Accounting Fundamentals: Analysis of Financial Performance and Position of Chocco plc

VerifiedAdded on 2023/06/18

|16

|1964

|277

AI Summary

This project explains the importance of accounting fundamentals and includes a profit and loss statement for Kedison Plc. It also evaluates the financial performance and position of Chocco plc with the help of different financial ratios. Suggestions have been made for improving the operations of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting Fundamentals

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Profit and loss statement for Kedison PLC .................................................................................3

Balance sheet for the year ended.................................................................................................4

Question 2........................................................................................................................................5

Calculation of ratios for Chocco plc............................................................................................5

Commenting on the financial performance and position of Chocco plc...................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Profit and loss statement for Kedison PLC .................................................................................3

Balance sheet for the year ended.................................................................................................4

Question 2........................................................................................................................................5

Calculation of ratios for Chocco plc............................................................................................5

Commenting on the financial performance and position of Chocco plc...................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

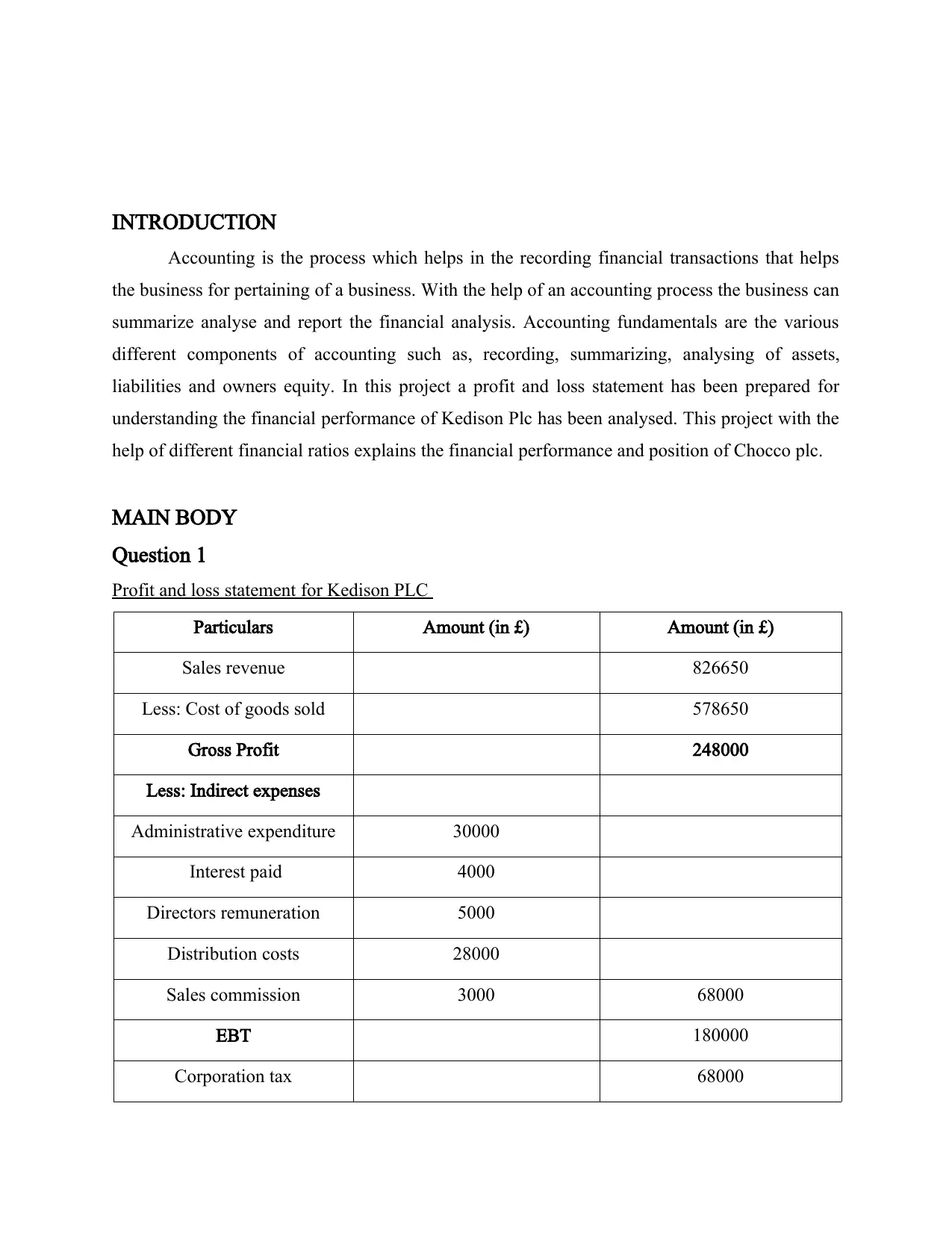

INTRODUCTION

Accounting is the process which helps in the recording financial transactions that helps

the business for pertaining of a business. With the help of an accounting process the business can

summarize analyse and report the financial analysis. Accounting fundamentals are the various

different components of accounting such as, recording, summarizing, analysing of assets,

liabilities and owners equity. In this project a profit and loss statement has been prepared for

understanding the financial performance of Kedison Plc has been analysed. This project with the

help of different financial ratios explains the financial performance and position of Chocco plc.

MAIN BODY

Question 1

Profit and loss statement for Kedison PLC

Particulars Amount (in £) Amount (in £)

Sales revenue 826650

Less: Cost of goods sold 578650

Gross Profit 248000

Less: Indirect expenses

Administrative expenditure 30000

Interest paid 4000

Directors remuneration 5000

Distribution costs 28000

Sales commission 3000 68000

EBT 180000

Corporation tax 68000

Accounting is the process which helps in the recording financial transactions that helps

the business for pertaining of a business. With the help of an accounting process the business can

summarize analyse and report the financial analysis. Accounting fundamentals are the various

different components of accounting such as, recording, summarizing, analysing of assets,

liabilities and owners equity. In this project a profit and loss statement has been prepared for

understanding the financial performance of Kedison Plc has been analysed. This project with the

help of different financial ratios explains the financial performance and position of Chocco plc.

MAIN BODY

Question 1

Profit and loss statement for Kedison PLC

Particulars Amount (in £) Amount (in £)

Sales revenue 826650

Less: Cost of goods sold 578650

Gross Profit 248000

Less: Indirect expenses

Administrative expenditure 30000

Interest paid 4000

Directors remuneration 5000

Distribution costs 28000

Sales commission 3000 68000

EBT 180000

Corporation tax 68000

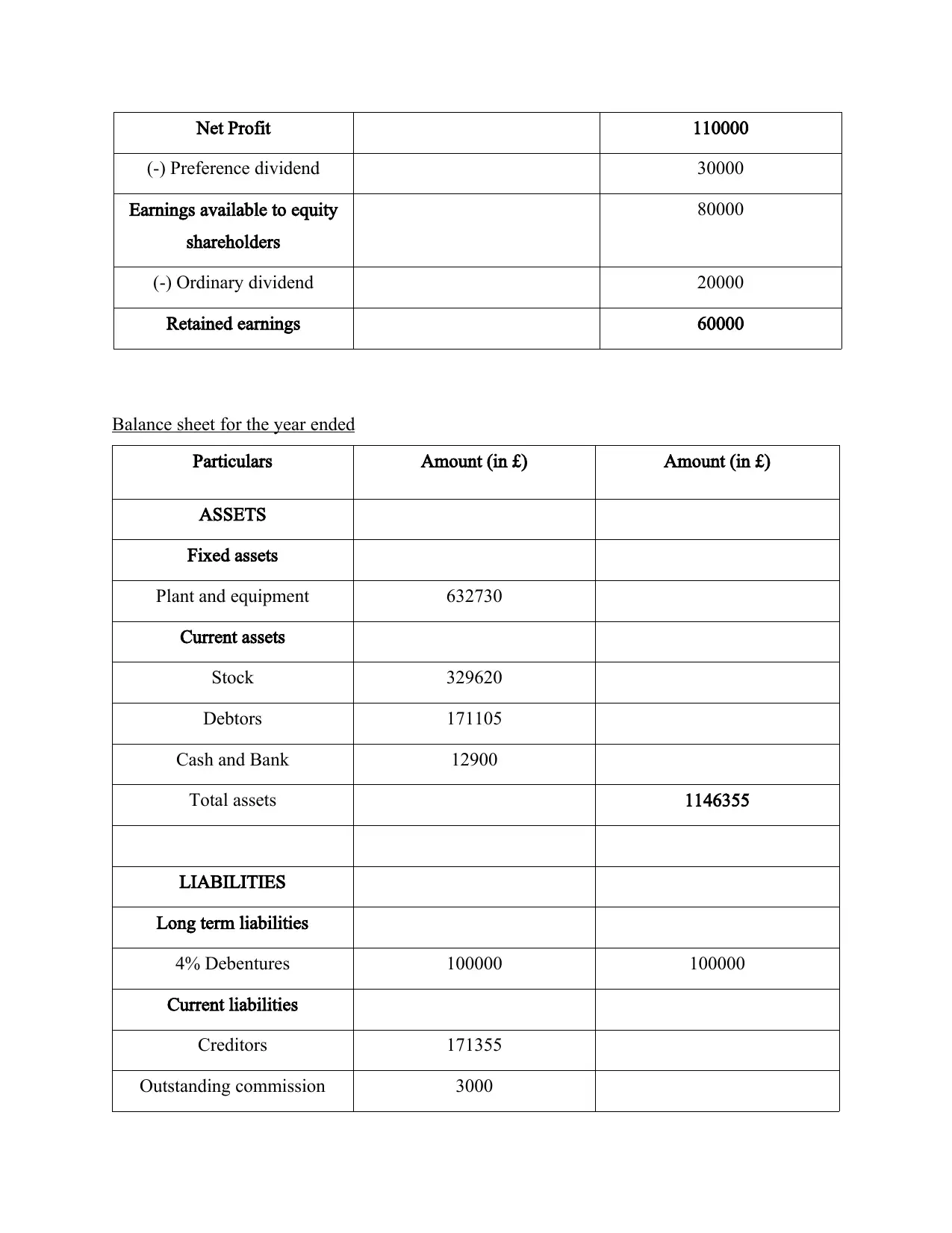

Net Profit 110000

(-) Preference dividend 30000

Earnings available to equity

shareholders

80000

(-) Ordinary dividend 20000

Retained earnings 60000

Balance sheet for the year ended

Particulars Amount (in £) Amount (in £)

ASSETS

Fixed assets

Plant and equipment 632730

Current assets

Stock 329620

Debtors 171105

Cash and Bank 12900

Total assets 1146355

LIABILITIES

Long term liabilities

4% Debentures 100000 100000

Current liabilities

Creditors 171355

Outstanding commission 3000

(-) Preference dividend 30000

Earnings available to equity

shareholders

80000

(-) Ordinary dividend 20000

Retained earnings 60000

Balance sheet for the year ended

Particulars Amount (in £) Amount (in £)

ASSETS

Fixed assets

Plant and equipment 632730

Current assets

Stock 329620

Debtors 171105

Cash and Bank 12900

Total assets 1146355

LIABILITIES

Long term liabilities

4% Debentures 100000 100000

Current liabilities

Creditors 171355

Outstanding commission 3000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Outstanding interest 2000

Tax payable 68000

Shareholders’ equity

Ordinary shares 310000

10% preference shares 300000

Profit for the period 110000

Retained earnings 60000

Total liabilities 1146355

Tax payable 68000

Shareholders’ equity

Ordinary shares 310000

10% preference shares 300000

Profit for the period 110000

Retained earnings 60000

Total liabilities 1146355

Question 2

Calculation of ratios for Chocco plc

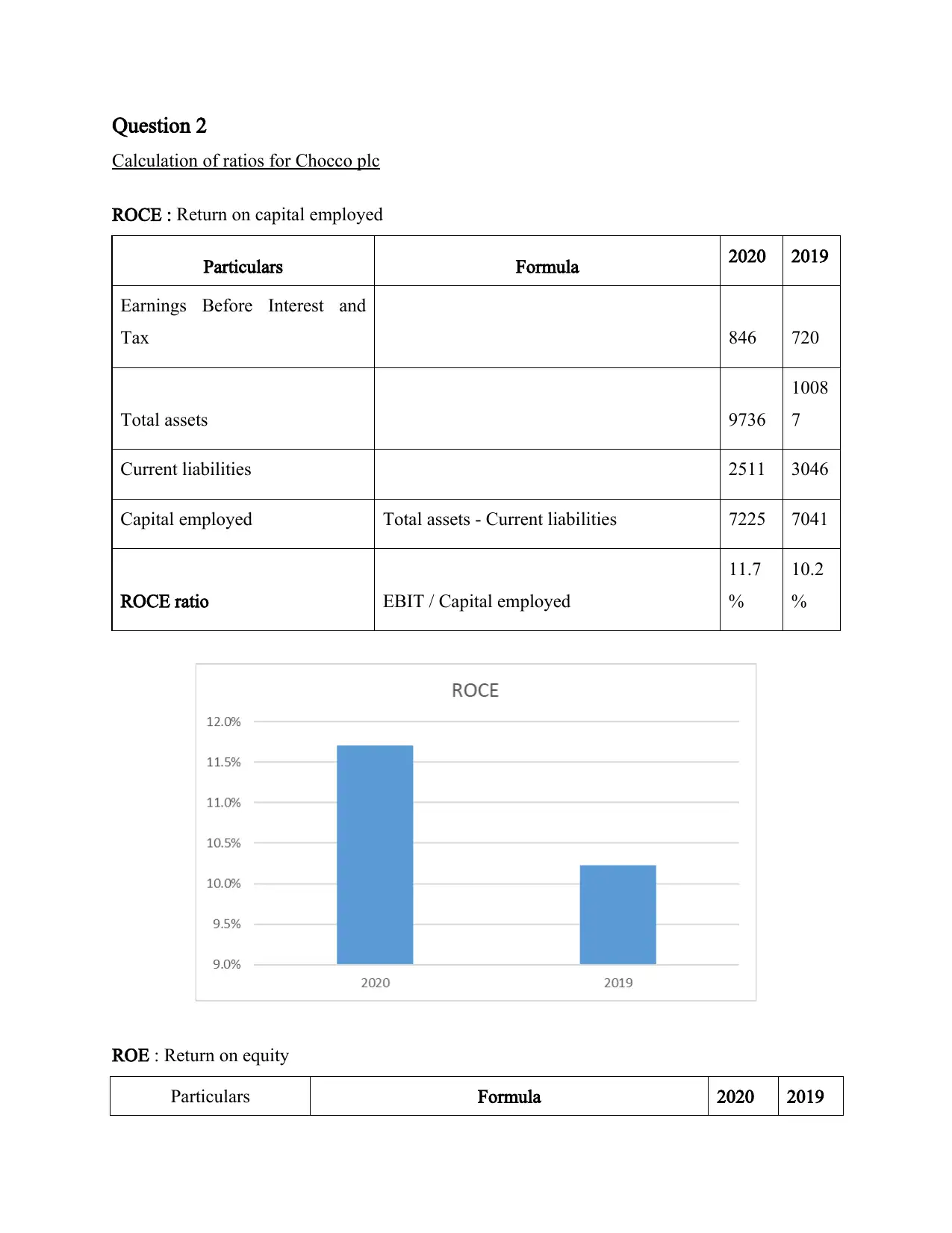

ROCE : Return on capital employed

Particulars Formula 2020 2019

Earnings Before Interest and

Tax 846 720

Total assets 9736

1008

7

Current liabilities 2511 3046

Capital employed Total assets - Current liabilities 7225 7041

ROCE ratio EBIT / Capital employed

11.7

%

10.2

%

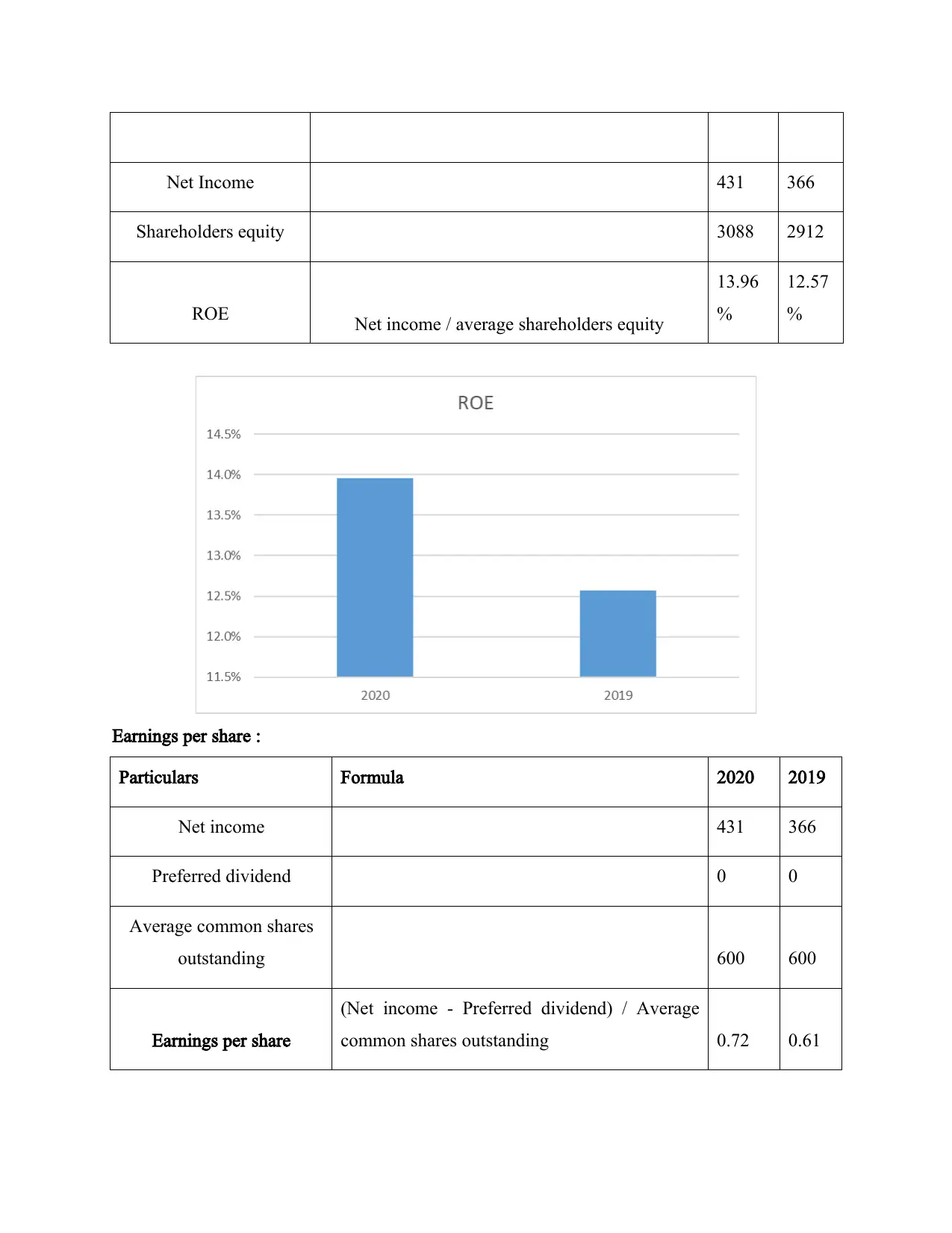

ROE : Return on equity

Particulars Formula 2020 2019

Calculation of ratios for Chocco plc

ROCE : Return on capital employed

Particulars Formula 2020 2019

Earnings Before Interest and

Tax 846 720

Total assets 9736

1008

7

Current liabilities 2511 3046

Capital employed Total assets - Current liabilities 7225 7041

ROCE ratio EBIT / Capital employed

11.7

%

10.2

%

ROE : Return on equity

Particulars Formula 2020 2019

Net Income 431 366

Shareholders equity 3088 2912

ROE Net income / average shareholders equity

13.96

%

12.57

%

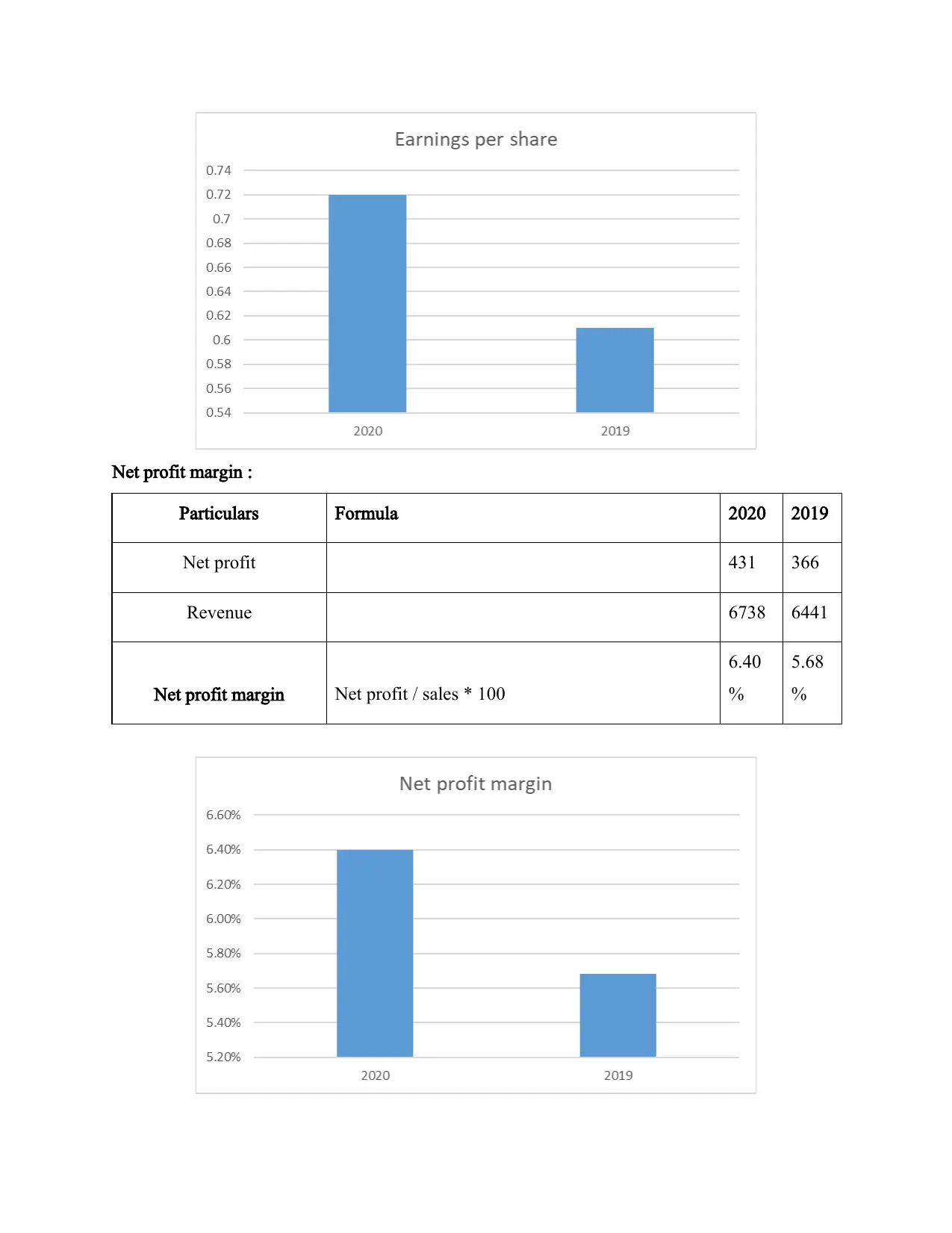

Earnings per share :

Particulars Formula 2020 2019

Net income 431 366

Preferred dividend 0 0

Average common shares

outstanding 600 600

Earnings per share

(Net income - Preferred dividend) / Average

common shares outstanding 0.72 0.61

Shareholders equity 3088 2912

ROE Net income / average shareholders equity

13.96

%

12.57

%

Earnings per share :

Particulars Formula 2020 2019

Net income 431 366

Preferred dividend 0 0

Average common shares

outstanding 600 600

Earnings per share

(Net income - Preferred dividend) / Average

common shares outstanding 0.72 0.61

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit margin :

Particulars Formula 2020 2019

Net profit 431 366

Revenue 6738 6441

Net profit margin Net profit / sales * 100

6.40

%

5.68

%

Particulars Formula 2020 2019

Net profit 431 366

Revenue 6738 6441

Net profit margin Net profit / sales * 100

6.40

%

5.68

%

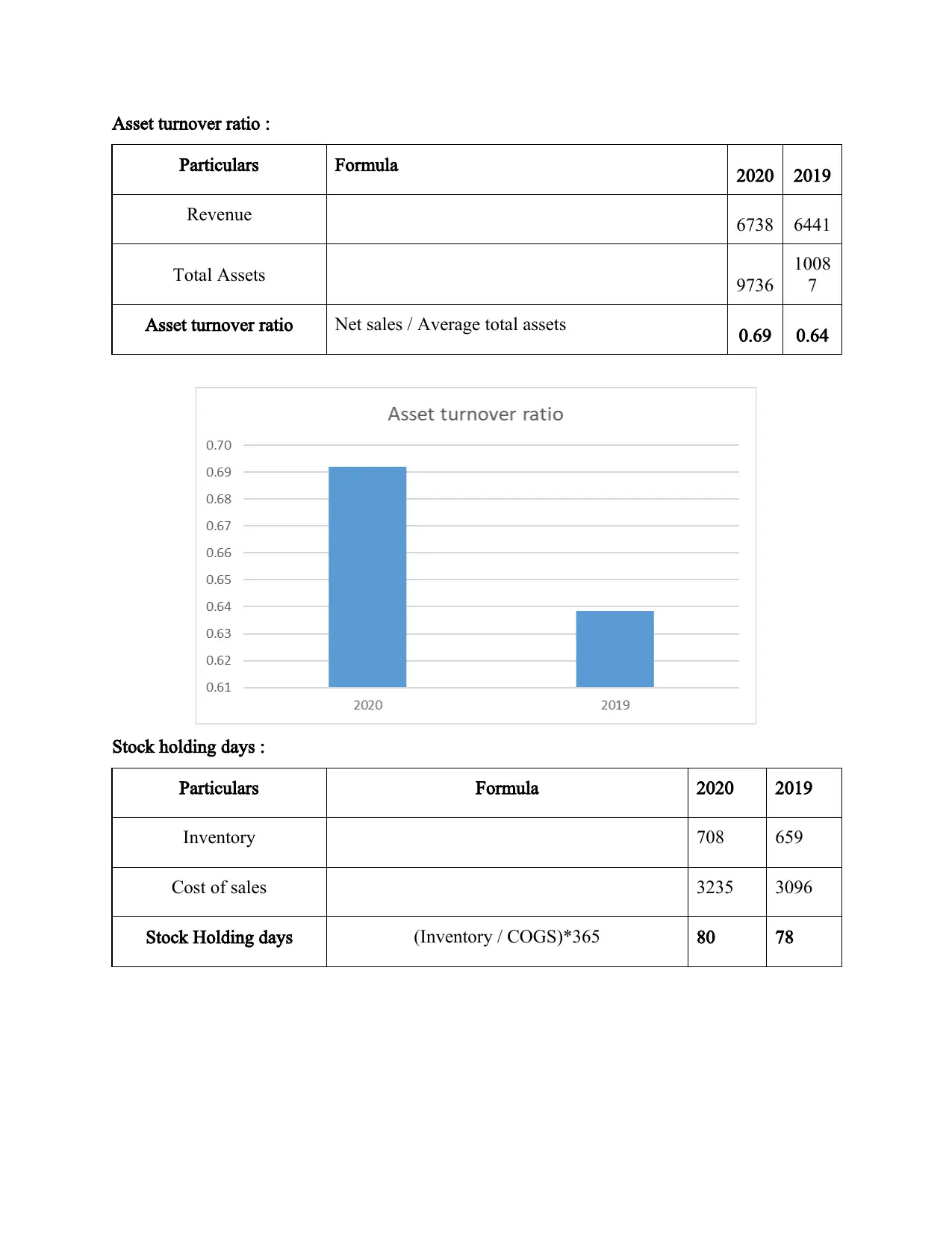

Asset turnover ratio :

Particulars Formula 2020 2019

Revenue 6738 6441

Total Assets 9736

1008

7

Asset turnover ratio Net sales / Average total assets 0.69 0.64

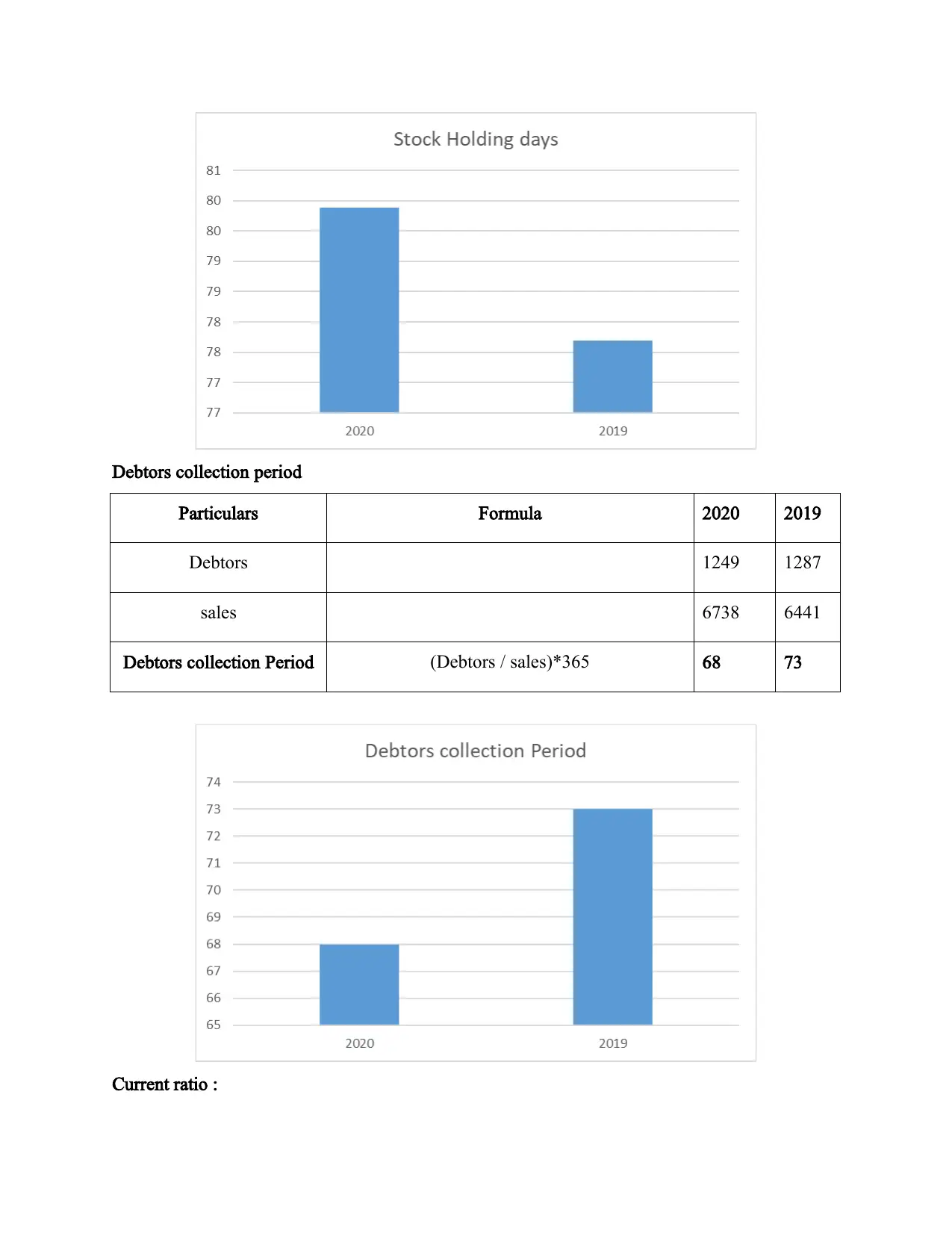

Stock holding days :

Particulars Formula 2020 2019

Inventory 708 659

Cost of sales 3235 3096

Stock Holding days (Inventory / COGS)*365 80 78

Particulars Formula 2020 2019

Revenue 6738 6441

Total Assets 9736

1008

7

Asset turnover ratio Net sales / Average total assets 0.69 0.64

Stock holding days :

Particulars Formula 2020 2019

Inventory 708 659

Cost of sales 3235 3096

Stock Holding days (Inventory / COGS)*365 80 78

Debtors collection period

Particulars Formula 2020 2019

Debtors 1249 1287

sales 6738 6441

Debtors collection Period (Debtors / sales)*365 68 73

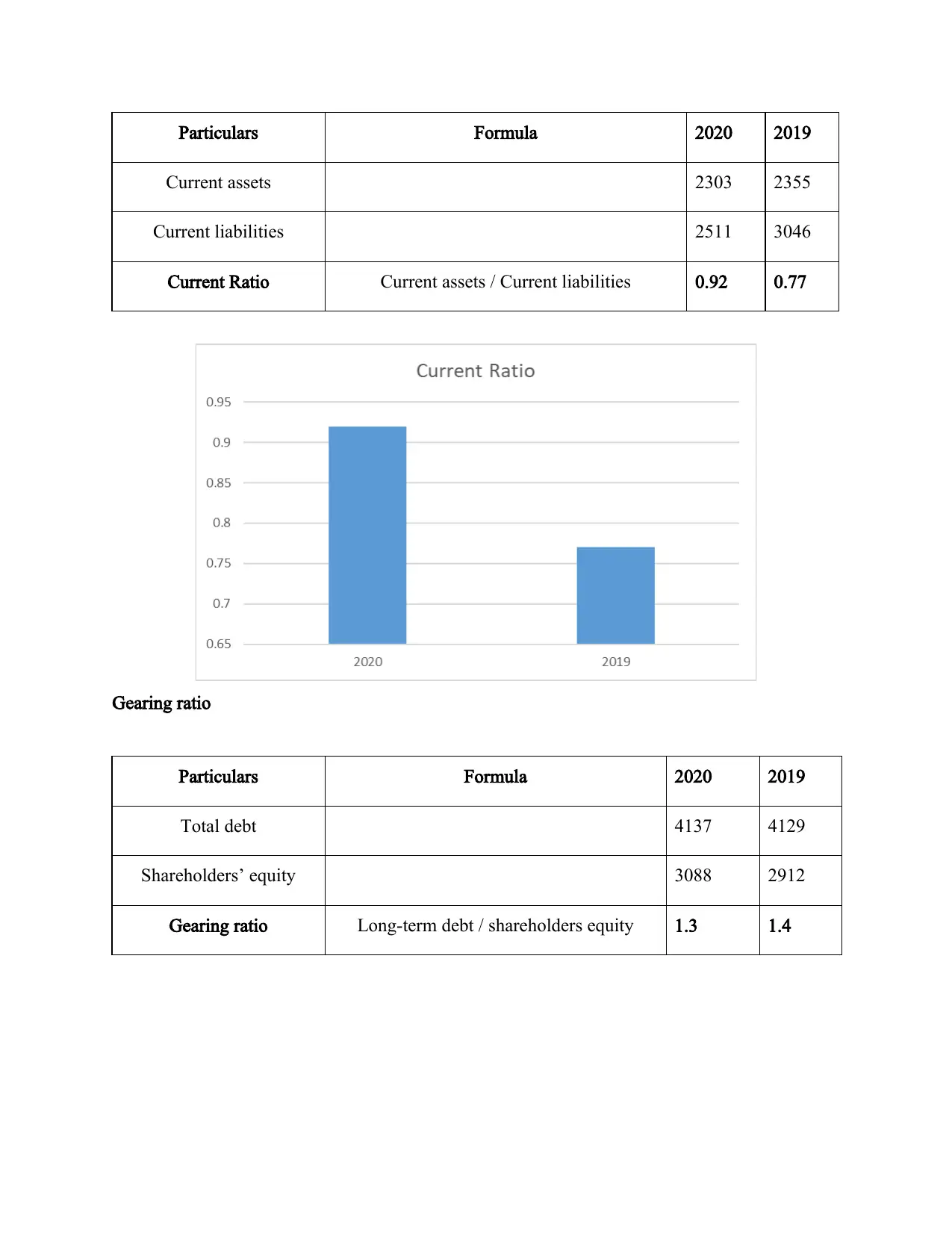

Current ratio :

Particulars Formula 2020 2019

Debtors 1249 1287

sales 6738 6441

Debtors collection Period (Debtors / sales)*365 68 73

Current ratio :

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Particulars Formula 2020 2019

Current assets 2303 2355

Current liabilities 2511 3046

Current Ratio Current assets / Current liabilities 0.92 0.77

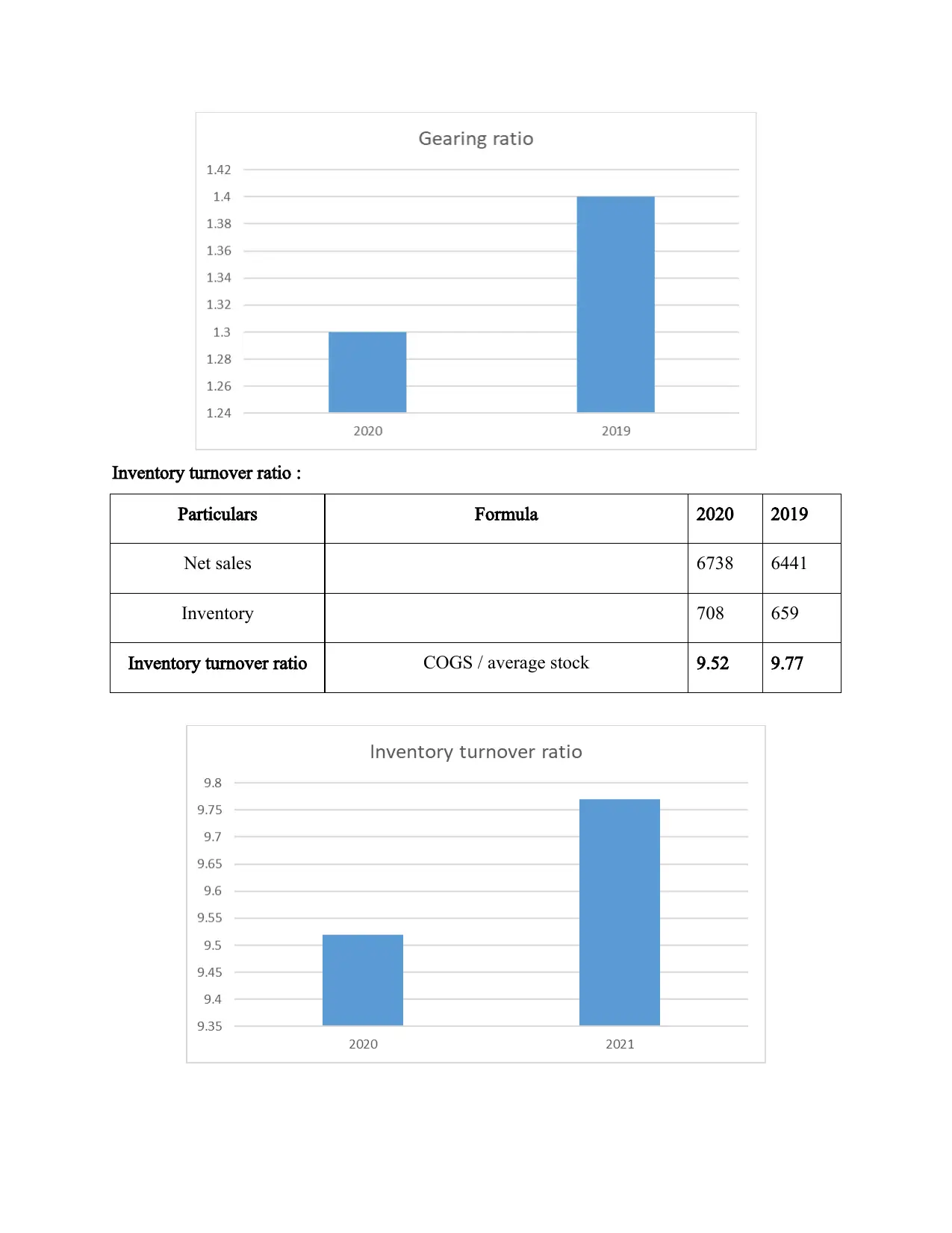

Gearing ratio

Particulars Formula 2020 2019

Total debt 4137 4129

Shareholders’ equity 3088 2912

Gearing ratio Long-term debt / shareholders equity 1.3 1.4

Current assets 2303 2355

Current liabilities 2511 3046

Current Ratio Current assets / Current liabilities 0.92 0.77

Gearing ratio

Particulars Formula 2020 2019

Total debt 4137 4129

Shareholders’ equity 3088 2912

Gearing ratio Long-term debt / shareholders equity 1.3 1.4

Inventory turnover ratio :

Particulars Formula 2020 2019

Net sales 6738 6441

Inventory 708 659

Inventory turnover ratio COGS / average stock 9.52 9.77

Particulars Formula 2020 2019

Net sales 6738 6441

Inventory 708 659

Inventory turnover ratio COGS / average stock 9.52 9.77

Commenting on the financial performance and position of Chocco plc

ROCE :

Return on capital employed shows the measurement of company's profitability in the

terms of its total capital. For the Chocco plc the return on capital employed showed a positive

result on the performance of the business in the following years as the ROCE increased from

10.2% to 11.7%. This shows that the company has utilized its capital much more efficiently than

as compared to the previous year (Rashid, 2018). Despite the positive trend in the ROCE this

organization can improve its performance even more by utilization of its resources in a more

efficient ways.

ROE :

Return on equity is the measurement of the company's profit with relation to the

shareholder's equity. In this organization the ROE ration has increased to 13.96% which in the

previous year was 12.57%. This shows that the business has been successful in generating return

with the help of the shareholder's money. Increasing rate of ROE is very advantageous for the

business it influences the investors to spending on the company. However, the ROE of the

company still does require improvement. This company can try to reduce its expenditure and try

to achieve efficiency in its operations for generating higher return (Rahman. and Fatmawati,

2020.

Earnings per share :

The amount of money that Chocco plc made out of each individual share is said to be it's

earning per share. The earning per share has also increased for this company as in 2020 it was

0.61 which then increased to 0.72. This indicates that the business is able to improve its

operations so that it can generate higher profit out of the investments. Chocco plc can increase its

EPS by improving its business strategies.

Net profit margin :

This is a ratio which tells about what is the percentage of profit that the company has

generated from its revenue. It indicates the amount of profit made by the company from £1. An

organization can increase its net profit margin by decreasing the total cost which its incurs.

Chocco plc has been successful in improving its Net profit margin from 5.68% to 6.40%.

ROCE :

Return on capital employed shows the measurement of company's profitability in the

terms of its total capital. For the Chocco plc the return on capital employed showed a positive

result on the performance of the business in the following years as the ROCE increased from

10.2% to 11.7%. This shows that the company has utilized its capital much more efficiently than

as compared to the previous year (Rashid, 2018). Despite the positive trend in the ROCE this

organization can improve its performance even more by utilization of its resources in a more

efficient ways.

ROE :

Return on equity is the measurement of the company's profit with relation to the

shareholder's equity. In this organization the ROE ration has increased to 13.96% which in the

previous year was 12.57%. This shows that the business has been successful in generating return

with the help of the shareholder's money. Increasing rate of ROE is very advantageous for the

business it influences the investors to spending on the company. However, the ROE of the

company still does require improvement. This company can try to reduce its expenditure and try

to achieve efficiency in its operations for generating higher return (Rahman. and Fatmawati,

2020.

Earnings per share :

The amount of money that Chocco plc made out of each individual share is said to be it's

earning per share. The earning per share has also increased for this company as in 2020 it was

0.61 which then increased to 0.72. This indicates that the business is able to improve its

operations so that it can generate higher profit out of the investments. Chocco plc can increase its

EPS by improving its business strategies.

Net profit margin :

This is a ratio which tells about what is the percentage of profit that the company has

generated from its revenue. It indicates the amount of profit made by the company from £1. An

organization can increase its net profit margin by decreasing the total cost which its incurs.

Chocco plc has been successful in improving its Net profit margin from 5.68% to 6.40%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, to improve the net profit margin even more the organization needs to utilize its

resources more efficiently.

Asset turnover ratio :

Asset turnover ratio measures the efficiency of the organization showing how much

revenue the company generates from its assets. It is important to have higher Asset turn over

ratio as it indicates efficiency of the business resources and management. Chocco plc has been

able to improve its asset turnover ratio slightly from 0.64 to 0.69 in 2020. This company was

able to do so with the help of improving its, production capacity, collection method and strong

inventory management (Dong, Tian and Chen, 2018).

Stock holding days :

Stock holding days shows the average number of days that the stock of the company

spends in the warehouse. For a company it is important to have shorter stock holding days. This

company has held its stock for 78 days in 2019, but in 2020 it increased to 80 days. This means

that the turnover of the stock took longer for the company. It also indicates that the business had

to incur more cost on keeping the stock in the inventory for extra 2 days. Thus, the organization

needs to focus on improving its marketing strategy.

Debtors collection period:

It is the time taken by the business for collecting the total amount of debt it has given. It

is quite natural that Chocco plc the time taken in the debtor's collection to be as little as possible.

This business has managed to do so as its debtors collection period was 73 days in 2019 which

decreased to 68 days. However, the company can reduce this period as well by offering the

debtors discount on early payment (Gullett, Kilgore and Geddie, 2018).

Current ratio :

It's the measurement of the ratio which measures the liquidity of the organization. This

ratio allows the investors to understand how a company is able to maximize the current assets of

the company with its balance sheet. The ideal current ratio is considered to be 2:1. This shows

the risk involved in the business for the investors. The current ration of Chocco plc is 0.92 in

2020 which in the 2019 was 0.77. Although the current ratio has improved it can improve more

if company can increase is business efficiency.

Gearing ratio :

resources more efficiently.

Asset turnover ratio :

Asset turnover ratio measures the efficiency of the organization showing how much

revenue the company generates from its assets. It is important to have higher Asset turn over

ratio as it indicates efficiency of the business resources and management. Chocco plc has been

able to improve its asset turnover ratio slightly from 0.64 to 0.69 in 2020. This company was

able to do so with the help of improving its, production capacity, collection method and strong

inventory management (Dong, Tian and Chen, 2018).

Stock holding days :

Stock holding days shows the average number of days that the stock of the company

spends in the warehouse. For a company it is important to have shorter stock holding days. This

company has held its stock for 78 days in 2019, but in 2020 it increased to 80 days. This means

that the turnover of the stock took longer for the company. It also indicates that the business had

to incur more cost on keeping the stock in the inventory for extra 2 days. Thus, the organization

needs to focus on improving its marketing strategy.

Debtors collection period:

It is the time taken by the business for collecting the total amount of debt it has given. It

is quite natural that Chocco plc the time taken in the debtor's collection to be as little as possible.

This business has managed to do so as its debtors collection period was 73 days in 2019 which

decreased to 68 days. However, the company can reduce this period as well by offering the

debtors discount on early payment (Gullett, Kilgore and Geddie, 2018).

Current ratio :

It's the measurement of the ratio which measures the liquidity of the organization. This

ratio allows the investors to understand how a company is able to maximize the current assets of

the company with its balance sheet. The ideal current ratio is considered to be 2:1. This shows

the risk involved in the business for the investors. The current ration of Chocco plc is 0.92 in

2020 which in the 2019 was 0.77. Although the current ratio has improved it can improve more

if company can increase is business efficiency.

Gearing ratio :

This ratio is the measurement of financial risk and also the expression of the total amount

of company's debt in the terms of its equity. In 2019 the gearing ratio was 1.4 which now has

decreased to 1.3. This decrease in the gearing ratio shows that the company at present is at lower

risk in comparison to earlier (Tenney and Kalenkoski, 2019).

Inventory turnover ratio :

Inventory turnover ratio is the financial ratio which shows the number of times company

has sold or re-invested in the inventory. The calculation of this ratio helps in making better

decision for the company regarding the pricing, manufacturing and marketing. Chocco plc has

decreased its inventory turnover ratio from 9.77 to 9.52 in 2020 which is positive as it is

important for a company to have low inventory turnover. The lower the inventory turnover ratio

it is better for the organization as the business is able to meet the demand of the customers

quickly (Lawal and et.al., 2020).

CONCLUSION

With the help of this project it can be concluded that accounting is very important for any

business for the analysation of its performance and better decision-making in the future. This

project was successful in showing the profit and loss account along with the balance sheet for

Kedison Plc. Utilization of the different ratios of the finance the financial performance of the

Chocco plc has been evaluated and suggestions has been made for improving the operations.

of company's debt in the terms of its equity. In 2019 the gearing ratio was 1.4 which now has

decreased to 1.3. This decrease in the gearing ratio shows that the company at present is at lower

risk in comparison to earlier (Tenney and Kalenkoski, 2019).

Inventory turnover ratio :

Inventory turnover ratio is the financial ratio which shows the number of times company

has sold or re-invested in the inventory. The calculation of this ratio helps in making better

decision for the company regarding the pricing, manufacturing and marketing. Chocco plc has

decreased its inventory turnover ratio from 9.77 to 9.52 in 2020 which is positive as it is

important for a company to have low inventory turnover. The lower the inventory turnover ratio

it is better for the organization as the business is able to meet the demand of the customers

quickly (Lawal and et.al., 2020).

CONCLUSION

With the help of this project it can be concluded that accounting is very important for any

business for the analysation of its performance and better decision-making in the future. This

project was successful in showing the profit and loss account along with the balance sheet for

Kedison Plc. Utilization of the different ratios of the finance the financial performance of the

Chocco plc has been evaluated and suggestions has been made for improving the operations.

REFERENCES

Books and Journals

Dong, M.C., Tian, S. and Chen, C.W., 2018. Predicting failure risk using financial ratios:

Quantile hazard model approach. The North American Journal of Economics and

Finance. 44. pp.204-220.

Gullett, N.S., Kilgore, R.W. and Geddie, M.F., 2018. Use of financial ratios to measure the

quality of earnings. Academy of Accounting and Financial Studies Journal. 22(2). pp.1-

12.

Lawal, A.I., and et.al., 2020. The impact of International Financial Reporting Standard (IFRS)

adoption on key financial ratios in Nigeria. Hum. Soc. Sci. Rev. 8(4). pp.289-300.

Rahman, T. and Fatmawati, K., 2020. The influence of financial ratios on non performing

financing of the sharia rural banks of Special Region of Yogyakarta (BPRS DIY) period

2015–2018. Asian Journal of Islamic Management. 2(1). pp.25-35.

Rashid, C.A., 2018. Efficiency of financial ratios analysis for evaluating companies’

liquidity. International Journal of Social Sciences & Educational Studies. 4(4). p.110.

Tenney, J.A. and Kalenkoski, C.M., 2019. Financial ratios and financial satisfaction: Exploring

associations between objective and subjective measures of financial well-being among

older Americans. Journal of Financial Counseling and Planning. 30(2). pp.231-243.

Books and Journals

Dong, M.C., Tian, S. and Chen, C.W., 2018. Predicting failure risk using financial ratios:

Quantile hazard model approach. The North American Journal of Economics and

Finance. 44. pp.204-220.

Gullett, N.S., Kilgore, R.W. and Geddie, M.F., 2018. Use of financial ratios to measure the

quality of earnings. Academy of Accounting and Financial Studies Journal. 22(2). pp.1-

12.

Lawal, A.I., and et.al., 2020. The impact of International Financial Reporting Standard (IFRS)

adoption on key financial ratios in Nigeria. Hum. Soc. Sci. Rev. 8(4). pp.289-300.

Rahman, T. and Fatmawati, K., 2020. The influence of financial ratios on non performing

financing of the sharia rural banks of Special Region of Yogyakarta (BPRS DIY) period

2015–2018. Asian Journal of Islamic Management. 2(1). pp.25-35.

Rashid, C.A., 2018. Efficiency of financial ratios analysis for evaluating companies’

liquidity. International Journal of Social Sciences & Educational Studies. 4(4). p.110.

Tenney, J.A. and Kalenkoski, C.M., 2019. Financial ratios and financial satisfaction: Exploring

associations between objective and subjective measures of financial well-being among

older Americans. Journal of Financial Counseling and Planning. 30(2). pp.231-243.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.