Accounting Information Systems

VerifiedAdded on 2023/03/21

|11

|1604

|82

AI Summary

This document discusses the existing acquisition and payment system in Oriental Traders and internal control weaknesses in Chipps' accounting information system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING INFORMATION SYSTEMS

Accounting Information Systems

Name of the Student:

Name of the University:

Authors Note:

Accounting Information Systems

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ACCOUNTING INFORMATION SYSTEMS

Contents

Part A:..............................................................................................................................................2

Part B:..............................................................................................................................................3

References:....................................................................................................................................10

ACCOUNTING INFORMATION SYSTEMS

Contents

Part A:..............................................................................................................................................2

Part B:..............................................................................................................................................3

References:....................................................................................................................................10

2

ACCOUNTING INFORMATION SYSTEMS

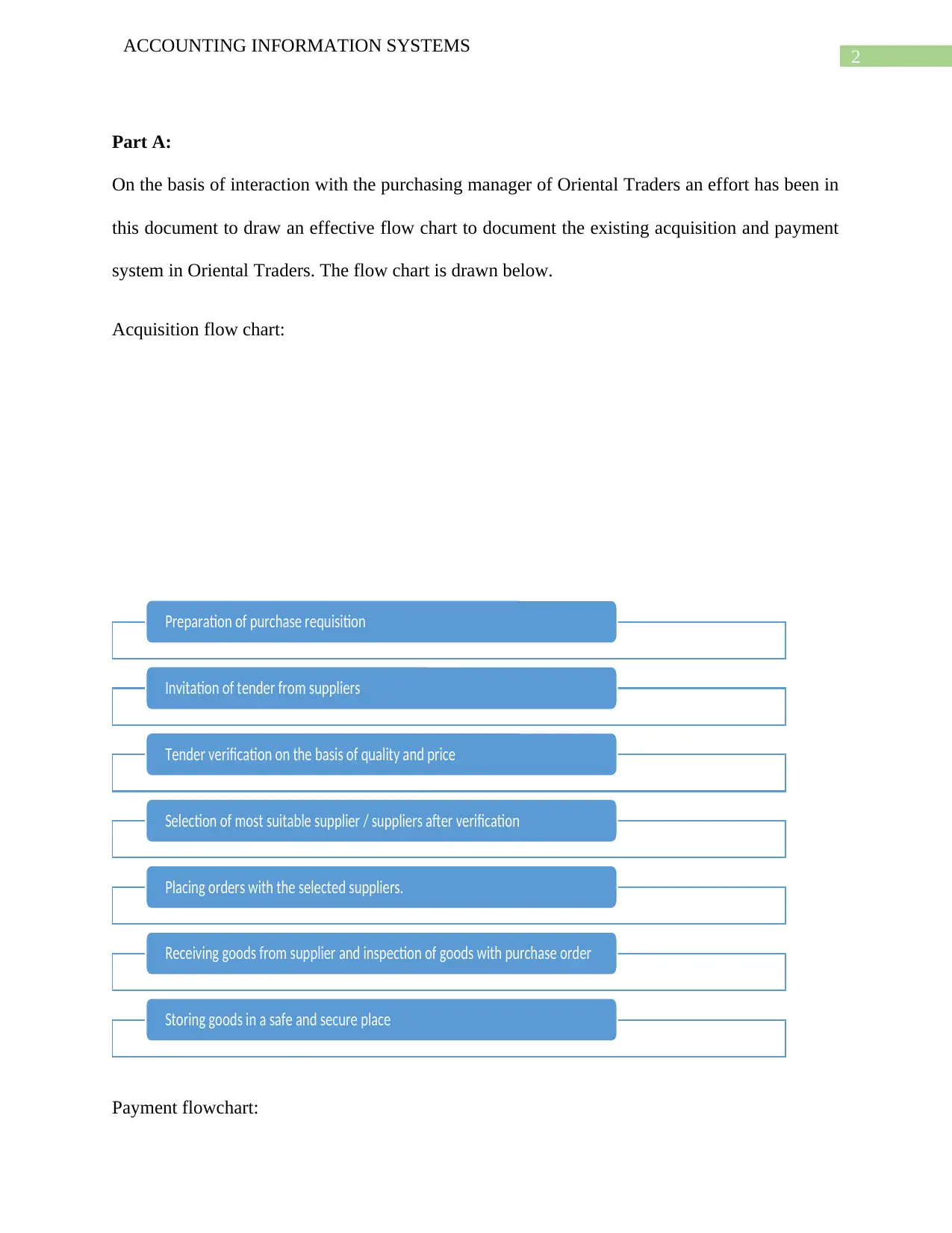

Part A:

On the basis of interaction with the purchasing manager of Oriental Traders an effort has been in

this document to draw an effective flow chart to document the existing acquisition and payment

system in Oriental Traders. The flow chart is drawn below.

Acquisition flow chart:

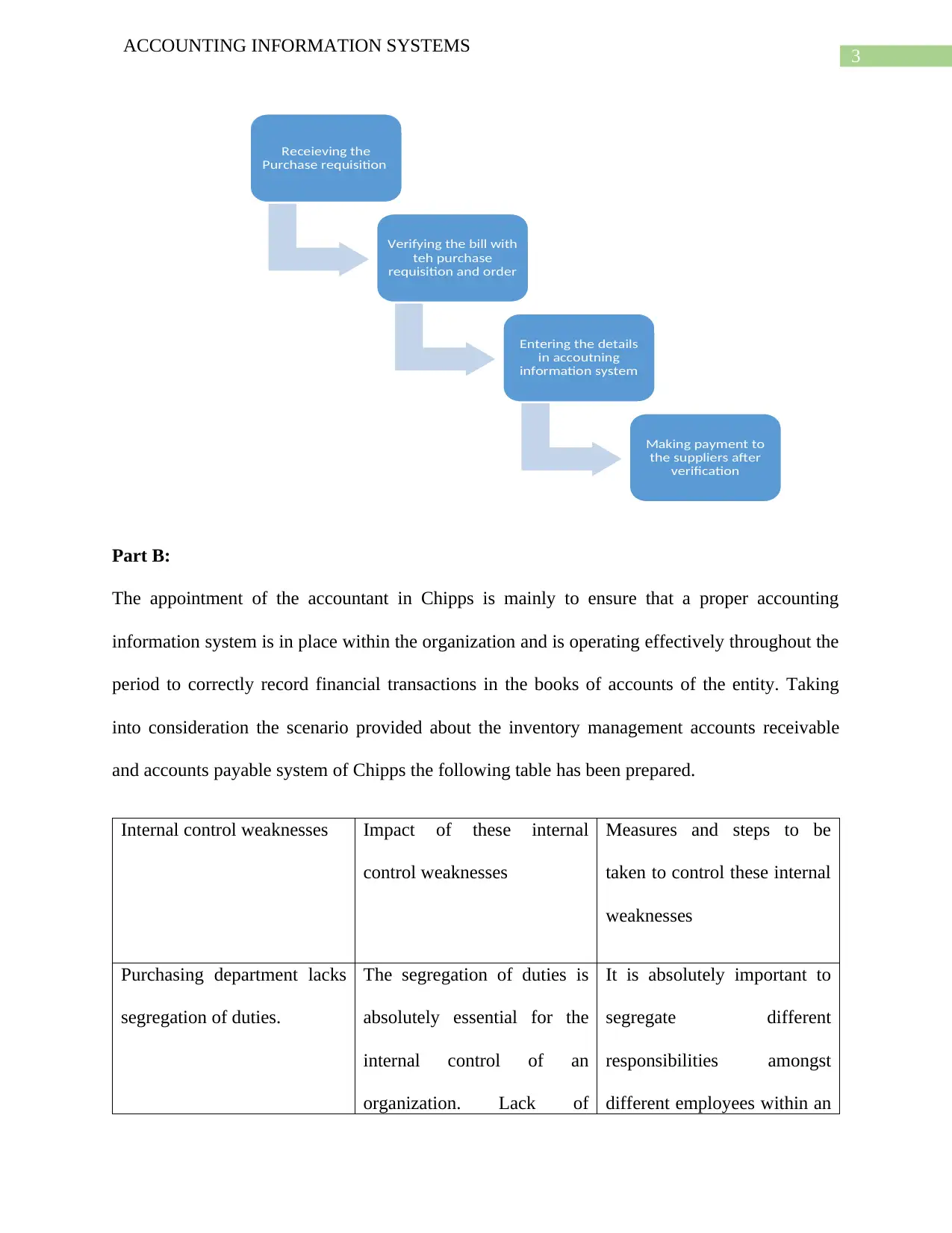

Payment flowchart:

Preparation of purchase requisition

Invitation of tender from suppliers

Tender verification on the basis of quality and price

Selection of most suitable supplier / suppliers after verification

Placing orders with the selected suppliers.

Receiving goods from supplier and inspection of goods with purchase order

Storing goods in a safe and secure place

ACCOUNTING INFORMATION SYSTEMS

Part A:

On the basis of interaction with the purchasing manager of Oriental Traders an effort has been in

this document to draw an effective flow chart to document the existing acquisition and payment

system in Oriental Traders. The flow chart is drawn below.

Acquisition flow chart:

Payment flowchart:

Preparation of purchase requisition

Invitation of tender from suppliers

Tender verification on the basis of quality and price

Selection of most suitable supplier / suppliers after verification

Placing orders with the selected suppliers.

Receiving goods from supplier and inspection of goods with purchase order

Storing goods in a safe and secure place

3

ACCOUNTING INFORMATION SYSTEMS

Part B:

The appointment of the accountant in Chipps is mainly to ensure that a proper accounting

information system is in place within the organization and is operating effectively throughout the

period to correctly record financial transactions in the books of accounts of the entity. Taking

into consideration the scenario provided about the inventory management accounts receivable

and accounts payable system of Chipps the following table has been prepared.

Internal control weaknesses Impact of these internal

control weaknesses

Measures and steps to be

taken to control these internal

weaknesses

Purchasing department lacks

segregation of duties.

The segregation of duties is

absolutely essential for the

internal control of an

organization. Lack of

It is absolutely important to

segregate different

responsibilities amongst

different employees within an

Receieving the

Purchase requisition

Verifying the bill with

teh purchase

requisition and order

Entering the details

in accoutning

information system

Making payment to

the suppliers after

verification

ACCOUNTING INFORMATION SYSTEMS

Part B:

The appointment of the accountant in Chipps is mainly to ensure that a proper accounting

information system is in place within the organization and is operating effectively throughout the

period to correctly record financial transactions in the books of accounts of the entity. Taking

into consideration the scenario provided about the inventory management accounts receivable

and accounts payable system of Chipps the following table has been prepared.

Internal control weaknesses Impact of these internal

control weaknesses

Measures and steps to be

taken to control these internal

weaknesses

Purchasing department lacks

segregation of duties.

The segregation of duties is

absolutely essential for the

internal control of an

organization. Lack of

It is absolutely important to

segregate different

responsibilities amongst

different employees within an

Receieving the

Purchase requisition

Verifying the bill with

teh purchase

requisition and order

Entering the details

in accoutning

information system

Making payment to

the suppliers after

verification

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ACCOUNTING INFORMATION SYSTEMS

segregation of responsibilities

results in overlapping of

different works. In case of

purchase department in

Chipps there are five clerks

who have been given the

responsibility of verification

of purchase requisitions

without fixing their specific

responsibilities. As a result

the no specific purchasing

clerk can be identified to fix

responsibilities in case there

is any mistake in verification

of purchase requisitions.

organization. Purchasing

clerks shall be given separate

responsibilities to ensure that

the verification of purchase

requisitions are properly

accounted for. Specific clerks

shall be given specific duties

to fix responsibilities in the

future in case of any mistake.

There is no standard

procedure in place to select

appropriate vendors to place

orders. The procurement

department has no standard

procedure to follow while

placing purchase orders with

As a result improper

procedure to select vendors to

purchase required goods the

quality and price of goods

both can be adversely

affected. The quality of goods

is very important for any

organization and thus, the

The procurement department

must follow the following

standard procedure to procure

required goods in the future.

Firstly, the management

should invite tenders from

suppliers and vendors.

ACCOUNTING INFORMATION SYSTEMS

segregation of responsibilities

results in overlapping of

different works. In case of

purchase department in

Chipps there are five clerks

who have been given the

responsibility of verification

of purchase requisitions

without fixing their specific

responsibilities. As a result

the no specific purchasing

clerk can be identified to fix

responsibilities in case there

is any mistake in verification

of purchase requisitions.

organization. Purchasing

clerks shall be given separate

responsibilities to ensure that

the verification of purchase

requisitions are properly

accounted for. Specific clerks

shall be given specific duties

to fix responsibilities in the

future in case of any mistake.

There is no standard

procedure in place to select

appropriate vendors to place

orders. The procurement

department has no standard

procedure to follow while

placing purchase orders with

As a result improper

procedure to select vendors to

purchase required goods the

quality and price of goods

both can be adversely

affected. The quality of goods

is very important for any

organization and thus, the

The procurement department

must follow the following

standard procedure to procure

required goods in the future.

Firstly, the management

should invite tenders from

suppliers and vendors.

5

ACCOUNTING INFORMATION SYSTEMS

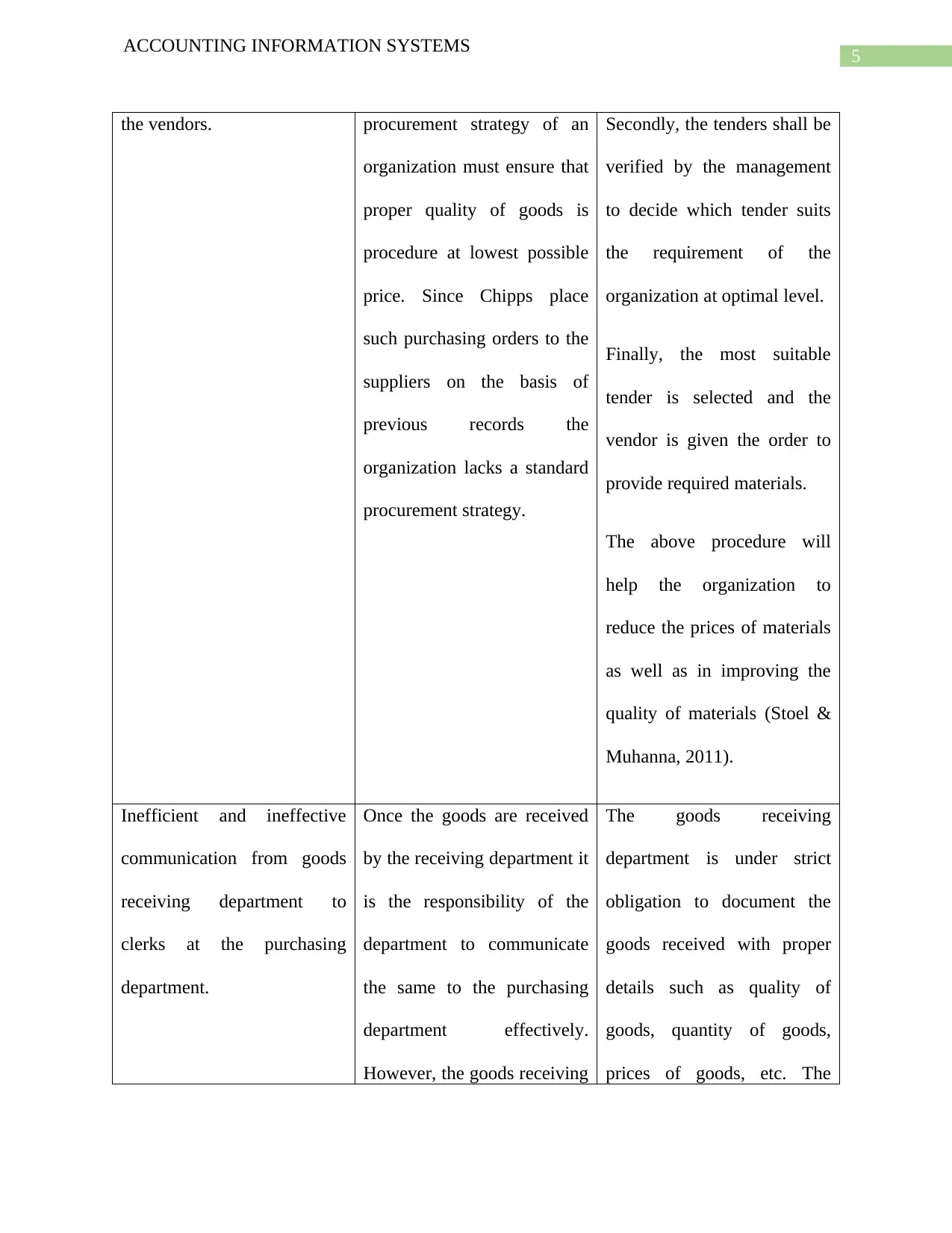

the vendors. procurement strategy of an

organization must ensure that

proper quality of goods is

procedure at lowest possible

price. Since Chipps place

such purchasing orders to the

suppliers on the basis of

previous records the

organization lacks a standard

procurement strategy.

Secondly, the tenders shall be

verified by the management

to decide which tender suits

the requirement of the

organization at optimal level.

Finally, the most suitable

tender is selected and the

vendor is given the order to

provide required materials.

The above procedure will

help the organization to

reduce the prices of materials

as well as in improving the

quality of materials (Stoel &

Muhanna, 2011).

Inefficient and ineffective

communication from goods

receiving department to

clerks at the purchasing

department.

Once the goods are received

by the receiving department it

is the responsibility of the

department to communicate

the same to the purchasing

department effectively.

However, the goods receiving

The goods receiving

department is under strict

obligation to document the

goods received with proper

details such as quality of

goods, quantity of goods,

prices of goods, etc. The

ACCOUNTING INFORMATION SYSTEMS

the vendors. procurement strategy of an

organization must ensure that

proper quality of goods is

procedure at lowest possible

price. Since Chipps place

such purchasing orders to the

suppliers on the basis of

previous records the

organization lacks a standard

procurement strategy.

Secondly, the tenders shall be

verified by the management

to decide which tender suits

the requirement of the

organization at optimal level.

Finally, the most suitable

tender is selected and the

vendor is given the order to

provide required materials.

The above procedure will

help the organization to

reduce the prices of materials

as well as in improving the

quality of materials (Stoel &

Muhanna, 2011).

Inefficient and ineffective

communication from goods

receiving department to

clerks at the purchasing

department.

Once the goods are received

by the receiving department it

is the responsibility of the

department to communicate

the same to the purchasing

department effectively.

However, the goods receiving

The goods receiving

department is under strict

obligation to document the

goods received with proper

details such as quality of

goods, quantity of goods,

prices of goods, etc. The

6

ACCOUNTING INFORMATION SYSTEMS

department verbally

communicates the matter of

goods receipt to the clerks in

purchasing department. As a

result there could be serious

mistake in verification and

inspection of actual goods

received and goods orders.

same written document shall

be copied and forwarded to

the purchasing clerks to

ensure there is proper

communication between the

receiving and purchasing

department. The verification

and inspection of goods

received shall be effectively

done only if the

communication between

different departments within

an organization regarding

then materials procedure is

effective and efficient.

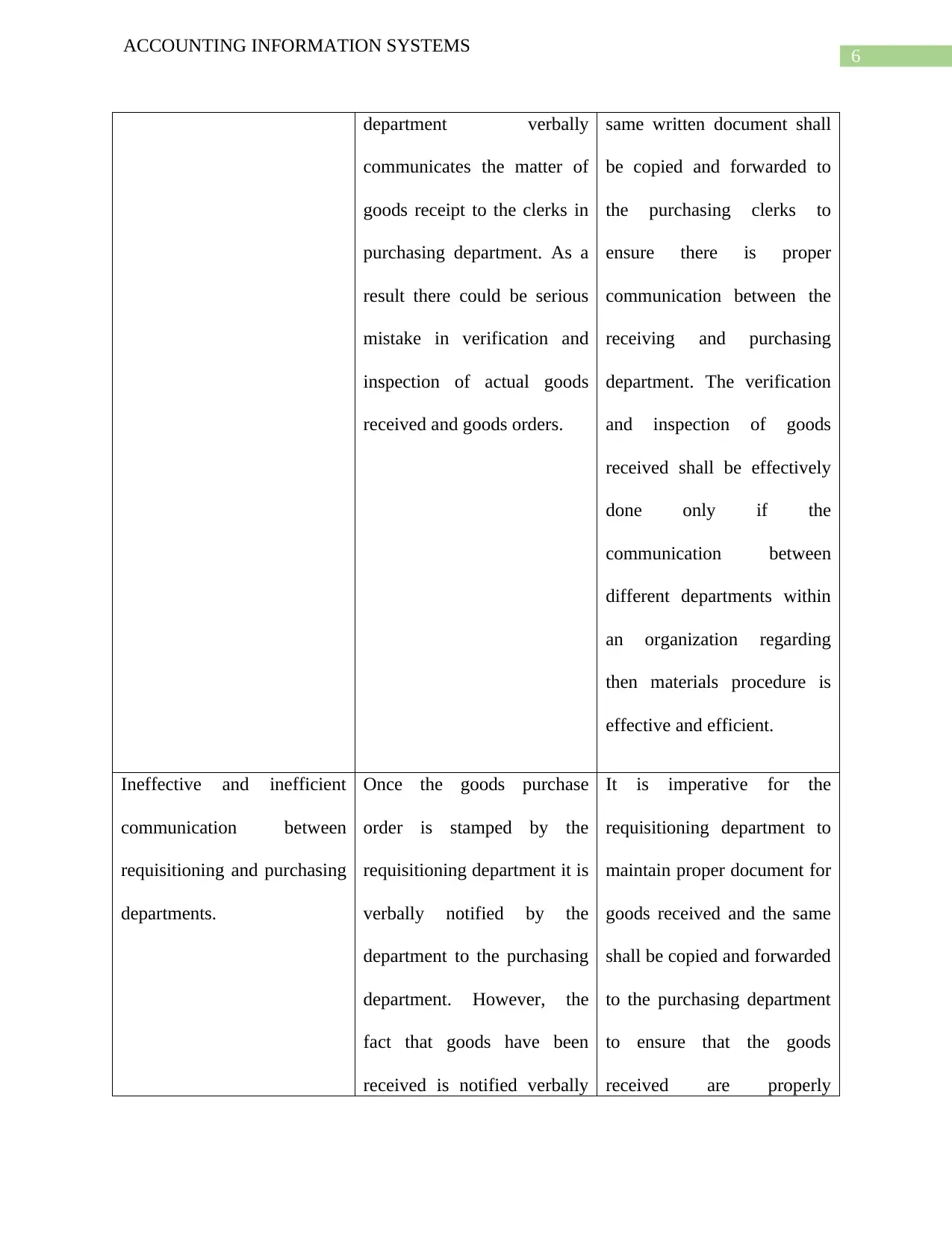

Ineffective and inefficient

communication between

requisitioning and purchasing

departments.

Once the goods purchase

order is stamped by the

requisitioning department it is

verbally notified by the

department to the purchasing

department. However, the

fact that goods have been

received is notified verbally

It is imperative for the

requisitioning department to

maintain proper document for

goods received and the same

shall be copied and forwarded

to the purchasing department

to ensure that the goods

received are properly

ACCOUNTING INFORMATION SYSTEMS

department verbally

communicates the matter of

goods receipt to the clerks in

purchasing department. As a

result there could be serious

mistake in verification and

inspection of actual goods

received and goods orders.

same written document shall

be copied and forwarded to

the purchasing clerks to

ensure there is proper

communication between the

receiving and purchasing

department. The verification

and inspection of goods

received shall be effectively

done only if the

communication between

different departments within

an organization regarding

then materials procedure is

effective and efficient.

Ineffective and inefficient

communication between

requisitioning and purchasing

departments.

Once the goods purchase

order is stamped by the

requisitioning department it is

verbally notified by the

department to the purchasing

department. However, the

fact that goods have been

received is notified verbally

It is imperative for the

requisitioning department to

maintain proper document for

goods received and the same

shall be copied and forwarded

to the purchasing department

to ensure that the goods

received are properly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEMS

can create number of serious

issues including lack of

details about the quality of

goods received, the quantity

of goods received will not be

property verified by the

purchasing department.

inspected and verified. Thus,

written communication is

must between requisitioning

and purchasing department to

ensure there is no weakness

in the internal control system

(Eutsler, Nickell & Robb,

2016).

Improper and unsafe way to

keep purchase orders by the

accounts payable clerk.

The accounts payable clerk

subsequent to the receipt of

POs keep these in open desks.

This could create serious

problems for the organization

as firstly, these can be

misplaced and lost and then

there is also possibility of

making improper and

unauthorized changes to these

POs to inflate or deflate the

amount recorded in these

orders for the narrow benefits

of different stakeholders at

the expense of the

The purchase orders must be

stored in a safe and secure

place, preferably in a locker

to reduce the risk of

misplacement, lost and

unauthorized changes in these

orders. The account payable

clerks should also record the

information in accounting

systems as soon as possible

once the POs are received.

ACCOUNTING INFORMATION SYSTEMS

can create number of serious

issues including lack of

details about the quality of

goods received, the quantity

of goods received will not be

property verified by the

purchasing department.

inspected and verified. Thus,

written communication is

must between requisitioning

and purchasing department to

ensure there is no weakness

in the internal control system

(Eutsler, Nickell & Robb,

2016).

Improper and unsafe way to

keep purchase orders by the

accounts payable clerk.

The accounts payable clerk

subsequent to the receipt of

POs keep these in open desks.

This could create serious

problems for the organization

as firstly, these can be

misplaced and lost and then

there is also possibility of

making improper and

unauthorized changes to these

POs to inflate or deflate the

amount recorded in these

orders for the narrow benefits

of different stakeholders at

the expense of the

The purchase orders must be

stored in a safe and secure

place, preferably in a locker

to reduce the risk of

misplacement, lost and

unauthorized changes in these

orders. The account payable

clerks should also record the

information in accounting

systems as soon as possible

once the POs are received.

8

ACCOUNTING INFORMATION SYSTEMS

organization.

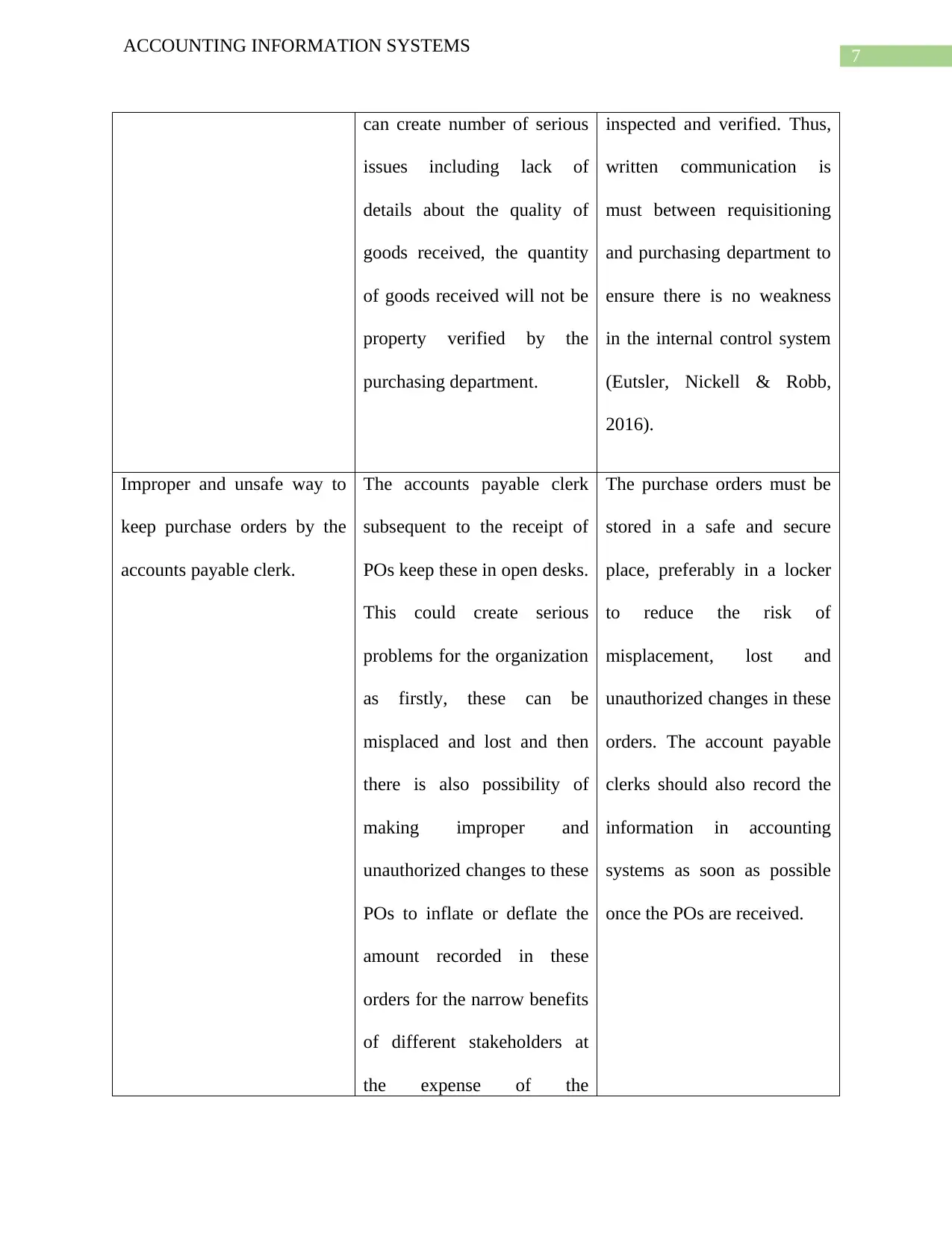

Verification of vendor

invoices by accounts payable

clerk.

Verification of vendor

invoices by accounts payable

clerk increases the risk of

manipulation in the account

payables ledger as the person

is responsible for the

recording entries in the

accounts payable ledger.

A different person shall be

responsible for verification of

invoices of vendors and not

the accounts payable clerk.

Segregation of cheques with

$5000 and above $5000 for

manual and automatic

signatures`.

It is absolutely improper to

segregate the cheques on the

basis of amount that too

under and above $5000. It is

better to ensure all cheques

are manually signed by the

signatory authority as there is

huge risk in using cheque

signature machine as the

person responsible to

maintain such machine will

have the opportunity to fraud

the organization.

Cheques shall be signed

manually in order to avoid the

risk of fraud.

ACCOUNTING INFORMATION SYSTEMS

organization.

Verification of vendor

invoices by accounts payable

clerk.

Verification of vendor

invoices by accounts payable

clerk increases the risk of

manipulation in the account

payables ledger as the person

is responsible for the

recording entries in the

accounts payable ledger.

A different person shall be

responsible for verification of

invoices of vendors and not

the accounts payable clerk.

Segregation of cheques with

$5000 and above $5000 for

manual and automatic

signatures`.

It is absolutely improper to

segregate the cheques on the

basis of amount that too

under and above $5000. It is

better to ensure all cheques

are manually signed by the

signatory authority as there is

huge risk in using cheque

signature machine as the

person responsible to

maintain such machine will

have the opportunity to fraud

the organization.

Cheques shall be signed

manually in order to avoid the

risk of fraud.

9

ACCOUNTING INFORMATION SYSTEMS

Cashier should not be given

any other responsibilities

apart from handling cash

however, the cashier of

Chipps is responsible to

maintain the cheque key

signature machine.

A cashier is responsible to

disburse cash and receive

cash. He shall not be allowed

to handle cheque signature

machine as this will create

conflict of interests. In this

case the confliction of interest

with the cashier maintaining

the cheque signature machine

key is quite apparent in

Chipps.

The cashier shall be given the

responsibilities of handling

cash only. Neither he should

be allowed to maintain

accounting records nor shall

he given the responsibility to

maintain the key of cheque

signature machine (Norman,

Rose & Rose, 2010).

It is important to note here that the above table has been prepared after considering the

information about the inventory and accounts payable management of Chipps as provided in the

documented. Thus, there could be number of others internal control weaknesses within the

organization in other facets of the organization but since no other information has been provided

about the internal operations of Chipps hence, it is not possible to comment on other facets of

organizational operation.

ACCOUNTING INFORMATION SYSTEMS

Cashier should not be given

any other responsibilities

apart from handling cash

however, the cashier of

Chipps is responsible to

maintain the cheque key

signature machine.

A cashier is responsible to

disburse cash and receive

cash. He shall not be allowed

to handle cheque signature

machine as this will create

conflict of interests. In this

case the confliction of interest

with the cashier maintaining

the cheque signature machine

key is quite apparent in

Chipps.

The cashier shall be given the

responsibilities of handling

cash only. Neither he should

be allowed to maintain

accounting records nor shall

he given the responsibility to

maintain the key of cheque

signature machine (Norman,

Rose & Rose, 2010).

It is important to note here that the above table has been prepared after considering the

information about the inventory and accounts payable management of Chipps as provided in the

documented. Thus, there could be number of others internal control weaknesses within the

organization in other facets of the organization but since no other information has been provided

about the internal operations of Chipps hence, it is not possible to comment on other facets of

organizational operation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ACCOUNTING INFORMATION SYSTEMS

References:

Eutsler, J., Nickell, E., & Robb, S. (2016). Fraud Risk Awareness and the Likelihood of Audit

Enforcement Action. Accounting Horizons, 30(3), 379-392. doi: 10.2308/acch-51490

Norman, C., Rose, A., & Rose, J. (2010). Internal audit reporting lines, fraud risk decomposition,

and assessments of fraud risk. Accounting, Organizations And Society, 35(5), 546-557. doi:

10.1016/j.aos.2009.12.003

Stoel, M., & Muhanna, W. (2011). IT internal control weaknesses and firm performance: An

organizational liability lens. International Journal Of Accounting Information

Systems, 12(4), 280-304. doi: 10.1016/j.accinf.2011.06.001

ACCOUNTING INFORMATION SYSTEMS

References:

Eutsler, J., Nickell, E., & Robb, S. (2016). Fraud Risk Awareness and the Likelihood of Audit

Enforcement Action. Accounting Horizons, 30(3), 379-392. doi: 10.2308/acch-51490

Norman, C., Rose, A., & Rose, J. (2010). Internal audit reporting lines, fraud risk decomposition,

and assessments of fraud risk. Accounting, Organizations And Society, 35(5), 546-557. doi:

10.1016/j.aos.2009.12.003

Stoel, M., & Muhanna, W. (2011). IT internal control weaknesses and firm performance: An

organizational liability lens. International Journal Of Accounting Information

Systems, 12(4), 280-304. doi: 10.1016/j.accinf.2011.06.001

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.