Accounting Spreadsheet Solutions: Financial Analysis & Reporting

VerifiedAdded on 2023/06/13

|15

|3456

|477

Homework Assignment

AI Summary

This assignment provides various accounting spreadsheet solutions covering topics such as financial reporting, inventory management using FIFO and LIFO methods, bank reconciliation, and bad debt estimation. It includes examples of normal and formula views for different financial statements, illustrating how spreadsheets can be used for accounting functions. The assignment also discusses the advantages and disadvantages of using spreadsheets in accounting, highlighting their role in performing calculations and managing financial data. Journal entries, bank reconciliation statements, and comparative analyses of inventory costing methods are also presented, offering a comprehensive overview of spreadsheet applications in accounting and financial analysis.

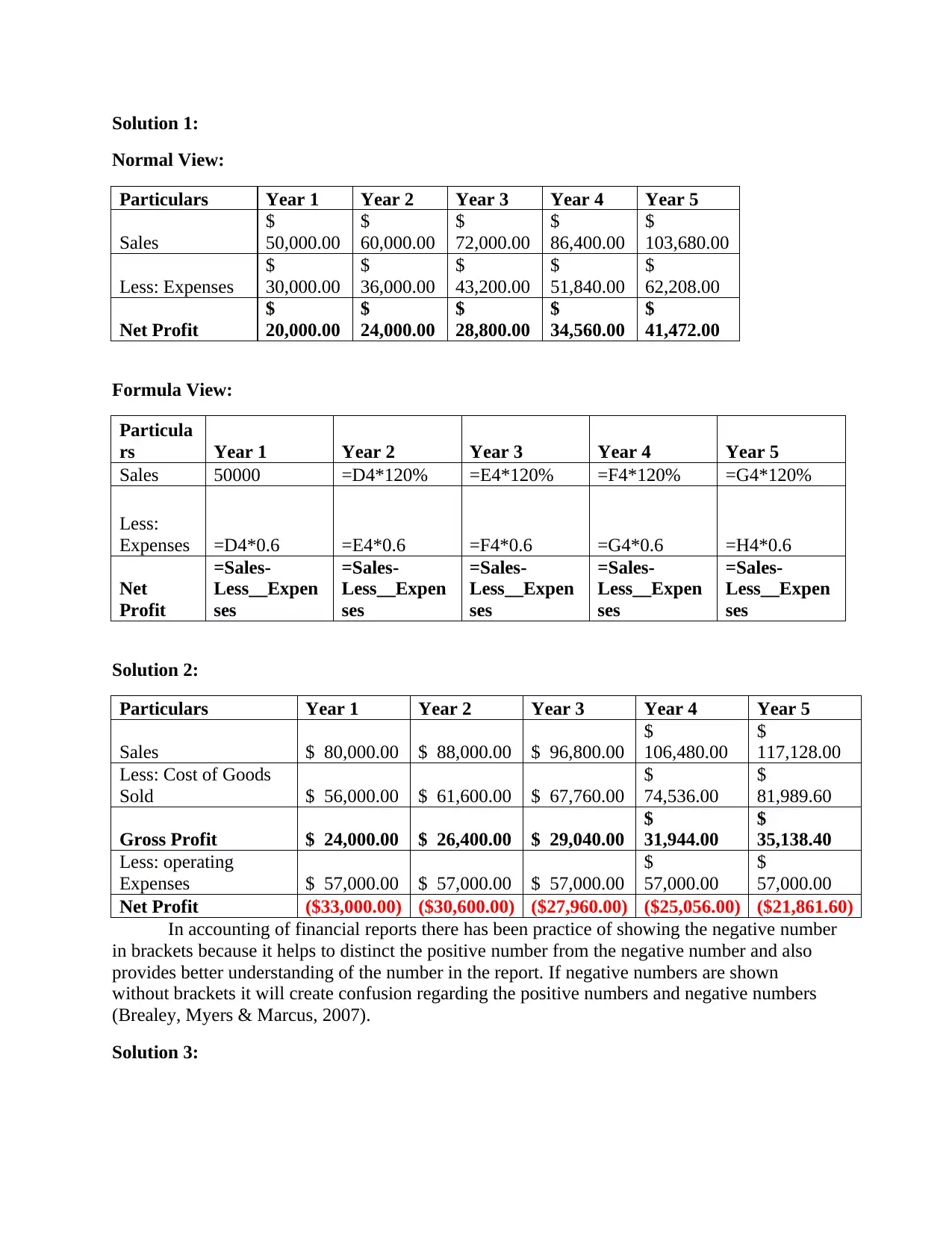

Solution 1:

Normal View:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Sales

$

50,000.00

$

60,000.00

$

72,000.00

$

86,400.00

$

103,680.00

Less: Expenses

$

30,000.00

$

36,000.00

$

43,200.00

$

51,840.00

$

62,208.00

Net Profit

$

20,000.00

$

24,000.00

$

28,800.00

$

34,560.00

$

41,472.00

Formula View:

Particula

rs Year 1 Year 2 Year 3 Year 4 Year 5

Sales 50000 =D4*120% =E4*120% =F4*120% =G4*120%

Less:

Expenses =D4*0.6 =E4*0.6 =F4*0.6 =G4*0.6 =H4*0.6

Net

Profit

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

Solution 2:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Sales $ 80,000.00 $ 88,000.00 $ 96,800.00

$

106,480.00

$

117,128.00

Less: Cost of Goods

Sold $ 56,000.00 $ 61,600.00 $ 67,760.00

$

74,536.00

$

81,989.60

Gross Profit $ 24,000.00 $ 26,400.00 $ 29,040.00

$

31,944.00

$

35,138.40

Less: operating

Expenses $ 57,000.00 $ 57,000.00 $ 57,000.00

$

57,000.00

$

57,000.00

Net Profit ($33,000.00) ($30,600.00) ($27,960.00) ($25,056.00) ($21,861.60)

In accounting of financial reports there has been practice of showing the negative number

in brackets because it helps to distinct the positive number from the negative number and also

provides better understanding of the number in the report. If negative numbers are shown

without brackets it will create confusion regarding the positive numbers and negative numbers

(Brealey, Myers & Marcus, 2007).

Solution 3:

Normal View:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Sales

$

50,000.00

$

60,000.00

$

72,000.00

$

86,400.00

$

103,680.00

Less: Expenses

$

30,000.00

$

36,000.00

$

43,200.00

$

51,840.00

$

62,208.00

Net Profit

$

20,000.00

$

24,000.00

$

28,800.00

$

34,560.00

$

41,472.00

Formula View:

Particula

rs Year 1 Year 2 Year 3 Year 4 Year 5

Sales 50000 =D4*120% =E4*120% =F4*120% =G4*120%

Less:

Expenses =D4*0.6 =E4*0.6 =F4*0.6 =G4*0.6 =H4*0.6

Net

Profit

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

=Sales-

Less__Expen

ses

Solution 2:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Sales $ 80,000.00 $ 88,000.00 $ 96,800.00

$

106,480.00

$

117,128.00

Less: Cost of Goods

Sold $ 56,000.00 $ 61,600.00 $ 67,760.00

$

74,536.00

$

81,989.60

Gross Profit $ 24,000.00 $ 26,400.00 $ 29,040.00

$

31,944.00

$

35,138.40

Less: operating

Expenses $ 57,000.00 $ 57,000.00 $ 57,000.00

$

57,000.00

$

57,000.00

Net Profit ($33,000.00) ($30,600.00) ($27,960.00) ($25,056.00) ($21,861.60)

In accounting of financial reports there has been practice of showing the negative number

in brackets because it helps to distinct the positive number from the negative number and also

provides better understanding of the number in the report. If negative numbers are shown

without brackets it will create confusion regarding the positive numbers and negative numbers

(Brealey, Myers & Marcus, 2007).

Solution 3:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

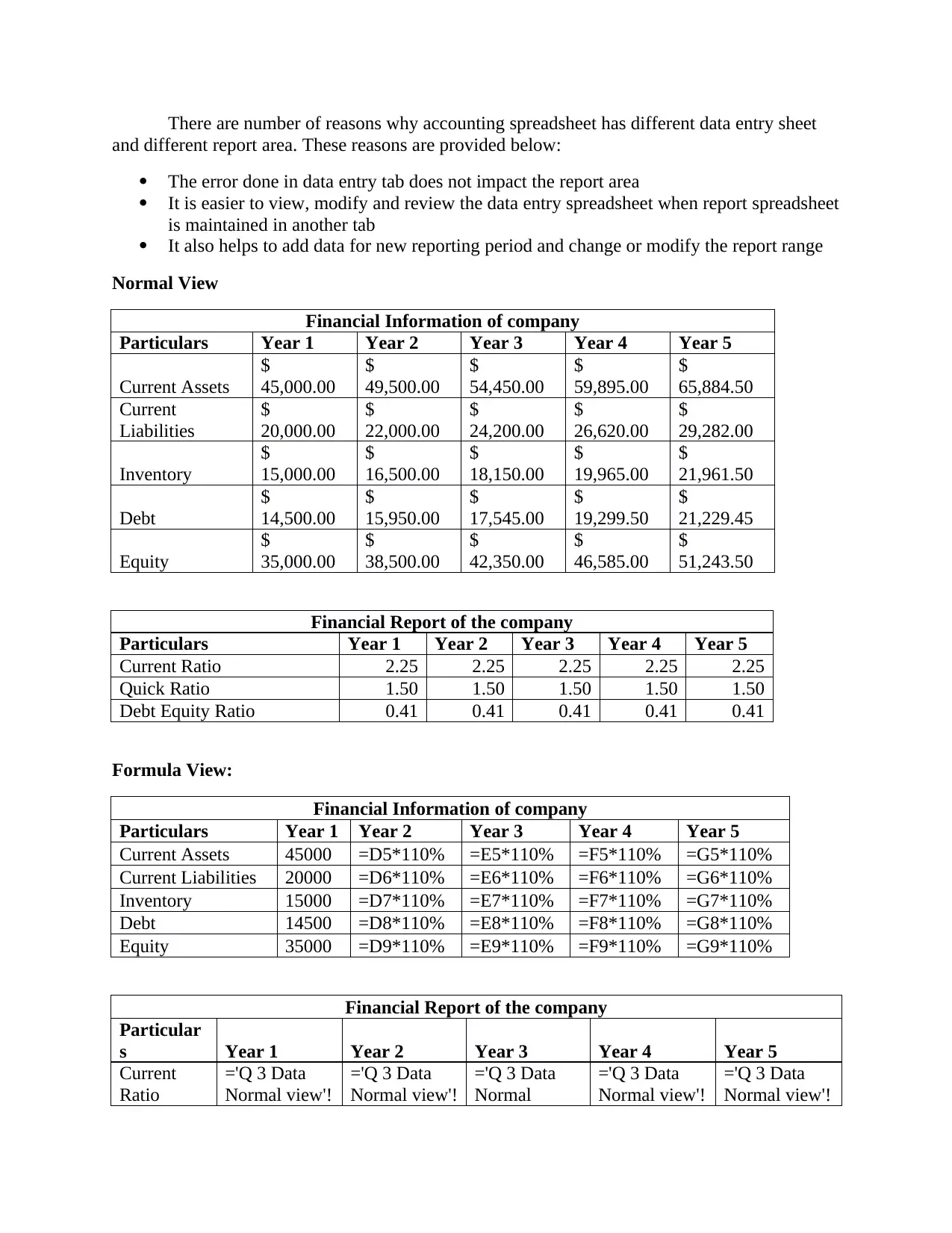

There are number of reasons why accounting spreadsheet has different data entry sheet

and different report area. These reasons are provided below:

The error done in data entry tab does not impact the report area

It is easier to view, modify and review the data entry spreadsheet when report spreadsheet

is maintained in another tab

It also helps to add data for new reporting period and change or modify the report range

Normal View

Financial Information of company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Assets

$

45,000.00

$

49,500.00

$

54,450.00

$

59,895.00

$

65,884.50

Current

Liabilities

$

20,000.00

$

22,000.00

$

24,200.00

$

26,620.00

$

29,282.00

Inventory

$

15,000.00

$

16,500.00

$

18,150.00

$

19,965.00

$

21,961.50

Debt

$

14,500.00

$

15,950.00

$

17,545.00

$

19,299.50

$

21,229.45

Equity

$

35,000.00

$

38,500.00

$

42,350.00

$

46,585.00

$

51,243.50

Financial Report of the company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Ratio 2.25 2.25 2.25 2.25 2.25

Quick Ratio 1.50 1.50 1.50 1.50 1.50

Debt Equity Ratio 0.41 0.41 0.41 0.41 0.41

Formula View:

Financial Information of company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Assets 45000 =D5*110% =E5*110% =F5*110% =G5*110%

Current Liabilities 20000 =D6*110% =E6*110% =F6*110% =G6*110%

Inventory 15000 =D7*110% =E7*110% =F7*110% =G7*110%

Debt 14500 =D8*110% =E8*110% =F8*110% =G8*110%

Equity 35000 =D9*110% =E9*110% =F9*110% =G9*110%

Financial Report of the company

Particular

s Year 1 Year 2 Year 3 Year 4 Year 5

Current

Ratio

='Q 3 Data

Normal view'!

='Q 3 Data

Normal view'!

='Q 3 Data

Normal

='Q 3 Data

Normal view'!

='Q 3 Data

Normal view'!

and different report area. These reasons are provided below:

The error done in data entry tab does not impact the report area

It is easier to view, modify and review the data entry spreadsheet when report spreadsheet

is maintained in another tab

It also helps to add data for new reporting period and change or modify the report range

Normal View

Financial Information of company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Assets

$

45,000.00

$

49,500.00

$

54,450.00

$

59,895.00

$

65,884.50

Current

Liabilities

$

20,000.00

$

22,000.00

$

24,200.00

$

26,620.00

$

29,282.00

Inventory

$

15,000.00

$

16,500.00

$

18,150.00

$

19,965.00

$

21,961.50

Debt

$

14,500.00

$

15,950.00

$

17,545.00

$

19,299.50

$

21,229.45

Equity

$

35,000.00

$

38,500.00

$

42,350.00

$

46,585.00

$

51,243.50

Financial Report of the company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Ratio 2.25 2.25 2.25 2.25 2.25

Quick Ratio 1.50 1.50 1.50 1.50 1.50

Debt Equity Ratio 0.41 0.41 0.41 0.41 0.41

Formula View:

Financial Information of company

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Current Assets 45000 =D5*110% =E5*110% =F5*110% =G5*110%

Current Liabilities 20000 =D6*110% =E6*110% =F6*110% =G6*110%

Inventory 15000 =D7*110% =E7*110% =F7*110% =G7*110%

Debt 14500 =D8*110% =E8*110% =F8*110% =G8*110%

Equity 35000 =D9*110% =E9*110% =F9*110% =G9*110%

Financial Report of the company

Particular

s Year 1 Year 2 Year 3 Year 4 Year 5

Current

Ratio

='Q 3 Data

Normal view'!

='Q 3 Data

Normal view'!

='Q 3 Data

Normal

='Q 3 Data

Normal view'!

='Q 3 Data

Normal view'!

D5/'Q 3 Data

Normal view'!

D6

E5/'Q 3 Data

Normal view'!

E6

view'!F5/'Q 3

Data Normal

view'!F6

G5/'Q 3 Data

Normal view'!

G6

H5/'Q 3 Data

Normal view'!

H6

Quick

Ratio

=('Q 3 Data

Normal view'!

D5-'Q 3 Data

Normal view'!

D7)/'Q 3 Data

Normal view'!

D6

=('Q 3 Data

Normal view'!

E5-'Q 3 Data

Normal view'!

E7)/'Q 3 Data

Normal view'!

E6

=('Q 3 Data

Normal

view'!F5-'Q 3

Data Normal

view'!F7)/'Q

3 Data

Normal

view'!F6

=('Q 3 Data

Normal view'!

G5-'Q 3 Data

Normal view'!

G7)/'Q 3 Data

Normal view'!

G6

=('Q 3 Data

Normal view'!

H5-'Q 3 Data

Normal view'!

H7)/'Q 3 Data

Normal view'!

H6

Debt

Equity

Ratio

='Q 3 Data

Normal view'!

D8/'Q 3 Data

Normal view'!

D9

='Q 3 Data

Normal view'!

E8/'Q 3 Data

Normal view'!

E9

='Q 3 Data

Normal

view'!F8/'Q 3

Data Normal

view'!F9

='Q 3 Data

Normal view'!

G8/'Q 3 Data

Normal view'!

G9

='Q 3 Data

Normal view'!

H8/'Q 3 Data

Normal view'!

H9

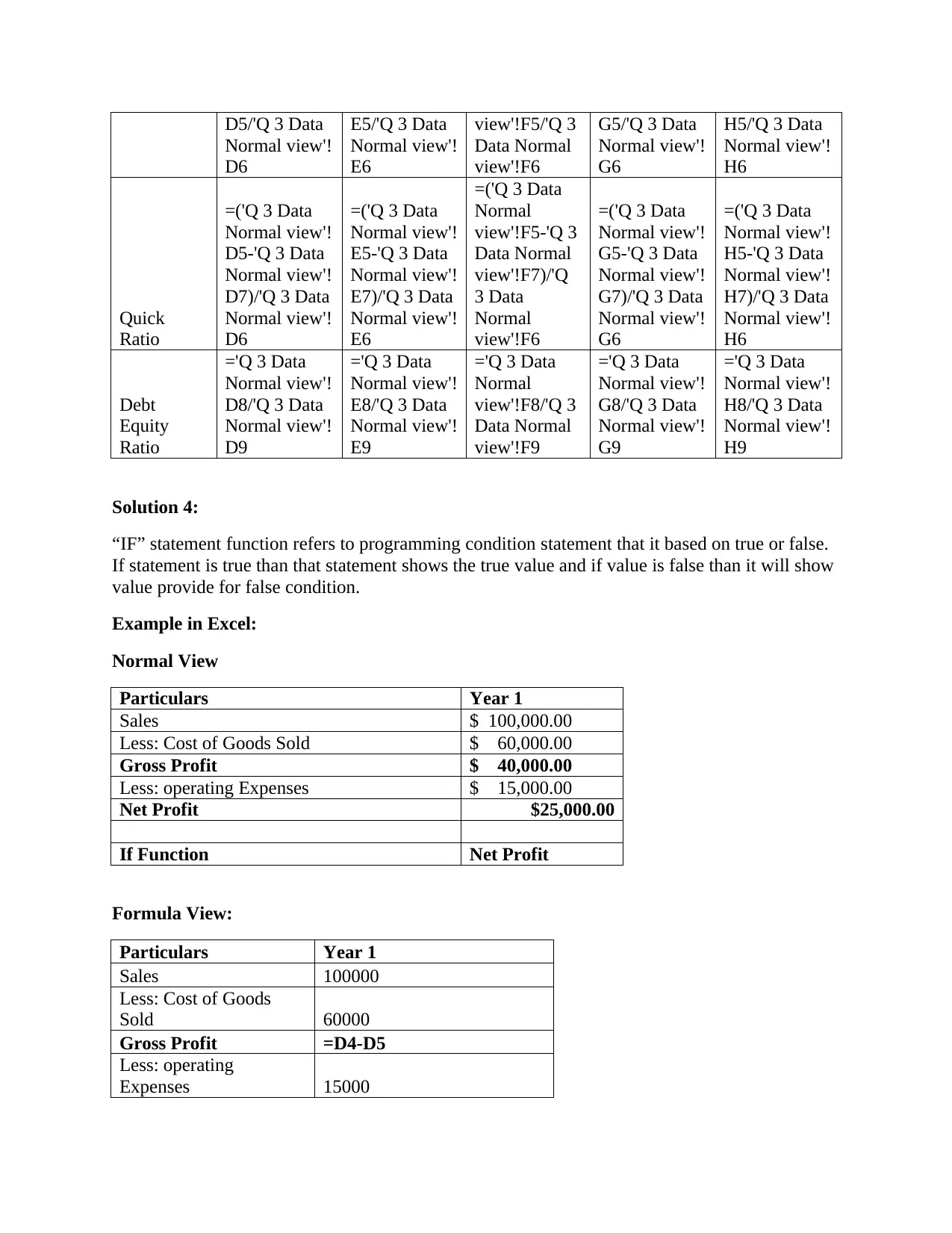

Solution 4:

“IF” statement function refers to programming condition statement that it based on true or false.

If statement is true than that statement shows the true value and if value is false than it will show

value provide for false condition.

Example in Excel:

Normal View

Particulars Year 1

Sales $ 100,000.00

Less: Cost of Goods Sold $ 60,000.00

Gross Profit $ 40,000.00

Less: operating Expenses $ 15,000.00

Net Profit $25,000.00

If Function Net Profit

Formula View:

Particulars Year 1

Sales 100000

Less: Cost of Goods

Sold 60000

Gross Profit =D4-D5

Less: operating

Expenses 15000

Normal view'!

D6

E5/'Q 3 Data

Normal view'!

E6

view'!F5/'Q 3

Data Normal

view'!F6

G5/'Q 3 Data

Normal view'!

G6

H5/'Q 3 Data

Normal view'!

H6

Quick

Ratio

=('Q 3 Data

Normal view'!

D5-'Q 3 Data

Normal view'!

D7)/'Q 3 Data

Normal view'!

D6

=('Q 3 Data

Normal view'!

E5-'Q 3 Data

Normal view'!

E7)/'Q 3 Data

Normal view'!

E6

=('Q 3 Data

Normal

view'!F5-'Q 3

Data Normal

view'!F7)/'Q

3 Data

Normal

view'!F6

=('Q 3 Data

Normal view'!

G5-'Q 3 Data

Normal view'!

G7)/'Q 3 Data

Normal view'!

G6

=('Q 3 Data

Normal view'!

H5-'Q 3 Data

Normal view'!

H7)/'Q 3 Data

Normal view'!

H6

Debt

Equity

Ratio

='Q 3 Data

Normal view'!

D8/'Q 3 Data

Normal view'!

D9

='Q 3 Data

Normal view'!

E8/'Q 3 Data

Normal view'!

E9

='Q 3 Data

Normal

view'!F8/'Q 3

Data Normal

view'!F9

='Q 3 Data

Normal view'!

G8/'Q 3 Data

Normal view'!

G9

='Q 3 Data

Normal view'!

H8/'Q 3 Data

Normal view'!

H9

Solution 4:

“IF” statement function refers to programming condition statement that it based on true or false.

If statement is true than that statement shows the true value and if value is false than it will show

value provide for false condition.

Example in Excel:

Normal View

Particulars Year 1

Sales $ 100,000.00

Less: Cost of Goods Sold $ 60,000.00

Gross Profit $ 40,000.00

Less: operating Expenses $ 15,000.00

Net Profit $25,000.00

If Function Net Profit

Formula View:

Particulars Year 1

Sales 100000

Less: Cost of Goods

Sold 60000

Gross Profit =D4-D5

Less: operating

Expenses 15000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

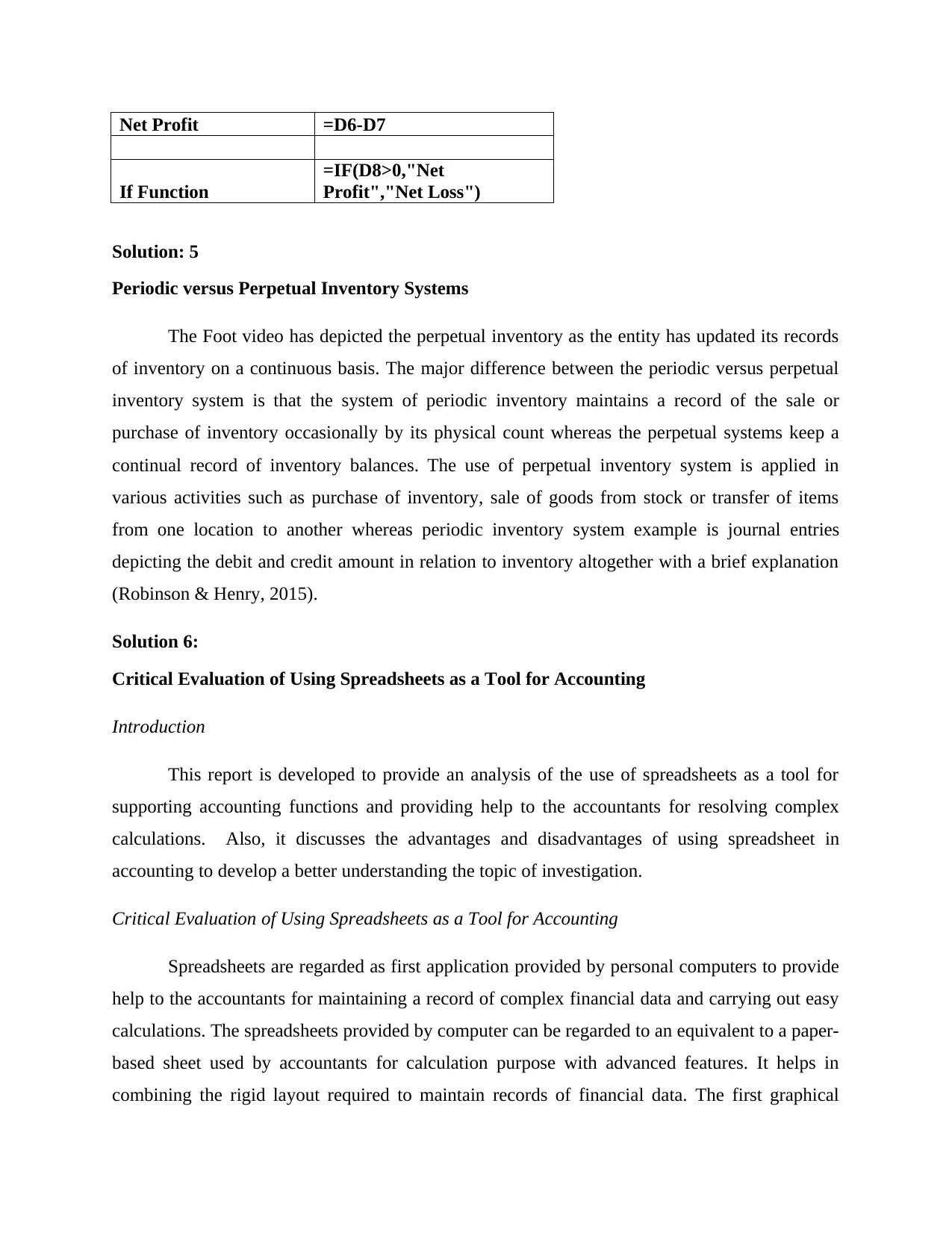

Net Profit =D6-D7

If Function

=IF(D8>0,"Net

Profit","Net Loss")

Solution: 5

Periodic versus Perpetual Inventory Systems

The Foot video has depicted the perpetual inventory as the entity has updated its records

of inventory on a continuous basis. The major difference between the periodic versus perpetual

inventory system is that the system of periodic inventory maintains a record of the sale or

purchase of inventory occasionally by its physical count whereas the perpetual systems keep a

continual record of inventory balances. The use of perpetual inventory system is applied in

various activities such as purchase of inventory, sale of goods from stock or transfer of items

from one location to another whereas periodic inventory system example is journal entries

depicting the debit and credit amount in relation to inventory altogether with a brief explanation

(Robinson & Henry, 2015).

Solution 6:

Critical Evaluation of Using Spreadsheets as a Tool for Accounting

Introduction

This report is developed to provide an analysis of the use of spreadsheets as a tool for

supporting accounting functions and providing help to the accountants for resolving complex

calculations. Also, it discusses the advantages and disadvantages of using spreadsheet in

accounting to develop a better understanding the topic of investigation.

Critical Evaluation of Using Spreadsheets as a Tool for Accounting

Spreadsheets are regarded as first application provided by personal computers to provide

help to the accountants for maintaining a record of complex financial data and carrying out easy

calculations. The spreadsheets provided by computer can be regarded to an equivalent to a paper-

based sheet used by accountants for calculation purpose with advanced features. It helps in

combining the rigid layout required to maintain records of financial data. The first graphical

If Function

=IF(D8>0,"Net

Profit","Net Loss")

Solution: 5

Periodic versus Perpetual Inventory Systems

The Foot video has depicted the perpetual inventory as the entity has updated its records

of inventory on a continuous basis. The major difference between the periodic versus perpetual

inventory system is that the system of periodic inventory maintains a record of the sale or

purchase of inventory occasionally by its physical count whereas the perpetual systems keep a

continual record of inventory balances. The use of perpetual inventory system is applied in

various activities such as purchase of inventory, sale of goods from stock or transfer of items

from one location to another whereas periodic inventory system example is journal entries

depicting the debit and credit amount in relation to inventory altogether with a brief explanation

(Robinson & Henry, 2015).

Solution 6:

Critical Evaluation of Using Spreadsheets as a Tool for Accounting

Introduction

This report is developed to provide an analysis of the use of spreadsheets as a tool for

supporting accounting functions and providing help to the accountants for resolving complex

calculations. Also, it discusses the advantages and disadvantages of using spreadsheet in

accounting to develop a better understanding the topic of investigation.

Critical Evaluation of Using Spreadsheets as a Tool for Accounting

Spreadsheets are regarded as first application provided by personal computers to provide

help to the accountants for maintaining a record of complex financial data and carrying out easy

calculations. The spreadsheets provided by computer can be regarded to an equivalent to a paper-

based sheet used by accountants for calculation purpose with advanced features. It helps in

combining the rigid layout required to maintain records of financial data. The first graphical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interface, known as modern spreadsheet was developed by Microsoft. The electronic spreadsheet

provided by the computers facilitated accountants to a large extent by providing them a platform

to perform calculations quickly and easily (Wahlen et al., 2017). The accountants at present are

incorporating the use of computer based spreadsheets largely to increase the productivity of

businesses by managing the complex financial data adequately leading to faster decision-making

(McWatters and Zimmerman, 2015). The advantages and disadvantages of spreadsheets use as a

tool for accounting can be discussed as follows:

Advantages

It enables in performing easy calculations by displaying numbers and formulas. The

different type of function provided by spreadsheets are auto sum, multiplication, dividing,

subtracting and other large variety of operations that can be used for better control of accounting

data and analysis. Also, the grid representing of the cells in the spreadsheet can be made in hide

or visible mode as per the requirement and format of the spreadsheet. It also eliminated the

requirements of using complex calculators to perform the accounting operations and thereby

reduces the administrative costs. These can also be used to automate the database by better

manipulation and interpretation of financial information provided in the spreadsheet (Carlberg,

2007).

Disadvantages

The major drawback of spreadsheets is that it causes deskilling as accountants need no

longer to use their mental capabilities for analyzing the accounting data that can be easily

performed with the use of electronic spreadsheet. Also, it negatively impacts the coordination

and interaction among the colleagues as they can individually perform the data analysis through

its use without requiring any external assistance. It also led to duplication of data and its

structure increase the need of storage. However, the integration of graphic and other word

processing features into the spreadsheet ahs improved its analysis function as it is much easier to

understand the information presented with the use of figures (Blackwood, 2014).

Solution 7:

Report

Ending Inventory on October 31

provided by the computers facilitated accountants to a large extent by providing them a platform

to perform calculations quickly and easily (Wahlen et al., 2017). The accountants at present are

incorporating the use of computer based spreadsheets largely to increase the productivity of

businesses by managing the complex financial data adequately leading to faster decision-making

(McWatters and Zimmerman, 2015). The advantages and disadvantages of spreadsheets use as a

tool for accounting can be discussed as follows:

Advantages

It enables in performing easy calculations by displaying numbers and formulas. The

different type of function provided by spreadsheets are auto sum, multiplication, dividing,

subtracting and other large variety of operations that can be used for better control of accounting

data and analysis. Also, the grid representing of the cells in the spreadsheet can be made in hide

or visible mode as per the requirement and format of the spreadsheet. It also eliminated the

requirements of using complex calculators to perform the accounting operations and thereby

reduces the administrative costs. These can also be used to automate the database by better

manipulation and interpretation of financial information provided in the spreadsheet (Carlberg,

2007).

Disadvantages

The major drawback of spreadsheets is that it causes deskilling as accountants need no

longer to use their mental capabilities for analyzing the accounting data that can be easily

performed with the use of electronic spreadsheet. Also, it negatively impacts the coordination

and interaction among the colleagues as they can individually perform the data analysis through

its use without requiring any external assistance. It also led to duplication of data and its

structure increase the need of storage. However, the integration of graphic and other word

processing features into the spreadsheet ahs improved its analysis function as it is much easier to

understand the information presented with the use of figures (Blackwood, 2014).

Solution 7:

Report

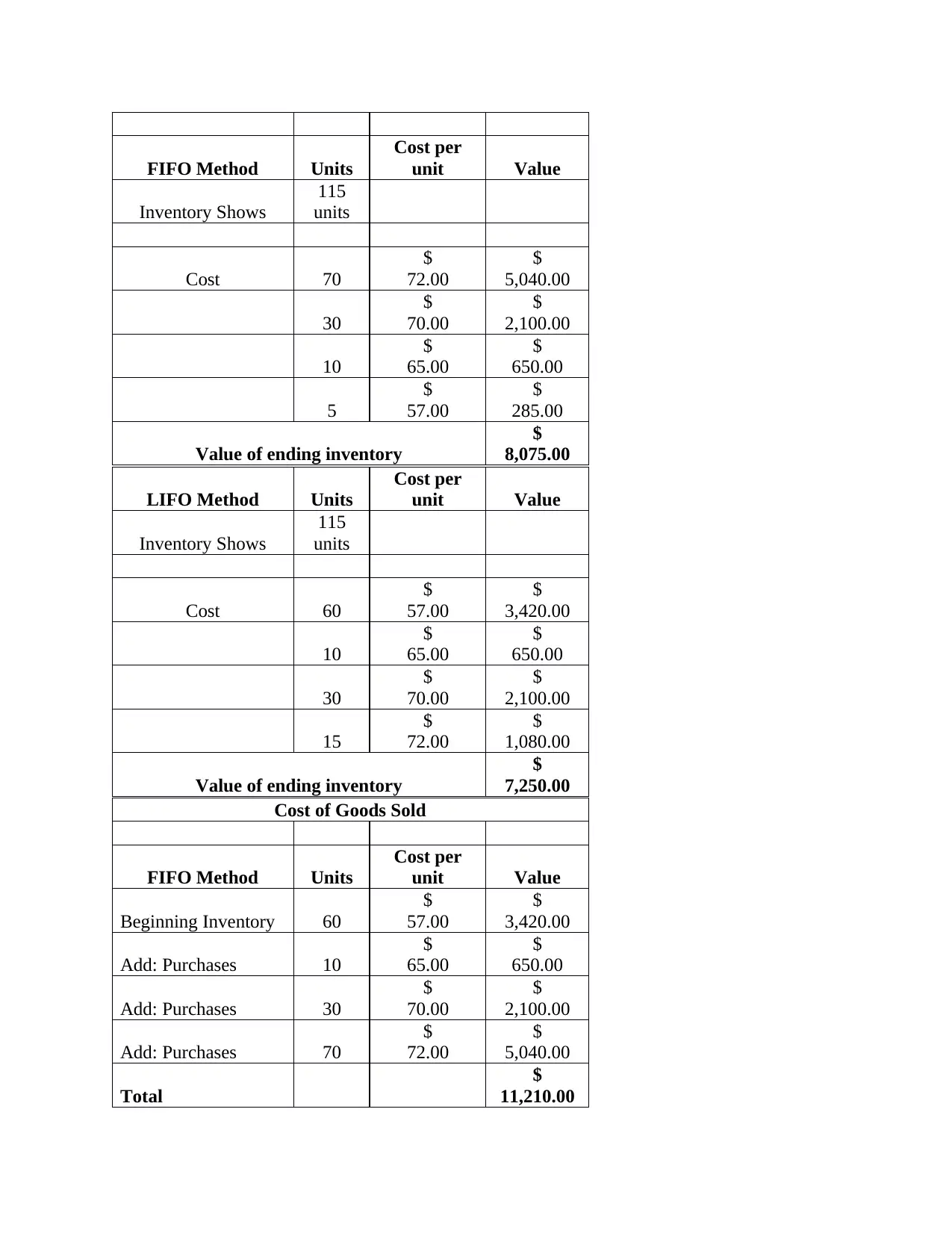

Ending Inventory on October 31

FIFO Method Units

Cost per

unit Value

Inventory Shows

115

units

Cost 70

$

72.00

$

5,040.00

30

$

70.00

$

2,100.00

10

$

65.00

$

650.00

5

$

57.00

$

285.00

Value of ending inventory

$

8,075.00

LIFO Method Units

Cost per

unit Value

Inventory Shows

115

units

Cost 60

$

57.00

$

3,420.00

10

$

65.00

$

650.00

30

$

70.00

$

2,100.00

15

$

72.00

$

1,080.00

Value of ending inventory

$

7,250.00

Cost of Goods Sold

FIFO Method Units

Cost per

unit Value

Beginning Inventory 60

$

57.00

$

3,420.00

Add: Purchases 10

$

65.00

$

650.00

Add: Purchases 30

$

70.00

$

2,100.00

Add: Purchases 70

$

72.00

$

5,040.00

Total

$

11,210.00

Cost per

unit Value

Inventory Shows

115

units

Cost 70

$

72.00

$

5,040.00

30

$

70.00

$

2,100.00

10

$

65.00

$

650.00

5

$

57.00

$

285.00

Value of ending inventory

$

8,075.00

LIFO Method Units

Cost per

unit Value

Inventory Shows

115

units

Cost 60

$

57.00

$

3,420.00

10

$

65.00

$

650.00

30

$

70.00

$

2,100.00

15

$

72.00

$

1,080.00

Value of ending inventory

$

7,250.00

Cost of Goods Sold

FIFO Method Units

Cost per

unit Value

Beginning Inventory 60

$

57.00

$

3,420.00

Add: Purchases 10

$

65.00

$

650.00

Add: Purchases 30

$

70.00

$

2,100.00

Add: Purchases 70

$

72.00

$

5,040.00

Total

$

11,210.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Closing

Inventory 115

$

8,075.00

Cost of Goods Sold

$

3,135.00

Cost of Goods Sold

LIFO Method Units

Cost per

unit Value

Beginning Inventory 60

$

57.00

$

3,420.00

Add: Purchases 10

$

65.00

$

650.00

Add: Purchases 30

$

70.00

$

2,100.00

Add: Purchases 70

$

72.00

$

5,040.00

Total

$

11,210.00

Less: Closing

Inventory 115

$

7,250.00

Cost of Goods Sold

$

3,960.00

Gross Profit

Particulars FIFO LIFO

Revenue

$

25,000.00

$

25,000.00

Less: Cost of goods

sold

$

3,135.00

$

3,960.00

Gross Profit

$

21,865.00

$

21,040.00

Solution 8:

Normal View:

Bank Reconciliation Statement

Particulars Amount Amount

Bank Balance on 31 July $ 21,453.00

Add: Deposit Transit $ 2,345.00

Balance $ 23,798.00

Less: Outstanding Checks

Cheque no. 1420

$

1,678.00

Cheque no. 1421 $

Inventory 115

$

8,075.00

Cost of Goods Sold

$

3,135.00

Cost of Goods Sold

LIFO Method Units

Cost per

unit Value

Beginning Inventory 60

$

57.00

$

3,420.00

Add: Purchases 10

$

65.00

$

650.00

Add: Purchases 30

$

70.00

$

2,100.00

Add: Purchases 70

$

72.00

$

5,040.00

Total

$

11,210.00

Less: Closing

Inventory 115

$

7,250.00

Cost of Goods Sold

$

3,960.00

Gross Profit

Particulars FIFO LIFO

Revenue

$

25,000.00

$

25,000.00

Less: Cost of goods

sold

$

3,135.00

$

3,960.00

Gross Profit

$

21,865.00

$

21,040.00

Solution 8:

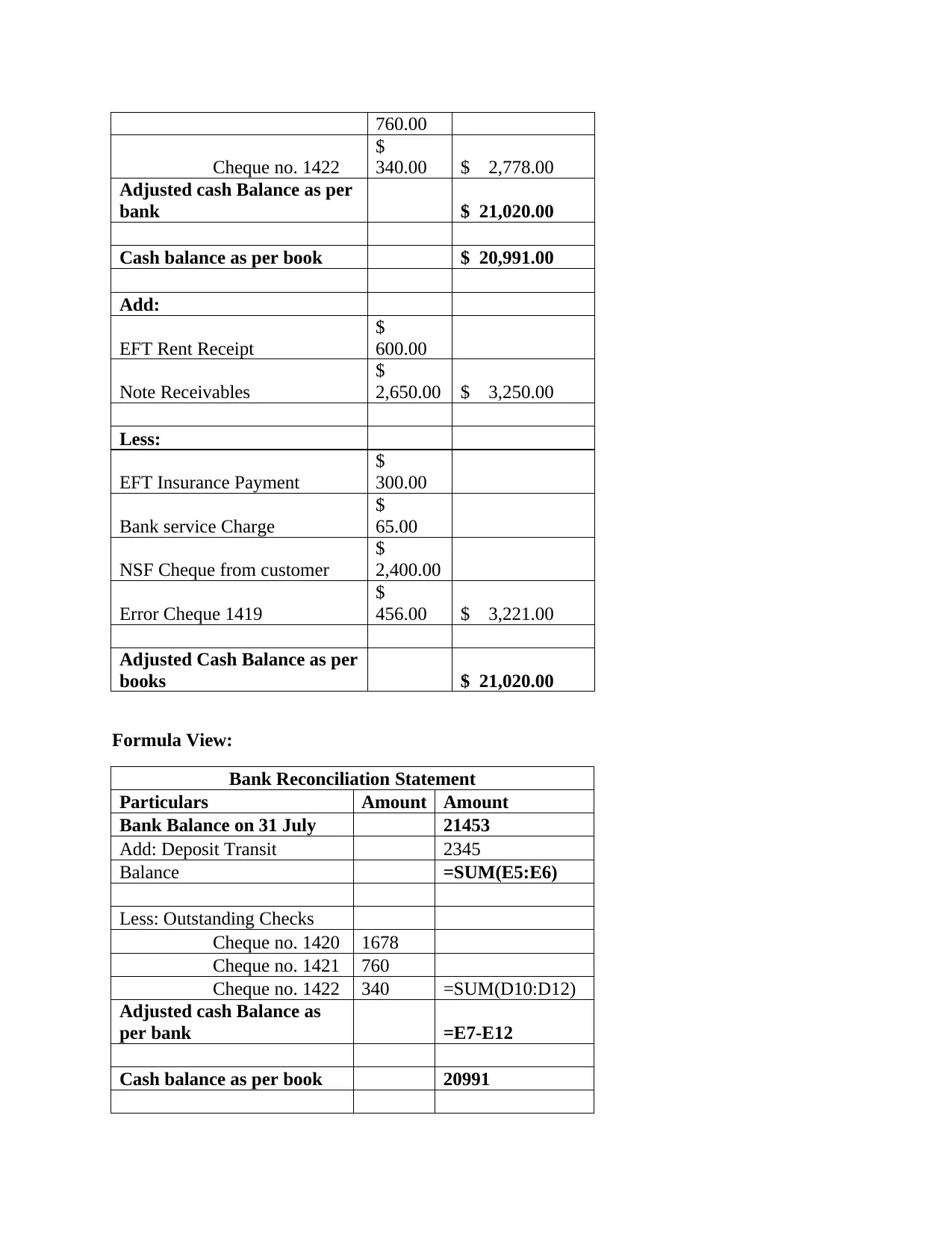

Normal View:

Bank Reconciliation Statement

Particulars Amount Amount

Bank Balance on 31 July $ 21,453.00

Add: Deposit Transit $ 2,345.00

Balance $ 23,798.00

Less: Outstanding Checks

Cheque no. 1420

$

1,678.00

Cheque no. 1421 $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

760.00

Cheque no. 1422

$

340.00 $ 2,778.00

Adjusted cash Balance as per

bank $ 21,020.00

Cash balance as per book $ 20,991.00

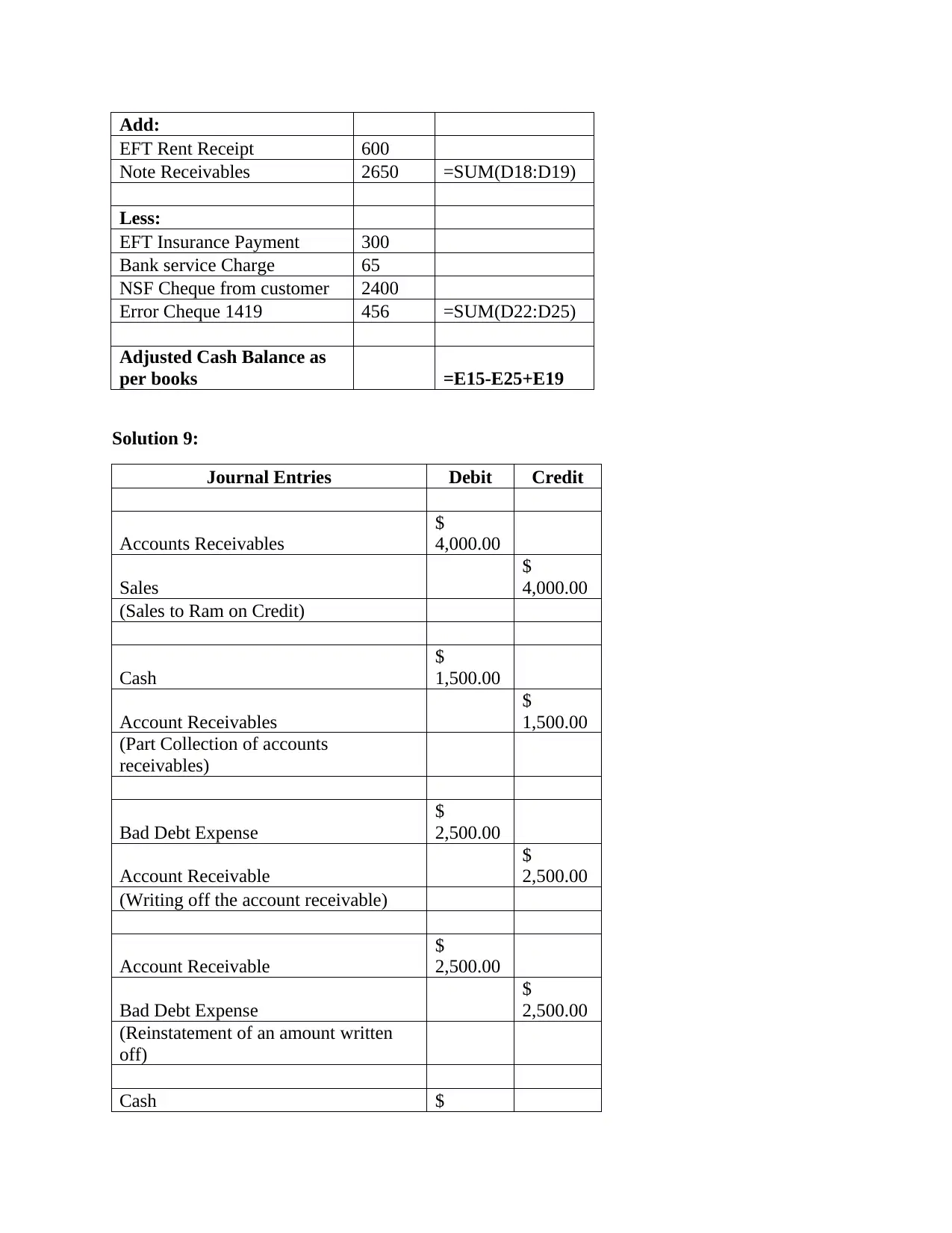

Add:

EFT Rent Receipt

$

600.00

Note Receivables

$

2,650.00 $ 3,250.00

Less:

EFT Insurance Payment

$

300.00

Bank service Charge

$

65.00

NSF Cheque from customer

$

2,400.00

Error Cheque 1419

$

456.00 $ 3,221.00

Adjusted Cash Balance as per

books $ 21,020.00

Formula View:

Bank Reconciliation Statement

Particulars Amount Amount

Bank Balance on 31 July 21453

Add: Deposit Transit 2345

Balance =SUM(E5:E6)

Less: Outstanding Checks

Cheque no. 1420 1678

Cheque no. 1421 760

Cheque no. 1422 340 =SUM(D10:D12)

Adjusted cash Balance as

per bank =E7-E12

Cash balance as per book 20991

Cheque no. 1422

$

340.00 $ 2,778.00

Adjusted cash Balance as per

bank $ 21,020.00

Cash balance as per book $ 20,991.00

Add:

EFT Rent Receipt

$

600.00

Note Receivables

$

2,650.00 $ 3,250.00

Less:

EFT Insurance Payment

$

300.00

Bank service Charge

$

65.00

NSF Cheque from customer

$

2,400.00

Error Cheque 1419

$

456.00 $ 3,221.00

Adjusted Cash Balance as per

books $ 21,020.00

Formula View:

Bank Reconciliation Statement

Particulars Amount Amount

Bank Balance on 31 July 21453

Add: Deposit Transit 2345

Balance =SUM(E5:E6)

Less: Outstanding Checks

Cheque no. 1420 1678

Cheque no. 1421 760

Cheque no. 1422 340 =SUM(D10:D12)

Adjusted cash Balance as

per bank =E7-E12

Cash balance as per book 20991

Add:

EFT Rent Receipt 600

Note Receivables 2650 =SUM(D18:D19)

Less:

EFT Insurance Payment 300

Bank service Charge 65

NSF Cheque from customer 2400

Error Cheque 1419 456 =SUM(D22:D25)

Adjusted Cash Balance as

per books =E15-E25+E19

Solution 9:

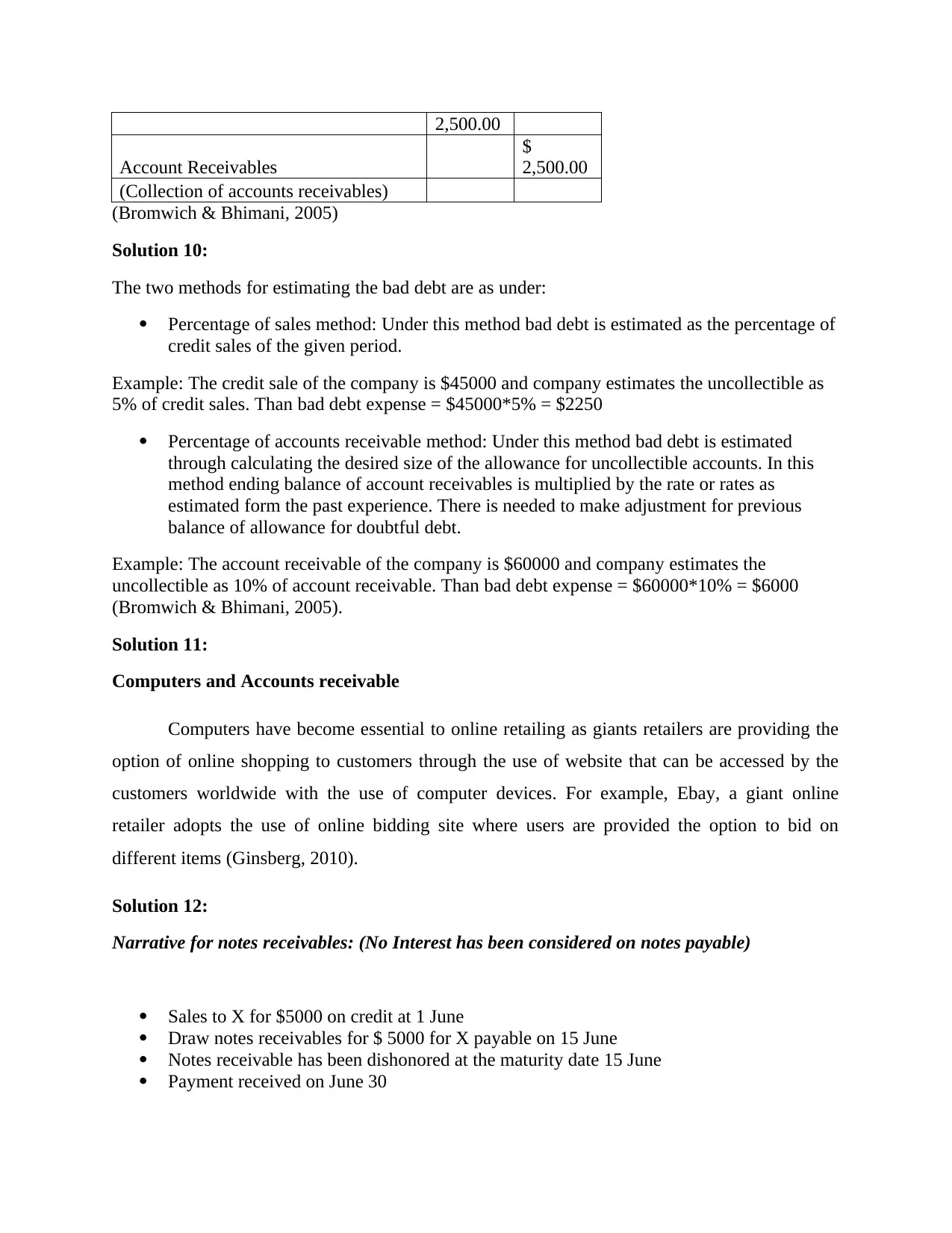

Journal Entries Debit Credit

Accounts Receivables

$

4,000.00

Sales

$

4,000.00

(Sales to Ram on Credit)

Cash

$

1,500.00

Account Receivables

$

1,500.00

(Part Collection of accounts

receivables)

Bad Debt Expense

$

2,500.00

Account Receivable

$

2,500.00

(Writing off the account receivable)

Account Receivable

$

2,500.00

Bad Debt Expense

$

2,500.00

(Reinstatement of an amount written

off)

Cash $

EFT Rent Receipt 600

Note Receivables 2650 =SUM(D18:D19)

Less:

EFT Insurance Payment 300

Bank service Charge 65

NSF Cheque from customer 2400

Error Cheque 1419 456 =SUM(D22:D25)

Adjusted Cash Balance as

per books =E15-E25+E19

Solution 9:

Journal Entries Debit Credit

Accounts Receivables

$

4,000.00

Sales

$

4,000.00

(Sales to Ram on Credit)

Cash

$

1,500.00

Account Receivables

$

1,500.00

(Part Collection of accounts

receivables)

Bad Debt Expense

$

2,500.00

Account Receivable

$

2,500.00

(Writing off the account receivable)

Account Receivable

$

2,500.00

Bad Debt Expense

$

2,500.00

(Reinstatement of an amount written

off)

Cash $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2,500.00

Account Receivables

$

2,500.00

(Collection of accounts receivables)

(Bromwich & Bhimani, 2005)

Solution 10:

The two methods for estimating the bad debt are as under:

Percentage of sales method: Under this method bad debt is estimated as the percentage of

credit sales of the given period.

Example: The credit sale of the company is $45000 and company estimates the uncollectible as

5% of credit sales. Than bad debt expense = $45000*5% = $2250

Percentage of accounts receivable method: Under this method bad debt is estimated

through calculating the desired size of the allowance for uncollectible accounts. In this

method ending balance of account receivables is multiplied by the rate or rates as

estimated form the past experience. There is needed to make adjustment for previous

balance of allowance for doubtful debt.

Example: The account receivable of the company is $60000 and company estimates the

uncollectible as 10% of account receivable. Than bad debt expense = $60000*10% = $6000

(Bromwich & Bhimani, 2005).

Solution 11:

Computers and Accounts receivable

Computers have become essential to online retailing as giants retailers are providing the

option of online shopping to customers through the use of website that can be accessed by the

customers worldwide with the use of computer devices. For example, Ebay, a giant online

retailer adopts the use of online bidding site where users are provided the option to bid on

different items (Ginsberg, 2010).

Solution 12:

Narrative for notes receivables: (No Interest has been considered on notes payable)

Sales to X for $5000 on credit at 1 June

Draw notes receivables for $ 5000 for X payable on 15 June

Notes receivable has been dishonored at the maturity date 15 June

Payment received on June 30

Account Receivables

$

2,500.00

(Collection of accounts receivables)

(Bromwich & Bhimani, 2005)

Solution 10:

The two methods for estimating the bad debt are as under:

Percentage of sales method: Under this method bad debt is estimated as the percentage of

credit sales of the given period.

Example: The credit sale of the company is $45000 and company estimates the uncollectible as

5% of credit sales. Than bad debt expense = $45000*5% = $2250

Percentage of accounts receivable method: Under this method bad debt is estimated

through calculating the desired size of the allowance for uncollectible accounts. In this

method ending balance of account receivables is multiplied by the rate or rates as

estimated form the past experience. There is needed to make adjustment for previous

balance of allowance for doubtful debt.

Example: The account receivable of the company is $60000 and company estimates the

uncollectible as 10% of account receivable. Than bad debt expense = $60000*10% = $6000

(Bromwich & Bhimani, 2005).

Solution 11:

Computers and Accounts receivable

Computers have become essential to online retailing as giants retailers are providing the

option of online shopping to customers through the use of website that can be accessed by the

customers worldwide with the use of computer devices. For example, Ebay, a giant online

retailer adopts the use of online bidding site where users are provided the option to bid on

different items (Ginsberg, 2010).

Solution 12:

Narrative for notes receivables: (No Interest has been considered on notes payable)

Sales to X for $5000 on credit at 1 June

Draw notes receivables for $ 5000 for X payable on 15 June

Notes receivable has been dishonored at the maturity date 15 June

Payment received on June 30

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Journal Entries Debit Credit

01-Jun Account Receivable

$

5,000.00

Sales

$

5,000.00

01-Jun Notes Receivable

$

5,000.00

Account Receivable

$

5,000.00

15-Jun Account receivable

$

5,000.00

Notes Receivable

$

5,000.00

30-Jun Cash

$

5,000.00

Account Receivable

$

5,000.00

Account Receivable

Date Particulars Debit Date Particulars Credit

01-

Jun Notes Receivable

$

5,000.00

01-

Jun Mr Y

$

5,000.00

30-

Jun Cash

$

5,000.00

15-

Jun Notes Receivable

$

5,000.00

Notes Receivable

Date Particulars Debit Date Particulars Credit

15-

Jun

Account

Receivable

$

5,000.00

01-

Jun

Account

Receivable

$

5,000.00

Cash

Date Particulars Debit Date Particulars Credit

30-

Jun

Account

Receivable

$

5,000.00

01-Jun Account Receivable

$

5,000.00

Sales

$

5,000.00

01-Jun Notes Receivable

$

5,000.00

Account Receivable

$

5,000.00

15-Jun Account receivable

$

5,000.00

Notes Receivable

$

5,000.00

30-Jun Cash

$

5,000.00

Account Receivable

$

5,000.00

Account Receivable

Date Particulars Debit Date Particulars Credit

01-

Jun Notes Receivable

$

5,000.00

01-

Jun Mr Y

$

5,000.00

30-

Jun Cash

$

5,000.00

15-

Jun Notes Receivable

$

5,000.00

Notes Receivable

Date Particulars Debit Date Particulars Credit

15-

Jun

Account

Receivable

$

5,000.00

01-

Jun

Account

Receivable

$

5,000.00

Cash

Date Particulars Debit Date Particulars Credit

30-

Jun

Account

Receivable

$

5,000.00

(Brigham & Michael, 2013)

Solution 13:

Work Integrated Assessment case study

Introduction

The present report is developed for providing an analysis of Wesfarmers as a shareholder

investment on the perspective of an investment advisor with accounting expertise. The analysis

has been carried out with examining the various ranges of the company activities such as

sustainability issues and financial information. The report also presents the charts created from

Wesfarmers data to represent a better analysis of the company performance.

Analysis of Wesfarmers as a Shareholder Investment

Wesfarmers, a supermarket giant of Australia, is involved in diverse business activities

such as supermarkets, liquor, hotels and convenience stores, home improvement and office

supplies. The company has reported a significant increase in the financial earnings in the year

2017 due to improvement in its core business activities. The balance sheet of the company has

reflected a strong position of its asset base and ability to overcome the external shocks. It is also

helping the company to realize the advantage of cost of capital and maintaining adequate sources

of funds such as bank facilities and global bond markets. Also, it has maintained a good credit

rating that is depicted from its strong cash flows statement. The company income statement has

reported an increase in the net profit after tax (NPAT) of about 22.1 per cent in the year 2017 as

compared to the year 2016. Also, there is increase in the return on equity of the company from

12.4% to 9.6% in the previous year. There is also an increase in the operating cash flows of the

company from $861 million to $4,226 million. This is largely due to higher earnings and its

effective management of inventory across its various business segments. Also, it has reduced its

capital expenses in the year 2017 as compared to the previous year by about 11.5 per cent

(Wesfarmers Limited: Annual Report, 2017).

The company has also developed a strong and effective sustainability framework based

on its solid core values of integrity and accountability. It has developed and maintained

operational excellence in its business activities by innovating in its product range and categories

Solution 13:

Work Integrated Assessment case study

Introduction

The present report is developed for providing an analysis of Wesfarmers as a shareholder

investment on the perspective of an investment advisor with accounting expertise. The analysis

has been carried out with examining the various ranges of the company activities such as

sustainability issues and financial information. The report also presents the charts created from

Wesfarmers data to represent a better analysis of the company performance.

Analysis of Wesfarmers as a Shareholder Investment

Wesfarmers, a supermarket giant of Australia, is involved in diverse business activities

such as supermarkets, liquor, hotels and convenience stores, home improvement and office

supplies. The company has reported a significant increase in the financial earnings in the year

2017 due to improvement in its core business activities. The balance sheet of the company has

reflected a strong position of its asset base and ability to overcome the external shocks. It is also

helping the company to realize the advantage of cost of capital and maintaining adequate sources

of funds such as bank facilities and global bond markets. Also, it has maintained a good credit

rating that is depicted from its strong cash flows statement. The company income statement has

reported an increase in the net profit after tax (NPAT) of about 22.1 per cent in the year 2017 as

compared to the year 2016. Also, there is increase in the return on equity of the company from

12.4% to 9.6% in the previous year. There is also an increase in the operating cash flows of the

company from $861 million to $4,226 million. This is largely due to higher earnings and its

effective management of inventory across its various business segments. Also, it has reduced its

capital expenses in the year 2017 as compared to the previous year by about 11.5 per cent

(Wesfarmers Limited: Annual Report, 2017).

The company has also developed a strong and effective sustainability framework based

on its solid core values of integrity and accountability. It has developed and maintained

operational excellence in its business activities by innovating in its product range and categories

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.