HA2042 Accounting Information Systems Case Study: Adam & Co. Analysis

VerifiedAdded on 2022/11/07

|19

|2662

|434

Case Study

AI Summary

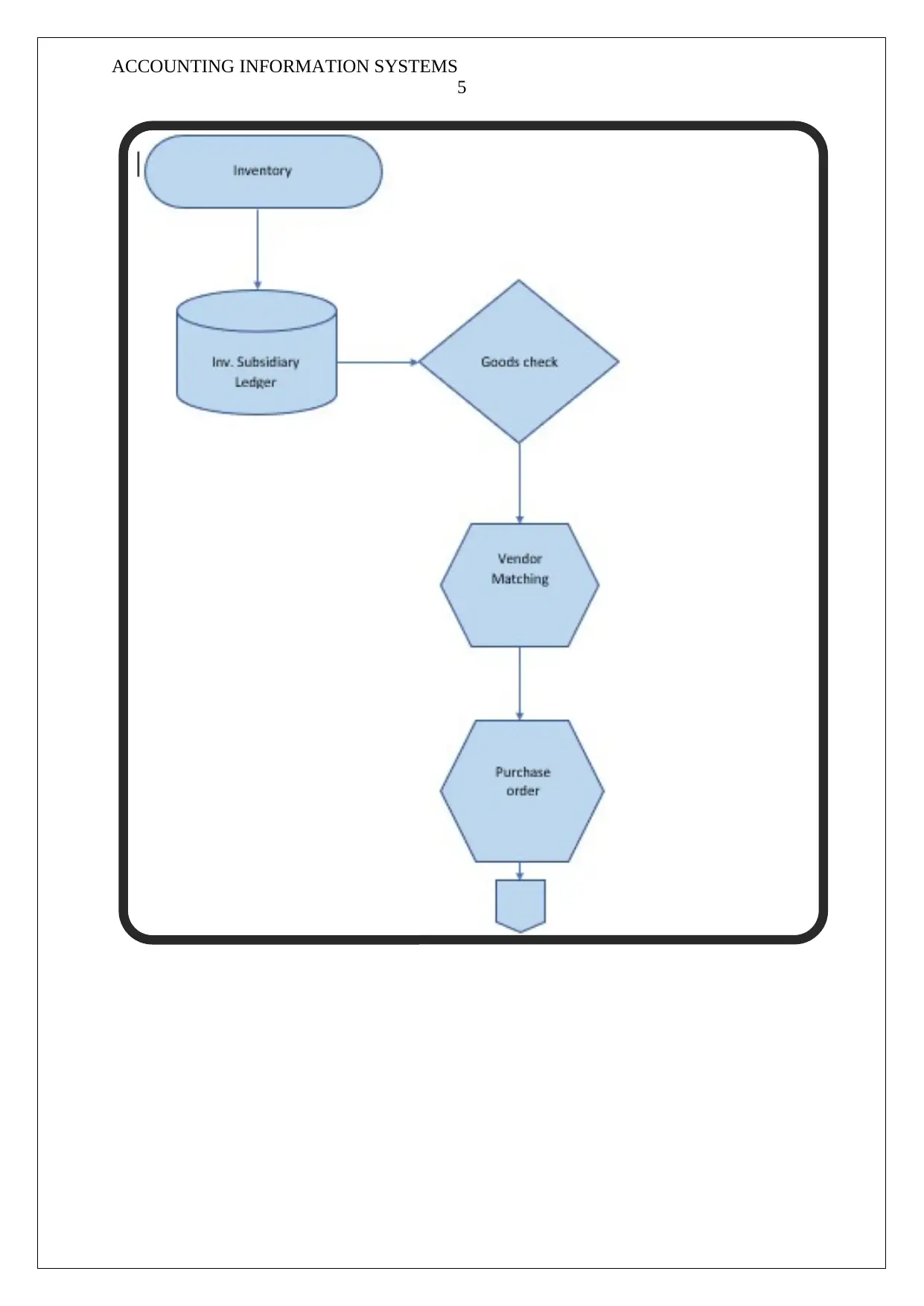

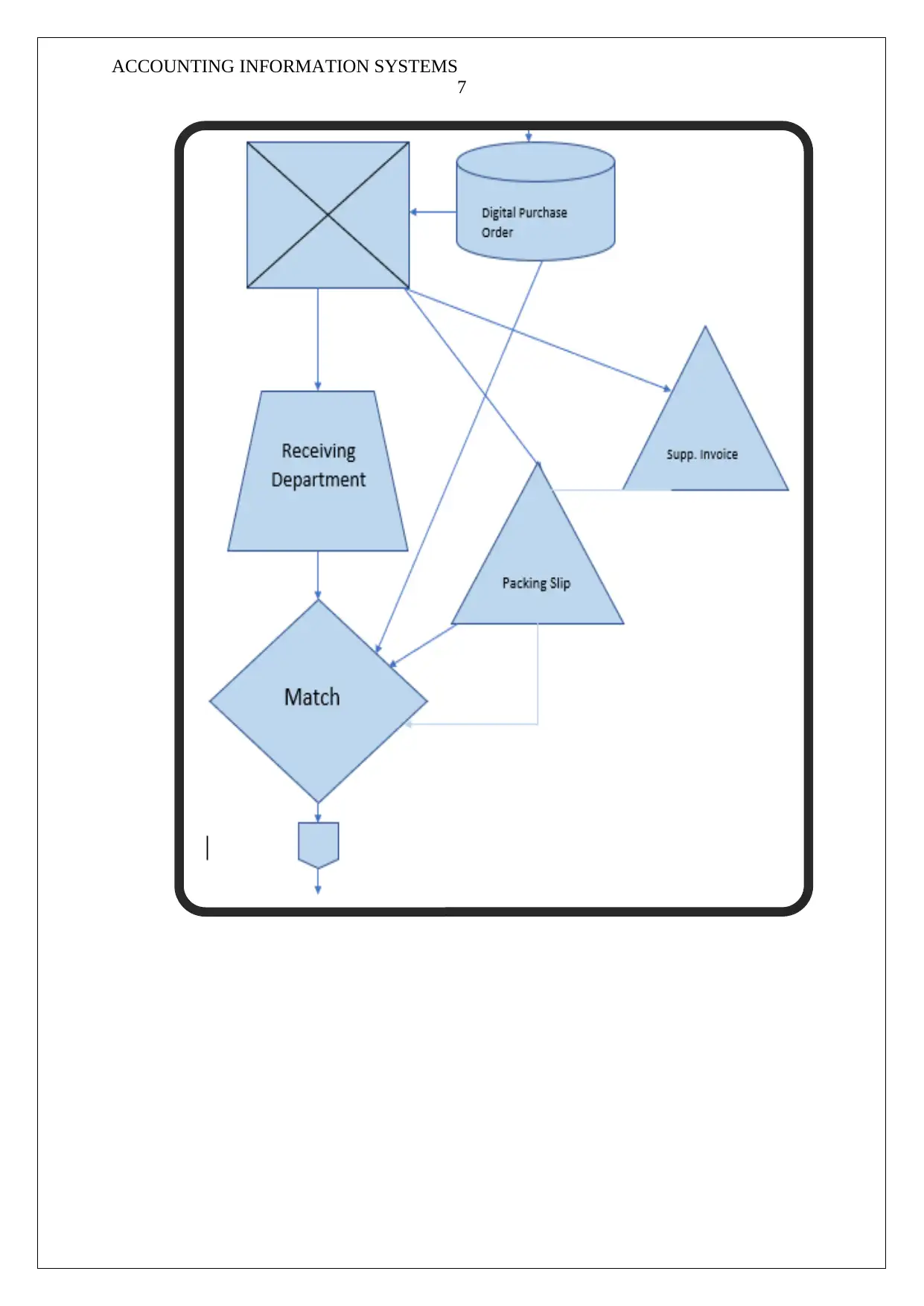

This case study examines the accounting information systems of Adam & Co., a wholesale supplier. The analysis focuses on three key systems: payroll, cash disbursements, and purchases. The study includes flowcharts illustrating the workflow within each system, from input to output. It also evaluates internal controls to identify potential weaknesses and proposes solutions to mitigate risks. The payroll system, cash disbursement system and purchases system are analysed in detail, including the inputs, processes, and outputs. The case study highlights the importance of a controlled accounting system and the need for cognitive presentation abilities for effective decision-making. The report also provides recommendations to improve the systems and enhance efficiency within the organization. The assignment provides a detailed overview of the accounting processes and internal controls within the company, highlighting potential weaknesses and suggesting improvements.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.