Accounting Fundamentals Homework: Financial Performance Analysis

VerifiedAdded on 2023/01/05

|7

|840

|80

Homework Assignment

AI Summary

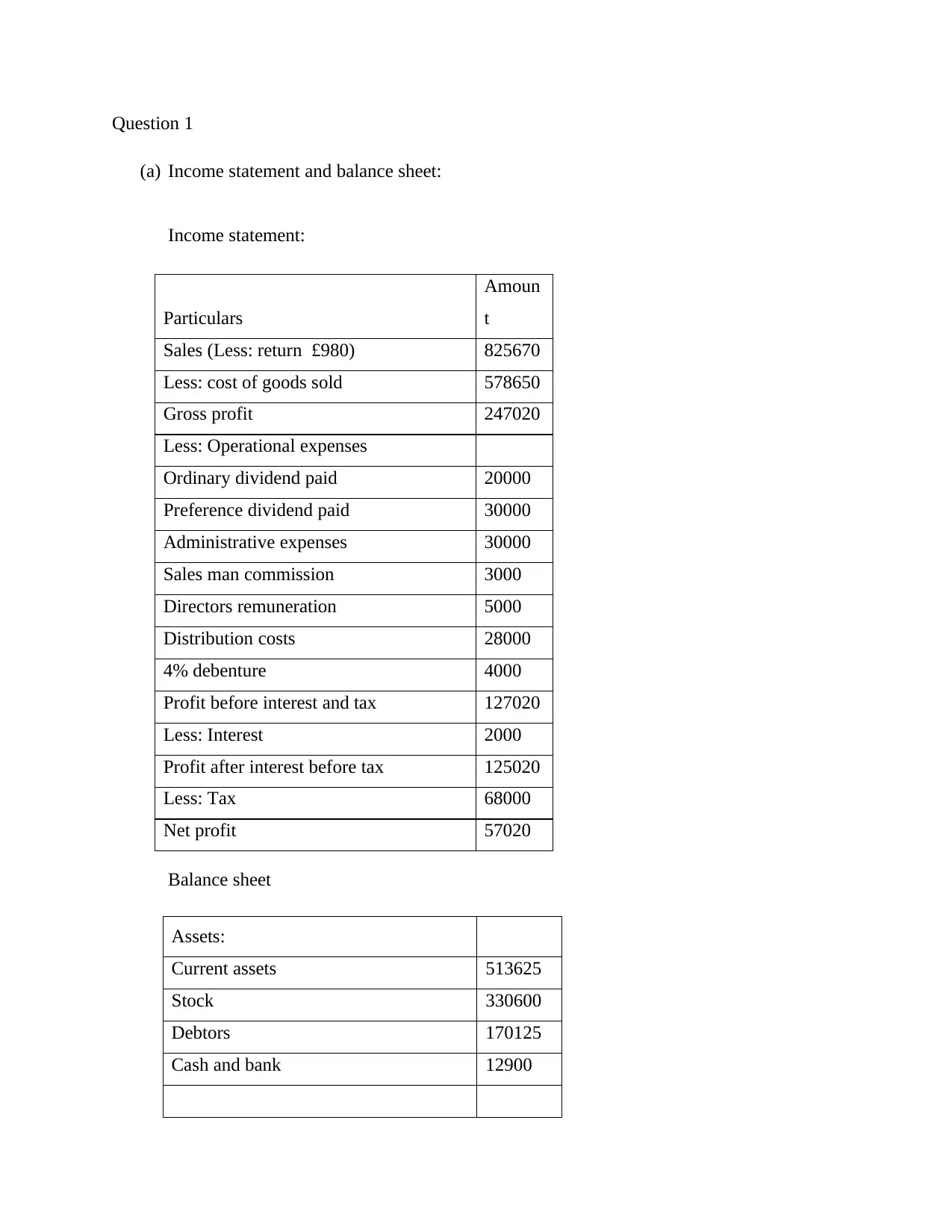

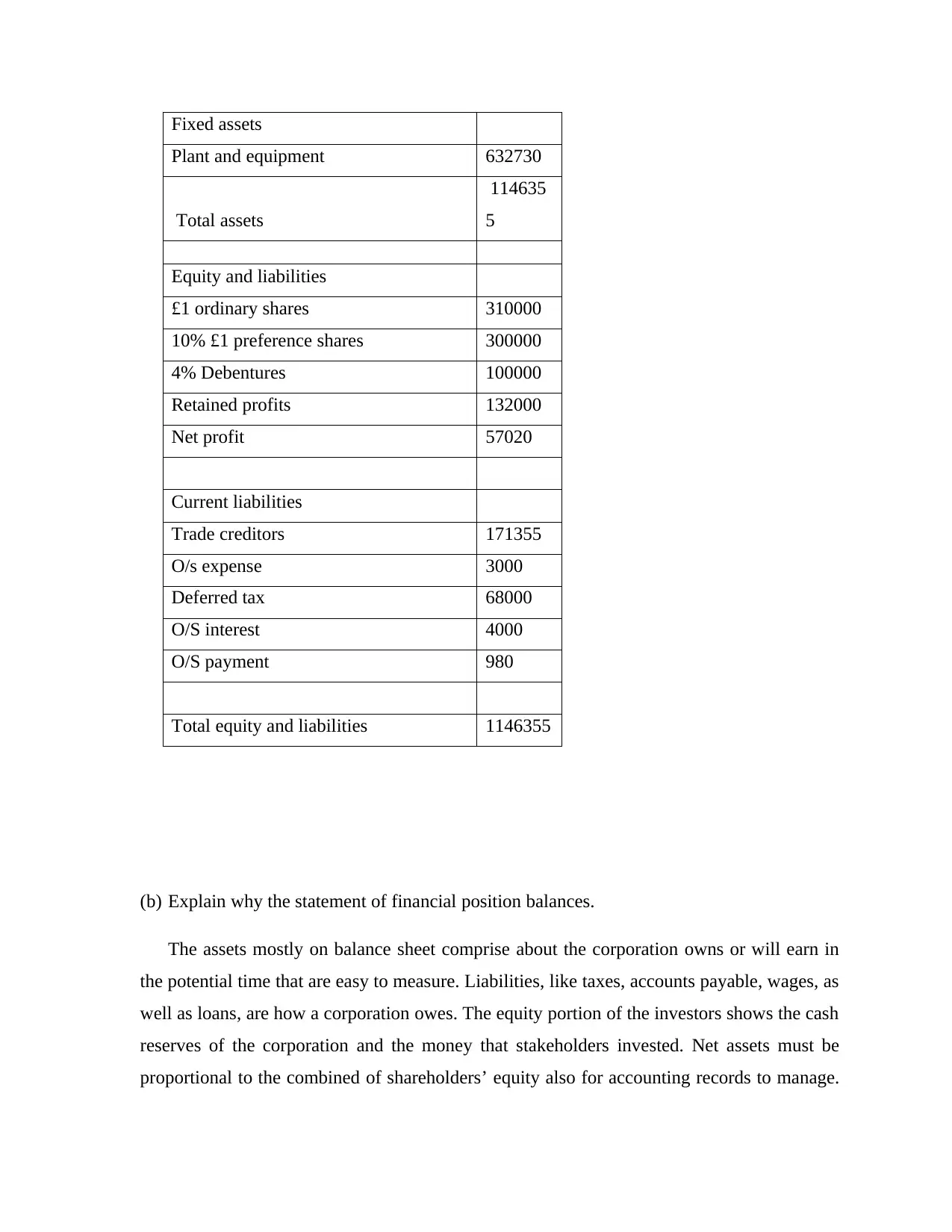

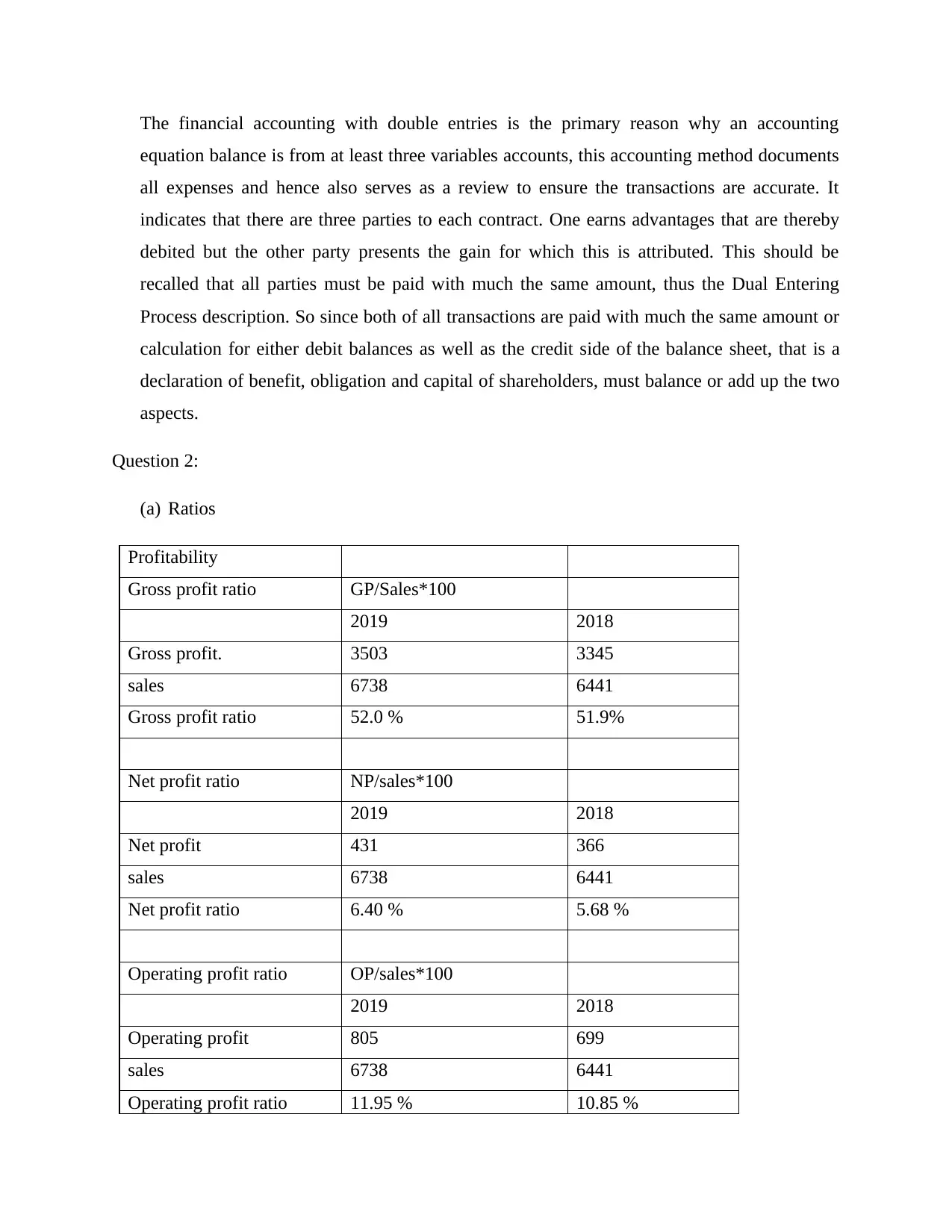

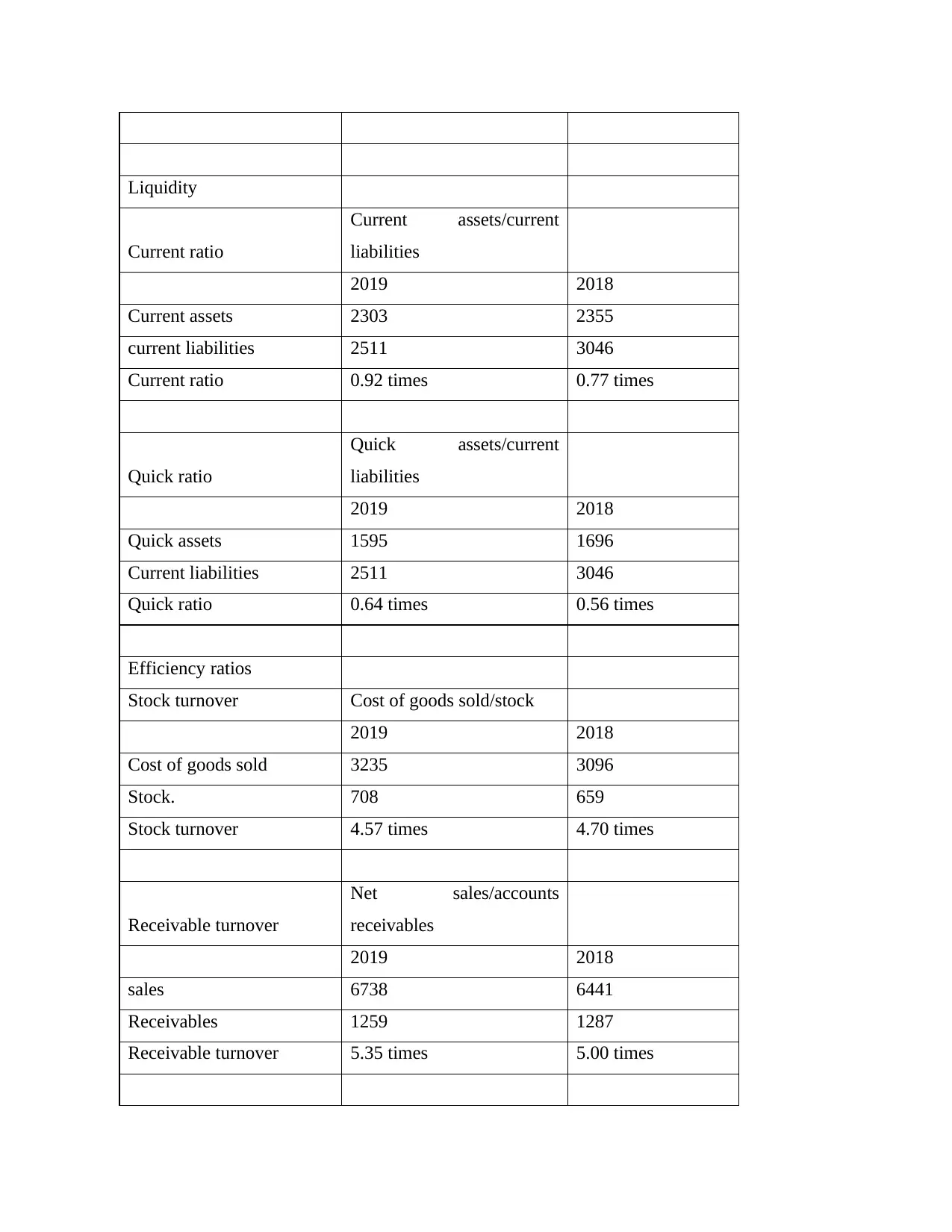

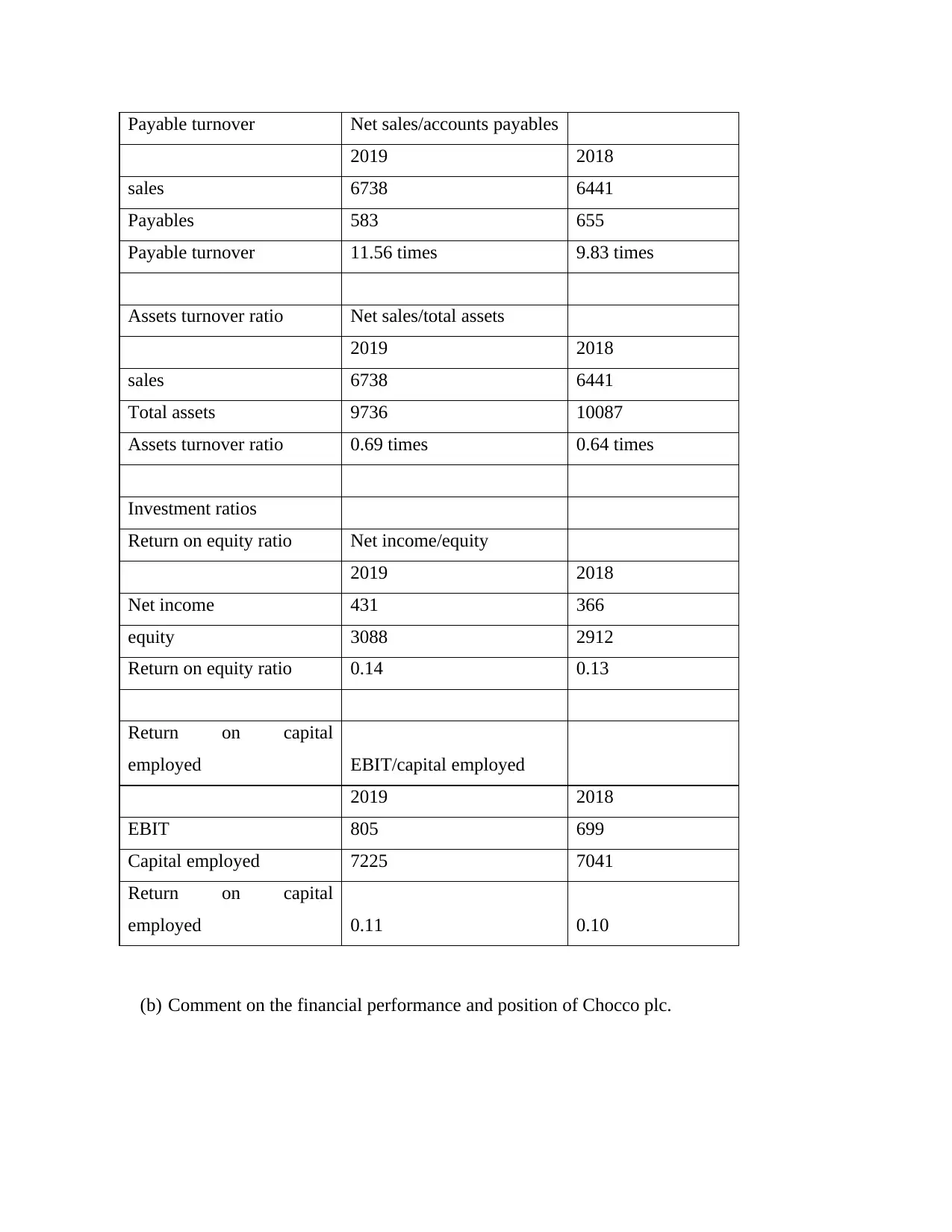

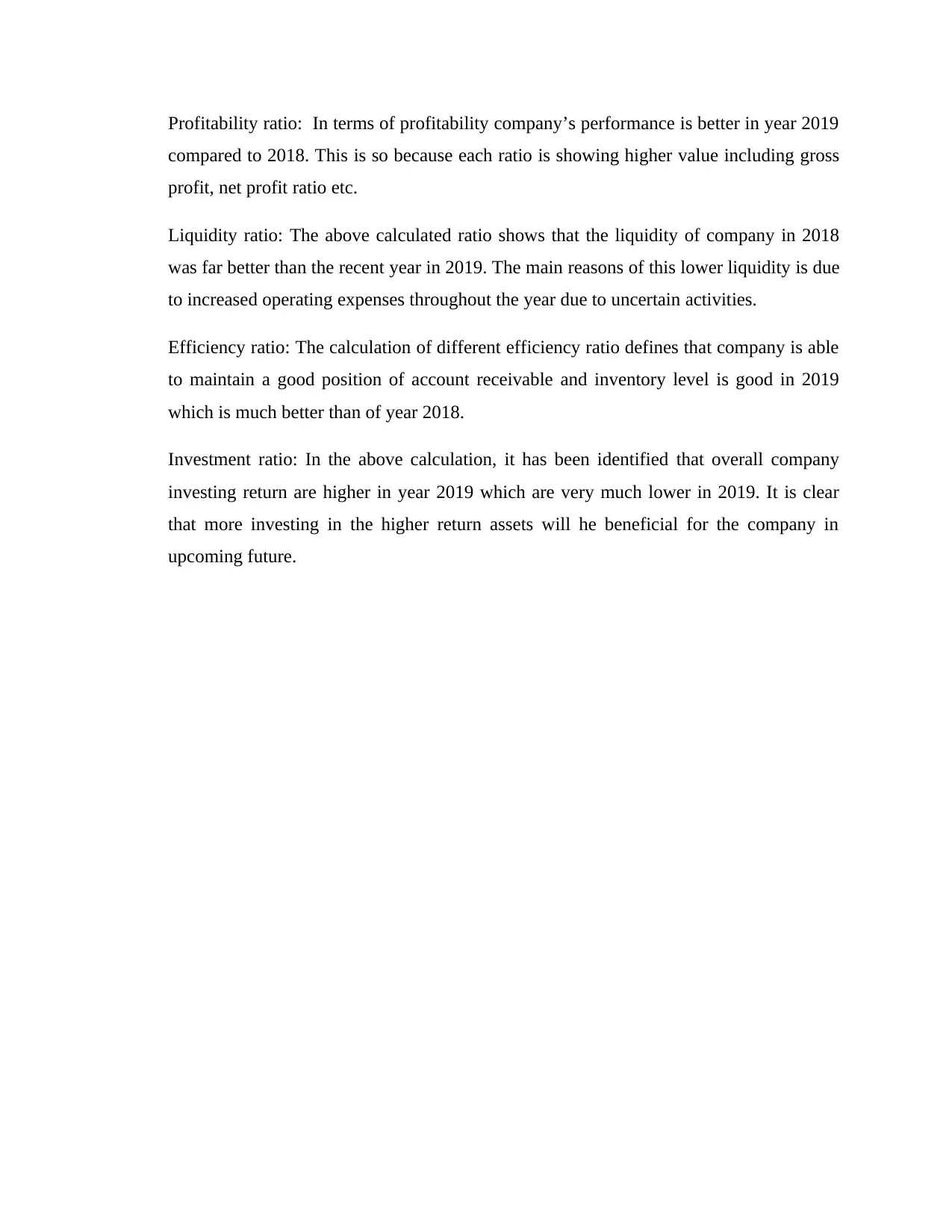

This accounting homework assignment provides a comprehensive solution to financial statement analysis. It begins with the preparation of an income statement and a balance sheet, detailing sales, cost of goods sold, operational expenses, assets, liabilities, and equity. The solution includes a discussion of why the statement of financial position balances, explaining the relationship between assets, liabilities, and equity. The assignment then delves into ratio analysis, calculating and interpreting profitability, liquidity, efficiency, and investment ratios for two consecutive years. The analysis includes a detailed commentary on the financial performance and position of Chocco plc, highlighting trends and insights derived from the ratios. The document provides a clear understanding of financial statement preparation and the application of ratio analysis to assess a company's financial health.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.