Accounting Fundamentals: Wales Plc Financial Statement Analysis Report

VerifiedAdded on 2023/01/09

|11

|3064

|82

Report

AI Summary

This comprehensive report delves into the core principles of accounting, providing a detailed analysis of financial statements, including the income statement and balance sheet. The report demonstrates the preparation of these statements using provided trial balance data for Wales Plc. Furthermore, it explores the calculation and interpretation of various financial ratios, offering insights into the performance of Jerry Plc across different periods. The report also identifies and discusses the interests of different user groups of company accounts, such as internal and external stakeholders, and evaluates the advantages and disadvantages of a highly regulated financial reporting regime. Finally, the report examines the limitations of financial statements, providing a well-rounded understanding of accounting fundamentals and their practical applications.

Accounting Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

1. Prepare Income statement for the year ended 31st December 2019.........................................1

2. Produce statement of financial position...................................................................................2

QUESTION 2..................................................................................................................................4

a. Calculation of various ratios for the organisation....................................................................4

b. Discussion of the situation which is revealed by the ratios.....................................................5

QUESTION 3..................................................................................................................................5

a. Identification of the three different user groups of company accounts and discussion of

reasons due to these user groups are interested in the information provided in final accounts...5

b. Discussion of the advantages and disadvantages of highly regulated financial reporting

regime..........................................................................................................................................6

c. Discussion of the limitations of financial statements..............................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

Question 1........................................................................................................................................1

1. Prepare Income statement for the year ended 31st December 2019.........................................1

2. Produce statement of financial position...................................................................................2

QUESTION 2..................................................................................................................................4

a. Calculation of various ratios for the organisation....................................................................4

b. Discussion of the situation which is revealed by the ratios.....................................................5

QUESTION 3..................................................................................................................................5

a. Identification of the three different user groups of company accounts and discussion of

reasons due to these user groups are interested in the information provided in final accounts...5

b. Discussion of the advantages and disadvantages of highly regulated financial reporting

regime..........................................................................................................................................6

c. Discussion of the limitations of financial statements..............................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting fundamentals are some of the key elements of accounting that are required to

be focused by all the entities so that the performance of business could be maintained. While

planning to analyse the future position of business the accountants can use financial statements

such as profit and loss account, balance sheet and cash flow statement. All of them can help to

analyse actual position of business and estimate it for future (Burger and Curtis, 2017). It is also

very important for the management teams of the entities to make sure that they are making

proper and appropriate adjustments in all the final accounts so that actual position of business

could be determined. Present report is based upon analysis of different aspects of accounting that

are required to be focused by all the entities. This assignment covers various topics such as

formulating of financial statements by making proper adjustments, calculation of ratios to

determine actual position of business etc. Apart from this, different groups of users of final

accounts and their interest in financial statements, advantage and disadvantage of highly

regulated financial reporting regime and limitation of final accounts are also covered in this

report.

Question 1

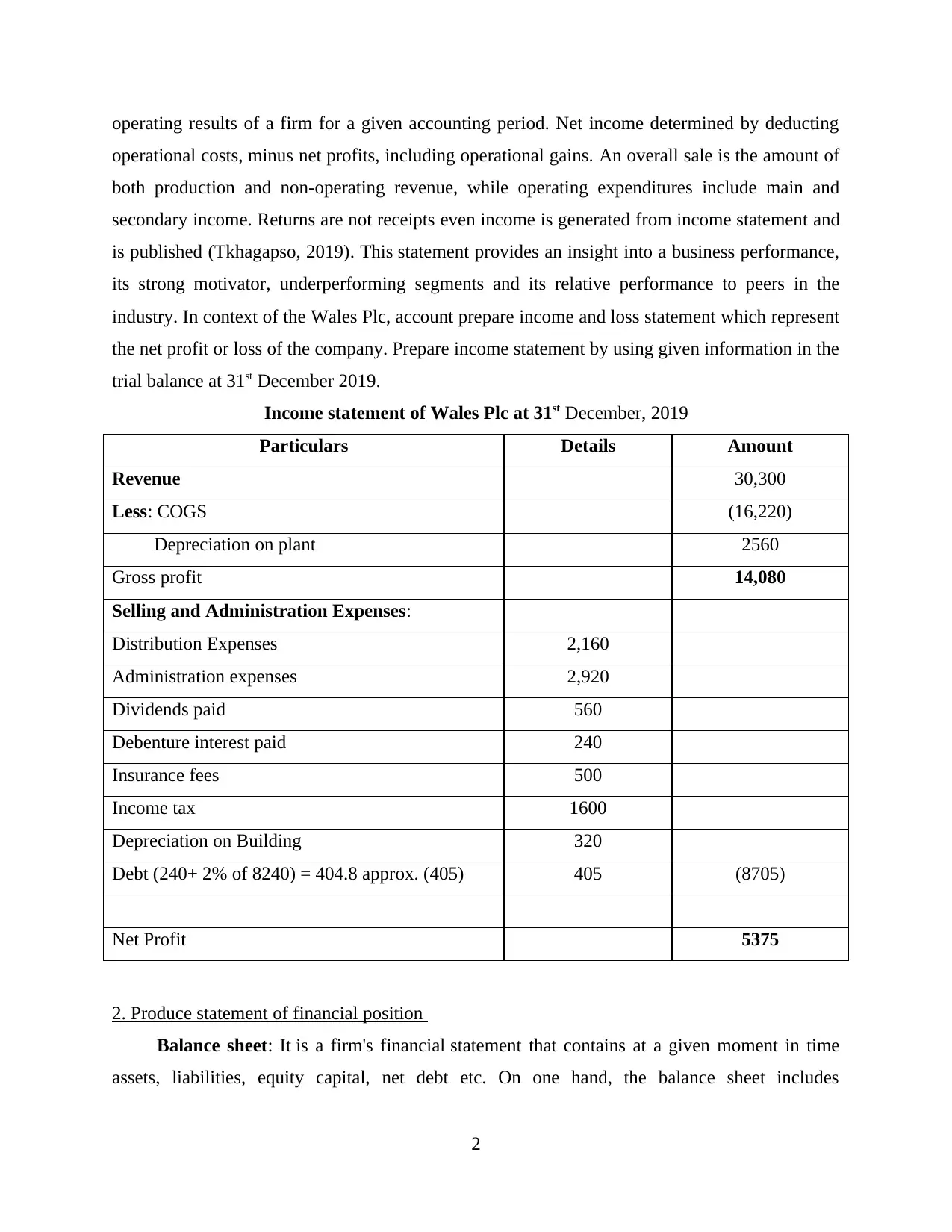

1. Prepare Income statement for the year ended 31st December 2019

Trial balance: A trial balance is a record keeping workbook where the balance of all

ledger accounts is collected into equivalent columns in debit and credit account numbers (Smith,

2019). A business annually schedules a trial inventory, usually after each monitoring cycle

concludes. A trial balance is meant to show the sum of all the debit appropriate balance is

equivalent to the total of all credit appropriate balance. The sum of the debit column is not

equivalent to the value of credit column than it will indicate that nominal ledger accounts are in

error.

Income Statement: The income statement is among the three essential financial

statements which used to disclose the financial results of a business for a given accounting

period. Other two main statements are balance sheet and the cash flow statement. Often

recognized as the profit & loss statement or revenue and cost statement, the income statement

reflects mainly on the business earnings and expenditures for a given period of time. It is the

main financial statements (along with the balance sheet and cash flow statement) that detail the

1

Accounting fundamentals are some of the key elements of accounting that are required to

be focused by all the entities so that the performance of business could be maintained. While

planning to analyse the future position of business the accountants can use financial statements

such as profit and loss account, balance sheet and cash flow statement. All of them can help to

analyse actual position of business and estimate it for future (Burger and Curtis, 2017). It is also

very important for the management teams of the entities to make sure that they are making

proper and appropriate adjustments in all the final accounts so that actual position of business

could be determined. Present report is based upon analysis of different aspects of accounting that

are required to be focused by all the entities. This assignment covers various topics such as

formulating of financial statements by making proper adjustments, calculation of ratios to

determine actual position of business etc. Apart from this, different groups of users of final

accounts and their interest in financial statements, advantage and disadvantage of highly

regulated financial reporting regime and limitation of final accounts are also covered in this

report.

Question 1

1. Prepare Income statement for the year ended 31st December 2019

Trial balance: A trial balance is a record keeping workbook where the balance of all

ledger accounts is collected into equivalent columns in debit and credit account numbers (Smith,

2019). A business annually schedules a trial inventory, usually after each monitoring cycle

concludes. A trial balance is meant to show the sum of all the debit appropriate balance is

equivalent to the total of all credit appropriate balance. The sum of the debit column is not

equivalent to the value of credit column than it will indicate that nominal ledger accounts are in

error.

Income Statement: The income statement is among the three essential financial

statements which used to disclose the financial results of a business for a given accounting

period. Other two main statements are balance sheet and the cash flow statement. Often

recognized as the profit & loss statement or revenue and cost statement, the income statement

reflects mainly on the business earnings and expenditures for a given period of time. It is the

main financial statements (along with the balance sheet and cash flow statement) that detail the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operating results of a firm for a given accounting period. Net income determined by deducting

operational costs, minus net profits, including operational gains. An overall sale is the amount of

both production and non-operating revenue, while operating expenditures include main and

secondary income. Returns are not receipts even income is generated from income statement and

is published (Tkhagapso, 2019). This statement provides an insight into a business performance,

its strong motivator, underperforming segments and its relative performance to peers in the

industry. In context of the Wales Plc, account prepare income and loss statement which represent

the net profit or loss of the company. Prepare income statement by using given information in the

trial balance at 31st December 2019.

Income statement of Wales Plc at 31st December, 2019

Particulars Details Amount

Revenue 30,300

Less: COGS (16,220)

Depreciation on plant 2560

Gross profit 14,080

Selling and Administration Expenses:

Distribution Expenses 2,160

Administration expenses 2,920

Dividends paid 560

Debenture interest paid 240

Insurance fees 500

Income tax 1600

Depreciation on Building 320

Debt (240+ 2% of 8240) = 404.8 approx. (405) 405 (8705)

Net Profit 5375

2. Produce statement of financial position

Balance sheet: It is a firm's financial statement that contains at a given moment in time

assets, liabilities, equity capital, net debt etc. On one hand, the balance sheet includes

2

operational costs, minus net profits, including operational gains. An overall sale is the amount of

both production and non-operating revenue, while operating expenditures include main and

secondary income. Returns are not receipts even income is generated from income statement and

is published (Tkhagapso, 2019). This statement provides an insight into a business performance,

its strong motivator, underperforming segments and its relative performance to peers in the

industry. In context of the Wales Plc, account prepare income and loss statement which represent

the net profit or loss of the company. Prepare income statement by using given information in the

trial balance at 31st December 2019.

Income statement of Wales Plc at 31st December, 2019

Particulars Details Amount

Revenue 30,300

Less: COGS (16,220)

Depreciation on plant 2560

Gross profit 14,080

Selling and Administration Expenses:

Distribution Expenses 2,160

Administration expenses 2,920

Dividends paid 560

Debenture interest paid 240

Insurance fees 500

Income tax 1600

Depreciation on Building 320

Debt (240+ 2% of 8240) = 404.8 approx. (405) 405 (8705)

Net Profit 5375

2. Produce statement of financial position

Balance sheet: It is a firm's financial statement that contains at a given moment in time

assets, liabilities, equity capital, net debt etc. On one hand, the balance sheet includes

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

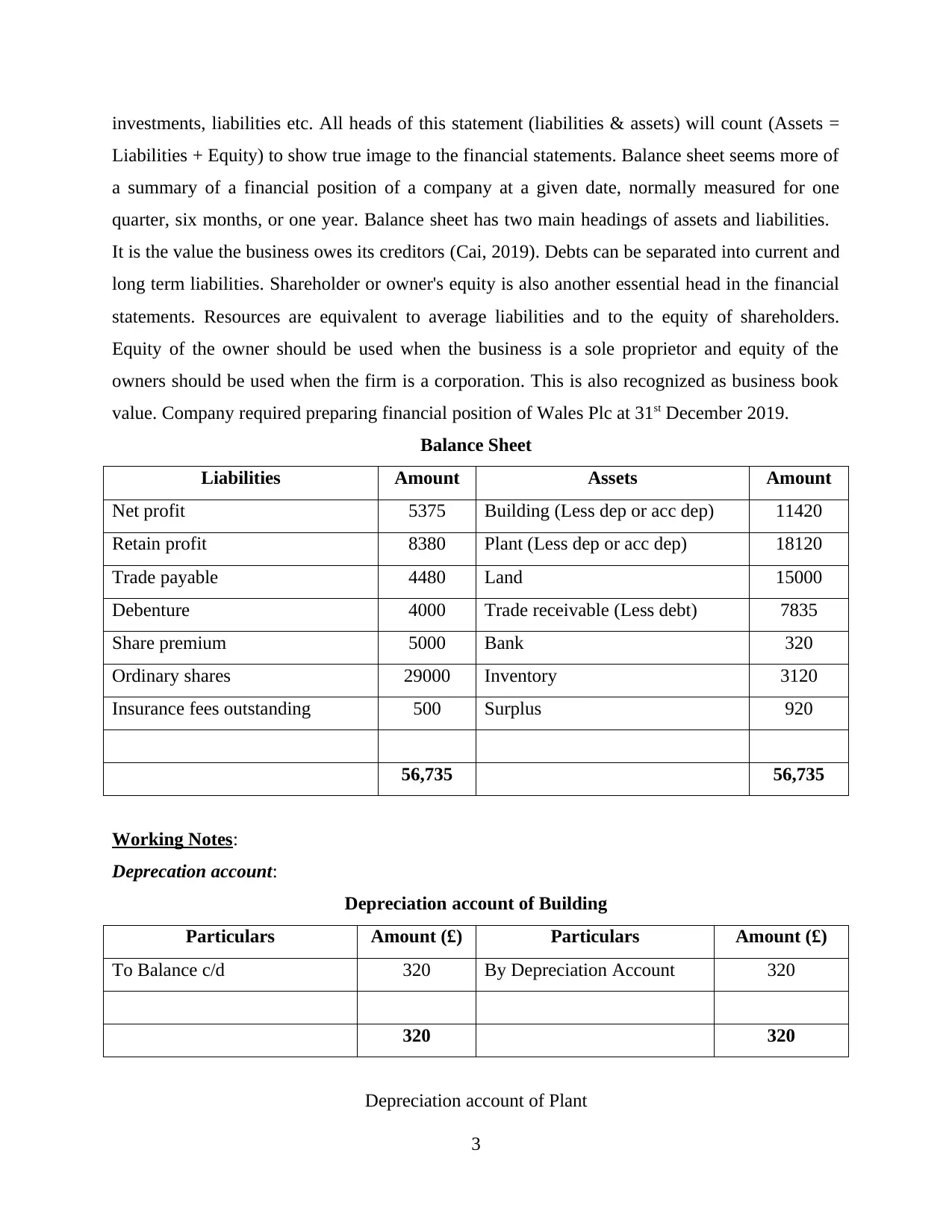

investments, liabilities etc. All heads of this statement (liabilities & assets) will count (Assets =

Liabilities + Equity) to show true image to the financial statements. Balance sheet seems more of

a summary of a financial position of a company at a given date, normally measured for one

quarter, six months, or one year. Balance sheet has two main headings of assets and liabilities.

It is the value the business owes its creditors (Cai, 2019). Debts can be separated into current and

long term liabilities. Shareholder or owner's equity is also another essential head in the financial

statements. Resources are equivalent to average liabilities and to the equity of shareholders.

Equity of the owner should be used when the business is a sole proprietor and equity of the

owners should be used when the firm is a corporation. This is also recognized as business book

value. Company required preparing financial position of Wales Plc at 31st December 2019.

Balance Sheet

Liabilities Amount Assets Amount

Net profit 5375 Building (Less dep or acc dep) 11420

Retain profit 8380 Plant (Less dep or acc dep) 18120

Trade payable 4480 Land 15000

Debenture 4000 Trade receivable (Less debt) 7835

Share premium 5000 Bank 320

Ordinary shares 29000 Inventory 3120

Insurance fees outstanding 500 Surplus 920

56,735 56,735

Working Notes:

Deprecation account:

Depreciation account of Building

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 320 By Depreciation Account 320

320 320

Depreciation account of Plant

3

Liabilities + Equity) to show true image to the financial statements. Balance sheet seems more of

a summary of a financial position of a company at a given date, normally measured for one

quarter, six months, or one year. Balance sheet has two main headings of assets and liabilities.

It is the value the business owes its creditors (Cai, 2019). Debts can be separated into current and

long term liabilities. Shareholder or owner's equity is also another essential head in the financial

statements. Resources are equivalent to average liabilities and to the equity of shareholders.

Equity of the owner should be used when the business is a sole proprietor and equity of the

owners should be used when the firm is a corporation. This is also recognized as business book

value. Company required preparing financial position of Wales Plc at 31st December 2019.

Balance Sheet

Liabilities Amount Assets Amount

Net profit 5375 Building (Less dep or acc dep) 11420

Retain profit 8380 Plant (Less dep or acc dep) 18120

Trade payable 4480 Land 15000

Debenture 4000 Trade receivable (Less debt) 7835

Share premium 5000 Bank 320

Ordinary shares 29000 Inventory 3120

Insurance fees outstanding 500 Surplus 920

56,735 56,735

Working Notes:

Deprecation account:

Depreciation account of Building

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 320 By Depreciation Account 320

320 320

Depreciation account of Plant

3

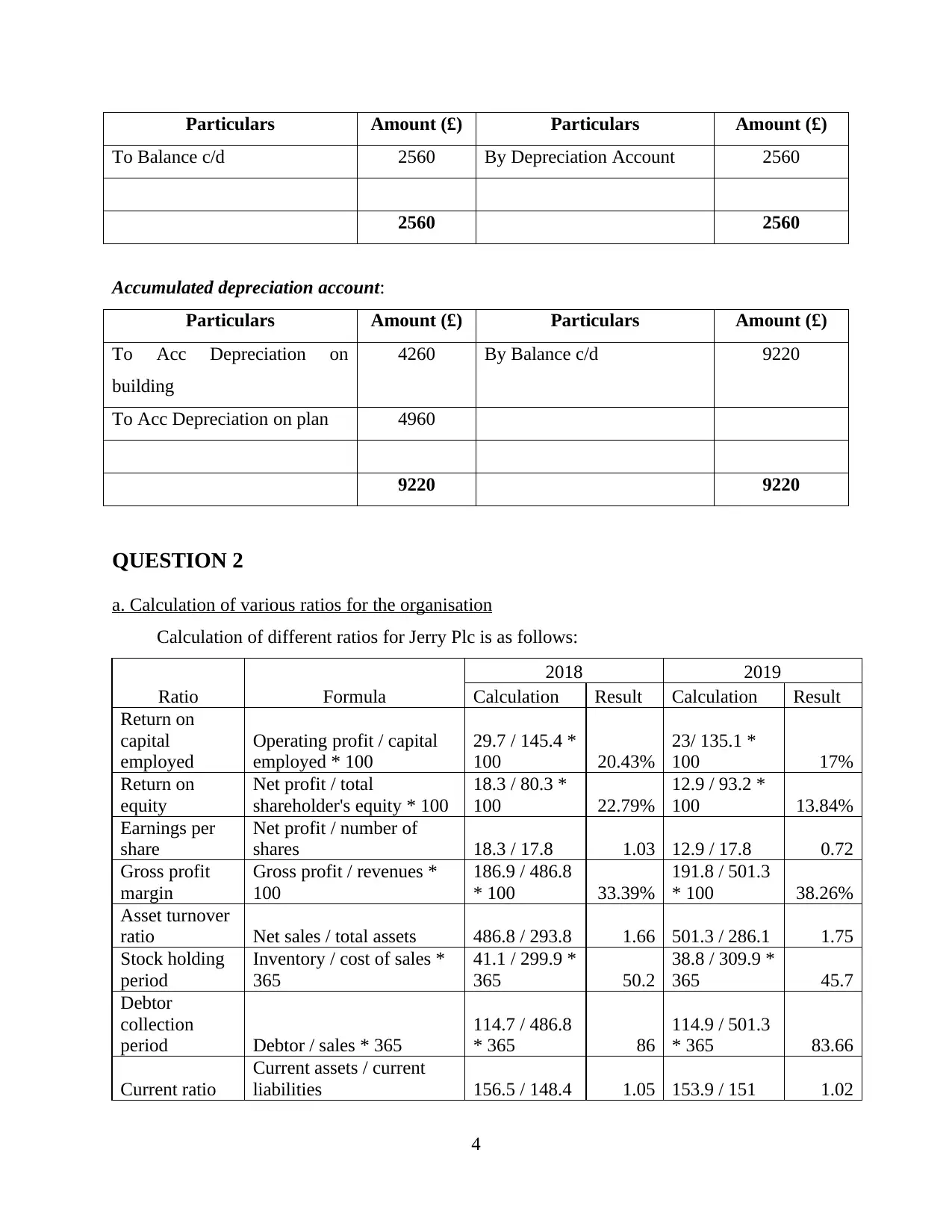

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 2560 By Depreciation Account 2560

2560 2560

Accumulated depreciation account:

Particulars Amount (£) Particulars Amount (£)

To Acc Depreciation on

building

4260 By Balance c/d 9220

To Acc Depreciation on plan 4960

9220 9220

QUESTION 2

a. Calculation of various ratios for the organisation

Calculation of different ratios for Jerry Plc is as follows:

Ratio Formula

2018 2019

Calculation Result Calculation Result

Return on

capital

employed

Operating profit / capital

employed * 100

29.7 / 145.4 *

100 20.43%

23/ 135.1 *

100 17%

Return on

equity

Net profit / total

shareholder's equity * 100

18.3 / 80.3 *

100 22.79%

12.9 / 93.2 *

100 13.84%

Earnings per

share

Net profit / number of

shares 18.3 / 17.8 1.03 12.9 / 17.8 0.72

Gross profit

margin

Gross profit / revenues *

100

186.9 / 486.8

* 100 33.39%

191.8 / 501.3

* 100 38.26%

Asset turnover

ratio Net sales / total assets 486.8 / 293.8 1.66 501.3 / 286.1 1.75

Stock holding

period

Inventory / cost of sales *

365

41.1 / 299.9 *

365 50.2

38.8 / 309.9 *

365 45.7

Debtor

collection

period Debtor / sales * 365

114.7 / 486.8

* 365 86

114.9 / 501.3

* 365 83.66

Current ratio

Current assets / current

liabilities 156.5 / 148.4 1.05 153.9 / 151 1.02

4

To Balance c/d 2560 By Depreciation Account 2560

2560 2560

Accumulated depreciation account:

Particulars Amount (£) Particulars Amount (£)

To Acc Depreciation on

building

4260 By Balance c/d 9220

To Acc Depreciation on plan 4960

9220 9220

QUESTION 2

a. Calculation of various ratios for the organisation

Calculation of different ratios for Jerry Plc is as follows:

Ratio Formula

2018 2019

Calculation Result Calculation Result

Return on

capital

employed

Operating profit / capital

employed * 100

29.7 / 145.4 *

100 20.43%

23/ 135.1 *

100 17%

Return on

equity

Net profit / total

shareholder's equity * 100

18.3 / 80.3 *

100 22.79%

12.9 / 93.2 *

100 13.84%

Earnings per

share

Net profit / number of

shares 18.3 / 17.8 1.03 12.9 / 17.8 0.72

Gross profit

margin

Gross profit / revenues *

100

186.9 / 486.8

* 100 33.39%

191.8 / 501.3

* 100 38.26%

Asset turnover

ratio Net sales / total assets 486.8 / 293.8 1.66 501.3 / 286.1 1.75

Stock holding

period

Inventory / cost of sales *

365

41.1 / 299.9 *

365 50.2

38.8 / 309.9 *

365 45.7

Debtor

collection

period Debtor / sales * 365

114.7 / 486.8

* 365 86

114.9 / 501.3

* 365 83.66

Current ratio

Current assets / current

liabilities 156.5 / 148.4 1.05 153.9 / 151 1.02

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

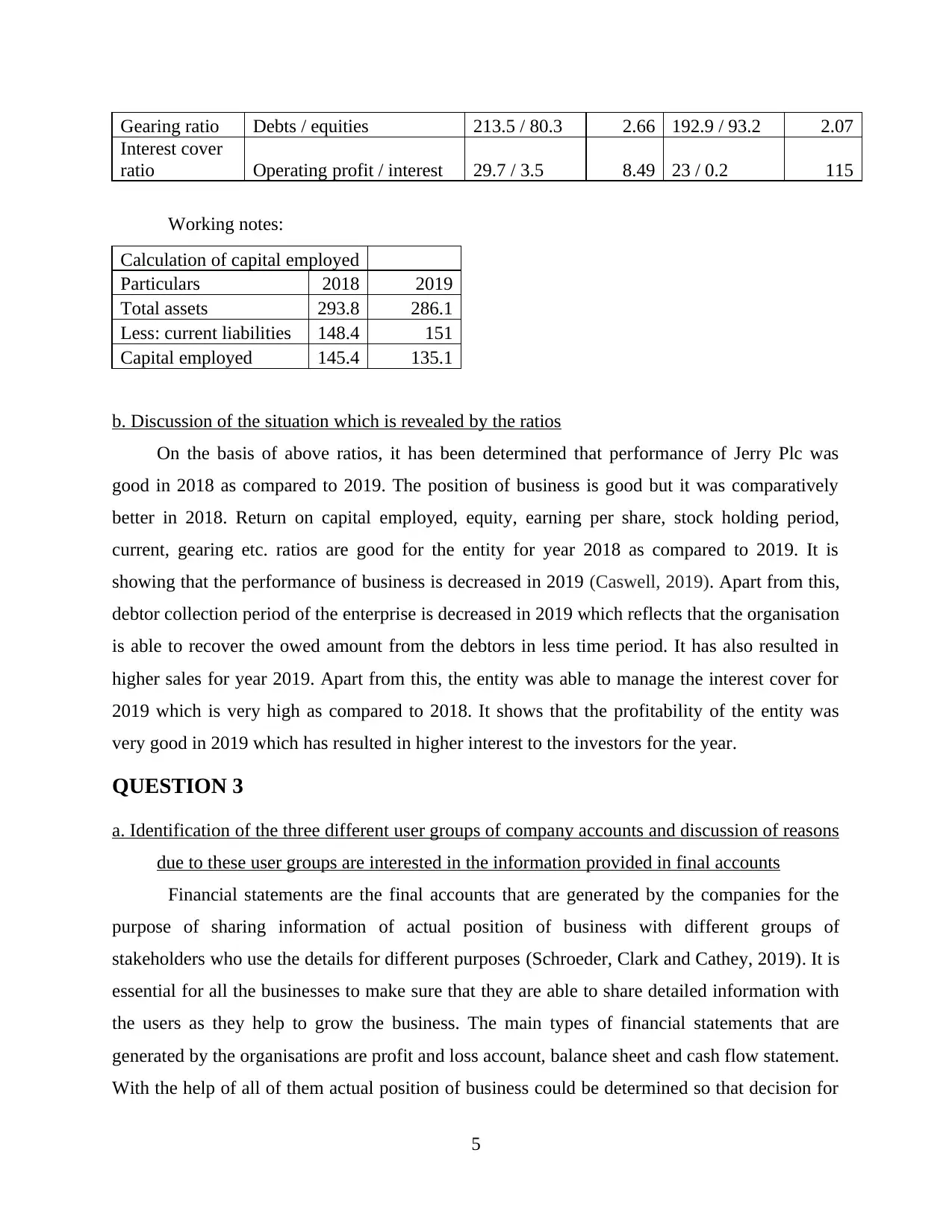

Gearing ratio Debts / equities 213.5 / 80.3 2.66 192.9 / 93.2 2.07

Interest cover

ratio Operating profit / interest 29.7 / 3.5 8.49 23 / 0.2 115

Working notes:

Calculation of capital employed

Particulars 2018 2019

Total assets 293.8 286.1

Less: current liabilities 148.4 151

Capital employed 145.4 135.1

b. Discussion of the situation which is revealed by the ratios

On the basis of above ratios, it has been determined that performance of Jerry Plc was

good in 2018 as compared to 2019. The position of business is good but it was comparatively

better in 2018. Return on capital employed, equity, earning per share, stock holding period,

current, gearing etc. ratios are good for the entity for year 2018 as compared to 2019. It is

showing that the performance of business is decreased in 2019 (Caswell, 2019). Apart from this,

debtor collection period of the enterprise is decreased in 2019 which reflects that the organisation

is able to recover the owed amount from the debtors in less time period. It has also resulted in

higher sales for year 2019. Apart from this, the entity was able to manage the interest cover for

2019 which is very high as compared to 2018. It shows that the profitability of the entity was

very good in 2019 which has resulted in higher interest to the investors for the year.

QUESTION 3

a. Identification of the three different user groups of company accounts and discussion of reasons

due to these user groups are interested in the information provided in final accounts

Financial statements are the final accounts that are generated by the companies for the

purpose of sharing information of actual position of business with different groups of

stakeholders who use the details for different purposes (Schroeder, Clark and Cathey, 2019). It is

essential for all the businesses to make sure that they are able to share detailed information with

the users as they help to grow the business. The main types of financial statements that are

generated by the organisations are profit and loss account, balance sheet and cash flow statement.

With the help of all of them actual position of business could be determined so that decision for

5

Interest cover

ratio Operating profit / interest 29.7 / 3.5 8.49 23 / 0.2 115

Working notes:

Calculation of capital employed

Particulars 2018 2019

Total assets 293.8 286.1

Less: current liabilities 148.4 151

Capital employed 145.4 135.1

b. Discussion of the situation which is revealed by the ratios

On the basis of above ratios, it has been determined that performance of Jerry Plc was

good in 2018 as compared to 2019. The position of business is good but it was comparatively

better in 2018. Return on capital employed, equity, earning per share, stock holding period,

current, gearing etc. ratios are good for the entity for year 2018 as compared to 2019. It is

showing that the performance of business is decreased in 2019 (Caswell, 2019). Apart from this,

debtor collection period of the enterprise is decreased in 2019 which reflects that the organisation

is able to recover the owed amount from the debtors in less time period. It has also resulted in

higher sales for year 2019. Apart from this, the entity was able to manage the interest cover for

2019 which is very high as compared to 2018. It shows that the profitability of the entity was

very good in 2019 which has resulted in higher interest to the investors for the year.

QUESTION 3

a. Identification of the three different user groups of company accounts and discussion of reasons

due to these user groups are interested in the information provided in final accounts

Financial statements are the final accounts that are generated by the companies for the

purpose of sharing information of actual position of business with different groups of

stakeholders who use the details for different purposes (Schroeder, Clark and Cathey, 2019). It is

essential for all the businesses to make sure that they are able to share detailed information with

the users as they help to grow the business. The main types of financial statements that are

generated by the organisations are profit and loss account, balance sheet and cash flow statement.

With the help of all of them actual position of business could be determined so that decision for

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

future could be formulated (Nichols, Wahlen and Wieland, 2017). There are various groups of

users who are interested in the information provided by final accounts. Three main groups from

all of them are described below:

Internal users: All the users of final accounts that are linked with the entity internally

are known as internal stakeholders. They use financial statements to analyse the performance of

company so that different types of decisions could be formed by them. Some of the internal users

are employees and managers. They are interested in the information of financial statements for

different purposes. Staff members use the information to analyse that they are working in a

financially strong company or not. Managers are mainly responsible for formulating of effective

strategies so that they can enhance performance of business and it is one of the main reasons sue

to which they are interested in the information of final accounts.

External users: All the outsider parties which external parts of the business are known as

external stakeholders. They use the financial statements to assess the market position of company

so that they can make further decisions (Patel, 2018). Some of them are creditors, investors,

government, customers etc. All of them are interested in the financial statements for different

purposes. Creditors use them to analyse credibility of business and investors use them to analyse

the ability of business to provide goods returns to them of their funds. Apart from this,

governmental parties use the final accounts of companies to make sure that right tax is paid by

the businesses or not and the business is executed in ethical manner or not. Customers use final

accounts to analyse that they are buying products from a financially strong or weak enterprise.

Board member: These are one of the main users of financial statements because they are

highly interested in the performance of business and they are also focused with decision making

in context of betterment of the entity. All the shareholders, directors, CEO etc. are part f this

group. They are interested in the information of final accounts because it is their responsibility to

run the business properly and for this purpose, they need to analyse actual position of company.

b. Discussion of the advantages and disadvantages of highly regulated financial reporting regime

Highly regulated financial reporting regime is very beneficial for all the businesses as well

as the users of final accounts because with the help of it, accurate information could be recorded

in the books of accounting. There are various advantages and disadvantages of it for users as

well as the preparer and all of them could be understood with the help of following discussion:

Advantages:

6

users who are interested in the information provided by final accounts. Three main groups from

all of them are described below:

Internal users: All the users of final accounts that are linked with the entity internally

are known as internal stakeholders. They use financial statements to analyse the performance of

company so that different types of decisions could be formed by them. Some of the internal users

are employees and managers. They are interested in the information of financial statements for

different purposes. Staff members use the information to analyse that they are working in a

financially strong company or not. Managers are mainly responsible for formulating of effective

strategies so that they can enhance performance of business and it is one of the main reasons sue

to which they are interested in the information of final accounts.

External users: All the outsider parties which external parts of the business are known as

external stakeholders. They use the financial statements to assess the market position of company

so that they can make further decisions (Patel, 2018). Some of them are creditors, investors,

government, customers etc. All of them are interested in the financial statements for different

purposes. Creditors use them to analyse credibility of business and investors use them to analyse

the ability of business to provide goods returns to them of their funds. Apart from this,

governmental parties use the final accounts of companies to make sure that right tax is paid by

the businesses or not and the business is executed in ethical manner or not. Customers use final

accounts to analyse that they are buying products from a financially strong or weak enterprise.

Board member: These are one of the main users of financial statements because they are

highly interested in the performance of business and they are also focused with decision making

in context of betterment of the entity. All the shareholders, directors, CEO etc. are part f this

group. They are interested in the information of final accounts because it is their responsibility to

run the business properly and for this purpose, they need to analyse actual position of company.

b. Discussion of the advantages and disadvantages of highly regulated financial reporting regime

Highly regulated financial reporting regime is very beneficial for all the businesses as well

as the users of final accounts because with the help of it, accurate information could be recorded

in the books of accounting. There are various advantages and disadvantages of it for users as

well as the preparer and all of them could be understood with the help of following discussion:

Advantages:

6

When highly regulated financial reporting regime will be followed by preparers then they

will be able to attract more and more investors because it will result in transparent and

accurate information the final accounts.

When highly regulated financial reporting regime will be followed by the entity then it

will be beneficial for users such as creditors and investors as it will help them to

determine that company will be able to repay their amount on time or not (Ward and

Calabrese, 2018).

Disadvantages:

The rules and regulations that are focused by highly regulated financial reporting regime

are very strict so if the preparers will make a small mistake unknowingly then it may

result in bad impact upon the market image of business.

One of the drawbacks of highly regulated financial reporting regime for the users is that it

may result in difficulty for them to understand the information of final accounts because

of different rules.

c. Discussion of the limitations of financial statements

Financial statements are prepared by all the entities to evaluate their actual position. There

are various limitations of them which are as follows:

All the final accounts are highly dependent upon the historical costs due to which actual

value of the business could not be determined by the stakeholders.

There is no discussion or assessment possible for non-financial issues with the help of

financial statements (Wright, 2017).

Slight changes in the rules regarding financial reporting may result in changes in whole

financial statements which may affect the accuracy of the accounts.

The possibility of making fraud in the financial statements is high because all of them

could be biased easily by the management teams.

CONCLUSION

From the above discussion it has been observed that accounting is the process of reporting

business transactions linked to a corporation. The accounting method involves the processing,

review and reporting of these activities to supervisory authorities, authorities and tax collecting

bodies. Accounting Financial Statements are a succinct description of financial activities over a

7

will be able to attract more and more investors because it will result in transparent and

accurate information the final accounts.

When highly regulated financial reporting regime will be followed by the entity then it

will be beneficial for users such as creditors and investors as it will help them to

determine that company will be able to repay their amount on time or not (Ward and

Calabrese, 2018).

Disadvantages:

The rules and regulations that are focused by highly regulated financial reporting regime

are very strict so if the preparers will make a small mistake unknowingly then it may

result in bad impact upon the market image of business.

One of the drawbacks of highly regulated financial reporting regime for the users is that it

may result in difficulty for them to understand the information of final accounts because

of different rules.

c. Discussion of the limitations of financial statements

Financial statements are prepared by all the entities to evaluate their actual position. There

are various limitations of them which are as follows:

All the final accounts are highly dependent upon the historical costs due to which actual

value of the business could not be determined by the stakeholders.

There is no discussion or assessment possible for non-financial issues with the help of

financial statements (Wright, 2017).

Slight changes in the rules regarding financial reporting may result in changes in whole

financial statements which may affect the accuracy of the accounts.

The possibility of making fraud in the financial statements is high because all of them

could be biased easily by the management teams.

CONCLUSION

From the above discussion it has been observed that accounting is the process of reporting

business transactions linked to a corporation. The accounting method involves the processing,

review and reporting of these activities to supervisory authorities, authorities and tax collecting

bodies. Accounting Financial Statements are a succinct description of financial activities over a

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial period, outlining the revenues, financial status and cash flows of a corporation. It plays

a crucial role in running a business successfully, as it lets the managers to track revenue and

expense, guarantees regulatory enforcement, and offers detailed financial reports for creditors,

managers, and government that can be used to make strategic decisions. This report concluded

that there are three main documents which are essential to prepared by the managers to make

effective strategies. Income statement helps in evaluating company’s overall expenses and

income; balance sheet shows the financial position of the company which helps investors to

make their financial decisions on the basis of it. In addition, ratio analysis helps the Jerry Plc to

evaluate their company’s performances in terms of profitability, liquidity, efficiency etc. Internal

as well as external parties are interested in the financial report of the company which allow

managers to make strategic decisions and stakeholders to understand that operating business

generate profit or not. There are several advantages or disadvantages which financial reporting

which are essential to evaluate before making any strategy.

8

a crucial role in running a business successfully, as it lets the managers to track revenue and

expense, guarantees regulatory enforcement, and offers detailed financial reports for creditors,

managers, and government that can be used to make strategic decisions. This report concluded

that there are three main documents which are essential to prepared by the managers to make

effective strategies. Income statement helps in evaluating company’s overall expenses and

income; balance sheet shows the financial position of the company which helps investors to

make their financial decisions on the basis of it. In addition, ratio analysis helps the Jerry Plc to

evaluate their company’s performances in terms of profitability, liquidity, efficiency etc. Internal

as well as external parties are interested in the financial report of the company which allow

managers to make strategic decisions and stakeholders to understand that operating business

generate profit or not. There are several advantages or disadvantages which financial reporting

which are essential to evaluate before making any strategy.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Burger, M. and Curtis, A., 2017. Aggregate margin debt and the divergence of price from

accounting fundamentals. Contemporary Accounting Research. 34(3). pp.1418-1445.

Cai, C. W., 2019. Triple‐entry accounting with blockchain: How far have we come?. Accounting

& Finance.

Caswell, S., 2019. An Analysis of Financial Accounting Fundamentals Through Case Studies.

Nichols, D. C., Wahlen, J. M. and Wieland, M. M., 2017. Pricing and Mispricing of Accounting

Fundamentals in the Time‐Series and in the Cross Section. Contemporary Accounting

Research. 34(3). pp.1378-1417.

Patel, K., 2018. Explaining value vs. growth investing through accounting

fundamentals. Financial Analysts Journal. 74(4). pp.31-32.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Smith, M., 2019. Research methods in accounting. SAGE Publications Limited.

Tkhagapso, R., 2019, October. Transformation of Fundamental Accounting Principles in the

Context of a Company Insolvency from the Perspective of the Digital Economy. In The

2018 International Conference on Digital Science (pp. 75-85). Springer, Cham.

Ward, D. M. and Calabrese, T., 2018. Accounting fundamentals for health care management.

Jones & Bartlett Learning.

Wright, C. J., 2017. Fundamentals of oil & gas accounting. PennWell Books.

9

Books & Journals

Burger, M. and Curtis, A., 2017. Aggregate margin debt and the divergence of price from

accounting fundamentals. Contemporary Accounting Research. 34(3). pp.1418-1445.

Cai, C. W., 2019. Triple‐entry accounting with blockchain: How far have we come?. Accounting

& Finance.

Caswell, S., 2019. An Analysis of Financial Accounting Fundamentals Through Case Studies.

Nichols, D. C., Wahlen, J. M. and Wieland, M. M., 2017. Pricing and Mispricing of Accounting

Fundamentals in the Time‐Series and in the Cross Section. Contemporary Accounting

Research. 34(3). pp.1378-1417.

Patel, K., 2018. Explaining value vs. growth investing through accounting

fundamentals. Financial Analysts Journal. 74(4). pp.31-32.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Smith, M., 2019. Research methods in accounting. SAGE Publications Limited.

Tkhagapso, R., 2019, October. Transformation of Fundamental Accounting Principles in the

Context of a Company Insolvency from the Perspective of the Digital Economy. In The

2018 International Conference on Digital Science (pp. 75-85). Springer, Cham.

Ward, D. M. and Calabrese, T., 2018. Accounting fundamentals for health care management.

Jones & Bartlett Learning.

Wright, C. J., 2017. Fundamentals of oil & gas accounting. PennWell Books.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.