AIS Report: Cloud Accounting Implementation at Goodie Gumdrops

VerifiedAdded on 2020/02/19

|8

|1478

|28

Report

AI Summary

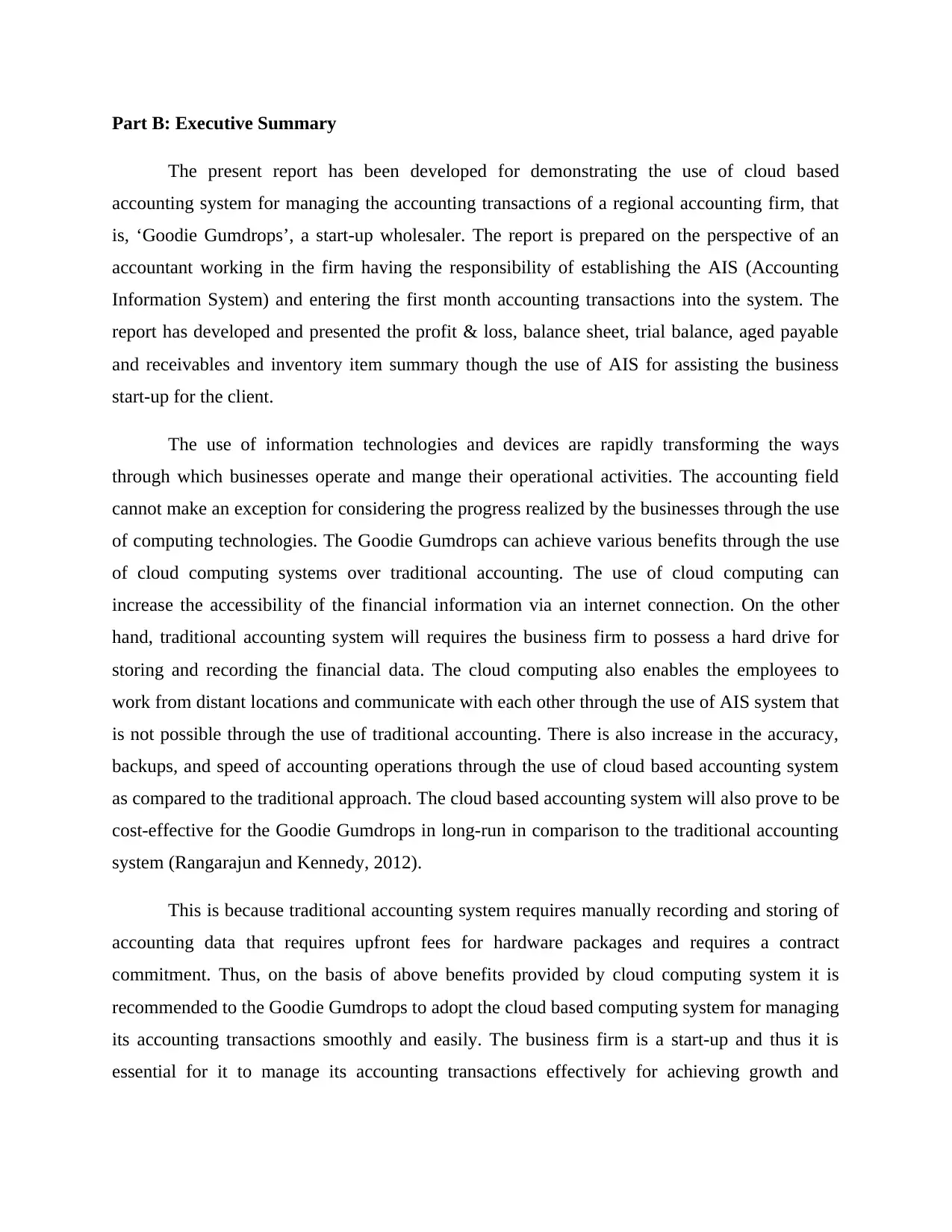

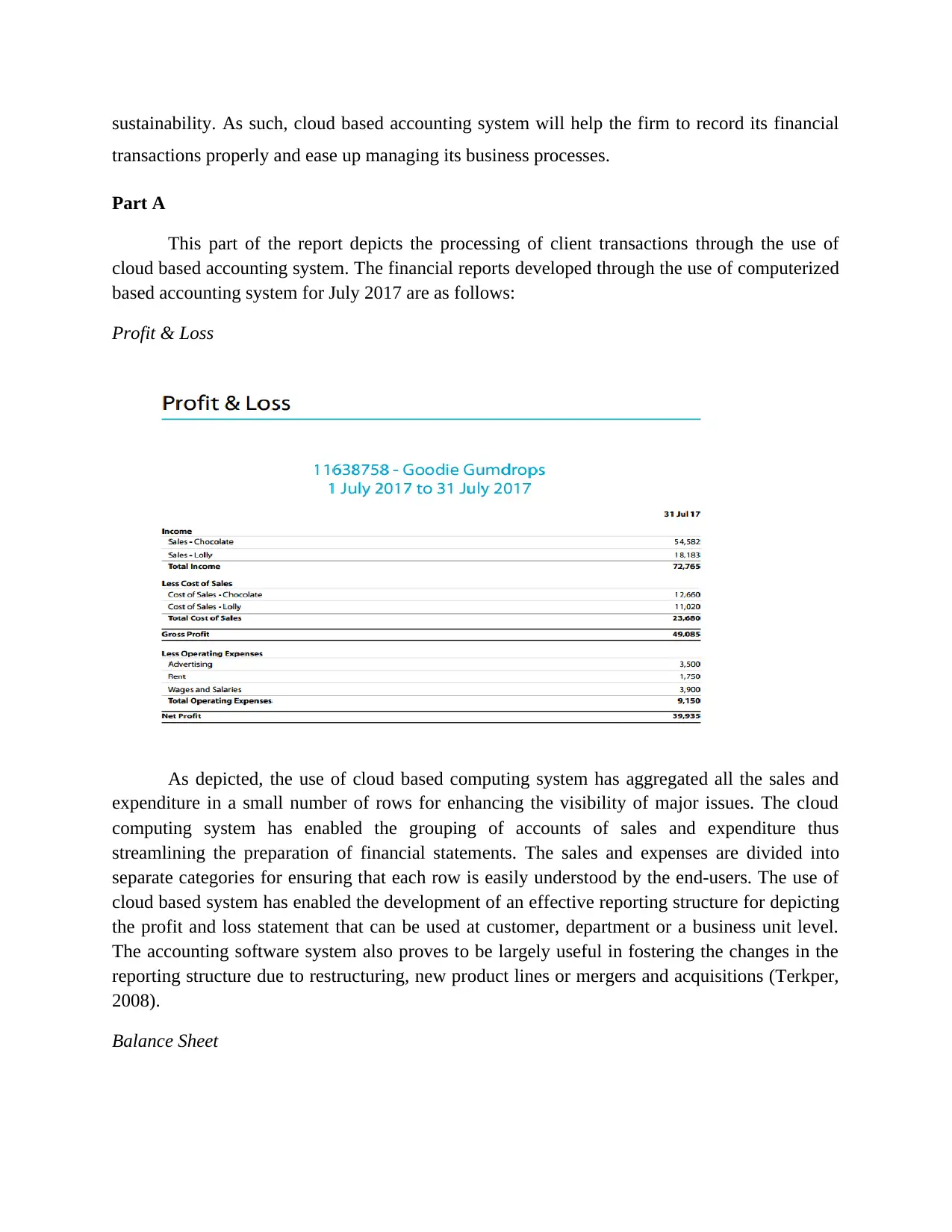

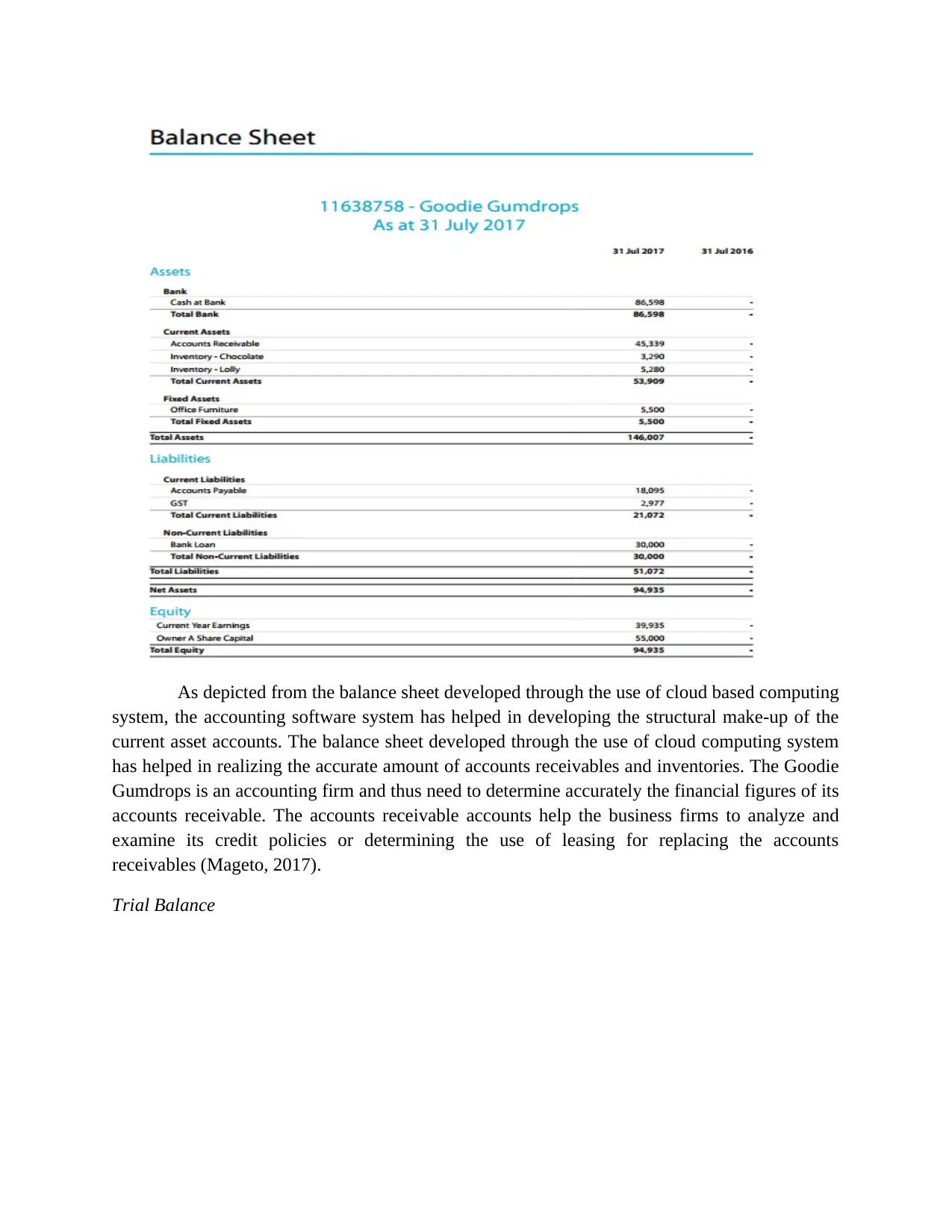

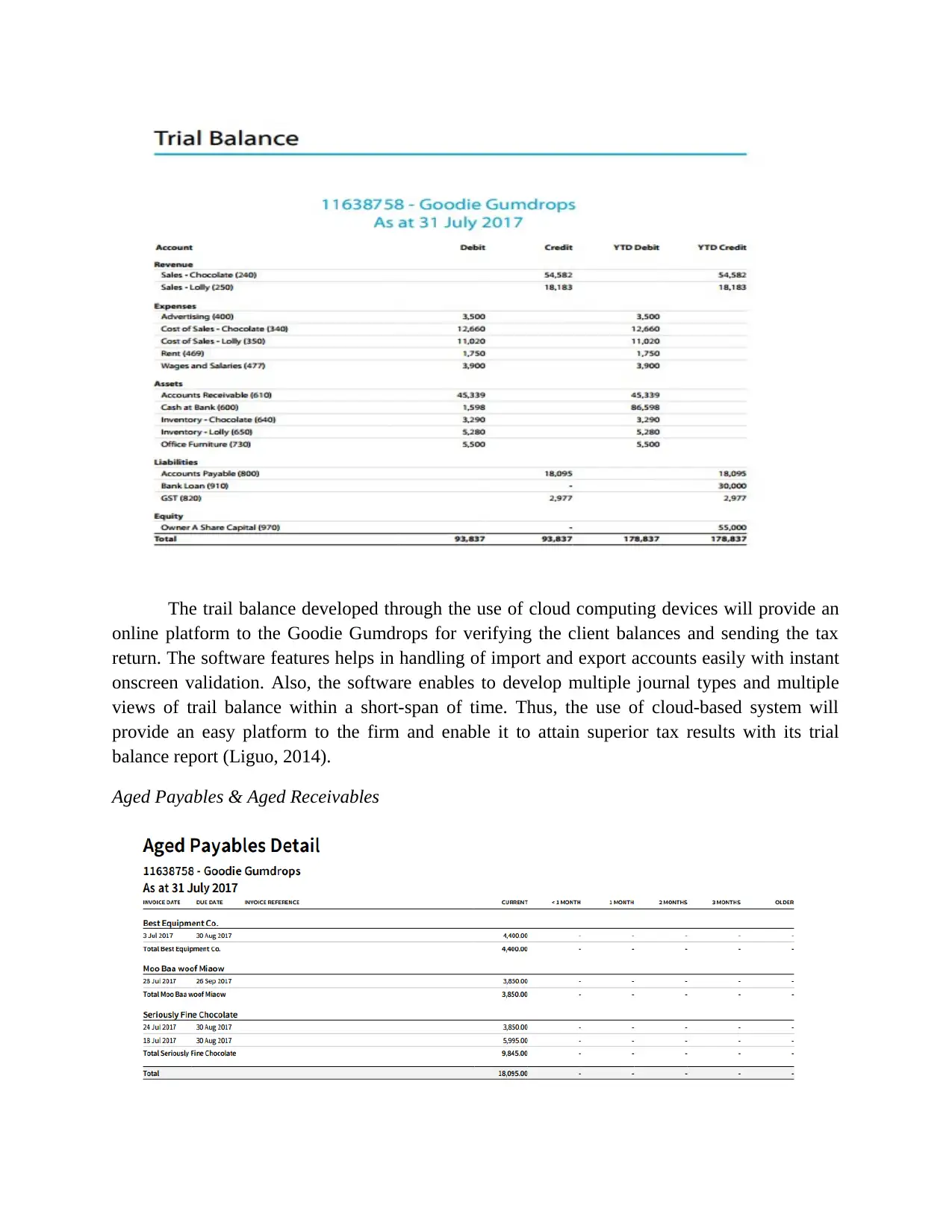

This report serves as an executive summary and detailed analysis of a cloud-based accounting information system (AIS) designed for Goodie Gumdrops, a start-up wholesaler. The report, prepared from an accountant's perspective, demonstrates the practical application of cloud computing in managing financial transactions. It showcases the creation of essential financial statements, including profit & loss, balance sheet, trial balance, aged payables and receivables, and inventory item summaries. The advantages of cloud computing over traditional methods are highlighted, such as increased accessibility, remote work capabilities, enhanced accuracy, and cost-effectiveness. The report emphasizes the benefits of cloud-based systems for start-ups, particularly in effectively managing financial transactions for sustainable growth. The report also details the processing of client transactions, the structure of current asset accounts, and the development of online platforms for verifying client balances. It concludes with a strong recommendation for Goodie Gumdrops to adopt a cloud-based accounting system to streamline business processes and improve operational efficiency. The report references several academic sources to support its findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.