Strategic Information Systems: Paradise Industries Case Study Analysis

VerifiedAdded on 2023/01/11

|10

|2510

|96

Case Study

AI Summary

This case study analyzes the strategic information systems of Paradise Industries, focusing on their accounting information systems. The report examines the purpose and role of accounting information systems in today's business environment, followed by detailed system flow charts of the expenditure and conversion cycles. It then identifies and analyzes the physical internal control weaknesses within the expenditure cycle, highlighting vulnerabilities in supplier selection, purchase order processing, and data verification. The study further assesses the risks inherent in the conversion cycle, such as the lack of integration between cycles and inadequate monitoring of raw material usage. Finally, the report recommends changes to reduce these risks and improve overall operational efficiency, emphasizing the need for enhanced internal controls and system integration.

STRATEGIC

INFORMATION SYSTEMS

FOR BUSINESS AND

ENTERPRISE

INFORMATION SYSTEMS

FOR BUSINESS AND

ENTERPRISE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Purpose and role of accounting information systems in Mapping today’s business environment

.....................................................................................................................................................1

System flow chart of expenditure cycle.......................................................................................2

System flow chart of conversion cycle........................................................................................3

Analysis of physical internal control weaknesses in the expenditure cycle................................5

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks. 6

CONCLUSION................................................................................................................................7

REREFENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Purpose and role of accounting information systems in Mapping today’s business environment

.....................................................................................................................................................1

System flow chart of expenditure cycle.......................................................................................2

System flow chart of conversion cycle........................................................................................3

Analysis of physical internal control weaknesses in the expenditure cycle................................5

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks. 6

CONCLUSION................................................................................................................................7

REREFENCES................................................................................................................................8

INTRODUCTION

Strategic information systems are those systems that are used by organizations which

helps them to alter their plans, business strategies and also helps them in managing their internal

operations in an appropriate manner. Such systems are extremely important for organizations as

it helps them to support major aspects of business such as data analysis, storage of accounting

information, record keeping, effective communication and for many other purposes (Cassidy,

2016). Most of the business and enterprises uses these strategic information systems in order to

manage and maintain their operations, deal with products or services offered by them and also

find opportunities in order to enhance their operational efficiency. There are various kinds of

strategic information system used that used by business and enterprises, one of them is

accounting information systems which is used by organizations in order to collect, manage, store,

retrieve, process, and report its financial data so it can be used by accountants, consultants,

business analysts, managers and others for management of business operations (Holder and et.

al., 2016). This report is based upon a case study of Paradise Industries who have a centralised

computer system with distributed terminals and recently they have been facing number of

operational problems and for this managing director of the company have hired a consultant to

assess its systems and processes. This report will lay emphasis upon System flow chart of

expenditure cycle and conversion cycle, analysis of physical internal control weaknesses in the

expenditure cycle, analysis of the risks exists in the conversion cycle and the changes needed to

reduce the risks.

MAIN BODY

Purpose and role of accounting information systems in Mapping today’s business environment

The main purpose of accounting information system is to store and collect all kinds of

accounting and financial data in order to produce report that can be used by managers so that

they can take effective and appropriate business decisions. It helps organizations in proving

proper and accurate data so that it can be used for other organizational operations (Zhang, Long

and Ma, 2018). It is used for different purposes within organizations. In paradise industries it can

be used for various purposes such as for updating general ledger accounts, purchase requisition,

update accounts payable subsidiary ledger and for many other purposes. If there is any kind of

item which is due to be paid then it helps in generating due amount of check to be paid.

1

Strategic information systems are those systems that are used by organizations which

helps them to alter their plans, business strategies and also helps them in managing their internal

operations in an appropriate manner. Such systems are extremely important for organizations as

it helps them to support major aspects of business such as data analysis, storage of accounting

information, record keeping, effective communication and for many other purposes (Cassidy,

2016). Most of the business and enterprises uses these strategic information systems in order to

manage and maintain their operations, deal with products or services offered by them and also

find opportunities in order to enhance their operational efficiency. There are various kinds of

strategic information system used that used by business and enterprises, one of them is

accounting information systems which is used by organizations in order to collect, manage, store,

retrieve, process, and report its financial data so it can be used by accountants, consultants,

business analysts, managers and others for management of business operations (Holder and et.

al., 2016). This report is based upon a case study of Paradise Industries who have a centralised

computer system with distributed terminals and recently they have been facing number of

operational problems and for this managing director of the company have hired a consultant to

assess its systems and processes. This report will lay emphasis upon System flow chart of

expenditure cycle and conversion cycle, analysis of physical internal control weaknesses in the

expenditure cycle, analysis of the risks exists in the conversion cycle and the changes needed to

reduce the risks.

MAIN BODY

Purpose and role of accounting information systems in Mapping today’s business environment

The main purpose of accounting information system is to store and collect all kinds of

accounting and financial data in order to produce report that can be used by managers so that

they can take effective and appropriate business decisions. It helps organizations in proving

proper and accurate data so that it can be used for other organizational operations (Zhang, Long

and Ma, 2018). It is used for different purposes within organizations. In paradise industries it can

be used for various purposes such as for updating general ledger accounts, purchase requisition,

update accounts payable subsidiary ledger and for many other purposes. If there is any kind of

item which is due to be paid then it helps in generating due amount of check to be paid.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, there are various kinds of issues or problems that they have been facing within their

business operations.

System flow chart of expenditure cycle

Most of the task done in expenditure cycle are done manually. When a purchase

requisition is generated it is directly printed on purchasing department. After than manually

purchasing clerk select suppliers in order to prepare purchase order (Haghighi and Torabi.,

2018). One purchase order is sent to supplier and another is sent to receiving department. After

this purchase clear open purchase order file with the help of an update program. When order is

received by the clerk, it is reconciled with packing slip and the purchasing order so that hard

copy of receiving report can be prepared. After this manually receiving report hard copy is

prepared in order to record quantity and quality of received goods. Two copies of this receiving

report are generated, one is sent to warehouse with items and another one is sent to receiving

department. Receiving clerk uses department terminal and add record to digital receiving report.

After receiving the digital receiving report, system automatically closes purchase order and

update inventory subsidiary ledger with the help of terminal. After this when invoice of suppliers

is received, records ate added to supplier’s invoice files which automatically on the basis of

financial records set up a liability in the accounts payable subsidiary ledger. This update updates

all affected general ledger accounts automatically. System scans accounts payable subsidiary

ledger every day and if there is any amount which is due to be paid then in such case, they print

cheque. One copy of suppliers is sent to cash disbursements and another to suppliers. After

payment amount is added to cheque register and liabilities of accounts payable subsidiary ledger

are removed.

2

business operations.

System flow chart of expenditure cycle

Most of the task done in expenditure cycle are done manually. When a purchase

requisition is generated it is directly printed on purchasing department. After than manually

purchasing clerk select suppliers in order to prepare purchase order (Haghighi and Torabi.,

2018). One purchase order is sent to supplier and another is sent to receiving department. After

this purchase clear open purchase order file with the help of an update program. When order is

received by the clerk, it is reconciled with packing slip and the purchasing order so that hard

copy of receiving report can be prepared. After this manually receiving report hard copy is

prepared in order to record quantity and quality of received goods. Two copies of this receiving

report are generated, one is sent to warehouse with items and another one is sent to receiving

department. Receiving clerk uses department terminal and add record to digital receiving report.

After receiving the digital receiving report, system automatically closes purchase order and

update inventory subsidiary ledger with the help of terminal. After this when invoice of suppliers

is received, records ate added to supplier’s invoice files which automatically on the basis of

financial records set up a liability in the accounts payable subsidiary ledger. This update updates

all affected general ledger accounts automatically. System scans accounts payable subsidiary

ledger every day and if there is any amount which is due to be paid then in such case, they print

cheque. One copy of suppliers is sent to cash disbursements and another to suppliers. After

payment amount is added to cheque register and liabilities of accounts payable subsidiary ledger

are removed.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

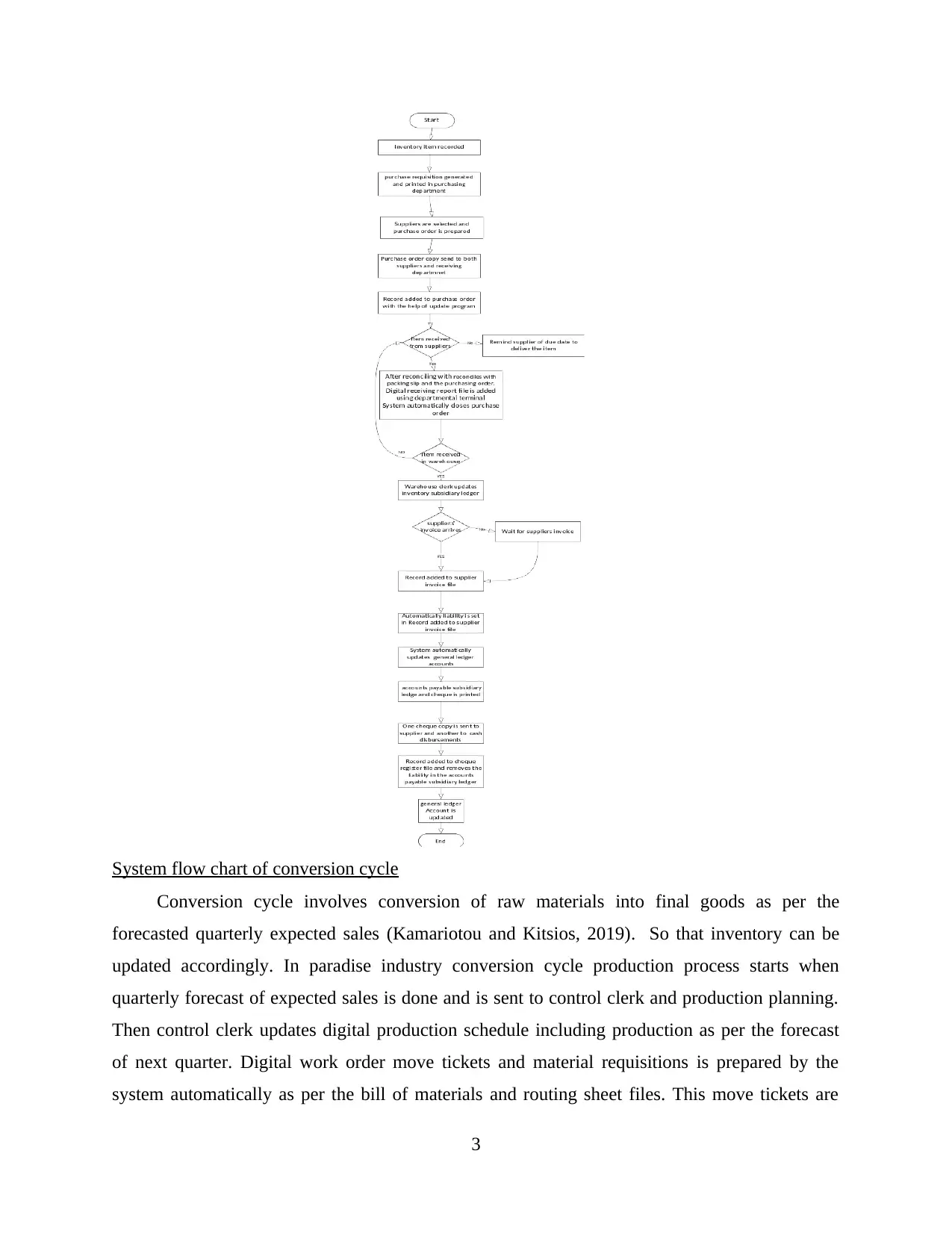

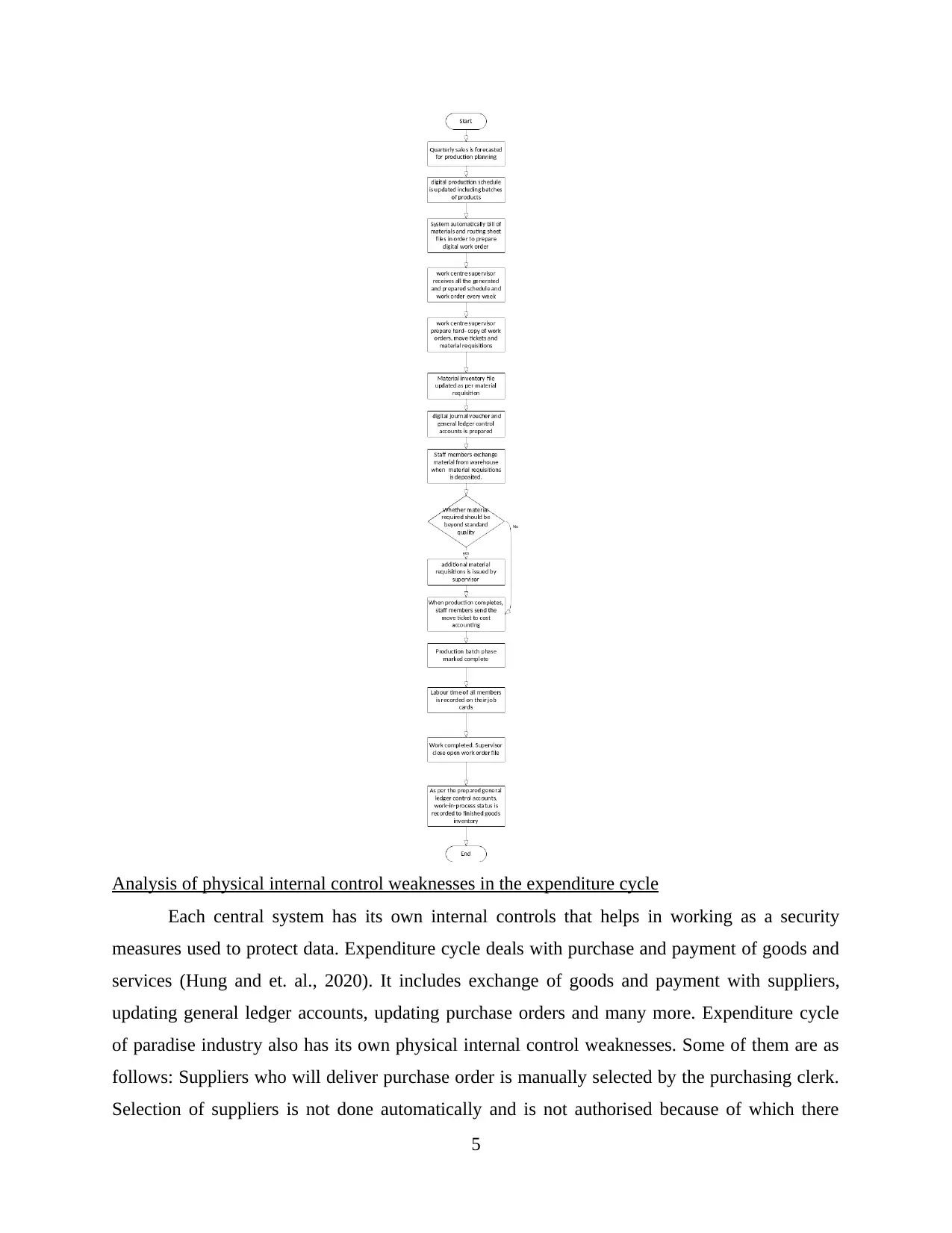

System flow chart of conversion cycle

Conversion cycle involves conversion of raw materials into final goods as per the

forecasted quarterly expected sales (Kamariotou and Kitsios, 2019). So that inventory can be

updated accordingly. In paradise industry conversion cycle production process starts when

quarterly forecast of expected sales is done and is sent to control clerk and production planning.

Then control clerk updates digital production schedule including production as per the forecast

of next quarter. Digital work order move tickets and material requisitions is prepared by the

system automatically as per the bill of materials and routing sheet files. This move tickets are

3

Conversion cycle involves conversion of raw materials into final goods as per the

forecasted quarterly expected sales (Kamariotou and Kitsios, 2019). So that inventory can be

updated accordingly. In paradise industry conversion cycle production process starts when

quarterly forecast of expected sales is done and is sent to control clerk and production planning.

Then control clerk updates digital production schedule including production as per the forecast

of next quarter. Digital work order move tickets and material requisitions is prepared by the

system automatically as per the bill of materials and routing sheet files. This move tickets are

3

sent to work centre supervisor’s terminal. All the digital documents are then accessed by work

centre supervisor so that they can print hard copy of work orders, move tickets and material

requisitions and sent copies to material requisitions to each work centre. material requisitions is

them set to warehouse so that material can be exchanges as per the requirement of work order.

Other than this, if additional material is required beyond the standard quality then in such case

additional material requisitions is issued by the supervisor. Warehouse clerk updates material

inventory file as per the copy of material requisitions and then one copy of it is sent to warehouse

office and another to cost accounting. Everyday at the end of the day, digital journal voucher and

general ledger control accounts is prepared. When the production is completed, all the staff

members sent their move ticket to cost accounting so that phase completion can be marked.

When the work order is completed supervisor closed the open work order. Cost accounting clerk

access digital work order and mark work in progress or work closed.

4

centre supervisor so that they can print hard copy of work orders, move tickets and material

requisitions and sent copies to material requisitions to each work centre. material requisitions is

them set to warehouse so that material can be exchanges as per the requirement of work order.

Other than this, if additional material is required beyond the standard quality then in such case

additional material requisitions is issued by the supervisor. Warehouse clerk updates material

inventory file as per the copy of material requisitions and then one copy of it is sent to warehouse

office and another to cost accounting. Everyday at the end of the day, digital journal voucher and

general ledger control accounts is prepared. When the production is completed, all the staff

members sent their move ticket to cost accounting so that phase completion can be marked.

When the work order is completed supervisor closed the open work order. Cost accounting clerk

access digital work order and mark work in progress or work closed.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of physical internal control weaknesses in the expenditure cycle

Each central system has its own internal controls that helps in working as a security

measures used to protect data. Expenditure cycle deals with purchase and payment of goods and

services (Hung and et. al., 2020). It includes exchange of goods and payment with suppliers,

updating general ledger accounts, updating purchase orders and many more. Expenditure cycle

of paradise industry also has its own physical internal control weaknesses. Some of them are as

follows: Suppliers who will deliver purchase order is manually selected by the purchasing clerk.

Selection of suppliers is not done automatically and is not authorised because of which there

5

Each central system has its own internal controls that helps in working as a security

measures used to protect data. Expenditure cycle deals with purchase and payment of goods and

services (Hung and et. al., 2020). It includes exchange of goods and payment with suppliers,

updating general ledger accounts, updating purchase orders and many more. Expenditure cycle

of paradise industry also has its own physical internal control weaknesses. Some of them are as

follows: Suppliers who will deliver purchase order is manually selected by the purchasing clerk.

Selection of suppliers is not done automatically and is not authorised because of which there

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

might be variation within final invoice, delivery date. In this no approval of requisition is done.

Not only this, selected suppliers are not approved by the department, they are directly selected

and purchase or is sent to them without any verification and authorization. Vendor and supplier

list is not even updated from time to time and their basic prices as well. Due to this receiving

incorrect quantities or damaged goods can increase. Purchase order within system is opened

manually by the purchase clerk with the help of update program. If any kind of issue or problem

within update program occurs then it can impact opening or closing of purchase order.

Reconciling of received item from suppliers with packing slip and the purchasing order is also

done manually by the receiving clerk and on the basis of it, receiving report is also prepared

manually. It is one of the major weakness of this cycle because any kind of mistake done by

receiving clerk, then in such case, issue can be generated within receiving report as well. It is one

of the main weakness because on the basis of this report, inventory subsidiary ledger is updated

automatically updated. So, it is extremely important to automate these task as it can impact

ledger updating because of which there can be chances within payable amount. Another physical

internal control weakness identified in this cycle was that User who will be using the system and

updating data or generating reports is not verified by the system i.e. anyone who has userid and

passwords can use the system and bring changes within it. In whole overall process cycle, there

is no verification or checking or approval within the system whether it is in terms of user using

the system, approval of invoice, selection of vendor and many more. It is important to focus on

this weakness of the system by the paradise industries in order to reduce problems associated

with expenditure cycle.

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks

Each system or a process has its own internal controls that helps in working as a security

measures used to protect data (Galliers, Leidner and Simeonova eds., 2020). Conversion cycle

deals with production of items as required according to the forecasted sales. There are various

kinds of risk exist within this conversion cycle which is required to be focused on and reduced so

that the issues or risk associated with the system can be reduced: Digital production schedule is

manually produced by the control clerk, so it becomes important for the company to appoint a

work centre supervisor so that production schedule can be brought into working because if the

supervisor is not appointed then it can become difficult to follow the production schedule

appropriately because of which there can be issues within final goods produced. There is no

6

Not only this, selected suppliers are not approved by the department, they are directly selected

and purchase or is sent to them without any verification and authorization. Vendor and supplier

list is not even updated from time to time and their basic prices as well. Due to this receiving

incorrect quantities or damaged goods can increase. Purchase order within system is opened

manually by the purchase clerk with the help of update program. If any kind of issue or problem

within update program occurs then it can impact opening or closing of purchase order.

Reconciling of received item from suppliers with packing slip and the purchasing order is also

done manually by the receiving clerk and on the basis of it, receiving report is also prepared

manually. It is one of the major weakness of this cycle because any kind of mistake done by

receiving clerk, then in such case, issue can be generated within receiving report as well. It is one

of the main weakness because on the basis of this report, inventory subsidiary ledger is updated

automatically updated. So, it is extremely important to automate these task as it can impact

ledger updating because of which there can be chances within payable amount. Another physical

internal control weakness identified in this cycle was that User who will be using the system and

updating data or generating reports is not verified by the system i.e. anyone who has userid and

passwords can use the system and bring changes within it. In whole overall process cycle, there

is no verification or checking or approval within the system whether it is in terms of user using

the system, approval of invoice, selection of vendor and many more. It is important to focus on

this weakness of the system by the paradise industries in order to reduce problems associated

with expenditure cycle.

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks

Each system or a process has its own internal controls that helps in working as a security

measures used to protect data (Galliers, Leidner and Simeonova eds., 2020). Conversion cycle

deals with production of items as required according to the forecasted sales. There are various

kinds of risk exist within this conversion cycle which is required to be focused on and reduced so

that the issues or risk associated with the system can be reduced: Digital production schedule is

manually produced by the control clerk, so it becomes important for the company to appoint a

work centre supervisor so that production schedule can be brought into working because if the

supervisor is not appointed then it can become difficult to follow the production schedule

appropriately because of which there can be issues within final goods produced. There is no

6

linkage between expenditure cycle and conversion cycle because of which risk of theft of

damage of raw materials can be increased. Which can impact further process such as lack of

availability of material beyond standard quality. So, it is important to link both expenditure and

conversion cycle within the system so that track of raw materials within the warehouse can be

kept as well as quality of the material can also be maintained. Another risk associated with

conversion cycle is that in this production process and current stage of production of raw

material is neither monitored nor controlled because of which excess raw material can be used

due to which shortage of raw material problem can be faced by the work centre. It is important to

continuously monitor the production process, amount of raw materials that are being used for

production so that shortage of raw material situation is not faced by the work centre.

There are various ways though which these risk associated with conversion cycle can be

reduced such as: A monitoring and controlling process should also be added within production

process and it should be first and the foremost responsibility of the supervisor to monitor usage

of raw materials within production process so that effective and appropriate usage of raw

materials is done for conversion process. Both conversion and expenditure cycles should be

linked so that as the forecasted quarterly sales is uploaded, raw materials required from

warehouse are selected automatically so that it does not becomes difficult for the supervisor to

develop a material requisition. This will also help in increasing effectiveness of production

process. Not only this, it will also help in maintaining quality of raw materials with the

warehouse.

CONCLUSION

From the above report it has been analysed that there are various kinds of issues that can

be faced by an organization when they have a centralized system in various operations. It is

important to focus on all the internal weaknesses and risk associated with the system so that

effective control measures and required chances can be brought within the system. These internal

physical weaknesses are required to be focused on because it can create various kinds of security

threats and can impact overall operational process as well. In the above report, physical internal

control weaknesses in the expenditure cycle has been analysed and identified that can impact

overall expenditure process and can create security threats as well. Other than this, in the above

report, risks exist in the conversion cycle has also been identified and ways in which such risk

can be reduced in an appropriate and effective manner.

7

damage of raw materials can be increased. Which can impact further process such as lack of

availability of material beyond standard quality. So, it is important to link both expenditure and

conversion cycle within the system so that track of raw materials within the warehouse can be

kept as well as quality of the material can also be maintained. Another risk associated with

conversion cycle is that in this production process and current stage of production of raw

material is neither monitored nor controlled because of which excess raw material can be used

due to which shortage of raw material problem can be faced by the work centre. It is important to

continuously monitor the production process, amount of raw materials that are being used for

production so that shortage of raw material situation is not faced by the work centre.

There are various ways though which these risk associated with conversion cycle can be

reduced such as: A monitoring and controlling process should also be added within production

process and it should be first and the foremost responsibility of the supervisor to monitor usage

of raw materials within production process so that effective and appropriate usage of raw

materials is done for conversion process. Both conversion and expenditure cycles should be

linked so that as the forecasted quarterly sales is uploaded, raw materials required from

warehouse are selected automatically so that it does not becomes difficult for the supervisor to

develop a material requisition. This will also help in increasing effectiveness of production

process. Not only this, it will also help in maintaining quality of raw materials with the

warehouse.

CONCLUSION

From the above report it has been analysed that there are various kinds of issues that can

be faced by an organization when they have a centralized system in various operations. It is

important to focus on all the internal weaknesses and risk associated with the system so that

effective control measures and required chances can be brought within the system. These internal

physical weaknesses are required to be focused on because it can create various kinds of security

threats and can impact overall operational process as well. In the above report, physical internal

control weaknesses in the expenditure cycle has been analysed and identified that can impact

overall expenditure process and can create security threats as well. Other than this, in the above

report, risks exist in the conversion cycle has also been identified and ways in which such risk

can be reduced in an appropriate and effective manner.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REREFENCES

Books and Journals

Cassidy, A., 2016. A practical guide to information systems strategic planning. CRC press.

Galliers, R.D., Leidner, D.E. and Simeonova, B. eds., 2020. Strategic Information Management:

Theory and Practice. Routledge.

Haghighi, S.M. and Torabi, S.A., 2018. A novel mixed sustainability-resilience framework for

evaluating hospital information systems. International journal of medical

informatics. 118. pp.16-28.

Holder, A., and et. al., 2016. Do material weaknesses in information technology-related internal

controls affect firms'8-K filing timeliness and compliance?. International Journal of

Accounting Information Systems. 22. pp.26-43.

Hung, S.Y., and et. al., 2020. Effect of information service competence and contextual factors on

the effectiveness of strategic information systems planning in Hospitals. In Hospital

Management and Emergency Medicine: Breakthroughs in Research and Practice (pp.

146-171). IGI Global.

Kamariotou, M. and Kitsios, F., 2019. Strategic information systems planning. In Advanced

Methodologies and Technologies in Business Operations and Management (pp. 535-

546). IGI Global.

Zhang, P., Long, J. and Ma, J., 2018. How IT Awareness Impacts IT Control Weaknesses and

Firm Performance. Journal of International Technology and Information

Management. 27(2). pp.99-120.

8

Books and Journals

Cassidy, A., 2016. A practical guide to information systems strategic planning. CRC press.

Galliers, R.D., Leidner, D.E. and Simeonova, B. eds., 2020. Strategic Information Management:

Theory and Practice. Routledge.

Haghighi, S.M. and Torabi, S.A., 2018. A novel mixed sustainability-resilience framework for

evaluating hospital information systems. International journal of medical

informatics. 118. pp.16-28.

Holder, A., and et. al., 2016. Do material weaknesses in information technology-related internal

controls affect firms'8-K filing timeliness and compliance?. International Journal of

Accounting Information Systems. 22. pp.26-43.

Hung, S.Y., and et. al., 2020. Effect of information service competence and contextual factors on

the effectiveness of strategic information systems planning in Hospitals. In Hospital

Management and Emergency Medicine: Breakthroughs in Research and Practice (pp.

146-171). IGI Global.

Kamariotou, M. and Kitsios, F., 2019. Strategic information systems planning. In Advanced

Methodologies and Technologies in Business Operations and Management (pp. 535-

546). IGI Global.

Zhang, P., Long, J. and Ma, J., 2018. How IT Awareness Impacts IT Control Weaknesses and

Firm Performance. Journal of International Technology and Information

Management. 27(2). pp.99-120.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.