Accounting Fundamentals Assignment 2022

VerifiedAdded on 2022/09/10

|33

|1554

|27

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING FUNDAMENTALS 1

ACCOUNTING

FUNDAMENTALS

ACCOUNTING

FUNDAMENTALS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING FUNDAMENTALS 2

Task 1:

Part a:

Journal entries:

Particulars Debit Credit

Apr-05 Cash 300.00

Capital 300.00

Apr-07 Purchases 200.00

Accounts payable 200.00

Apr-08 Cash 250.00

Loan 250.00

Apr-15 Motor van 150.00

Cash 150.00

Task 1:

Part a:

Journal entries:

Particulars Debit Credit

Apr-05 Cash 300.00

Capital 300.00

Apr-07 Purchases 200.00

Accounts payable 200.00

Apr-08 Cash 250.00

Loan 250.00

Apr-15 Motor van 150.00

Cash 150.00

ACCOUNTING FUNDAMENTALS 3

Apr-20 Accounts receivables 350.00

Sales 350.00

Apr-28 Rent expense 50.00

Cash 50.00

Apr-29 Loan 200.00

Cash 200.00

Apr-30 Rent expense 60.00

Cash 60.00

Part b:

Particulars Debit Credit

Cash

240.0

0

Accounts receivables

350.0

0

Motor van

150.0

0

Loan

50.0

0

Accounts payable 350.0

Apr-20 Accounts receivables 350.00

Sales 350.00

Apr-28 Rent expense 50.00

Cash 50.00

Apr-29 Loan 200.00

Cash 200.00

Apr-30 Rent expense 60.00

Cash 60.00

Part b:

Particulars Debit Credit

Cash

240.0

0

Accounts receivables

350.0

0

Motor van

150.0

0

Loan

50.0

0

Accounts payable 350.0

ACCOUNTING FUNDAMENTALS 4

0

Capital

300.0

0

Drawings

60.0

0

Purchases

200.0

0

Sales

350.0

0

Rent expense

50.0

0

Total

1,050.0

0

1,050.0

0

-

Part c:

Statement of income

Particulars Amount

Sales 350.00

0

Capital

300.0

0

Drawings

60.0

0

Purchases

200.0

0

Sales

350.0

0

Rent expense

50.0

0

Total

1,050.0

0

1,050.0

0

-

Part c:

Statement of income

Particulars Amount

Sales 350.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING FUNDAMENTALS 5

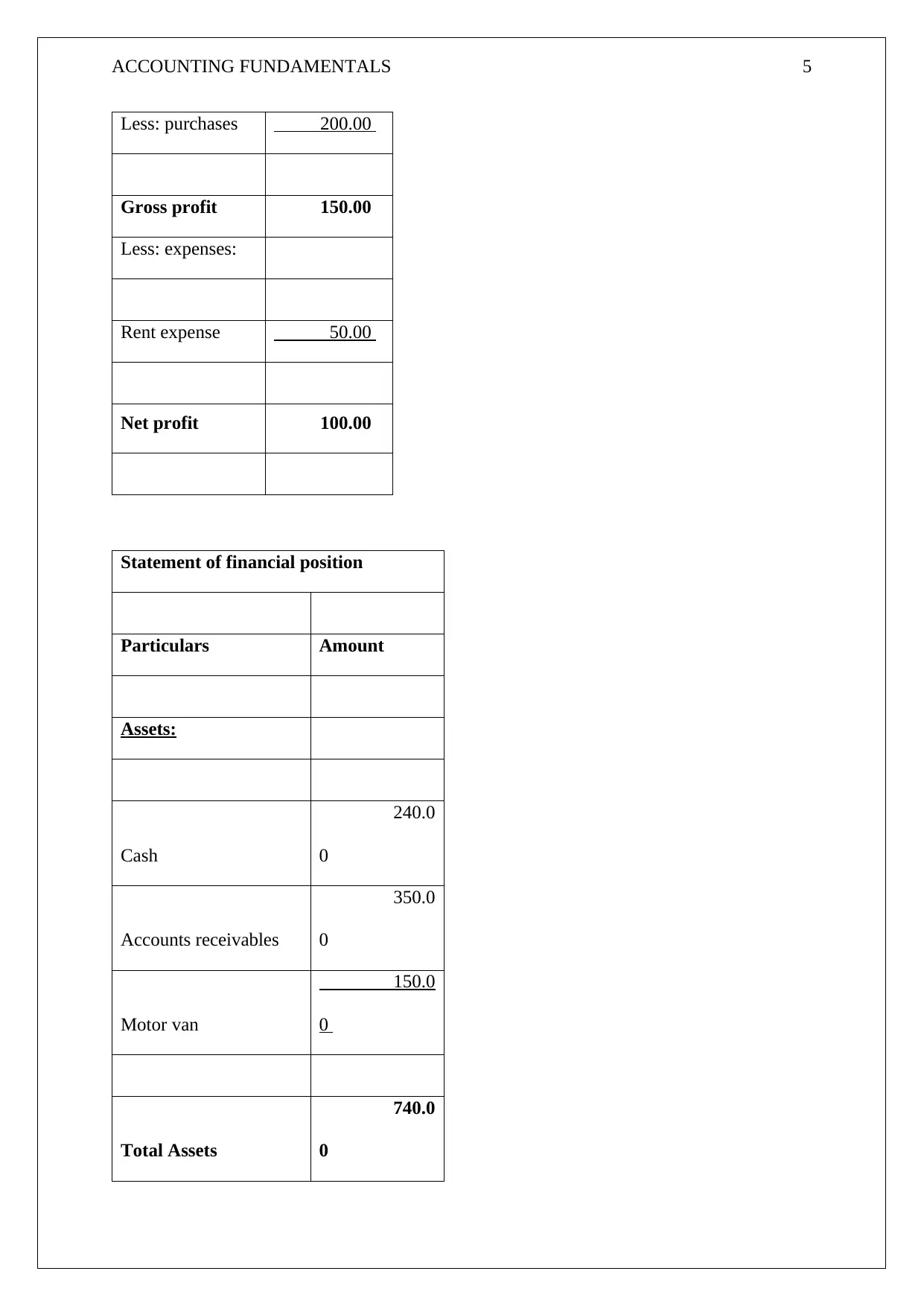

Less: purchases 200.00

Gross profit 150.00

Less: expenses:

Rent expense 50.00

Net profit 100.00

Statement of financial position

Particulars Amount

Assets:

Cash

240.0

0

Accounts receivables

350.0

0

Motor van

150.0

0

Total Assets

740.0

0

Less: purchases 200.00

Gross profit 150.00

Less: expenses:

Rent expense 50.00

Net profit 100.00

Statement of financial position

Particulars Amount

Assets:

Cash

240.0

0

Accounts receivables

350.0

0

Motor van

150.0

0

Total Assets

740.0

0

ACCOUNTING FUNDAMENTALS 6

Liabilities and

shareholders equity:

Loan

50.0

0

Accounts payable

350.0

0

Capital less drawings

340.0

0

Total liabilities and

shareholders equity 740

Task 2:

Part a:

Cash Purchases Motor Van Loan

Part

icula

rs

De

bit

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it Credit

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

J

a

Capi 5

,00

J

a

Ca 1

3

J

a

Ca 6

0

J

a

Ca 1

0

Liabilities and

shareholders equity:

Loan

50.0

0

Accounts payable

350.0

0

Capital less drawings

340.0

0

Total liabilities and

shareholders equity 740

Task 2:

Part a:

Cash Purchases Motor Van Loan

Part

icula

rs

De

bit

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it Credit

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

J

a

Capi 5

,00

J

a

Ca 1

3

J

a

Ca 6

0

J

a

Ca 1

0

ACCOUNTING FUNDAMENTALS 7

n

-

0

1 tal

0.0

0

n

-

0

3 sh

0

0

n

-

0

2 sh 0

n

-

0

4 sh

0

0

J

a

n

-

0

2

Mot

or

van

6

0

0

J

a

n

-

2

7

Ca

sh

3

5

0

J

a

n

-

0

3

Purc

hase

s

1

3

0

0

J

a

n

-

0

4 Loan

10

00

J

a

n

Mot

or

expe

2

0

0

n

-

0

1 tal

0.0

0

n

-

0

3 sh

0

0

n

-

0

2 sh 0

n

-

0

4 sh

0

0

J

a

n

-

0

2

Mot

or

van

6

0

0

J

a

n

-

2

7

Ca

sh

3

5

0

J

a

n

-

0

3

Purc

hase

s

1

3

0

0

J

a

n

-

0

4 Loan

10

00

J

a

n

Mot

or

expe

2

0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS 8

-

1

0 nses

J

a

n

-

2

4

Stor

age

expe

nses

1

5

0

J

a

n

-

2

0

Sale

s

80

0

J

a

n

-

2

7 Loan

3

5

0

J

a

n

-

Dra

wing

s

1

7

5

-

1

0 nses

J

a

n

-

2

4

Stor

age

expe

nses

1

5

0

J

a

n

-

2

0

Sale

s

80

0

J

a

n

-

2

7 Loan

3

5

0

J

a

n

-

Dra

wing

s

1

7

5

ACCOUNTING FUNDAMENTALS 9

3

0

Motor

expenses Capital Drawings Sales

Part

icula

rs

De

bit

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it Credit

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

J

a

n

-

1

0 Cash

20

0

J

a

n

-

0

1

Ca

sh 5,000.00

J

a

n

-

3

0

Ca

sh

1

7

5

J

a

n

-

2

0

Ca

sh

8

0

0

Storage

expenses

Part

icula

rs

De

bit

C

r

e

di

3

0

Motor

expenses Capital Drawings Sales

Part

icula

rs

De

bit

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it Credit

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

Pa

rti

cul

ars

D

e

b

it

C

r

e

di

t

J

a

n

-

1

0 Cash

20

0

J

a

n

-

0

1

Ca

sh 5,000.00

J

a

n

-

3

0

Ca

sh

1

7

5

J

a

n

-

2

0

Ca

sh

8

0

0

Storage

expenses

Part

icula

rs

De

bit

C

r

e

di

ACCOUNTING FUNDAMENTALS 10

t

J

a

n

-

2

4 Cash

15

0

Journal entries:

Particulars Debit Credit

Jan-01 Cash 5,000.00

Capital 5,000.00

Jan-02 Motor van 600.00

Cash 600.00

Jan-03 Purchases 1,300.00

Accounts payable 1,300.00

Jan-04 Cash 1,000.00

t

J

a

n

-

2

4 Cash

15

0

Journal entries:

Particulars Debit Credit

Jan-01 Cash 5,000.00

Capital 5,000.00

Jan-02 Motor van 600.00

Cash 600.00

Jan-03 Purchases 1,300.00

Accounts payable 1,300.00

Jan-04 Cash 1,000.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING FUNDAMENTALS 11

Loan 1,000.00

Jan-10 Motor expense 200.00

Cash 200.00

Jan-13 Accounts receivables 300.00

Sales 300.00

Jan-20 Accounts receivables 500.00

Sales 500.00

Jan-24 Storage expense 150.00

Cash 150.00

Jan-27 Loan 350.00

Cash 350.00

Jan-30 Drawings 175.00

Cash 175.00

Part b:

Particulars Debit Credit

Cash 4,025.0

Loan 1,000.00

Jan-10 Motor expense 200.00

Cash 200.00

Jan-13 Accounts receivables 300.00

Sales 300.00

Jan-20 Accounts receivables 500.00

Sales 500.00

Jan-24 Storage expense 150.00

Cash 150.00

Jan-27 Loan 350.00

Cash 350.00

Jan-30 Drawings 175.00

Cash 175.00

Part b:

Particulars Debit Credit

Cash 4,025.0

ACCOUNTING FUNDAMENTALS 12

0

Motor van

600.0

0

Drawings

175.0

0

Loan

650.0

0

Capital

5,000.0

0

Purchases

1,300.0

0

Sales

800.0

0

Motor expenses

200.0

0

Storage expenses

150.0

0

Total

6,450.0

0

6,450.0

0

Part c:

Statement of income

Particulars Amount

0

Motor van

600.0

0

Drawings

175.0

0

Loan

650.0

0

Capital

5,000.0

0

Purchases

1,300.0

0

Sales

800.0

0

Motor expenses

200.0

0

Storage expenses

150.0

0

Total

6,450.0

0

6,450.0

0

Part c:

Statement of income

Particulars Amount

ACCOUNTING FUNDAMENTALS 13

Sales

800.

00

Less: cost of goods

sold

500.

00

Gross profit

300.

00

Less: expenses:

Motor expenses

200.

00

Storage expenses

150.

00

Net profit

-

50.00

Statement of financial position

Particulars Amount

Assets:

Cash 4,025.0

Sales

800.

00

Less: cost of goods

sold

500.

00

Gross profit

300.

00

Less: expenses:

Motor expenses

200.

00

Storage expenses

150.

00

Net profit

-

50.00

Statement of financial position

Particulars Amount

Assets:

Cash 4,025.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

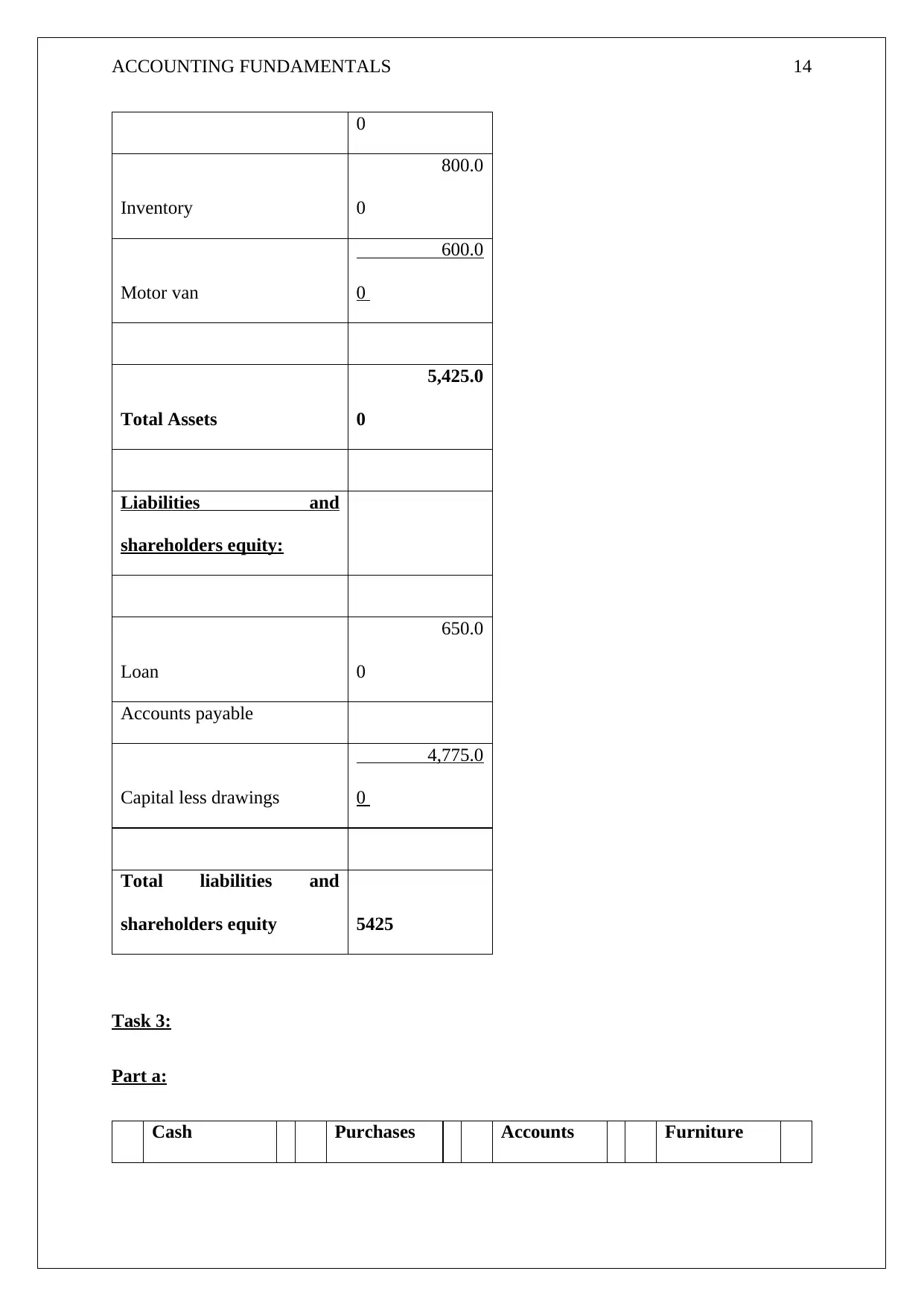

ACCOUNTING FUNDAMENTALS 14

0

Inventory

800.0

0

Motor van

600.0

0

Total Assets

5,425.0

0

Liabilities and

shareholders equity:

Loan

650.0

0

Accounts payable

Capital less drawings

4,775.0

0

Total liabilities and

shareholders equity 5425

Task 3:

Part a:

Cash Purchases Accounts Furniture

0

Inventory

800.0

0

Motor van

600.0

0

Total Assets

5,425.0

0

Liabilities and

shareholders equity:

Loan

650.0

0

Accounts payable

Capital less drawings

4,775.0

0

Total liabilities and

shareholders equity 5425

Task 3:

Part a:

Cash Purchases Accounts Furniture

ACCOUNTING FUNDAMENTALS 15

payable and fixtures

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

Part

icul

ars

D

e

b

it

C

r

e

d

it

Parti

cular

s

D

e

b

it

C

r

e

d

it

J

a

n

-

0

1

Openi

ng

balan

ce

34

3.

00

J

a

n

-

0

5

Acc

ount

s

paya

ble

1

5

0

J

a

n

-

0

1

Ope

ning

bala

nce

3

3

J

a

n

-

0

1

Openi

ng

balan

ce

1

9

8

J

a

n

-

0

1

J

a

n

-

0

7

Acco

unts

receiv

ables 18

J

a

n

-

1

4 Cash

7

5

J

a

n

-

0

7

Cas

h

1

8

J

a

n

-

0

9

Acco

unts

payab

le

2

1

J

a

n

-

0

9

Cas

h

2

1

payable and fixtures

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

Part

icul

ars

D

e

b

it

C

r

e

d

it

Parti

cular

s

D

e

b

it

C

r

e

d

it

J

a

n

-

0

1

Openi

ng

balan

ce

34

3.

00

J

a

n

-

0

5

Acc

ount

s

paya

ble

1

5

0

J

a

n

-

0

1

Ope

ning

bala

nce

3

3

J

a

n

-

0

1

Openi

ng

balan

ce

1

9

8

J

a

n

-

0

1

J

a

n

-

0

7

Acco

unts

receiv

ables 18

J

a

n

-

1

4 Cash

7

5

J

a

n

-

0

7

Cas

h

1

8

J

a

n

-

0

9

Acco

unts

payab

le

2

1

J

a

n

-

0

9

Cas

h

2

1

ACCOUNTING FUNDAMENTALS 16

J

a

n

-

0

9 Sales 64

J

a

n

-

1

5

Cas

h

1

2

J

a

n

-

1

4

Wage

s

1

4

J

a

n

-

1

4

Purch

ases

7

5

J

a

n

-

1

5

Acco

unts

payab

le

1

2

J Offic 3

J

a

n

-

0

9 Sales 64

J

a

n

-

1

5

Cas

h

1

2

J

a

n

-

1

4

Wage

s

1

4

J

a

n

-

1

4

Purch

ases

7

5

J

a

n

-

1

5

Acco

unts

payab

le

1

2

J Offic 3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING FUNDAMENTALS 17

a

n

-

2

0

e

desk 2

J

a

n

-

2

1

Wage

s

1

7

J

a

n

-

2

1 Sales

11

0

J

a

n

-

2

3

Offic

e

expen

ses 3

J

a

Acco

unts

25

a

n

-

2

0

e

desk 2

J

a

n

-

2

1

Wage

s

1

7

J

a

n

-

2

1 Sales

11

0

J

a

n

-

2

3

Offic

e

expen

ses 3

J

a

Acco

unts

25

ACCOUNTING FUNDAMENTALS 18

n

-

2

8

receiv

ables

J

a

n

-

2

8 Sales 84

J

a

n

-

3

1 Sales 30

J

a

n

-

2

8

Wage

s 15

Office desk

Office

expenses Drawings Sales

n

-

2

8

receiv

ables

J

a

n

-

2

8 Sales 84

J

a

n

-

3

1 Sales 30

J

a

n

-

2

8

Wage

s 15

Office desk

Office

expenses Drawings Sales

ACCOUNTING FUNDAMENTALS 19

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

Part

icul

ars

D

e

b

it

C

r

e

d

it

Parti

cular

s

D

e

b

it

C

r

e

d

it

J

a

n

-

2

0 Cash 32

J

a

n

-

2

3 Cash 3

J

a

n

-

0

2

Acco

unts

receiv

ables

1

2

4

J

a

n

-

1

1

Acco

unts

receiv

ables

6

4

J

a

n

-

2

4 Cash

1

1

0

J Cash 8

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

Part

icul

ars

D

e

b

it

C

r

e

d

it

Parti

cular

s

D

e

b

it

C

r

e

d

it

J

a

n

-

2

0 Cash 32

J

a

n

-

2

3 Cash 3

J

a

n

-

0

2

Acco

unts

receiv

ables

1

2

4

J

a

n

-

1

1

Acco

unts

receiv

ables

6

4

J

a

n

-

2

4 Cash

1

1

0

J Cash 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS 20

a

n

-

2

8 4

Wages

expense

Accounts

receivables

J

a

n

-

3

1 Cash

3

0

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

J

a

n

-

0

5 Cash 12

J

a

n

-

0

1

Ope

ning

bala

nce

8

3

J

a

n

Cash 14 J

a

n

Sale

s

1

2

4

a

n

-

2

8 4

Wages

expense

Accounts

receivables

J

a

n

-

3

1 Cash

3

0

Parti

cular

s

De

bi

t

C

r

e

d

it

Part

icula

rs

D

e

b

it

C

r

e

d

it

J

a

n

-

0

5 Cash 12

J

a

n

-

0

1

Ope

ning

bala

nce

8

3

J

a

n

Cash 14 J

a

n

Sale

s

1

2

4

ACCOUNTING FUNDAMENTALS 21

-

1

4

-

0

2

J

a

n

-

2

1 Cash 17

J

a

n

-

2

3 Cash

2

5

J

a

n

-

2

8 Cash 15

Journal entries:

Particulars Debit Credit

Jan-

02 Accounts receivables 124.00

Sales 124.00

Jan- Wages 12

-

1

4

-

0

2

J

a

n

-

2

1 Cash 17

J

a

n

-

2

3 Cash

2

5

J

a

n

-

2

8 Cash 15

Journal entries:

Particulars Debit Credit

Jan-

02 Accounts receivables 124.00

Sales 124.00

Jan- Wages 12

ACCOUNTING FUNDAMENTALS 22

05

Cash 12.00

Jan-

07 Purchases 150

Accounts payable 150.00

Jan-

09 Accounts payable 21.00

Cash 21.00

Jan-

11 Cash 64.00

Sales 64.00

Jan-

14 Wages 14.00

Cash 14.00

Jan-

15 Purchases 75.00

Accounts payable 75.00

Jan-

15 Accounts payable 12.00

Cash 12.00

05

Cash 12.00

Jan-

07 Purchases 150

Accounts payable 150.00

Jan-

09 Accounts payable 21.00

Cash 21.00

Jan-

11 Cash 64.00

Sales 64.00

Jan-

14 Wages 14.00

Cash 14.00

Jan-

15 Purchases 75.00

Accounts payable 75.00

Jan-

15 Accounts payable 12.00

Cash 12.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

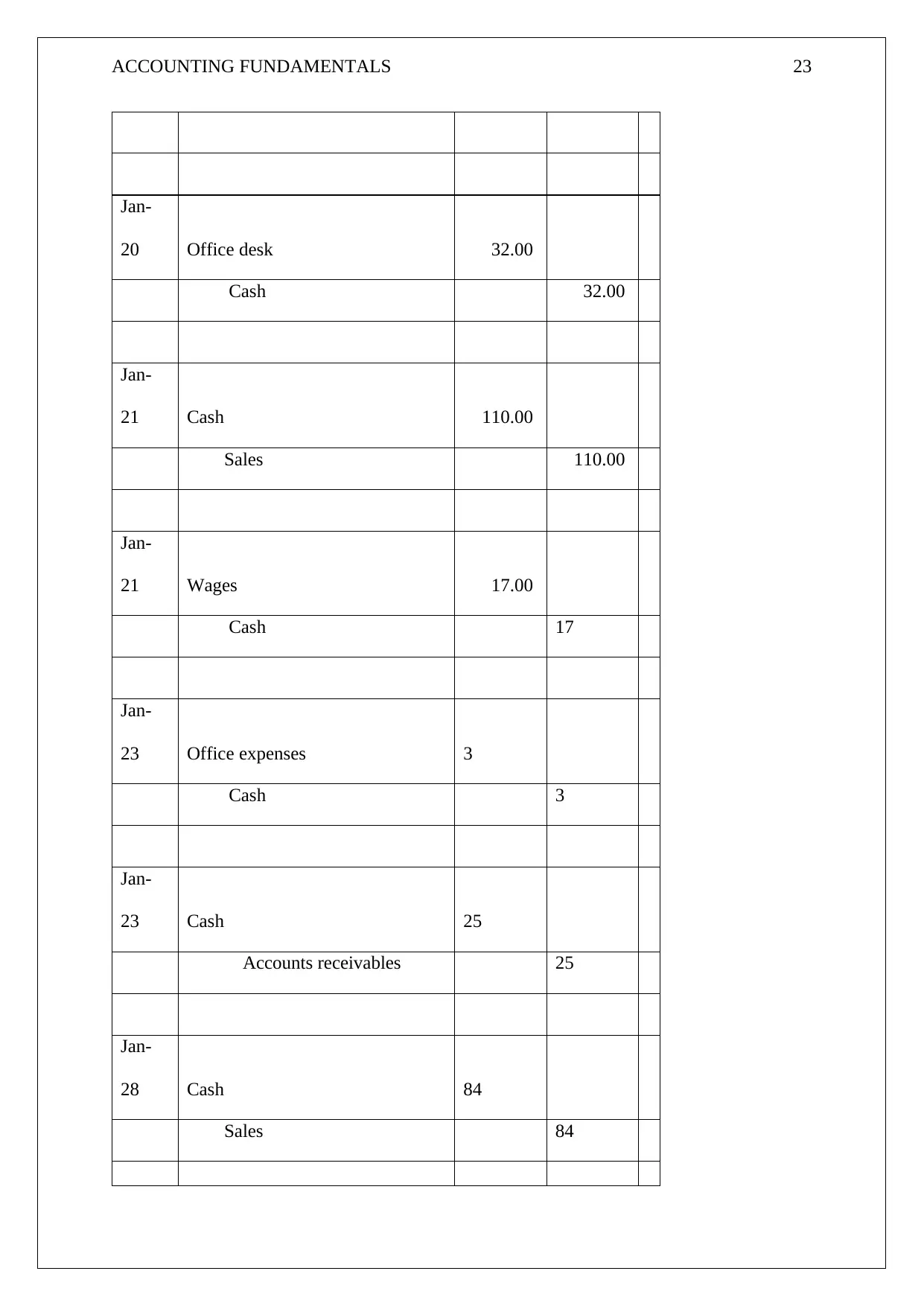

ACCOUNTING FUNDAMENTALS 23

Jan-

20 Office desk 32.00

Cash 32.00

Jan-

21 Cash 110.00

Sales 110.00

Jan-

21 Wages 17.00

Cash 17

Jan-

23 Office expenses 3

Cash 3

Jan-

23 Cash 25

Accounts receivables 25

Jan-

28 Cash 84

Sales 84

Jan-

20 Office desk 32.00

Cash 32.00

Jan-

21 Cash 110.00

Sales 110.00

Jan-

21 Wages 17.00

Cash 17

Jan-

23 Office expenses 3

Cash 3

Jan-

23 Cash 25

Accounts receivables 25

Jan-

28 Cash 84

Sales 84

ACCOUNTING FUNDAMENTALS 24

Jan-

28 Wages 15

Cash 15

Jan-

31 Cash 30

Sales 30

Part b:

Particulars Debit Credit

Cash in hand

473.0

0

Inventory

458.0

0

Furniture and fixtures

198.0

0

Receivables

164.0

0

Office desk

32.0

0

Accounts payable

150.0

0

Jan-

28 Wages 15

Cash 15

Jan-

31 Cash 30

Sales 30

Part b:

Particulars Debit Credit

Cash in hand

473.0

0

Inventory

458.0

0

Furniture and fixtures

198.0

0

Receivables

164.0

0

Office desk

32.0

0

Accounts payable

150.0

0

ACCOUNTING FUNDAMENTALS 25

Capital

1,049.0

0

Sales

412.0

0

Purchases

225.0

0

Wages expenses

58.0

0

Office expenses

3.0

0

Total

1,611.0

0

1,611.0

0

Part c:

Statement of income

Particulars Amount

Sales 412.00

Less: cost of goods sold 309.00

Capital

1,049.0

0

Sales

412.0

0

Purchases

225.0

0

Wages expenses

58.0

0

Office expenses

3.0

0

Total

1,611.0

0

1,611.0

0

Part c:

Statement of income

Particulars Amount

Sales 412.00

Less: cost of goods sold 309.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS 26

Gross profit 103.00

Less: expenses:

Wages expenses 58.00

Office expenses 3.00

Net profit 42.00

Statement of financial position

Particulars Amount

Assets:

Cash

473.0

0

Inventory

374.0

0

Furniture and fixtures

198.0

0

Receivables

164.0

0

Office desk

32.0

0

Gross profit 103.00

Less: expenses:

Wages expenses 58.00

Office expenses 3.00

Net profit 42.00

Statement of financial position

Particulars Amount

Assets:

Cash

473.0

0

Inventory

374.0

0

Furniture and fixtures

198.0

0

Receivables

164.0

0

Office desk

32.0

0

ACCOUNTING FUNDAMENTALS 27

Total Assets

1,241.0

0

Liabilities and

shareholders equity:

Accounts payable

150.0

0

Capital less drawings

1,091.0

0

Total liabilities and

shareholders equity

1,241.0

0

-

Task 4:

Particulars Debit Credit

Accounts

receivables -

Accounts payable

4,850.0

0

Cash 6,505.0

Total Assets

1,241.0

0

Liabilities and

shareholders equity:

Accounts payable

150.0

0

Capital less drawings

1,091.0

0

Total liabilities and

shareholders equity

1,241.0

0

-

Task 4:

Particulars Debit Credit

Accounts

receivables -

Accounts payable

4,850.0

0

Cash 6,505.0

ACCOUNTING FUNDAMENTALS 28

0

Sales

22,075.0

0

Purchases

20,420.0

0

Total

26,925.0

0

26,925.0

0

Claire

Particulars Debit Credit

Jun-02 Sales 8,075.00

Jun-22 Sales return 1,000.00

Jun-24 Cash 7,075.00

Total -

Jane

Particulars Debit Credit

Jun-20 Sales 6,000.00

0

Sales

22,075.0

0

Purchases

20,420.0

0

Total

26,925.0

0

26,925.0

0

Claire

Particulars Debit Credit

Jun-02 Sales 8,075.00

Jun-22 Sales return 1,000.00

Jun-24 Cash 7,075.00

Total -

Jane

Particulars Debit Credit

Jun-20 Sales 6,000.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING FUNDAMENTALS 29

Total 6,000.00

Georgina

Particulars Debit Credit

Jun-13 Purchases

11,160.0

0

Jun-25 Cash

11,160.0

0

Total -

Andrew

Particular

s Debit Credit

Jun-21 Purchases

4,410.0

0

Jun-27 Cash

4,410.0

0

Total 6,000.00

Georgina

Particulars Debit Credit

Jun-13 Purchases

11,160.0

0

Jun-25 Cash

11,160.0

0

Total -

Andrew

Particular

s Debit Credit

Jun-21 Purchases

4,410.0

0

Jun-27 Cash

4,410.0

0

ACCOUNTING FUNDAMENTALS 30

Total 0

Hywel

Particulars Debit Credit

Jun-14 Sales

9,000.0

0

Jun-25 Cash

9,000.0

0

Total -

Mandy

Particulars Debit Credit

Jun-24 Purchases

4,850.0

0

Total

4,850.0

0

Total 0

Hywel

Particulars Debit Credit

Jun-14 Sales

9,000.0

0

Jun-25 Cash

9,000.0

0

Total -

Mandy

Particulars Debit Credit

Jun-24 Purchases

4,850.0

0

Total

4,850.0

0

ACCOUNTING FUNDAMENTALS 31

Task 5:

The capital expenditures are the expenses that are incurred on the fixed assets. These are the

expense that are expected to be incurred on the productive assets of the company and are

usually of a long term in nature whereas, the revenue expenditure is the one which is

connected with any specific revenue transaction or an operating period. The expense include

the cost of goods sold or the repairs and the maintenance expenses. Hence, the difference

between the above stated 2 expense are as follows:

With regard to riming of these expense, the capital expenditures are charged as an

expense over a longer period of time through the charging of depreciation expenses

whereas the revenue expenditure is the one which is charged as an expense in the

current period of after a short period of time.

With regard to consumption, the capital expenditure is assumed to have been

consumed over the period of the useful life of the fixed asset.

With regard to size, the capital expenses involve a much more amount when

compared with the amount involved in the revenue expenditure. This is mainly due to

the fact that the expense is classified as the capital expenditure in case the same is

more than the threshold value and if not, then the same is considered to be a revenue

expenditure. But then there is a certain a huge amount of expense which could still be

classified as the revenue expenditure as long as the same is connected with the sale of

the transactions or the period costs (Accounting tools, 2019).

The capital expenditure is incurred when the fixed assets are purchased whereas the

revenue expenditure is incurred on the day to day business operations of the company

and also, on the maintenance of the fixed assets.

Task 5:

The capital expenditures are the expenses that are incurred on the fixed assets. These are the

expense that are expected to be incurred on the productive assets of the company and are

usually of a long term in nature whereas, the revenue expenditure is the one which is

connected with any specific revenue transaction or an operating period. The expense include

the cost of goods sold or the repairs and the maintenance expenses. Hence, the difference

between the above stated 2 expense are as follows:

With regard to riming of these expense, the capital expenditures are charged as an

expense over a longer period of time through the charging of depreciation expenses

whereas the revenue expenditure is the one which is charged as an expense in the

current period of after a short period of time.

With regard to consumption, the capital expenditure is assumed to have been

consumed over the period of the useful life of the fixed asset.

With regard to size, the capital expenses involve a much more amount when

compared with the amount involved in the revenue expenditure. This is mainly due to

the fact that the expense is classified as the capital expenditure in case the same is

more than the threshold value and if not, then the same is considered to be a revenue

expenditure. But then there is a certain a huge amount of expense which could still be

classified as the revenue expenditure as long as the same is connected with the sale of

the transactions or the period costs (Accounting tools, 2019).

The capital expenditure is incurred when the fixed assets are purchased whereas the

revenue expenditure is incurred on the day to day business operations of the company

and also, on the maintenance of the fixed assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS 32

With regard to the earning capacity, the capital expenditure leads to an increase in the

earning capacity of the company whereas the revenue expenditure does not lead to an

increase in the existing capacity of the asset.

The capital ensue is incurred for the capital items and hence are recorded on the assets

size of the balance sheet whereas the revenue expense is incurred for the purposes of

book keeping in accounting (Accounting coach, 2019).

The benefits of capital expense are spread over a period of years whereas the benefits

of revenue expense are for a limited period of time or for an accounting year only.

The capital expense is non-recurring in nature and is one time in nature whereas the

revenue expense is recurring and is regular in nature

The amount spent on fixed assets is considered as the capital expenditure whereas the

money spent on the fixed asset after the same has been used is considered to be a

revenue expenditure.

The capital expense leads to the acquisition of the assets and the same is used for the

purposes of earning profits and then the same s sold once they become unfit for the

business whereas the revenue expense does not result in the acquisition of the asset

and the same is considered as the daily activity (Toppr, 2019).

With regard to the earning capacity, the capital expenditure leads to an increase in the

earning capacity of the company whereas the revenue expenditure does not lead to an

increase in the existing capacity of the asset.

The capital ensue is incurred for the capital items and hence are recorded on the assets

size of the balance sheet whereas the revenue expense is incurred for the purposes of

book keeping in accounting (Accounting coach, 2019).

The benefits of capital expense are spread over a period of years whereas the benefits

of revenue expense are for a limited period of time or for an accounting year only.

The capital expense is non-recurring in nature and is one time in nature whereas the

revenue expense is recurring and is regular in nature

The amount spent on fixed assets is considered as the capital expenditure whereas the

money spent on the fixed asset after the same has been used is considered to be a

revenue expenditure.

The capital expense leads to the acquisition of the assets and the same is used for the

purposes of earning profits and then the same s sold once they become unfit for the

business whereas the revenue expense does not result in the acquisition of the asset

and the same is considered as the daily activity (Toppr, 2019).

ACCOUNTING FUNDAMENTALS 33

References:

AccountingCoach.com. (2019). What is a capital expenditure versus a revenue expenditure?

| AccountingCoach. [online] Available at: https://www.accountingcoach.com/blog/capital-

expenditure-revenue-expenditure [Accessed 18 Dec. 2019].

AccountingTools. (2019). The difference between capital expenditures and revenue

expenditures — AccountingTools. [online] Available at:

https://www.accountingtools.com/articles/the-difference-between-capital-expenditures-and-

revenue-expe.html [Accessed 18 Dec. 2019].

Topdifferences.com. (2019). Difference between Capital Expenditure and Revenue

Expenditure. [online] Available at: https://topdifferences.com/difference-between-capital-

expenditure-and-revenue-expenditure/ [Accessed 18 Dec. 2019].

References:

AccountingCoach.com. (2019). What is a capital expenditure versus a revenue expenditure?

| AccountingCoach. [online] Available at: https://www.accountingcoach.com/blog/capital-

expenditure-revenue-expenditure [Accessed 18 Dec. 2019].

AccountingTools. (2019). The difference between capital expenditures and revenue

expenditures — AccountingTools. [online] Available at:

https://www.accountingtools.com/articles/the-difference-between-capital-expenditures-and-

revenue-expe.html [Accessed 18 Dec. 2019].

Topdifferences.com. (2019). Difference between Capital Expenditure and Revenue

Expenditure. [online] Available at: https://topdifferences.com/difference-between-capital-

expenditure-and-revenue-expenditure/ [Accessed 18 Dec. 2019].

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.