Recording Business Transactions: Journal Entries and Analysis

VerifiedAdded on 2022/12/30

|12

|2405

|207

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of accounting principles and practices. It begins by explaining the importance of accounting in recording, summarizing, and analyzing financial transactions for internal and external users, highlighting the advantages and disadvantages of maintaining accounting records. The main body of the assignment includes journal entries for a business, ledger accounts, and a trial balance. It also presents an income statement for Airman Company, analyzing its financial performance and the impact of external factors such as the COVID-19 pandemic on sales, inventory, and expenses. The document covers various aspects of financial accounting, including the preparation of financial statements, the recording of transactions, and the analysis of business performance. The assignment concludes with a summary of the key concepts and their practical applications in business decision-making.

RECORDING BUSINESS

TRANSACTIONS

TRANSACTIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1.......................................................................................................................................3

PART 2.......................................................................................................................................5

PART 3.......................................................................................................................................6

Part 4..........................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1.......................................................................................................................................3

PART 2.......................................................................................................................................5

PART 3.......................................................................................................................................6

Part 4..........................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The file explains the meaning of accounting that accounting is all about recording

transactions, summarizing and analysing transaction and making decision on the basis of these

transactions. It explains that there are internal users like management, shareholder and external

users like government, customers etc. make the decisions that makes the decisions and there are

various advantages like availability of accurate data for audit, evaluation of position of the

company and disadvantages like estimated data etc.

The file also includes the financial information in journal form and it also shows the income

statement of Airman company and evaluate the reason of difference in profit of the company

from 2009.

MAIN BODY

PART 1

a) Users of accounting information for decision-making: - The accounting information can be

used by the company for facilitating smooth and efficient decision-making such that

organizational objectives can be achieved. The users of such information can be divided into two

parts namely the internal as well as the external users of the information. (Warren, Jonick, and

Schneider, 2020).

External users: - They are outside the organization.

1) Creditors and Lenders- They use accounting information in order to find out the

credibility of the company or the borrower, that will they be able to repay, assets and

liabilities, financial position, past performance etc. They get themselves assured before

lending money (Collier, 2015).

2) Investors- They are the users of accounting information as they need to find out whether

the capital they provide is safe or not. For such analysis the financial data needs to be

studied to gather information regarding the future probability and growth prospects of the

company.

3) Government Regulatory Bodies- The information proves to be essential for these

authorities as they get informed regarding economy and market conditions. They can

assess the amount of tax payable and also regulate that no illegal operations being carried

on by the company.

The file explains the meaning of accounting that accounting is all about recording

transactions, summarizing and analysing transaction and making decision on the basis of these

transactions. It explains that there are internal users like management, shareholder and external

users like government, customers etc. make the decisions that makes the decisions and there are

various advantages like availability of accurate data for audit, evaluation of position of the

company and disadvantages like estimated data etc.

The file also includes the financial information in journal form and it also shows the income

statement of Airman company and evaluate the reason of difference in profit of the company

from 2009.

MAIN BODY

PART 1

a) Users of accounting information for decision-making: - The accounting information can be

used by the company for facilitating smooth and efficient decision-making such that

organizational objectives can be achieved. The users of such information can be divided into two

parts namely the internal as well as the external users of the information. (Warren, Jonick, and

Schneider, 2020).

External users: - They are outside the organization.

1) Creditors and Lenders- They use accounting information in order to find out the

credibility of the company or the borrower, that will they be able to repay, assets and

liabilities, financial position, past performance etc. They get themselves assured before

lending money (Collier, 2015).

2) Investors- They are the users of accounting information as they need to find out whether

the capital they provide is safe or not. For such analysis the financial data needs to be

studied to gather information regarding the future probability and growth prospects of the

company.

3) Government Regulatory Bodies- The information proves to be essential for these

authorities as they get informed regarding economy and market conditions. They can

assess the amount of tax payable and also regulate that no illegal operations being carried

on by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4) Lawmakers- They also play key role by staying updated with the accounting and

financial information to know the position of local economy and then bring changes in

the existing laws to compete globally (Russell, Milne, and Dey, 2017).

5) Customers- They acquire information from such accounts to know whether the products

that are sold by the company are of optimum quality and price or not.

6) Public- The public also has say in a company as they make sure that company does not

ruin the society. The company has certain corporate social responsibility that it has to

fulfil for the betterment of the society (Bagdasaryan, 2019). It is to be ensured that no

harmful effluents are disposed off, environmental protection, less pollution, sustainable

development, funds for development of society etc. The company can build good brand

image by observing such responsibilities.

Internal Users: - They are within the organization.

1) Shareholders- They are the internal parties which use this information to know whether

the management of the company is making apt use of their capital or not. What returns

have they generated in the year is the key idea they need to get.

2) Management- The information is used for smooth and efficient decision-making by using

various tools over the financial information as provided to the managers which is also

called management accounting. Certain decisions like make or buy, expansion or

downsize and the borrowing or investment has to be made to improve operational

efficiency of the business.

3) Employees- They use in assessing their work effectiveness as well as that of the

company. As their job security and well-being depends on the performance of the

company it is to be made sure that the company is moving in right direction and is able to

achieve its goals (B Romney,. 2018).

b) Advantages of recording accounting information: -

1) Helps in providing information regarding Financial performance of the company-

Keeping good accounting records by the accountant for the period in consideration helps

the users of such information informed about the financial well-being of the company. It

helps in determining the current profitability of the company and accordingly such

statements could be analysed to know the future growth prospects of the company.

financial information to know the position of local economy and then bring changes in

the existing laws to compete globally (Russell, Milne, and Dey, 2017).

5) Customers- They acquire information from such accounts to know whether the products

that are sold by the company are of optimum quality and price or not.

6) Public- The public also has say in a company as they make sure that company does not

ruin the society. The company has certain corporate social responsibility that it has to

fulfil for the betterment of the society (Bagdasaryan, 2019). It is to be ensured that no

harmful effluents are disposed off, environmental protection, less pollution, sustainable

development, funds for development of society etc. The company can build good brand

image by observing such responsibilities.

Internal Users: - They are within the organization.

1) Shareholders- They are the internal parties which use this information to know whether

the management of the company is making apt use of their capital or not. What returns

have they generated in the year is the key idea they need to get.

2) Management- The information is used for smooth and efficient decision-making by using

various tools over the financial information as provided to the managers which is also

called management accounting. Certain decisions like make or buy, expansion or

downsize and the borrowing or investment has to be made to improve operational

efficiency of the business.

3) Employees- They use in assessing their work effectiveness as well as that of the

company. As their job security and well-being depends on the performance of the

company it is to be made sure that the company is moving in right direction and is able to

achieve its goals (B Romney,. 2018).

b) Advantages of recording accounting information: -

1) Helps in providing information regarding Financial performance of the company-

Keeping good accounting records by the accountant for the period in consideration helps

the users of such information informed about the financial well-being of the company. It

helps in determining the current profitability of the company and accordingly such

statements could be analysed to know the future growth prospects of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

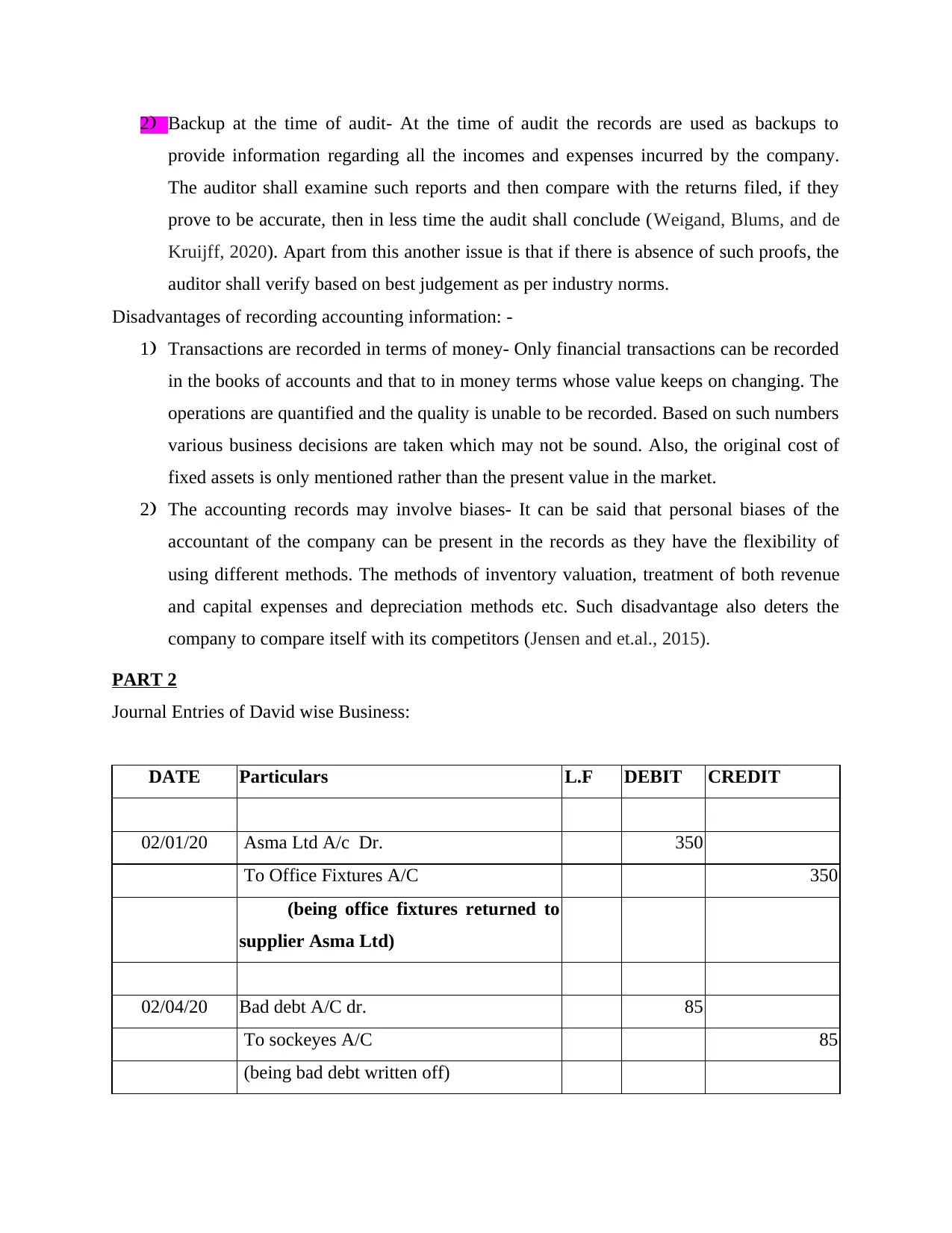

2) Backup at the time of audit- At the time of audit the records are used as backups to

provide information regarding all the incomes and expenses incurred by the company.

The auditor shall examine such reports and then compare with the returns filed, if they

prove to be accurate, then in less time the audit shall conclude (Weigand, Blums, and de

Kruijff, 2020). Apart from this another issue is that if there is absence of such proofs, the

auditor shall verify based on best judgement as per industry norms.

Disadvantages of recording accounting information: -

1) Transactions are recorded in terms of money- Only financial transactions can be recorded

in the books of accounts and that to in money terms whose value keeps on changing. The

operations are quantified and the quality is unable to be recorded. Based on such numbers

various business decisions are taken which may not be sound. Also, the original cost of

fixed assets is only mentioned rather than the present value in the market.

2) The accounting records may involve biases- It can be said that personal biases of the

accountant of the company can be present in the records as they have the flexibility of

using different methods. The methods of inventory valuation, treatment of both revenue

and capital expenses and depreciation methods etc. Such disadvantage also deters the

company to compare itself with its competitors (Jensen and et.al., 2015).

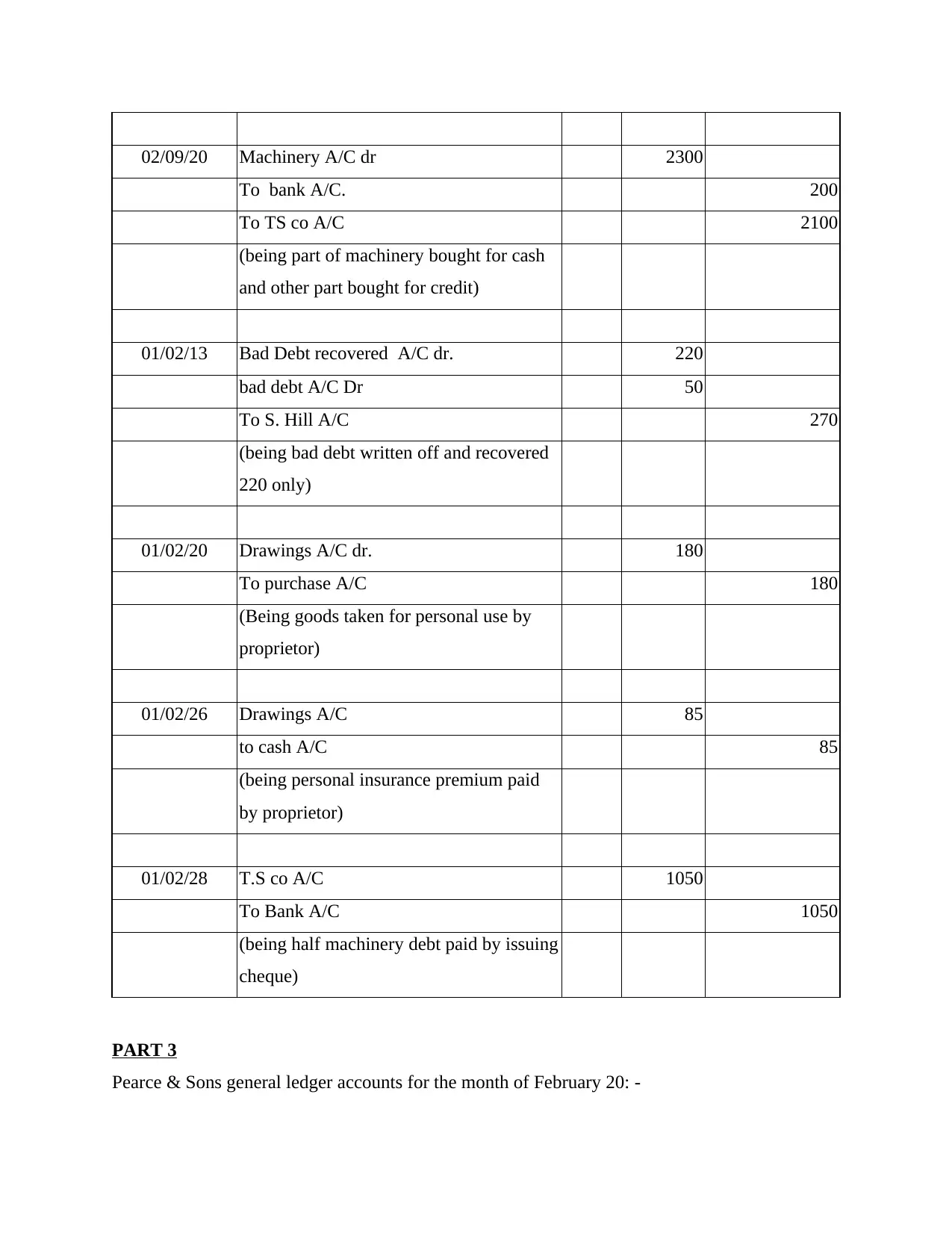

PART 2

Journal Entries of David wise Business:

DATE Particulars L.F DEBIT CREDIT

02/01/20 Asma Ltd A/c Dr. 350

To Office Fixtures A/C 350

(being office fixtures returned to

supplier Asma Ltd)

02/04/20 Bad debt A/C dr. 85

To sockeyes A/C 85

(being bad debt written off)

provide information regarding all the incomes and expenses incurred by the company.

The auditor shall examine such reports and then compare with the returns filed, if they

prove to be accurate, then in less time the audit shall conclude (Weigand, Blums, and de

Kruijff, 2020). Apart from this another issue is that if there is absence of such proofs, the

auditor shall verify based on best judgement as per industry norms.

Disadvantages of recording accounting information: -

1) Transactions are recorded in terms of money- Only financial transactions can be recorded

in the books of accounts and that to in money terms whose value keeps on changing. The

operations are quantified and the quality is unable to be recorded. Based on such numbers

various business decisions are taken which may not be sound. Also, the original cost of

fixed assets is only mentioned rather than the present value in the market.

2) The accounting records may involve biases- It can be said that personal biases of the

accountant of the company can be present in the records as they have the flexibility of

using different methods. The methods of inventory valuation, treatment of both revenue

and capital expenses and depreciation methods etc. Such disadvantage also deters the

company to compare itself with its competitors (Jensen and et.al., 2015).

PART 2

Journal Entries of David wise Business:

DATE Particulars L.F DEBIT CREDIT

02/01/20 Asma Ltd A/c Dr. 350

To Office Fixtures A/C 350

(being office fixtures returned to

supplier Asma Ltd)

02/04/20 Bad debt A/C dr. 85

To sockeyes A/C 85

(being bad debt written off)

02/09/20 Machinery A/C dr 2300

To bank A/C. 200

To TS co A/C 2100

(being part of machinery bought for cash

and other part bought for credit)

01/02/13 Bad Debt recovered A/C dr. 220

bad debt A/C Dr 50

To S. Hill A/C 270

(being bad debt written off and recovered

220 only)

01/02/20 Drawings A/C dr. 180

To purchase A/C 180

(Being goods taken for personal use by

proprietor)

01/02/26 Drawings A/C 85

to cash A/C 85

(being personal insurance premium paid

by proprietor)

01/02/28 T.S co A/C 1050

To Bank A/C 1050

(being half machinery debt paid by issuing

cheque)

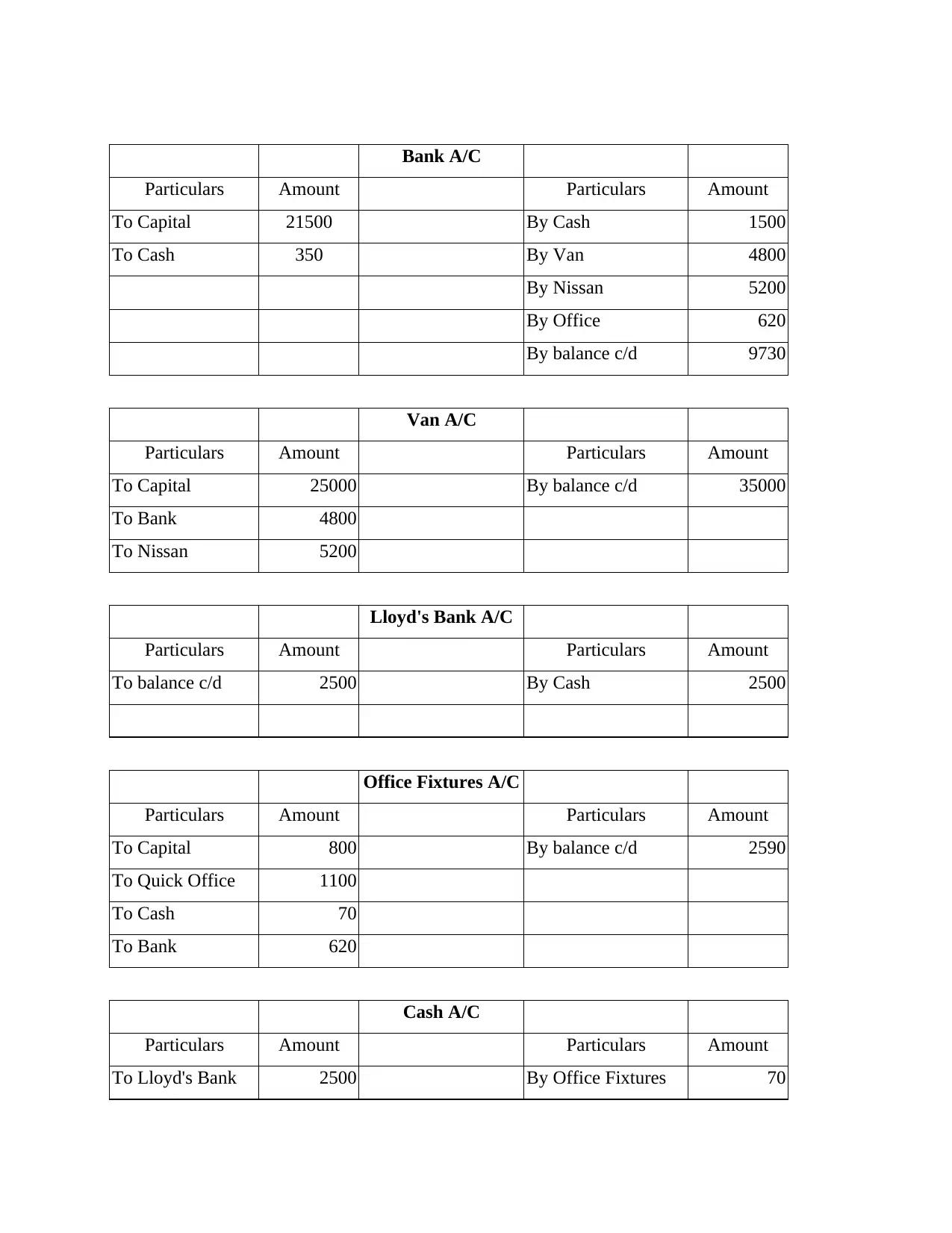

PART 3

Pearce & Sons general ledger accounts for the month of February 20: -

To bank A/C. 200

To TS co A/C 2100

(being part of machinery bought for cash

and other part bought for credit)

01/02/13 Bad Debt recovered A/C dr. 220

bad debt A/C Dr 50

To S. Hill A/C 270

(being bad debt written off and recovered

220 only)

01/02/20 Drawings A/C dr. 180

To purchase A/C 180

(Being goods taken for personal use by

proprietor)

01/02/26 Drawings A/C 85

to cash A/C 85

(being personal insurance premium paid

by proprietor)

01/02/28 T.S co A/C 1050

To Bank A/C 1050

(being half machinery debt paid by issuing

cheque)

PART 3

Pearce & Sons general ledger accounts for the month of February 20: -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank A/C

Particulars Amount Particulars Amount

To Capital 21500 By Cash 1500

To Cash 350 By Van 4800

By Nissan 5200

By Office 620

By balance c/d 9730

Van A/C

Particulars Amount Particulars Amount

To Capital 25000 By balance c/d 35000

To Bank 4800

To Nissan 5200

Lloyd's Bank A/C

Particulars Amount Particulars Amount

To balance c/d 2500 By Cash 2500

Office Fixtures A/C

Particulars Amount Particulars Amount

To Capital 800 By balance c/d 2590

To Quick Office 1100

To Cash 70

To Bank 620

Cash A/C

Particulars Amount Particulars Amount

To Lloyd's Bank 2500 By Office Fixtures 70

Particulars Amount Particulars Amount

To Capital 21500 By Cash 1500

To Cash 350 By Van 4800

By Nissan 5200

By Office 620

By balance c/d 9730

Van A/C

Particulars Amount Particulars Amount

To Capital 25000 By balance c/d 35000

To Bank 4800

To Nissan 5200

Lloyd's Bank A/C

Particulars Amount Particulars Amount

To balance c/d 2500 By Cash 2500

Office Fixtures A/C

Particulars Amount Particulars Amount

To Capital 800 By balance c/d 2590

To Quick Office 1100

To Cash 70

To Bank 620

Cash A/C

Particulars Amount Particulars Amount

To Lloyd's Bank 2500 By Office Fixtures 70

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Bank 1500 By Bank 350

By balance c/d 3580

Quick Office Ltd.

A/C

Particulars Amount Particulars Amount

To balance c/d 1100 By Office Fixtures 1100

Nissan Co. A/C

Particulars Amount Particulars Amount

To Bank 5200 By Van 5200

Capital A/C

Particulars Amount Particulars Amount

To balance c/d 47300 By Bank 21500

By Van 25000

By Office Fixtures 800

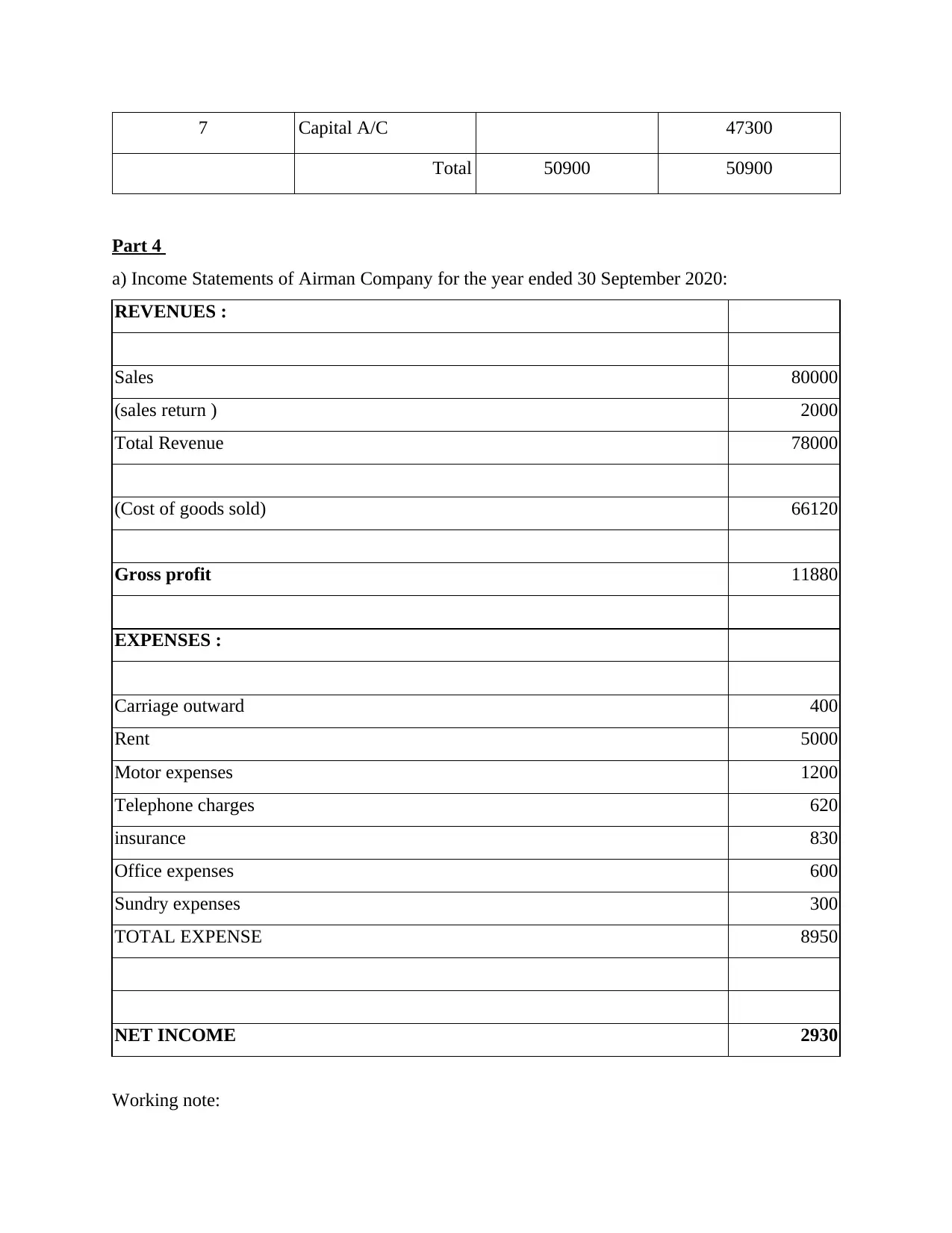

Trail Balance as at 30 February, 20: -

Trial Balance

S. No Particulars Dr. Cr.

1 Bank A/C 9730

2 Van A/C 35000

3 Lloyd's Bank A/C 2500

4 Office Fixtures A/C 2590

5 Cash in Hand A/C 3580

6 Quick Office Ltd. A/C 1100

By balance c/d 3580

Quick Office Ltd.

A/C

Particulars Amount Particulars Amount

To balance c/d 1100 By Office Fixtures 1100

Nissan Co. A/C

Particulars Amount Particulars Amount

To Bank 5200 By Van 5200

Capital A/C

Particulars Amount Particulars Amount

To balance c/d 47300 By Bank 21500

By Van 25000

By Office Fixtures 800

Trail Balance as at 30 February, 20: -

Trial Balance

S. No Particulars Dr. Cr.

1 Bank A/C 9730

2 Van A/C 35000

3 Lloyd's Bank A/C 2500

4 Office Fixtures A/C 2590

5 Cash in Hand A/C 3580

6 Quick Office Ltd. A/C 1100

7 Capital A/C 47300

Total 50900 50900

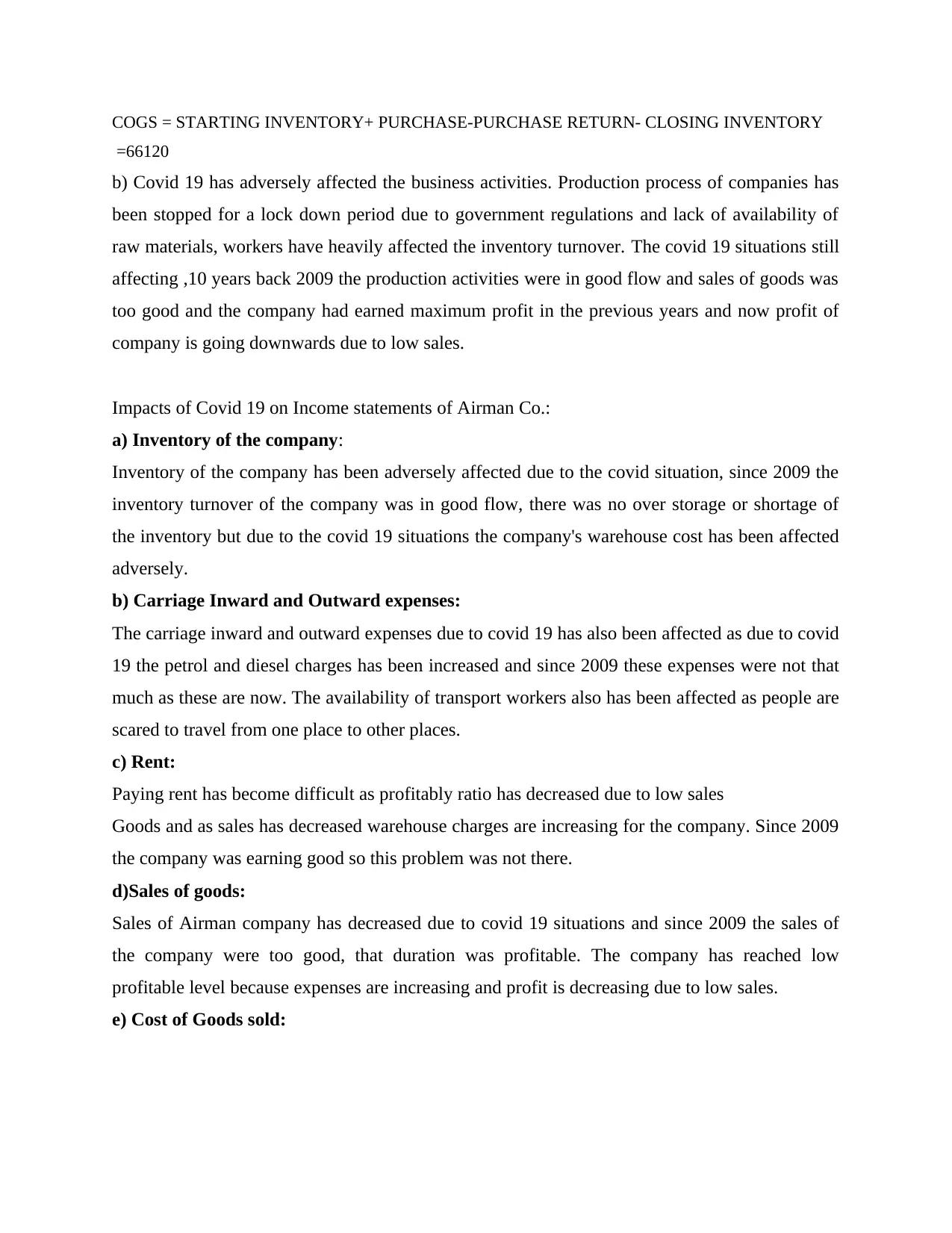

Part 4

a) Income Statements of Airman Company for the year ended 30 September 2020:

REVENUES :

Sales 80000

(sales return ) 2000

Total Revenue 78000

(Cost of goods sold) 66120

Gross profit 11880

EXPENSES :

Carriage outward 400

Rent 5000

Motor expenses 1200

Telephone charges 620

insurance 830

Office expenses 600

Sundry expenses 300

TOTAL EXPENSE 8950

NET INCOME 2930

Working note:

Total 50900 50900

Part 4

a) Income Statements of Airman Company for the year ended 30 September 2020:

REVENUES :

Sales 80000

(sales return ) 2000

Total Revenue 78000

(Cost of goods sold) 66120

Gross profit 11880

EXPENSES :

Carriage outward 400

Rent 5000

Motor expenses 1200

Telephone charges 620

insurance 830

Office expenses 600

Sundry expenses 300

TOTAL EXPENSE 8950

NET INCOME 2930

Working note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COGS = STARTING INVENTORY+ PURCHASE-PURCHASE RETURN- CLOSING INVENTORY

=66120

b) Covid 19 has adversely affected the business activities. Production process of companies has

been stopped for a lock down period due to government regulations and lack of availability of

raw materials, workers have heavily affected the inventory turnover. The covid 19 situations still

affecting ,10 years back 2009 the production activities were in good flow and sales of goods was

too good and the company had earned maximum profit in the previous years and now profit of

company is going downwards due to low sales.

Impacts of Covid 19 on Income statements of Airman Co.:

a) Inventory of the company:

Inventory of the company has been adversely affected due to the covid situation, since 2009 the

inventory turnover of the company was in good flow, there was no over storage or shortage of

the inventory but due to the covid 19 situations the company's warehouse cost has been affected

adversely.

b) Carriage Inward and Outward expenses:

The carriage inward and outward expenses due to covid 19 has also been affected as due to covid

19 the petrol and diesel charges has been increased and since 2009 these expenses were not that

much as these are now. The availability of transport workers also has been affected as people are

scared to travel from one place to other places.

c) Rent:

Paying rent has become difficult as profitably ratio has decreased due to low sales

Goods and as sales has decreased warehouse charges are increasing for the company. Since 2009

the company was earning good so this problem was not there.

d)Sales of goods:

Sales of Airman company has decreased due to covid 19 situations and since 2009 the sales of

the company were too good, that duration was profitable. The company has reached low

profitable level because expenses are increasing and profit is decreasing due to low sales.

e) Cost of Goods sold:

=66120

b) Covid 19 has adversely affected the business activities. Production process of companies has

been stopped for a lock down period due to government regulations and lack of availability of

raw materials, workers have heavily affected the inventory turnover. The covid 19 situations still

affecting ,10 years back 2009 the production activities were in good flow and sales of goods was

too good and the company had earned maximum profit in the previous years and now profit of

company is going downwards due to low sales.

Impacts of Covid 19 on Income statements of Airman Co.:

a) Inventory of the company:

Inventory of the company has been adversely affected due to the covid situation, since 2009 the

inventory turnover of the company was in good flow, there was no over storage or shortage of

the inventory but due to the covid 19 situations the company's warehouse cost has been affected

adversely.

b) Carriage Inward and Outward expenses:

The carriage inward and outward expenses due to covid 19 has also been affected as due to covid

19 the petrol and diesel charges has been increased and since 2009 these expenses were not that

much as these are now. The availability of transport workers also has been affected as people are

scared to travel from one place to other places.

c) Rent:

Paying rent has become difficult as profitably ratio has decreased due to low sales

Goods and as sales has decreased warehouse charges are increasing for the company. Since 2009

the company was earning good so this problem was not there.

d)Sales of goods:

Sales of Airman company has decreased due to covid 19 situations and since 2009 the sales of

the company were too good, that duration was profitable. The company has reached low

profitable level because expenses are increasing and profit is decreasing due to low sales.

e) Cost of Goods sold:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Availability of Raw material has become difficult as compared to previous time also prices of

raw material has increase, lack of availability of carriage inward, paying rent of factory, etc. has

increased cost of goods sold and it has impacted the profitability of the company.

The situation of company is not good as before, the company has low profitably, more cost of

goods sold, more expenses of transportation, low sales all the factors of income statement has

proved that the since 2009 period was better than 2020 covid period.

f) Account Receivable:

Due to covid 19 the debtors are also delaying paying the amount its making the company less

liquidate as compared to before, the company used to receive the more cash since 2009. 2020

situation has become worst as the company is unable to sell more goods and also collection

period has also increased as compare to before the company is trying to recover the losses which

it has bear in lock down. The lock down period was bad period for company because it has led

the company's position down as compare to before. The distribution area of sales has also

decreased because most of the people are scared to buy the products.

CONCLUSION

By summarizing report it can be articulated that accounting plays an important role in

decision making and provides information for evaluation of company's position and it also

provides information in journal entries , ledger, trial balance, and income statements and also

gives the accurate information so company can compare its position from past data and evaluate

the factors that need improvement for company growth and also shows the irrelevant factor

whose cost can be deducted to lower down the cost of production. Strategies can be made to

bring changes in cost of goods sale and sales strategies can be made. The strategies should be

more productive as compared to before because the market has changed so the ideas and

strategies should also be changed so the company can recover and gain growth.

raw material has increase, lack of availability of carriage inward, paying rent of factory, etc. has

increased cost of goods sold and it has impacted the profitability of the company.

The situation of company is not good as before, the company has low profitably, more cost of

goods sold, more expenses of transportation, low sales all the factors of income statement has

proved that the since 2009 period was better than 2020 covid period.

f) Account Receivable:

Due to covid 19 the debtors are also delaying paying the amount its making the company less

liquidate as compared to before, the company used to receive the more cash since 2009. 2020

situation has become worst as the company is unable to sell more goods and also collection

period has also increased as compare to before the company is trying to recover the losses which

it has bear in lock down. The lock down period was bad period for company because it has led

the company's position down as compare to before. The distribution area of sales has also

decreased because most of the people are scared to buy the products.

CONCLUSION

By summarizing report it can be articulated that accounting plays an important role in

decision making and provides information for evaluation of company's position and it also

provides information in journal entries , ledger, trial balance, and income statements and also

gives the accurate information so company can compare its position from past data and evaluate

the factors that need improvement for company growth and also shows the irrelevant factor

whose cost can be deducted to lower down the cost of production. Strategies can be made to

bring changes in cost of goods sale and sales strategies can be made. The strategies should be

more productive as compared to before because the market has changed so the ideas and

strategies should also be changed so the company can recover and gain growth.

REFERENCES

Books and Journals

B Romney, M., 2018. Accounting information systems. Pearson Education Limited.

Bagdasaryan, R., 2019. The Structure of the Trial Balance. In International Conference on

Integrated Science.–Springer, Cham (pp. 103-116).

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Jensen, T. and et.al., 2015. Fundamental accounting principles. W. Ross MacDonald School

Resource Services Library.

Russell, S., Milne, M. J. and Dey, C., 2017. Accounts of nature and the nature of

accounts. Accounting, Auditing & Accountability Journal.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Weigand, H., Blums, I. and de Kruijff, J., 2020. Shared Ledger Accounting—Implementing the

Economic Exchange pattern. Information Systems. 90. p.101437.

Books and Journals

B Romney, M., 2018. Accounting information systems. Pearson Education Limited.

Bagdasaryan, R., 2019. The Structure of the Trial Balance. In International Conference on

Integrated Science.–Springer, Cham (pp. 103-116).

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Jensen, T. and et.al., 2015. Fundamental accounting principles. W. Ross MacDonald School

Resource Services Library.

Russell, S., Milne, M. J. and Dey, C., 2017. Accounts of nature and the nature of

accounts. Accounting, Auditing & Accountability Journal.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Weigand, H., Blums, I. and de Kruijff, J., 2020. Shared Ledger Accounting—Implementing the

Economic Exchange pattern. Information Systems. 90. p.101437.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.