Accounting Fundamentals: Financial Statements, Ratios, and Analysis

VerifiedAdded on 2023/06/18

|17

|2407

|188

AI Summary

This article covers the basics of accounting fundamentals, including financial statements, balance sheets, and income statements. It also includes a detailed analysis of financial ratios for Chocco plc, a chocolate and confectionery manufacturer. The article provides insights into the company's profitability, liquidity, and efficiency, along with suggestions for future development. The subject is Accounting, and the course code is not mentioned. The article is relevant for students studying accounting in any college or university.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING

FUNDAMENTALS

FUNDAMENTALS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION- 1.................................................................................................................................3

a) Financial statements of Kedison PLC.....................................................................................3

b) Reason for balancing of the statement of financial position...................................................6

QUESTION- 2.................................................................................................................................6

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION- 1.................................................................................................................................3

a) Financial statements of Kedison PLC.....................................................................................3

b) Reason for balancing of the statement of financial position...................................................6

QUESTION- 2.................................................................................................................................6

REFERENCES..............................................................................................................................17

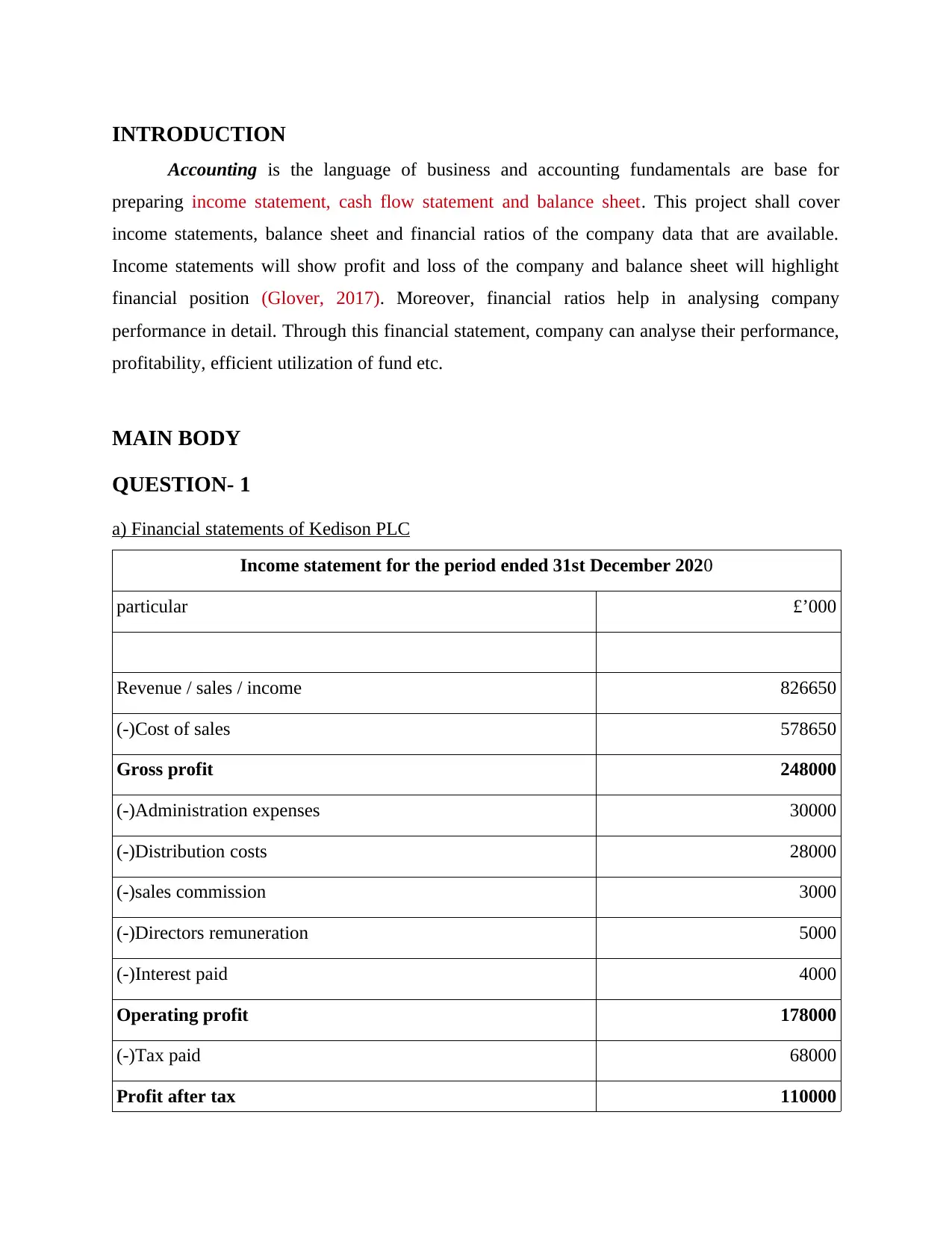

INTRODUCTION

Accounting is the language of business and accounting fundamentals are base for

preparing income statement, cash flow statement and balance sheet. This project shall cover

income statements, balance sheet and financial ratios of the company data that are available.

Income statements will show profit and loss of the company and balance sheet will highlight

financial position (Glover, 2017). Moreover, financial ratios help in analysing company

performance in detail. Through this financial statement, company can analyse their performance,

profitability, efficient utilization of fund etc.

MAIN BODY

QUESTION- 1

a) Financial statements of Kedison PLC

Income statement for the period ended 31st December 2020

particular £’000

Revenue / sales / income 826650

(-)Cost of sales 578650

Gross profit 248000

(-)Administration expenses 30000

(-)Distribution costs 28000

(-)sales commission 3000

(-)Directors remuneration 5000

(-)Interest paid 4000

Operating profit 178000

(-)Tax paid 68000

Profit after tax 110000

Accounting is the language of business and accounting fundamentals are base for

preparing income statement, cash flow statement and balance sheet. This project shall cover

income statements, balance sheet and financial ratios of the company data that are available.

Income statements will show profit and loss of the company and balance sheet will highlight

financial position (Glover, 2017). Moreover, financial ratios help in analysing company

performance in detail. Through this financial statement, company can analyse their performance,

profitability, efficient utilization of fund etc.

MAIN BODY

QUESTION- 1

a) Financial statements of Kedison PLC

Income statement for the period ended 31st December 2020

particular £’000

Revenue / sales / income 826650

(-)Cost of sales 578650

Gross profit 248000

(-)Administration expenses 30000

(-)Distribution costs 28000

(-)sales commission 3000

(-)Directors remuneration 5000

(-)Interest paid 4000

Operating profit 178000

(-)Tax paid 68000

Profit after tax 110000

(-) preference dividend 30000

Amount for equity shareholder 80000

(-)ordinary dividend 20000

Retained earnings 60000

Financial position as on 31st December 2020

particular £’000

Assets

Plant and equipment 632730

debtors 171105

Cash and bank 12900

stock 329620

Total assets 1146355

Liabilities

long term liabilities

4% debenture 100000

Current liabilities

Trade creditors 171355

Outstanding commission 3000

Amount for equity shareholder 80000

(-)ordinary dividend 20000

Retained earnings 60000

Financial position as on 31st December 2020

particular £’000

Assets

Plant and equipment 632730

debtors 171105

Cash and bank 12900

stock 329620

Total assets 1146355

Liabilities

long term liabilities

4% debenture 100000

Current liabilities

Trade creditors 171355

Outstanding commission 3000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

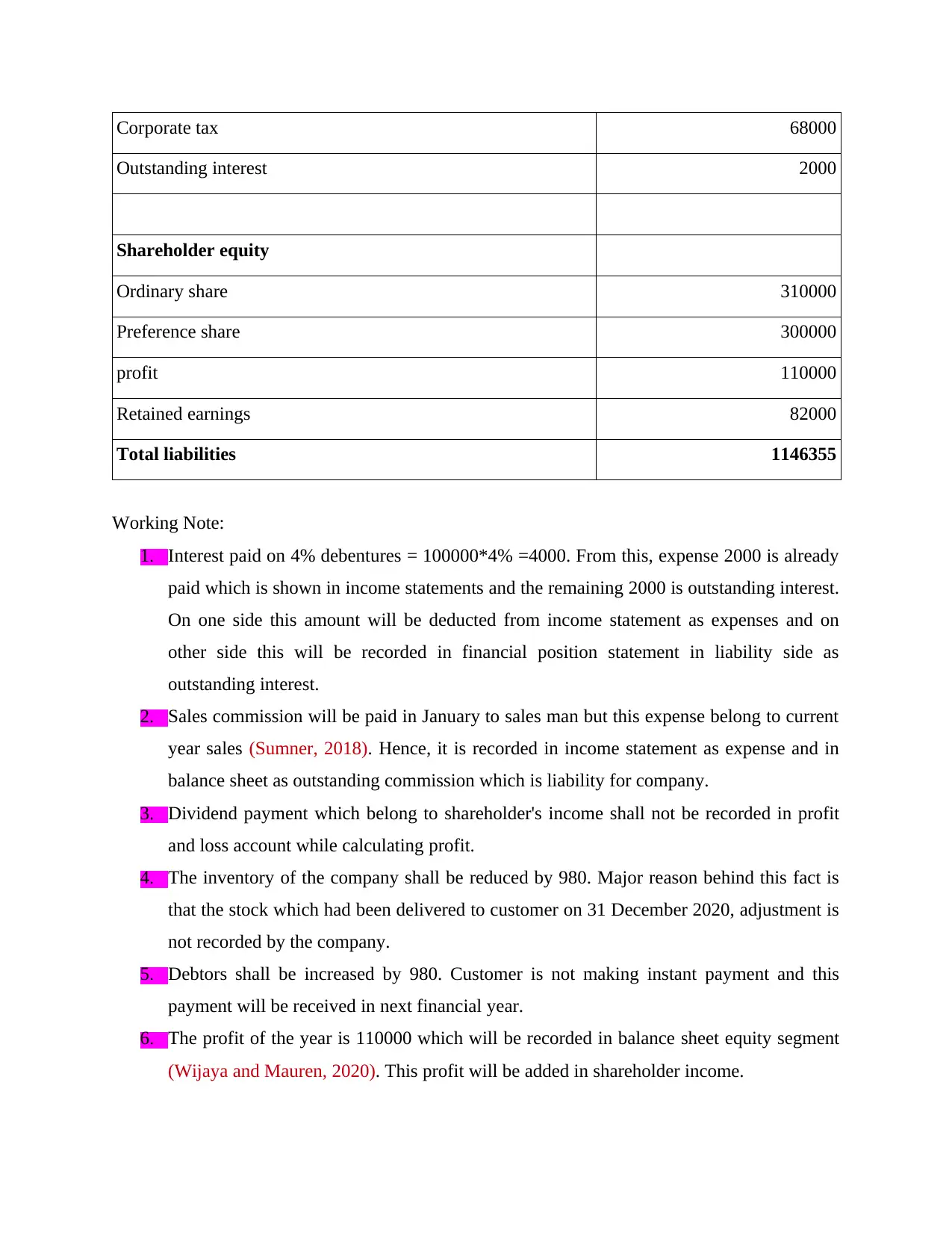

Corporate tax 68000

Outstanding interest 2000

Shareholder equity

Ordinary share 310000

Preference share 300000

profit 110000

Retained earnings 82000

Total liabilities 1146355

Working Note:

1. Interest paid on 4% debentures = 100000*4% =4000. From this, expense 2000 is already

paid which is shown in income statements and the remaining 2000 is outstanding interest.

On one side this amount will be deducted from income statement as expenses and on

other side this will be recorded in financial position statement in liability side as

outstanding interest.

2. Sales commission will be paid in January to sales man but this expense belong to current

year sales (Sumner, 2018). Hence, it is recorded in income statement as expense and in

balance sheet as outstanding commission which is liability for company.

3. Dividend payment which belong to shareholder's income shall not be recorded in profit

and loss account while calculating profit.

4. The inventory of the company shall be reduced by 980. Major reason behind this fact is

that the stock which had been delivered to customer on 31 December 2020, adjustment is

not recorded by the company.

5. Debtors shall be increased by 980. Customer is not making instant payment and this

payment will be received in next financial year.

6. The profit of the year is 110000 which will be recorded in balance sheet equity segment

(Wijaya and Mauren, 2020). This profit will be added in shareholder income.

Outstanding interest 2000

Shareholder equity

Ordinary share 310000

Preference share 300000

profit 110000

Retained earnings 82000

Total liabilities 1146355

Working Note:

1. Interest paid on 4% debentures = 100000*4% =4000. From this, expense 2000 is already

paid which is shown in income statements and the remaining 2000 is outstanding interest.

On one side this amount will be deducted from income statement as expenses and on

other side this will be recorded in financial position statement in liability side as

outstanding interest.

2. Sales commission will be paid in January to sales man but this expense belong to current

year sales (Sumner, 2018). Hence, it is recorded in income statement as expense and in

balance sheet as outstanding commission which is liability for company.

3. Dividend payment which belong to shareholder's income shall not be recorded in profit

and loss account while calculating profit.

4. The inventory of the company shall be reduced by 980. Major reason behind this fact is

that the stock which had been delivered to customer on 31 December 2020, adjustment is

not recorded by the company.

5. Debtors shall be increased by 980. Customer is not making instant payment and this

payment will be received in next financial year.

6. The profit of the year is 110000 which will be recorded in balance sheet equity segment

(Wijaya and Mauren, 2020). This profit will be added in shareholder income.

7. Retain earnings shall be used for dividend payment which are deducted from current year

retain earnings that is 132000-50000= 82000. This shall be paid 30000 to preference

shareholder and 20000 will to equity shareholder as dividend. So remaining 82000 shall

be recorded in balance sheet equity segment.

8. Corporate tax shall be paid, which is deducted from profit before tax (EBT) and on the

other side this shall be shown in balance sheet liabilities segment.

b) Reason for balancing of the statement of financial position

Accounting equation is known as base for double entry system in which assets is equivalent to

liabilities and shareholder equity. Balance sheet is based on this equation where one is assets side

and other is liabilities side to prove this equation, it needs to be balanced (Witczak and Zimny,

2021). Double entry system ensure that each entry has double aspect one is on debit side and

other is on credit side. This equation of accounting ensure that both the side of balance sheet are

equal and in addition to it also shows that how company is procuring and deploying the fund.

The accounting equation is also called as error detection tool because whenever debit accounts is

not equal to credit accounts means there is an error.

QUESTION- 2

Financial Ratio analysis of Chocco plc, A chocolate and confectionery manufacture

Financial Ratios

s.

no particular formulas 2020 2019

1

Return on capital

employed

Earnings before interest and tax / capital

employed 11.71% 10.23%

Earnings before interest

and tax 846 720

Capital employed Total assets- current liabilities 7225 7041

retain earnings that is 132000-50000= 82000. This shall be paid 30000 to preference

shareholder and 20000 will to equity shareholder as dividend. So remaining 82000 shall

be recorded in balance sheet equity segment.

8. Corporate tax shall be paid, which is deducted from profit before tax (EBT) and on the

other side this shall be shown in balance sheet liabilities segment.

b) Reason for balancing of the statement of financial position

Accounting equation is known as base for double entry system in which assets is equivalent to

liabilities and shareholder equity. Balance sheet is based on this equation where one is assets side

and other is liabilities side to prove this equation, it needs to be balanced (Witczak and Zimny,

2021). Double entry system ensure that each entry has double aspect one is on debit side and

other is on credit side. This equation of accounting ensure that both the side of balance sheet are

equal and in addition to it also shows that how company is procuring and deploying the fund.

The accounting equation is also called as error detection tool because whenever debit accounts is

not equal to credit accounts means there is an error.

QUESTION- 2

Financial Ratio analysis of Chocco plc, A chocolate and confectionery manufacture

Financial Ratios

s.

no particular formulas 2020 2019

1

Return on capital

employed

Earnings before interest and tax / capital

employed 11.71% 10.23%

Earnings before interest

and tax 846 720

Capital employed Total assets- current liabilities 7225 7041

0.09

0.095

0.1

0.105

0.11

0.115

0.12

RETURN ON CAPITAL EMPLOYED

2020

2019

YEAR

PERCENTAGE

Interpretation:

Return on capital employed ratio is used to measure profitability of the company means how

efficiently company is utilizing their fund to generate profit. As above calculation, it has shown

that earning of the company increased by 1.48% means company is attractively using fund in

order to increase profit (Huo and et.al., 2018). It can be improved more by selling off

unprofitable assets or by paying off debt, inventory management etc.

2 Return on equity Net income / shareholder's equity 13.96% 12.57%

Net income 431 366

Shareholder's equity 3088 2912

0.095

0.1

0.105

0.11

0.115

0.12

RETURN ON CAPITAL EMPLOYED

2020

2019

YEAR

PERCENTAGE

Interpretation:

Return on capital employed ratio is used to measure profitability of the company means how

efficiently company is utilizing their fund to generate profit. As above calculation, it has shown

that earning of the company increased by 1.48% means company is attractively using fund in

order to increase profit (Huo and et.al., 2018). It can be improved more by selling off

unprofitable assets or by paying off debt, inventory management etc.

2 Return on equity Net income / shareholder's equity 13.96% 12.57%

Net income 431 366

Shareholder's equity 3088 2912

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.052

0.054

0.056

0.058

0.06

0.062

0.064

RETURN ON EQUITY

2020

2019

YEAR

PERCENTAGE

Interpretation:

Return on equity ratio is used to measure profitability of company in respect to equity. This ratio

ensures that how well equity fund is utilizing to get more profit. From the above calculation, it

has shown that company is efficiently utilizing their capital and this ratio is increased by 1.39%

from 2019 to 2020 which is good for the company (Felber, Campos and Sanchis, 2019 ). This

ratio can be improved by reducing cost or by raise the price of the product, investing idle cash,

use financial leverage to increase profitability.

3 Earnings per share Net profit / No. Of equity shares 0.72 0.61

Net profit 431 366

No. Of outstanding share 600 600

0.054

0.056

0.058

0.06

0.062

0.064

RETURN ON EQUITY

2020

2019

YEAR

PERCENTAGE

Interpretation:

Return on equity ratio is used to measure profitability of company in respect to equity. This ratio

ensures that how well equity fund is utilizing to get more profit. From the above calculation, it

has shown that company is efficiently utilizing their capital and this ratio is increased by 1.39%

from 2019 to 2020 which is good for the company (Felber, Campos and Sanchis, 2019 ). This

ratio can be improved by reducing cost or by raise the price of the product, investing idle cash,

use financial leverage to increase profitability.

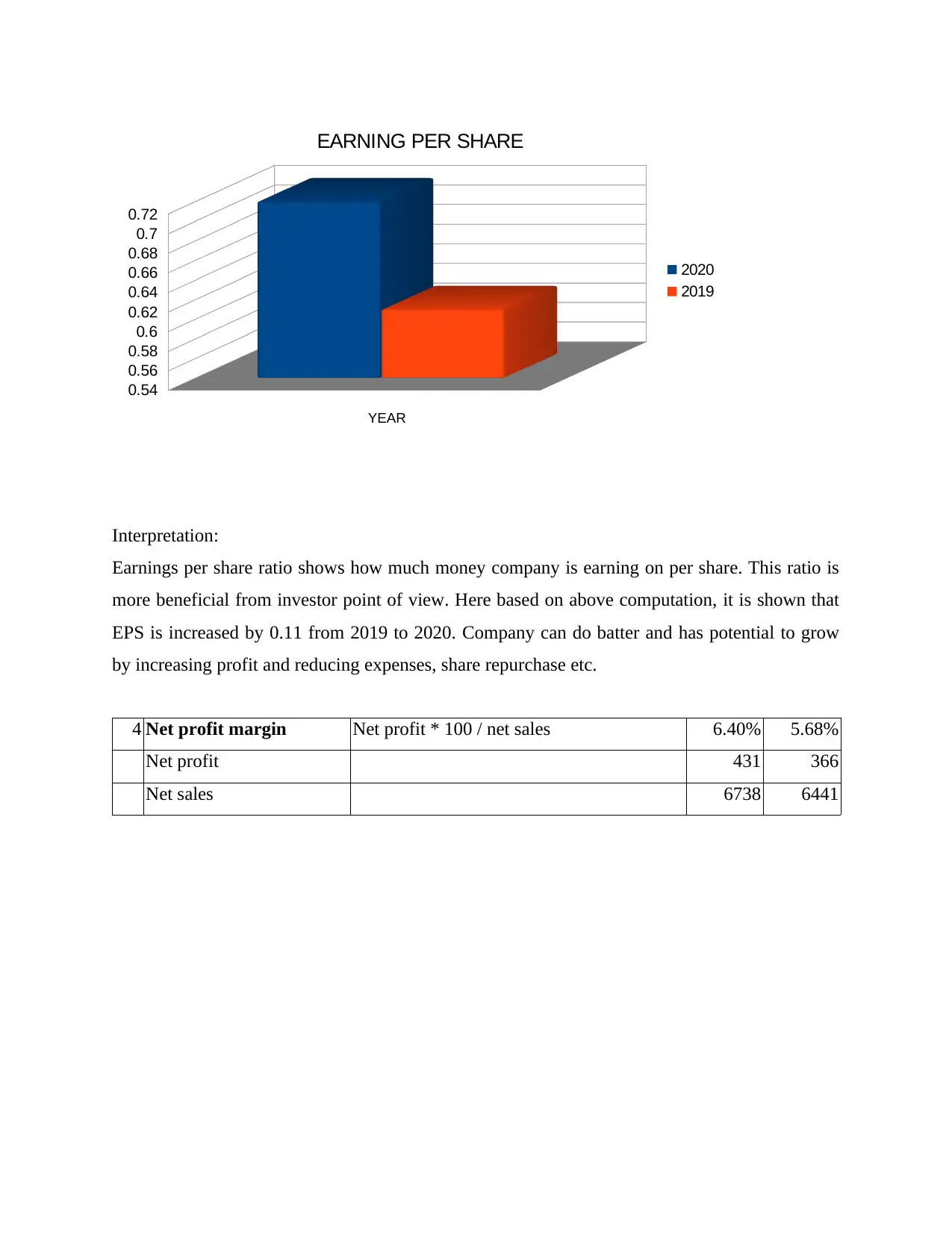

3 Earnings per share Net profit / No. Of equity shares 0.72 0.61

Net profit 431 366

No. Of outstanding share 600 600

0.54

0.56

0.58

0.6

0.62

0.64

0.66

0.68

0.7

0.72

EARNING PER SHARE

2020

2019

YEAR

Interpretation:

Earnings per share ratio shows how much money company is earning on per share. This ratio is

more beneficial from investor point of view. Here based on above computation, it is shown that

EPS is increased by 0.11 from 2019 to 2020. Company can do batter and has potential to grow

by increasing profit and reducing expenses, share repurchase etc.

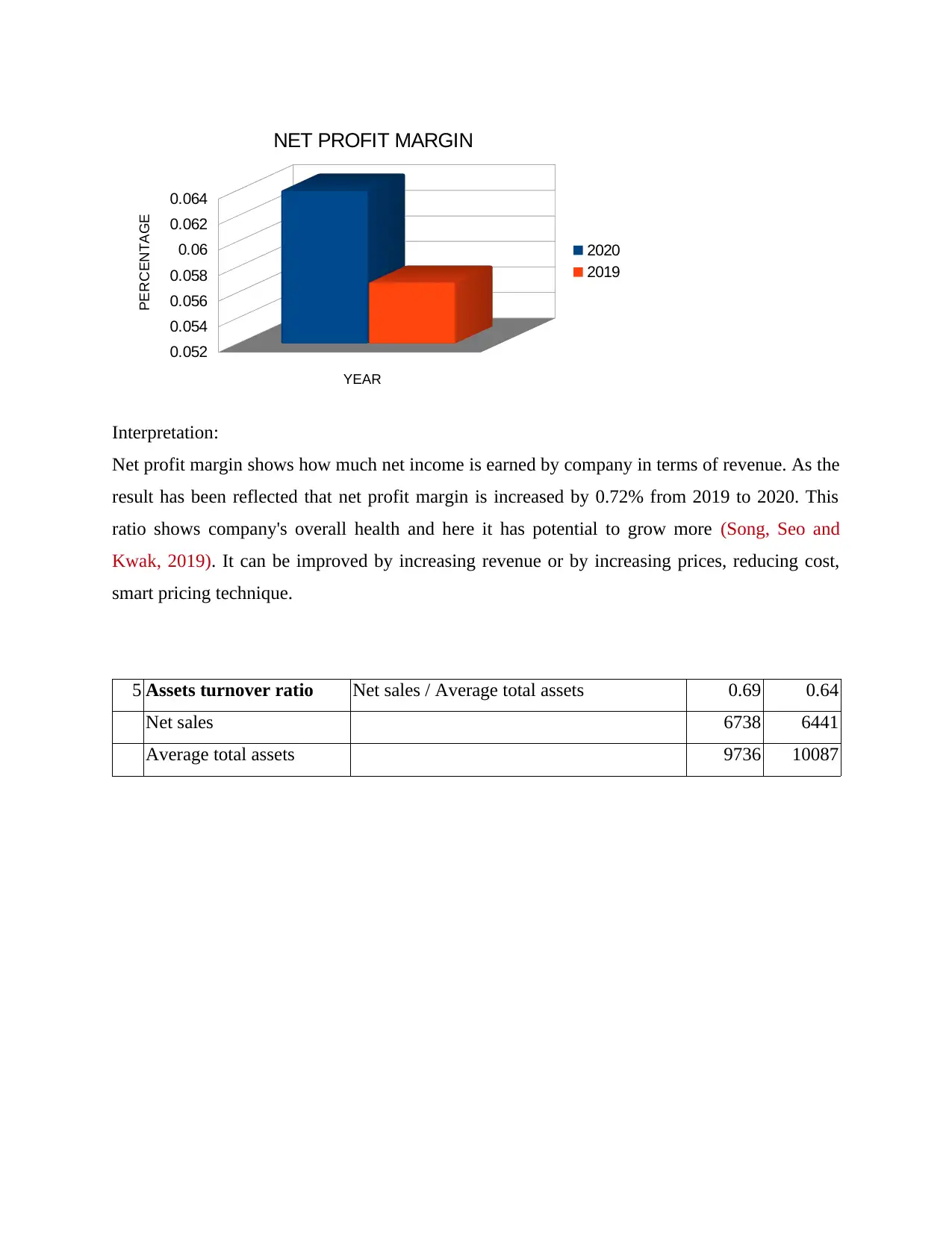

4 Net profit margin Net profit * 100 / net sales 6.40% 5.68%

Net profit 431 366

Net sales 6738 6441

0.56

0.58

0.6

0.62

0.64

0.66

0.68

0.7

0.72

EARNING PER SHARE

2020

2019

YEAR

Interpretation:

Earnings per share ratio shows how much money company is earning on per share. This ratio is

more beneficial from investor point of view. Here based on above computation, it is shown that

EPS is increased by 0.11 from 2019 to 2020. Company can do batter and has potential to grow

by increasing profit and reducing expenses, share repurchase etc.

4 Net profit margin Net profit * 100 / net sales 6.40% 5.68%

Net profit 431 366

Net sales 6738 6441

0.052

0.054

0.056

0.058

0.06

0.062

0.064

NET PROFIT MARGIN

2020

2019

YEAR

PERCENTAGE

Interpretation:

Net profit margin shows how much net income is earned by company in terms of revenue. As the

result has been reflected that net profit margin is increased by 0.72% from 2019 to 2020. This

ratio shows company's overall health and here it has potential to grow more (Song, Seo and

Kwak, 2019). It can be improved by increasing revenue or by increasing prices, reducing cost,

smart pricing technique.

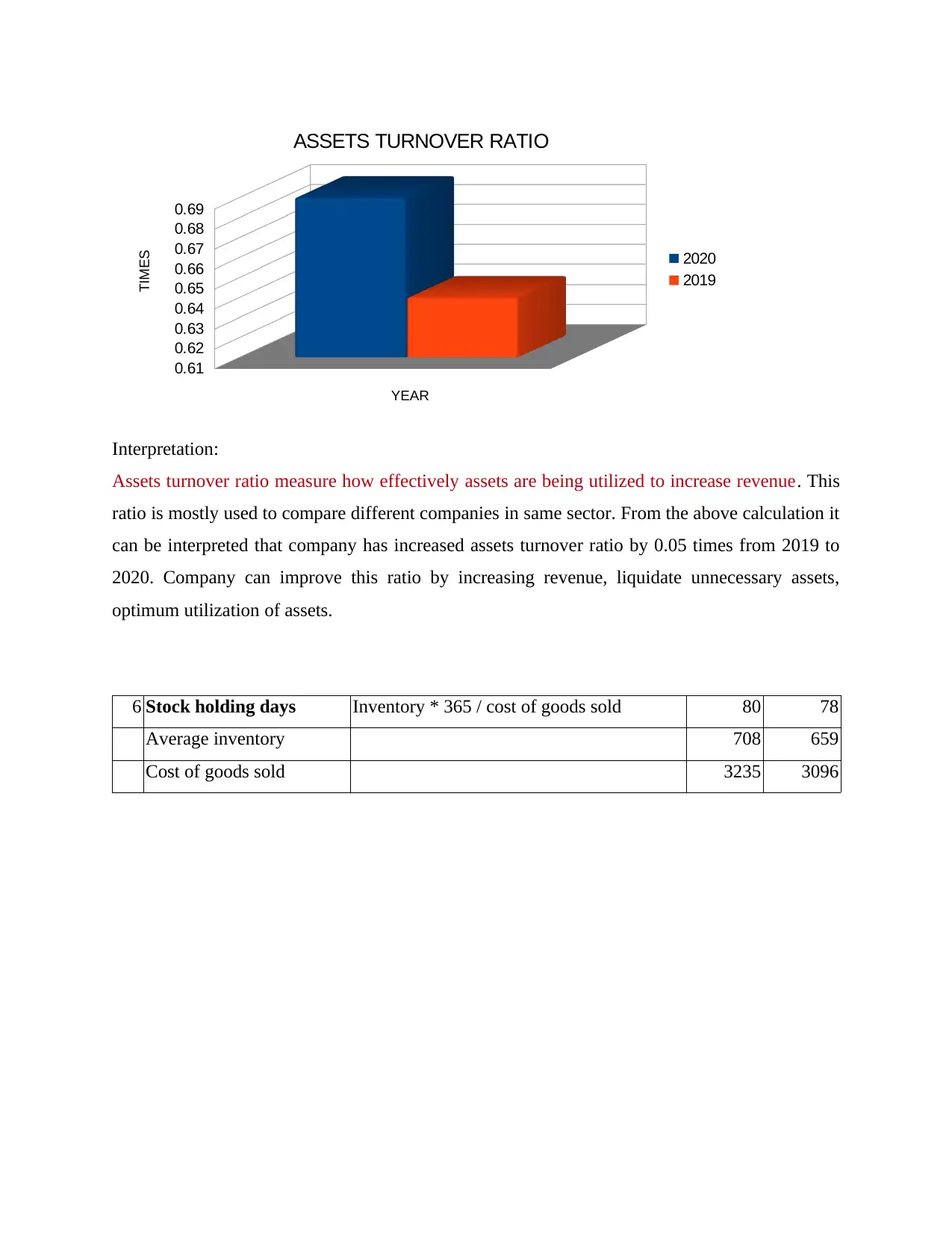

5 Assets turnover ratio Net sales / Average total assets 0.69 0.64

Net sales 6738 6441

Average total assets 9736 10087

0.054

0.056

0.058

0.06

0.062

0.064

NET PROFIT MARGIN

2020

2019

YEAR

PERCENTAGE

Interpretation:

Net profit margin shows how much net income is earned by company in terms of revenue. As the

result has been reflected that net profit margin is increased by 0.72% from 2019 to 2020. This

ratio shows company's overall health and here it has potential to grow more (Song, Seo and

Kwak, 2019). It can be improved by increasing revenue or by increasing prices, reducing cost,

smart pricing technique.

5 Assets turnover ratio Net sales / Average total assets 0.69 0.64

Net sales 6738 6441

Average total assets 9736 10087

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

0.61

0.62

0.63

0.64

0.65

0.66

0.67

0.68

0.69

ASSETS TURNOVER RATIO

2020

2019

YEAR

TIMES

Interpretation:

Assets turnover ratio measure how effectively assets are being utilized to increase revenue. This

ratio is mostly used to compare different companies in same sector. From the above calculation it

can be interpreted that company has increased assets turnover ratio by 0.05 times from 2019 to

2020. Company can improve this ratio by increasing revenue, liquidate unnecessary assets,

optimum utilization of assets.

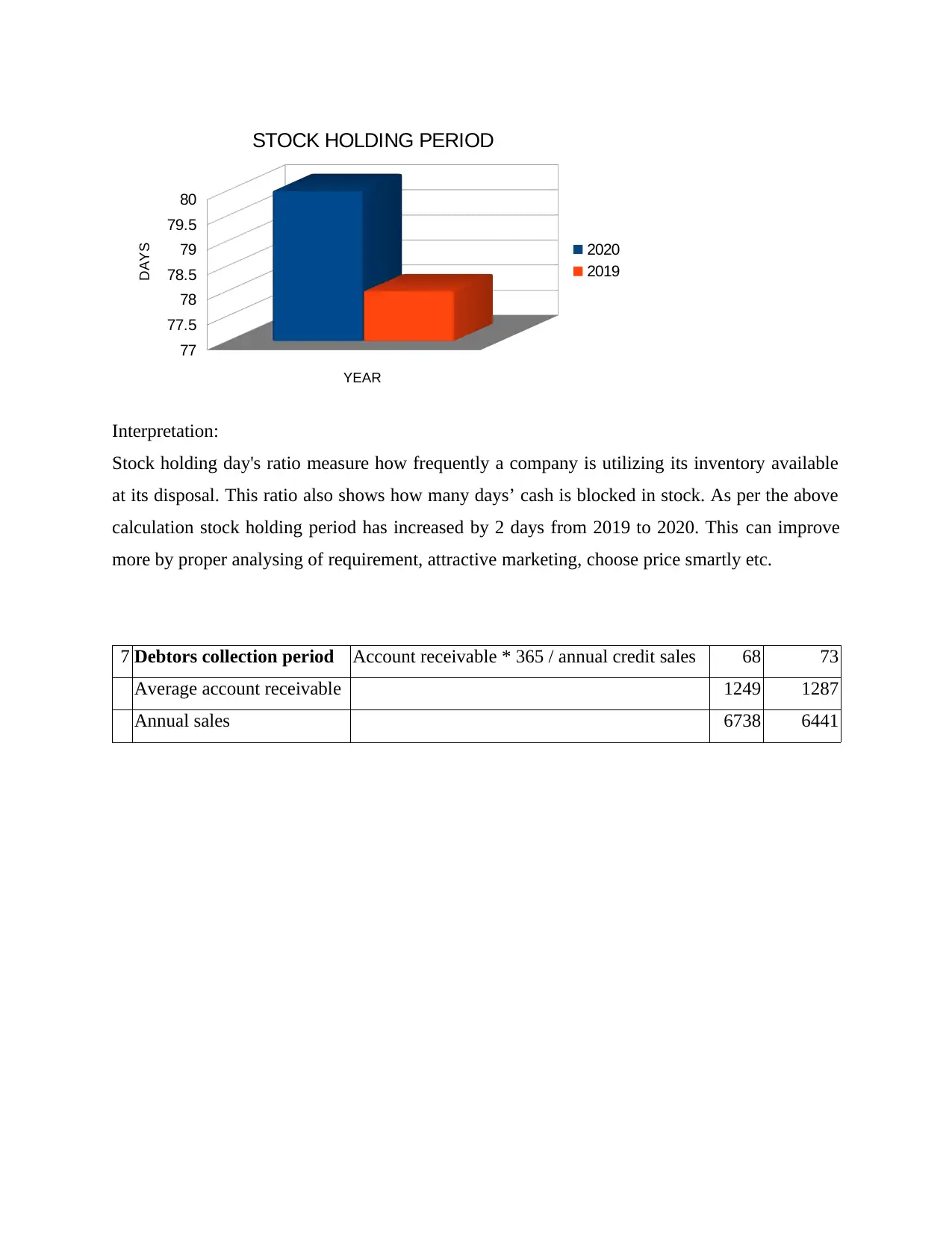

6 Stock holding days Inventory * 365 / cost of goods sold 80 78

Average inventory 708 659

Cost of goods sold 3235 3096

0.62

0.63

0.64

0.65

0.66

0.67

0.68

0.69

ASSETS TURNOVER RATIO

2020

2019

YEAR

TIMES

Interpretation:

Assets turnover ratio measure how effectively assets are being utilized to increase revenue. This

ratio is mostly used to compare different companies in same sector. From the above calculation it

can be interpreted that company has increased assets turnover ratio by 0.05 times from 2019 to

2020. Company can improve this ratio by increasing revenue, liquidate unnecessary assets,

optimum utilization of assets.

6 Stock holding days Inventory * 365 / cost of goods sold 80 78

Average inventory 708 659

Cost of goods sold 3235 3096

77

77.5

78

78.5

79

79.5

80

STOCK HOLDING PERIOD

2020

2019

YEAR

DAYS

Interpretation:

Stock holding day's ratio measure how frequently a company is utilizing its inventory available

at its disposal. This ratio also shows how many days’ cash is blocked in stock. As per the above

calculation stock holding period has increased by 2 days from 2019 to 2020. This can improve

more by proper analysing of requirement, attractive marketing, choose price smartly etc.

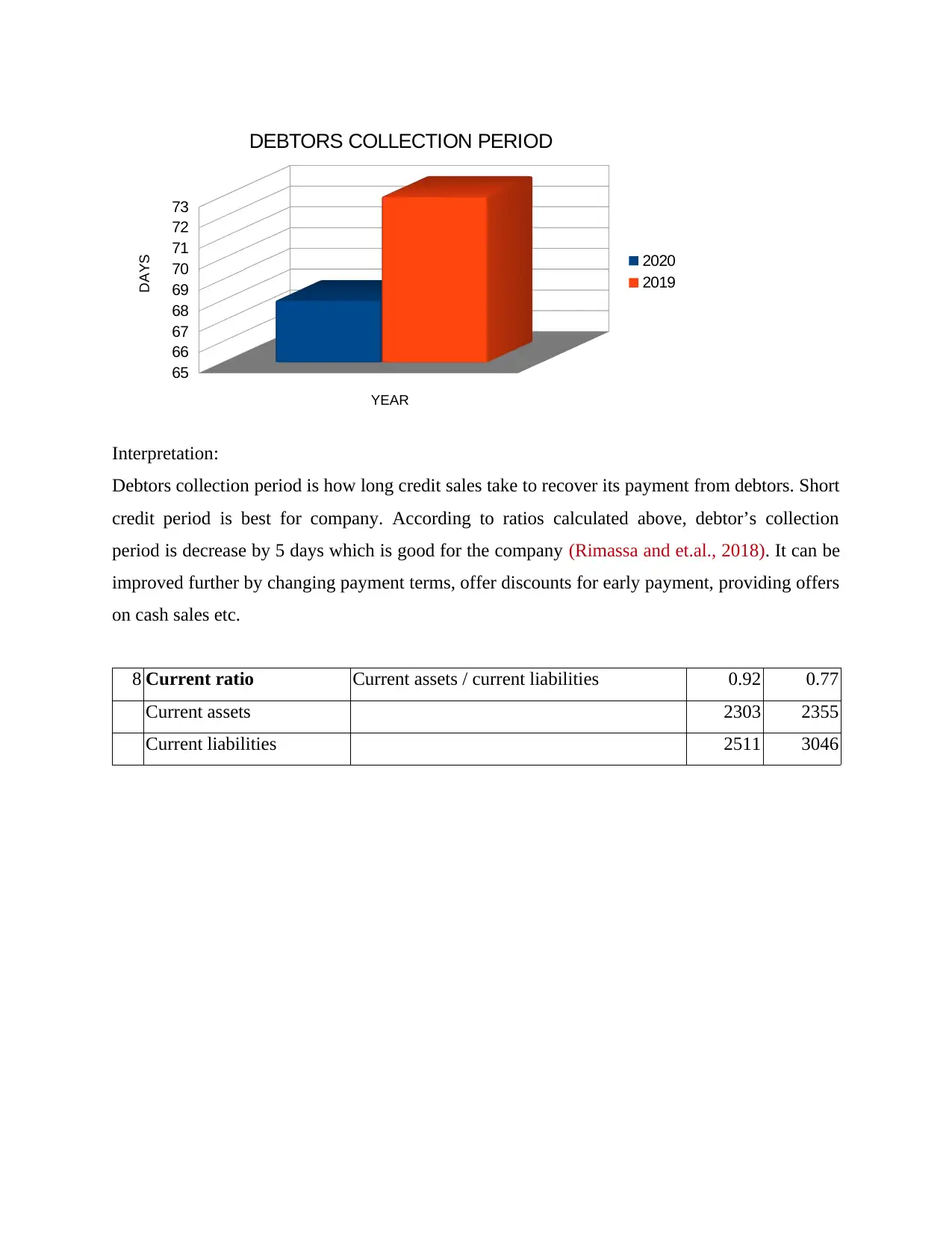

7 Debtors collection period Account receivable * 365 / annual credit sales 68 73

Average account receivable 1249 1287

Annual sales 6738 6441

77.5

78

78.5

79

79.5

80

STOCK HOLDING PERIOD

2020

2019

YEAR

DAYS

Interpretation:

Stock holding day's ratio measure how frequently a company is utilizing its inventory available

at its disposal. This ratio also shows how many days’ cash is blocked in stock. As per the above

calculation stock holding period has increased by 2 days from 2019 to 2020. This can improve

more by proper analysing of requirement, attractive marketing, choose price smartly etc.

7 Debtors collection period Account receivable * 365 / annual credit sales 68 73

Average account receivable 1249 1287

Annual sales 6738 6441

65

66

67

68

69

70

71

72

73

DEBTORS COLLECTION PERIOD

2020

2019

YEAR

DAYS

Interpretation:

Debtors collection period is how long credit sales take to recover its payment from debtors. Short

credit period is best for company. According to ratios calculated above, debtor’s collection

period is decrease by 5 days which is good for the company (Rimassa and et.al., 2018). It can be

improved further by changing payment terms, offer discounts for early payment, providing offers

on cash sales etc.

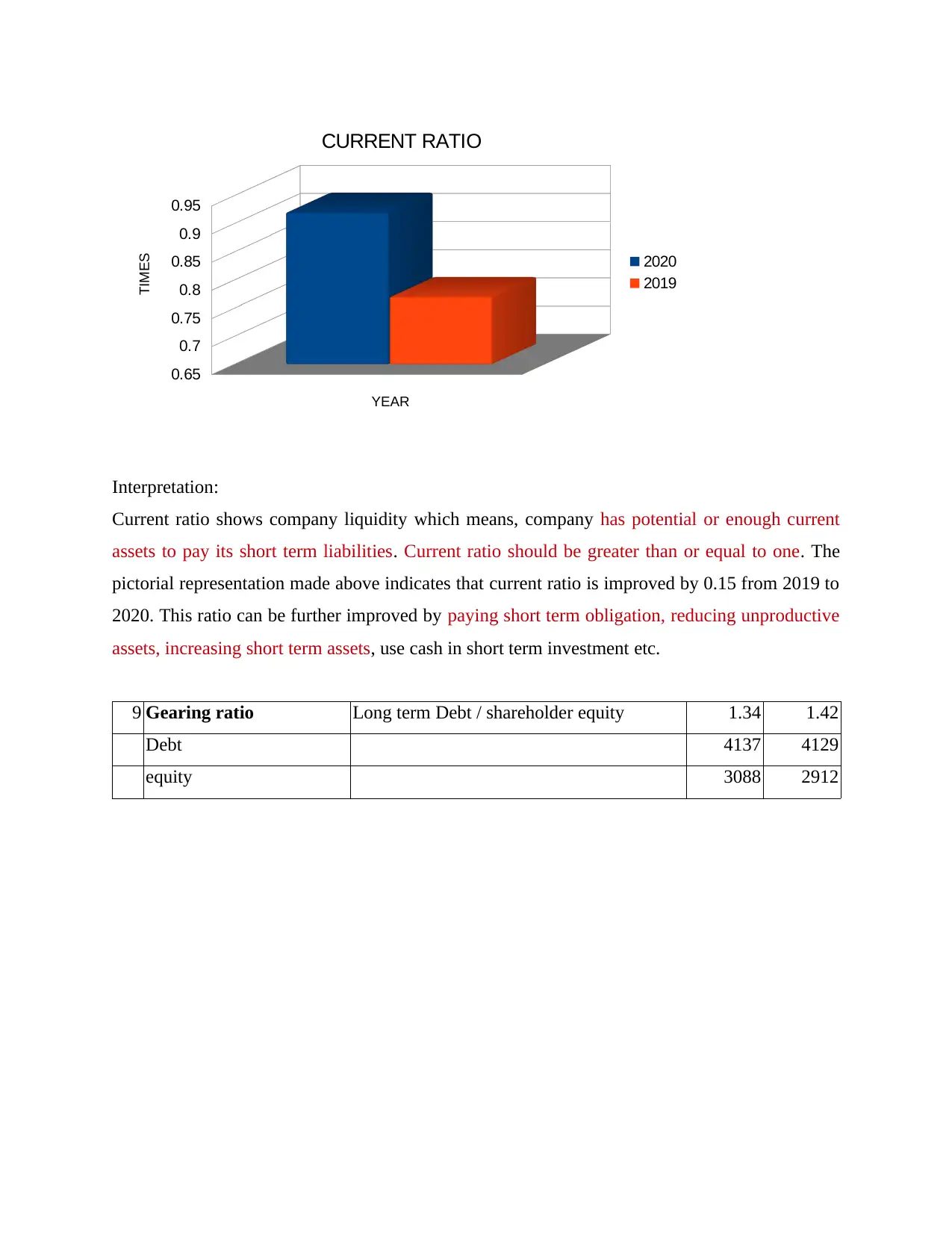

8 Current ratio Current assets / current liabilities 0.92 0.77

Current assets 2303 2355

Current liabilities 2511 3046

66

67

68

69

70

71

72

73

DEBTORS COLLECTION PERIOD

2020

2019

YEAR

DAYS

Interpretation:

Debtors collection period is how long credit sales take to recover its payment from debtors. Short

credit period is best for company. According to ratios calculated above, debtor’s collection

period is decrease by 5 days which is good for the company (Rimassa and et.al., 2018). It can be

improved further by changing payment terms, offer discounts for early payment, providing offers

on cash sales etc.

8 Current ratio Current assets / current liabilities 0.92 0.77

Current assets 2303 2355

Current liabilities 2511 3046

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.65

0.7

0.75

0.8

0.85

0.9

0.95

CURRENT RATIO

2020

2019

YEAR

TIMES

Interpretation:

Current ratio shows company liquidity which means, company has potential or enough current

assets to pay its short term liabilities. Current ratio should be greater than or equal to one. The

pictorial representation made above indicates that current ratio is improved by 0.15 from 2019 to

2020. This ratio can be further improved by paying short term obligation, reducing unproductive

assets, increasing short term assets, use cash in short term investment etc.

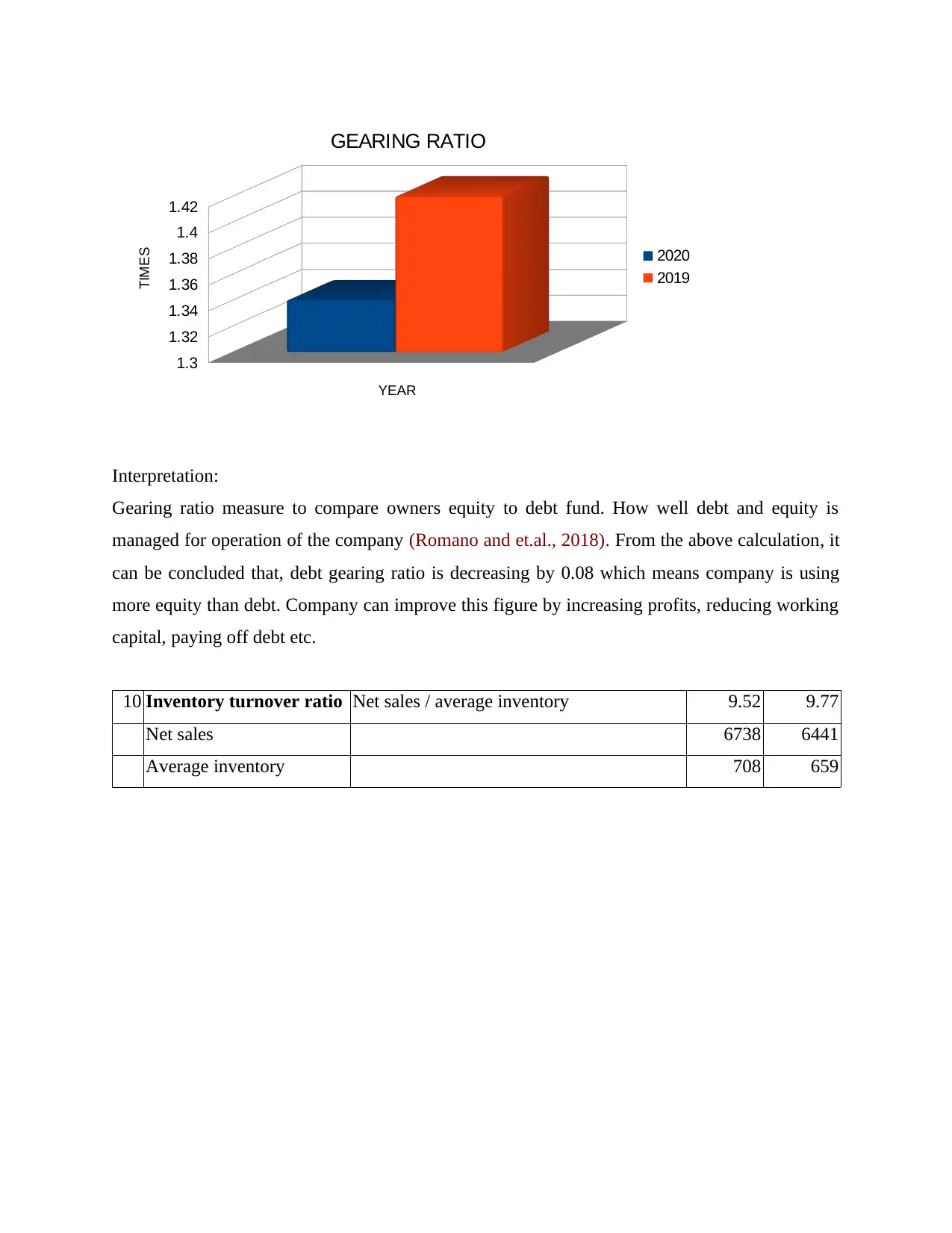

9 Gearing ratio Long term Debt / shareholder equity 1.34 1.42

Debt 4137 4129

equity 3088 2912

0.7

0.75

0.8

0.85

0.9

0.95

CURRENT RATIO

2020

2019

YEAR

TIMES

Interpretation:

Current ratio shows company liquidity which means, company has potential or enough current

assets to pay its short term liabilities. Current ratio should be greater than or equal to one. The

pictorial representation made above indicates that current ratio is improved by 0.15 from 2019 to

2020. This ratio can be further improved by paying short term obligation, reducing unproductive

assets, increasing short term assets, use cash in short term investment etc.

9 Gearing ratio Long term Debt / shareholder equity 1.34 1.42

Debt 4137 4129

equity 3088 2912

1.3

1.32

1.34

1.36

1.38

1.4

1.42

GEARING RATIO

2020

2019

YEAR

TIMES

Interpretation:

Gearing ratio measure to compare owners equity to debt fund. How well debt and equity is

managed for operation of the company (Romano and et.al., 2018). From the above calculation, it

can be concluded that, debt gearing ratio is decreasing by 0.08 which means company is using

more equity than debt. Company can improve this figure by increasing profits, reducing working

capital, paying off debt etc.

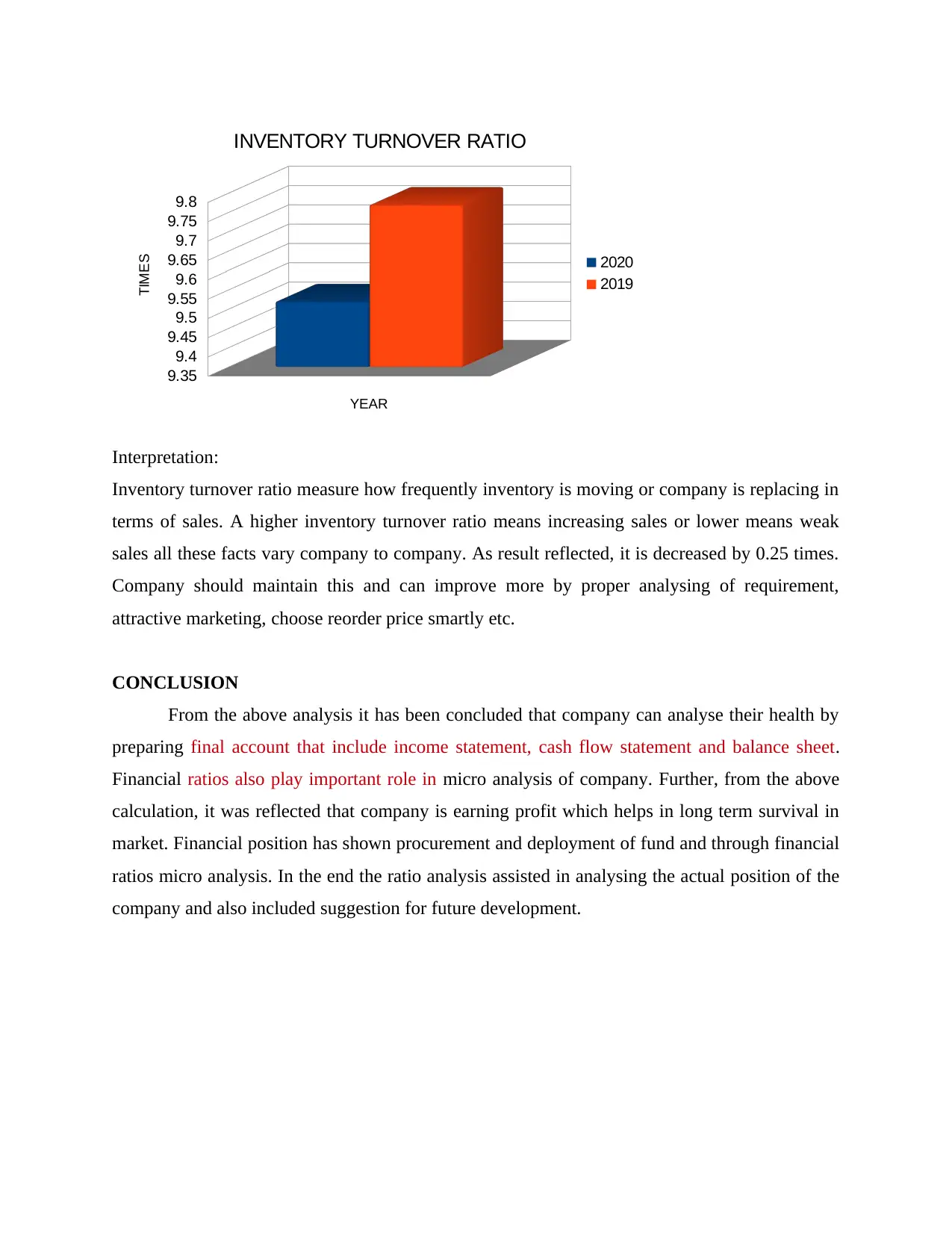

10 Inventory turnover ratio Net sales / average inventory 9.52 9.77

Net sales 6738 6441

Average inventory 708 659

1.32

1.34

1.36

1.38

1.4

1.42

GEARING RATIO

2020

2019

YEAR

TIMES

Interpretation:

Gearing ratio measure to compare owners equity to debt fund. How well debt and equity is

managed for operation of the company (Romano and et.al., 2018). From the above calculation, it

can be concluded that, debt gearing ratio is decreasing by 0.08 which means company is using

more equity than debt. Company can improve this figure by increasing profits, reducing working

capital, paying off debt etc.

10 Inventory turnover ratio Net sales / average inventory 9.52 9.77

Net sales 6738 6441

Average inventory 708 659

9.35

9.4

9.45

9.5

9.55

9.6

9.65

9.7

9.75

9.8

INVENTORY TURNOVER RATIO

2020

2019

YEAR

TIMES

Interpretation:

Inventory turnover ratio measure how frequently inventory is moving or company is replacing in

terms of sales. A higher inventory turnover ratio means increasing sales or lower means weak

sales all these facts vary company to company. As result reflected, it is decreased by 0.25 times.

Company should maintain this and can improve more by proper analysing of requirement,

attractive marketing, choose reorder price smartly etc.

CONCLUSION

From the above analysis it has been concluded that company can analyse their health by

preparing final account that include income statement, cash flow statement and balance sheet.

Financial ratios also play important role in micro analysis of company. Further, from the above

calculation, it was reflected that company is earning profit which helps in long term survival in

market. Financial position has shown procurement and deployment of fund and through financial

ratios micro analysis. In the end the ratio analysis assisted in analysing the actual position of the

company and also included suggestion for future development.

9.4

9.45

9.5

9.55

9.6

9.65

9.7

9.75

9.8

INVENTORY TURNOVER RATIO

2020

2019

YEAR

TIMES

Interpretation:

Inventory turnover ratio measure how frequently inventory is moving or company is replacing in

terms of sales. A higher inventory turnover ratio means increasing sales or lower means weak

sales all these facts vary company to company. As result reflected, it is decreased by 0.25 times.

Company should maintain this and can improve more by proper analysing of requirement,

attractive marketing, choose reorder price smartly etc.

CONCLUSION

From the above analysis it has been concluded that company can analyse their health by

preparing final account that include income statement, cash flow statement and balance sheet.

Financial ratios also play important role in micro analysis of company. Further, from the above

calculation, it was reflected that company is earning profit which helps in long term survival in

market. Financial position has shown procurement and deployment of fund and through financial

ratios micro analysis. In the end the ratio analysis assisted in analysing the actual position of the

company and also included suggestion for future development.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Felber, C., Campos, V. and Sanchis, J.R., 2019. The common good balance sheet, an adequate

tool to capture non-financials?. Sustainability. 11(14). p.3791.

Glover, D.R., 2017. Satellite radio communications fundamentals and link budgets. Handbook of

Satellite Applications, JN Pelton, S. Madry, and S. Camacho-Lara, ed. pp.293-324.

Huo, T. and et.al., 2018. China's energy consumption in the building sector: A Statistical

Yearbook-Energy Balance Sheet based splitting method. Journal of cleaner production.

185. pp.665-679.

Rimassa, L. and et.al., 2018. Tivantinib for second-line treatment of MET-high, advanced

hepatocellular carcinoma (METIV-HCC): a final analysis of a phase 3, randomised,

placebo-controlled study. The Lancet Oncology. 19(5). pp.682-693.

Romano, A. and et.al., 2018. Newly diagnosed hepatocellular carcinoma in patients with

advanced hepatitis C treated with DAAs: a prospective population study. Journal of

hepatology. 69(2). pp.345-352.

Song, D.W., Seo, Y.J. and Kwak, D.W., 2019. Learning from Hanjin Shipping’s failure: A

holistic interpretation on its causes and reasons. Transport Policy. 82. pp.77-87.

Sumner, D.A., 2018. New california milk marketing regulations will not change economic

fundamentals. Choices. 33(4). pp.1-6.

Wijaya, H. and Mauren, H.C., 2020. Factors Influencing Income Smoothing Practices With Firm

Size Moderation. Jurnal Akuntansi. 24(2). pp.250-265.

Witczak, R. and Zimny, A., 2021. The economic nature of deferred income and the accuracy of

the assessment of financial condition ratios. Zeszyty Teoretyczne Rachunkowości. (45

(1)). pp.155-172.

Books and Journals

Felber, C., Campos, V. and Sanchis, J.R., 2019. The common good balance sheet, an adequate

tool to capture non-financials?. Sustainability. 11(14). p.3791.

Glover, D.R., 2017. Satellite radio communications fundamentals and link budgets. Handbook of

Satellite Applications, JN Pelton, S. Madry, and S. Camacho-Lara, ed. pp.293-324.

Huo, T. and et.al., 2018. China's energy consumption in the building sector: A Statistical

Yearbook-Energy Balance Sheet based splitting method. Journal of cleaner production.

185. pp.665-679.

Rimassa, L. and et.al., 2018. Tivantinib for second-line treatment of MET-high, advanced

hepatocellular carcinoma (METIV-HCC): a final analysis of a phase 3, randomised,

placebo-controlled study. The Lancet Oncology. 19(5). pp.682-693.

Romano, A. and et.al., 2018. Newly diagnosed hepatocellular carcinoma in patients with

advanced hepatitis C treated with DAAs: a prospective population study. Journal of

hepatology. 69(2). pp.345-352.

Song, D.W., Seo, Y.J. and Kwak, D.W., 2019. Learning from Hanjin Shipping’s failure: A

holistic interpretation on its causes and reasons. Transport Policy. 82. pp.77-87.

Sumner, D.A., 2018. New california milk marketing regulations will not change economic

fundamentals. Choices. 33(4). pp.1-6.

Wijaya, H. and Mauren, H.C., 2020. Factors Influencing Income Smoothing Practices With Firm

Size Moderation. Jurnal Akuntansi. 24(2). pp.250-265.

Witczak, R. and Zimny, A., 2021. The economic nature of deferred income and the accuracy of

the assessment of financial condition ratios. Zeszyty Teoretyczne Rachunkowości. (45

(1)). pp.155-172.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.