Accounting Integrated Reporting: Financial Statement Analysis Report

VerifiedAdded on 2021/12/23

|14

|2476

|22

Report

AI Summary

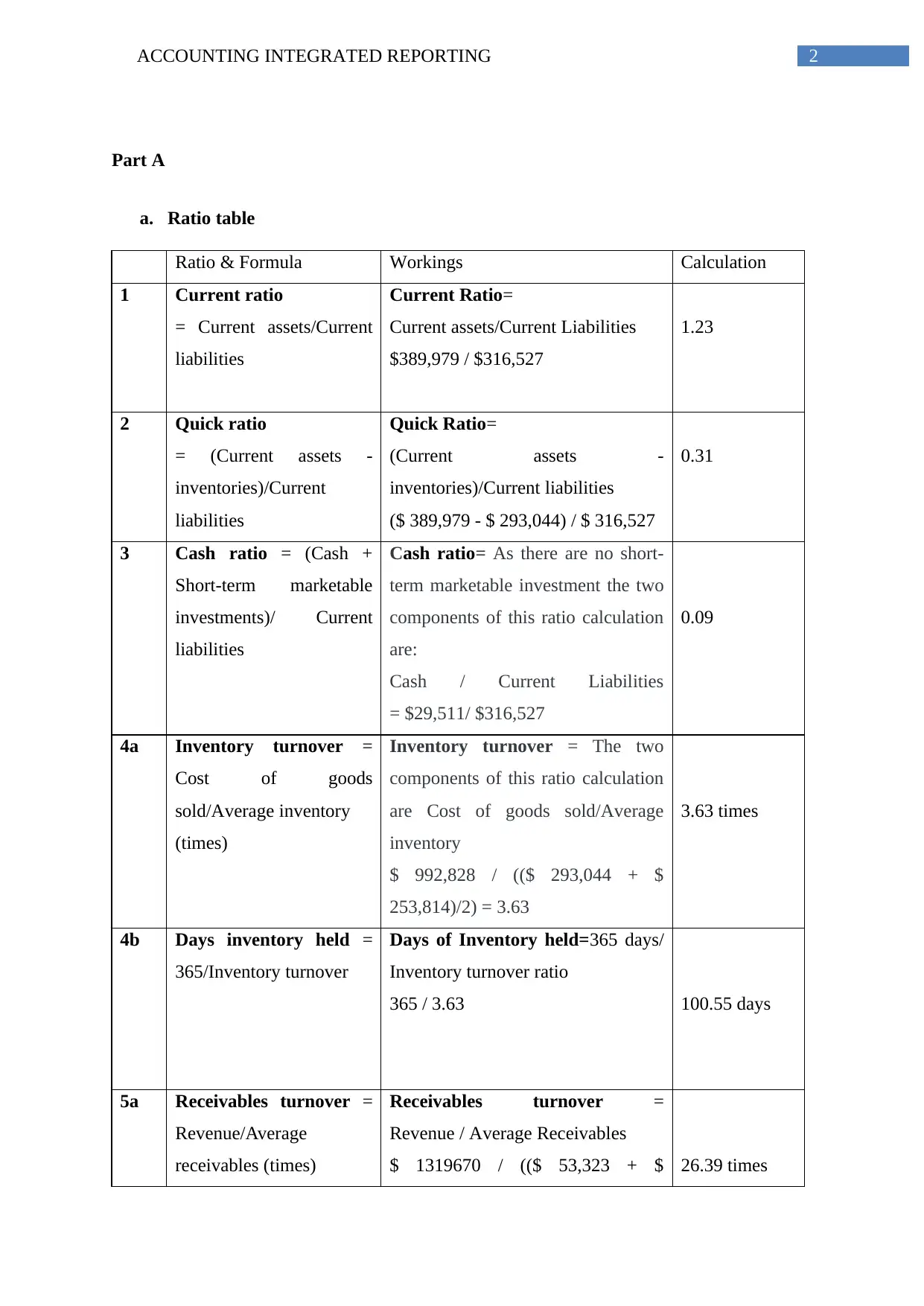

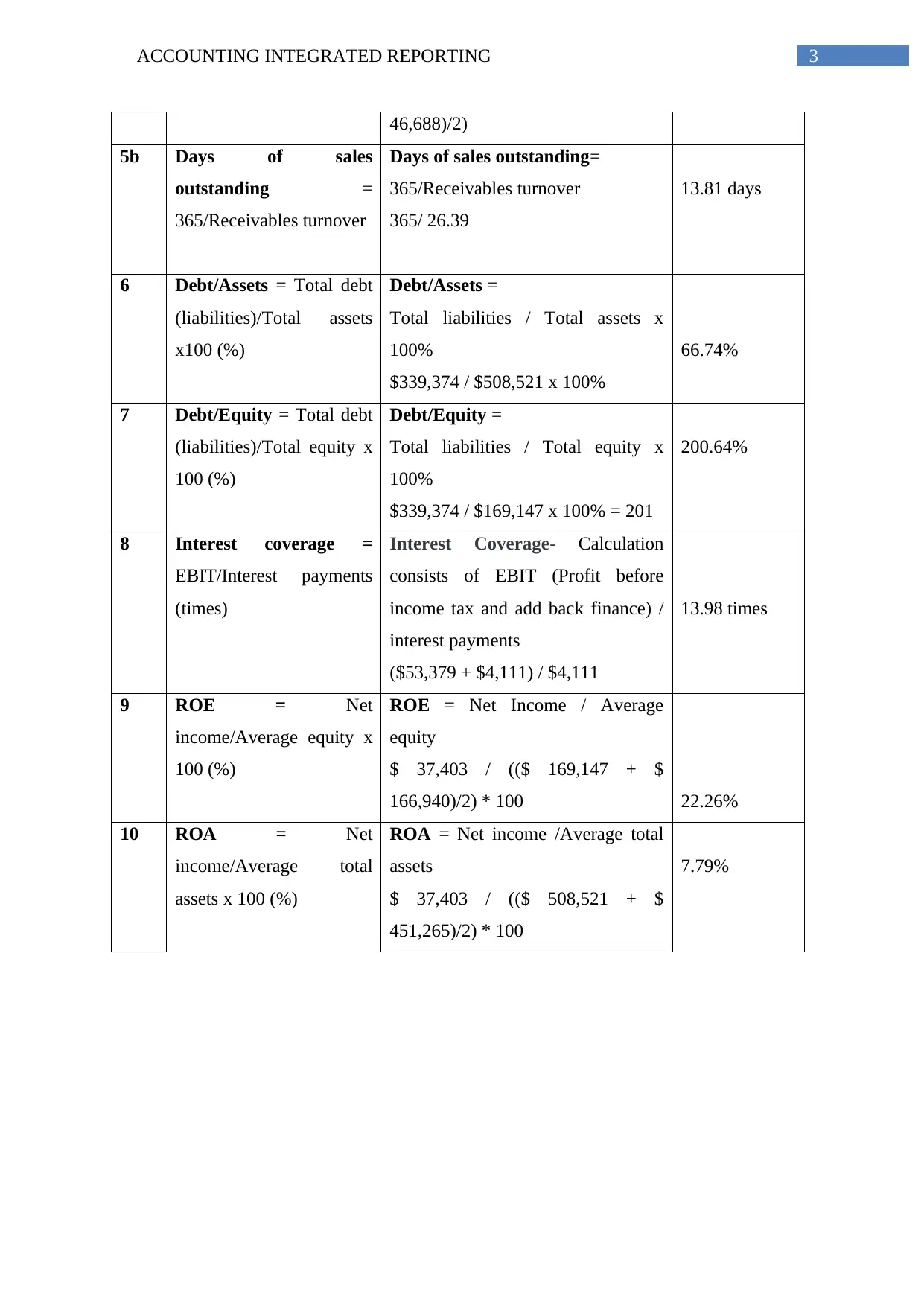

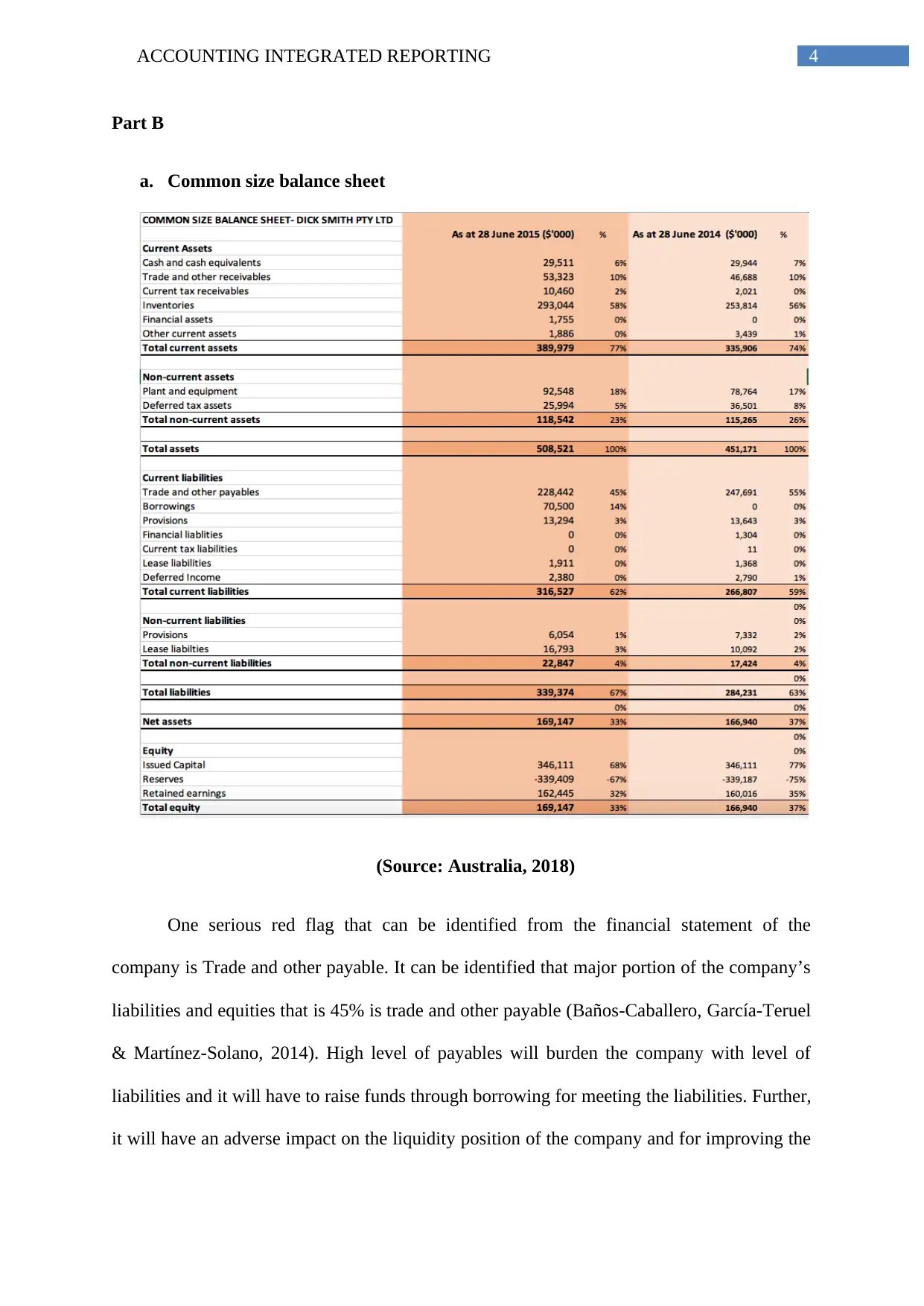

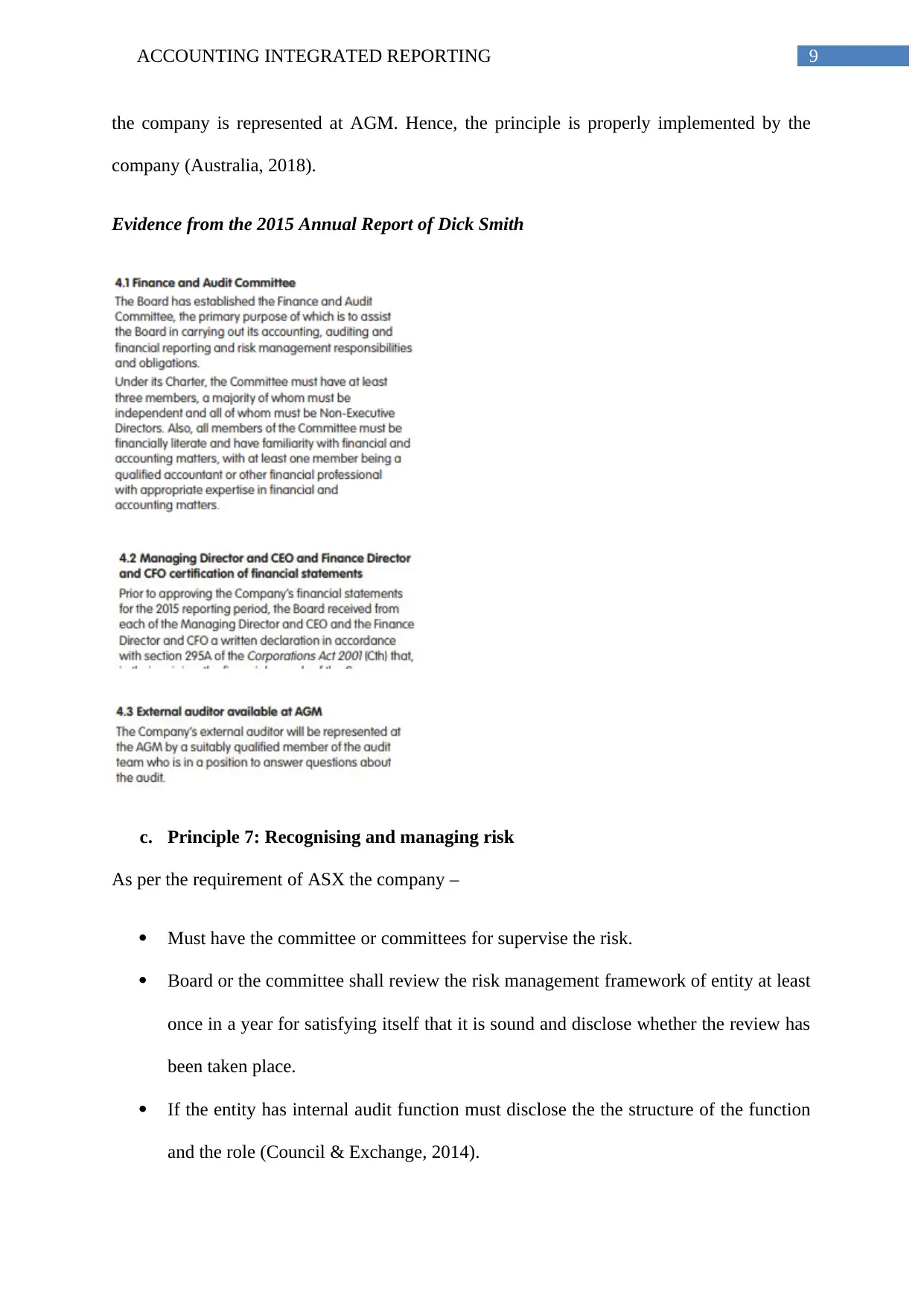

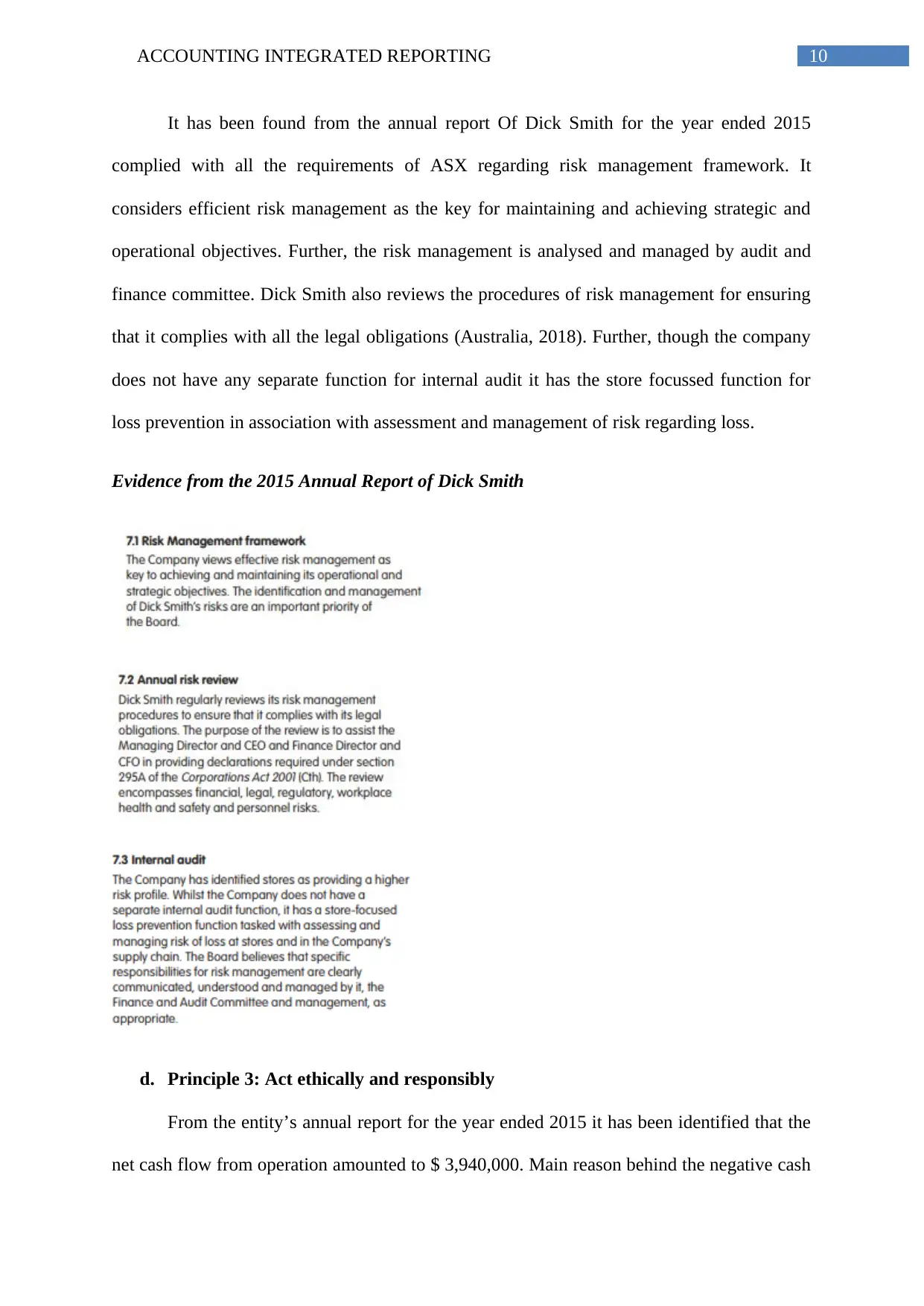

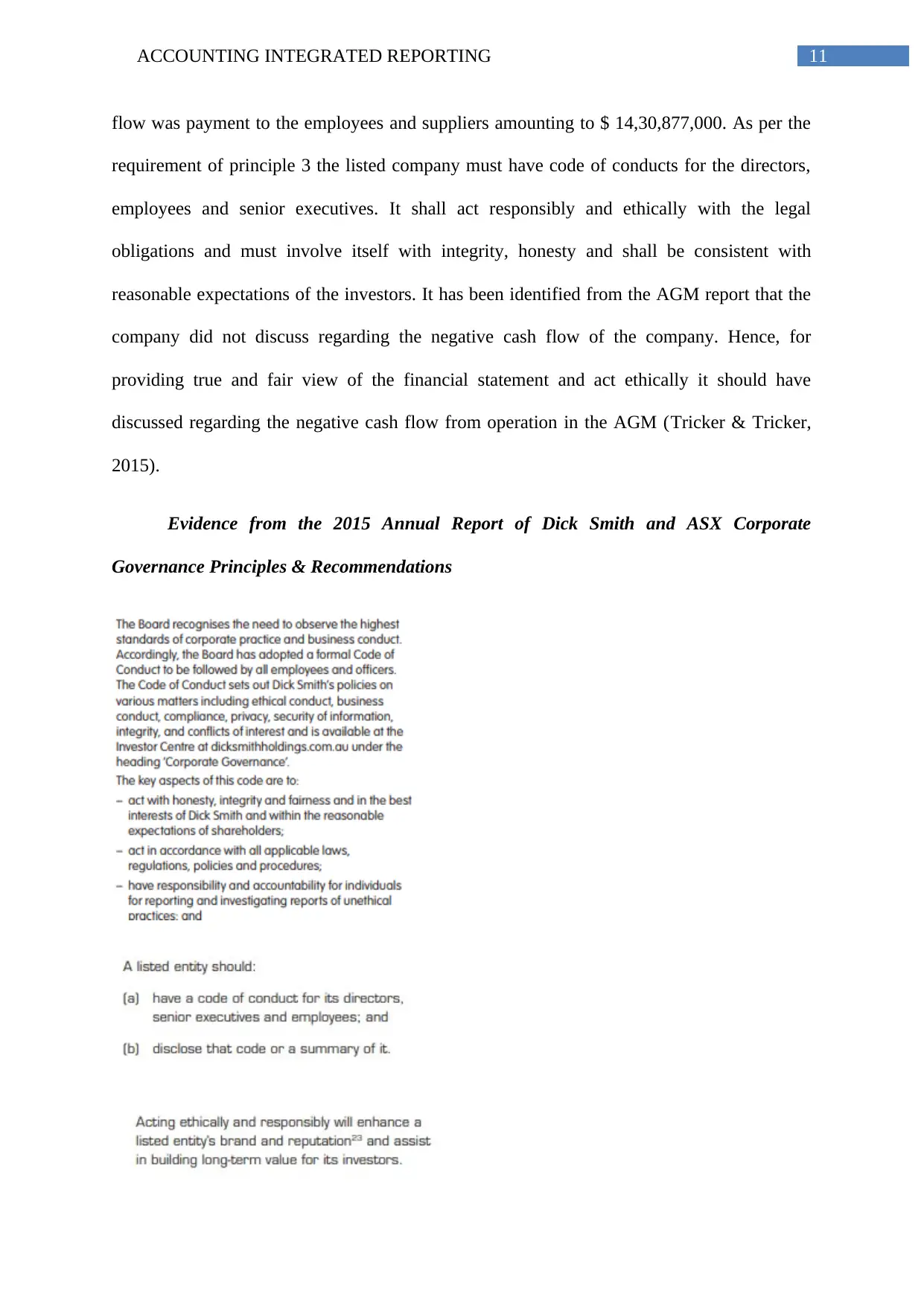

This report provides a comprehensive analysis of accounting integrated reporting, encompassing financial statement analysis, ratio calculations, and corporate governance principles. Part A presents a detailed ratio table, calculating key financial ratios such as current ratio, quick ratio, cash ratio, inventory turnover, receivables turnover, debt-to-asset ratio, debt-to-equity ratio, interest coverage, ROE, and ROA. Part B focuses on the common-size balance sheet and consolidated statement of cash flows, identifying potential financial red flags and warning signs. Part C delves into the application of corporate governance principles, specifically examining the structure of the board for adding value (Principle 2), safeguarding integrity in corporate reporting (Principle 4), recognizing and managing risk (Principle 7), and acting ethically and responsibly (Principle 3). The analysis utilizes the 2015 annual report of Dick Smith as a case study, evaluating the company's compliance with ASX guidelines and identifying areas for improvement. The report incorporates a skeptical view, highlighting potential shortcomings in the company's disclosures and practices. References are included to support the analysis.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.