Accounting Fundamentals Homework: Breakeven Analysis and Profitability

VerifiedAdded on 2023/01/06

|7

|1040

|73

Homework Assignment

AI Summary

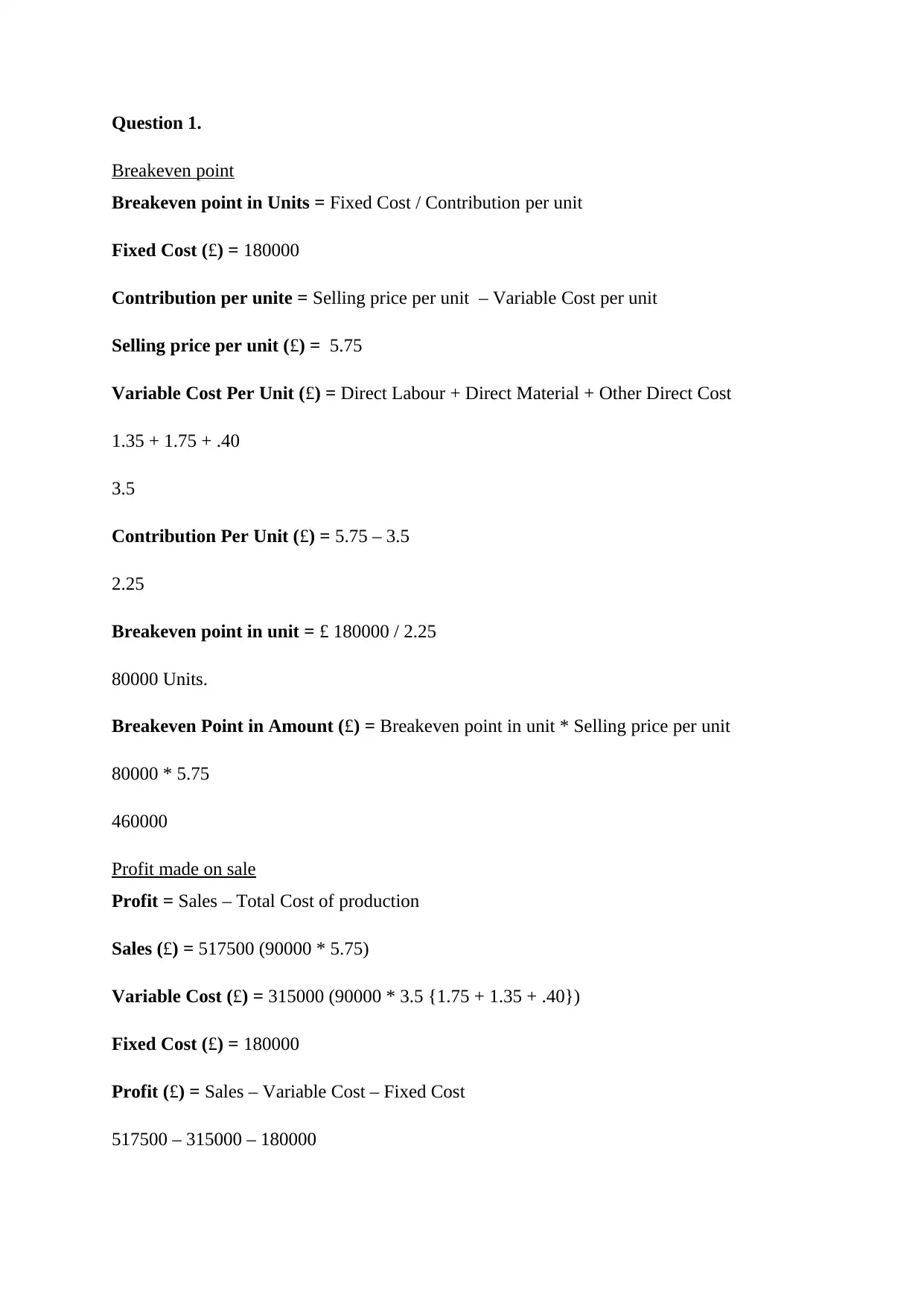

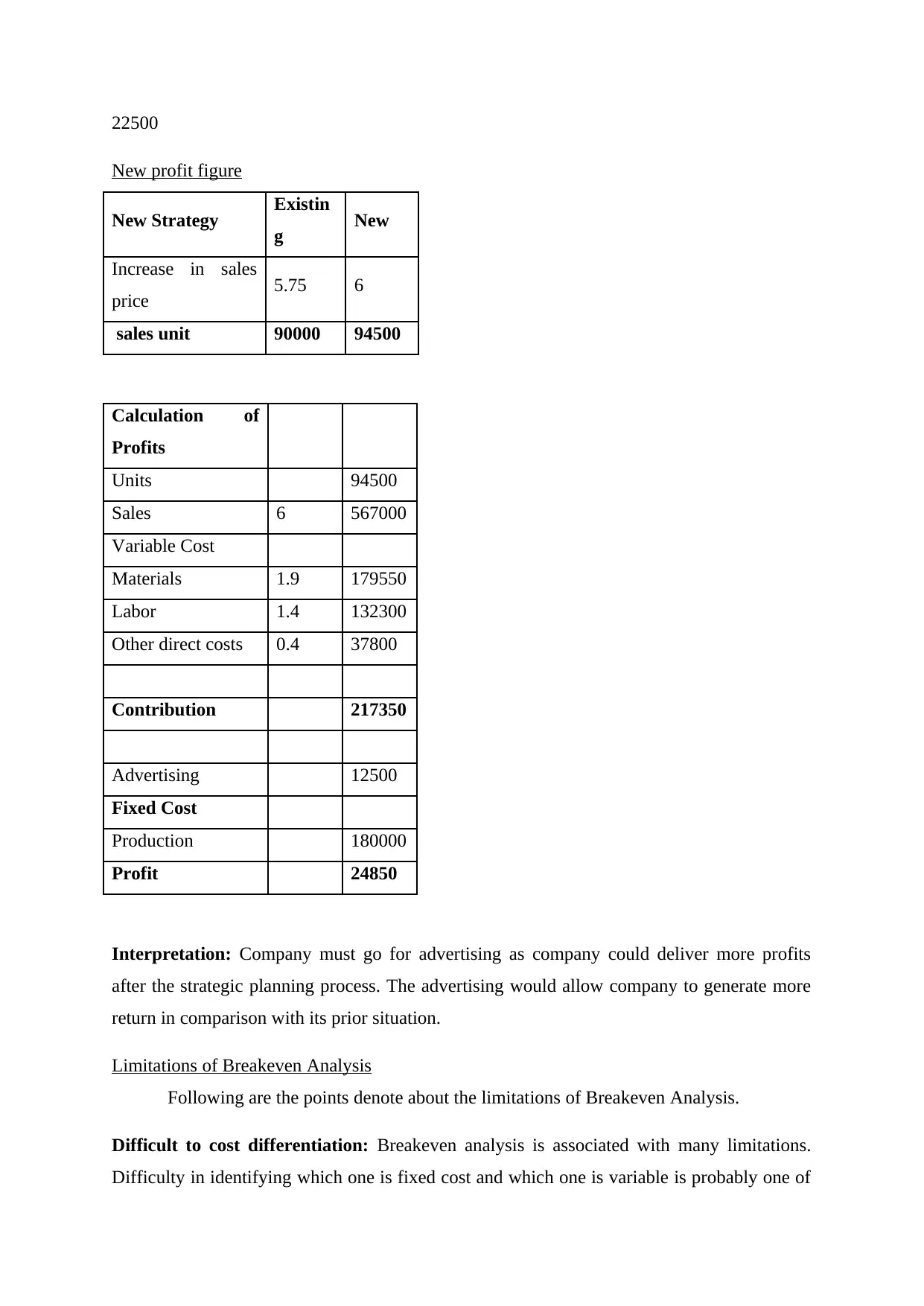

This document presents a comprehensive solution to an accounting fundamentals assignment. It begins with a detailed calculation of the breakeven point in units and amount, followed by a profit analysis based on given sales and cost figures. The solution includes a 'new profit figure' scenario, incorporating a strategic advertising plan, and a discussion of the limitations of breakeven analysis, such as difficulties in cost differentiation, complexities with semi-variable costs, and complicated calculations. The assignment then delves into the significance of management accounting, explaining its role in business decision-making and its impact on improving profitability. It concludes by outlining key techniques of management accounting, including margin analysis, trend analysis, capital budgeting, and inventory valuation, providing a well-rounded overview of the subject matter.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.