Accounting Fundamentals Report: Financial Analysis and Reporting, 2023

VerifiedAdded on 2023/01/09

|11

|2919

|93

Report

AI Summary

This report provides a comprehensive analysis of accounting fundamentals. It begins with an income statement and statement of position for the year 2019, including detailed calculations and working notes. The report then delves into ratio analysis, comparing financial data from 2018 and 2019 to assess profitability, efficiency, and liquidity. Key ratios such as Return on Equity (ROE), Earnings Per Share (EPS), Gross Profit Ratio, and Current Ratio are calculated and analyzed to evaluate the company's performance. The report further identifies and discusses three user groups of financial statements: owners and investors, management, and trade creditors, highlighting their respective needs and interests. Finally, the report examines the advantages and disadvantages of financial reporting, including its role in decision-making and the potential for manipulation or bias.

ACCOUNTING

FUNDAMENTALS

FUNDAMENTALS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

QUESTION 1..................................................................................................................................3

Question 2........................................................................................................................................4

a. calculation of ratios..................................................................................................................4

b. Analyzing the results...............................................................................................................5

QUESTION 3..................................................................................................................................7

(a).................................................................................................................................................7

(b).................................................................................................................................................8

(c).................................................................................................................................................8

REFERENCES..............................................................................................................................10

QUESTION 1..................................................................................................................................3

Question 2........................................................................................................................................4

a. calculation of ratios..................................................................................................................4

b. Analyzing the results...............................................................................................................5

QUESTION 3..................................................................................................................................7

(a).................................................................................................................................................7

(b).................................................................................................................................................8

(c).................................................................................................................................................8

REFERENCES..............................................................................................................................10

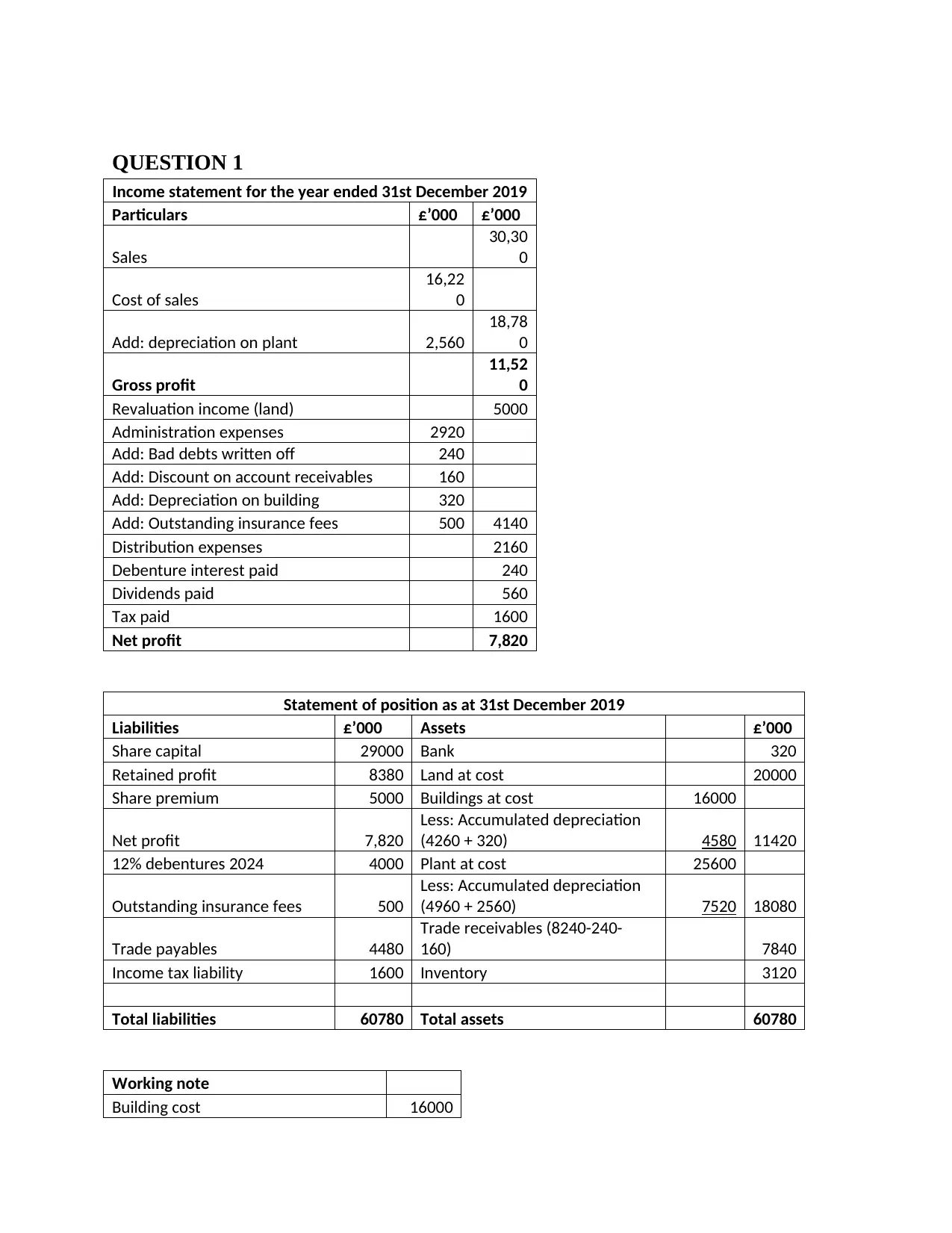

QUESTION 1

Income statement for the year ended 31st December 2019

Particulars £’000 £’000

Sales

30,30

0

Cost of sales

16,22

0

Add: depreciation on plant 2,560

18,78

0

Gross profit

11,52

0

Revaluation income (land) 5000

Administration expenses 2920

Add: Bad debts written off 240

Add: Discount on account receivables 160

Add: Depreciation on building 320

Add: Outstanding insurance fees 500 4140

Distribution expenses 2160

Debenture interest paid 240

Dividends paid 560

Tax paid 1600

Net profit 7,820

Statement of position as at 31st December 2019

Liabilities £’000 Assets £’000

Share capital 29000 Bank 320

Retained profit 8380 Land at cost 20000

Share premium 5000 Buildings at cost 16000

Net profit 7,820

Less: Accumulated depreciation

(4260 + 320) 4580 11420

12% debentures 2024 4000 Plant at cost 25600

Outstanding insurance fees 500

Less: Accumulated depreciation

(4960 + 2560) 7520 18080

Trade payables 4480

Trade receivables (8240-240-

160) 7840

Income tax liability 1600 Inventory 3120

Total liabilities 60780 Total assets 60780

Working note

Building cost 16000

Income statement for the year ended 31st December 2019

Particulars £’000 £’000

Sales

30,30

0

Cost of sales

16,22

0

Add: depreciation on plant 2,560

18,78

0

Gross profit

11,52

0

Revaluation income (land) 5000

Administration expenses 2920

Add: Bad debts written off 240

Add: Discount on account receivables 160

Add: Depreciation on building 320

Add: Outstanding insurance fees 500 4140

Distribution expenses 2160

Debenture interest paid 240

Dividends paid 560

Tax paid 1600

Net profit 7,820

Statement of position as at 31st December 2019

Liabilities £’000 Assets £’000

Share capital 29000 Bank 320

Retained profit 8380 Land at cost 20000

Share premium 5000 Buildings at cost 16000

Net profit 7,820

Less: Accumulated depreciation

(4260 + 320) 4580 11420

12% debentures 2024 4000 Plant at cost 25600

Outstanding insurance fees 500

Less: Accumulated depreciation

(4960 + 2560) 7520 18080

Trade payables 4480

Trade receivables (8240-240-

160) 7840

Income tax liability 1600 Inventory 3120

Total liabilities 60780 Total assets 60780

Working note

Building cost 16000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

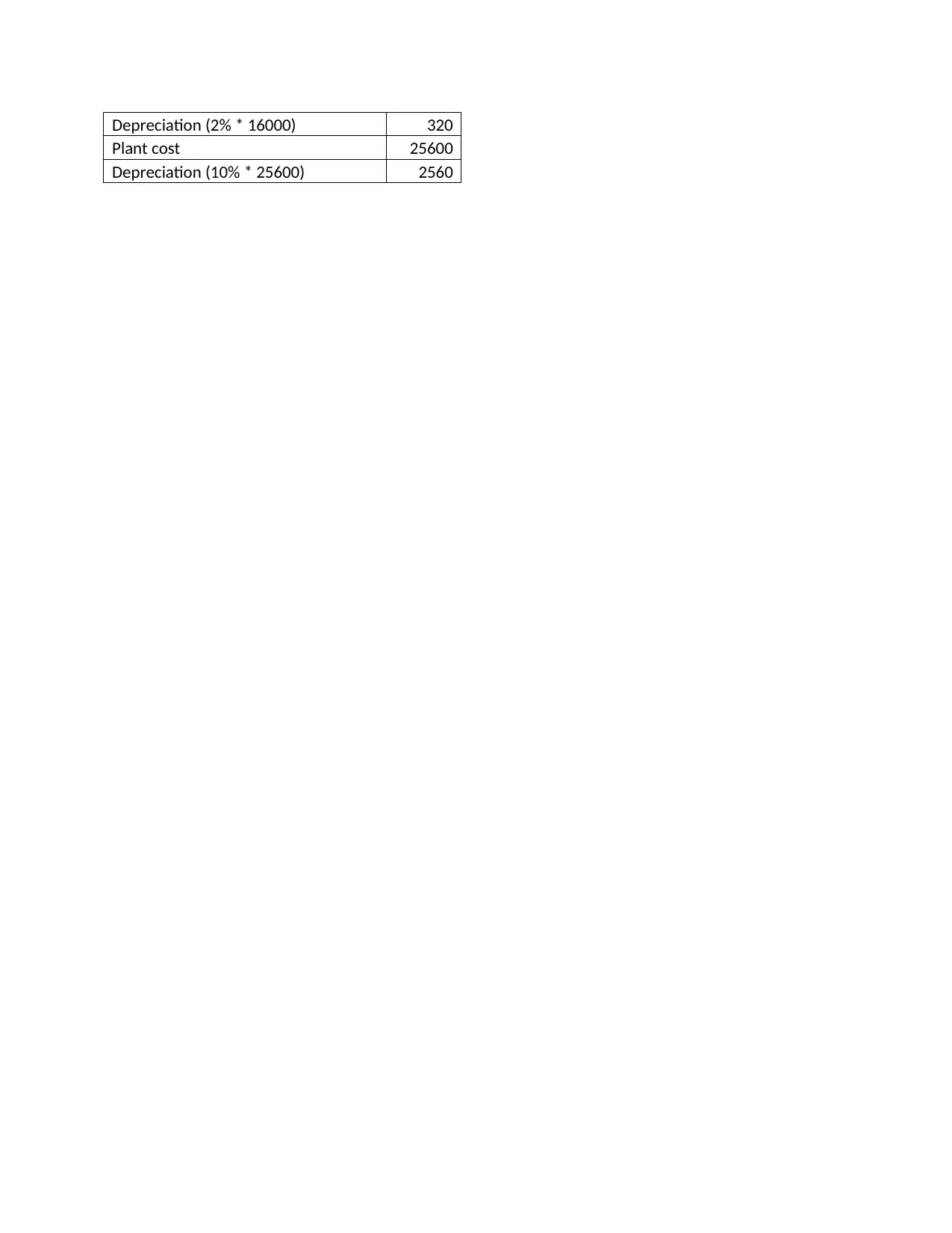

Depreciation (2% * 16000) 320

Plant cost 25600

Depreciation (10% * 25600) 2560

Plant cost 25600

Depreciation (10% * 25600) 2560

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

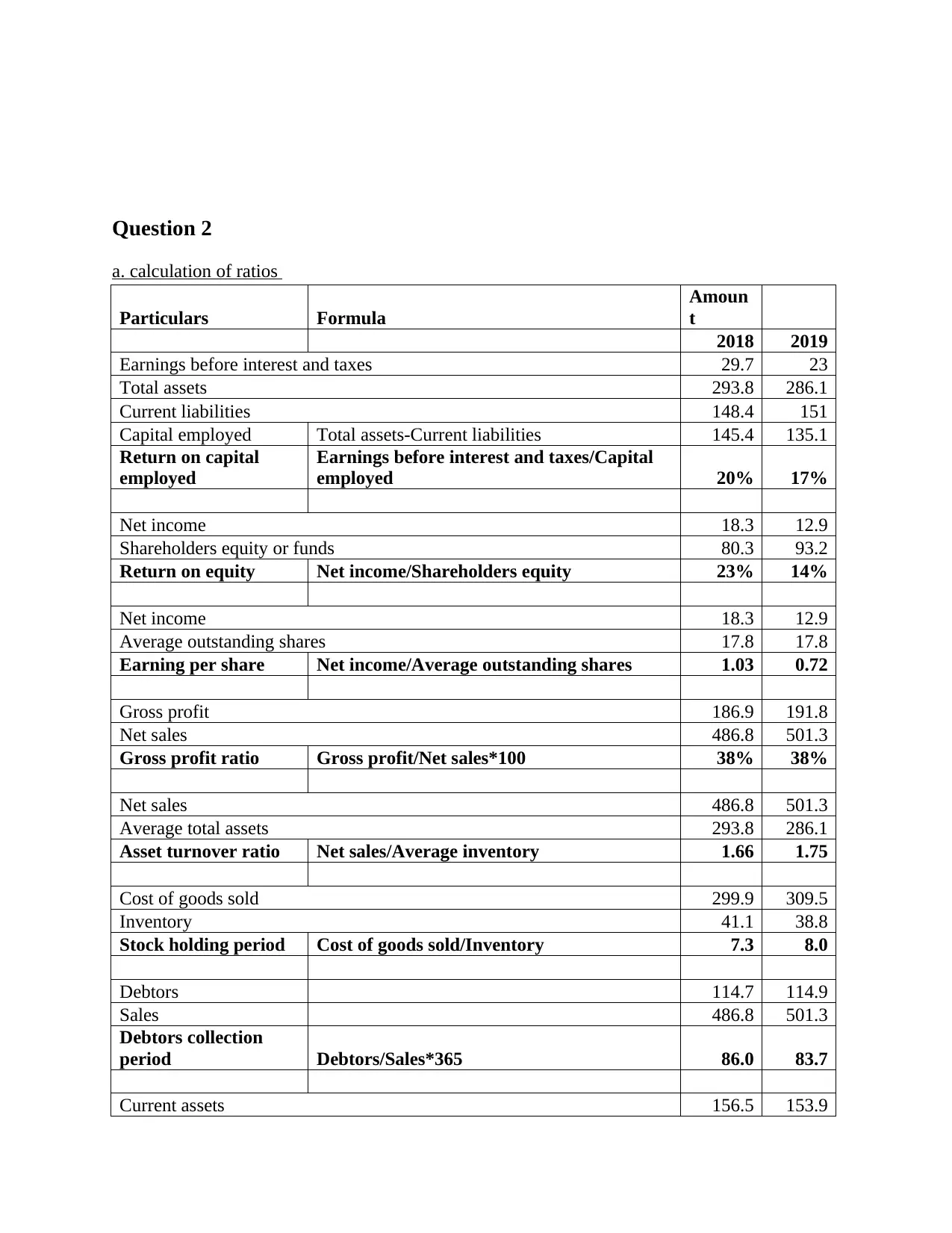

Question 2

a. calculation of ratios

Particulars Formula

Amoun

t

2018 2019

Earnings before interest and taxes 29.7 23

Total assets 293.8 286.1

Current liabilities 148.4 151

Capital employed Total assets-Current liabilities 145.4 135.1

Return on capital

employed

Earnings before interest and taxes/Capital

employed 20% 17%

Net income 18.3 12.9

Shareholders equity or funds 80.3 93.2

Return on equity Net income/Shareholders equity 23% 14%

Net income 18.3 12.9

Average outstanding shares 17.8 17.8

Earning per share Net income/Average outstanding shares 1.03 0.72

Gross profit 186.9 191.8

Net sales 486.8 501.3

Gross profit ratio Gross profit/Net sales*100 38% 38%

Net sales 486.8 501.3

Average total assets 293.8 286.1

Asset turnover ratio Net sales/Average inventory 1.66 1.75

Cost of goods sold 299.9 309.5

Inventory 41.1 38.8

Stock holding period Cost of goods sold/Inventory 7.3 8.0

Debtors 114.7 114.9

Sales 486.8 501.3

Debtors collection

period Debtors/Sales*365 86.0 83.7

Current assets 156.5 153.9

a. calculation of ratios

Particulars Formula

Amoun

t

2018 2019

Earnings before interest and taxes 29.7 23

Total assets 293.8 286.1

Current liabilities 148.4 151

Capital employed Total assets-Current liabilities 145.4 135.1

Return on capital

employed

Earnings before interest and taxes/Capital

employed 20% 17%

Net income 18.3 12.9

Shareholders equity or funds 80.3 93.2

Return on equity Net income/Shareholders equity 23% 14%

Net income 18.3 12.9

Average outstanding shares 17.8 17.8

Earning per share Net income/Average outstanding shares 1.03 0.72

Gross profit 186.9 191.8

Net sales 486.8 501.3

Gross profit ratio Gross profit/Net sales*100 38% 38%

Net sales 486.8 501.3

Average total assets 293.8 286.1

Asset turnover ratio Net sales/Average inventory 1.66 1.75

Cost of goods sold 299.9 309.5

Inventory 41.1 38.8

Stock holding period Cost of goods sold/Inventory 7.3 8.0

Debtors 114.7 114.9

Sales 486.8 501.3

Debtors collection

period Debtors/Sales*365 86.0 83.7

Current assets 156.5 153.9

Current liabilities 148.4 151

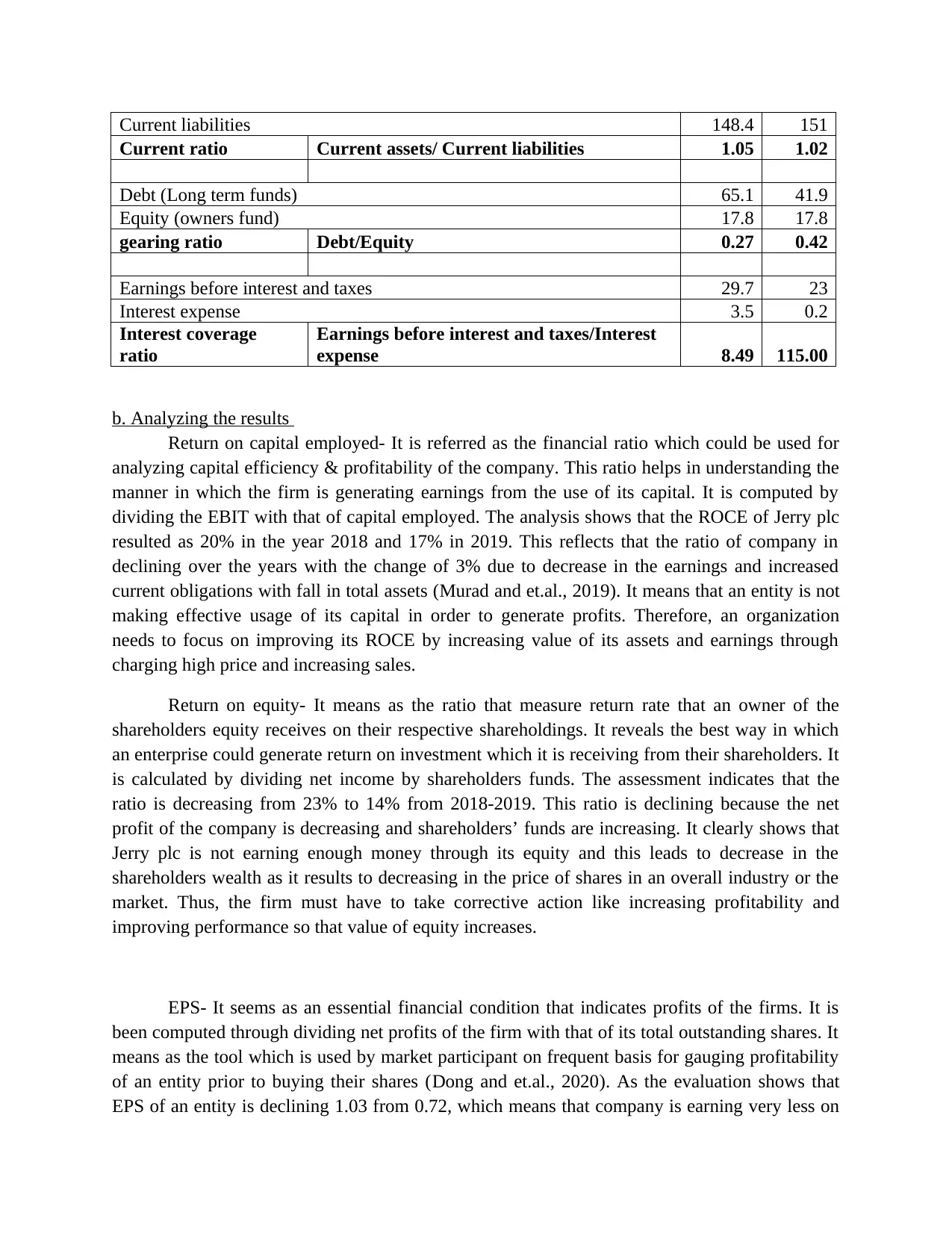

Current ratio Current assets/ Current liabilities 1.05 1.02

Debt (Long term funds) 65.1 41.9

Equity (owners fund) 17.8 17.8

gearing ratio Debt/Equity 0.27 0.42

Earnings before interest and taxes 29.7 23

Interest expense 3.5 0.2

Interest coverage

ratio

Earnings before interest and taxes/Interest

expense 8.49 115.00

b. Analyzing the results

Return on capital employed- It is referred as the financial ratio which could be used for

analyzing capital efficiency & profitability of the company. This ratio helps in understanding the

manner in which the firm is generating earnings from the use of its capital. It is computed by

dividing the EBIT with that of capital employed. The analysis shows that the ROCE of Jerry plc

resulted as 20% in the year 2018 and 17% in 2019. This reflects that the ratio of company in

declining over the years with the change of 3% due to decrease in the earnings and increased

current obligations with fall in total assets (Murad and et.al., 2019). It means that an entity is not

making effective usage of its capital in order to generate profits. Therefore, an organization

needs to focus on improving its ROCE by increasing value of its assets and earnings through

charging high price and increasing sales.

Return on equity- It means as the ratio that measure return rate that an owner of the

shareholders equity receives on their respective shareholdings. It reveals the best way in which

an enterprise could generate return on investment which it is receiving from their shareholders. It

is calculated by dividing net income by shareholders funds. The assessment indicates that the

ratio is decreasing from 23% to 14% from 2018-2019. This ratio is declining because the net

profit of the company is decreasing and shareholders’ funds are increasing. It clearly shows that

Jerry plc is not earning enough money through its equity and this leads to decrease in the

shareholders wealth as it results to decreasing in the price of shares in an overall industry or the

market. Thus, the firm must have to take corrective action like increasing profitability and

improving performance so that value of equity increases.

EPS- It seems as an essential financial condition that indicates profits of the firms. It is

been computed through dividing net profits of the firm with that of its total outstanding shares. It

means as the tool which is used by market participant on frequent basis for gauging profitability

of an entity prior to buying their shares (Dong and et.al., 2020). As the evaluation shows that

EPS of an entity is declining 1.03 from 0.72, which means that company is earning very less on

Current ratio Current assets/ Current liabilities 1.05 1.02

Debt (Long term funds) 65.1 41.9

Equity (owners fund) 17.8 17.8

gearing ratio Debt/Equity 0.27 0.42

Earnings before interest and taxes 29.7 23

Interest expense 3.5 0.2

Interest coverage

ratio

Earnings before interest and taxes/Interest

expense 8.49 115.00

b. Analyzing the results

Return on capital employed- It is referred as the financial ratio which could be used for

analyzing capital efficiency & profitability of the company. This ratio helps in understanding the

manner in which the firm is generating earnings from the use of its capital. It is computed by

dividing the EBIT with that of capital employed. The analysis shows that the ROCE of Jerry plc

resulted as 20% in the year 2018 and 17% in 2019. This reflects that the ratio of company in

declining over the years with the change of 3% due to decrease in the earnings and increased

current obligations with fall in total assets (Murad and et.al., 2019). It means that an entity is not

making effective usage of its capital in order to generate profits. Therefore, an organization

needs to focus on improving its ROCE by increasing value of its assets and earnings through

charging high price and increasing sales.

Return on equity- It means as the ratio that measure return rate that an owner of the

shareholders equity receives on their respective shareholdings. It reveals the best way in which

an enterprise could generate return on investment which it is receiving from their shareholders. It

is calculated by dividing net income by shareholders funds. The assessment indicates that the

ratio is decreasing from 23% to 14% from 2018-2019. This ratio is declining because the net

profit of the company is decreasing and shareholders’ funds are increasing. It clearly shows that

Jerry plc is not earning enough money through its equity and this leads to decrease in the

shareholders wealth as it results to decreasing in the price of shares in an overall industry or the

market. Thus, the firm must have to take corrective action like increasing profitability and

improving performance so that value of equity increases.

EPS- It seems as an essential financial condition that indicates profits of the firms. It is

been computed through dividing net profits of the firm with that of its total outstanding shares. It

means as the tool which is used by market participant on frequent basis for gauging profitability

of an entity prior to buying their shares (Dong and et.al., 2020). As the evaluation shows that

EPS of an entity is declining 1.03 from 0.72, which means that company is earning very less on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

its per share value. This is because the net income of Jerry Plc is decreasing with no change in its

average shares. Therefore, the firm should take appropriate measures for improving its earnings

per share by earnings increased profitability.

Gross profit ratio- It refers to the metric that an analyst uses for analyzing financial

condition of company through computing an amount of the money that is left over the sales of

product after reducing COGS. The ratio is calculated by dividing gross profits by that of the net

sales for assessing operational performance of the company. The results show that the GP ratio

remains as stable in both the years that are 38% in 2018 and 2019. This is because the GP and

sales of Jerry Plc is increasing with very little margin so that ratio does not change from one

period to other (Ardalan, 2017). This in turn shows that company is seeking for improving its

operational efficiency by increasing sales and ensuring control over its cost. The firm would e

taking measures for increasing its GP margin by making optimum use of its resources.

Asset turnover ratio- It referred as ratio that reflects the value present between company’

revenue and asset value. It deemed as an indicator of efficiency through which an entity is

deploying its own assets for producing or generating revenue. It is considered as the determinant

of an enterprise performance in entire market and industry. Higher the ATR, more efficient a

firm is in generating the revenue from that of its assets. However, lower ratio reflects inefficient

use of assets in generating revenue. The analysis depicts that ATR of Jerry Plc is increasing

which clearly depicts that an organization is generating higher sales by making use of its assets

in an effective & efficient manner. This shows that efficiency position of the company is

becoming better from one accounting period to other.

Inventory holding period- It means as ratio that shows an average time that an entity

takes in turning its inventory into the sales including the goods that are WIP. It is determined by

dividing cost of sales with that of inventory or goods. Lower holding period is preferred because

it reflects that inventory remains for a shorter duration in the premises and very less time is taken

in clearing off the goods (Alladio and et.al., 2017). However, higher ITR shows that company is

holding its inventory for a long term period at the workplace. The analysis shows that ITR days

is increasing with little value which means that an entity seeks for increasing its holding period

in terms of inventory.

Average collection period- This ratio signifies the time period taken by the firm to

receive its payments that is been owed by their clients in form of the trade receivables. An entity

compute it’s ACP in ensuring that it has sufficient cash with which it could meet its finance

related obligations in an effective way. It is expressed by dividing the trade receivables by that of

sales for assessing the days in which the firm collects its receipts. The results reflects that debtors

receivable period is declining over the years which clearly shows that company is seeking for

reducing the period of collection through receiving the amount due within 83 days rather 86

days.

average shares. Therefore, the firm should take appropriate measures for improving its earnings

per share by earnings increased profitability.

Gross profit ratio- It refers to the metric that an analyst uses for analyzing financial

condition of company through computing an amount of the money that is left over the sales of

product after reducing COGS. The ratio is calculated by dividing gross profits by that of the net

sales for assessing operational performance of the company. The results show that the GP ratio

remains as stable in both the years that are 38% in 2018 and 2019. This is because the GP and

sales of Jerry Plc is increasing with very little margin so that ratio does not change from one

period to other (Ardalan, 2017). This in turn shows that company is seeking for improving its

operational efficiency by increasing sales and ensuring control over its cost. The firm would e

taking measures for increasing its GP margin by making optimum use of its resources.

Asset turnover ratio- It referred as ratio that reflects the value present between company’

revenue and asset value. It deemed as an indicator of efficiency through which an entity is

deploying its own assets for producing or generating revenue. It is considered as the determinant

of an enterprise performance in entire market and industry. Higher the ATR, more efficient a

firm is in generating the revenue from that of its assets. However, lower ratio reflects inefficient

use of assets in generating revenue. The analysis depicts that ATR of Jerry Plc is increasing

which clearly depicts that an organization is generating higher sales by making use of its assets

in an effective & efficient manner. This shows that efficiency position of the company is

becoming better from one accounting period to other.

Inventory holding period- It means as ratio that shows an average time that an entity

takes in turning its inventory into the sales including the goods that are WIP. It is determined by

dividing cost of sales with that of inventory or goods. Lower holding period is preferred because

it reflects that inventory remains for a shorter duration in the premises and very less time is taken

in clearing off the goods (Alladio and et.al., 2017). However, higher ITR shows that company is

holding its inventory for a long term period at the workplace. The analysis shows that ITR days

is increasing with little value which means that an entity seeks for increasing its holding period

in terms of inventory.

Average collection period- This ratio signifies the time period taken by the firm to

receive its payments that is been owed by their clients in form of the trade receivables. An entity

compute it’s ACP in ensuring that it has sufficient cash with which it could meet its finance

related obligations in an effective way. It is expressed by dividing the trade receivables by that of

sales for assessing the days in which the firm collects its receipts. The results reflects that debtors

receivable period is declining over the years which clearly shows that company is seeking for

reducing the period of collection through receiving the amount due within 83 days rather 86

days.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current ratio- It means as the liquidity ratio that measures an ability of the company in

paying its short term liabilities with the cash generated from their current assets. It tells the

investors the manner in which firm could maximize its current assets on balance sheet for

satisfying other payables and current debt (Wen and Zhu, 2019). It is calculated by dividing

current assets with that of the short run obligations in order to understand the liquidity position of

Jerry Plc. Higher the CR, better is the liquidity condition of an enterprise and vice versa. The CR

ratio of Jerry Plc is seen as stable in both the accounting periods as the value remains as 1.05 and

1.02. This clearly states that an entity is not making optimum but adequate use of the assets. It

has not attained ideal liquid position because of decrease in current assets and increase in short

term obligations. Therefore in order to attain optimal or ideal position, the firm must have to take

corrective measures such as collecting the receivables on time and making payment to the

creditors within the specified time frame.

Gearing ratio- This means as financial ratio which compares owners funds to the debt that

is been borrowed by firm. It seems as measure of the financial leverage which demonstrates a

degree towards which operations of an entity is funded by the equity capital over debt financing.

It is determined by dividing debt with equity for analyzing the amount of borrowed funds.

Greater is the D/E ratio; poor is the leverage position of firm as it shows that company is having

higher borrowed money as compared to equities (Pesaran and et.al., 2018). As the D/E ratio of

Jerry Plc is increasing from one period to other, this clearly shows that it has borrowed large

amount of funds in comparison to its owned funds.

Interest coverage ratio- It is the measure of an entity’s ability in meeting its interest

related payments. It equates to the earnings before interest and the taxes for the time period that

is of one year dividing it by finance cost for same period (Messerlian and Gaskins, 2017). The

ICR of Jerry Plc is showing an increasing trend which means that leverage position of the firm is

becoming good as its ability in paying off its interest obligation is increasing.

QUESTION 3

(a)

Three different user groups of financial statements are stated below.

Owners and investors: The stockholders of the companies require the financial data in

order to to assist them with settling on decisions on how to manage their ventures (portions of

stock), for example hold, sell, or purchase more. The prospective investors of the company need

data to survey the organization's potential for progress and gainfulness. Similarly, entrepreneurs

need financial data to decide whether the business is gainful and whether to proceed, improve or

drop it.

Management: In small companies, the board may incorporate the proprietors. In large

associations, the board members are of hired professional who are endowed with the duty of

paying its short term liabilities with the cash generated from their current assets. It tells the

investors the manner in which firm could maximize its current assets on balance sheet for

satisfying other payables and current debt (Wen and Zhu, 2019). It is calculated by dividing

current assets with that of the short run obligations in order to understand the liquidity position of

Jerry Plc. Higher the CR, better is the liquidity condition of an enterprise and vice versa. The CR

ratio of Jerry Plc is seen as stable in both the accounting periods as the value remains as 1.05 and

1.02. This clearly states that an entity is not making optimum but adequate use of the assets. It

has not attained ideal liquid position because of decrease in current assets and increase in short

term obligations. Therefore in order to attain optimal or ideal position, the firm must have to take

corrective measures such as collecting the receivables on time and making payment to the

creditors within the specified time frame.

Gearing ratio- This means as financial ratio which compares owners funds to the debt that

is been borrowed by firm. It seems as measure of the financial leverage which demonstrates a

degree towards which operations of an entity is funded by the equity capital over debt financing.

It is determined by dividing debt with equity for analyzing the amount of borrowed funds.

Greater is the D/E ratio; poor is the leverage position of firm as it shows that company is having

higher borrowed money as compared to equities (Pesaran and et.al., 2018). As the D/E ratio of

Jerry Plc is increasing from one period to other, this clearly shows that it has borrowed large

amount of funds in comparison to its owned funds.

Interest coverage ratio- It is the measure of an entity’s ability in meeting its interest

related payments. It equates to the earnings before interest and the taxes for the time period that

is of one year dividing it by finance cost for same period (Messerlian and Gaskins, 2017). The

ICR of Jerry Plc is showing an increasing trend which means that leverage position of the firm is

becoming good as its ability in paying off its interest obligation is increasing.

QUESTION 3

(a)

Three different user groups of financial statements are stated below.

Owners and investors: The stockholders of the companies require the financial data in

order to to assist them with settling on decisions on how to manage their ventures (portions of

stock), for example hold, sell, or purchase more. The prospective investors of the company need

data to survey the organization's potential for progress and gainfulness. Similarly, entrepreneurs

need financial data to decide whether the business is gainful and whether to proceed, improve or

drop it.

Management: In small companies, the board may incorporate the proprietors. In large

associations, the board members are of hired professional who are endowed with the duty of

operating the business or a piece of the business (Preda, 2019). They go about as an agent of the

proprietors. The managers, regardless of whether proprietors or employed, routinely face

monetary choices such as - How much supplies will we buy? Do we have enough money? What

amount did we make a year ago? Did we meet our objectives? Every one of those, and numerous

different inquiries and business choices, require examination of financial information.

Trade creditors:Just like lenders, exchange leasers or providers are keen on the

organization's capacity to pay commitments when they become due. They are in any case

particularly keen on the organization's liquidity – its capacity to meet up with its short-term

commitments.

(b)

Advantages and disadvantages of financial reporting

Advantages Disadvantages

It provides various types of decision-

making tools which assist the users

of the information in taking right

decision. For preparer of the reports,

it becomes important in knowing the

actual financial picture of the

company which is used in taking

relevant decisions (Matuszyk and

Rymkiewicz, 2018).

The financial reports are being used

by the government authorities in

evaluating whether the company is

working complying with the

required regulations or not.The

preparer can take advantage of the

same and clearly state in its reports

all the regulations it has followed

which will create a positive and

good image in the eyes of law.

The reports are being prepared

considering various policies and

regulations of which the users are

might be aware of which leads to

wrong decision making on their part.

Also, the preparer is required to gain

knowledge of each regulations and

its impact on the financial position

and performance of the company

which is very difficult.

In case of any problem or mistake in

the preparation of the reports, the

users might consider it true and

based on it , takes decisions and on

knowing the same, the preparer is

held liable for the mistake and the

loss that might have incurred to the

users.

proprietors. The managers, regardless of whether proprietors or employed, routinely face

monetary choices such as - How much supplies will we buy? Do we have enough money? What

amount did we make a year ago? Did we meet our objectives? Every one of those, and numerous

different inquiries and business choices, require examination of financial information.

Trade creditors:Just like lenders, exchange leasers or providers are keen on the

organization's capacity to pay commitments when they become due. They are in any case

particularly keen on the organization's liquidity – its capacity to meet up with its short-term

commitments.

(b)

Advantages and disadvantages of financial reporting

Advantages Disadvantages

It provides various types of decision-

making tools which assist the users

of the information in taking right

decision. For preparer of the reports,

it becomes important in knowing the

actual financial picture of the

company which is used in taking

relevant decisions (Matuszyk and

Rymkiewicz, 2018).

The financial reports are being used

by the government authorities in

evaluating whether the company is

working complying with the

required regulations or not.The

preparer can take advantage of the

same and clearly state in its reports

all the regulations it has followed

which will create a positive and

good image in the eyes of law.

The reports are being prepared

considering various policies and

regulations of which the users are

might be aware of which leads to

wrong decision making on their part.

Also, the preparer is required to gain

knowledge of each regulations and

its impact on the financial position

and performance of the company

which is very difficult.

In case of any problem or mistake in

the preparation of the reports, the

users might consider it true and

based on it , takes decisions and on

knowing the same, the preparer is

held liable for the mistake and the

loss that might have incurred to the

users.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(c)

Limitations of financial statements

Financial statements don't uncover the current worth of the organization. At first, items

recorded at their cost. The worth of assets and obligations changes with time. This leads

to misleading figures.

The figures of assets that shows up in the statements relies upon the principles of the

individual who manages it (Velte and Stawinoga, 2017). For instance, the technique for

depreciation, method of amortization and so on, relies upon the individual judgment of

the accounting.

In the event that the circumstance of expansion the rate is moderately high, the measures

of advantages and liabilities to be decided sheet will show up excessively low, as we can't

modify it for swelling. This for the most part applies to long haul resources.

On the off chance that an organization needs to contrast the outcomes of its organization

with other organizations, their financial summaries might not be generally similar, in

light of the fact that various organizations utilize diverse accounting practices.

Limitations of financial statements

Financial statements don't uncover the current worth of the organization. At first, items

recorded at their cost. The worth of assets and obligations changes with time. This leads

to misleading figures.

The figures of assets that shows up in the statements relies upon the principles of the

individual who manages it (Velte and Stawinoga, 2017). For instance, the technique for

depreciation, method of amortization and so on, relies upon the individual judgment of

the accounting.

In the event that the circumstance of expansion the rate is moderately high, the measures

of advantages and liabilities to be decided sheet will show up excessively low, as we can't

modify it for swelling. This for the most part applies to long haul resources.

On the off chance that an organization needs to contrast the outcomes of its organization

with other organizations, their financial summaries might not be generally similar, in

light of the fact that various organizations utilize diverse accounting practices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal

Alladio, E. and et.al., 2017. Direct and indirect alcohol biomarkers data collected in hair

samples-multivariate data analysis and likelihood ratio interpretation perspectives. Data

in brief. 12. pp.1-8.

Ardalan, K., 2017. Advancing the Interpretation of the Du Pont Equation. Journal of Modern

Accounting and Auditing. 13(7). pp.294-298.

Dong, G. and et.al., 2020. The win ratio: on interpretation and handling of ties. Statistics in

Biopharmaceutical Research. 12(1). pp.99-106.

Matuszyk, I. and Rymkiewicz, B., 2018. Integrated Reporting as a Tool for Communicating with

Stakeholders–Advantages and Disadvantages. In E3S Web of Conferences (Vol. 35, p.

06004). EDP Sciences.

Messerlian, C. and Gaskins, A. J., 2017. Epidemiologic approaches for studying assisted

reproductive technologies: design, methods, analysis, and interpretation. Current

epidemiology reports. 4(2). pp.124-132.

Murad, M. H. and et.al., 2019. When continuous outcomes are measured using different scales:

guide for meta-analysis and interpretation. Bmj. 364.

Pesaran, B. and et.al., 2018. Investigating large-scale brain dynamics using field potential

recordings: analysis and interpretation. Nature neuroscience. 21(7). pp.903-919.

Preda, I., 2019. The Information Content Of Audit Opinion For Users Of Financial

Statements. Oradea Journal of Business and Economics. 4(2). pp.102-111.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of empirical research,

limitations and future research implications. Journal of Management Control, 28(3),

pp.275-320.

Wen, H. and Zhu, T., 2019. Interpretation of Financial Statements.

Books and journal

Alladio, E. and et.al., 2017. Direct and indirect alcohol biomarkers data collected in hair

samples-multivariate data analysis and likelihood ratio interpretation perspectives. Data

in brief. 12. pp.1-8.

Ardalan, K., 2017. Advancing the Interpretation of the Du Pont Equation. Journal of Modern

Accounting and Auditing. 13(7). pp.294-298.

Dong, G. and et.al., 2020. The win ratio: on interpretation and handling of ties. Statistics in

Biopharmaceutical Research. 12(1). pp.99-106.

Matuszyk, I. and Rymkiewicz, B., 2018. Integrated Reporting as a Tool for Communicating with

Stakeholders–Advantages and Disadvantages. In E3S Web of Conferences (Vol. 35, p.

06004). EDP Sciences.

Messerlian, C. and Gaskins, A. J., 2017. Epidemiologic approaches for studying assisted

reproductive technologies: design, methods, analysis, and interpretation. Current

epidemiology reports. 4(2). pp.124-132.

Murad, M. H. and et.al., 2019. When continuous outcomes are measured using different scales:

guide for meta-analysis and interpretation. Bmj. 364.

Pesaran, B. and et.al., 2018. Investigating large-scale brain dynamics using field potential

recordings: analysis and interpretation. Nature neuroscience. 21(7). pp.903-919.

Preda, I., 2019. The Information Content Of Audit Opinion For Users Of Financial

Statements. Oradea Journal of Business and Economics. 4(2). pp.102-111.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of empirical research,

limitations and future research implications. Journal of Management Control, 28(3),

pp.275-320.

Wen, H. and Zhu, T., 2019. Interpretation of Financial Statements.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.