Accounting Report: Bonza Handtools Ltd. Profit Analysis and Costing

VerifiedAdded on 2020/06/03

|12

|2205

|69

Report

AI Summary

This accounting report analyzes various financial aspects for Bonza Handtools Ltd. It begins by evaluating different proposals to increase profitability, considering factors like pricing, advertising, and sales volume. The report then assesses the impact of different production capacities on profits, followed by a discussion on treating salaries and depreciation as assets. Further, the report delves into overhead allocation rates, the costing of a special order, and the determination of the minimum price per trailer. The conclusion emphasizes the importance of accurate cost and profit analysis for optimal financial outcomes, including the impact of advertising budgets and the treatment of salaries and depreciation in financial statements. The report utilizes tables and illustrations to present financial data and analysis.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1: Financial suggestions to the senior staff..................................................................1

Question 2: Opinion on level of the bid......................................................................................4

Question 3 Salaries and depreciation considered as assets in the balance sheet.........................5

Question 4...................................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Question 1: Financial suggestions to the senior staff..................................................................1

Question 2: Opinion on level of the bid......................................................................................4

Question 3 Salaries and depreciation considered as assets in the balance sheet.........................5

Question 4...................................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Illustration Index

Illustration 1: Comparison of profits................................................................................................4

Index of Tables

Table 1: Actual profits in previous year..........................................................................................1

Table 2: Estimated profits from Proposal 1.....................................................................................1

Table 3: Estimated profits from Proposal 2.....................................................................................2

Table 4: Estimated profits from Proposal 3.....................................................................................2

Table 5: Profits for Tassie Company...............................................................................................4

Table 6: Profits from Case 1............................................................................................................4

Table 7: Profits from Case 2............................................................................................................5

Table 8: Overhead Allocation Rate..................................................................................................6

Table 9: Total Cost of Special order................................................................................................6

Table 10: Total cost with Machine Hours........................................................................................6

Table 11: Minimum Price per Trailer..............................................................................................7

Illustration 1: Comparison of profits................................................................................................4

Index of Tables

Table 1: Actual profits in previous year..........................................................................................1

Table 2: Estimated profits from Proposal 1.....................................................................................1

Table 3: Estimated profits from Proposal 2.....................................................................................2

Table 4: Estimated profits from Proposal 3.....................................................................................2

Table 5: Profits for Tassie Company...............................................................................................4

Table 6: Profits from Case 1............................................................................................................4

Table 7: Profits from Case 2............................................................................................................5

Table 8: Overhead Allocation Rate..................................................................................................6

Table 9: Total Cost of Special order................................................................................................6

Table 10: Total cost with Machine Hours........................................................................................6

Table 11: Minimum Price per Trailer..............................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

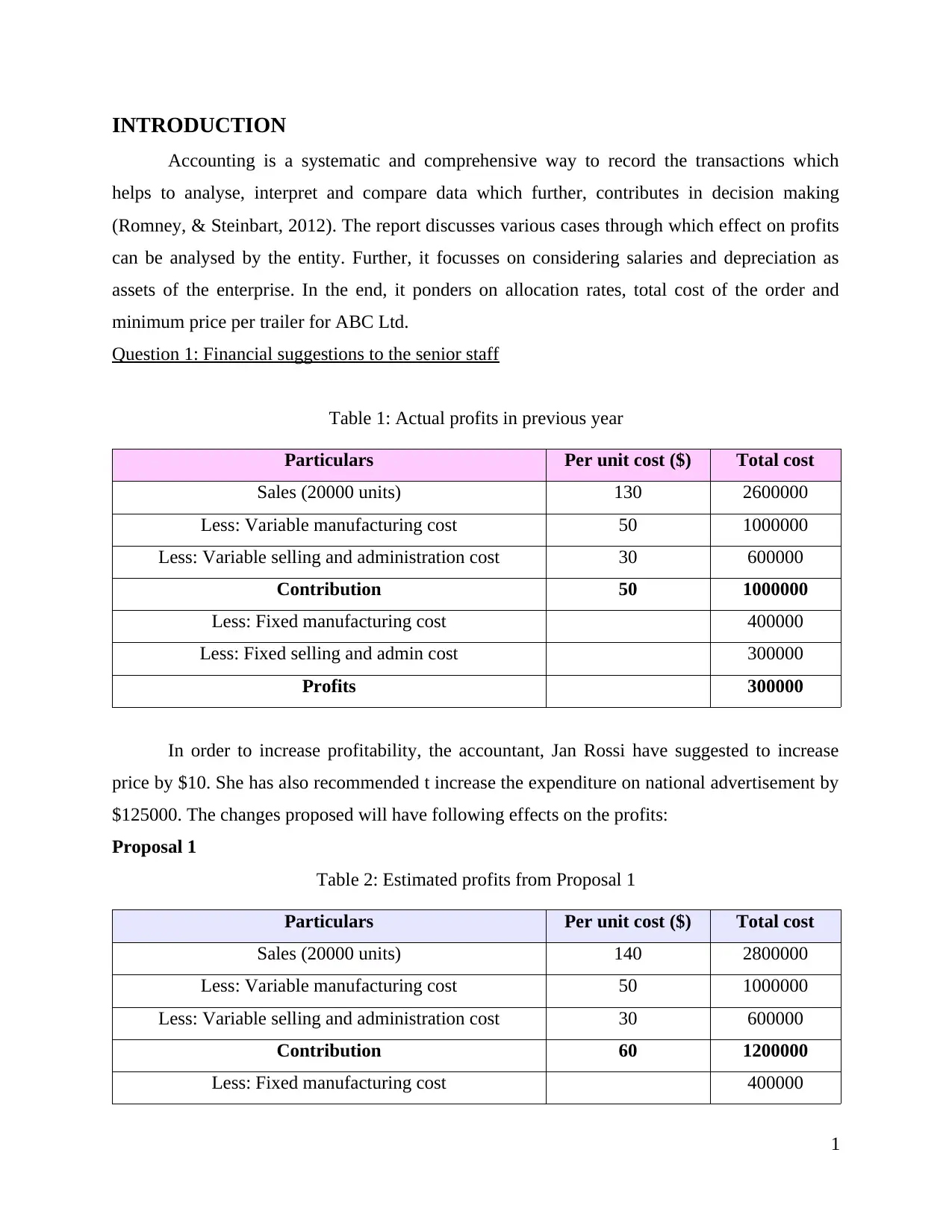

INTRODUCTION

Accounting is a systematic and comprehensive way to record the transactions which

helps to analyse, interpret and compare data which further, contributes in decision making

(Romney, & Steinbart, 2012). The report discusses various cases through which effect on profits

can be analysed by the entity. Further, it focusses on considering salaries and depreciation as

assets of the enterprise. In the end, it ponders on allocation rates, total cost of the order and

minimum price per trailer for ABC Ltd.

Question 1: Financial suggestions to the senior staff

Table 1: Actual profits in previous year

Particulars Per unit cost ($) Total cost

Sales (20000 units) 130 2600000

Less: Variable manufacturing cost 50 1000000

Less: Variable selling and administration cost 30 600000

Contribution 50 1000000

Less: Fixed manufacturing cost 400000

Less: Fixed selling and admin cost 300000

Profits 300000

In order to increase profitability, the accountant, Jan Rossi have suggested to increase

price by $10. She has also recommended t increase the expenditure on national advertisement by

$125000. The changes proposed will have following effects on the profits:

Proposal 1

Table 2: Estimated profits from Proposal 1

Particulars Per unit cost ($) Total cost

Sales (20000 units) 140 2800000

Less: Variable manufacturing cost 50 1000000

Less: Variable selling and administration cost 30 600000

Contribution 60 1200000

Less: Fixed manufacturing cost 400000

1

Accounting is a systematic and comprehensive way to record the transactions which

helps to analyse, interpret and compare data which further, contributes in decision making

(Romney, & Steinbart, 2012). The report discusses various cases through which effect on profits

can be analysed by the entity. Further, it focusses on considering salaries and depreciation as

assets of the enterprise. In the end, it ponders on allocation rates, total cost of the order and

minimum price per trailer for ABC Ltd.

Question 1: Financial suggestions to the senior staff

Table 1: Actual profits in previous year

Particulars Per unit cost ($) Total cost

Sales (20000 units) 130 2600000

Less: Variable manufacturing cost 50 1000000

Less: Variable selling and administration cost 30 600000

Contribution 50 1000000

Less: Fixed manufacturing cost 400000

Less: Fixed selling and admin cost 300000

Profits 300000

In order to increase profitability, the accountant, Jan Rossi have suggested to increase

price by $10. She has also recommended t increase the expenditure on national advertisement by

$125000. The changes proposed will have following effects on the profits:

Proposal 1

Table 2: Estimated profits from Proposal 1

Particulars Per unit cost ($) Total cost

Sales (20000 units) 140 2800000

Less: Variable manufacturing cost 50 1000000

Less: Variable selling and administration cost 30 600000

Contribution 60 1200000

Less: Fixed manufacturing cost 400000

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Fixed selling and admin cost 300000

Less: Advertising cost 125000

Profits 375000

It is expected that by implementing on this proposal, the company will be able to increase

profits from $3,00,000 to $3,75,000. It will prove ton be profitable for the company. However, it

can lead to decrease in sales of the company as it can lose its customers due to high selling price

(Johnson, & Noguera, 2012).

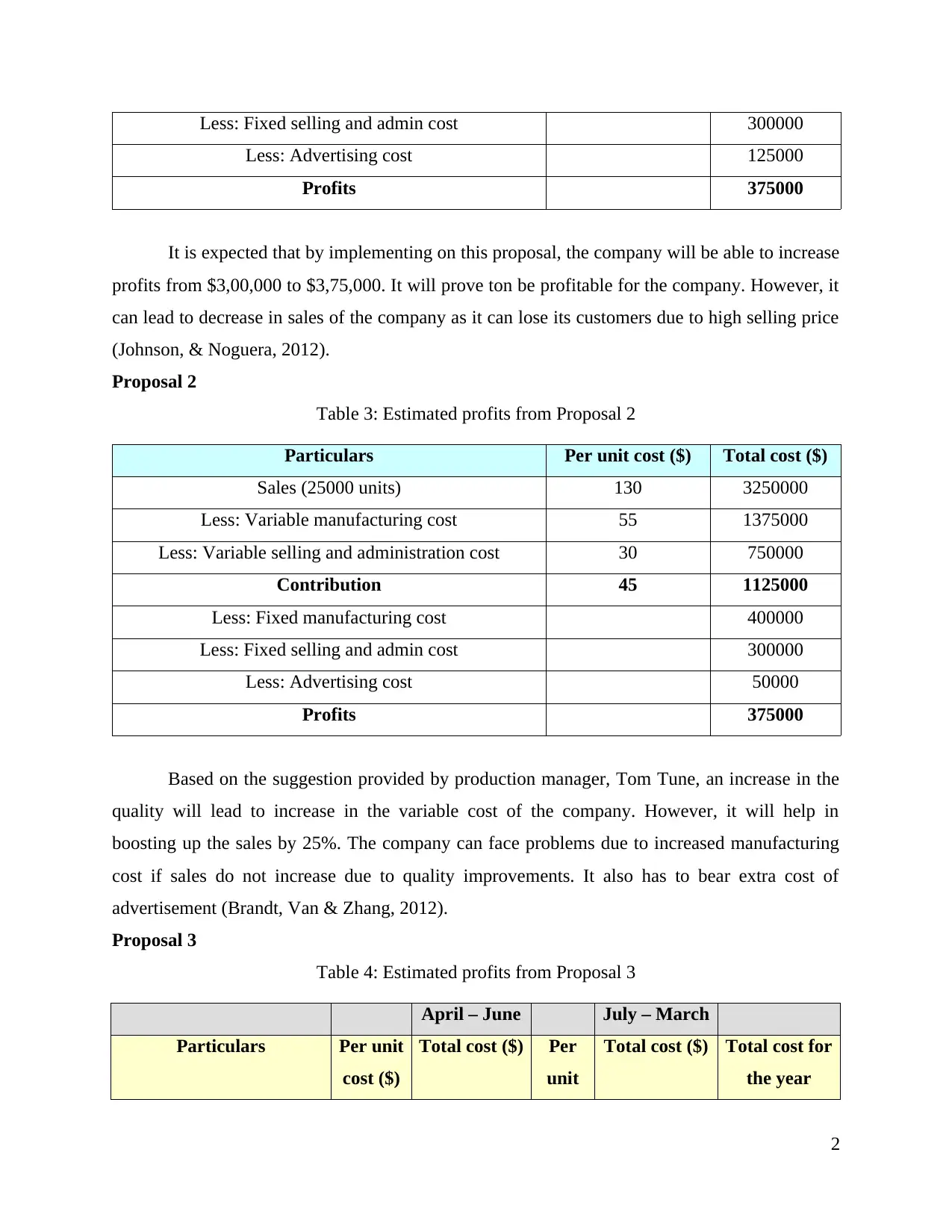

Proposal 2

Table 3: Estimated profits from Proposal 2

Particulars Per unit cost ($) Total cost ($)

Sales (25000 units) 130 3250000

Less: Variable manufacturing cost 55 1375000

Less: Variable selling and administration cost 30 750000

Contribution 45 1125000

Less: Fixed manufacturing cost 400000

Less: Fixed selling and admin cost 300000

Less: Advertising cost 50000

Profits 375000

Based on the suggestion provided by production manager, Tom Tune, an increase in the

quality will lead to increase in the variable cost of the company. However, it will help in

boosting up the sales by 25%. The company can face problems due to increased manufacturing

cost if sales do not increase due to quality improvements. It also has to bear extra cost of

advertisement (Brandt, Van & Zhang, 2012).

Proposal 3

Table 4: Estimated profits from Proposal 3

April – June July – March

Particulars Per unit

cost ($)

Total cost ($) Per

unit

Total cost ($) Total cost for

the year

2

Less: Advertising cost 125000

Profits 375000

It is expected that by implementing on this proposal, the company will be able to increase

profits from $3,00,000 to $3,75,000. It will prove ton be profitable for the company. However, it

can lead to decrease in sales of the company as it can lose its customers due to high selling price

(Johnson, & Noguera, 2012).

Proposal 2

Table 3: Estimated profits from Proposal 2

Particulars Per unit cost ($) Total cost ($)

Sales (25000 units) 130 3250000

Less: Variable manufacturing cost 55 1375000

Less: Variable selling and administration cost 30 750000

Contribution 45 1125000

Less: Fixed manufacturing cost 400000

Less: Fixed selling and admin cost 300000

Less: Advertising cost 50000

Profits 375000

Based on the suggestion provided by production manager, Tom Tune, an increase in the

quality will lead to increase in the variable cost of the company. However, it will help in

boosting up the sales by 25%. The company can face problems due to increased manufacturing

cost if sales do not increase due to quality improvements. It also has to bear extra cost of

advertisement (Brandt, Van & Zhang, 2012).

Proposal 3

Table 4: Estimated profits from Proposal 3

April – June July – March

Particulars Per unit

cost ($)

Total cost ($) Per

unit

Total cost ($) Total cost for

the year

2

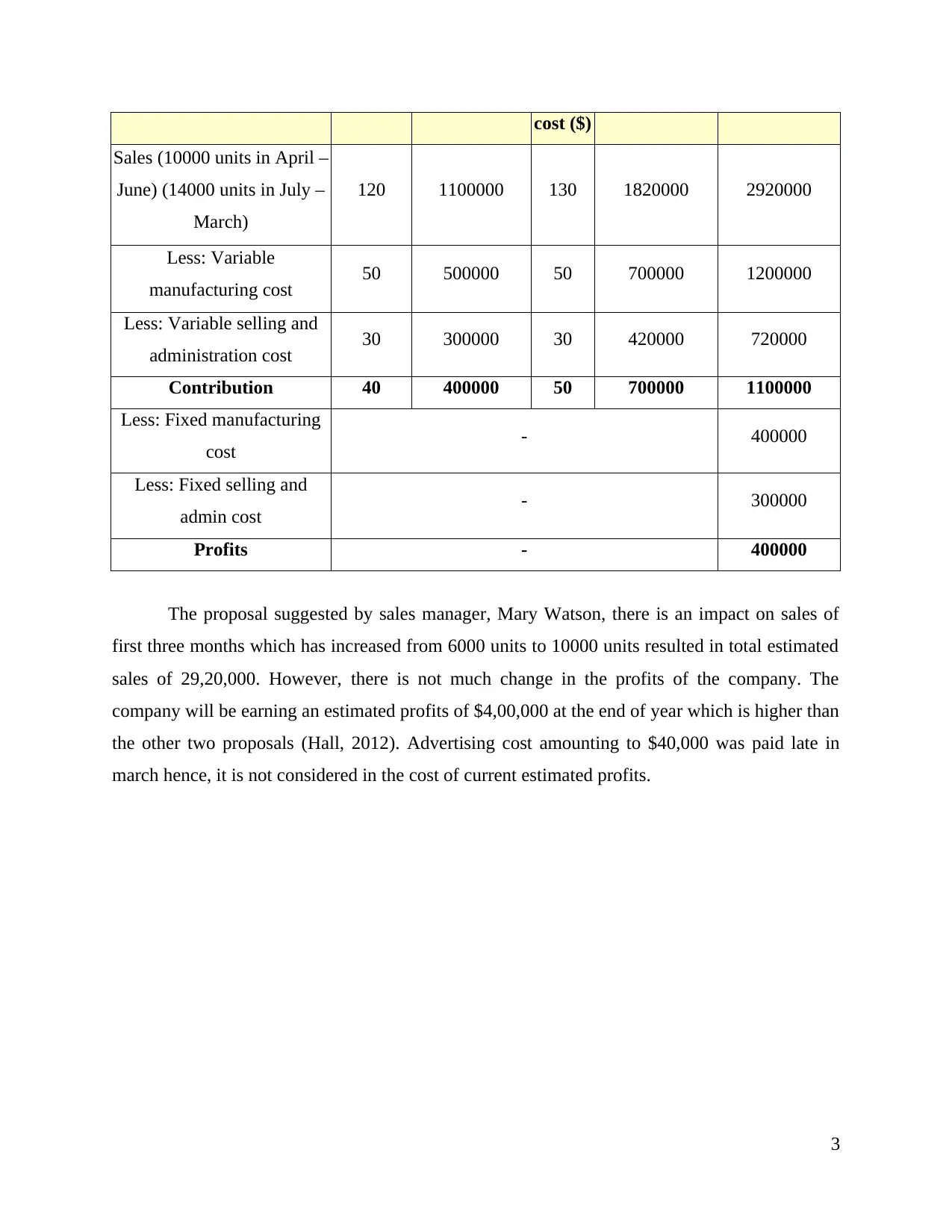

cost ($)

Sales (10000 units in April –

June) (14000 units in July –

March)

120 1100000 130 1820000 2920000

Less: Variable

manufacturing cost 50 500000 50 700000 1200000

Less: Variable selling and

administration cost 30 300000 30 420000 720000

Contribution 40 400000 50 700000 1100000

Less: Fixed manufacturing

cost - 400000

Less: Fixed selling and

admin cost - 300000

Profits - 400000

The proposal suggested by sales manager, Mary Watson, there is an impact on sales of

first three months which has increased from 6000 units to 10000 units resulted in total estimated

sales of 29,20,000. However, there is not much change in the profits of the company. The

company will be earning an estimated profits of $4,00,000 at the end of year which is higher than

the other two proposals (Hall, 2012). Advertising cost amounting to $40,000 was paid late in

march hence, it is not considered in the cost of current estimated profits.

3

Sales (10000 units in April –

June) (14000 units in July –

March)

120 1100000 130 1820000 2920000

Less: Variable

manufacturing cost 50 500000 50 700000 1200000

Less: Variable selling and

administration cost 30 300000 30 420000 720000

Contribution 40 400000 50 700000 1100000

Less: Fixed manufacturing

cost - 400000

Less: Fixed selling and

admin cost - 300000

Profits - 400000

The proposal suggested by sales manager, Mary Watson, there is an impact on sales of

first three months which has increased from 6000 units to 10000 units resulted in total estimated

sales of 29,20,000. However, there is not much change in the profits of the company. The

company will be earning an estimated profits of $4,00,000 at the end of year which is higher than

the other two proposals (Hall, 2012). Advertising cost amounting to $40,000 was paid late in

march hence, it is not considered in the cost of current estimated profits.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

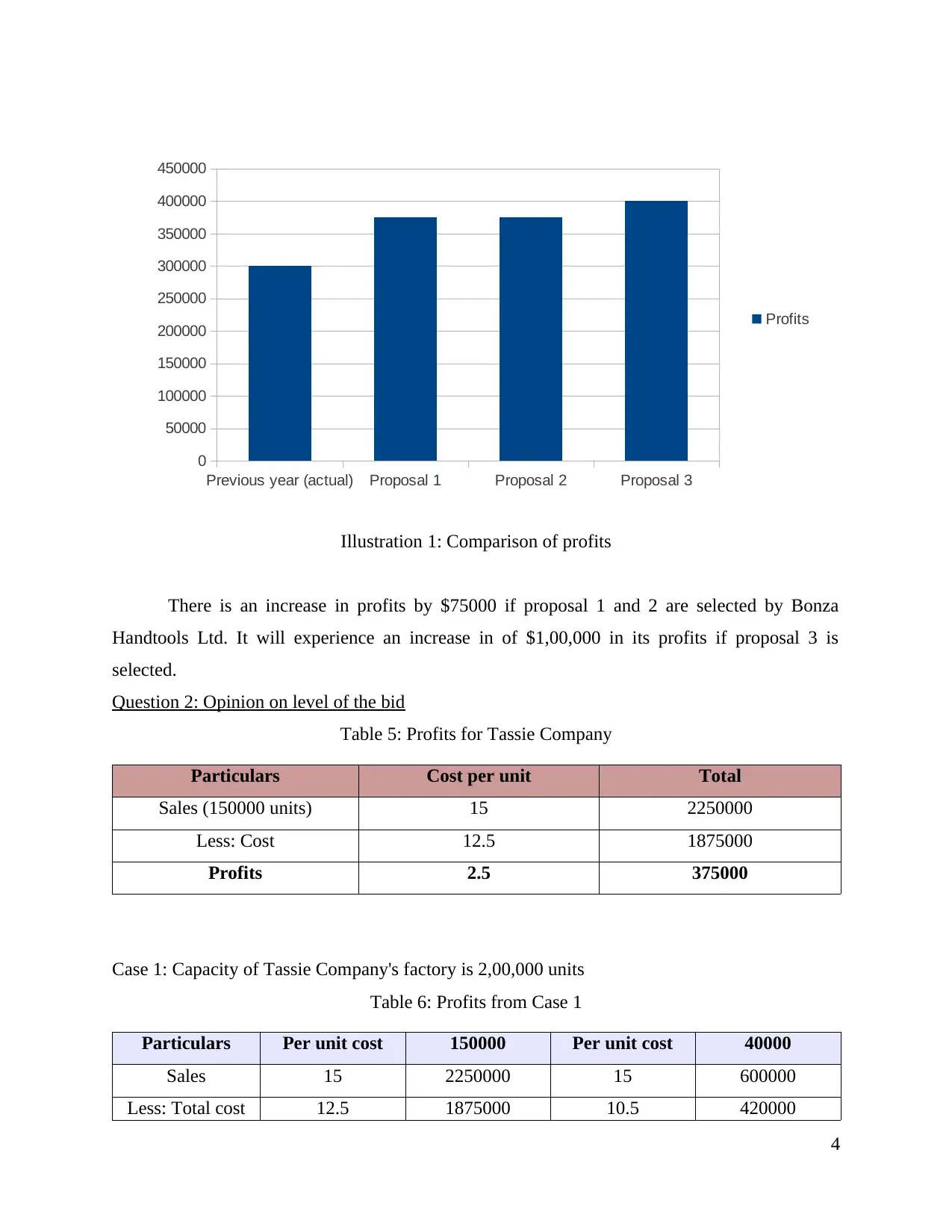

There is an increase in profits by $75000 if proposal 1 and 2 are selected by Bonza

Handtools Ltd. It will experience an increase in of $1,00,000 in its profits if proposal 3 is

selected.

Question 2: Opinion on level of the bid

Table 5: Profits for Tassie Company

Particulars Cost per unit Total

Sales (150000 units) 15 2250000

Less: Cost 12.5 1875000

Profits 2.5 375000

Case 1: Capacity of Tassie Company's factory is 2,00,000 units

Table 6: Profits from Case 1

Particulars Per unit cost 150000 Per unit cost 40000

Sales 15 2250000 15 600000

Less: Total cost 12.5 1875000 10.5 420000

4

Previous year (actual) Proposal 1 Proposal 2 Proposal 3

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

Profits

Illustration 1: Comparison of profits

Handtools Ltd. It will experience an increase in of $1,00,000 in its profits if proposal 3 is

selected.

Question 2: Opinion on level of the bid

Table 5: Profits for Tassie Company

Particulars Cost per unit Total

Sales (150000 units) 15 2250000

Less: Cost 12.5 1875000

Profits 2.5 375000

Case 1: Capacity of Tassie Company's factory is 2,00,000 units

Table 6: Profits from Case 1

Particulars Per unit cost 150000 Per unit cost 40000

Sales 15 2250000 15 600000

Less: Total cost 12.5 1875000 10.5 420000

4

Previous year (actual) Proposal 1 Proposal 2 Proposal 3

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

Profits

Illustration 1: Comparison of profits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

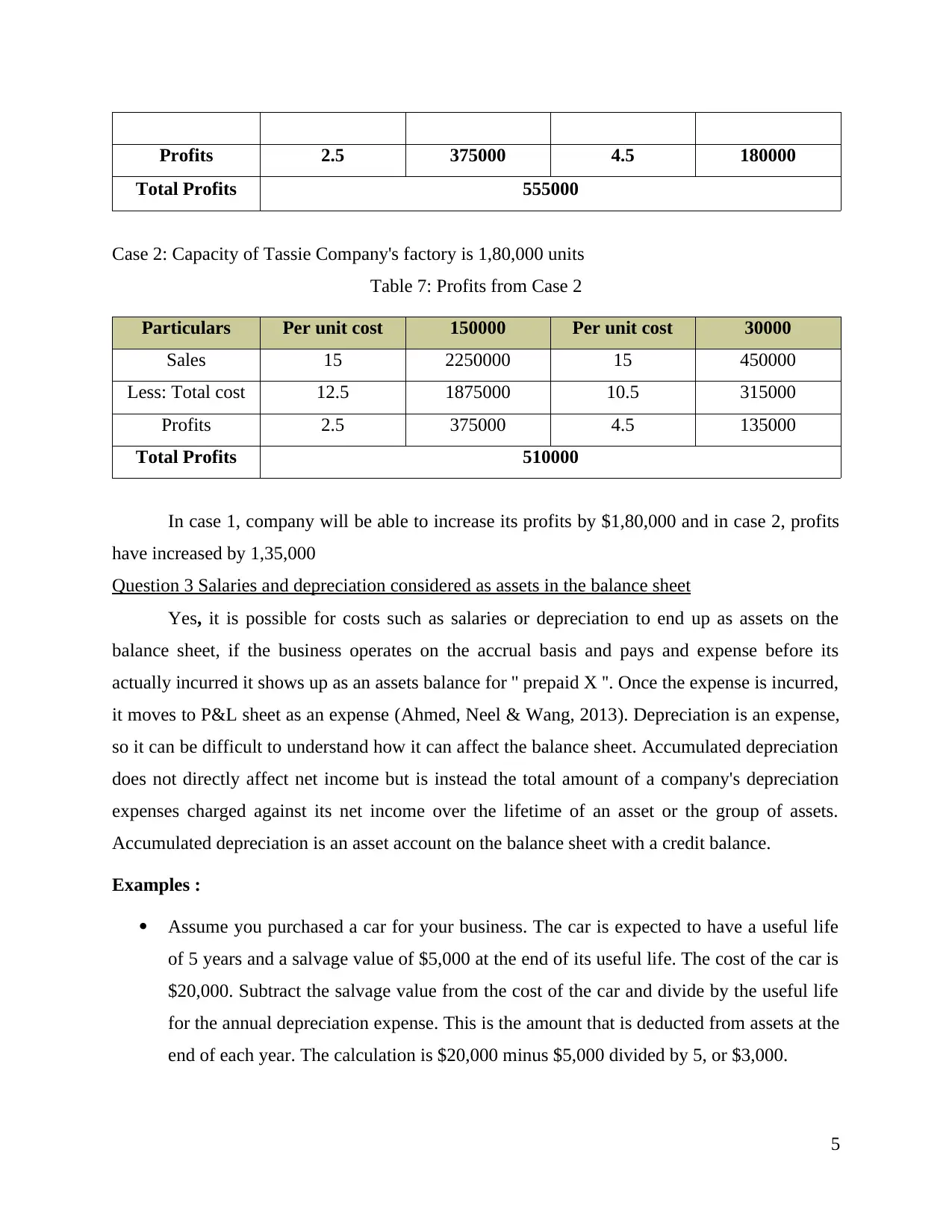

Profits 2.5 375000 4.5 180000

Total Profits 555000

Case 2: Capacity of Tassie Company's factory is 1,80,000 units

Table 7: Profits from Case 2

Particulars Per unit cost 150000 Per unit cost 30000

Sales 15 2250000 15 450000

Less: Total cost 12.5 1875000 10.5 315000

Profits 2.5 375000 4.5 135000

Total Profits 510000

In case 1, company will be able to increase its profits by $1,80,000 and in case 2, profits

have increased by 1,35,000

Question 3 Salaries and depreciation considered as assets in the balance sheet

Yes, it is possible for costs such as salaries or depreciation to end up as assets on the

balance sheet, if the business operates on the accrual basis and pays and expense before its

actually incurred it shows up as an assets balance for '' prepaid X ''. Once the expense is incurred,

it moves to P&L sheet as an expense (Ahmed, Neel & Wang, 2013). Depreciation is an expense,

so it can be difficult to understand how it can affect the balance sheet. Accumulated depreciation

does not directly affect net income but is instead the total amount of a company's depreciation

expenses charged against its net income over the lifetime of an asset or the group of assets.

Accumulated depreciation is an asset account on the balance sheet with a credit balance.

Examples :

Assume you purchased a car for your business. The car is expected to have a useful life

of 5 years and a salvage value of $5,000 at the end of its useful life. The cost of the car is

$20,000. Subtract the salvage value from the cost of the car and divide by the useful life

for the annual depreciation expense. This is the amount that is deducted from assets at the

end of each year. The calculation is $20,000 minus $5,000 divided by 5, or $3,000.

5

Total Profits 555000

Case 2: Capacity of Tassie Company's factory is 1,80,000 units

Table 7: Profits from Case 2

Particulars Per unit cost 150000 Per unit cost 30000

Sales 15 2250000 15 450000

Less: Total cost 12.5 1875000 10.5 315000

Profits 2.5 375000 4.5 135000

Total Profits 510000

In case 1, company will be able to increase its profits by $1,80,000 and in case 2, profits

have increased by 1,35,000

Question 3 Salaries and depreciation considered as assets in the balance sheet

Yes, it is possible for costs such as salaries or depreciation to end up as assets on the

balance sheet, if the business operates on the accrual basis and pays and expense before its

actually incurred it shows up as an assets balance for '' prepaid X ''. Once the expense is incurred,

it moves to P&L sheet as an expense (Ahmed, Neel & Wang, 2013). Depreciation is an expense,

so it can be difficult to understand how it can affect the balance sheet. Accumulated depreciation

does not directly affect net income but is instead the total amount of a company's depreciation

expenses charged against its net income over the lifetime of an asset or the group of assets.

Accumulated depreciation is an asset account on the balance sheet with a credit balance.

Examples :

Assume you purchased a car for your business. The car is expected to have a useful life

of 5 years and a salvage value of $5,000 at the end of its useful life. The cost of the car is

$20,000. Subtract the salvage value from the cost of the car and divide by the useful life

for the annual depreciation expense. This is the amount that is deducted from assets at the

end of each year. The calculation is $20,000 minus $5,000 divided by 5, or $3,000.

5

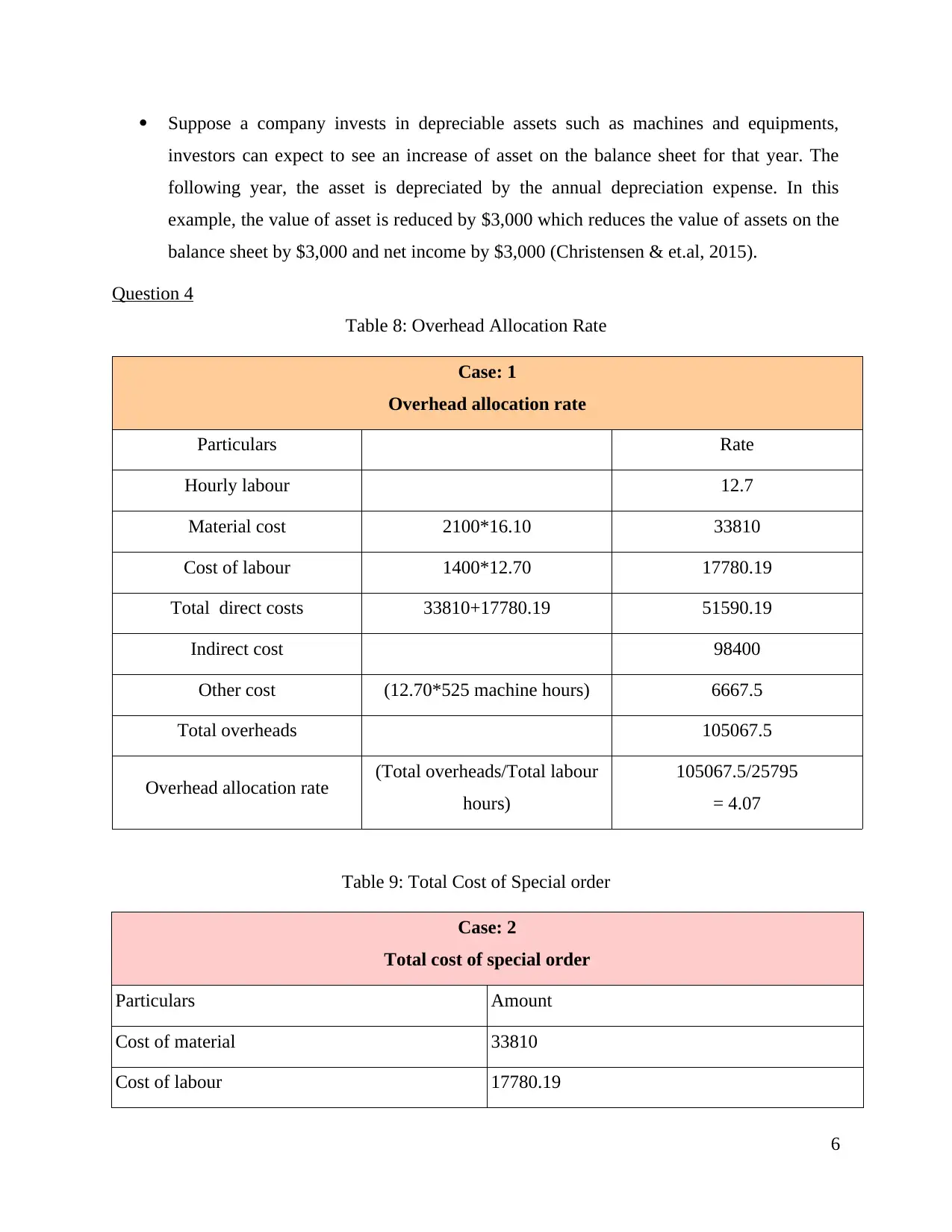

Suppose a company invests in depreciable assets such as machines and equipments,

investors can expect to see an increase of asset on the balance sheet for that year. The

following year, the asset is depreciated by the annual depreciation expense. In this

example, the value of asset is reduced by $3,000 which reduces the value of assets on the

balance sheet by $3,000 and net income by $3,000 (Christensen & et.al, 2015).

Question 4

Table 8: Overhead Allocation Rate

Case: 1

Overhead allocation rate

Particulars Rate

Hourly labour 12.7

Material cost 2100*16.10 33810

Cost of labour 1400*12.70 17780.19

Total direct costs 33810+17780.19 51590.19

Indirect cost 98400

Other cost (12.70*525 machine hours) 6667.5

Total overheads 105067.5

Overhead allocation rate (Total overheads/Total labour

hours)

105067.5/25795

= 4.07

Table 9: Total Cost of Special order

Case: 2

Total cost of special order

Particulars Amount

Cost of material 33810

Cost of labour 17780.19

6

investors can expect to see an increase of asset on the balance sheet for that year. The

following year, the asset is depreciated by the annual depreciation expense. In this

example, the value of asset is reduced by $3,000 which reduces the value of assets on the

balance sheet by $3,000 and net income by $3,000 (Christensen & et.al, 2015).

Question 4

Table 8: Overhead Allocation Rate

Case: 1

Overhead allocation rate

Particulars Rate

Hourly labour 12.7

Material cost 2100*16.10 33810

Cost of labour 1400*12.70 17780.19

Total direct costs 33810+17780.19 51590.19

Indirect cost 98400

Other cost (12.70*525 machine hours) 6667.5

Total overheads 105067.5

Overhead allocation rate (Total overheads/Total labour

hours)

105067.5/25795

= 4.07

Table 9: Total Cost of Special order

Case: 2

Total cost of special order

Particulars Amount

Cost of material 33810

Cost of labour 17780.19

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

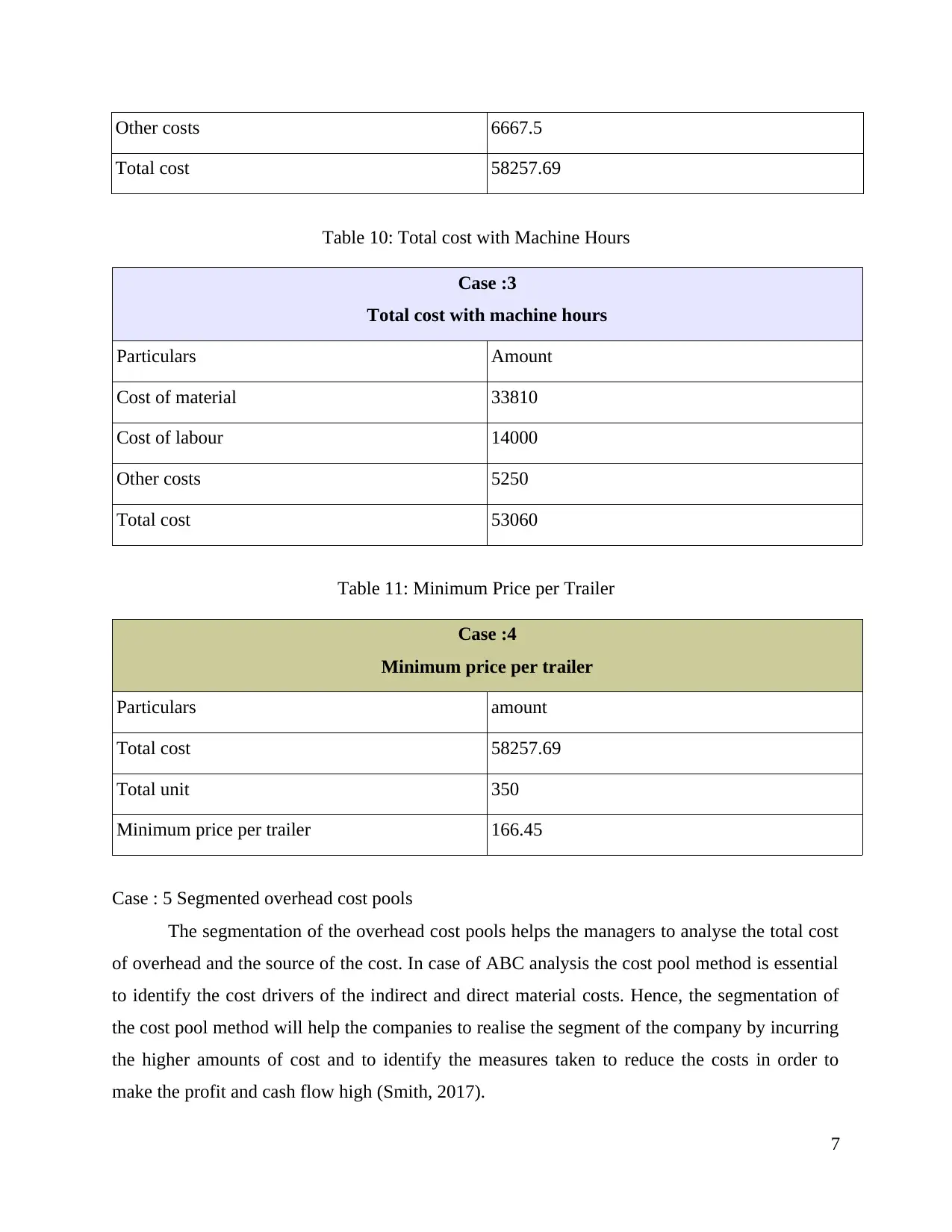

Other costs 6667.5

Total cost 58257.69

Table 10: Total cost with Machine Hours

Case :3

Total cost with machine hours

Particulars Amount

Cost of material 33810

Cost of labour 14000

Other costs 5250

Total cost 53060

Table 11: Minimum Price per Trailer

Case :4

Minimum price per trailer

Particulars amount

Total cost 58257.69

Total unit 350

Minimum price per trailer 166.45

Case : 5 Segmented overhead cost pools

The segmentation of the overhead cost pools helps the managers to analyse the total cost

of overhead and the source of the cost. In case of ABC analysis the cost pool method is essential

to identify the cost drivers of the indirect and direct material costs. Hence, the segmentation of

the cost pool method will help the companies to realise the segment of the company by incurring

the higher amounts of cost and to identify the measures taken to reduce the costs in order to

make the profit and cash flow high (Smith, 2017).

7

Total cost 58257.69

Table 10: Total cost with Machine Hours

Case :3

Total cost with machine hours

Particulars Amount

Cost of material 33810

Cost of labour 14000

Other costs 5250

Total cost 53060

Table 11: Minimum Price per Trailer

Case :4

Minimum price per trailer

Particulars amount

Total cost 58257.69

Total unit 350

Minimum price per trailer 166.45

Case : 5 Segmented overhead cost pools

The segmentation of the overhead cost pools helps the managers to analyse the total cost

of overhead and the source of the cost. In case of ABC analysis the cost pool method is essential

to identify the cost drivers of the indirect and direct material costs. Hence, the segmentation of

the cost pool method will help the companies to realise the segment of the company by incurring

the higher amounts of cost and to identify the measures taken to reduce the costs in order to

make the profit and cash flow high (Smith, 2017).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

Based on the above report, it can be concluded that it is important to correctly analyse the

selling price and cost in order to attain maximum profits for the organization (Weil, Schipper &

Francis, 2013). The entity should consider all aspect related to sales before deciding advertising

budget for itself. Salaries and depreciation can be considered as an asset for the entity if amounts

have been paid in advance.

8

Based on the above report, it can be concluded that it is important to correctly analyse the

selling price and cost in order to attain maximum profits for the organization (Weil, Schipper &

Francis, 2013). The entity should consider all aspect related to sales before deciding advertising

budget for itself. Salaries and depreciation can be considered as an asset for the entity if amounts

have been paid in advance.

8

REFERENCES

Books and Journals

Ahmed, A. S., Neel, M. & Wang, D. (2013). Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

1344-1372.

Brandt, L., Van Biesebroeck, J. & Zhang, Y. (2012). Creative accounting or creative

destruction? Firm-level productivity growth in Chinese manufacturing. Journal of

development economics. 97(2). 339-351.

Christensen, H. B. & et.al. (2015). Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). 31-61.

Hall, J. A. (2012). Accounting information systems. Cengage Learning.

Johnson, R. C. & Noguera, G. (2012). Accounting for intermediates: Production sharing and

trade in value added. Journal of international Economics. 86(2). 224-236.

Romney, M. B. & Steinbart, P. J. (2012). Accounting information systems. Boston: Pearson.

Smith, M. (2017). Research methods in accounting. Sage.

Weil, R. L., Schipper, K. & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

9

Books and Journals

Ahmed, A. S., Neel, M. & Wang, D. (2013). Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

1344-1372.

Brandt, L., Van Biesebroeck, J. & Zhang, Y. (2012). Creative accounting or creative

destruction? Firm-level productivity growth in Chinese manufacturing. Journal of

development economics. 97(2). 339-351.

Christensen, H. B. & et.al. (2015). Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). 31-61.

Hall, J. A. (2012). Accounting information systems. Cengage Learning.

Johnson, R. C. & Noguera, G. (2012). Accounting for intermediates: Production sharing and

trade in value added. Journal of international Economics. 86(2). 224-236.

Romney, M. B. & Steinbart, P. J. (2012). Accounting information systems. Boston: Pearson.

Smith, M. (2017). Research methods in accounting. Sage.

Weil, R. L., Schipper, K. & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12