Comprehensive Report on Accounting Fundamentals: Analysis & Techniques

VerifiedAdded on 2023/06/18

|10

|1715

|357

Report

AI Summary

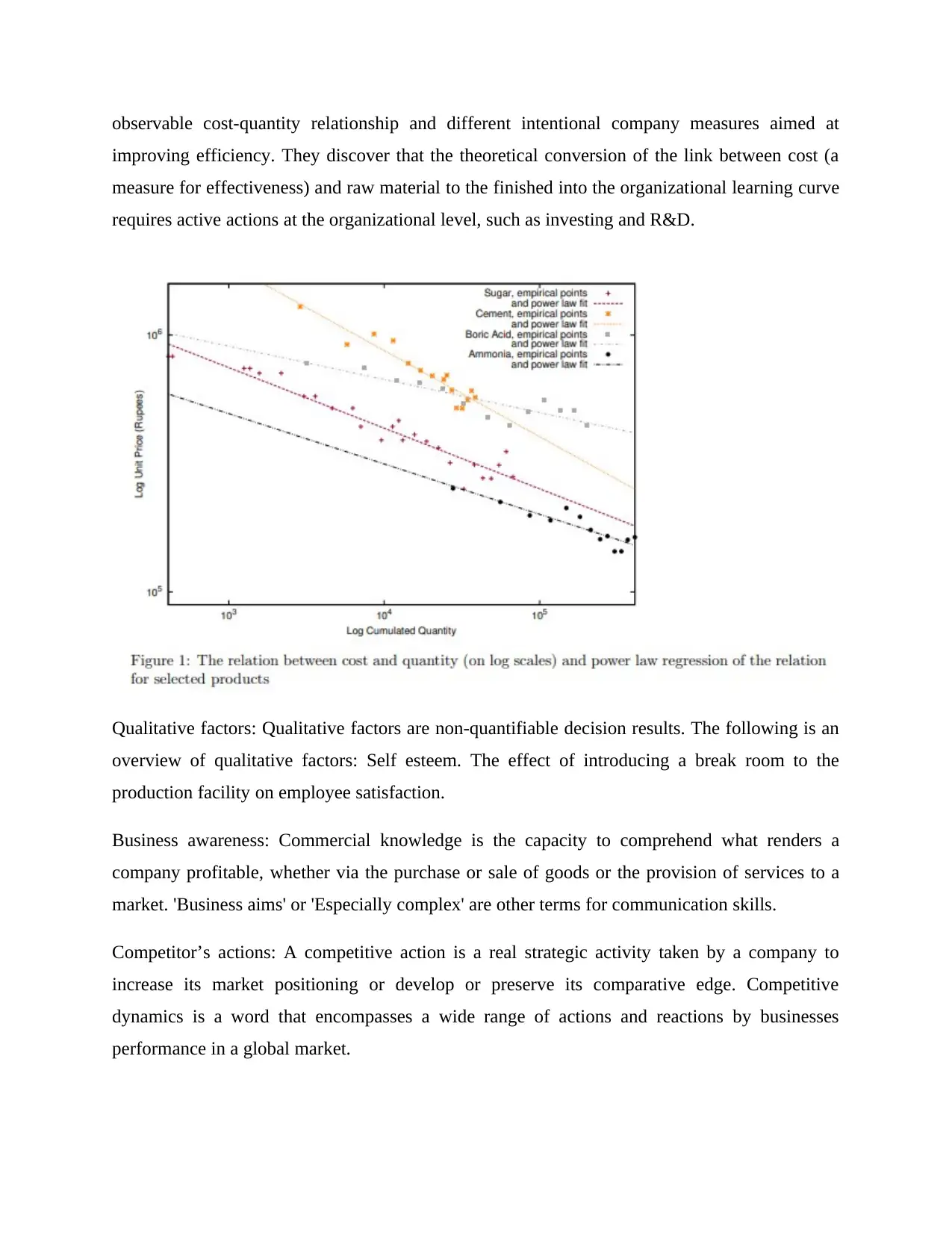

This report provides a comprehensive overview of accounting fundamentals, focusing on key concepts and techniques. It examines the limitations of linear and non-linear equations in representing cost-quantity relationships and discusses the impact of qualitative factors on decision-making. The report also explores the necessity of management accounting in business strategy formulation, planning, controlling activities, efficient resource utilization, and corporate governance. Furthermore, it analyzes various management accounting techniques such as break-even analysis, budgeting (including incremental and activity-based budgeting), and capital investment appraisal methods like net present value and accounting rate of return. The document concludes with a list of references, making it a valuable resource for students. Desklib provides this and many other solved assignments and past papers for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.