Accounting Fundamentals Assessment 1: Income Statement and Ratios

VerifiedAdded on 2023/01/05

|12

|1158

|96

Homework Assignment

AI Summary

This assignment solution for Accounting Fundamentals covers the preparation of financial statements, including the income statement and balance sheet, and their interpretation through ratio analysis. Question 1 presents the income statement and balance sheet for a company, followed by an explanation of why the statement of financial position balances. Question 2 focuses on ratio analysis, including profitability, efficiency, liquidity, financing, and investment ratios, for Chocco plc for the years 2018 and 2019. The assignment provides detailed calculations and comments on the financial performance and position of the company based on the analyzed ratios. The conclusion emphasizes the importance of accounting in recording transactions and preparing financial reports. References to relevant accounting literature are also provided.

ACCOUNTING FUNDAMENTALS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1....................................................................................................................................3

Question 2:...................................................................................................................................5

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1....................................................................................................................................3

Question 2:...................................................................................................................................5

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Accounting can be described as a mechanism by which financial transactions are reported in a

way that can lead to the preparing of financial reports (Kranacher and Riley, 2019). The study is

based on two different activities in which details about the planning of the income statement and

balance sheet is contained in the first task. Although task two is focused on interpretation of the

findings of the given organisation by way of ratio analysis.

MAIN BODY

Question 1

(a)Income statement and balance sheet:

Income statement:

Income statement

For the year ended on 31st December 2018

Particulars Amount(£)

Sales 826,650.00

Add: Goods sold on 31st 980.00 827,630.00

Cost of goods sold -578,650.00

Gross Profit 248,980.00

Less: Expenses

Administrative expenses 30,000.00

Accounting can be described as a mechanism by which financial transactions are reported in a

way that can lead to the preparing of financial reports (Kranacher and Riley, 2019). The study is

based on two different activities in which details about the planning of the income statement and

balance sheet is contained in the first task. Although task two is focused on interpretation of the

findings of the given organisation by way of ratio analysis.

MAIN BODY

Question 1

(a)Income statement and balance sheet:

Income statement:

Income statement

For the year ended on 31st December 2018

Particulars Amount(£)

Sales 826,650.00

Add: Goods sold on 31st 980.00 827,630.00

Cost of goods sold -578,650.00

Gross Profit 248,980.00

Less: Expenses

Administrative expenses 30,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

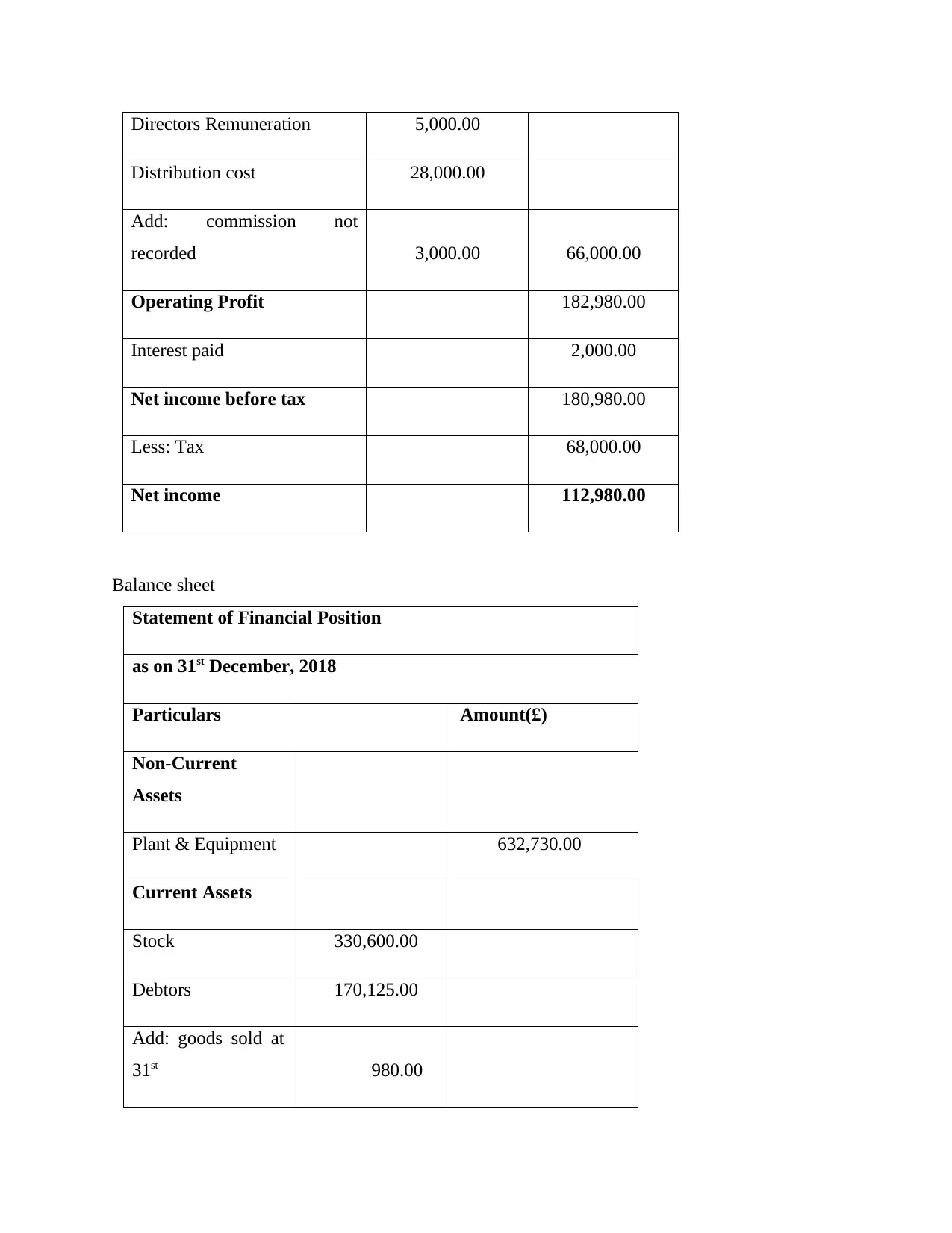

Directors Remuneration 5,000.00

Distribution cost 28,000.00

Add: commission not

recorded 3,000.00 66,000.00

Operating Profit 182,980.00

Interest paid 2,000.00

Net income before tax 180,980.00

Less: Tax 68,000.00

Net income 112,980.00

Balance sheet

Statement of Financial Position

as on 31st December, 2018

Particulars Amount(£)

Non-Current

Assets

Plant & Equipment 632,730.00

Current Assets

Stock 330,600.00

Debtors 170,125.00

Add: goods sold at

31st 980.00

Distribution cost 28,000.00

Add: commission not

recorded 3,000.00 66,000.00

Operating Profit 182,980.00

Interest paid 2,000.00

Net income before tax 180,980.00

Less: Tax 68,000.00

Net income 112,980.00

Balance sheet

Statement of Financial Position

as on 31st December, 2018

Particulars Amount(£)

Non-Current

Assets

Plant & Equipment 632,730.00

Current Assets

Stock 330,600.00

Debtors 170,125.00

Add: goods sold at

31st 980.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

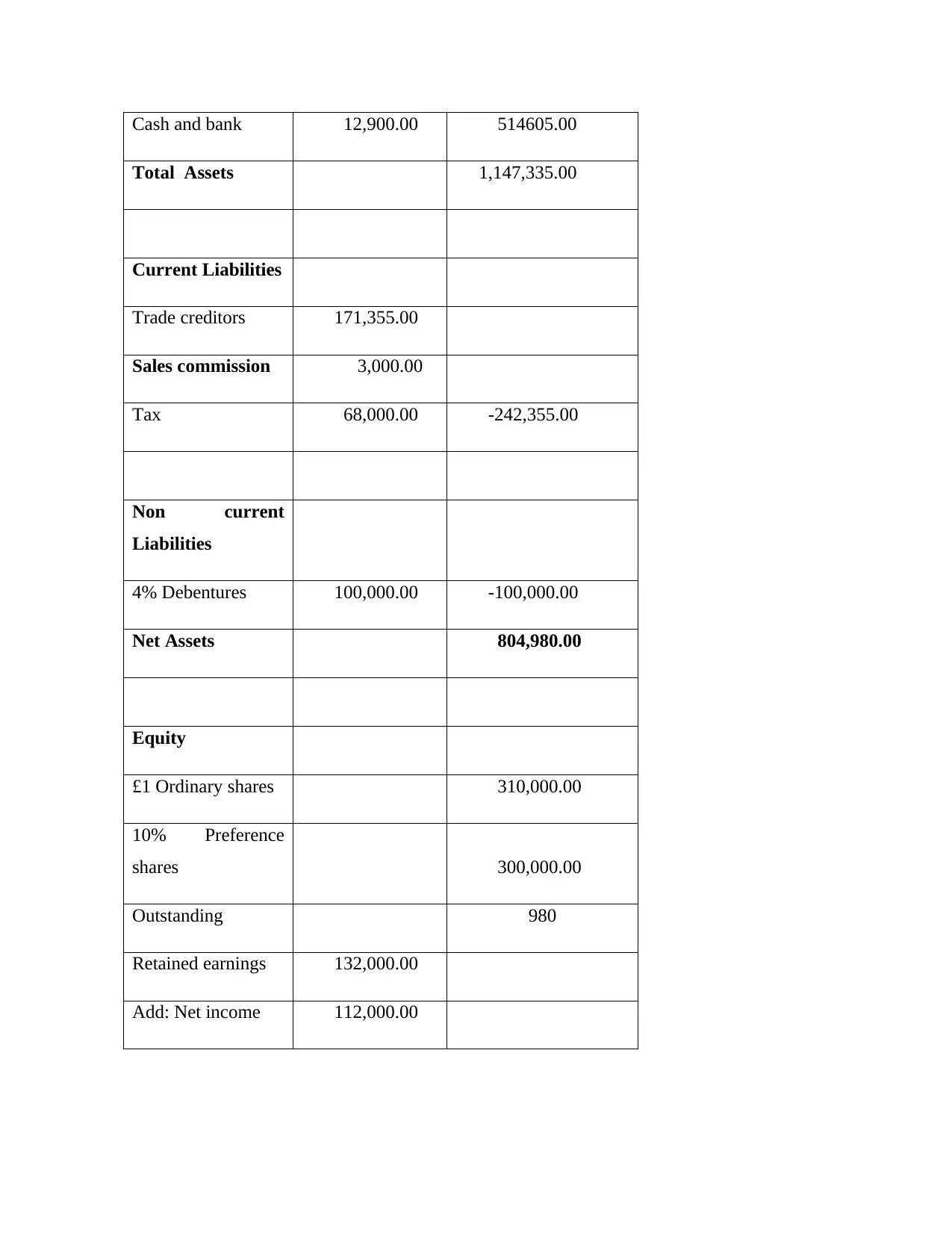

Cash and bank 12,900.00 514605.00

Total Assets 1,147,335.00

Current Liabilities

Trade creditors 171,355.00

Sales commission 3,000.00

Tax 68,000.00 -242,355.00

Non current

Liabilities

4% Debentures 100,000.00 -100,000.00

Net Assets 804,980.00

Equity

£1 Ordinary shares 310,000.00

10% Preference

shares 300,000.00

Outstanding 980

Retained earnings 132,000.00

Add: Net income 112,000.00

Total Assets 1,147,335.00

Current Liabilities

Trade creditors 171,355.00

Sales commission 3,000.00

Tax 68,000.00 -242,355.00

Non current

Liabilities

4% Debentures 100,000.00 -100,000.00

Net Assets 804,980.00

Equity

£1 Ordinary shares 310,000.00

10% Preference

shares 300,000.00

Outstanding 980

Retained earnings 132,000.00

Add: Net income 112,000.00

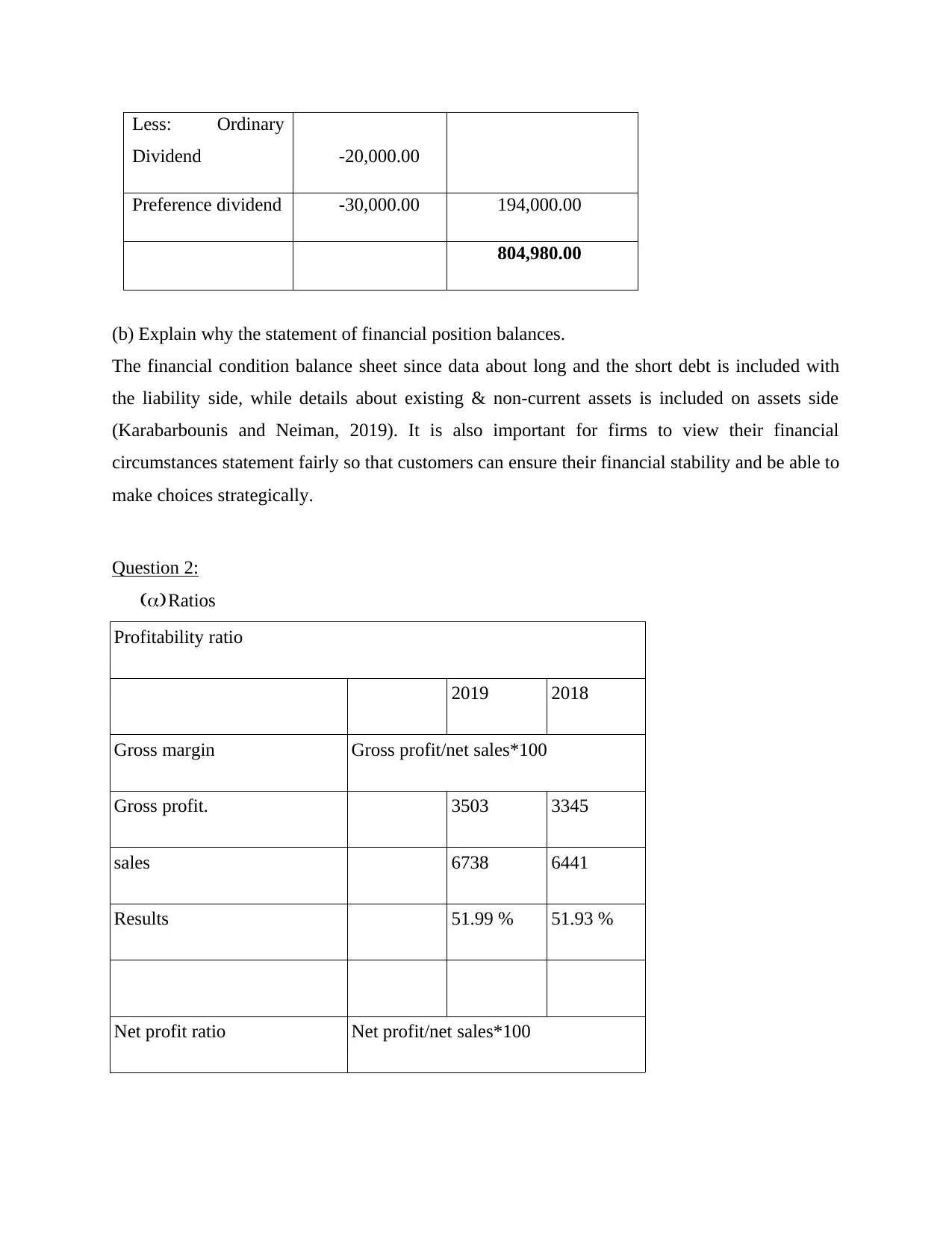

Less: Ordinary

Dividend -20,000.00

Preference dividend -30,000.00 194,000.00

804,980.00

(b) Explain why the statement of financial position balances.

The financial condition balance sheet since data about long and the short debt is included with

the liability side, while details about existing & non-current assets is included on assets side

(Karabarbounis and Neiman, 2019). It is also important for firms to view their financial

circumstances statement fairly so that customers can ensure their financial stability and be able to

make choices strategically.

Question 2:

(a)Ratios

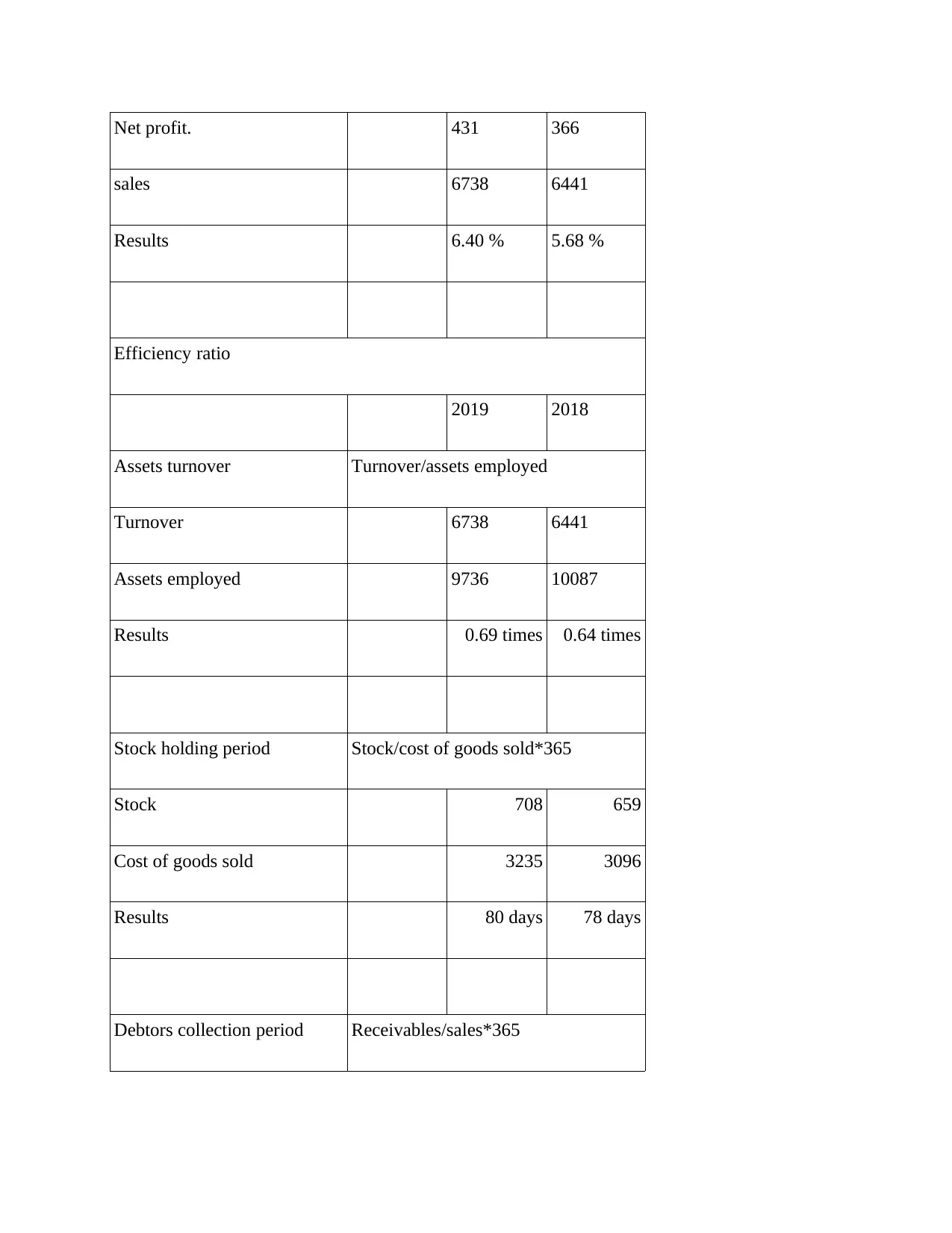

Profitability ratio

2019 2018

Gross margin Gross profit/net sales*100

Gross profit. 3503 3345

sales 6738 6441

Results 51.99 % 51.93 %

Net profit ratio Net profit/net sales*100

Dividend -20,000.00

Preference dividend -30,000.00 194,000.00

804,980.00

(b) Explain why the statement of financial position balances.

The financial condition balance sheet since data about long and the short debt is included with

the liability side, while details about existing & non-current assets is included on assets side

(Karabarbounis and Neiman, 2019). It is also important for firms to view their financial

circumstances statement fairly so that customers can ensure their financial stability and be able to

make choices strategically.

Question 2:

(a)Ratios

Profitability ratio

2019 2018

Gross margin Gross profit/net sales*100

Gross profit. 3503 3345

sales 6738 6441

Results 51.99 % 51.93 %

Net profit ratio Net profit/net sales*100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit. 431 366

sales 6738 6441

Results 6.40 % 5.68 %

Efficiency ratio

2019 2018

Assets turnover Turnover/assets employed

Turnover 6738 6441

Assets employed 9736 10087

Results 0.69 times 0.64 times

Stock holding period Stock/cost of goods sold*365

Stock 708 659

Cost of goods sold 3235 3096

Results 80 days 78 days

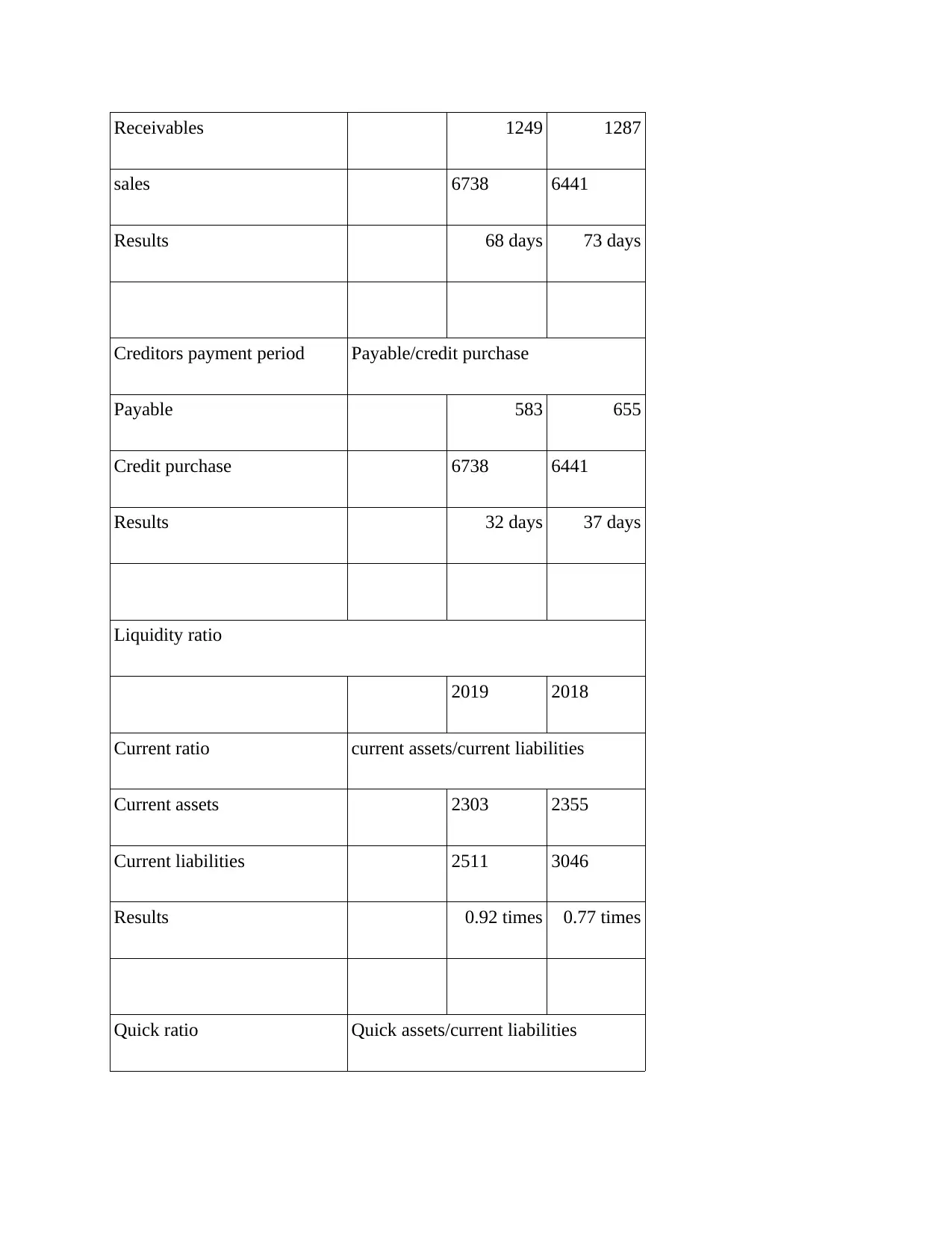

Debtors collection period Receivables/sales*365

sales 6738 6441

Results 6.40 % 5.68 %

Efficiency ratio

2019 2018

Assets turnover Turnover/assets employed

Turnover 6738 6441

Assets employed 9736 10087

Results 0.69 times 0.64 times

Stock holding period Stock/cost of goods sold*365

Stock 708 659

Cost of goods sold 3235 3096

Results 80 days 78 days

Debtors collection period Receivables/sales*365

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receivables 1249 1287

sales 6738 6441

Results 68 days 73 days

Creditors payment period Payable/credit purchase

Payable 583 655

Credit purchase 6738 6441

Results 32 days 37 days

Liquidity ratio

2019 2018

Current ratio current assets/current liabilities

Current assets 2303 2355

Current liabilities 2511 3046

Results 0.92 times 0.77 times

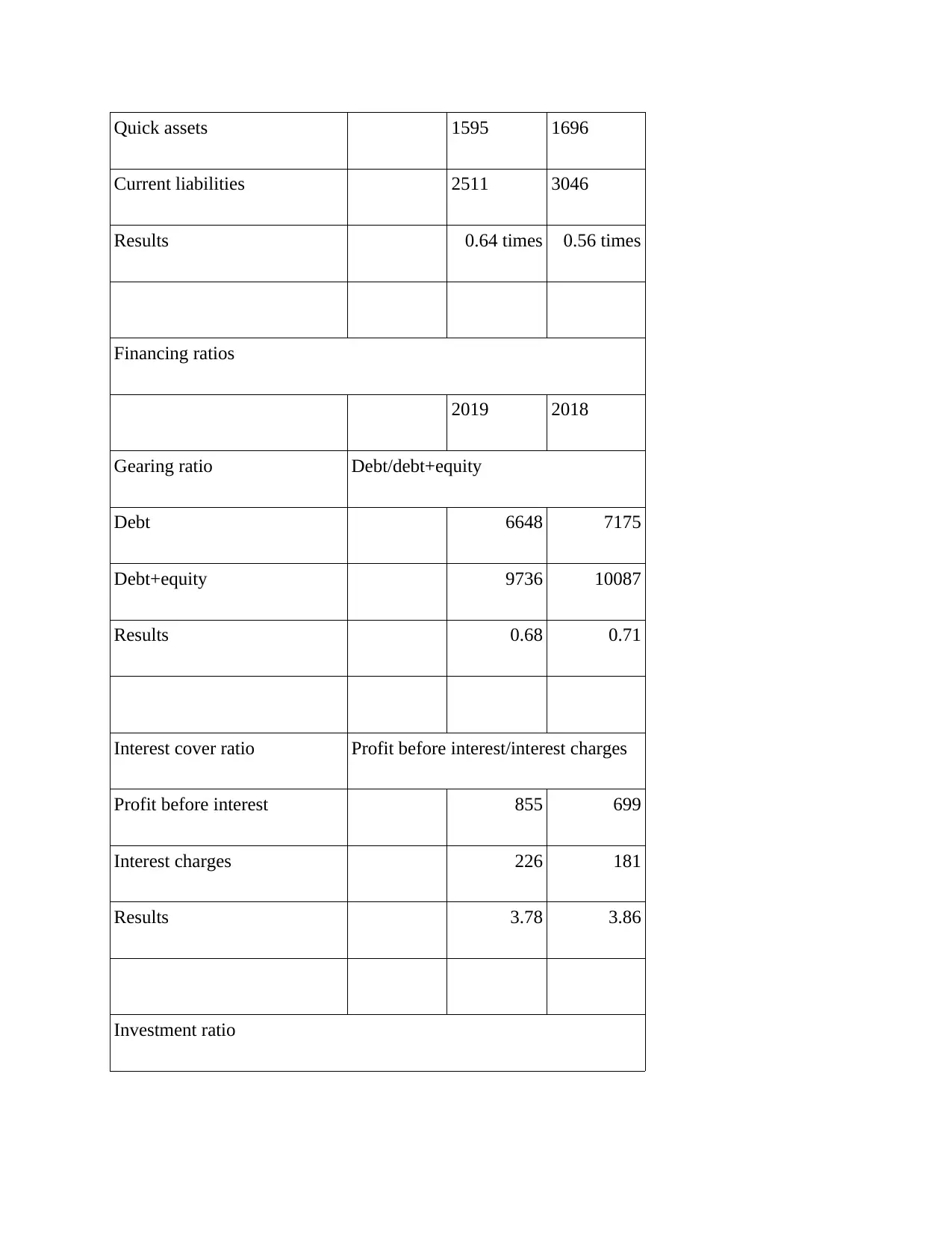

Quick ratio Quick assets/current liabilities

sales 6738 6441

Results 68 days 73 days

Creditors payment period Payable/credit purchase

Payable 583 655

Credit purchase 6738 6441

Results 32 days 37 days

Liquidity ratio

2019 2018

Current ratio current assets/current liabilities

Current assets 2303 2355

Current liabilities 2511 3046

Results 0.92 times 0.77 times

Quick ratio Quick assets/current liabilities

Quick assets 1595 1696

Current liabilities 2511 3046

Results 0.64 times 0.56 times

Financing ratios

2019 2018

Gearing ratio Debt/debt+equity

Debt 6648 7175

Debt+equity 9736 10087

Results 0.68 0.71

Interest cover ratio Profit before interest/interest charges

Profit before interest 855 699

Interest charges 226 181

Results 3.78 3.86

Investment ratio

Current liabilities 2511 3046

Results 0.64 times 0.56 times

Financing ratios

2019 2018

Gearing ratio Debt/debt+equity

Debt 6648 7175

Debt+equity 9736 10087

Results 0.68 0.71

Interest cover ratio Profit before interest/interest charges

Profit before interest 855 699

Interest charges 226 181

Results 3.78 3.86

Investment ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

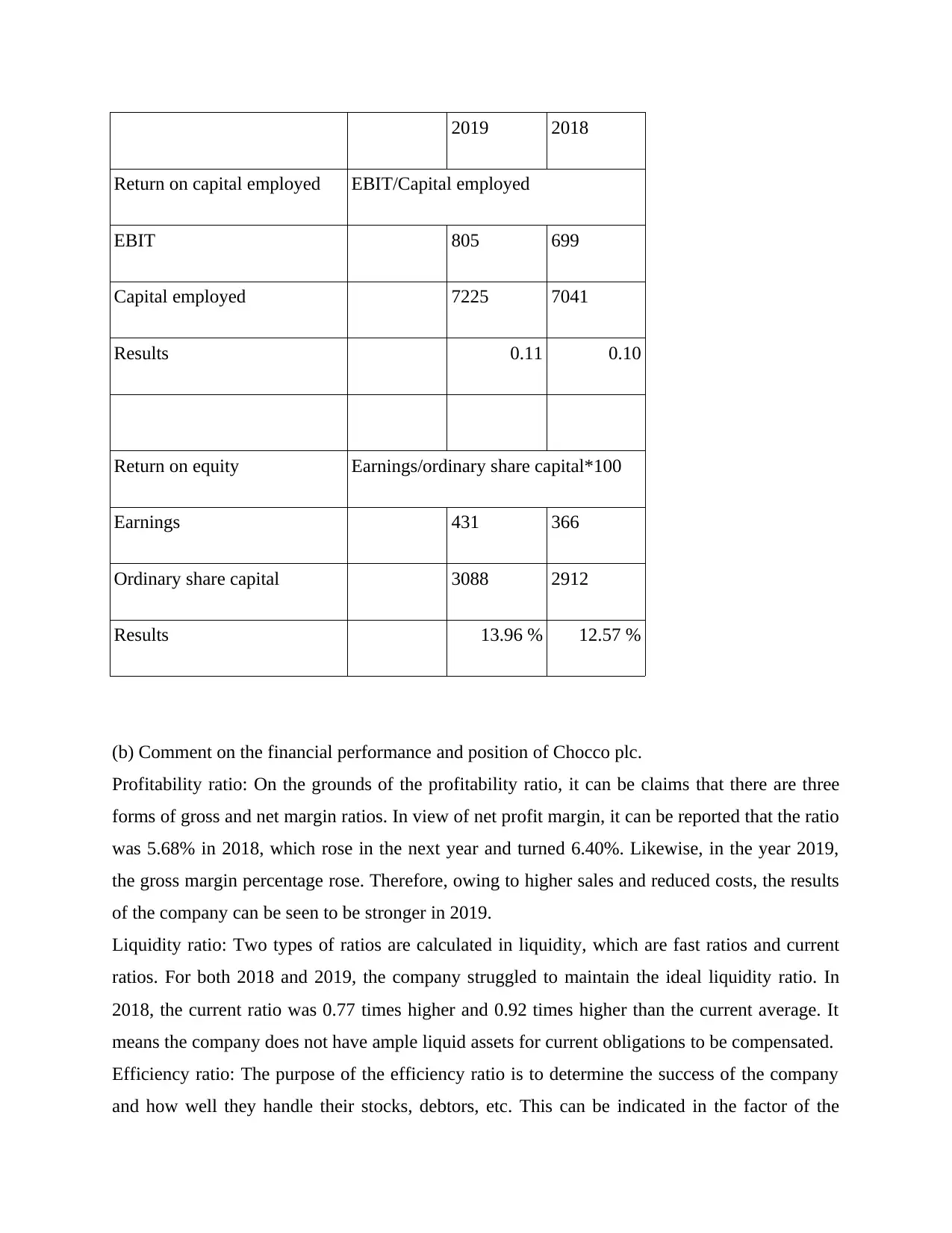

2019 2018

Return on capital employed EBIT/Capital employed

EBIT 805 699

Capital employed 7225 7041

Results 0.11 0.10

Return on equity Earnings/ordinary share capital*100

Earnings 431 366

Ordinary share capital 3088 2912

Results 13.96 % 12.57 %

(b) Comment on the financial performance and position of Chocco plc.

Profitability ratio: On the grounds of the profitability ratio, it can be claims that there are three

forms of gross and net margin ratios. In view of net profit margin, it can be reported that the ratio

was 5.68% in 2018, which rose in the next year and turned 6.40%. Likewise, in the year 2019,

the gross margin percentage rose. Therefore, owing to higher sales and reduced costs, the results

of the company can be seen to be stronger in 2019.

Liquidity ratio: Two types of ratios are calculated in liquidity, which are fast ratios and current

ratios. For both 2018 and 2019, the company struggled to maintain the ideal liquidity ratio. In

2018, the current ratio was 0.77 times higher and 0.92 times higher than the current average. It

means the company does not have ample liquid assets for current obligations to be compensated.

Efficiency ratio: The purpose of the efficiency ratio is to determine the success of the company

and how well they handle their stocks, debtors, etc. This can be indicated in the factor of the

Return on capital employed EBIT/Capital employed

EBIT 805 699

Capital employed 7225 7041

Results 0.11 0.10

Return on equity Earnings/ordinary share capital*100

Earnings 431 366

Ordinary share capital 3088 2912

Results 13.96 % 12.57 %

(b) Comment on the financial performance and position of Chocco plc.

Profitability ratio: On the grounds of the profitability ratio, it can be claims that there are three

forms of gross and net margin ratios. In view of net profit margin, it can be reported that the ratio

was 5.68% in 2018, which rose in the next year and turned 6.40%. Likewise, in the year 2019,

the gross margin percentage rose. Therefore, owing to higher sales and reduced costs, the results

of the company can be seen to be stronger in 2019.

Liquidity ratio: Two types of ratios are calculated in liquidity, which are fast ratios and current

ratios. For both 2018 and 2019, the company struggled to maintain the ideal liquidity ratio. In

2018, the current ratio was 0.77 times higher and 0.92 times higher than the current average. It

means the company does not have ample liquid assets for current obligations to be compensated.

Efficiency ratio: The purpose of the efficiency ratio is to determine the success of the company

and how well they handle their stocks, debtors, etc. This can be indicated in the factor of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

creditor turnover ratio that the efficiency of the firm increased as the amount of days to pay

creditors reduced. In comparison, the debtors' turnover ratio has fell by 5 days in 2019. These

ratios indicate that the organisation is more able to handle its performance in 2019 relative to

2018.

Investment ratio: Various categories of ratios are calculated under the expenditure ratio, namely

return on working capital and return on earnings. The output in both ratios is less than average,

since the return on the resources invested for both years is too poor. In 2019, the return on equity

is rising, which indicates that the company is able to produce higher profits this year.

Financing ratio: In terms of the gearing ratio, it may be reported that it is under one and this

indicates that the firm is unable to efficiently handle its debts and equity. In 2019, the interest

coverage level is still smaller, which would be an indicator of the company's inadequate growth

in the competitive year, which has to be changed by increasing equity volume.

CONCLUSION

On the basis of above project report this can be concluded that accounting plays a key role in

order to record different kinds of transactions in an effective manner. This is so because by help

of different kinds of accounting rules and regulations, it becomes easier for managers to prepare

financial reports. The report concludes that given company's performance is better in year 2019

as compared to year 2018.

creditors reduced. In comparison, the debtors' turnover ratio has fell by 5 days in 2019. These

ratios indicate that the organisation is more able to handle its performance in 2019 relative to

2018.

Investment ratio: Various categories of ratios are calculated under the expenditure ratio, namely

return on working capital and return on earnings. The output in both ratios is less than average,

since the return on the resources invested for both years is too poor. In 2019, the return on equity

is rising, which indicates that the company is able to produce higher profits this year.

Financing ratio: In terms of the gearing ratio, it may be reported that it is under one and this

indicates that the firm is unable to efficiently handle its debts and equity. In 2019, the interest

coverage level is still smaller, which would be an indicator of the company's inadequate growth

in the competitive year, which has to be changed by increasing equity volume.

CONCLUSION

On the basis of above project report this can be concluded that accounting plays a key role in

order to record different kinds of transactions in an effective manner. This is so because by help

of different kinds of accounting rules and regulations, it becomes easier for managers to prepare

financial reports. The report concludes that given company's performance is better in year 2019

as compared to year 2018.

REFERENCES

Kranacher, M.J. and Riley, R., 2019. Forensic accounting and fraud examination. John Wiley &

Sons.

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual, 33(1), pp.167-228.

Kranacher, M.J. and Riley, R., 2019. Forensic accounting and fraud examination. John Wiley &

Sons.

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual, 33(1), pp.167-228.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12