Accounting Fundamentals Assignment

VerifiedAdded on 2020/12/10

|19

|4647

|349

Homework Assignment

AI Summary

This assignment covers accounting fundamentals, including ledger accounts, trial balance, and financial statements. It analyzes various companies, demonstrating the application of accounting principles in real-world scenarios. The assignment also distinguishes between revenue expenditure and capital expenditure, providing a comprehensive understanding of these key accounting concepts.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING

FUNDAMENTALS

FUNDAMENTALS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Ledger accounts of Maxim...............................................................................................1

(b) Trial balance of Maxim ....................................................................................................3

(c) Final Statements of maxim...............................................................................................4

TASK 2............................................................................................................................................5

(a) Ledgers accounts of Pendo...............................................................................................5

(b) Trial balance of Pendo......................................................................................................6

(c) Income statement of Pendo...............................................................................................7

TASK 3............................................................................................................................................8

(a) Ledger accounts of Mafuta...............................................................................................8

(b) Trial balance of Mafuta...................................................................................................10

TASK 4..........................................................................................................................................11

(a) Ledger accounts of Ricardo............................................................................................11

(b) Trial balance of Ricardo.................................................................................................14

TASK 5..........................................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Ledger accounts of Maxim...............................................................................................1

(b) Trial balance of Maxim ....................................................................................................3

(c) Final Statements of maxim...............................................................................................4

TASK 2............................................................................................................................................5

(a) Ledgers accounts of Pendo...............................................................................................5

(b) Trial balance of Pendo......................................................................................................6

(c) Income statement of Pendo...............................................................................................7

TASK 3............................................................................................................................................8

(a) Ledger accounts of Mafuta...............................................................................................8

(b) Trial balance of Mafuta...................................................................................................10

TASK 4..........................................................................................................................................11

(a) Ledger accounts of Ricardo............................................................................................11

(b) Trial balance of Ricardo.................................................................................................14

TASK 5..........................................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Accounting fundamentals are using as tool by every company for accounting activities.

(Joseph and Renardy, 2013). With the help of these tools solve complex terms that are occur in

business when recorded transactions. Advanced accounting totally depended on the fundamental

equation that described all business's success and failure. These fundamentals are helping to deal

with particular financial function of business. This report consist of analysis of ledger accounts,

income statement and financial position statement of each company. Evaluation distinction

between revenue expenditure and capital expenditure as per international accounting standard is

also performed in this report.

TASK 1

(a) Ledger accounts of Maxim

Accounting terms are firstly recorded in journal account as entries than these entries are

recorded in ledger accounts. These accounts are helping to maintain all component that are

connected to financial statements (Niroomandi, et. Al, 2012). Financial information are stored in

ledger account and presenting opening balance and closing balance of each account during

accounting period. Single transactions are identified with in a ledger account with a transaction

number. Ledger accounts are divided into two parts according to financial statements these are

income statement ledger account and balance sheet ledger account.

1

Accounting fundamentals are using as tool by every company for accounting activities.

(Joseph and Renardy, 2013). With the help of these tools solve complex terms that are occur in

business when recorded transactions. Advanced accounting totally depended on the fundamental

equation that described all business's success and failure. These fundamentals are helping to deal

with particular financial function of business. This report consist of analysis of ledger accounts,

income statement and financial position statement of each company. Evaluation distinction

between revenue expenditure and capital expenditure as per international accounting standard is

also performed in this report.

TASK 1

(a) Ledger accounts of Maxim

Accounting terms are firstly recorded in journal account as entries than these entries are

recorded in ledger accounts. These accounts are helping to maintain all component that are

connected to financial statements (Niroomandi, et. Al, 2012). Financial information are stored in

ledger account and presenting opening balance and closing balance of each account during

accounting period. Single transactions are identified with in a ledger account with a transaction

number. Ledger accounts are divided into two parts according to financial statements these are

income statement ledger account and balance sheet ledger account.

1

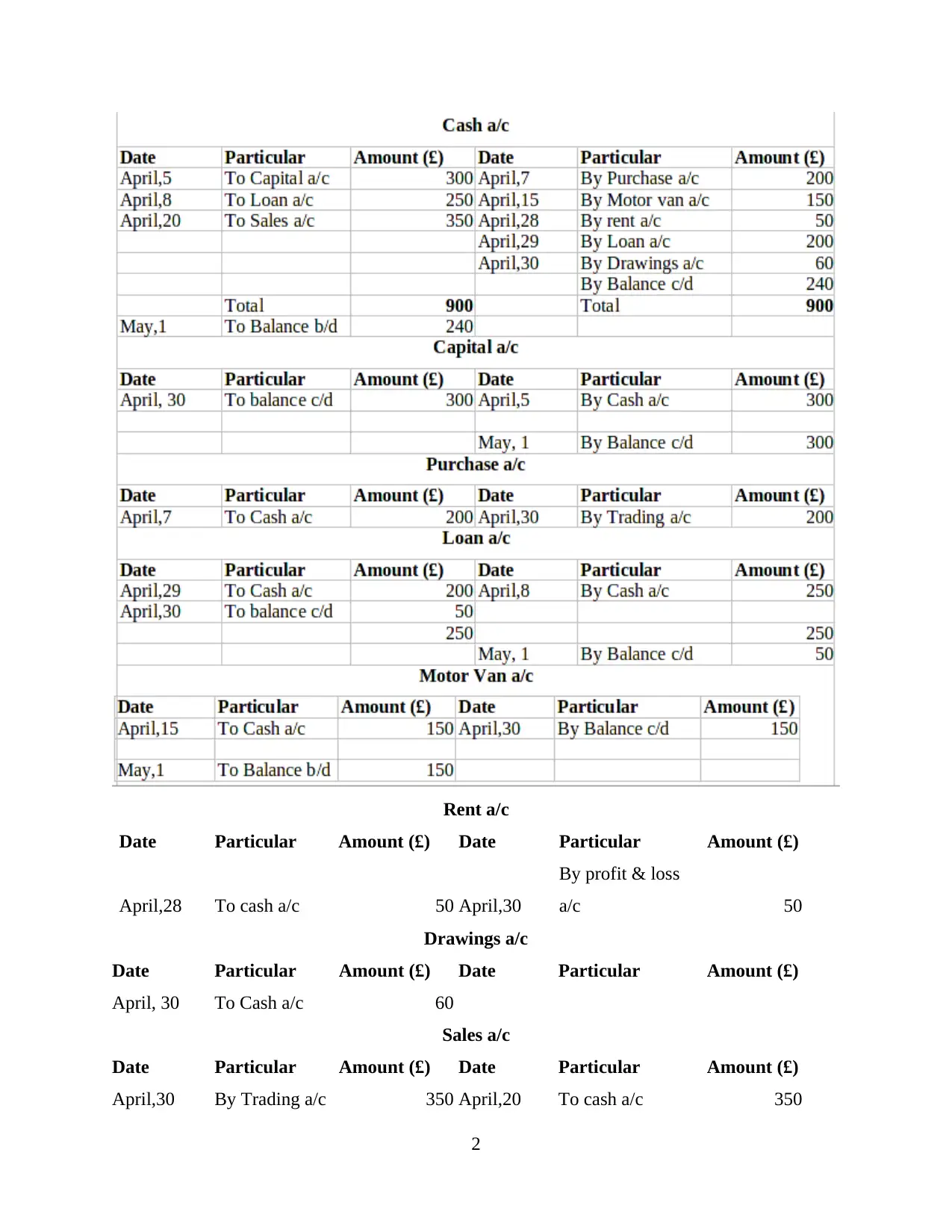

Rent a/c

Date Particular Amount (£) Date Particular Amount (£)

April,28 To cash a/c 50 April,30

By profit & loss

a/c 50

Drawings a/c

Date Particular Amount (£) Date Particular Amount (£)

April, 30 To Cash a/c 60

Sales a/c

Date Particular Amount (£) Date Particular Amount (£)

April,30 By Trading a/c 350 April,20 To cash a/c 350

2

Date Particular Amount (£) Date Particular Amount (£)

April,28 To cash a/c 50 April,30

By profit & loss

a/c 50

Drawings a/c

Date Particular Amount (£) Date Particular Amount (£)

April, 30 To Cash a/c 60

Sales a/c

Date Particular Amount (£) Date Particular Amount (£)

April,30 By Trading a/c 350 April,20 To cash a/c 350

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

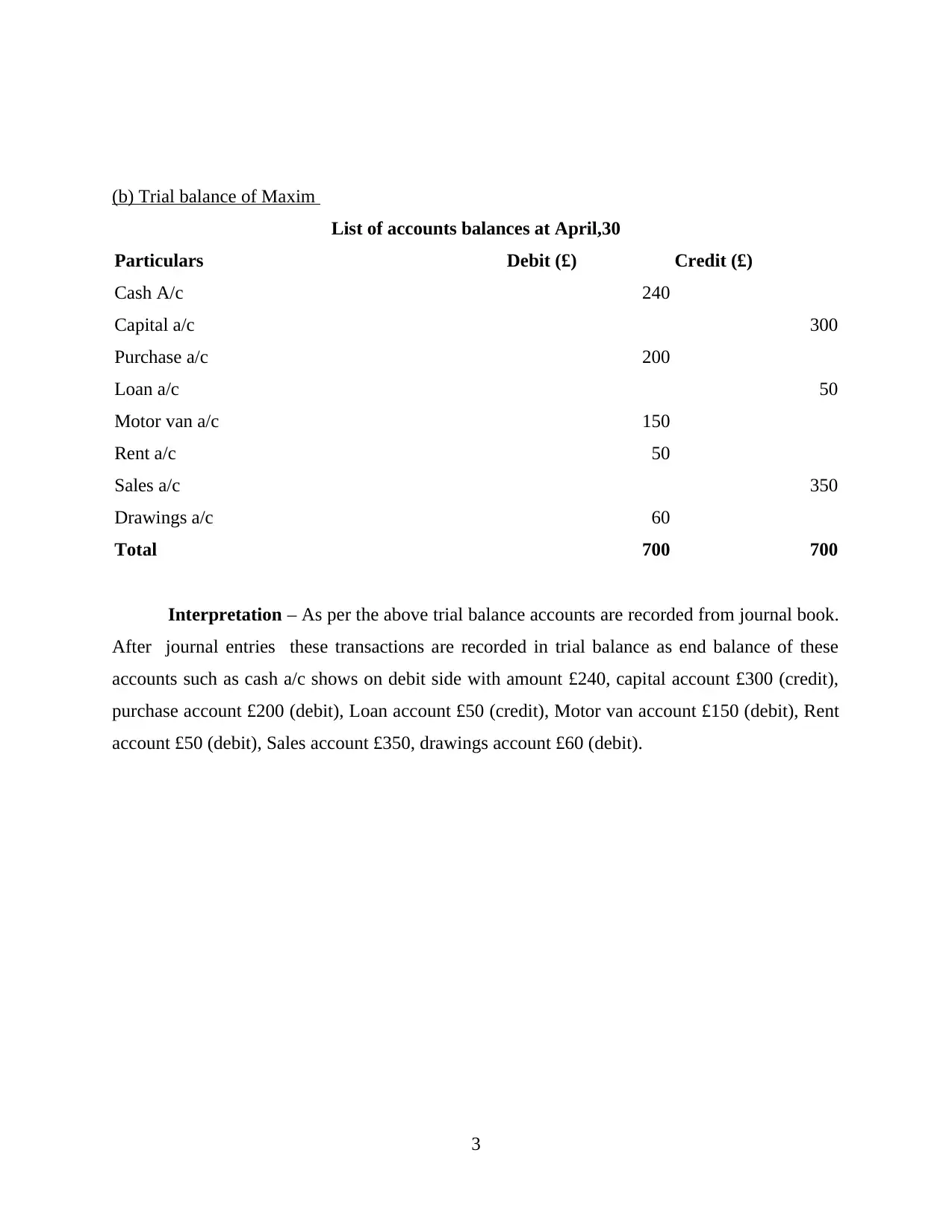

(b) Trial balance of Maxim

List of accounts balances at April,30

Particulars Debit (£) Credit (£)

Cash A/c 240

Capital a/c 300

Purchase a/c 200

Loan a/c 50

Motor van a/c 150

Rent a/c 50

Sales a/c 350

Drawings a/c 60

Total 700 700

Interpretation – As per the above trial balance accounts are recorded from journal book.

After journal entries these transactions are recorded in trial balance as end balance of these

accounts such as cash a/c shows on debit side with amount £240, capital account £300 (credit),

purchase account £200 (debit), Loan account £50 (credit), Motor van account £150 (debit), Rent

account £50 (debit), Sales account £350, drawings account £60 (debit).

3

List of accounts balances at April,30

Particulars Debit (£) Credit (£)

Cash A/c 240

Capital a/c 300

Purchase a/c 200

Loan a/c 50

Motor van a/c 150

Rent a/c 50

Sales a/c 350

Drawings a/c 60

Total 700 700

Interpretation – As per the above trial balance accounts are recorded from journal book.

After journal entries these transactions are recorded in trial balance as end balance of these

accounts such as cash a/c shows on debit side with amount £240, capital account £300 (credit),

purchase account £200 (debit), Loan account £50 (credit), Motor van account £150 (debit), Rent

account £50 (debit), Sales account £350, drawings account £60 (debit).

3

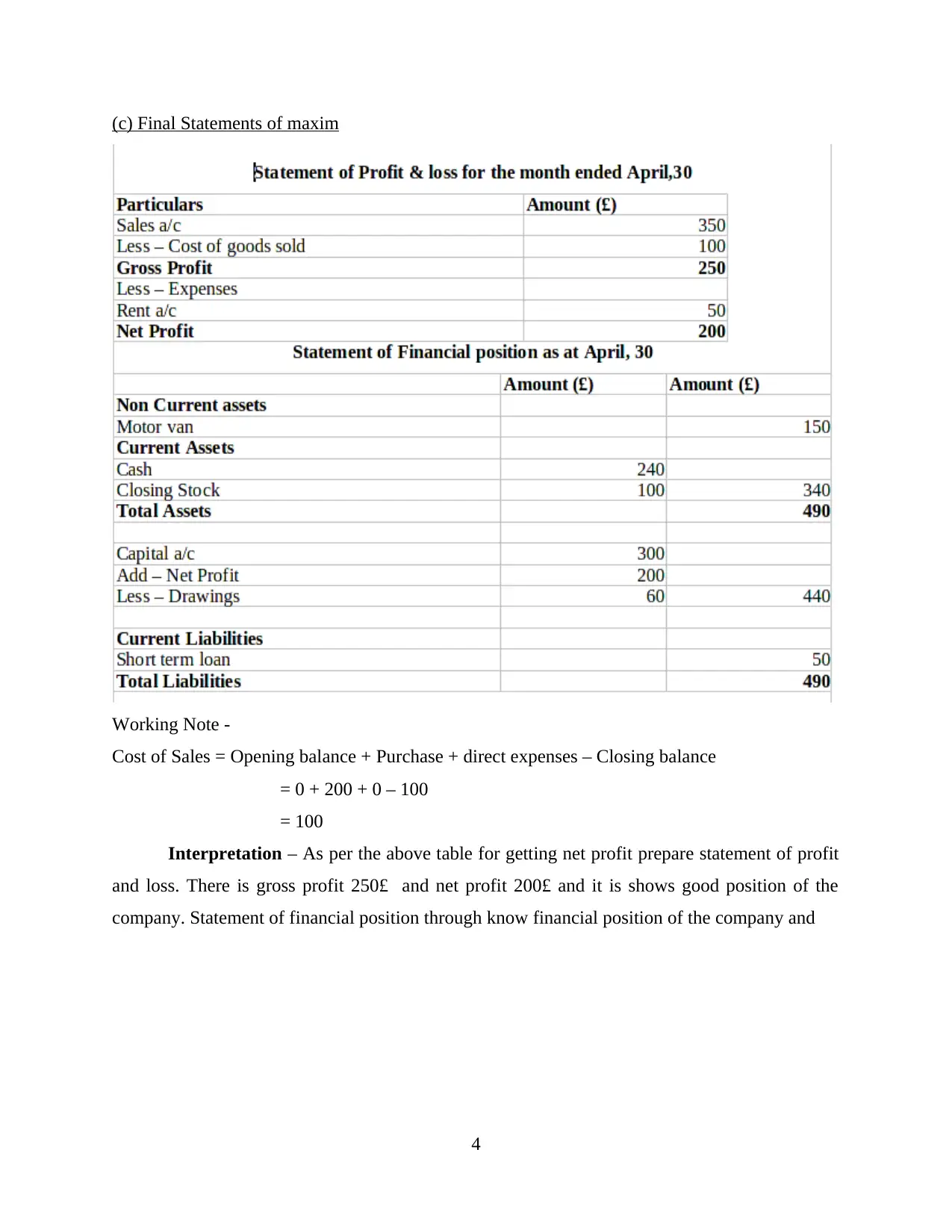

(c) Final Statements of maxim

Working Note -

Cost of Sales = Opening balance + Purchase + direct expenses – Closing balance

= 0 + 200 + 0 – 100

= 100

Interpretation – As per the above table for getting net profit prepare statement of profit

and loss. There is gross profit 250£ and net profit 200£ and it is shows good position of the

company. Statement of financial position through know financial position of the company and

4

Working Note -

Cost of Sales = Opening balance + Purchase + direct expenses – Closing balance

= 0 + 200 + 0 – 100

= 100

Interpretation – As per the above table for getting net profit prepare statement of profit

and loss. There is gross profit 250£ and net profit 200£ and it is shows good position of the

company. Statement of financial position through know financial position of the company and

4

TASK 2

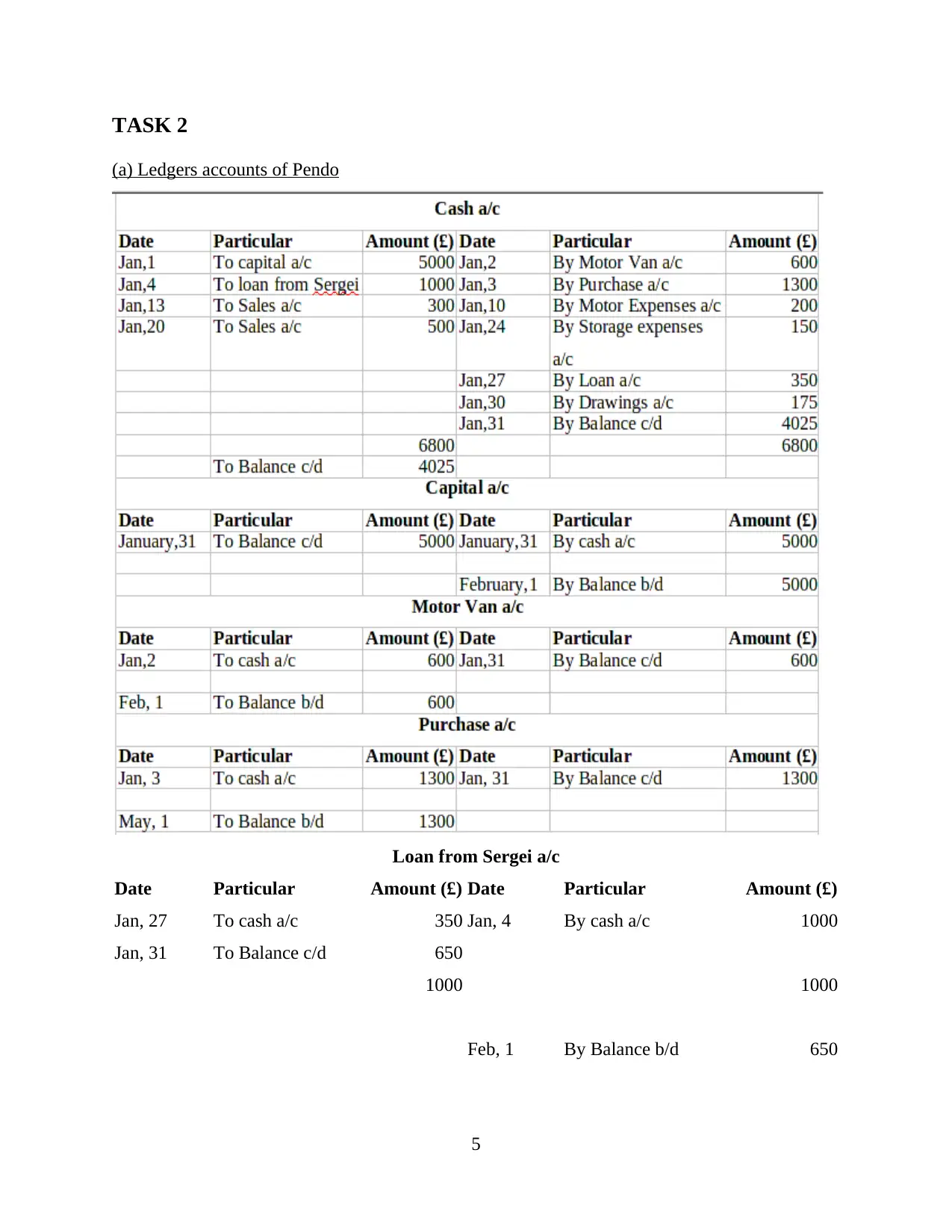

(a) Ledgers accounts of Pendo

Loan from Sergei a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 27 To cash a/c 350 Jan, 4 By cash a/c 1000

Jan, 31 To Balance c/d 650

1000 1000

Feb, 1 By Balance b/d 650

5

(a) Ledgers accounts of Pendo

Loan from Sergei a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 27 To cash a/c 350 Jan, 4 By cash a/c 1000

Jan, 31 To Balance c/d 650

1000 1000

Feb, 1 By Balance b/d 650

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

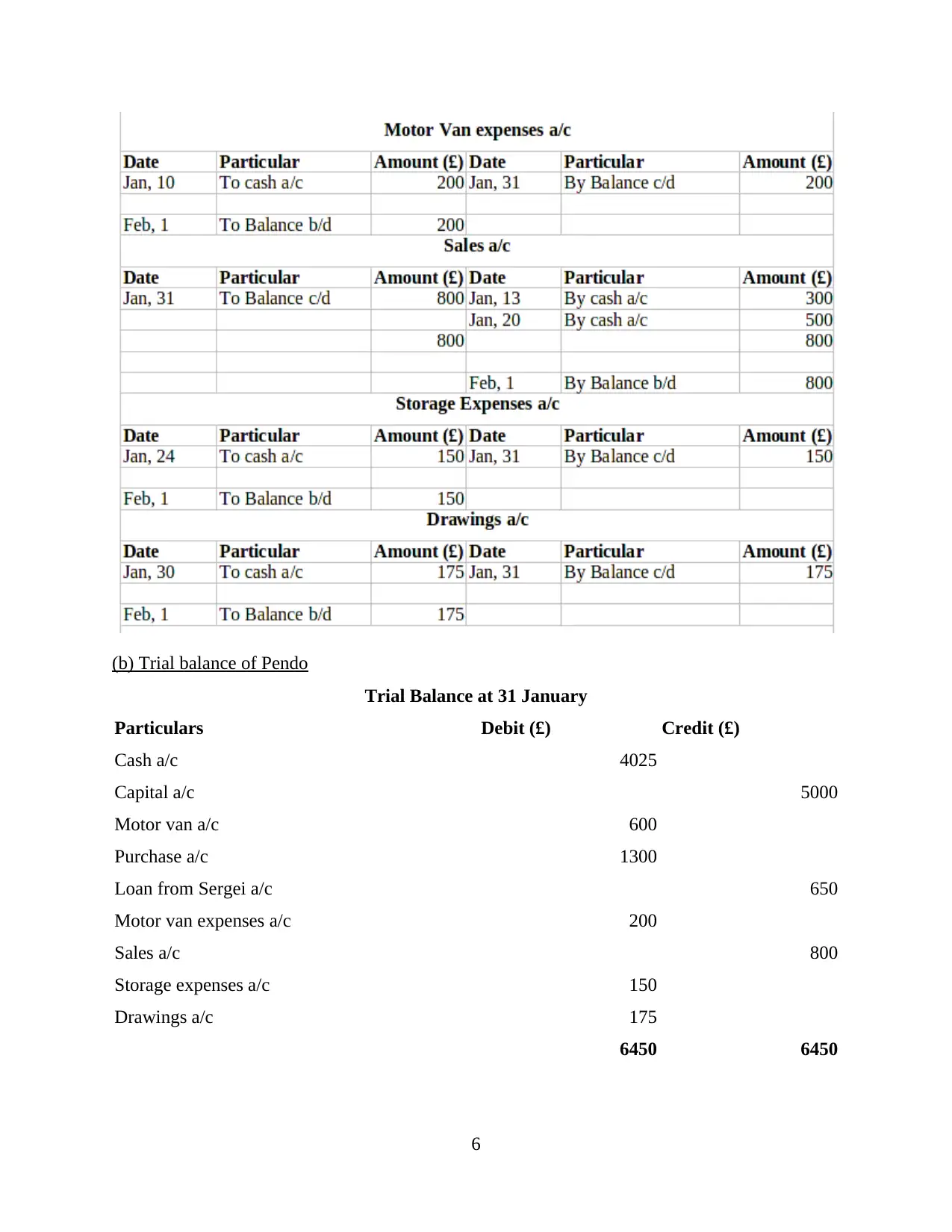

(b) Trial balance of Pendo

Trial Balance at 31 January

Particulars Debit (£) Credit (£)

Cash a/c 4025

Capital a/c 5000

Motor van a/c 600

Purchase a/c 1300

Loan from Sergei a/c 650

Motor van expenses a/c 200

Sales a/c 800

Storage expenses a/c 150

Drawings a/c 175

6450 6450

6

Trial Balance at 31 January

Particulars Debit (£) Credit (£)

Cash a/c 4025

Capital a/c 5000

Motor van a/c 600

Purchase a/c 1300

Loan from Sergei a/c 650

Motor van expenses a/c 200

Sales a/c 800

Storage expenses a/c 150

Drawings a/c 175

6450 6450

6

Interpretation – As per the above table there are presents all closing balances of the

various accounts these are as follows – Cash account £4025 (debit), capital account £5000

(credit), motor van account £600 (debit), purchase account £1300 (debit), Loan account £650

(credit), motor van expenses account £200 (debit), sales account £800 (credit), storage expenses

account £150 (debit), and drawings account £175 (debit).

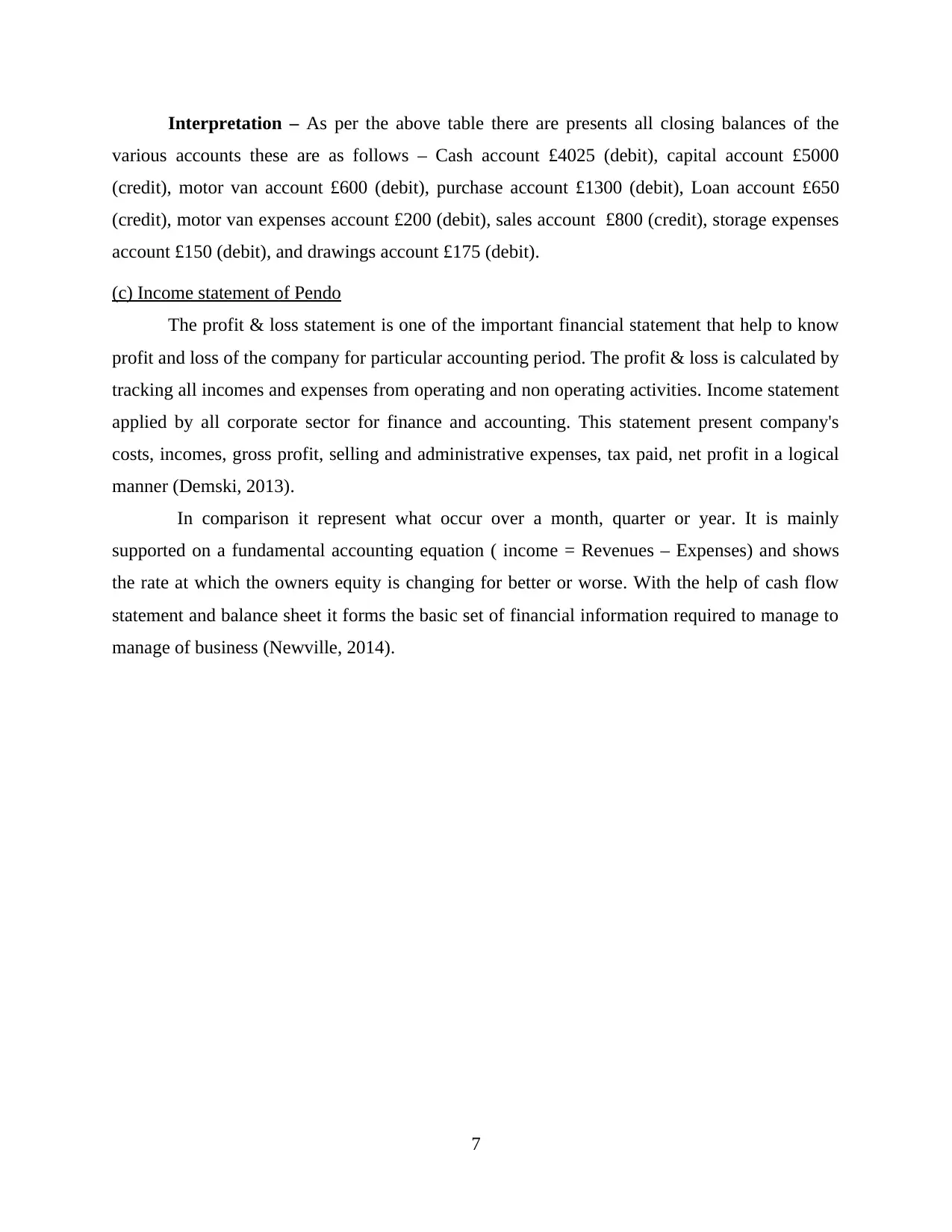

(c) Income statement of Pendo

The profit & loss statement is one of the important financial statement that help to know

profit and loss of the company for particular accounting period. The profit & loss is calculated by

tracking all incomes and expenses from operating and non operating activities. Income statement

applied by all corporate sector for finance and accounting. This statement present company's

costs, incomes, gross profit, selling and administrative expenses, tax paid, net profit in a logical

manner (Demski, 2013).

In comparison it represent what occur over a month, quarter or year. It is mainly

supported on a fundamental accounting equation ( income = Revenues – Expenses) and shows

the rate at which the owners equity is changing for better or worse. With the help of cash flow

statement and balance sheet it forms the basic set of financial information required to manage to

manage of business (Newville, 2014).

7

various accounts these are as follows – Cash account £4025 (debit), capital account £5000

(credit), motor van account £600 (debit), purchase account £1300 (debit), Loan account £650

(credit), motor van expenses account £200 (debit), sales account £800 (credit), storage expenses

account £150 (debit), and drawings account £175 (debit).

(c) Income statement of Pendo

The profit & loss statement is one of the important financial statement that help to know

profit and loss of the company for particular accounting period. The profit & loss is calculated by

tracking all incomes and expenses from operating and non operating activities. Income statement

applied by all corporate sector for finance and accounting. This statement present company's

costs, incomes, gross profit, selling and administrative expenses, tax paid, net profit in a logical

manner (Demski, 2013).

In comparison it represent what occur over a month, quarter or year. It is mainly

supported on a fundamental accounting equation ( income = Revenues – Expenses) and shows

the rate at which the owners equity is changing for better or worse. With the help of cash flow

statement and balance sheet it forms the basic set of financial information required to manage to

manage of business (Newville, 2014).

7

TASK 3

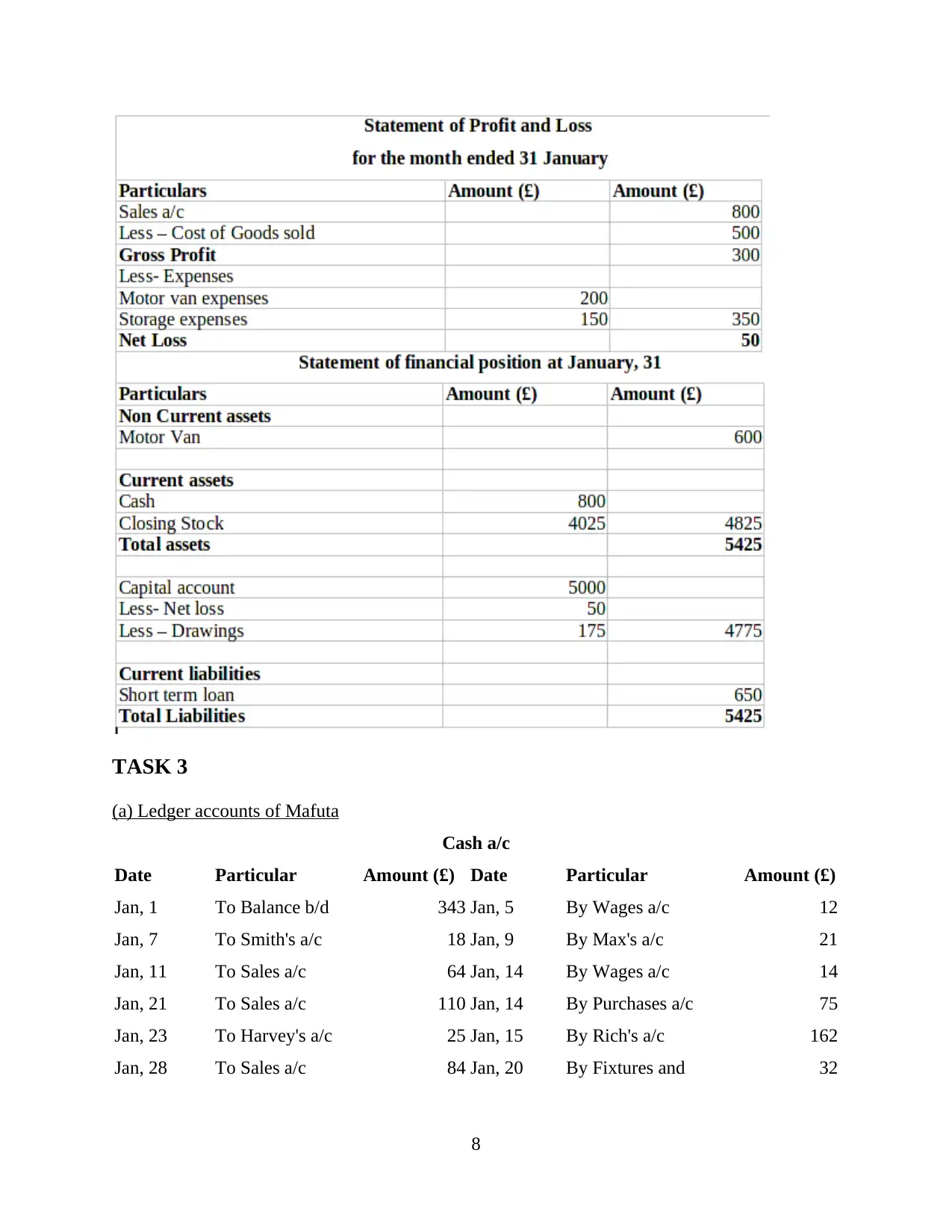

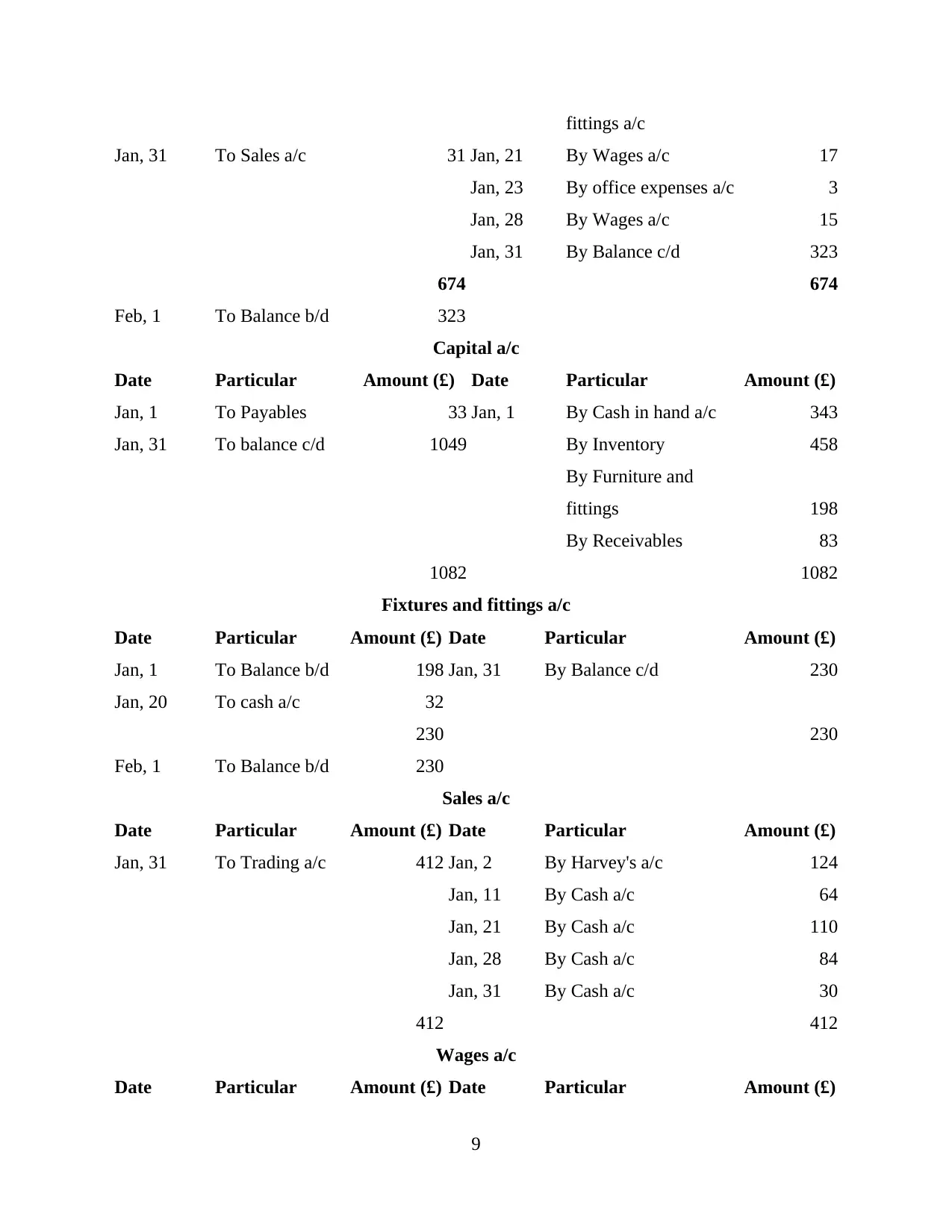

(a) Ledger accounts of Mafuta

Cash a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 343 Jan, 5 By Wages a/c 12

Jan, 7 To Smith's a/c 18 Jan, 9 By Max's a/c 21

Jan, 11 To Sales a/c 64 Jan, 14 By Wages a/c 14

Jan, 21 To Sales a/c 110 Jan, 14 By Purchases a/c 75

Jan, 23 To Harvey's a/c 25 Jan, 15 By Rich's a/c 162

Jan, 28 To Sales a/c 84 Jan, 20 By Fixtures and 32

8

(a) Ledger accounts of Mafuta

Cash a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 343 Jan, 5 By Wages a/c 12

Jan, 7 To Smith's a/c 18 Jan, 9 By Max's a/c 21

Jan, 11 To Sales a/c 64 Jan, 14 By Wages a/c 14

Jan, 21 To Sales a/c 110 Jan, 14 By Purchases a/c 75

Jan, 23 To Harvey's a/c 25 Jan, 15 By Rich's a/c 162

Jan, 28 To Sales a/c 84 Jan, 20 By Fixtures and 32

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

fittings a/c

Jan, 31 To Sales a/c 31 Jan, 21 By Wages a/c 17

Jan, 23 By office expenses a/c 3

Jan, 28 By Wages a/c 15

Jan, 31 By Balance c/d 323

674 674

Feb, 1 To Balance b/d 323

Capital a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Payables 33 Jan, 1 By Cash in hand a/c 343

Jan, 31 To balance c/d 1049 By Inventory 458

By Furniture and

fittings 198

By Receivables 83

1082 1082

Fixtures and fittings a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 198 Jan, 31 By Balance c/d 230

Jan, 20 To cash a/c 32

230 230

Feb, 1 To Balance b/d 230

Sales a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 31 To Trading a/c 412 Jan, 2 By Harvey's a/c 124

Jan, 11 By Cash a/c 64

Jan, 21 By Cash a/c 110

Jan, 28 By Cash a/c 84

Jan, 31 By Cash a/c 30

412 412

Wages a/c

Date Particular Amount (£) Date Particular Amount (£)

9

Jan, 31 To Sales a/c 31 Jan, 21 By Wages a/c 17

Jan, 23 By office expenses a/c 3

Jan, 28 By Wages a/c 15

Jan, 31 By Balance c/d 323

674 674

Feb, 1 To Balance b/d 323

Capital a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Payables 33 Jan, 1 By Cash in hand a/c 343

Jan, 31 To balance c/d 1049 By Inventory 458

By Furniture and

fittings 198

By Receivables 83

1082 1082

Fixtures and fittings a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 198 Jan, 31 By Balance c/d 230

Jan, 20 To cash a/c 32

230 230

Feb, 1 To Balance b/d 230

Sales a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 31 To Trading a/c 412 Jan, 2 By Harvey's a/c 124

Jan, 11 By Cash a/c 64

Jan, 21 By Cash a/c 110

Jan, 28 By Cash a/c 84

Jan, 31 By Cash a/c 30

412 412

Wages a/c

Date Particular Amount (£) Date Particular Amount (£)

9

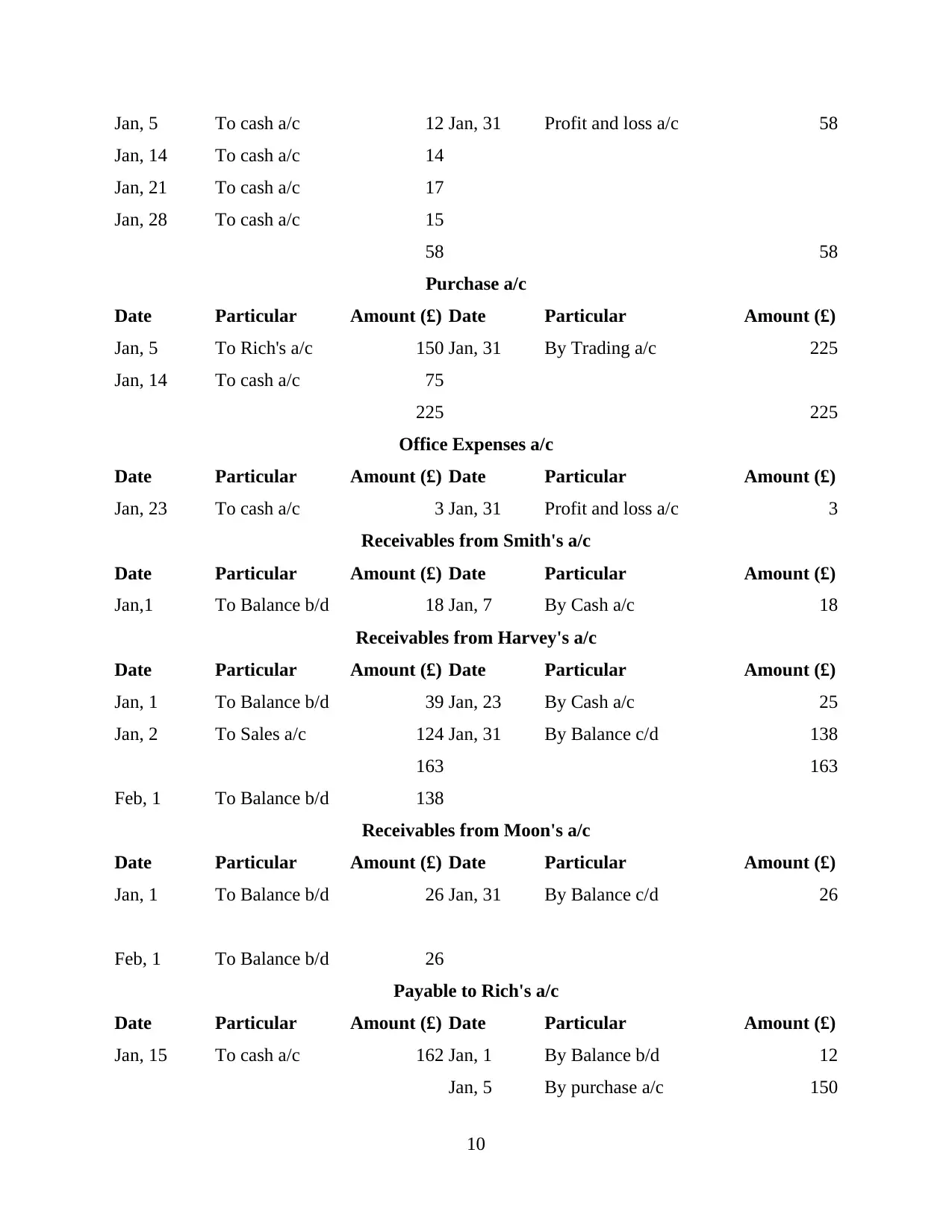

Jan, 5 To cash a/c 12 Jan, 31 Profit and loss a/c 58

Jan, 14 To cash a/c 14

Jan, 21 To cash a/c 17

Jan, 28 To cash a/c 15

58 58

Purchase a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 5 To Rich's a/c 150 Jan, 31 By Trading a/c 225

Jan, 14 To cash a/c 75

225 225

Office Expenses a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 23 To cash a/c 3 Jan, 31 Profit and loss a/c 3

Receivables from Smith's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan,1 To Balance b/d 18 Jan, 7 By Cash a/c 18

Receivables from Harvey's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 39 Jan, 23 By Cash a/c 25

Jan, 2 To Sales a/c 124 Jan, 31 By Balance c/d 138

163 163

Feb, 1 To Balance b/d 138

Receivables from Moon's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 26 Jan, 31 By Balance c/d 26

Feb, 1 To Balance b/d 26

Payable to Rich's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 15 To cash a/c 162 Jan, 1 By Balance b/d 12

Jan, 5 By purchase a/c 150

10

Jan, 14 To cash a/c 14

Jan, 21 To cash a/c 17

Jan, 28 To cash a/c 15

58 58

Purchase a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 5 To Rich's a/c 150 Jan, 31 By Trading a/c 225

Jan, 14 To cash a/c 75

225 225

Office Expenses a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 23 To cash a/c 3 Jan, 31 Profit and loss a/c 3

Receivables from Smith's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan,1 To Balance b/d 18 Jan, 7 By Cash a/c 18

Receivables from Harvey's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 39 Jan, 23 By Cash a/c 25

Jan, 2 To Sales a/c 124 Jan, 31 By Balance c/d 138

163 163

Feb, 1 To Balance b/d 138

Receivables from Moon's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 26 Jan, 31 By Balance c/d 26

Feb, 1 To Balance b/d 26

Payable to Rich's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 15 To cash a/c 162 Jan, 1 By Balance b/d 12

Jan, 5 By purchase a/c 150

10

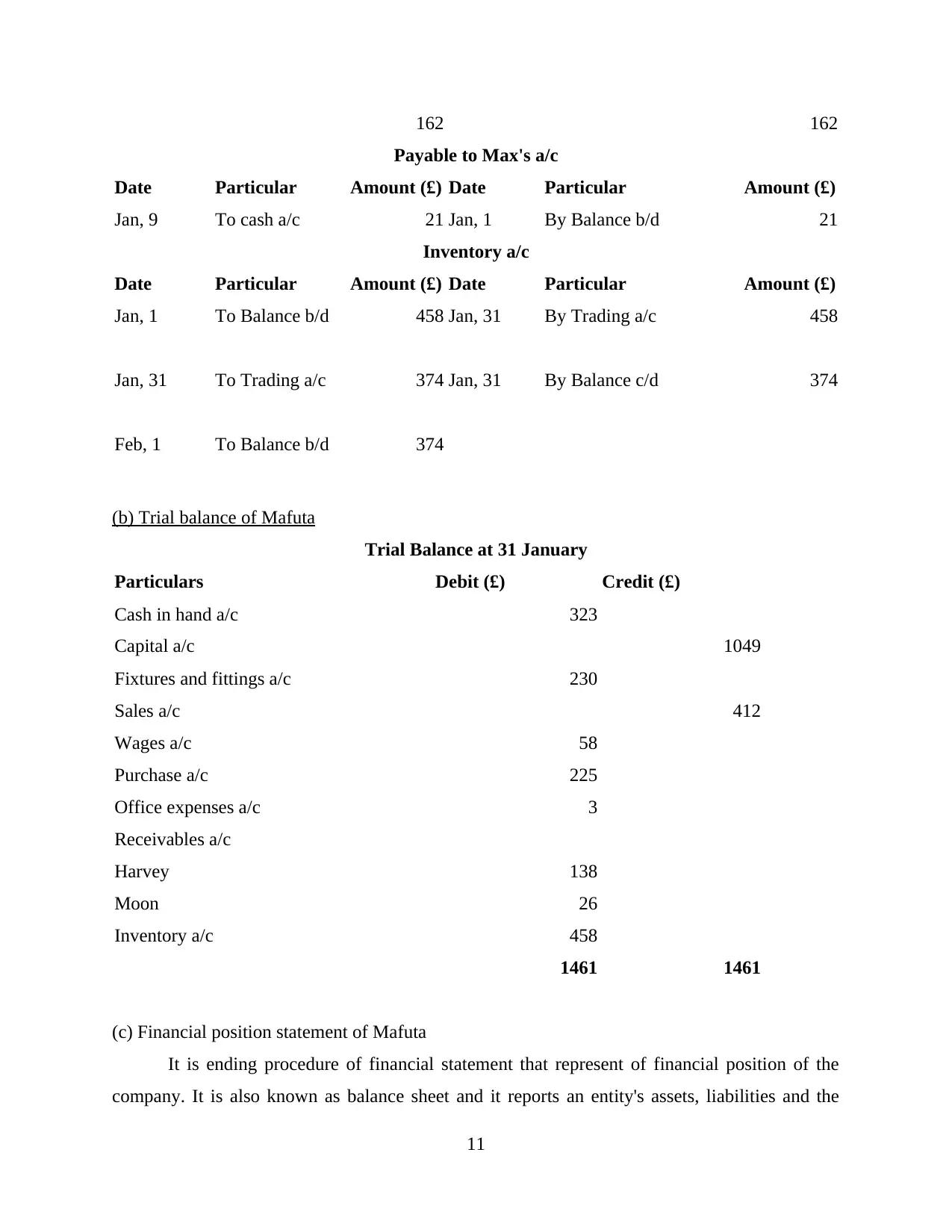

162 162

Payable to Max's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 9 To cash a/c 21 Jan, 1 By Balance b/d 21

Inventory a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 458 Jan, 31 By Trading a/c 458

Jan, 31 To Trading a/c 374 Jan, 31 By Balance c/d 374

Feb, 1 To Balance b/d 374

(b) Trial balance of Mafuta

Trial Balance at 31 January

Particulars Debit (£) Credit (£)

Cash in hand a/c 323

Capital a/c 1049

Fixtures and fittings a/c 230

Sales a/c 412

Wages a/c 58

Purchase a/c 225

Office expenses a/c 3

Receivables a/c

Harvey 138

Moon 26

Inventory a/c 458

1461 1461

(c) Financial position statement of Mafuta

It is ending procedure of financial statement that represent of financial position of the

company. It is also known as balance sheet and it reports an entity's assets, liabilities and the

11

Payable to Max's a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 9 To cash a/c 21 Jan, 1 By Balance b/d 21

Inventory a/c

Date Particular Amount (£) Date Particular Amount (£)

Jan, 1 To Balance b/d 458 Jan, 31 By Trading a/c 458

Jan, 31 To Trading a/c 374 Jan, 31 By Balance c/d 374

Feb, 1 To Balance b/d 374

(b) Trial balance of Mafuta

Trial Balance at 31 January

Particulars Debit (£) Credit (£)

Cash in hand a/c 323

Capital a/c 1049

Fixtures and fittings a/c 230

Sales a/c 412

Wages a/c 58

Purchase a/c 225

Office expenses a/c 3

Receivables a/c

Harvey 138

Moon 26

Inventory a/c 458

1461 1461

(c) Financial position statement of Mafuta

It is ending procedure of financial statement that represent of financial position of the

company. It is also known as balance sheet and it reports an entity's assets, liabilities and the

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

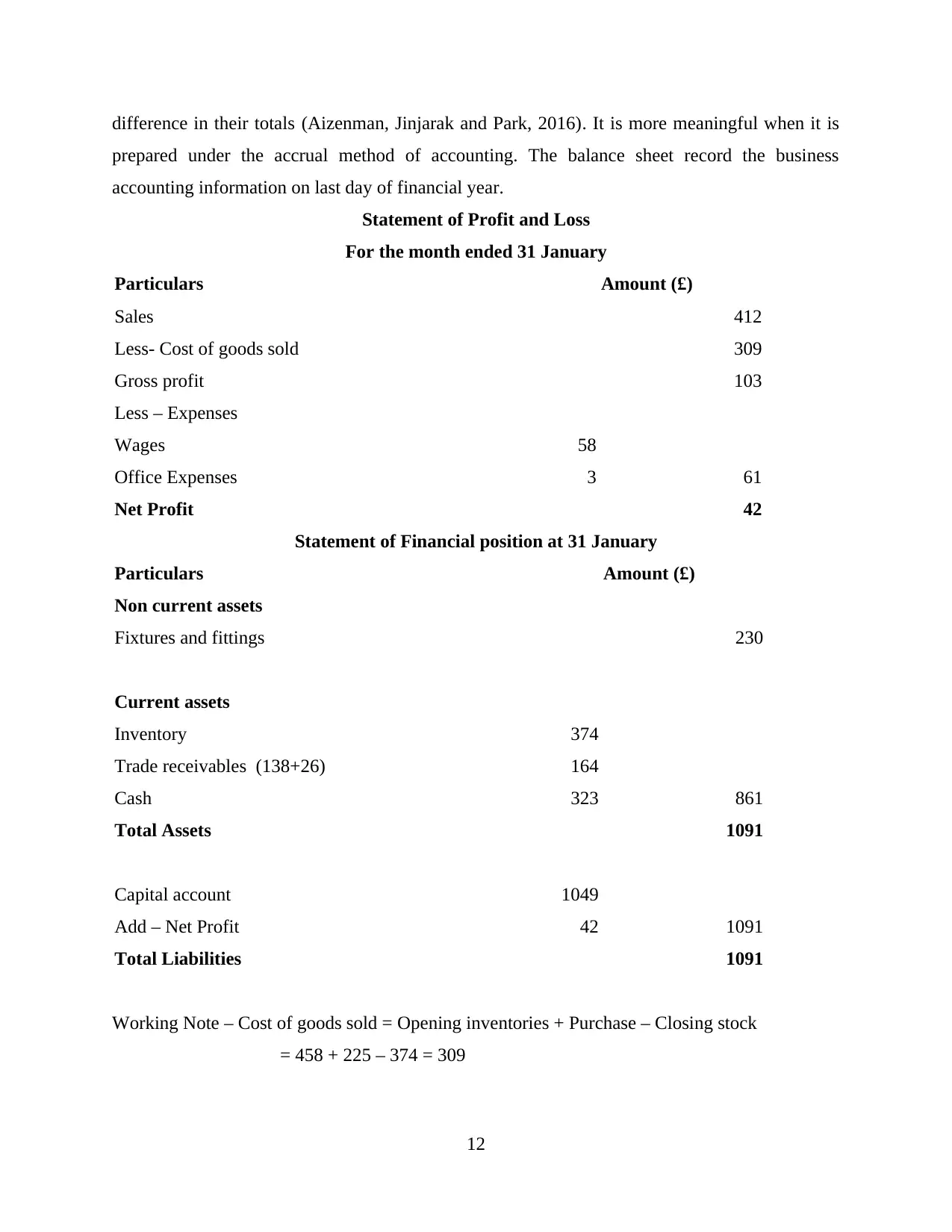

difference in their totals (Aizenman, Jinjarak and Park, 2016). It is more meaningful when it is

prepared under the accrual method of accounting. The balance sheet record the business

accounting information on last day of financial year.

Statement of Profit and Loss

For the month ended 31 January

Particulars Amount (£)

Sales 412

Less- Cost of goods sold 309

Gross profit 103

Less – Expenses

Wages 58

Office Expenses 3 61

Net Profit 42

Statement of Financial position at 31 January

Particulars Amount (£)

Non current assets

Fixtures and fittings 230

Current assets

Inventory 374

Trade receivables (138+26) 164

Cash 323 861

Total Assets 1091

Capital account 1049

Add – Net Profit 42 1091

Total Liabilities 1091

Working Note – Cost of goods sold = Opening inventories + Purchase – Closing stock

= 458 + 225 – 374 = 309

12

prepared under the accrual method of accounting. The balance sheet record the business

accounting information on last day of financial year.

Statement of Profit and Loss

For the month ended 31 January

Particulars Amount (£)

Sales 412

Less- Cost of goods sold 309

Gross profit 103

Less – Expenses

Wages 58

Office Expenses 3 61

Net Profit 42

Statement of Financial position at 31 January

Particulars Amount (£)

Non current assets

Fixtures and fittings 230

Current assets

Inventory 374

Trade receivables (138+26) 164

Cash 323 861

Total Assets 1091

Capital account 1049

Add – Net Profit 42 1091

Total Liabilities 1091

Working Note – Cost of goods sold = Opening inventories + Purchase – Closing stock

= 458 + 225 – 374 = 309

12

TASK 4

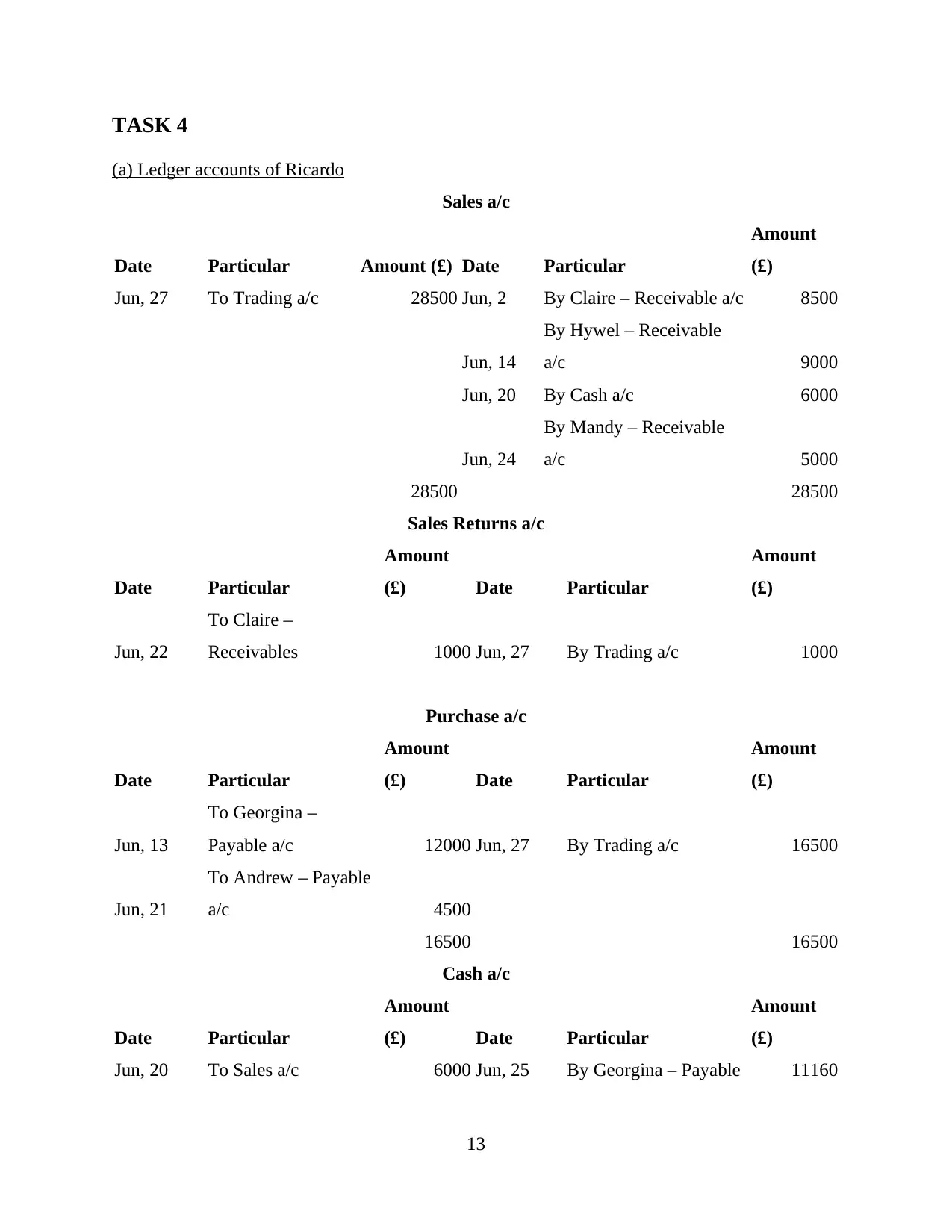

(a) Ledger accounts of Ricardo

Sales a/c

Date Particular Amount (£) Date Particular

Amount

(£)

Jun, 27 To Trading a/c 28500 Jun, 2 By Claire – Receivable a/c 8500

Jun, 14

By Hywel – Receivable

a/c 9000

Jun, 20 By Cash a/c 6000

Jun, 24

By Mandy – Receivable

a/c 5000

28500 28500

Sales Returns a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 22

To Claire –

Receivables 1000 Jun, 27 By Trading a/c 1000

Purchase a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 13

To Georgina –

Payable a/c 12000 Jun, 27 By Trading a/c 16500

Jun, 21

To Andrew – Payable

a/c 4500

16500 16500

Cash a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 20 To Sales a/c 6000 Jun, 25 By Georgina – Payable 11160

13

(a) Ledger accounts of Ricardo

Sales a/c

Date Particular Amount (£) Date Particular

Amount

(£)

Jun, 27 To Trading a/c 28500 Jun, 2 By Claire – Receivable a/c 8500

Jun, 14

By Hywel – Receivable

a/c 9000

Jun, 20 By Cash a/c 6000

Jun, 24

By Mandy – Receivable

a/c 5000

28500 28500

Sales Returns a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 22

To Claire –

Receivables 1000 Jun, 27 By Trading a/c 1000

Purchase a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 13

To Georgina –

Payable a/c 12000 Jun, 27 By Trading a/c 16500

Jun, 21

To Andrew – Payable

a/c 4500

16500 16500

Cash a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 20 To Sales a/c 6000 Jun, 25 By Georgina – Payable 11160

13

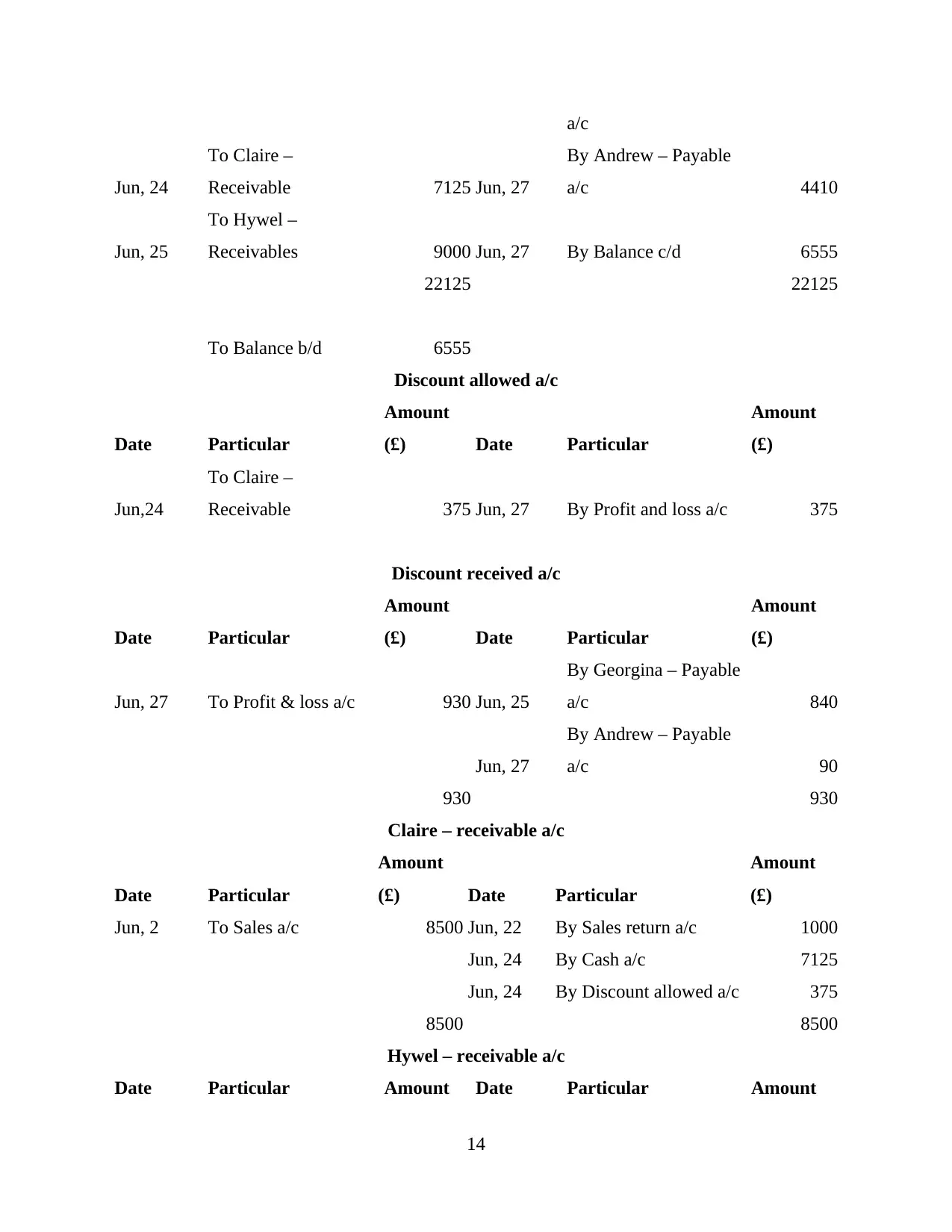

a/c

Jun, 24

To Claire –

Receivable 7125 Jun, 27

By Andrew – Payable

a/c 4410

Jun, 25

To Hywel –

Receivables 9000 Jun, 27 By Balance c/d 6555

22125 22125

To Balance b/d 6555

Discount allowed a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun,24

To Claire –

Receivable 375 Jun, 27 By Profit and loss a/c 375

Discount received a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 27 To Profit & loss a/c 930 Jun, 25

By Georgina – Payable

a/c 840

Jun, 27

By Andrew – Payable

a/c 90

930 930

Claire – receivable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 2 To Sales a/c 8500 Jun, 22 By Sales return a/c 1000

Jun, 24 By Cash a/c 7125

Jun, 24 By Discount allowed a/c 375

8500 8500

Hywel – receivable a/c

Date Particular Amount Date Particular Amount

14

Jun, 24

To Claire –

Receivable 7125 Jun, 27

By Andrew – Payable

a/c 4410

Jun, 25

To Hywel –

Receivables 9000 Jun, 27 By Balance c/d 6555

22125 22125

To Balance b/d 6555

Discount allowed a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun,24

To Claire –

Receivable 375 Jun, 27 By Profit and loss a/c 375

Discount received a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 27 To Profit & loss a/c 930 Jun, 25

By Georgina – Payable

a/c 840

Jun, 27

By Andrew – Payable

a/c 90

930 930

Claire – receivable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 2 To Sales a/c 8500 Jun, 22 By Sales return a/c 1000

Jun, 24 By Cash a/c 7125

Jun, 24 By Discount allowed a/c 375

8500 8500

Hywel – receivable a/c

Date Particular Amount Date Particular Amount

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

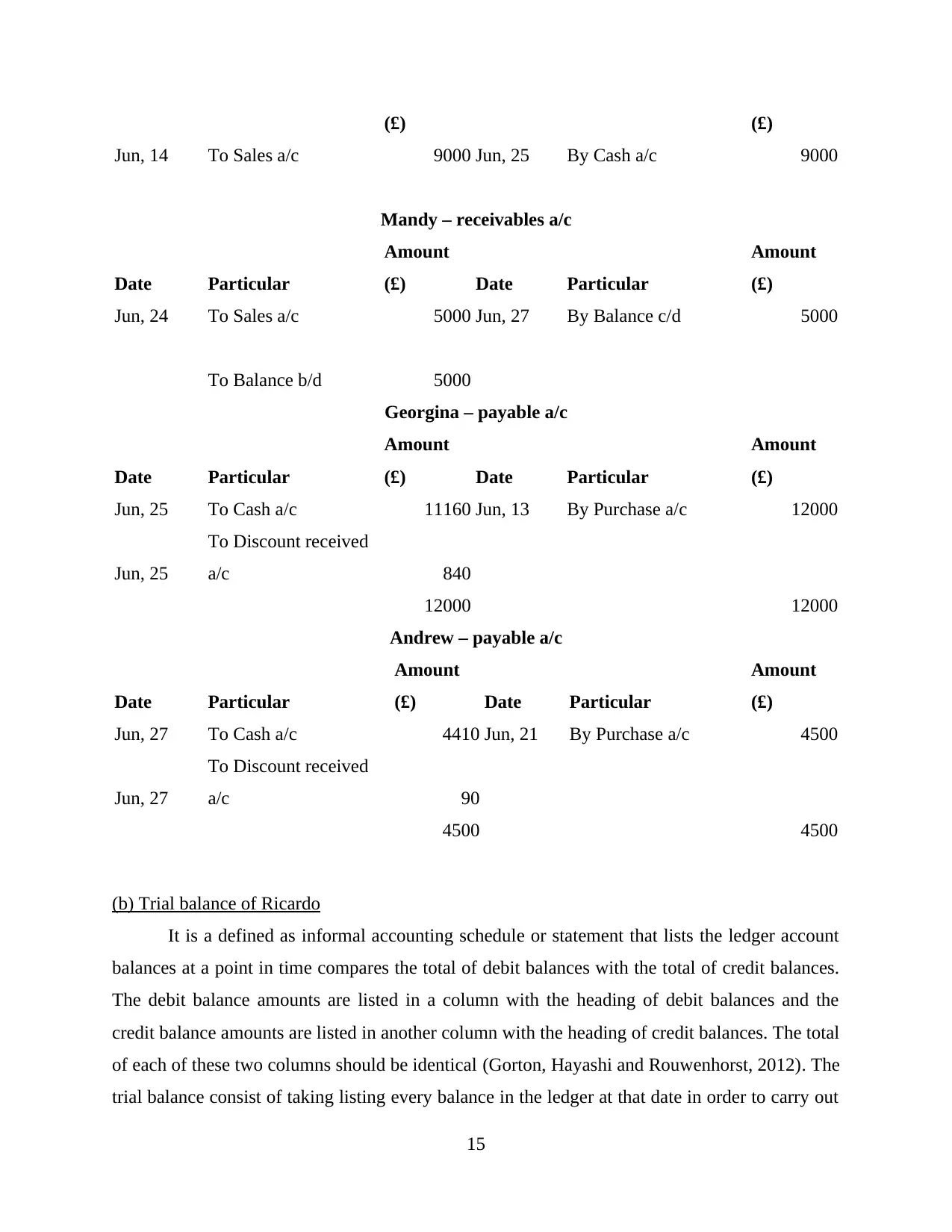

(£) (£)

Jun, 14 To Sales a/c 9000 Jun, 25 By Cash a/c 9000

Mandy – receivables a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 24 To Sales a/c 5000 Jun, 27 By Balance c/d 5000

To Balance b/d 5000

Georgina – payable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 25 To Cash a/c 11160 Jun, 13 By Purchase a/c 12000

Jun, 25

To Discount received

a/c 840

12000 12000

Andrew – payable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 27 To Cash a/c 4410 Jun, 21 By Purchase a/c 4500

Jun, 27

To Discount received

a/c 90

4500 4500

(b) Trial balance of Ricardo

It is a defined as informal accounting schedule or statement that lists the ledger account

balances at a point in time compares the total of debit balances with the total of credit balances.

The debit balance amounts are listed in a column with the heading of debit balances and the

credit balance amounts are listed in another column with the heading of credit balances. The total

of each of these two columns should be identical (Gorton, Hayashi and Rouwenhorst, 2012). The

trial balance consist of taking listing every balance in the ledger at that date in order to carry out

15

Jun, 14 To Sales a/c 9000 Jun, 25 By Cash a/c 9000

Mandy – receivables a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 24 To Sales a/c 5000 Jun, 27 By Balance c/d 5000

To Balance b/d 5000

Georgina – payable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 25 To Cash a/c 11160 Jun, 13 By Purchase a/c 12000

Jun, 25

To Discount received

a/c 840

12000 12000

Andrew – payable a/c

Date Particular

Amount

(£) Date Particular

Amount

(£)

Jun, 27 To Cash a/c 4410 Jun, 21 By Purchase a/c 4500

Jun, 27

To Discount received

a/c 90

4500 4500

(b) Trial balance of Ricardo

It is a defined as informal accounting schedule or statement that lists the ledger account

balances at a point in time compares the total of debit balances with the total of credit balances.

The debit balance amounts are listed in a column with the heading of debit balances and the

credit balance amounts are listed in another column with the heading of credit balances. The total

of each of these two columns should be identical (Gorton, Hayashi and Rouwenhorst, 2012). The

trial balance consist of taking listing every balance in the ledger at that date in order to carry out

15

an arithmetic check of double entry system. To analysis the total of debits and credits in the

accounts are equal, the accountant periodically prepares a trial balances.

Trial balance at 27 June of Ricardo

Particulars Debit Credit

Sales a/c 28500

Purchase a/c 16500

Cash a/c 6555

Sales return a/c 1000

Mandy – Receivable 5000

Discount allowed a/c 930

Discount Received a/c 375

29430 29430

TASK 5

Revenue Expenditure -

Daily basis repairs are related to revenue expenditure because these are deduct directly

from an account such as maintenance and repairs expenses (Dhillon, et. Al, 2014). It is also

known as income statement expenditure. These costs are connected to assets that are not

beneficial because they will not supply a financial benefit in future periods. In different words,

revenues expenditure are excess expenses obtain because of an assets but they don't add any

extra amount to the asset or addition its useful life or productivity. These type expenses are not

recorded in book value of the assets because it is not providing benefits in future. These

expenditure are shows in income statement instead of Balance sheet life (Rahman and Hassan,

2013).

Capital Expenditure -

It mention to funds which are used by business to purchase new machinery and

equipment to modify and improve the business. It is spent for maintenance of long term assets to

improve the capacity and efficiency of those assets (Hutton, 2017). Long term assets are

normally physical, fixed and non consumable assets like property, equipment or infrastructure

that have a useful life of more than one accounting period. Capital expenditure broadly takes two

forms first one maintenance expenditures, where by business buy new assets that extend the

useful life of existing assets. Second one is expansion expenditure. It is important to understand

16

accounts are equal, the accountant periodically prepares a trial balances.

Trial balance at 27 June of Ricardo

Particulars Debit Credit

Sales a/c 28500

Purchase a/c 16500

Cash a/c 6555

Sales return a/c 1000

Mandy – Receivable 5000

Discount allowed a/c 930

Discount Received a/c 375

29430 29430

TASK 5

Revenue Expenditure -

Daily basis repairs are related to revenue expenditure because these are deduct directly

from an account such as maintenance and repairs expenses (Dhillon, et. Al, 2014). It is also

known as income statement expenditure. These costs are connected to assets that are not

beneficial because they will not supply a financial benefit in future periods. In different words,

revenues expenditure are excess expenses obtain because of an assets but they don't add any

extra amount to the asset or addition its useful life or productivity. These type expenses are not

recorded in book value of the assets because it is not providing benefits in future. These

expenditure are shows in income statement instead of Balance sheet life (Rahman and Hassan,

2013).

Capital Expenditure -

It mention to funds which are used by business to purchase new machinery and

equipment to modify and improve the business. It is spent for maintenance of long term assets to

improve the capacity and efficiency of those assets (Hutton, 2017). Long term assets are

normally physical, fixed and non consumable assets like property, equipment or infrastructure

that have a useful life of more than one accounting period. Capital expenditure broadly takes two

forms first one maintenance expenditures, where by business buy new assets that extend the

useful life of existing assets. Second one is expansion expenditure. It is important to understand

16

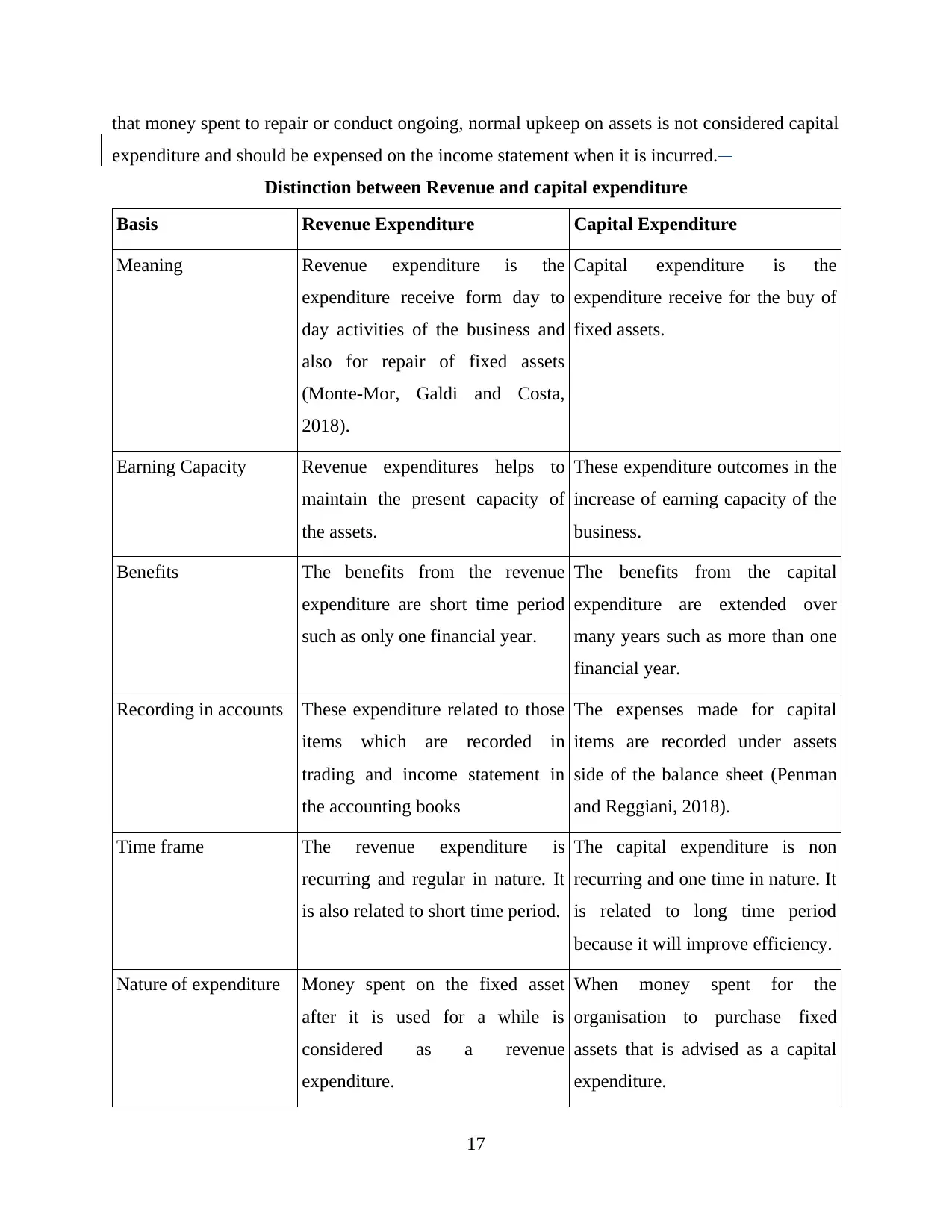

that money spent to repair or conduct ongoing, normal upkeep on assets is not considered capital

expenditure and should be expensed on the income statement when it is incurred.

Distinction between Revenue and capital expenditure

Basis Revenue Expenditure Capital Expenditure

Meaning Revenue expenditure is the

expenditure receive form day to

day activities of the business and

also for repair of fixed assets

(Monte‐Mor, Galdi and Costa,

2018).

Capital expenditure is the

expenditure receive for the buy of

fixed assets.

Earning Capacity Revenue expenditures helps to

maintain the present capacity of

the assets.

These expenditure outcomes in the

increase of earning capacity of the

business.

Benefits The benefits from the revenue

expenditure are short time period

such as only one financial year.

The benefits from the capital

expenditure are extended over

many years such as more than one

financial year.

Recording in accounts These expenditure related to those

items which are recorded in

trading and income statement in

the accounting books

The expenses made for capital

items are recorded under assets

side of the balance sheet (Penman

and Reggiani, 2018).

Time frame The revenue expenditure is

recurring and regular in nature. It

is also related to short time period.

The capital expenditure is non

recurring and one time in nature. It

is related to long time period

because it will improve efficiency.

Nature of expenditure Money spent on the fixed asset

after it is used for a while is

considered as a revenue

expenditure.

When money spent for the

organisation to purchase fixed

assets that is advised as a capital

expenditure.

17

expenditure and should be expensed on the income statement when it is incurred.

Distinction between Revenue and capital expenditure

Basis Revenue Expenditure Capital Expenditure

Meaning Revenue expenditure is the

expenditure receive form day to

day activities of the business and

also for repair of fixed assets

(Monte‐Mor, Galdi and Costa,

2018).

Capital expenditure is the

expenditure receive for the buy of

fixed assets.

Earning Capacity Revenue expenditures helps to

maintain the present capacity of

the assets.

These expenditure outcomes in the

increase of earning capacity of the

business.

Benefits The benefits from the revenue

expenditure are short time period

such as only one financial year.

The benefits from the capital

expenditure are extended over

many years such as more than one

financial year.

Recording in accounts These expenditure related to those

items which are recorded in

trading and income statement in

the accounting books

The expenses made for capital

items are recorded under assets

side of the balance sheet (Penman

and Reggiani, 2018).

Time frame The revenue expenditure is

recurring and regular in nature. It

is also related to short time period.

The capital expenditure is non

recurring and one time in nature. It

is related to long time period

because it will improve efficiency.

Nature of expenditure Money spent on the fixed asset

after it is used for a while is

considered as a revenue

expenditure.

When money spent for the

organisation to purchase fixed

assets that is advised as a capital

expenditure.

17

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.