Accounting Fundamentals 1: Chocco Plc Financial Analysis Report

VerifiedAdded on 2023/01/05

|11

|2341

|69

Report

AI Summary

This report presents a detailed analysis of Chocco Plc's financial performance based on accounting fundamentals. It begins with the company's final accounts, including an income statement and statement of financial position, along with necessary journal entries to reflect outstanding commis...

Accounting fundamentals

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Main Body.......................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

References......................................................................................................................................11

2

Main Body.......................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

References......................................................................................................................................11

2

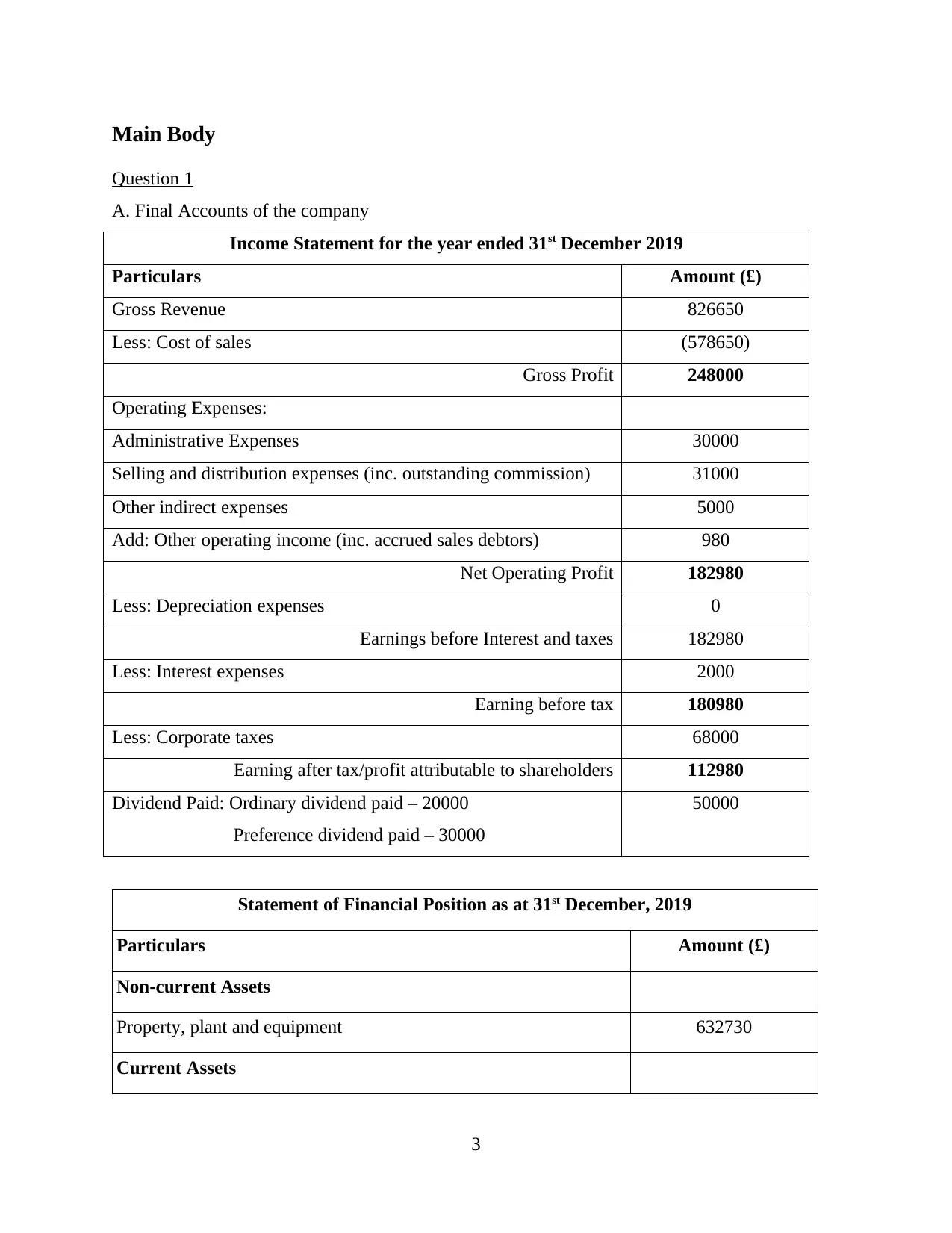

Main Body

Question 1

A. Final Accounts of the company

Income Statement for the year ended 31st December 2019

Particulars Amount (£)

Gross Revenue 826650

Less: Cost of sales (578650)

Gross Profit 248000

Operating Expenses:

Administrative Expenses 30000

Selling and distribution expenses (inc. outstanding commission) 31000

Other indirect expenses 5000

Add: Other operating income (inc. accrued sales debtors) 980

Net Operating Profit 182980

Less: Depreciation expenses 0

Earnings before Interest and taxes 182980

Less: Interest expenses 2000

Earning before tax 180980

Less: Corporate taxes 68000

Earning after tax/profit attributable to shareholders 112980

Dividend Paid: Ordinary dividend paid – 20000

Preference dividend paid – 30000

50000

Statement of Financial Position as at 31st December, 2019

Particulars Amount (£)

Non-current Assets

Property, plant and equipment 632730

Current Assets

3

Question 1

A. Final Accounts of the company

Income Statement for the year ended 31st December 2019

Particulars Amount (£)

Gross Revenue 826650

Less: Cost of sales (578650)

Gross Profit 248000

Operating Expenses:

Administrative Expenses 30000

Selling and distribution expenses (inc. outstanding commission) 31000

Other indirect expenses 5000

Add: Other operating income (inc. accrued sales debtors) 980

Net Operating Profit 182980

Less: Depreciation expenses 0

Earnings before Interest and taxes 182980

Less: Interest expenses 2000

Earning before tax 180980

Less: Corporate taxes 68000

Earning after tax/profit attributable to shareholders 112980

Dividend Paid: Ordinary dividend paid – 20000

Preference dividend paid – 30000

50000

Statement of Financial Position as at 31st December, 2019

Particulars Amount (£)

Non-current Assets

Property, plant and equipment 632730

Current Assets

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

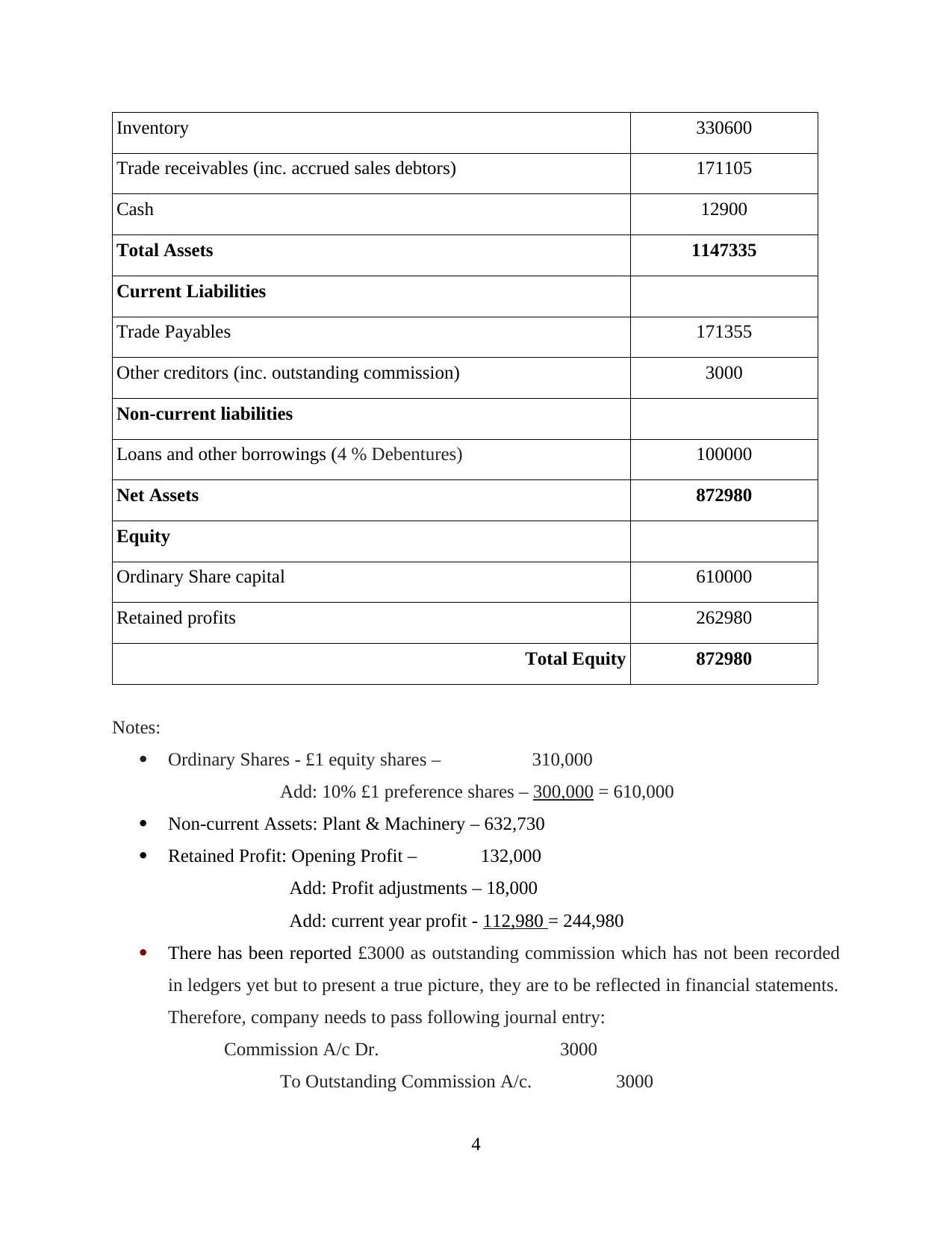

Inventory 330600

Trade receivables (inc. accrued sales debtors) 171105

Cash 12900

Total Assets 1147335

Current Liabilities

Trade Payables 171355

Other creditors (inc. outstanding commission) 3000

Non-current liabilities

Loans and other borrowings (4 % Debentures) 100000

Net Assets 872980

Equity

Ordinary Share capital 610000

Retained profits 262980

Total Equity 872980

Notes:

Ordinary Shares - £1 equity shares – 310,000

Add: 10% £1 preference shares – 300,000 = 610,000

Non-current Assets: Plant & Machinery – 632,730

Retained Profit: Opening Profit – 132,000

Add: Profit adjustments – 18,000

Add: current year profit - 112,980 = 244,980

There has been reported £3000 as outstanding commission which has not been recorded

in ledgers yet but to present a true picture, they are to be reflected in financial statements.

Therefore, company needs to pass following journal entry:

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

4

Trade receivables (inc. accrued sales debtors) 171105

Cash 12900

Total Assets 1147335

Current Liabilities

Trade Payables 171355

Other creditors (inc. outstanding commission) 3000

Non-current liabilities

Loans and other borrowings (4 % Debentures) 100000

Net Assets 872980

Equity

Ordinary Share capital 610000

Retained profits 262980

Total Equity 872980

Notes:

Ordinary Shares - £1 equity shares – 310,000

Add: 10% £1 preference shares – 300,000 = 610,000

Non-current Assets: Plant & Machinery – 632,730

Retained Profit: Opening Profit – 132,000

Add: Profit adjustments – 18,000

Add: current year profit - 112,980 = 244,980

There has been reported £3000 as outstanding commission which has not been recorded

in ledgers yet but to present a true picture, they are to be reflected in financial statements.

Therefore, company needs to pass following journal entry:

Commission A/c Dr. 3000

To Outstanding Commission A/c. 3000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accordingly, these accounts will now be reflected in income statement by adding

outstanding commission to commission account while outstanding commission will be reflected

in current liabilities of the Statement of Financial position.

It has also been reported that the goods were worth £980 were sent to customers, payment

of which will be received later and therefore, it has not been recorded in ledgers but to

present a true picture, company needs to pass following journal entry so that it can reflect

in financial statement:

Accrued sales debtors A/c Dr. 980

To Sales debtors A/c 980

Accordingly, these accounts will now be reflected in income statement by adding accrued

sales debtors to sales debtors account while accrued sales debtors will be reflected in current

assets of the Statement of Financial position.

B. Why the statement of financial position balances.

Balance Sheet or statement of financial position follows the accounting principle of

double entry which says that all transactions shall be recorded in two different accounts in which

they have an equal and opposite effects (Brown and Johnston, 2019). This principle also helps in

checking whether the entries are consistent and properly recorded or not. Balance Sheet is also

based on this principle and has formula of,

Assets = Liabilities + Equity

Two sides of this formula add up to make the total value in the business on its own. Assets

side represents break down of the value used in the business while other side of liabilities and

equity breaks down the source of funding, as to how this value was acquired. Since, one side

represents value in the business and other side represents source of that funding, they must be

equal so as to ensure that all financial transactions are duly recorded.

Question 2

A. Ratio Analysis

It is a quantitative method which helps a company in knowing about its liquidity,

efficiency, profitability, etc. from the data presented in its financial statements (Samonas, 2015).

Therefore, in other words, it is the analysis of financial health of company in mathematical

terms. Below mentioned are different kinds of ratios:

5

outstanding commission to commission account while outstanding commission will be reflected

in current liabilities of the Statement of Financial position.

It has also been reported that the goods were worth £980 were sent to customers, payment

of which will be received later and therefore, it has not been recorded in ledgers but to

present a true picture, company needs to pass following journal entry so that it can reflect

in financial statement:

Accrued sales debtors A/c Dr. 980

To Sales debtors A/c 980

Accordingly, these accounts will now be reflected in income statement by adding accrued

sales debtors to sales debtors account while accrued sales debtors will be reflected in current

assets of the Statement of Financial position.

B. Why the statement of financial position balances.

Balance Sheet or statement of financial position follows the accounting principle of

double entry which says that all transactions shall be recorded in two different accounts in which

they have an equal and opposite effects (Brown and Johnston, 2019). This principle also helps in

checking whether the entries are consistent and properly recorded or not. Balance Sheet is also

based on this principle and has formula of,

Assets = Liabilities + Equity

Two sides of this formula add up to make the total value in the business on its own. Assets

side represents break down of the value used in the business while other side of liabilities and

equity breaks down the source of funding, as to how this value was acquired. Since, one side

represents value in the business and other side represents source of that funding, they must be

equal so as to ensure that all financial transactions are duly recorded.

Question 2

A. Ratio Analysis

It is a quantitative method which helps a company in knowing about its liquidity,

efficiency, profitability, etc. from the data presented in its financial statements (Samonas, 2015).

Therefore, in other words, it is the analysis of financial health of company in mathematical

terms. Below mentioned are different kinds of ratios:

5

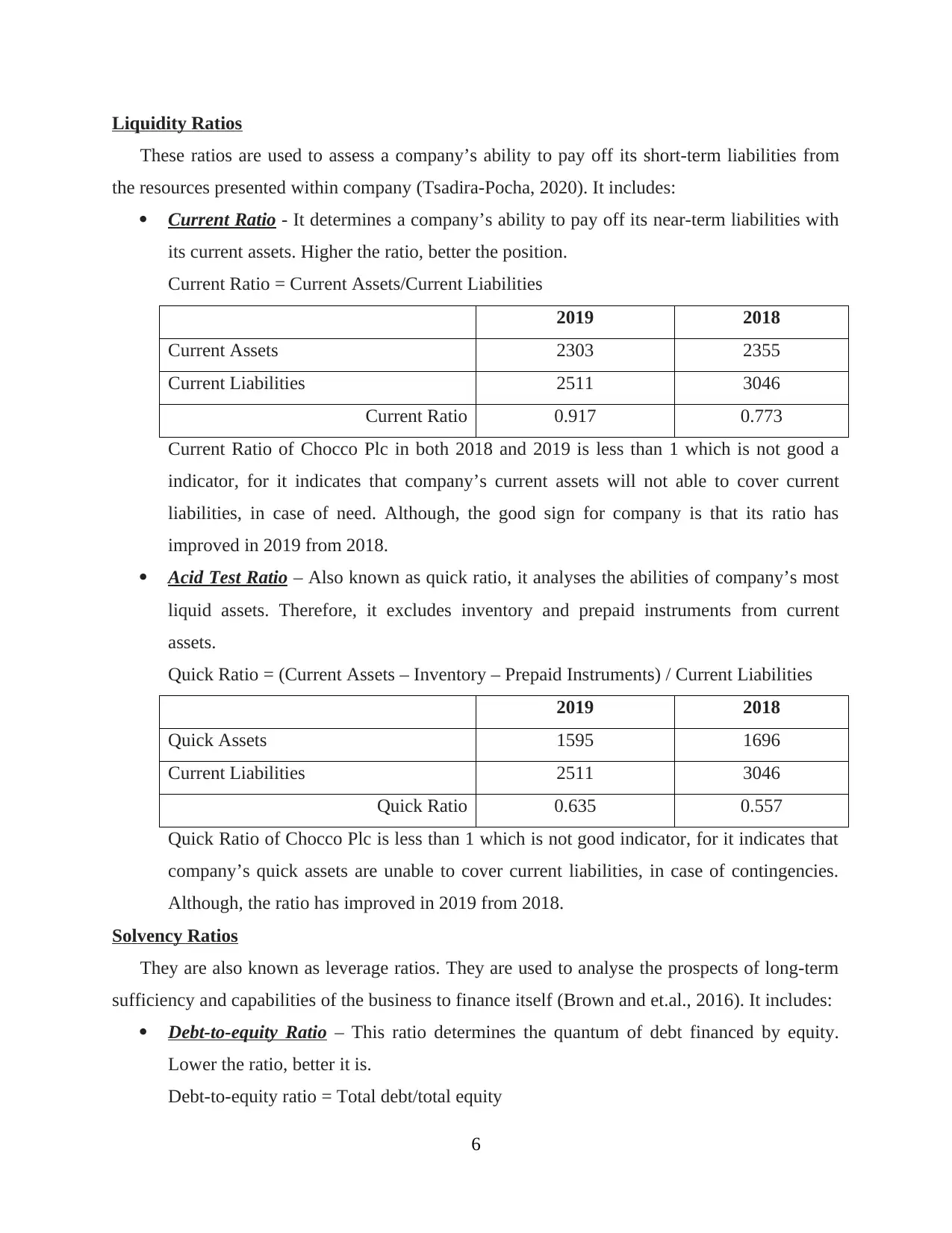

Liquidity Ratios

These ratios are used to assess a company’s ability to pay off its short-term liabilities from

the resources presented within company (Tsadira-Pocha, 2020). It includes:

Current Ratio - It determines a company’s ability to pay off its near-term liabilities with

its current assets. Higher the ratio, better the position.

Current Ratio = Current Assets/Current Liabilities

2019 2018

Current Assets 2303 2355

Current Liabilities 2511 3046

Current Ratio 0.917 0.773

Current Ratio of Chocco Plc in both 2018 and 2019 is less than 1 which is not good a

indicator, for it indicates that company’s current assets will not able to cover current

liabilities, in case of need. Although, the good sign for company is that its ratio has

improved in 2019 from 2018.

Acid Test Ratio – Also known as quick ratio, it analyses the abilities of company’s most

liquid assets. Therefore, it excludes inventory and prepaid instruments from current

assets.

Quick Ratio = (Current Assets – Inventory – Prepaid Instruments) / Current Liabilities

2019 2018

Quick Assets 1595 1696

Current Liabilities 2511 3046

Quick Ratio 0.635 0.557

Quick Ratio of Chocco Plc is less than 1 which is not good indicator, for it indicates that

company’s quick assets are unable to cover current liabilities, in case of contingencies.

Although, the ratio has improved in 2019 from 2018.

Solvency Ratios

They are also known as leverage ratios. They are used to analyse the prospects of long-term

sufficiency and capabilities of the business to finance itself (Brown and et.al., 2016). It includes:

Debt-to-equity Ratio – This ratio determines the quantum of debt financed by equity.

Lower the ratio, better it is.

Debt-to-equity ratio = Total debt/total equity

6

These ratios are used to assess a company’s ability to pay off its short-term liabilities from

the resources presented within company (Tsadira-Pocha, 2020). It includes:

Current Ratio - It determines a company’s ability to pay off its near-term liabilities with

its current assets. Higher the ratio, better the position.

Current Ratio = Current Assets/Current Liabilities

2019 2018

Current Assets 2303 2355

Current Liabilities 2511 3046

Current Ratio 0.917 0.773

Current Ratio of Chocco Plc in both 2018 and 2019 is less than 1 which is not good a

indicator, for it indicates that company’s current assets will not able to cover current

liabilities, in case of need. Although, the good sign for company is that its ratio has

improved in 2019 from 2018.

Acid Test Ratio – Also known as quick ratio, it analyses the abilities of company’s most

liquid assets. Therefore, it excludes inventory and prepaid instruments from current

assets.

Quick Ratio = (Current Assets – Inventory – Prepaid Instruments) / Current Liabilities

2019 2018

Quick Assets 1595 1696

Current Liabilities 2511 3046

Quick Ratio 0.635 0.557

Quick Ratio of Chocco Plc is less than 1 which is not good indicator, for it indicates that

company’s quick assets are unable to cover current liabilities, in case of contingencies.

Although, the ratio has improved in 2019 from 2018.

Solvency Ratios

They are also known as leverage ratios. They are used to analyse the prospects of long-term

sufficiency and capabilities of the business to finance itself (Brown and et.al., 2016). It includes:

Debt-to-equity Ratio – This ratio determines the quantum of debt financed by equity.

Lower the ratio, better it is.

Debt-to-equity ratio = Total debt/total equity

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

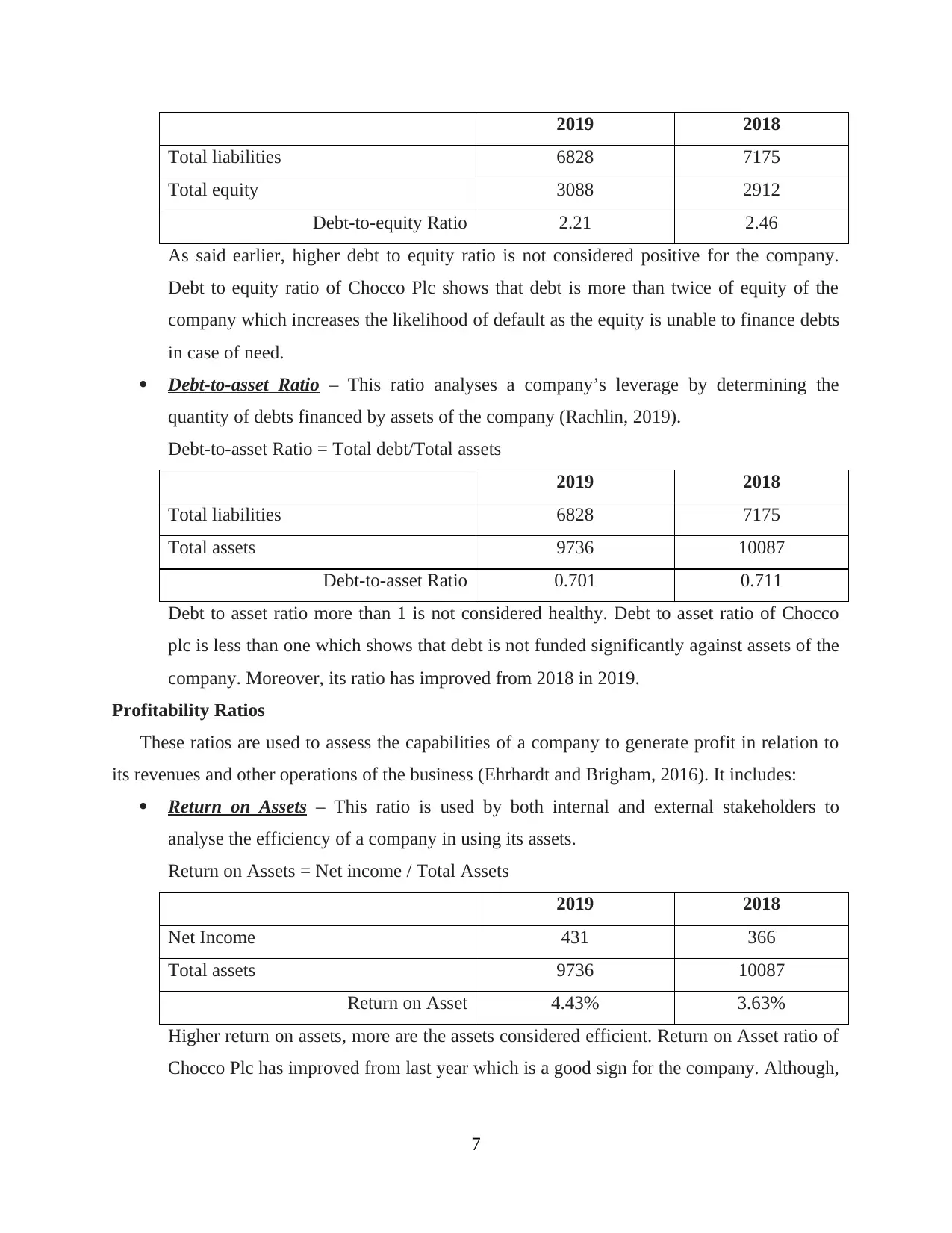

2019 2018

Total liabilities 6828 7175

Total equity 3088 2912

Debt-to-equity Ratio 2.21 2.46

As said earlier, higher debt to equity ratio is not considered positive for the company.

Debt to equity ratio of Chocco Plc shows that debt is more than twice of equity of the

company which increases the likelihood of default as the equity is unable to finance debts

in case of need.

Debt-to-asset Ratio – This ratio analyses a company’s leverage by determining the

quantity of debts financed by assets of the company (Rachlin, 2019).

Debt-to-asset Ratio = Total debt/Total assets

2019 2018

Total liabilities 6828 7175

Total assets 9736 10087

Debt-to-asset Ratio 0.701 0.711

Debt to asset ratio more than 1 is not considered healthy. Debt to asset ratio of Chocco

plc is less than one which shows that debt is not funded significantly against assets of the

company. Moreover, its ratio has improved from 2018 in 2019.

Profitability Ratios

These ratios are used to assess the capabilities of a company to generate profit in relation to

its revenues and other operations of the business (Ehrhardt and Brigham, 2016). It includes:

Return on Assets – This ratio is used by both internal and external stakeholders to

analyse the efficiency of a company in using its assets.

Return on Assets = Net income / Total Assets

2019 2018

Net Income 431 366

Total assets 9736 10087

Return on Asset 4.43% 3.63%

Higher return on assets, more are the assets considered efficient. Return on Asset ratio of

Chocco Plc has improved from last year which is a good sign for the company. Although,

7

Total liabilities 6828 7175

Total equity 3088 2912

Debt-to-equity Ratio 2.21 2.46

As said earlier, higher debt to equity ratio is not considered positive for the company.

Debt to equity ratio of Chocco Plc shows that debt is more than twice of equity of the

company which increases the likelihood of default as the equity is unable to finance debts

in case of need.

Debt-to-asset Ratio – This ratio analyses a company’s leverage by determining the

quantity of debts financed by assets of the company (Rachlin, 2019).

Debt-to-asset Ratio = Total debt/Total assets

2019 2018

Total liabilities 6828 7175

Total assets 9736 10087

Debt-to-asset Ratio 0.701 0.711

Debt to asset ratio more than 1 is not considered healthy. Debt to asset ratio of Chocco

plc is less than one which shows that debt is not funded significantly against assets of the

company. Moreover, its ratio has improved from 2018 in 2019.

Profitability Ratios

These ratios are used to assess the capabilities of a company to generate profit in relation to

its revenues and other operations of the business (Ehrhardt and Brigham, 2016). It includes:

Return on Assets – This ratio is used by both internal and external stakeholders to

analyse the efficiency of a company in using its assets.

Return on Assets = Net income / Total Assets

2019 2018

Net Income 431 366

Total assets 9736 10087

Return on Asset 4.43% 3.63%

Higher return on assets, more are the assets considered efficient. Return on Asset ratio of

Chocco Plc has improved from last year which is a good sign for the company. Although,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the ratio is not high enough and company needs to keep on making efforts to improve

their profit so that it can have better returns on assets.

Efficiency Ratios

These ratios are also called as activity ratios and are used to evaluate the capabilities of a

company in utilising its assets and liabilities to improvise its profits (Chandra, 2017). It includes:

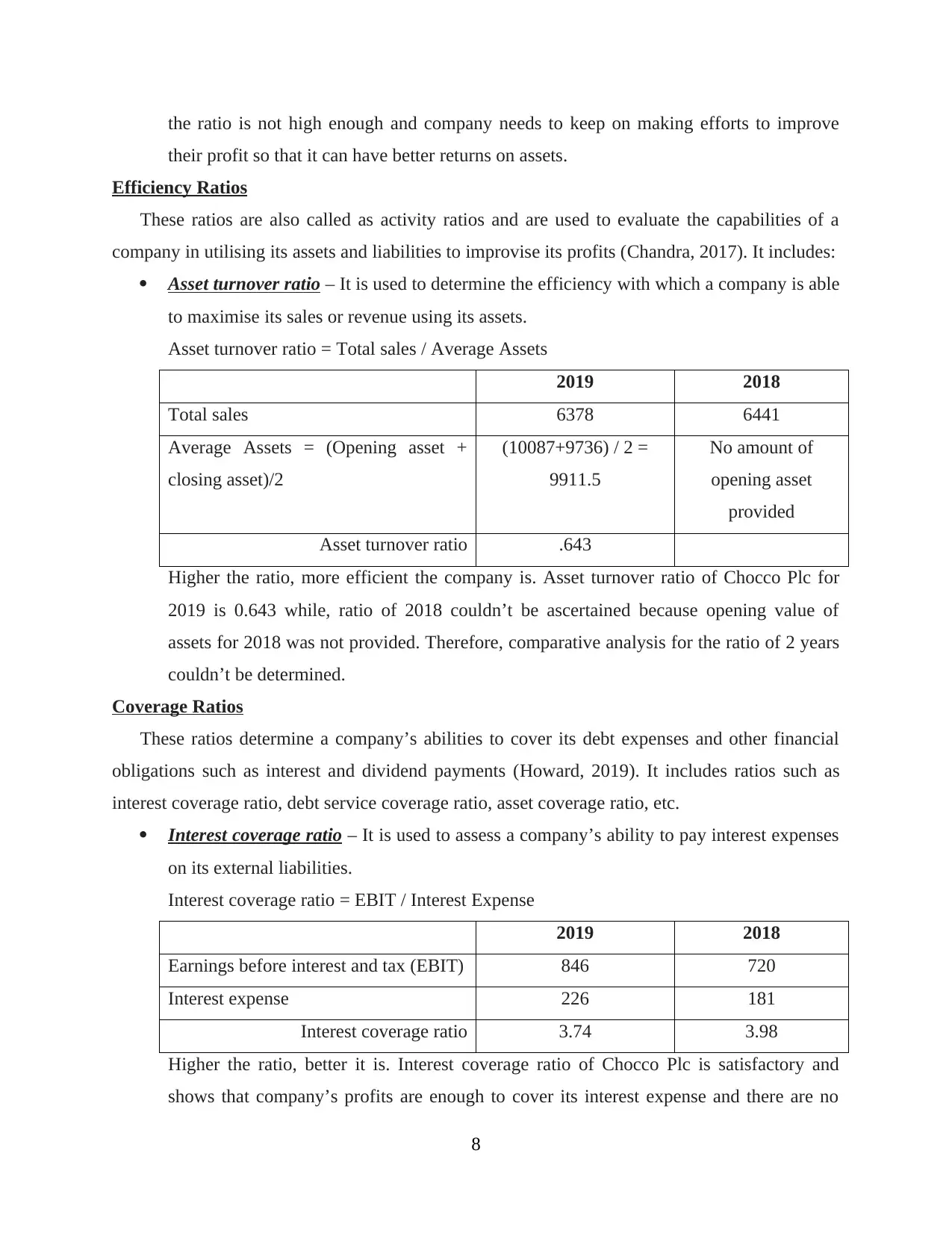

Asset turnover ratio – It is used to determine the efficiency with which a company is able

to maximise its sales or revenue using its assets.

Asset turnover ratio = Total sales / Average Assets

2019 2018

Total sales 6378 6441

Average Assets = (Opening asset +

closing asset)/2

(10087+9736) / 2 =

9911.5

No amount of

opening asset

provided

Asset turnover ratio .643

Higher the ratio, more efficient the company is. Asset turnover ratio of Chocco Plc for

2019 is 0.643 while, ratio of 2018 couldn’t be ascertained because opening value of

assets for 2018 was not provided. Therefore, comparative analysis for the ratio of 2 years

couldn’t be determined.

Coverage Ratios

These ratios determine a company’s abilities to cover its debt expenses and other financial

obligations such as interest and dividend payments (Howard, 2019). It includes ratios such as

interest coverage ratio, debt service coverage ratio, asset coverage ratio, etc.

Interest coverage ratio – It is used to assess a company’s ability to pay interest expenses

on its external liabilities.

Interest coverage ratio = EBIT / Interest Expense

2019 2018

Earnings before interest and tax (EBIT) 846 720

Interest expense 226 181

Interest coverage ratio 3.74 3.98

Higher the ratio, better it is. Interest coverage ratio of Chocco Plc is satisfactory and

shows that company’s profits are enough to cover its interest expense and there are no

8

their profit so that it can have better returns on assets.

Efficiency Ratios

These ratios are also called as activity ratios and are used to evaluate the capabilities of a

company in utilising its assets and liabilities to improvise its profits (Chandra, 2017). It includes:

Asset turnover ratio – It is used to determine the efficiency with which a company is able

to maximise its sales or revenue using its assets.

Asset turnover ratio = Total sales / Average Assets

2019 2018

Total sales 6378 6441

Average Assets = (Opening asset +

closing asset)/2

(10087+9736) / 2 =

9911.5

No amount of

opening asset

provided

Asset turnover ratio .643

Higher the ratio, more efficient the company is. Asset turnover ratio of Chocco Plc for

2019 is 0.643 while, ratio of 2018 couldn’t be ascertained because opening value of

assets for 2018 was not provided. Therefore, comparative analysis for the ratio of 2 years

couldn’t be determined.

Coverage Ratios

These ratios determine a company’s abilities to cover its debt expenses and other financial

obligations such as interest and dividend payments (Howard, 2019). It includes ratios such as

interest coverage ratio, debt service coverage ratio, asset coverage ratio, etc.

Interest coverage ratio – It is used to assess a company’s ability to pay interest expenses

on its external liabilities.

Interest coverage ratio = EBIT / Interest Expense

2019 2018

Earnings before interest and tax (EBIT) 846 720

Interest expense 226 181

Interest coverage ratio 3.74 3.98

Higher the ratio, better it is. Interest coverage ratio of Chocco Plc is satisfactory and

shows that company’s profits are enough to cover its interest expense and there are no

8

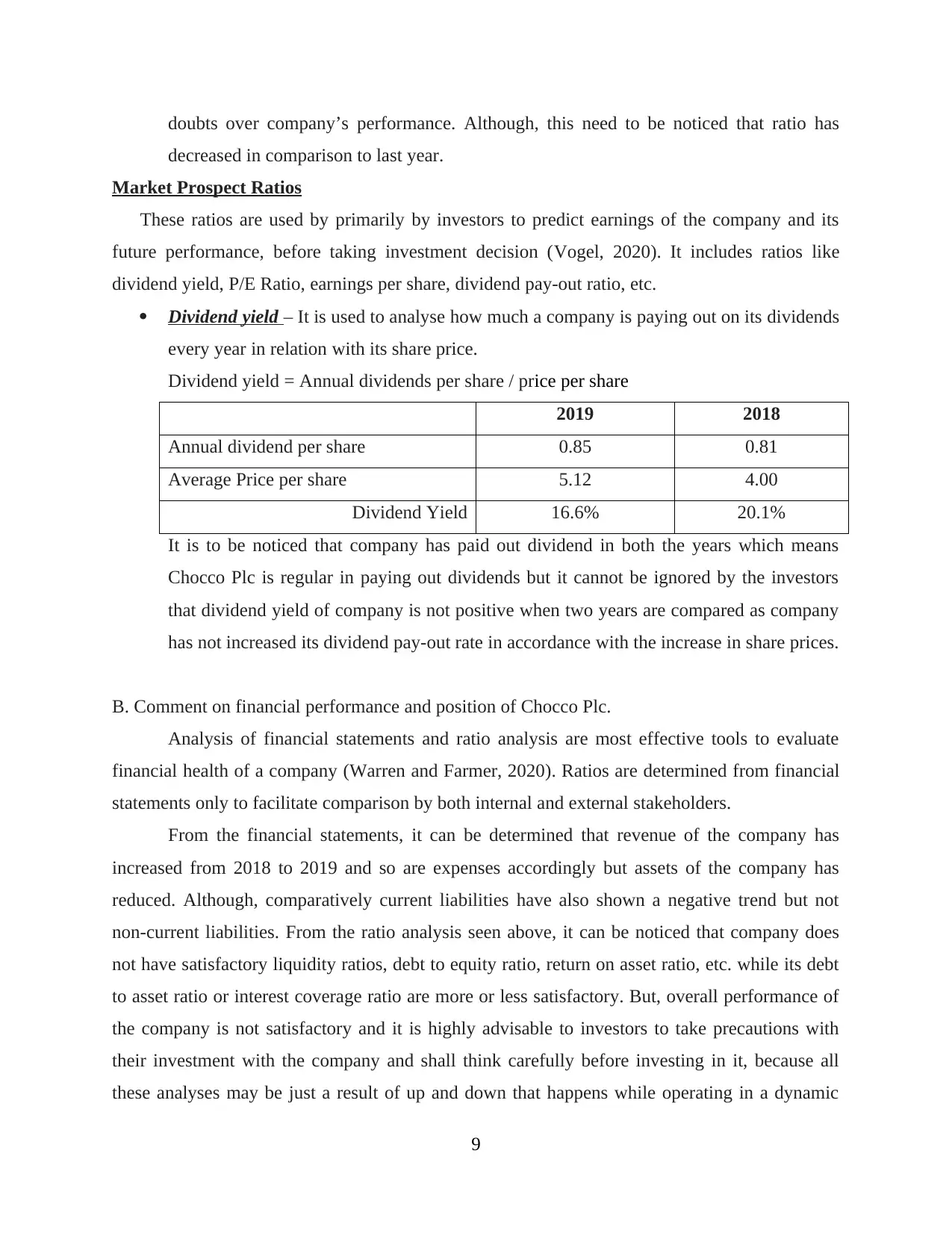

doubts over company’s performance. Although, this need to be noticed that ratio has

decreased in comparison to last year.

Market Prospect Ratios

These ratios are used by primarily by investors to predict earnings of the company and its

future performance, before taking investment decision (Vogel, 2020). It includes ratios like

dividend yield, P/E Ratio, earnings per share, dividend pay-out ratio, etc.

Dividend yield – It is used to analyse how much a company is paying out on its dividends

every year in relation with its share price.

Dividend yield = Annual dividends per share / price per share

2019 2018

Annual dividend per share 0.85 0.81

Average Price per share 5.12 4.00

Dividend Yield 16.6% 20.1%

It is to be noticed that company has paid out dividend in both the years which means

Chocco Plc is regular in paying out dividends but it cannot be ignored by the investors

that dividend yield of company is not positive when two years are compared as company

has not increased its dividend pay-out rate in accordance with the increase in share prices.

B. Comment on financial performance and position of Chocco Plc.

Analysis of financial statements and ratio analysis are most effective tools to evaluate

financial health of a company (Warren and Farmer, 2020). Ratios are determined from financial

statements only to facilitate comparison by both internal and external stakeholders.

From the financial statements, it can be determined that revenue of the company has

increased from 2018 to 2019 and so are expenses accordingly but assets of the company has

reduced. Although, comparatively current liabilities have also shown a negative trend but not

non-current liabilities. From the ratio analysis seen above, it can be noticed that company does

not have satisfactory liquidity ratios, debt to equity ratio, return on asset ratio, etc. while its debt

to asset ratio or interest coverage ratio are more or less satisfactory. But, overall performance of

the company is not satisfactory and it is highly advisable to investors to take precautions with

their investment with the company and shall think carefully before investing in it, because all

these analyses may be just a result of up and down that happens while operating in a dynamic

9

decreased in comparison to last year.

Market Prospect Ratios

These ratios are used by primarily by investors to predict earnings of the company and its

future performance, before taking investment decision (Vogel, 2020). It includes ratios like

dividend yield, P/E Ratio, earnings per share, dividend pay-out ratio, etc.

Dividend yield – It is used to analyse how much a company is paying out on its dividends

every year in relation with its share price.

Dividend yield = Annual dividends per share / price per share

2019 2018

Annual dividend per share 0.85 0.81

Average Price per share 5.12 4.00

Dividend Yield 16.6% 20.1%

It is to be noticed that company has paid out dividend in both the years which means

Chocco Plc is regular in paying out dividends but it cannot be ignored by the investors

that dividend yield of company is not positive when two years are compared as company

has not increased its dividend pay-out rate in accordance with the increase in share prices.

B. Comment on financial performance and position of Chocco Plc.

Analysis of financial statements and ratio analysis are most effective tools to evaluate

financial health of a company (Warren and Farmer, 2020). Ratios are determined from financial

statements only to facilitate comparison by both internal and external stakeholders.

From the financial statements, it can be determined that revenue of the company has

increased from 2018 to 2019 and so are expenses accordingly but assets of the company has

reduced. Although, comparatively current liabilities have also shown a negative trend but not

non-current liabilities. From the ratio analysis seen above, it can be noticed that company does

not have satisfactory liquidity ratios, debt to equity ratio, return on asset ratio, etc. while its debt

to asset ratio or interest coverage ratio are more or less satisfactory. But, overall performance of

the company is not satisfactory and it is highly advisable to investors to take precautions with

their investment with the company and shall think carefully before investing in it, because all

these analyses may be just a result of up and down that happens while operating in a dynamic

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business environment. Financial ratios of Chocco Plc are also needed to be compared with its

industry benchmark and competitors to know more about its market value, which is useful to

determine a company's worth for investors.

10

industry benchmark and competitors to know more about its market value, which is useful to

determine a company's worth for investors.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journal

Brown, R.G. and Johnston, K.S., 2019. Paciolo on accounting. Routledge.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

Tsadira-Pocha, Z., 2020. Fair value accounting hierarchy, value relevance, quality of financial

statements and procyclical leverage: an empirical analysis in context’ (Doctoral

dissertation, School of Business Administration).

Brown, M.T. and et.al., 2016. Financial management in the sport industry. Taylor & Francis.

Rachlin, R., 2019. Return on Investment Manual: Tools and Applications for Managing

Financial Results: Tools and Applications for Managing Financial Results. Routledge.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Howard, D.R., 2019. Financing sport. International Journal of Sport Communication, 12,

pp.306-309.

Vogel, H.L., 2020. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Warren, C.S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

11

Books and Journal

Brown, R.G. and Johnston, K.S., 2019. Paciolo on accounting. Routledge.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

Tsadira-Pocha, Z., 2020. Fair value accounting hierarchy, value relevance, quality of financial

statements and procyclical leverage: an empirical analysis in context’ (Doctoral

dissertation, School of Business Administration).

Brown, M.T. and et.al., 2016. Financial management in the sport industry. Taylor & Francis.

Rachlin, R., 2019. Return on Investment Manual: Tools and Applications for Managing

Financial Results: Tools and Applications for Managing Financial Results. Routledge.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Howard, D.R., 2019. Financing sport. International Journal of Sport Communication, 12,

pp.306-309.

Vogel, H.L., 2020. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Warren, C.S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.