Accounting Fundamentals Assessment 1

VerifiedAdded on 2023/06/18

|10

|2194

|446

AI Summary

This article discusses the statement of profit and loss statement and financial position, balance sheet, and ratio analysis of Chocco Plc. It explains the importance of balancing the statement of financial position and provides a detailed analysis of various ratios. The article also includes references for further reading.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting fundamental

assessment 1

assessment 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

QUESTION 1...................................................................................................................................3

QUESTION 2 ..................................................................................................................................6

References .......................................................................................................................................9

QUESTION 1...................................................................................................................................3

QUESTION 2 ..................................................................................................................................6

References .......................................................................................................................................9

QUESTION 1

A). For Kedison Plc the statement of profit and loss statement and financial position is prepared

for the ended year 31st December 2019

Profit and loss statement

It is also known as income statement which reflects the financial description of the business

presenting the revenue and expenses of specific period. The business worth is revealed by

comprising all the financial activities. The profit and loss for the given period is determined and

helps in gaining the understanding of financial health business. The financial performance is

reported through the financial statements (Ahmed, A.S and et.al., 2019).

PARTICULARS AMOUNT

Revenue (amount of goods or service sold for period) 827630

Cost of sales 578650

Gross profit 248980

Distribution cost 31000

Administration cost 85000

Other income 0

Operating profit 135980

Income from investment 0

Finance cost 2000

Profit before tax 130980

Taxation 68000

A). For Kedison Plc the statement of profit and loss statement and financial position is prepared

for the ended year 31st December 2019

Profit and loss statement

It is also known as income statement which reflects the financial description of the business

presenting the revenue and expenses of specific period. The business worth is revealed by

comprising all the financial activities. The profit and loss for the given period is determined and

helps in gaining the understanding of financial health business. The financial performance is

reported through the financial statements (Ahmed, A.S and et.al., 2019).

PARTICULARS AMOUNT

Revenue (amount of goods or service sold for period) 827630

Cost of sales 578650

Gross profit 248980

Distribution cost 31000

Administration cost 85000

Other income 0

Operating profit 135980

Income from investment 0

Finance cost 2000

Profit before tax 130980

Taxation 68000

Net profit 62980

Financial position statement

The statement of the financial position is also called as balance sheet reporting assets, Liabilities

and equity of the organisation on the given date. The accounting information of the company is

recorded in the financial position at the end of the accounting period. The financial position

statement is used for financial analysis by making comparison of current assets and current

liabilities. It comprises the equation of balance sheet ASETS= liabilities + capital (Ardalan, K.,

2019).

ASSETS 1147335

LIABILITIES AND

STAKEHOLDERS

EQUITY 1147335

Non current assets Current liabilities 174355

Property, plant 632730 Non current liabilities 100000

Intangible assets 0

Total non current assets 632730 Liabilities. 274355

Current assets Share capital 310000

Stock 330600 Share premium 300000

Trade receivable 171105 Other reserves 0

Cash 12900 Retained earnings 132000

Financial position statement

The statement of the financial position is also called as balance sheet reporting assets, Liabilities

and equity of the organisation on the given date. The accounting information of the company is

recorded in the financial position at the end of the accounting period. The financial position

statement is used for financial analysis by making comparison of current assets and current

liabilities. It comprises the equation of balance sheet ASETS= liabilities + capital (Ardalan, K.,

2019).

ASSETS 1147335

LIABILITIES AND

STAKEHOLDERS

EQUITY 1147335

Non current assets Current liabilities 174355

Property, plant 632730 Non current liabilities 100000

Intangible assets 0

Total non current assets 632730 Liabilities. 274355

Current assets Share capital 310000

Stock 330600 Share premium 300000

Trade receivable 171105 Other reserves 0

Cash 12900 Retained earnings 132000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Profit before tax 130980

Total of current assets 514605 EQUITY/CAPITAL 872980

Working notes:

Ordinary Shares - £1 ES – 310,000

Add: 10% £1 PS – 300,000 = 610,000

N/c Assets: Plant & Machinery – 632,730

Retained Profit: Operating margin profit – 132,000

Add: Profit regulations – 18,000

Add: CY profit - 112,980 = 244,980

In the ledger account unpaid commission of £3000 is founded which was not recorded

and to show the accurate picture it is stated in annual reports. In regards to this the

business has passed the related journal entry.

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

Therefore, the transactions is represented in the income report which apply deferral revenue for

the compensation budget and remained financial statement performance is expressed throughout

the present liabilities by the committeem (Brunelli, S. and Di Carlo, E., 2020).

The items that were shipped to customers of amounting £ 980 is been stated in the transaction

which is to be paid in future and in ledger account the entry is not been recorded to reveal the

accurate representation. For such the journal entry is passed by the company to show the

transaction in financial statement.

Accrued debtor sales a/c Dr. 980

To sales Debtor 980

In the revenue statement the funds are expressed by incorporating accumulated sales of debtor

collectors to the sales of borrower account. In the same accounting records the accumulated

debtor sales is represented throu8ghiut the current assets.

B). Why does the statement of financial position balance?

The balance sheet of the company is defined as the summary of all corporate assets and

liabilities which display the left over amount after the sale of all assets and all debts are paid off.

Total of current assets 514605 EQUITY/CAPITAL 872980

Working notes:

Ordinary Shares - £1 ES – 310,000

Add: 10% £1 PS – 300,000 = 610,000

N/c Assets: Plant & Machinery – 632,730

Retained Profit: Operating margin profit – 132,000

Add: Profit regulations – 18,000

Add: CY profit - 112,980 = 244,980

In the ledger account unpaid commission of £3000 is founded which was not recorded

and to show the accurate picture it is stated in annual reports. In regards to this the

business has passed the related journal entry.

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

Therefore, the transactions is represented in the income report which apply deferral revenue for

the compensation budget and remained financial statement performance is expressed throughout

the present liabilities by the committeem (Brunelli, S. and Di Carlo, E., 2020).

The items that were shipped to customers of amounting £ 980 is been stated in the transaction

which is to be paid in future and in ledger account the entry is not been recorded to reveal the

accurate representation. For such the journal entry is passed by the company to show the

transaction in financial statement.

Accrued debtor sales a/c Dr. 980

To sales Debtor 980

In the revenue statement the funds are expressed by incorporating accumulated sales of debtor

collectors to the sales of borrower account. In the same accounting records the accumulated

debtor sales is represented throu8ghiut the current assets.

B). Why does the statement of financial position balance?

The balance sheet of the company is defined as the summary of all corporate assets and

liabilities which display the left over amount after the sale of all assets and all debts are paid off.

The balance sheet is also recognised as the statement of financial position which reveals the

picture of assets and liabilities or can be said as net worth (Guralnik, B. and Sohbati, R., 2019).

The accounting principle of double entry helps in balancing of the balance sheet which is

considered as major reason. In the two different accounts the accounting system records the

transactions and hence to ensure the consistency it also acts as check. The assets is the first

category in the balance sheet classified on three major categories such as current assets which is

expected to converted into cash within the year by representing all the values of the assets and

used for paying the current expenses and funding ongoing operations. The long term investments

are the non current assets of the company and last the fixed assets such as plant & equipment,

intangible assets like trademark. In the balance sheet the liabilities is classifies ad curren6t

liabilities which is short term liability are due within one year comprising of accounts payable ,

accrued expenses. Non current liabilities is also shown in balance sheet under the head of

liabilities which defines to long-term obligations and repayment is not within a year. In the

shareholder equity the company helps retained earnings for reinvestment and to pay the debts.

The retained earnings is not paid to the shareholder in form of dividend (Lee, C.M. and Watts,

E.M., 2021). The company net worth is represented by the shareholder equity and helps in

determining the financial status. In conducting fundamental analysis or computation of financial

ratios the balance sheet is used in other important financial statement of income and cash flow

statement. The balancing of the financial statement helps in understanding the company health

by correctly following double entry accounting process. The balancing of the balance helps the

stakeholders in understanding the liquidity position and performance of the company. The

company growth is determined by comparing the balance sheet of over the years. The ability of

the company is analysed to get the understanding of the project expansion and unexpected

expenses which requires the balancing of balance sheet. The statement of the financial position is

balanced to determine the risk and return and used to secure business loans,. The balancing of the

balance sheet helps in guiding the effective management decisions. The outsiders uses the

balance sheet to know the financial status to investors, stakeholders and lenders.

QUESTION 2

RATIO FORMULA 2020 2019

CALCULATI RESUL CALCULATI RESUL

picture of assets and liabilities or can be said as net worth (Guralnik, B. and Sohbati, R., 2019).

The accounting principle of double entry helps in balancing of the balance sheet which is

considered as major reason. In the two different accounts the accounting system records the

transactions and hence to ensure the consistency it also acts as check. The assets is the first

category in the balance sheet classified on three major categories such as current assets which is

expected to converted into cash within the year by representing all the values of the assets and

used for paying the current expenses and funding ongoing operations. The long term investments

are the non current assets of the company and last the fixed assets such as plant & equipment,

intangible assets like trademark. In the balance sheet the liabilities is classifies ad curren6t

liabilities which is short term liability are due within one year comprising of accounts payable ,

accrued expenses. Non current liabilities is also shown in balance sheet under the head of

liabilities which defines to long-term obligations and repayment is not within a year. In the

shareholder equity the company helps retained earnings for reinvestment and to pay the debts.

The retained earnings is not paid to the shareholder in form of dividend (Lee, C.M. and Watts,

E.M., 2021). The company net worth is represented by the shareholder equity and helps in

determining the financial status. In conducting fundamental analysis or computation of financial

ratios the balance sheet is used in other important financial statement of income and cash flow

statement. The balancing of the financial statement helps in understanding the company health

by correctly following double entry accounting process. The balancing of the balance helps the

stakeholders in understanding the liquidity position and performance of the company. The

company growth is determined by comparing the balance sheet of over the years. The ability of

the company is analysed to get the understanding of the project expansion and unexpected

expenses which requires the balancing of balance sheet. The statement of the financial position is

balanced to determine the risk and return and used to secure business loans,. The balancing of the

balance sheet helps in guiding the effective management decisions. The outsiders uses the

balance sheet to know the financial status to investors, stakeholders and lenders.

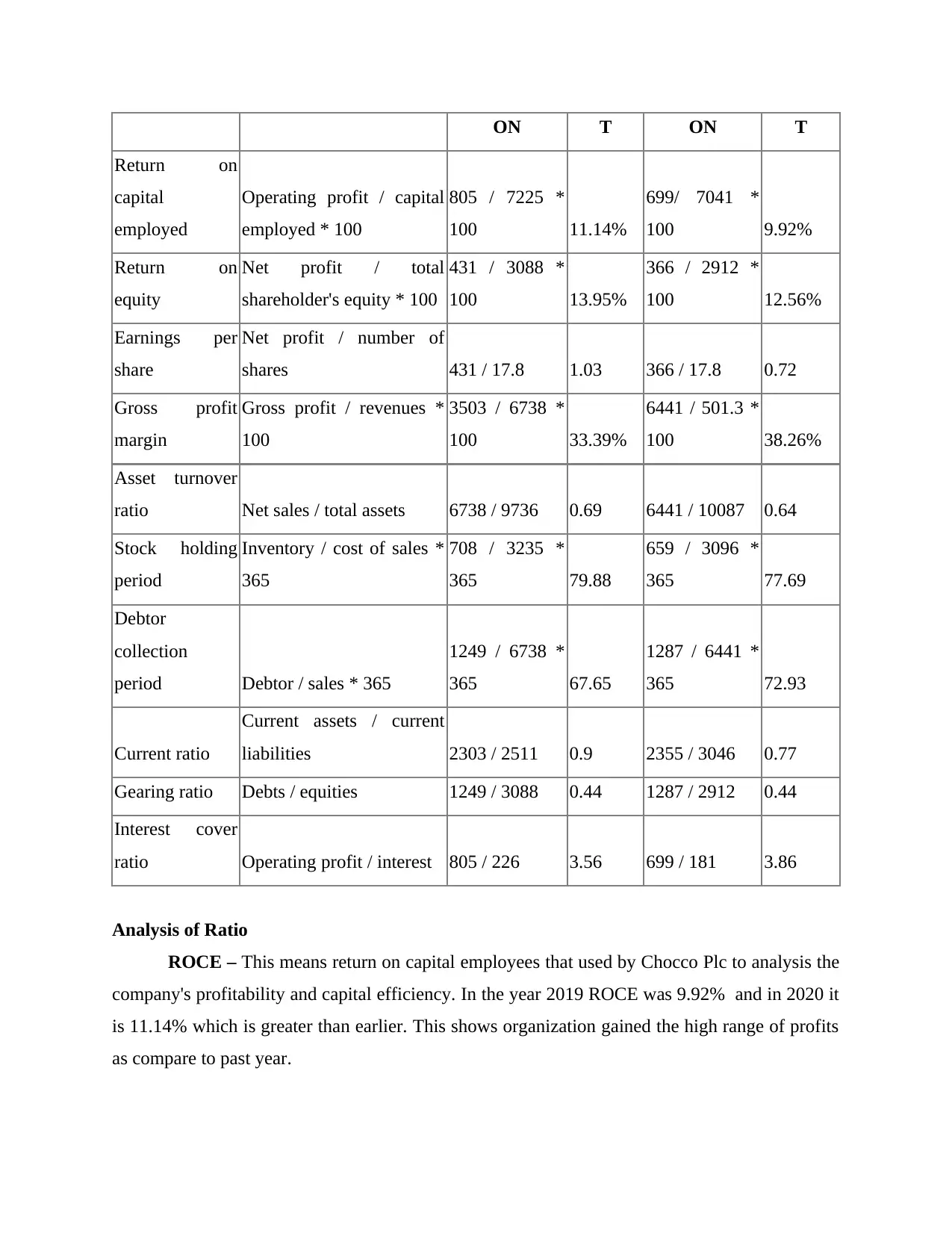

QUESTION 2

RATIO FORMULA 2020 2019

CALCULATI RESUL CALCULATI RESUL

ON T ON T

Return on

capital

employed

Operating profit / capital

employed * 100

805 / 7225 *

100 11.14%

699/ 7041 *

100 9.92%

Return on

equity

Net profit / total

shareholder's equity * 100

431 / 3088 *

100 13.95%

366 / 2912 *

100 12.56%

Earnings per

share

Net profit / number of

shares 431 / 17.8 1.03 366 / 17.8 0.72

Gross profit

margin

Gross profit / revenues *

100

3503 / 6738 *

100 33.39%

6441 / 501.3 *

100 38.26%

Asset turnover

ratio Net sales / total assets 6738 / 9736 0.69 6441 / 10087 0.64

Stock holding

period

Inventory / cost of sales *

365

708 / 3235 *

365 79.88

659 / 3096 *

365 77.69

Debtor

collection

period Debtor / sales * 365

1249 / 6738 *

365 67.65

1287 / 6441 *

365 72.93

Current ratio

Current assets / current

liabilities 2303 / 2511 0.9 2355 / 3046 0.77

Gearing ratio Debts / equities 1249 / 3088 0.44 1287 / 2912 0.44

Interest cover

ratio Operating profit / interest 805 / 226 3.56 699 / 181 3.86

Analysis of Ratio

ROCE – This means return on capital employees that used by Chocco Plc to analysis the

company's profitability and capital efficiency. In the year 2019 ROCE was 9.92% and in 2020 it

is 11.14% which is greater than earlier. This shows organization gained the high range of profits

as compare to past year.

Return on

capital

employed

Operating profit / capital

employed * 100

805 / 7225 *

100 11.14%

699/ 7041 *

100 9.92%

Return on

equity

Net profit / total

shareholder's equity * 100

431 / 3088 *

100 13.95%

366 / 2912 *

100 12.56%

Earnings per

share

Net profit / number of

shares 431 / 17.8 1.03 366 / 17.8 0.72

Gross profit

margin

Gross profit / revenues *

100

3503 / 6738 *

100 33.39%

6441 / 501.3 *

100 38.26%

Asset turnover

ratio Net sales / total assets 6738 / 9736 0.69 6441 / 10087 0.64

Stock holding

period

Inventory / cost of sales *

365

708 / 3235 *

365 79.88

659 / 3096 *

365 77.69

Debtor

collection

period Debtor / sales * 365

1249 / 6738 *

365 67.65

1287 / 6441 *

365 72.93

Current ratio

Current assets / current

liabilities 2303 / 2511 0.9 2355 / 3046 0.77

Gearing ratio Debts / equities 1249 / 3088 0.44 1287 / 2912 0.44

Interest cover

ratio Operating profit / interest 805 / 226 3.56 699 / 181 3.86

Analysis of Ratio

ROCE – This means return on capital employees that used by Chocco Plc to analysis the

company's profitability and capital efficiency. In the year 2019 ROCE was 9.92% and in 2020 it

is 11.14% which is greater than earlier. This shows organization gained the high range of profits

as compare to past year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROE – This is a measure tool which used by Chocco Plc to analyse the shareholder's

equity that can help to increase business performance. From the calculate it can be interpreted

that ROE of 2019 was 12.56% and in 2020 it is 13.95% that shows higher participation of equity

shareholders in the organization (Merkt, H., 2021).

EPS – This ratio exactly states earning or net income of organization that is split up on a

per share basis. The EPS of 2019 was .72 where as 2020's EPS is 1.03 that is good for the

Chocco Plc as it helps to retain higher funds.

Gross Profit Margin – This ratio states net income generated as a percentage of

revenues receives that increase productivity. In the year 2019 GP ratio was 38.26 % and in 2020

it is 33.395 that is less that past year. The reason behind reducing pro0fit margin is increases in

expenses and debts of Chocco Plc while operating the business.

Assets Turn over ratio – This ration is used to know the organization's efficiency which

arises by analysing assets and it produce the revenues. From the ratio calculation it has analysed

that Chocco Plc get possession of high range of assets than past year. In 2019 assets turn over

ratio was 0.64 and in 2020 it is 0.69 that is good for organization as assets value increased.

Stock Holding period – This can be explained as amount of time and investment that is

held by an investors or the period between the purchase and sale of security. The stock holding

period of 2019 was 77.68 days and 2020 79.88 that states in current year 0organization holds

more stock (Poscher, R., 2021).

Debtors Collection period – This means a field period of time in which amount will be

revived that is accrued while buying something. The debtors collection period of 2019 was 72.93

days. On the other side, DCP of 2020 is 67.65 days that is good as organization would received

the amount in less days than past year.

Current Ratio – This states as a popular metric that used across industry for assessing

company's short term liquidity. The Current ratio of 2019 was 0.77 and CR of 2020 is 0.91

which is greater. As compare to past year, Chocco Plc has higher capacity to maintain liquidity

in their workplace. The ideal CR for organisation is 2:1 that can help to manage all expenses and

develop business performance (Snell, R.L and et.al., 2019).

Gearing Ratio – This is a general classification stating a financial ratio, used to compare

some form of Owner's equity to funds borrowed by the company. In the year 2019 and 2021,

gearing ratio is 0.44 that can helps to know organization have limited fund to pay off their debts.

equity that can help to increase business performance. From the calculate it can be interpreted

that ROE of 2019 was 12.56% and in 2020 it is 13.95% that shows higher participation of equity

shareholders in the organization (Merkt, H., 2021).

EPS – This ratio exactly states earning or net income of organization that is split up on a

per share basis. The EPS of 2019 was .72 where as 2020's EPS is 1.03 that is good for the

Chocco Plc as it helps to retain higher funds.

Gross Profit Margin – This ratio states net income generated as a percentage of

revenues receives that increase productivity. In the year 2019 GP ratio was 38.26 % and in 2020

it is 33.395 that is less that past year. The reason behind reducing pro0fit margin is increases in

expenses and debts of Chocco Plc while operating the business.

Assets Turn over ratio – This ration is used to know the organization's efficiency which

arises by analysing assets and it produce the revenues. From the ratio calculation it has analysed

that Chocco Plc get possession of high range of assets than past year. In 2019 assets turn over

ratio was 0.64 and in 2020 it is 0.69 that is good for organization as assets value increased.

Stock Holding period – This can be explained as amount of time and investment that is

held by an investors or the period between the purchase and sale of security. The stock holding

period of 2019 was 77.68 days and 2020 79.88 that states in current year 0organization holds

more stock (Poscher, R., 2021).

Debtors Collection period – This means a field period of time in which amount will be

revived that is accrued while buying something. The debtors collection period of 2019 was 72.93

days. On the other side, DCP of 2020 is 67.65 days that is good as organization would received

the amount in less days than past year.

Current Ratio – This states as a popular metric that used across industry for assessing

company's short term liquidity. The Current ratio of 2019 was 0.77 and CR of 2020 is 0.91

which is greater. As compare to past year, Chocco Plc has higher capacity to maintain liquidity

in their workplace. The ideal CR for organisation is 2:1 that can help to manage all expenses and

develop business performance (Snell, R.L and et.al., 2019).

Gearing Ratio – This is a general classification stating a financial ratio, used to compare

some form of Owner's equity to funds borrowed by the company. In the year 2019 and 2021,

gearing ratio is 0.44 that can helps to know organization have limited fund to pay off their debts.

Interest coverage ratio – This means debts and profitability ratio that states how a

company can pay interest on its outstanding debts. In relation to Chocco Plc, interest coverage

ratio was 3.86 and in 2020 is 3.56 which is less. This is beneficial for organization as it has to

pay less interest on their outstanding debts (Wirth, C and et.al., 2021).

company can pay interest on its outstanding debts. In relation to Chocco Plc, interest coverage

ratio was 3.86 and in 2020 is 3.56 which is less. This is beneficial for organization as it has to

pay less interest on their outstanding debts (Wirth, C and et.al., 2021).

References

Ahmed, A.S and et.al., 2019. An empirical analysis of the effects of the Dodd-Frank Act on

determinants of credit ratings. Available at SSRN 2991922.

Ardalan, K., 2019. Equity home bias: a review essay. Journal of Economic Surveys, 33(3),

pp.949-967.

Brunelli, S. and Di Carlo, E., 2020. Accountability, ethics and sustainability of

organizations. Accounting, Finance, Sustainability, Governance and Fraud: Theory and

Application, 4, pp.82-123.

Guralnik, B. and Sohbati, R., 2019. Fundamentals of luminescence photo-and

thermochronometry. In Advances In Physics And Applications Of Optically And

Thermally Stimulated Luminescence (pp. 399-437).

Lee, C.M. and Watts, E.M., 2021. Tick size tolls: Can a trading slowdown improve earnings

news discovery?. The Accounting Review, 96(3), pp.373-401.

Merkt, H., 2021, July. The Dynamic Relationship between German Corporate Law and Financial

Market Law. In Legal Theory and Interpretation in a Dynamic Society (pp. 131-148).

Nomos Verlagsgesellschaft mbH & Co. KG.

Poscher, R., 2021, July. The Normative Construction of Legislative Intent. In Legal Theory and

Interpretation in a Dynamic Society (pp. 11-46). Nomos Verlagsgesellschaft mbH & Co.

KG.

Snell, R.L and et.al., 2019. Fundamentals of Radio Astronomy: Astrophysics. CRC Press.

Wirth, C and et.al., 2021. Fundamentals of finance: Financial institutions and markets, personal

finance, financial management. Massey University Press.

Ahmed, A.S and et.al., 2019. An empirical analysis of the effects of the Dodd-Frank Act on

determinants of credit ratings. Available at SSRN 2991922.

Ardalan, K., 2019. Equity home bias: a review essay. Journal of Economic Surveys, 33(3),

pp.949-967.

Brunelli, S. and Di Carlo, E., 2020. Accountability, ethics and sustainability of

organizations. Accounting, Finance, Sustainability, Governance and Fraud: Theory and

Application, 4, pp.82-123.

Guralnik, B. and Sohbati, R., 2019. Fundamentals of luminescence photo-and

thermochronometry. In Advances In Physics And Applications Of Optically And

Thermally Stimulated Luminescence (pp. 399-437).

Lee, C.M. and Watts, E.M., 2021. Tick size tolls: Can a trading slowdown improve earnings

news discovery?. The Accounting Review, 96(3), pp.373-401.

Merkt, H., 2021, July. The Dynamic Relationship between German Corporate Law and Financial

Market Law. In Legal Theory and Interpretation in a Dynamic Society (pp. 131-148).

Nomos Verlagsgesellschaft mbH & Co. KG.

Poscher, R., 2021, July. The Normative Construction of Legislative Intent. In Legal Theory and

Interpretation in a Dynamic Society (pp. 11-46). Nomos Verlagsgesellschaft mbH & Co.

KG.

Snell, R.L and et.al., 2019. Fundamentals of Radio Astronomy: Astrophysics. CRC Press.

Wirth, C and et.al., 2021. Fundamentals of finance: Financial institutions and markets, personal

finance, financial management. Massey University Press.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.