Accounting Fundamentals Assessment 1 - Eccles plc Financial Analysis

VerifiedAdded on 2023/01/05

|10

|2158

|86

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting fundamentals assessment, focusing on the financial analysis of Eccles plc and Chocco Plc. It includes the preparation of an income statement and a statement of financial position for Eccles plc, along with detailed working notes. The solution further delves into ratio analysis, covering liquidity, solvency, profitability, efficiency, coverage, and market prospect ratios, providing calculations and interpretations for both Eccles plc and Chocco Plc. The analysis offers insights into the financial performance and position of Chocco Plc, highlighting key areas like profitability, debt management, and overall financial health. The document also addresses the balancing of the statement of financial position and explains the underlying accounting principles. Finally, the document provides comments on the financial performance and position of Chocco Plc, analyzing financial ratios and the overall financial health of the company.

Accounting fundamental

assessment 1

assessment 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTIONS...................................................................................................................................3

1. Eccles plc for the year ended 31st December 2018Eccles plc for the year ended 31st

December 2018............................................................................................................................3

B. Why the statement of financial position balances...................................................................5

Question 2........................................................................................................................................6

A. Ratio Analysis.........................................................................................................................6

B. Comment on financial performance and position of Chocco Plc...........................................9

QUESTIONS...................................................................................................................................3

1. Eccles plc for the year ended 31st December 2018Eccles plc for the year ended 31st

December 2018............................................................................................................................3

B. Why the statement of financial position balances...................................................................5

Question 2........................................................................................................................................6

A. Ratio Analysis.........................................................................................................................6

B. Comment on financial performance and position of Chocco Plc...........................................9

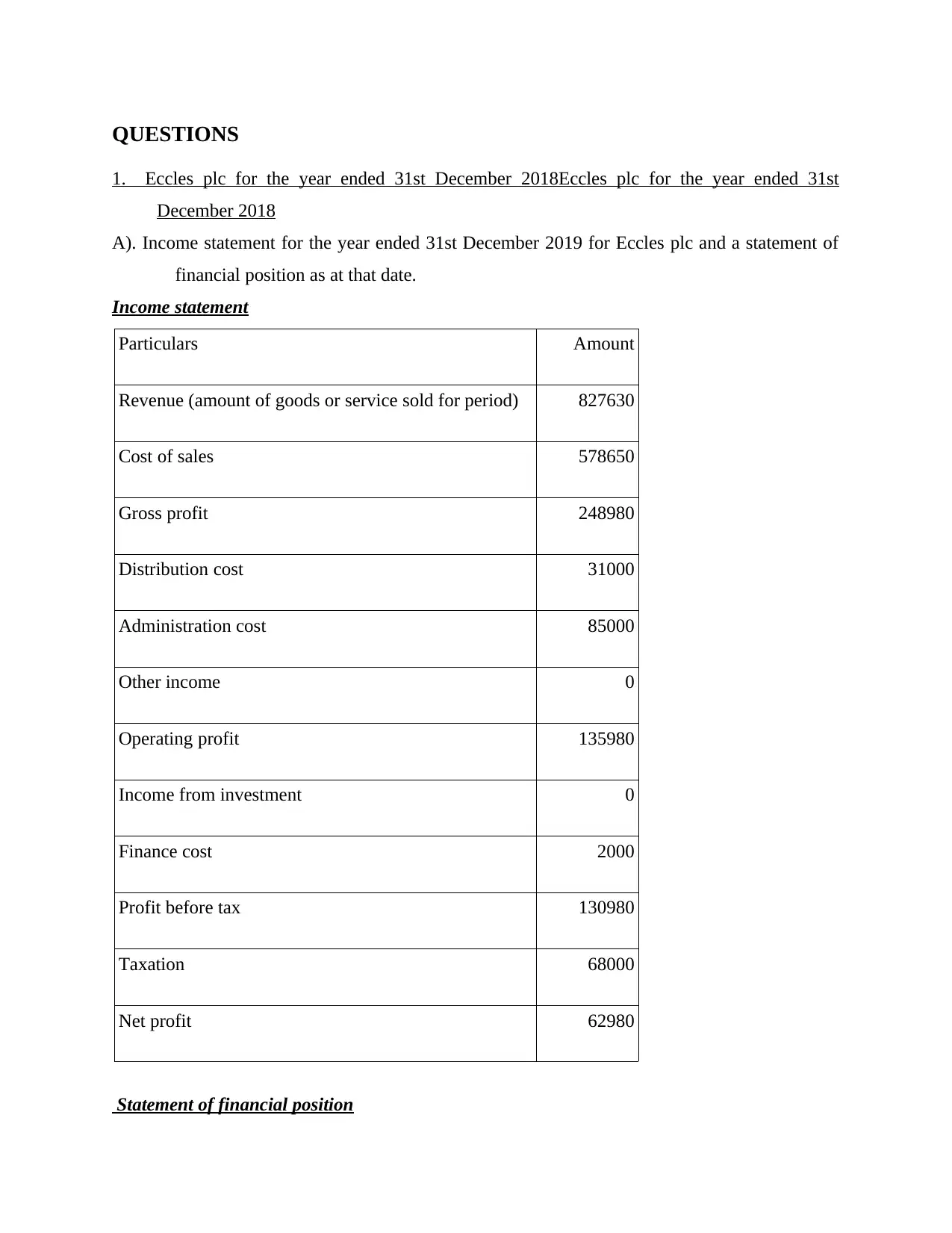

QUESTIONS

1. Eccles plc for the year ended 31st December 2018Eccles plc for the year ended 31st

December 2018

A). Income statement for the year ended 31st December 2019 for Eccles plc and a statement of

financial position as at that date.

Income statement

Particulars Amount

Revenue (amount of goods or service sold for period) 827630

Cost of sales 578650

Gross profit 248980

Distribution cost 31000

Administration cost 85000

Other income 0

Operating profit 135980

Income from investment 0

Finance cost 2000

Profit before tax 130980

Taxation 68000

Net profit 62980

Statement of financial position

1. Eccles plc for the year ended 31st December 2018Eccles plc for the year ended 31st

December 2018

A). Income statement for the year ended 31st December 2019 for Eccles plc and a statement of

financial position as at that date.

Income statement

Particulars Amount

Revenue (amount of goods or service sold for period) 827630

Cost of sales 578650

Gross profit 248980

Distribution cost 31000

Administration cost 85000

Other income 0

Operating profit 135980

Income from investment 0

Finance cost 2000

Profit before tax 130980

Taxation 68000

Net profit 62980

Statement of financial position

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

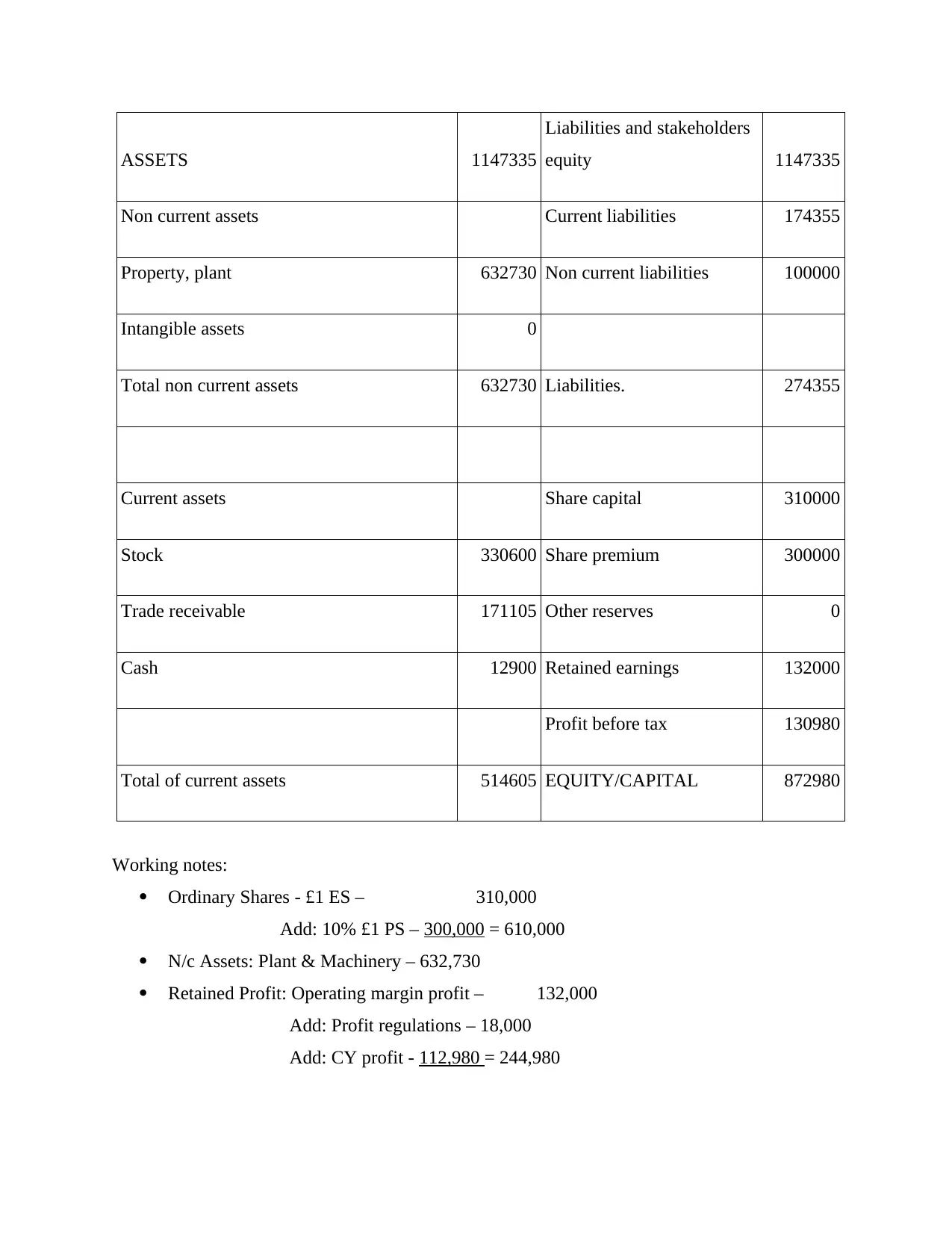

ASSETS 1147335

Liabilities and stakeholders

equity 1147335

Non current assets Current liabilities 174355

Property, plant 632730 Non current liabilities 100000

Intangible assets 0

Total non current assets 632730 Liabilities. 274355

Current assets Share capital 310000

Stock 330600 Share premium 300000

Trade receivable 171105 Other reserves 0

Cash 12900 Retained earnings 132000

Profit before tax 130980

Total of current assets 514605 EQUITY/CAPITAL 872980

Working notes:

Ordinary Shares - £1 ES – 310,000

Add: 10% £1 PS – 300,000 = 610,000

N/c Assets: Plant & Machinery – 632,730

Retained Profit: Operating margin profit – 132,000

Add: Profit regulations – 18,000

Add: CY profit - 112,980 = 244,980

Liabilities and stakeholders

equity 1147335

Non current assets Current liabilities 174355

Property, plant 632730 Non current liabilities 100000

Intangible assets 0

Total non current assets 632730 Liabilities. 274355

Current assets Share capital 310000

Stock 330600 Share premium 300000

Trade receivable 171105 Other reserves 0

Cash 12900 Retained earnings 132000

Profit before tax 130980

Total of current assets 514605 EQUITY/CAPITAL 872980

Working notes:

Ordinary Shares - £1 ES – 310,000

Add: 10% £1 PS – 300,000 = 610,000

N/c Assets: Plant & Machinery – 632,730

Retained Profit: Operating margin profit – 132,000

Add: Profit regulations – 18,000

Add: CY profit - 112,980 = 244,980

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£3000 is already identified as an unpaid commission that is not yet registered in ledger

accounts, but should be expressed in annual reports to show a true picture. Business must

then pass the corresponding journal entry:

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

These transactions will therefore be represented throughout the report of income by

applying the deferred revenue to just the budget of the compensation, whereas the remaining

committee would be expressed throughout the existing liabilities including the financial

statements performance.

It has even been stated that the items were shipped to consumers costing £ 980, transaction of

which would be paid later and as such it not been registered in ledger accounts, thus to show an

accurate representation, the corporation must pass the accompanying journal entry because it can

be as seen within financial statement:

Accrued debtor sales a/c …..dr 980

To sales Debtor 980

Appropriately, by incorporating accumulated sales debt collectors to just the sales

borrower account, such funds would now be expressed in the revenue statement, whereas

accumulated sales debtors would be represented throughout the current assets of that same

accounting records.

B. Why the statement of financial position balances.

The accounting theory of that double entries that states that certain expenses are reported

in two distinct documents through this they have exactly equal consequences, is accompanied by

the income statement as well as financial situation statement (Brown and Johnston, 2019). This

theory also assists in testing not when the reports are appropriate and registered properly. This

theory is however centred on the Balance Sheet but has the equation of

Assets = obligations (company) + Equity

In order to generate the overall output of the corporation under its own, 2 sections of such an

equation actually amount. The asset side reflects the overview of the resources shown in the

company, whereas the basis of financing is split down by the other aspect of assets and liabilities

about how this quality was obtained. As each aspect reflects market capitalisation as well as the

accounts, but should be expressed in annual reports to show a true picture. Business must

then pass the corresponding journal entry:

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

These transactions will therefore be represented throughout the report of income by

applying the deferred revenue to just the budget of the compensation, whereas the remaining

committee would be expressed throughout the existing liabilities including the financial

statements performance.

It has even been stated that the items were shipped to consumers costing £ 980, transaction of

which would be paid later and as such it not been registered in ledger accounts, thus to show an

accurate representation, the corporation must pass the accompanying journal entry because it can

be as seen within financial statement:

Accrued debtor sales a/c …..dr 980

To sales Debtor 980

Appropriately, by incorporating accumulated sales debt collectors to just the sales

borrower account, such funds would now be expressed in the revenue statement, whereas

accumulated sales debtors would be represented throughout the current assets of that same

accounting records.

B. Why the statement of financial position balances.

The accounting theory of that double entries that states that certain expenses are reported

in two distinct documents through this they have exactly equal consequences, is accompanied by

the income statement as well as financial situation statement (Brown and Johnston, 2019). This

theory also assists in testing not when the reports are appropriate and registered properly. This

theory is however centred on the Balance Sheet but has the equation of

Assets = obligations (company) + Equity

In order to generate the overall output of the corporation under its own, 2 sections of such an

equation actually amount. The asset side reflects the overview of the resources shown in the

company, whereas the basis of financing is split down by the other aspect of assets and liabilities

about how this quality was obtained. As each aspect reflects market capitalisation as well as the

other sides is the provider of that financing, they should be equivalent in order to make sure that

certain cash products are accurately registered.

Question 2

A. Ratio Analysis

It is really a statistical approach that allows a business to learn from either the information

stored in its annual reports regarding its profitability, productivity, sustainability, etc. (Samonas,

2015). Thus the, in many other words, it is indeed a statistical study of the economic stability of

a corporation. Various types of proportions are listed below:

Liquidity Ratios

Current Ratio

These proportion are being used to determine the capacity of a firm to paying everything off

short-term obligations from company-submitted capital (Tsadira-Pocha, 2020). It encompasses:

Current Ratio-The willingness of a business to make off all its near-term obligations including its

liquid liability is calculated. The greater the percentage, the stronger their capacity to pay debts.

Formula = Current Assets/Current Liabilities

2019 2018

Current Assets 2303 2355

Current Liabilities 2511 3046

Current Ratio 0.917 0.773

Chocco Plc's recent number is small for both 2018 and 2019, which isn't really a positive

indication, as it means that the current assets of the firm will not be enough to compensate

current liabilities if appropriate. Nevertheless, the positive sign for industry would be that the

proportion has risen in 2019 over 2018.

Acid Test Ratio: Formerly it is recognized as fast ratio, as it investigates the capacities of

the most available business assets. It also removes from existing assets the warehouse and

accrued instruments.

Formula: = (Current Assets – Inventory – Prepaid Instruments) / Current Liabilities

2019 2018

Quick Assets 1595 1696

Current Liabilities 2511 3046

certain cash products are accurately registered.

Question 2

A. Ratio Analysis

It is really a statistical approach that allows a business to learn from either the information

stored in its annual reports regarding its profitability, productivity, sustainability, etc. (Samonas,

2015). Thus the, in many other words, it is indeed a statistical study of the economic stability of

a corporation. Various types of proportions are listed below:

Liquidity Ratios

Current Ratio

These proportion are being used to determine the capacity of a firm to paying everything off

short-term obligations from company-submitted capital (Tsadira-Pocha, 2020). It encompasses:

Current Ratio-The willingness of a business to make off all its near-term obligations including its

liquid liability is calculated. The greater the percentage, the stronger their capacity to pay debts.

Formula = Current Assets/Current Liabilities

2019 2018

Current Assets 2303 2355

Current Liabilities 2511 3046

Current Ratio 0.917 0.773

Chocco Plc's recent number is small for both 2018 and 2019, which isn't really a positive

indication, as it means that the current assets of the firm will not be enough to compensate

current liabilities if appropriate. Nevertheless, the positive sign for industry would be that the

proportion has risen in 2019 over 2018.

Acid Test Ratio: Formerly it is recognized as fast ratio, as it investigates the capacities of

the most available business assets. It also removes from existing assets the warehouse and

accrued instruments.

Formula: = (Current Assets – Inventory – Prepaid Instruments) / Current Liabilities

2019 2018

Quick Assets 1595 1696

Current Liabilities 2511 3046

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick Ratio 0.635 0.557

Chocco Plc's acid test Ratio is lower than 1 that is not really a positive measure, since it

suggests that in the event of uncertainties, the company's quick reserves are insufficient to

compensate existing liabilities. In 2019, however, the proportion changed from 2018

onwards.

Solvency Ratios

These are also recognized as leverage proportion as well. These are being used to assess

the company's chances of long-term adequacy and willingness to fund itself (Brown and et.al.,

2016). It encompasses:

Debt-to-equity ratio: This ratio calculates the equity-funded amount of debt. The smaller the

proportion it is consider to be more effective

Formula: Total debt/total equity

2019 2018

Total liabilities 6828 7175

Total equity 3088 2912

Debt-to-equity Ratio 2.21 2.46

Greater leverage to equity ratios are not deemed well for the firm, as reported earlier. Chocco

Plc's debt equity ratio reveals the leverage is much more than double the corporation's

capital, which raises the risk of failure when the capital is insufficient to fund obligations if

appropriate.

Debt-to-asset Ratio

This proportion is used to analyses the debt of the business by calculating the amount of

loans funded by the company's assets (Rachlin, 2019).

Formula: Total debt/Total assets

2019 2018

Total liabilities 6828 7175

Total assets 9736 10087

Debt-to-asset Ratio 0.701 0.711

The amount of debt to assets greater than 1 is not deemed to be safe. Chocco plc's debt-to

- asset proportion is much less than, that means the borrowing is also not substantially financed

and against firm net income. In comparison, in 2019, the ratio increased from 2018.

Chocco Plc's acid test Ratio is lower than 1 that is not really a positive measure, since it

suggests that in the event of uncertainties, the company's quick reserves are insufficient to

compensate existing liabilities. In 2019, however, the proportion changed from 2018

onwards.

Solvency Ratios

These are also recognized as leverage proportion as well. These are being used to assess

the company's chances of long-term adequacy and willingness to fund itself (Brown and et.al.,

2016). It encompasses:

Debt-to-equity ratio: This ratio calculates the equity-funded amount of debt. The smaller the

proportion it is consider to be more effective

Formula: Total debt/total equity

2019 2018

Total liabilities 6828 7175

Total equity 3088 2912

Debt-to-equity Ratio 2.21 2.46

Greater leverage to equity ratios are not deemed well for the firm, as reported earlier. Chocco

Plc's debt equity ratio reveals the leverage is much more than double the corporation's

capital, which raises the risk of failure when the capital is insufficient to fund obligations if

appropriate.

Debt-to-asset Ratio

This proportion is used to analyses the debt of the business by calculating the amount of

loans funded by the company's assets (Rachlin, 2019).

Formula: Total debt/Total assets

2019 2018

Total liabilities 6828 7175

Total assets 9736 10087

Debt-to-asset Ratio 0.701 0.711

The amount of debt to assets greater than 1 is not deemed to be safe. Chocco plc's debt-to

- asset proportion is much less than, that means the borrowing is also not substantially financed

and against firm net income. In comparison, in 2019, the ratio increased from 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitability Ratios

Such ratio is used to determine a corporation's potential to earn earnings in comparison to

its sales as well as other company activities (Ehrhardt and Brigham, 2016). It encompasses:

ROA- Both internally and externally creditors are using this calculation to assess a company's

performance in managing working capital.

Formula: Net income / Total Assets

2019 2018

Net Income 431 366

Total assets 9736 10087

Return on Asset 4.43% 3.63%

The greater the ROA the more effective the capital are perceived to be. Chocco Plc's

return on assets has increased over the last year, which would be a good thing also for firm. The

proportion is indeed not large enough, however, as well as the organisation has to continue to

make attempts to increase its profitability so that it would have higher asset returns.

Efficiency Ratios

These measures are often referred to as operation measures that are used to measure a company's

ability to leverage its financial assets to increase its earnings (Chandra, 2017). It encompasses:

Asset turnover ratio: This is used to assess the frequency with which a firm can use its properties

to increase its profits or income.

Formula: Total sales / Average Assets

2019 2018

Total sales 6378 6441

Average Assets = (Opening asset +

closing asset)/2

(10087+9736) / 2 =

9911.5

No amount of

opening asset

provided

Asset turnover ratio .643

The greater the percentage, the more powerful the organisation is. Chocco Plc's inventory

turnover proportion for 2019 is 0.643, whereas the 2018 ratio cannot be calculated because the

opening valuation of resources for 2018 was also not given. Consequently, comparison study

cannot be calculated for the 2 year measure.

Coverage Ratios

Such ratio is used to determine a corporation's potential to earn earnings in comparison to

its sales as well as other company activities (Ehrhardt and Brigham, 2016). It encompasses:

ROA- Both internally and externally creditors are using this calculation to assess a company's

performance in managing working capital.

Formula: Net income / Total Assets

2019 2018

Net Income 431 366

Total assets 9736 10087

Return on Asset 4.43% 3.63%

The greater the ROA the more effective the capital are perceived to be. Chocco Plc's

return on assets has increased over the last year, which would be a good thing also for firm. The

proportion is indeed not large enough, however, as well as the organisation has to continue to

make attempts to increase its profitability so that it would have higher asset returns.

Efficiency Ratios

These measures are often referred to as operation measures that are used to measure a company's

ability to leverage its financial assets to increase its earnings (Chandra, 2017). It encompasses:

Asset turnover ratio: This is used to assess the frequency with which a firm can use its properties

to increase its profits or income.

Formula: Total sales / Average Assets

2019 2018

Total sales 6378 6441

Average Assets = (Opening asset +

closing asset)/2

(10087+9736) / 2 =

9911.5

No amount of

opening asset

provided

Asset turnover ratio .643

The greater the percentage, the more powerful the organisation is. Chocco Plc's inventory

turnover proportion for 2019 is 0.643, whereas the 2018 ratio cannot be calculated because the

opening valuation of resources for 2018 was also not given. Consequently, comparison study

cannot be calculated for the 2 year measure.

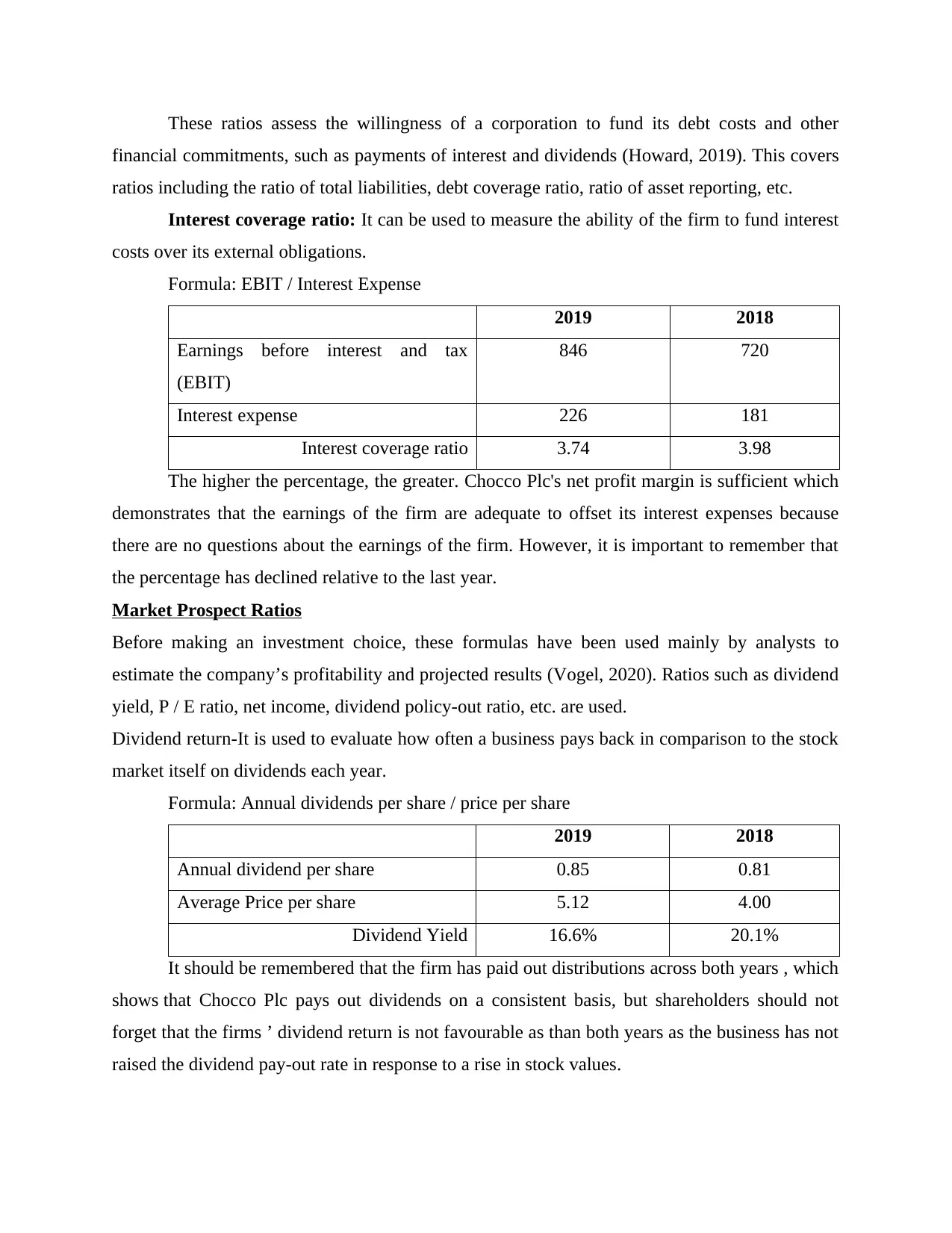

Coverage Ratios

These ratios assess the willingness of a corporation to fund its debt costs and other

financial commitments, such as payments of interest and dividends (Howard, 2019). This covers

ratios including the ratio of total liabilities, debt coverage ratio, ratio of asset reporting, etc.

Interest coverage ratio: It can be used to measure the ability of the firm to fund interest

costs over its external obligations.

Formula: EBIT / Interest Expense

2019 2018

Earnings before interest and tax

(EBIT)

846 720

Interest expense 226 181

Interest coverage ratio 3.74 3.98

The higher the percentage, the greater. Chocco Plc's net profit margin is sufficient which

demonstrates that the earnings of the firm are adequate to offset its interest expenses because

there are no questions about the earnings of the firm. However, it is important to remember that

the percentage has declined relative to the last year.

Market Prospect Ratios

Before making an investment choice, these formulas have been used mainly by analysts to

estimate the company’s profitability and projected results (Vogel, 2020). Ratios such as dividend

yield, P / E ratio, net income, dividend policy-out ratio, etc. are used.

Dividend return-It is used to evaluate how often a business pays back in comparison to the stock

market itself on dividends each year.

Formula: Annual dividends per share / price per share

2019 2018

Annual dividend per share 0.85 0.81

Average Price per share 5.12 4.00

Dividend Yield 16.6% 20.1%

It should be remembered that the firm has paid out distributions across both years , which

shows that Chocco Plc pays out dividends on a consistent basis, but shareholders should not

forget that the firms ’ dividend return is not favourable as than both years as the business has not

raised the dividend pay-out rate in response to a rise in stock values.

financial commitments, such as payments of interest and dividends (Howard, 2019). This covers

ratios including the ratio of total liabilities, debt coverage ratio, ratio of asset reporting, etc.

Interest coverage ratio: It can be used to measure the ability of the firm to fund interest

costs over its external obligations.

Formula: EBIT / Interest Expense

2019 2018

Earnings before interest and tax

(EBIT)

846 720

Interest expense 226 181

Interest coverage ratio 3.74 3.98

The higher the percentage, the greater. Chocco Plc's net profit margin is sufficient which

demonstrates that the earnings of the firm are adequate to offset its interest expenses because

there are no questions about the earnings of the firm. However, it is important to remember that

the percentage has declined relative to the last year.

Market Prospect Ratios

Before making an investment choice, these formulas have been used mainly by analysts to

estimate the company’s profitability and projected results (Vogel, 2020). Ratios such as dividend

yield, P / E ratio, net income, dividend policy-out ratio, etc. are used.

Dividend return-It is used to evaluate how often a business pays back in comparison to the stock

market itself on dividends each year.

Formula: Annual dividends per share / price per share

2019 2018

Annual dividend per share 0.85 0.81

Average Price per share 5.12 4.00

Dividend Yield 16.6% 20.1%

It should be remembered that the firm has paid out distributions across both years , which

shows that Chocco Plc pays out dividends on a consistent basis, but shareholders should not

forget that the firms ’ dividend return is not favourable as than both years as the business has not

raised the dividend pay-out rate in response to a rise in stock values.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B. Comment on financial performance and position of Chocco Plc.

Financial performance analysis as well as financial ratios evaluation are the most powerful

methods for assessing a firm's earnings wellbeing (Warren and Farmer, 2020). Then to allow

correlation from both different stakeholders are percentages calculated from financial reports.

This can be calculated by the financial reports which the net revenue have grown through 2018

to 2019, such that costs have risen, but the financial profits have decreased. However, there has

also been a drastic decrease in relatively existing liabilities, but just not liabilities of the

company. This can be observed from the above-mentioned ratio review that the business has

never had adequate profitability ratio, debt-to - equity proportions, asset-to-asset ratios, etc.,

whereas its debt-to - asset percentages or interest-to-asset ratios are somewhat sufficient.

However, the company's average success is not sufficient and shareholders are strongly

recommended to take risks in financial investment strategy and to think very carefully when

participating in it, since both of these assessments can only be the consequence of side to side

that exists when working in a lively market setting. Chocco Plc's liquidity accounts often need to

be contrasted with the business average, and rivals need to understand enough about its current

value, that are helpful for assessing the performance of a business for shareholders.

Financial performance analysis as well as financial ratios evaluation are the most powerful

methods for assessing a firm's earnings wellbeing (Warren and Farmer, 2020). Then to allow

correlation from both different stakeholders are percentages calculated from financial reports.

This can be calculated by the financial reports which the net revenue have grown through 2018

to 2019, such that costs have risen, but the financial profits have decreased. However, there has

also been a drastic decrease in relatively existing liabilities, but just not liabilities of the

company. This can be observed from the above-mentioned ratio review that the business has

never had adequate profitability ratio, debt-to - equity proportions, asset-to-asset ratios, etc.,

whereas its debt-to - asset percentages or interest-to-asset ratios are somewhat sufficient.

However, the company's average success is not sufficient and shareholders are strongly

recommended to take risks in financial investment strategy and to think very carefully when

participating in it, since both of these assessments can only be the consequence of side to side

that exists when working in a lively market setting. Chocco Plc's liquidity accounts often need to

be contrasted with the business average, and rivals need to understand enough about its current

value, that are helpful for assessing the performance of a business for shareholders.

1 out of 10