Accounting Information Systems: Adam & Co. Case Study Analysis Report

VerifiedAdded on 2022/10/19

|17

|3472

|343

Case Study

AI Summary

This case study analyzes the accounting information systems of Adam & Co., a Perth-based wholesaler, focusing on its expenditure cycle. The analysis reveals a centralized accounting system with weaknesses in the purchase, cash disbursement, and payroll systems. The purchase system lacks proper inventory checks, and clerks overlook their duties, leading to risks such as financial loss. The cash disbursement system suffers from a lack of document verification and personnel, increasing the risk of errors and theft. The payroll system, relying on manual timecards, also presents internal control weaknesses. The study identifies specific risks associated with each system, including financial theft, favoritism, and errors, emphasizing the need for improved internal controls and segregation of duties to mitigate these risks and enhance financial accountability. The case study concludes by summarizing the identified weaknesses and risks, highlighting the need for improvements in each system.

Running head: ACCOUNTING INFORMATION SYSTEMS

Accounting Information Systems

By Name of the Student

Group Number

Module Name

Accounting Information Systems

By Name of the Student

Group Number

Module Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEMS

Executive Summary

The study relates to Perth-based wholesaler Adam & Co. The main business of the company

is to sell industrial supplies after sourcing its inventory from countries such as Vietnam,

China and Thailand. The report has generated an analysis of the expenditure cycle of the

company. The findings of this evaluation have revealed that the company follows a

centralised accounting system. However, in the purchase system the ARC, APC and the PC

completely overlooks the process of checking the inventory in order to update accounts and

preparing receiving reports and forwarding the same to the cash disbursement department.

Additionally, the assigned clerks in the PD and AP department completely overlooks their

duties. A critical analysis has been able to identify is weaknesses and risks such as reputation

loss, financial loss and increased debt burden.

ACCOUNTING INFORMATION SYSTEMS

Executive Summary

The study relates to Perth-based wholesaler Adam & Co. The main business of the company

is to sell industrial supplies after sourcing its inventory from countries such as Vietnam,

China and Thailand. The report has generated an analysis of the expenditure cycle of the

company. The findings of this evaluation have revealed that the company follows a

centralised accounting system. However, in the purchase system the ARC, APC and the PC

completely overlooks the process of checking the inventory in order to update accounts and

preparing receiving reports and forwarding the same to the cash disbursement department.

Additionally, the assigned clerks in the PD and AP department completely overlooks their

duties. A critical analysis has been able to identify is weaknesses and risks such as reputation

loss, financial loss and increased debt burden.

2

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction................................................................................................................................3

System Flowchart of purchase systems......................................................................................4

Purchase system’s internal control weakness............................................................................5

Risk associated with Purchase system’s weakness....................................................................6

System Flowchart of cash disbursement system........................................................................7

Cash disbursement system’s internal control weakness.............................................................8

Risk associated with cash disbursement system’s weakness.....................................................8

System Flowchart of payroll system........................................................................................10

Payroll system’s internal control weakness.............................................................................11

Risk associated with payroll system’s weakness.....................................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction................................................................................................................................3

System Flowchart of purchase systems......................................................................................4

Purchase system’s internal control weakness............................................................................5

Risk associated with Purchase system’s weakness....................................................................6

System Flowchart of cash disbursement system........................................................................7

Cash disbursement system’s internal control weakness.............................................................8

Risk associated with cash disbursement system’s weakness.....................................................8

System Flowchart of payroll system........................................................................................10

Payroll system’s internal control weakness.............................................................................11

Risk associated with payroll system’s weakness.....................................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEMS

Introduction

The first section of the report reviews the existing literature of existing systems,

thereby putting emphasis on internal control and usefulness of conducting audits. In the

subsequent sections, the report has depicted the weakness in Adam & Co.’s internal control

and risks related to the identified weaknesses. According to DeFond and Lennox (2017),

internal control ensures that the financial statements of an entity are prepared as per the

relevant international standard. The study also illustrates how internal control can be stated as

the process brought by the entity’s board of director and other personnel for guaranteeing

achieving the desired objectives. Based on the several types of other research studies, it has

been discerned that only a handful of large private companies is mandated to conduct audits

(Vanstraelen and Schelleman 2017). However, this research has emphasized on the benefit of

voluntarily conducting audits in an organization. Furthermore, auditing has a pivotal role

towards the accuracy of the financial statement corporate accountability and governance

mechanism (Lisic et al. 2019). As stated by Knecheland Salterio (2016), more than 37%

firms in the US conduct audit on a voluntary basis. These entities were seen to have a

remarkably low loan default ratio compared to an audit firm. This study emphasizes on the

importance in auditing of the “payroll functions”, “purchase systems” and “disbursement

of cash” of Adam & Co. along with the risks in each process.

ACCOUNTING INFORMATION SYSTEMS

Introduction

The first section of the report reviews the existing literature of existing systems,

thereby putting emphasis on internal control and usefulness of conducting audits. In the

subsequent sections, the report has depicted the weakness in Adam & Co.’s internal control

and risks related to the identified weaknesses. According to DeFond and Lennox (2017),

internal control ensures that the financial statements of an entity are prepared as per the

relevant international standard. The study also illustrates how internal control can be stated as

the process brought by the entity’s board of director and other personnel for guaranteeing

achieving the desired objectives. Based on the several types of other research studies, it has

been discerned that only a handful of large private companies is mandated to conduct audits

(Vanstraelen and Schelleman 2017). However, this research has emphasized on the benefit of

voluntarily conducting audits in an organization. Furthermore, auditing has a pivotal role

towards the accuracy of the financial statement corporate accountability and governance

mechanism (Lisic et al. 2019). As stated by Knecheland Salterio (2016), more than 37%

firms in the US conduct audit on a voluntary basis. These entities were seen to have a

remarkably low loan default ratio compared to an audit firm. This study emphasizes on the

importance in auditing of the “payroll functions”, “purchase systems” and “disbursement

of cash” of Adam & Co. along with the risks in each process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

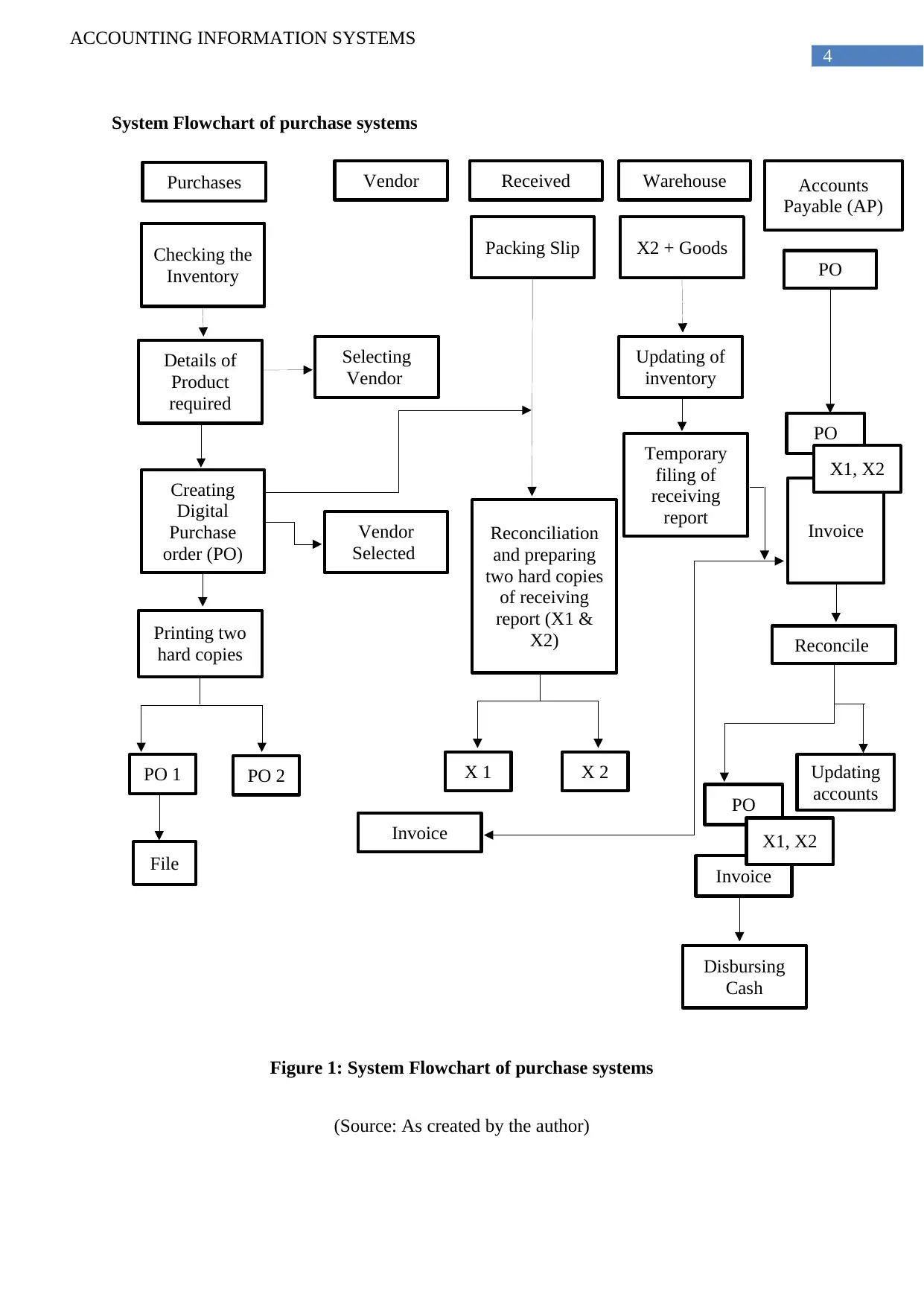

ACCOUNTING INFORMATION SYSTEMS

Purchases Vendor Received Warehouse Accounts

Payable (AP)

Checking the

Inventory

Details of

Product

required

Creating

Digital

Purchase

order (PO)

Printing two

hard copies

PO 1 PO 2

File

Selecting

Vendor

Packing Slip

Vendor

Selected

Reconciliation

and preparing

two hard copies

of receiving

report (X1 &

X2)

X 1 X 2

X2 + Goods

Updating of

inventory

Temporary

filing of

receiving

report

Invoice

Invoice

PO

PO

X1, X2

Reconcile

PO

Invoice

X1, X2

Disbursing

Cash

Updating

accounts

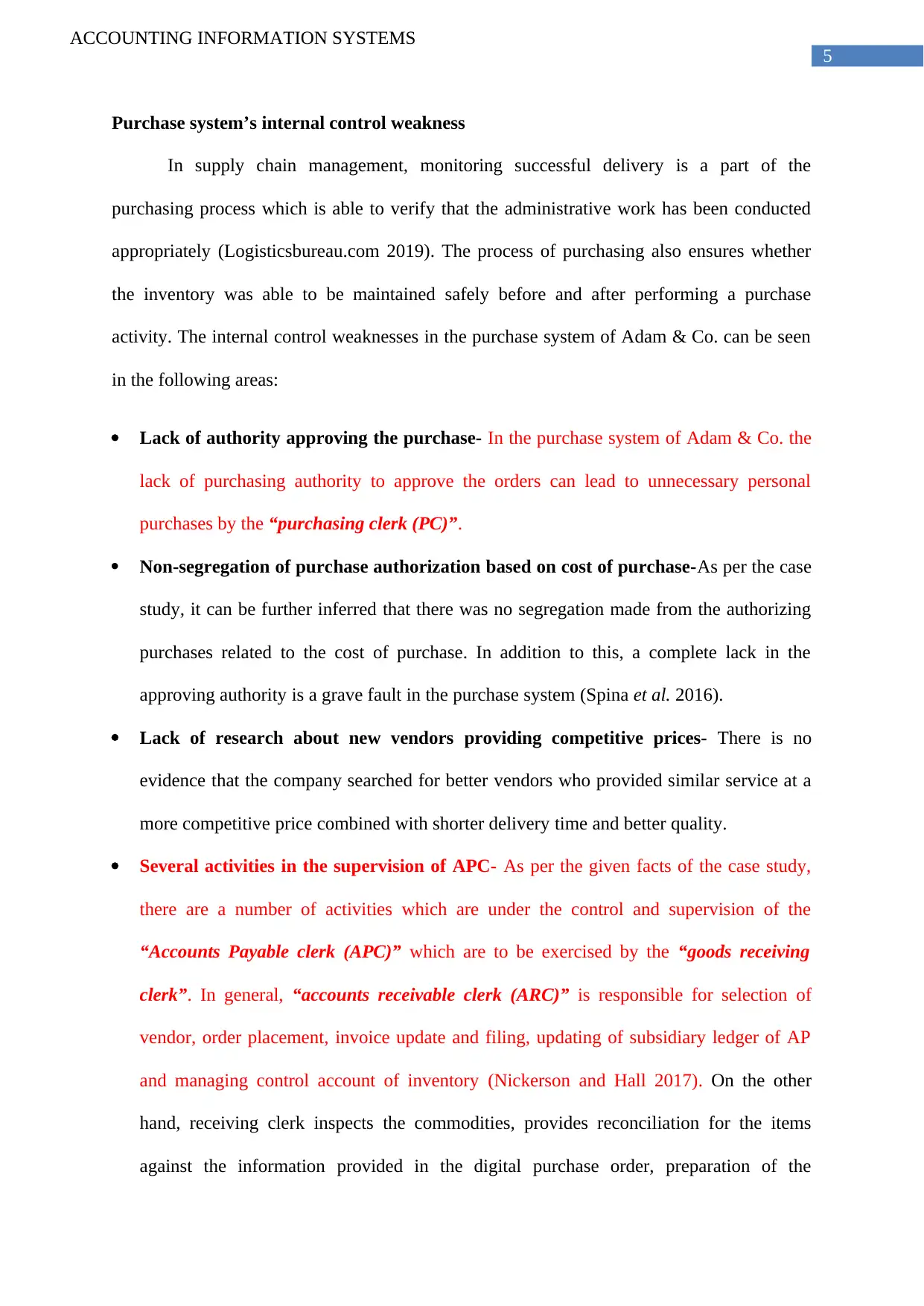

System Flowchart of purchase systems

Figure 1: System Flowchart of purchase systems

(Source: As created by the author)

ACCOUNTING INFORMATION SYSTEMS

Purchases Vendor Received Warehouse Accounts

Payable (AP)

Checking the

Inventory

Details of

Product

required

Creating

Digital

Purchase

order (PO)

Printing two

hard copies

PO 1 PO 2

File

Selecting

Vendor

Packing Slip

Vendor

Selected

Reconciliation

and preparing

two hard copies

of receiving

report (X1 &

X2)

X 1 X 2

X2 + Goods

Updating of

inventory

Temporary

filing of

receiving

report

Invoice

Invoice

PO

PO

X1, X2

Reconcile

PO

Invoice

X1, X2

Disbursing

Cash

Updating

accounts

System Flowchart of purchase systems

Figure 1: System Flowchart of purchase systems

(Source: As created by the author)

5

ACCOUNTING INFORMATION SYSTEMS

Purchase system’s internal control weakness

In supply chain management, monitoring successful delivery is a part of the

purchasing process which is able to verify that the administrative work has been conducted

appropriately (Logisticsbureau.com 2019). The process of purchasing also ensures whether

the inventory was able to be maintained safely before and after performing a purchase

activity. The internal control weaknesses in the purchase system of Adam & Co. can be seen

in the following areas:

Lack of authority approving the purchase- In the purchase system of Adam & Co. the

lack of purchasing authority to approve the orders can lead to unnecessary personal

purchases by the “purchasing clerk (PC)”.

Non-segregation of purchase authorization based on cost of purchase-As per the case

study, it can be further inferred that there was no segregation made from the authorizing

purchases related to the cost of purchase. In addition to this, a complete lack in the

approving authority is a grave fault in the purchase system (Spina et al. 2016).

Lack of research about new vendors providing competitive prices- There is no

evidence that the company searched for better vendors who provided similar service at a

more competitive price combined with shorter delivery time and better quality.

Several activities in the supervision of APC- As per the given facts of the case study,

there are a number of activities which are under the control and supervision of the

“Accounts Payable clerk (APC)” which are to be exercised by the “goods receiving

clerk”. In general, “accounts receivable clerk (ARC)” is responsible for selection of

vendor, order placement, invoice update and filing, updating of subsidiary ledger of AP

and managing control account of inventory (Nickerson and Hall 2017). On the other

hand, receiving clerk inspects the commodities, provides reconciliation for the items

against the information provided in the digital purchase order, preparation of the

ACCOUNTING INFORMATION SYSTEMS

Purchase system’s internal control weakness

In supply chain management, monitoring successful delivery is a part of the

purchasing process which is able to verify that the administrative work has been conducted

appropriately (Logisticsbureau.com 2019). The process of purchasing also ensures whether

the inventory was able to be maintained safely before and after performing a purchase

activity. The internal control weaknesses in the purchase system of Adam & Co. can be seen

in the following areas:

Lack of authority approving the purchase- In the purchase system of Adam & Co. the

lack of purchasing authority to approve the orders can lead to unnecessary personal

purchases by the “purchasing clerk (PC)”.

Non-segregation of purchase authorization based on cost of purchase-As per the case

study, it can be further inferred that there was no segregation made from the authorizing

purchases related to the cost of purchase. In addition to this, a complete lack in the

approving authority is a grave fault in the purchase system (Spina et al. 2016).

Lack of research about new vendors providing competitive prices- There is no

evidence that the company searched for better vendors who provided similar service at a

more competitive price combined with shorter delivery time and better quality.

Several activities in the supervision of APC- As per the given facts of the case study,

there are a number of activities which are under the control and supervision of the

“Accounts Payable clerk (APC)” which are to be exercised by the “goods receiving

clerk”. In general, “accounts receivable clerk (ARC)” is responsible for selection of

vendor, order placement, invoice update and filing, updating of subsidiary ledger of AP

and managing control account of inventory (Nickerson and Hall 2017). On the other

hand, receiving clerk inspects the commodities, provides reconciliation for the items

against the information provided in the digital purchase order, preparation of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING INFORMATION SYSTEMS

receiving reports, packing slip and updating subsidiary ledgers of inventory (Recruiting

Resources 2016). However, at Adam & co. an APC performs similar duties like an ARC.

Risk associated with Purchase system’s weakness

Risk of financial theft - The purchase system provides complete authority to the ARC

for approving the orders. As there is no segregation of purchase authorization based on

cost of purchase ARC may misuse this power for ordering commodities for personal use

or even carry out a theft by faking purchasing of a product. Such a weakness in the

purchase system poses the risk of financial theft driven by excessive and improper

allocation of cost (Holmes 2018).

Favoritism or collusion brought by lack of research about new vendors- As the

company does not make any initiative to find more information about vendors providing a

competitive price, it may lead to collusion or favoritism from the supplier pertaining to

continuous orders.

Risk of approving poor quality product- The organization clearly lacks specialized

personnel for approving the quality of the commodities received. It is also worth

mentioning that a copy of the receiving report is collected by the APC who further files

the report in the department. This has a lot of scope for fraud at each step being carried

out by either clerk. It can further lead to approving the poor quality or quantity of

products provided by the vendor in return for gifts or bribes. There clearly needs to be a

segregation of duties for reviewing the purchase process (Zepeda, Nyaga and Young

2016).

ACCOUNTING INFORMATION SYSTEMS

receiving reports, packing slip and updating subsidiary ledgers of inventory (Recruiting

Resources 2016). However, at Adam & co. an APC performs similar duties like an ARC.

Risk associated with Purchase system’s weakness

Risk of financial theft - The purchase system provides complete authority to the ARC

for approving the orders. As there is no segregation of purchase authorization based on

cost of purchase ARC may misuse this power for ordering commodities for personal use

or even carry out a theft by faking purchasing of a product. Such a weakness in the

purchase system poses the risk of financial theft driven by excessive and improper

allocation of cost (Holmes 2018).

Favoritism or collusion brought by lack of research about new vendors- As the

company does not make any initiative to find more information about vendors providing a

competitive price, it may lead to collusion or favoritism from the supplier pertaining to

continuous orders.

Risk of approving poor quality product- The organization clearly lacks specialized

personnel for approving the quality of the commodities received. It is also worth

mentioning that a copy of the receiving report is collected by the APC who further files

the report in the department. This has a lot of scope for fraud at each step being carried

out by either clerk. It can further lead to approving the poor quality or quantity of

products provided by the vendor in return for gifts or bribes. There clearly needs to be a

segregation of duties for reviewing the purchase process (Zepeda, Nyaga and Young

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEMS

Accounts

Receivable

Disbursement of

Cash Treasurer Vendor

PO

X1, X2

Invoice

Completed the

filing as per

clearance date

Preparing the

cheque

Update accounts

Due Date

Signature

ChequeCopy

PO

X1, X2

Invoice

Copy

Close File

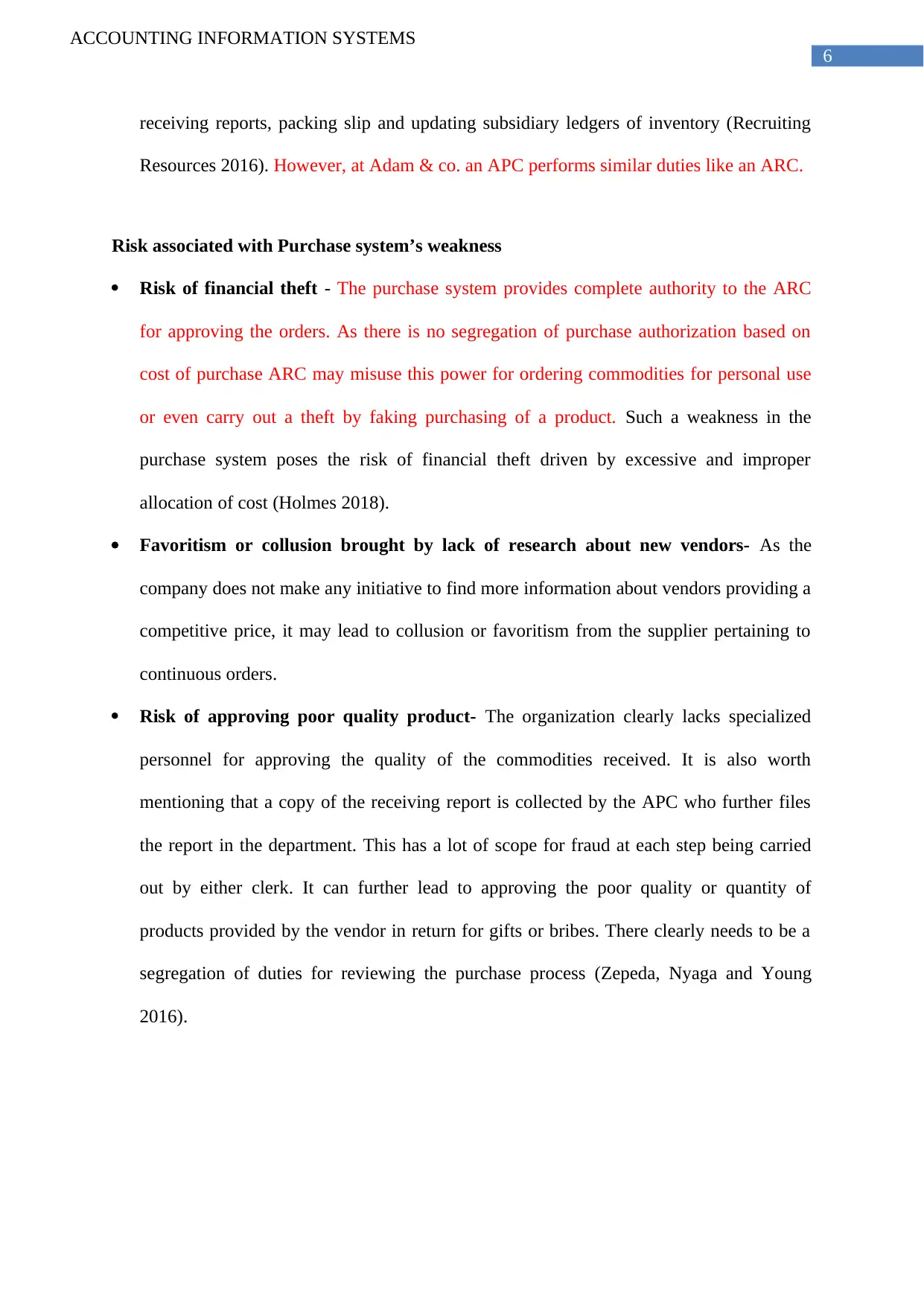

System Flowchart of cash disbursement system

Figure 2: System Flowchart of cash disbursement system

(Source: As created by the author)

ACCOUNTING INFORMATION SYSTEMS

Accounts

Receivable

Disbursement of

Cash Treasurer Vendor

PO

X1, X2

Invoice

Completed the

filing as per

clearance date

Preparing the

cheque

Update accounts

Due Date

Signature

ChequeCopy

PO

X1, X2

Invoice

Copy

Close File

System Flowchart of cash disbursement system

Figure 2: System Flowchart of cash disbursement system

(Source: As created by the author)

8

ACCOUNTING INFORMATION SYSTEMS

Cash disbursement system’s internal control weakness

The cash disbursement procedure relates to process the cash and cash equivalents

pertaining to procurement operations. The importance of a “cash distribution system” allows

an organization to process the payments accurately in the AP department whenever it is due

(Ellis 2018). It is customary for the AP department to notify any corrections which are to be

made for properly maintaining the vendor accounts required for the disbursement of the cash.

The weakness in the cash disbursement procedure of Adam & co. has been discussed in the

subsequent sections.

Lack of written confirmation of the documents from AP department - The main issue

with this system is associated to the clerk not signing of the documents from the AP

department. Due to this, there is no accountability of the actions within the department.

Lack of counter checking and reviewing of the cheques- Based on the given facts of

the case study, the treasurer in Adam & Co. receives and prepares a check for signing

without being faced with any additional information in form of invoice, receiving report

or purchase order (Bemo et al. 2017).

Lack of personnel - The “cash disbursement clerk” has the excessive burden with duties

such as filing invoice, writing checks, maintaining AP subsidiary ledger and updating the

cheque register. There is a lack of personnel to handle such burgeoning pressure of work.

Risk associated with cash disbursement system’s weakness

Risk of error in reviewing documents-The “cash disbursement clerk” does not sign the

documents arriving from the AP. As the clerk cannot be held responsible, this may lead to

serious issues for the organization in the future with no trail to follow when reviewing the

documents in the department.

ACCOUNTING INFORMATION SYSTEMS

Cash disbursement system’s internal control weakness

The cash disbursement procedure relates to process the cash and cash equivalents

pertaining to procurement operations. The importance of a “cash distribution system” allows

an organization to process the payments accurately in the AP department whenever it is due

(Ellis 2018). It is customary for the AP department to notify any corrections which are to be

made for properly maintaining the vendor accounts required for the disbursement of the cash.

The weakness in the cash disbursement procedure of Adam & co. has been discussed in the

subsequent sections.

Lack of written confirmation of the documents from AP department - The main issue

with this system is associated to the clerk not signing of the documents from the AP

department. Due to this, there is no accountability of the actions within the department.

Lack of counter checking and reviewing of the cheques- Based on the given facts of

the case study, the treasurer in Adam & Co. receives and prepares a check for signing

without being faced with any additional information in form of invoice, receiving report

or purchase order (Bemo et al. 2017).

Lack of personnel - The “cash disbursement clerk” has the excessive burden with duties

such as filing invoice, writing checks, maintaining AP subsidiary ledger and updating the

cheque register. There is a lack of personnel to handle such burgeoning pressure of work.

Risk associated with cash disbursement system’s weakness

Risk of error in reviewing documents-The “cash disbursement clerk” does not sign the

documents arriving from the AP. As the clerk cannot be held responsible, this may lead to

serious issues for the organization in the future with no trail to follow when reviewing the

documents in the department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEMS

Risk of theft and financial loss - As the treasurer receives the cheques for signing

without any additional information, there is a possibility of theft in the Department. The

cash disbursement clerk can fill incorrect amount in cheques either deliberately or by

mistake steal money from the company resulted from collusion with the employees or

vendors of the company. In case the clerk fills incorrect amount lesser than the payable

amount, it may lead to strained relationship with the vendor. Moreover, Adam & Co.

may lose track of the errors as the clerk did not put his signature in the documents

received. In case the clerk fills a wrong amount by mistake which is higher than the

payable amount, it will lead to a financial loss for the company.

Risk of error caused by cash disbursement clerk- The cash disbursement clerk has to

perform lots of duties which may lead to higher scope of error. There is a possibility that

the clerk forgets to update the accounts, thereby making the financial accounts incorrect,

confusing and chaotic. Additionally, there is no provision to review the activities

associated to the “cash disbursement clerk”. This has provided the clerk with the

opportunity for carrying out fraudulent activities.

ACCOUNTING INFORMATION SYSTEMS

Risk of theft and financial loss - As the treasurer receives the cheques for signing

without any additional information, there is a possibility of theft in the Department. The

cash disbursement clerk can fill incorrect amount in cheques either deliberately or by

mistake steal money from the company resulted from collusion with the employees or

vendors of the company. In case the clerk fills incorrect amount lesser than the payable

amount, it may lead to strained relationship with the vendor. Moreover, Adam & Co.

may lose track of the errors as the clerk did not put his signature in the documents

received. In case the clerk fills a wrong amount by mistake which is higher than the

payable amount, it will lead to a financial loss for the company.

Risk of error caused by cash disbursement clerk- The cash disbursement clerk has to

perform lots of duties which may lead to higher scope of error. There is a possibility that

the clerk forgets to update the accounts, thereby making the financial accounts incorrect,

confusing and chaotic. Additionally, there is no provision to review the activities

associated to the “cash disbursement clerk”. This has provided the clerk with the

opportunity for carrying out fraudulent activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING INFORMATION SYSTEMS

Supervisors Payroll

Department (PD)

Accounts

payable (AP)

General

ledger (GL)

Time Cards Time Cards

Review Updating the

records

followed by

preparing the

pay checks

Pay cheques

Printing Payroll

register (two copies)

Y1 Y2

Time cards

Y1

File

Y2

Disbursement

voucher

Y2

Voucher

Imprest

account

cheque

Copy

File

Y2

Voucher

File

Time Cards

Pay cheques

Distribution

followed by

review

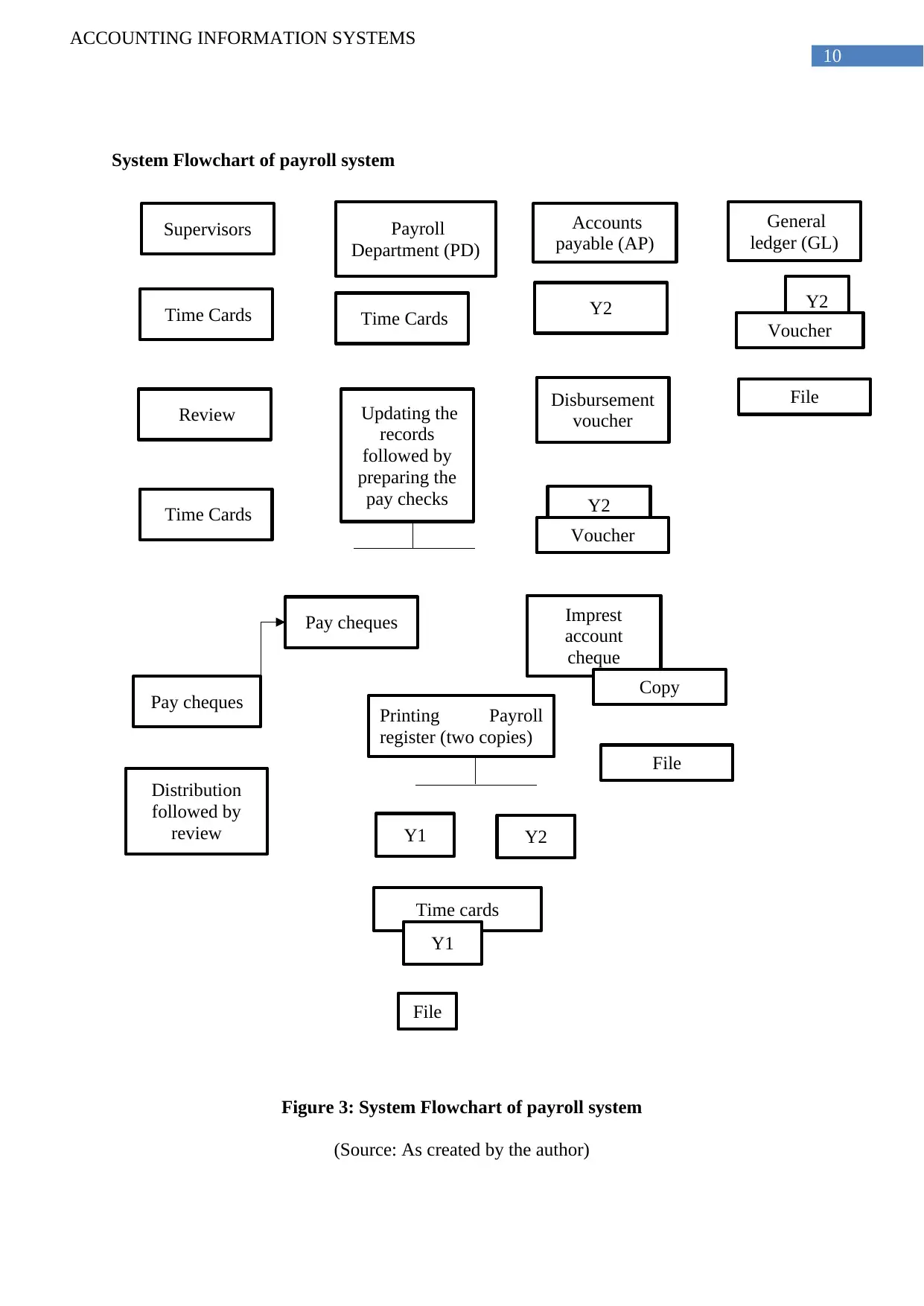

System Flowchart of payroll system

Figure 3: System Flowchart of payroll system

(Source: As created by the author)

ACCOUNTING INFORMATION SYSTEMS

Supervisors Payroll

Department (PD)

Accounts

payable (AP)

General

ledger (GL)

Time Cards Time Cards

Review Updating the

records

followed by

preparing the

pay checks

Pay cheques

Printing Payroll

register (two copies)

Y1 Y2

Time cards

Y1

File

Y2

Disbursement

voucher

Y2

Voucher

Imprest

account

cheque

Copy

File

Y2

Voucher

File

Time Cards

Pay cheques

Distribution

followed by

review

System Flowchart of payroll system

Figure 3: System Flowchart of payroll system

(Source: As created by the author)

11

ACCOUNTING INFORMATION SYSTEMS

Payroll system’s internal control weakness

A payroll system is maintained for keeping track of the work duration of the

employees, no. of days worked, leave balance, computing wages, completion of direct

deposits and withholding taxes. The main purpose of such a system is to keep track of

relevant activities by which employers pay an employee (Asif and Webb 2015).

Maintaining a manual timecard system- It is to be noted that Adam & Co. maintains a

manual timecard system where the employee’s record their work hours on a timecard.

The review of the timecard is performed manually by the supervisor and forwarded to the

respective payroll department during each week (Woo, Asiabase Technologies Ltd 2017).

Insufficient segregation of duties- The payroll clerk has to perform several duties

relating to data entry in the timecard to the central payroll system, taking printout of pay

cheques, taking a printout of two hard copies of the payroll register, posting of digital

employee records, forwarding cheques to the supervisor and filing of time cards.

Absence of payroll preview- The internal control lacks any system for previewing

payroll or “Human Resource Information Systems” where the data is processed for

checking the accuracy of total working hours, number of employees and leave balance of

an employee (Noe et al. 2017). This is a necessary initiative to be taken by the individual

departments for maintaining separate systems for payroll for better monitoring and

review.

Risk associated with payroll system’s weakness

Risk of overpaying the employees and increased tax burdens- As the employee

attendance is maintained in a manual timecard system, there is a high possibility that

ACCOUNTING INFORMATION SYSTEMS

Payroll system’s internal control weakness

A payroll system is maintained for keeping track of the work duration of the

employees, no. of days worked, leave balance, computing wages, completion of direct

deposits and withholding taxes. The main purpose of such a system is to keep track of

relevant activities by which employers pay an employee (Asif and Webb 2015).

Maintaining a manual timecard system- It is to be noted that Adam & Co. maintains a

manual timecard system where the employee’s record their work hours on a timecard.

The review of the timecard is performed manually by the supervisor and forwarded to the

respective payroll department during each week (Woo, Asiabase Technologies Ltd 2017).

Insufficient segregation of duties- The payroll clerk has to perform several duties

relating to data entry in the timecard to the central payroll system, taking printout of pay

cheques, taking a printout of two hard copies of the payroll register, posting of digital

employee records, forwarding cheques to the supervisor and filing of time cards.

Absence of payroll preview- The internal control lacks any system for previewing

payroll or “Human Resource Information Systems” where the data is processed for

checking the accuracy of total working hours, number of employees and leave balance of

an employee (Noe et al. 2017). This is a necessary initiative to be taken by the individual

departments for maintaining separate systems for payroll for better monitoring and

review.

Risk associated with payroll system’s weakness

Risk of overpaying the employees and increased tax burdens- As the employee

attendance is maintained in a manual timecard system, there is a high possibility that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.