be seen as a

science.

Purpose

The main purpose of administrative accounting is to help the administration to perform its skills

effectively. Important elements of managers are organization, selection, coordination and

control. Board of Directors accounting will help the administration to achieve these skills

effectively:

Effective Control:

Routine costs and budgetary control are essential elements of a board's accountability. These

procedures set goals, different directions and financial plans with exposure assessment and

movement control.

Coordination:

The records to be kept should be encouraged over time. The records need to be filled in as a basis

to make sure what comes next.

The term Management Accounting is made up of two words "Management” and “Accounting”.

It is a study of the administrative aspects of accounting. The tab property is a tool for dynamic

use. The emphasis of the board's accounting is to update the accounting in a useful way for the

administration in terms of circulation and performance control.

Nature

Despite the fact that Management Accounting is the most recent branch in the field of

accounting, it could be viewed as a science and incomplete as an art. It is a study of "Evaluation

and synthesis" and information on the conservation of "Deciphering" art books.

Management Accounts derives its findings through the mixing, preparation and targeted analysis

of information on the increased figure. It is therefore based on "Themes and increasing progress

and issues". From this point of view, the conservation of management books can be seen as a

science.

Purpose

The main purpose of administrative accounting is to help the administration to perform its skills

effectively. Important elements of managers are organization, selection, coordination and

control. Board of Directors accounting will help the administration to achieve these skills

effectively:

Effective Control:

Routine costs and budgetary control are essential elements of a board's accountability. These

procedures set goals, different directions and financial plans with exposure assessment and

movement control.

Coordination:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

They are given the objectives of various departments and their administration pays attention to

their presentation from time to time. This relentless news helps the administration to implement a

number of exercises to improve overall performance.

Decision Making:

Regulatory accounting provides close-knit information and analysis to explain possible strategy

and dynamics.

Characteristics

Provide financial information:

The main emphasis on accounts managers is to bring data related to money to the board. Data are

reasonably provided to different levels of managers to study approaches and dynamics.

Cause and Effect Analysis:

Financial accounting is limited to the inclusion of an income statement and balance sheet. Board

accounting examines the logical location and results of subsequent raw numbers. The possibility

is being explored that there are no unfortunate reasons for misfortunes. In the event that there are

no advantages, the variable that influences the gain is analyzed in the same way. The

measurement of the benefit is compared with the expenditure, contracts, capital employed and so

on, to arrive at correct decisions characterized by the impact of these factors on profit.

Forecasting:

Accountants are concerned about making choices about their future use. This includes

expectations and expectations for the future. It is useful for organizing and setting destinations.

Similarities between cost and management accounting:

(I) Both cost and management accounting are maintained in accordance with the dual accounting

system.

their presentation from time to time. This relentless news helps the administration to implement a

number of exercises to improve overall performance.

Decision Making:

Regulatory accounting provides close-knit information and analysis to explain possible strategy

and dynamics.

Characteristics

Provide financial information:

The main emphasis on accounts managers is to bring data related to money to the board. Data are

reasonably provided to different levels of managers to study approaches and dynamics.

Cause and Effect Analysis:

Financial accounting is limited to the inclusion of an income statement and balance sheet. Board

accounting examines the logical location and results of subsequent raw numbers. The possibility

is being explored that there are no unfortunate reasons for misfortunes. In the event that there are

no advantages, the variable that influences the gain is analyzed in the same way. The

measurement of the benefit is compared with the expenditure, contracts, capital employed and so

on, to arrive at correct decisions characterized by the impact of these factors on profit.

Forecasting:

Accountants are concerned about making choices about their future use. This includes

expectations and expectations for the future. It is useful for organizing and setting destinations.

Similarities between cost and management accounting:

(I) Both cost and management accounting are maintained in accordance with the dual accounting

system.

(ii) Entry of transaction, both in terms of cost and management accounting, is done on the basis

of good foundations, applications and archives.

(iii) Both cost accounting and management accounting reflect the gain or loss of the asset.

(iv) Both expense accounting and management accounting cover how you coordinate the related

expenses and income of the movement for this period.

(v) Both accounting frameworks contain a table of direct and capped costs.

(vi) Both accounting frameworks allow companies to be concerned about the disclosure and

acceptance of exchange results.

(vii) Both accounting frameworks assist the administration in defining future business strategy

and making various management choices.

Differences:

(I) Financial records are deep in the nature and distribution of all business exchanges while

expense accounts disclose only those exchanges identified by the collection and offering of items

and administrations.

(ii) Financial records govern all aspects of expenses, misfortunes, salaries and benefits but

expense accounts govern only those items of expenses which go into creation costs.

(iii) Financial records do not include an analysis of usage as determined by components,

capabilities, behavior, categories or items. Expenditure accounts record expenses by components,

capabilities, instability, divisions and so on, for regular analysis.

of good foundations, applications and archives.

(iii) Both cost accounting and management accounting reflect the gain or loss of the asset.

(iv) Both expense accounting and management accounting cover how you coordinate the related

expenses and income of the movement for this period.

(v) Both accounting frameworks contain a table of direct and capped costs.

(vi) Both accounting frameworks allow companies to be concerned about the disclosure and

acceptance of exchange results.

(vii) Both accounting frameworks assist the administration in defining future business strategy

and making various management choices.

Differences:

(I) Financial records are deep in the nature and distribution of all business exchanges while

expense accounts disclose only those exchanges identified by the collection and offering of items

and administrations.

(ii) Financial records govern all aspects of expenses, misfortunes, salaries and benefits but

expense accounts govern only those items of expenses which go into creation costs.

(iii) Financial records do not include an analysis of usage as determined by components,

capabilities, behavior, categories or items. Expenditure accounts record expenses by components,

capabilities, instability, divisions and so on, for regular analysis.

(iv) Financial records will not present the bookkeeping data in a prescribed structure and broken

down to disclose the cost per unit at all levels. Cost accounts show everything in terms of cost

adjustment and analysis so that all unit costs appear at each stage of creation.

(v) Financial records determine the overall benefit of the business while expense accounts

manage item savings, visual work, office relocation and process-wise gain.

(vi) Financial records are governed by actual facts and figures only. Expense accounts govern

items simply as valuations because expense account results do not normally count with cash-

related record results.

(vii) Financial records do not show data identifying consumption of goods and loss of working

hours and machine hours. In cost accounts, again, full data indicates a wide range of waste

generated during creation.

b) Use of cost and management accounting in develop long and short strategies of

organizations

The decisions that have to be made in order to ensure effective resources allocation requires a

variety of information that only management accounting can make available to managers. The

role of management accounting has changed over time, depending on the financial situation.

Clearly, in an invisible, violent and uncertain state, administrators' data needs are expanding and

evolving and the conservation of textbooks - as a specific data source for the administrative

framework - can meet these pre-requisites, which he changed his boss search tools and practices

forever. A cost picture is used, from a single perspective, for the liquidity response needs (to

evaluate the objects of the resource reports) and, once again, for the internal data needs

concerning the methodological development, to determine the key options motivate and also act.

At the moment, the company's position has proven to be more "relevant" to the elements, which

have forced them to strive for a much stronger cost, quality and administrative structure. The

data that administrators need sees problems, such as quality, delivery times, and feasibility of the

ongoing exercises just like the articles / administrations and customer profit.

down to disclose the cost per unit at all levels. Cost accounts show everything in terms of cost

adjustment and analysis so that all unit costs appear at each stage of creation.

(v) Financial records determine the overall benefit of the business while expense accounts

manage item savings, visual work, office relocation and process-wise gain.

(vi) Financial records are governed by actual facts and figures only. Expense accounts govern

items simply as valuations because expense account results do not normally count with cash-

related record results.

(vii) Financial records do not show data identifying consumption of goods and loss of working

hours and machine hours. In cost accounts, again, full data indicates a wide range of waste

generated during creation.

b) Use of cost and management accounting in develop long and short strategies of

organizations

The decisions that have to be made in order to ensure effective resources allocation requires a

variety of information that only management accounting can make available to managers. The

role of management accounting has changed over time, depending on the financial situation.

Clearly, in an invisible, violent and uncertain state, administrators' data needs are expanding and

evolving and the conservation of textbooks - as a specific data source for the administrative

framework - can meet these pre-requisites, which he changed his boss search tools and practices

forever. A cost picture is used, from a single perspective, for the liquidity response needs (to

evaluate the objects of the resource reports) and, once again, for the internal data needs

concerning the methodological development, to determine the key options motivate and also act.

At the moment, the company's position has proven to be more "relevant" to the elements, which

have forced them to strive for a much stronger cost, quality and administrative structure. The

data that administrators need sees problems, such as quality, delivery times, and feasibility of the

ongoing exercises just like the articles / administrations and customer profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The critical cost of managers is due to ongoing changes that require constant change in the tools

and methods to improve the core position of associations. In order for the data provided by the

board’s accounts to be useful to the directors, in order to achieve the association’s essential

objectives, the management’s accounts should be organized and used to follow the association' s

essential technical practices, examine relationship with financial conditions, costs associated

with customers, competitors and so on.

Task 3

Responsibilities of management accountants

Management accountants work for open agencies, private organizations and government offices.

They are also called accountants, administrative accountants, modern accountants, private

accountants or corporate accountants, but all have comparable secondary capabilities. within a

group. Getting information ready for use within an organization is one of the best known events

for an administrative accountant of different types of accounting roles, such as open accounting.

A management accountant differentiates the models and opens the doors to development, breaks

and monitors the risks, supports the subsidies and the financing of the activities and maintains

the screen and the maintenance. They can also create and maintain a financial framework for the

organization and manage their accountants and information managers. Board custodians may

also have a specific problem, such as liability or design.

Some of the important roles of management accountant have been discussed below:

Control:

The accounting reports and investigation plans of the administration's accountants, such as

standard costs, financial plans, examination and understanding of the change, investigation of the

flow of money and shops, the managers of liquidity, the evaluation of the execution and the

accounting of the homework and so on for checking.

Dynamic:

and methods to improve the core position of associations. In order for the data provided by the

board’s accounts to be useful to the directors, in order to achieve the association’s essential

objectives, the management’s accounts should be organized and used to follow the association' s

essential technical practices, examine relationship with financial conditions, costs associated

with customers, competitors and so on.

Task 3

Responsibilities of management accountants

Management accountants work for open agencies, private organizations and government offices.

They are also called accountants, administrative accountants, modern accountants, private

accountants or corporate accountants, but all have comparable secondary capabilities. within a

group. Getting information ready for use within an organization is one of the best known events

for an administrative accountant of different types of accounting roles, such as open accounting.

A management accountant differentiates the models and opens the doors to development, breaks

and monitors the risks, supports the subsidies and the financing of the activities and maintains

the screen and the maintenance. They can also create and maintain a financial framework for the

organization and manage their accountants and information managers. Board custodians may

also have a specific problem, such as liability or design.

Some of the important roles of management accountant have been discussed below:

Control:

The accounting reports and investigation plans of the administration's accountants, such as

standard costs, financial plans, examination and understanding of the change, investigation of the

flow of money and shops, the managers of liquidity, the evaluation of the execution and the

accounting of the homework and so on for checking.

Dynamic:

The accounting officer of the managers provides vital data to the board of directors in the

transitory choice, e.g. Ideal combination of articles, creation or purchase, rent or purchase,

evaluation of an article, end of an article and so on and long-range choices, e.g. Capital planning,

risk assessment, venture capital financing and so on.

Maintaining the best asset structure:

An accountant has a lot of work to do in fundraising and defense. He must choose to maintain a

legitimate mix of responsibility and value. Raising funds through liability is cheaper because of

tax cuts.

However that may be, it is risky because a liability commitment must be paid regardless of

whether the company receives satisfactory benefits or not. In this way, the custodian of the board

of directors must maintain a separate capital structure and duly take into account the different

costs of the capital assumptions, the impact and the probability of exchange of value.

Participate in the regulatory process:

An administrative accountant occupies a vital position in society. He interprets the staff and also

has line authority over the accountant and various representatives in his office. Provides

assistance to administrators on audit data requirements and methods used. It moves the relevant

data from the insignificant and brings it back in a single structure to the administration and at

some point to interesting external collections.

Long and short term resistance design:

The executive accountant has an important role in estimating future financial and commercial

times for making future arrangements, such as long-haul plans, key retention Management

books, corporate figure system, and advertising analysis and so on.

Task 4

Discuss the differences between management and financial accounting

Accounting, which describes the method of recording, ordering and summarizing finances,

business exchanges and opportunities and the verification of results. It is used by elements to

transitory choice, e.g. Ideal combination of articles, creation or purchase, rent or purchase,

evaluation of an article, end of an article and so on and long-range choices, e.g. Capital planning,

risk assessment, venture capital financing and so on.

Maintaining the best asset structure:

An accountant has a lot of work to do in fundraising and defense. He must choose to maintain a

legitimate mix of responsibility and value. Raising funds through liability is cheaper because of

tax cuts.

However that may be, it is risky because a liability commitment must be paid regardless of

whether the company receives satisfactory benefits or not. In this way, the custodian of the board

of directors must maintain a separate capital structure and duly take into account the different

costs of the capital assumptions, the impact and the probability of exchange of value.

Participate in the regulatory process:

An administrative accountant occupies a vital position in society. He interprets the staff and also

has line authority over the accountant and various representatives in his office. Provides

assistance to administrators on audit data requirements and methods used. It moves the relevant

data from the insignificant and brings it back in a single structure to the administration and at

some point to interesting external collections.

Long and short term resistance design:

The executive accountant has an important role in estimating future financial and commercial

times for making future arrangements, such as long-haul plans, key retention Management

books, corporate figure system, and advertising analysis and so on.

Task 4

Discuss the differences between management and financial accounting

Accounting, which describes the method of recording, ordering and summarizing finances,

business exchanges and opportunities and the verification of results. It is used by elements to

track their currency exchanges. Budget accounting and accounting management are the two parts

of accounting. Cash-strapped accounting emphasizes the ability to give a true and fair view of

the financial position of the organization at its various meetings.

The difference between financial and managerial accounting is that cash accounting is the range

of accounting information for making tax summaries, and administrative accounting is the

internal control used to represent commercial exchanges.

Financial accounting is an accounting framework that is concerned with the readiness of the tax

summary for external meetings such as loan managers, investors, speculators, suppliers, banks,

customers and so on. This is the most impeccable type of accounting in which relevant records

and details of information are made, to provide important and meaningful data to the customers.

Financial accounting is based on various suspects, standards and information such as concern,

relevance, coordination, recognition, conservatism, consistency, collection, registration costs and

so on. The financial statements report consists of a balance sheet, an income statement and an

explanation of the cash flows established in accordance with the standards issued by the relevant

standard.

Indeed, the objectives of management accounting provide management with both thematic and

quantitative data, to help them dynamically and therefore increase profitability.

Management accounting, also known as managerial accounting, is the managers who help the

association's management to define agreements and to anticipate, regulate and control the

association's daily business activities. Both quantitative and personal data will be acquired and

analyzed by administrative accounting.

The utilitarian region of the management accounting isn't restricted to giving a money related or

cost data as it were. Rather, it extricates the applicable and material data from budgetary and cost

bookkeeping to help the administration in planning, defining objectives, dynamic, and so forth.

The bookkeeping should be possible according to the prerequisite of the administration, for

of accounting. Cash-strapped accounting emphasizes the ability to give a true and fair view of

the financial position of the organization at its various meetings.

The difference between financial and managerial accounting is that cash accounting is the range

of accounting information for making tax summaries, and administrative accounting is the

internal control used to represent commercial exchanges.

Financial accounting is an accounting framework that is concerned with the readiness of the tax

summary for external meetings such as loan managers, investors, speculators, suppliers, banks,

customers and so on. This is the most impeccable type of accounting in which relevant records

and details of information are made, to provide important and meaningful data to the customers.

Financial accounting is based on various suspects, standards and information such as concern,

relevance, coordination, recognition, conservatism, consistency, collection, registration costs and

so on. The financial statements report consists of a balance sheet, an income statement and an

explanation of the cash flows established in accordance with the standards issued by the relevant

standard.

Indeed, the objectives of management accounting provide management with both thematic and

quantitative data, to help them dynamically and therefore increase profitability.

Management accounting, also known as managerial accounting, is the managers who help the

association's management to define agreements and to anticipate, regulate and control the

association's daily business activities. Both quantitative and personal data will be acquired and

analyzed by administrative accounting.

The utilitarian region of the management accounting isn't restricted to giving a money related or

cost data as it were. Rather, it extricates the applicable and material data from budgetary and cost

bookkeeping to help the administration in planning, defining objectives, dynamic, and so forth.

The bookkeeping should be possible according to the prerequisite of the administration, for

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

example week after week, month to month, quarterly, and so forth and there is no organization

set based on which it is to be accounted for.

Below are the differences between both accounting systems:

SYSTEMS

Cash accounting is only about creating profit and not about general how the organization

operates. Again, administrative accounting looks for bottlenecks and explores various

approaches to improve profits by killing bottlenecks.

REPORTING FOCUS

Cash accounting focuses on making budget summaries to share with internal and external

partners and the general public. Administrative accounting focuses on the shared operational

response within an organization.

AGGREGATION

Cash accounting takes care of all the activity, while point-and-click management accounting

continues to grow. Administrative accounting focuses on gritty relationships such as the benefits

of everything, product offerings, messages and geographic locations.

EFFICIENCY

Company productivity and capability are assessed through cash accounting. Administrative

accounting describes what causes a problem and how you can fix it.

TIMING

The financial statements are expected at the end of the accounting period, while the management

reports may be provided more and more frequently, to provide administrators with the relevant

data that they can follow in the immediately.

PROVEN INFORMATION

set based on which it is to be accounted for.

Below are the differences between both accounting systems:

SYSTEMS

Cash accounting is only about creating profit and not about general how the organization

operates. Again, administrative accounting looks for bottlenecks and explores various

approaches to improve profits by killing bottlenecks.

REPORTING FOCUS

Cash accounting focuses on making budget summaries to share with internal and external

partners and the general public. Administrative accounting focuses on the shared operational

response within an organization.

AGGREGATION

Cash accounting takes care of all the activity, while point-and-click management accounting

continues to grow. Administrative accounting focuses on gritty relationships such as the benefits

of everything, product offerings, messages and geographic locations.

EFFICIENCY

Company productivity and capability are assessed through cash accounting. Administrative

accounting describes what causes a problem and how you can fix it.

TIMING

The financial statements are expected at the end of the accounting period, while the management

reports may be provided more and more frequently, to provide administrators with the relevant

data that they can follow in the immediately.

PROVEN INFORMATION

Great accuracy is expected to show that cash records are correct. Cash accounting relies on this

very accurate information, while administrative accounting most of the time manages signals that

are limited to actual determinations.

STANDARDS

At the time of administrative accounting for internal use, it is not possible to establish guidelines

for the collection of such data. In addition, budget accounts need to maintain different accounting

principles.

TIME PERIOD

Cash accounting looks to the past to analyze the results associated with cash flows, so it is

generally committed. Administrative accounting looks to the future with estimation.

VALUATION

Cash accounting about knows the best possible estimate of an organization’s benefits and

obligations. Administrative accounting is only about the value of these things to an

organization’s efficiency.

SWOT Analysis of Management Accounting

The SWOT analysis for cost or SWOT-CM methods was introduced in the world to break down

the features and disadvantages of cost strategies and individually identify the capabilities and

risks arising from cost strategy from the the outdoor situation. To explain the ideas identified by

the SWOT test, we clarify below the terms used, as follows:

1. The virtues of unparalleled ambition or skills are the approach at a more important level

compared to different strategies applied specifically for a similar purpose, specific to the

effective management of the organization, which promises a special welfare position in relation

to them.

2. The obvious shortcomings are the lack of communication or ineffectiveness of the strategies

studied.

very accurate information, while administrative accounting most of the time manages signals that

are limited to actual determinations.

STANDARDS

At the time of administrative accounting for internal use, it is not possible to establish guidelines

for the collection of such data. In addition, budget accounts need to maintain different accounting

principles.

TIME PERIOD

Cash accounting looks to the past to analyze the results associated with cash flows, so it is

generally committed. Administrative accounting looks to the future with estimation.

VALUATION

Cash accounting about knows the best possible estimate of an organization’s benefits and

obligations. Administrative accounting is only about the value of these things to an

organization’s efficiency.

SWOT Analysis of Management Accounting

The SWOT analysis for cost or SWOT-CM methods was introduced in the world to break down

the features and disadvantages of cost strategies and individually identify the capabilities and

risks arising from cost strategy from the the outdoor situation. To explain the ideas identified by

the SWOT test, we clarify below the terms used, as follows:

1. The virtues of unparalleled ambition or skills are the approach at a more important level

compared to different strategies applied specifically for a similar purpose, specific to the

effective management of the organization, which promises a special welfare position in relation

to them.

2. The obvious shortcomings are the lack of communication or ineffectiveness of the strategies

studied.

3. Openings speak to external presentations obtained by taking advantage of various data

provided by that strategy, in order to profitably exploit emerging opportunities.

Doors are open for all innovations and this need to be identified in order to make the right

decision on the system for the product or they can be realized, especially on the basis of the

results that come from the various inter- translations given to the financial data.

4. The dangers of exhibits concern negative or negatively influenced parts, which can occur at

the time of a strategy, so to speak, situations or moments that can negatively affect the

individual's abilities management appropriately addresses the item in order to fully achieve its

goals, thereby reducing its achievement of cash and cash. Contrary to conditions, dangers of

different nature and causes can occur as indicated by specific body exercises and poor condition.

Practical risk concerns allow you to take appropriate measures to avoid or limit their impact.

SWOT is a progressive study, which allows the analysis of the past and future states of the

costing strategy, in this way extracting the progressive ideas that came out. A decision that is

based on a SWOT analysis can be seen as a soft-minded study of board accounting techniques,

individual costing strategies, to create or eliminate features, deficiencies, openings, risks and

causes. it can be implemented, make recommendations to eliminate or reduce negative comments

or respect positive ones.

provided by that strategy, in order to profitably exploit emerging opportunities.

Doors are open for all innovations and this need to be identified in order to make the right

decision on the system for the product or they can be realized, especially on the basis of the

results that come from the various inter- translations given to the financial data.

4. The dangers of exhibits concern negative or negatively influenced parts, which can occur at

the time of a strategy, so to speak, situations or moments that can negatively affect the

individual's abilities management appropriately addresses the item in order to fully achieve its

goals, thereby reducing its achievement of cash and cash. Contrary to conditions, dangers of

different nature and causes can occur as indicated by specific body exercises and poor condition.

Practical risk concerns allow you to take appropriate measures to avoid or limit their impact.

SWOT is a progressive study, which allows the analysis of the past and future states of the

costing strategy, in this way extracting the progressive ideas that came out. A decision that is

based on a SWOT analysis can be seen as a soft-minded study of board accounting techniques,

individual costing strategies, to create or eliminate features, deficiencies, openings, risks and

causes. it can be implemented, make recommendations to eliminate or reduce negative comments

or respect positive ones.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Drury, C.M., 2013. Management and cost accounting. Springer.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T., 2002. Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Goretzki, L. and Strauss, E. eds., 2017. The role of the management accountant: Local variations

and global influences. Routledge.

Lepistö, L., Dobroszek, J., Moilanen, S. and Zarzycka, E., 2018. Being a management

accountant in a shared services centre. Journal of Accounting & Organizational Change.

Mitter, C. and Hiebl, M.R., 2017. The role of management accounting in international

entrepreneurship. Journal of Accounting & Organizational Change.

Gibbs, B.T., 2017. An insider research into the changing role of the management accountant

during organisational change (Doctoral dissertation, Liverpool John Moores University).

Hlaciuc, E., Vultur, P., Cretu, F. and Ailoaiei, R., 2017. The interface between financial and

management accounting. The USV Annals of Economics and Public Administration, 17(2

(26)), pp.103-110.

Tenhunen, M.L., 2018. THE IMPORTANT NEED OF GENERAL ACCOUNTING AND

MANAGEMENT ACCOUNTING. Euromentor Journal-Studies about education, 9(04),

pp.37-43.

Ramachandran, N. and Kakani, R.K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Cuzdriorean, D.D., 2017. The use of management accounting practices by Romanian small and

medium-sized enterprises: A field study. Journal of Accounting and Management

Information Systems, 16(2), pp.291-312.

Drury, C.M., 2013. Management and cost accounting. Springer.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T., 2002. Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Goretzki, L. and Strauss, E. eds., 2017. The role of the management accountant: Local variations

and global influences. Routledge.

Lepistö, L., Dobroszek, J., Moilanen, S. and Zarzycka, E., 2018. Being a management

accountant in a shared services centre. Journal of Accounting & Organizational Change.

Mitter, C. and Hiebl, M.R., 2017. The role of management accounting in international

entrepreneurship. Journal of Accounting & Organizational Change.

Gibbs, B.T., 2017. An insider research into the changing role of the management accountant

during organisational change (Doctoral dissertation, Liverpool John Moores University).

Hlaciuc, E., Vultur, P., Cretu, F. and Ailoaiei, R., 2017. The interface between financial and

management accounting. The USV Annals of Economics and Public Administration, 17(2

(26)), pp.103-110.

Tenhunen, M.L., 2018. THE IMPORTANT NEED OF GENERAL ACCOUNTING AND

MANAGEMENT ACCOUNTING. Euromentor Journal-Studies about education, 9(04),

pp.37-43.

Ramachandran, N. and Kakani, R.K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Cuzdriorean, D.D., 2017. The use of management accounting practices by Romanian small and

medium-sized enterprises: A field study. Journal of Accounting and Management

Information Systems, 16(2), pp.291-312.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.