Financial and Management Accounting Report - Semester 1

VerifiedAdded on 2023/01/05

|18

|3258

|68

Report

AI Summary

This comprehensive accounting report delves into key concepts within financial and management accounting. It begins by explaining the books of prime entry, including sales day books, purchase day books, and the cash book, providing examples to illustrate their usage. The report then discusses essential accounting concepts such as trial balances and financial statements (income statement, balance sheet, and cash flow statement), highlighting the differences between financial and management accounting. It further examines the advantages and disadvantages of various business entities, including partnerships, corporations, sole proprietorships, cooperatives, and limited liability companies. Finally, the report explores the classification of costs and contrasts absorption costing with marginal costing approaches, offering a complete overview of critical accounting principles.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

ABSTRACT...............................................................................................................................3

INTRODUCTION......................................................................................................................4

MAIN BODY.............................................................................................................................4

1. Understanding the books of prime entry in details............................................................4

2. Discussing the accounting concepts...................................................................................6

3. Advantages and disadvantages of business entities.........................................................10

4. Classification of costs and the difference between absorption costing and marginal

costing approaches...............................................................................................................12

CONCLUSION AND RECOMMENDATIONS.....................................................................16

REFERENCES.........................................................................................................................17

ABSTRACT...............................................................................................................................3

INTRODUCTION......................................................................................................................4

MAIN BODY.............................................................................................................................4

1. Understanding the books of prime entry in details............................................................4

2. Discussing the accounting concepts...................................................................................6

3. Advantages and disadvantages of business entities.........................................................10

4. Classification of costs and the difference between absorption costing and marginal

costing approaches...............................................................................................................12

CONCLUSION AND RECOMMENDATIONS.....................................................................16

REFERENCES.........................................................................................................................17

ABSTRACT

This report is based on the accounting field which present about the key concepts in

relation to financial and management accounting. It covers the books of entries, accounting

terms, pros and cons of business entities and the various costing concepts.

This report is based on the accounting field which present about the key concepts in

relation to financial and management accounting. It covers the books of entries, accounting

terms, pros and cons of business entities and the various costing concepts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

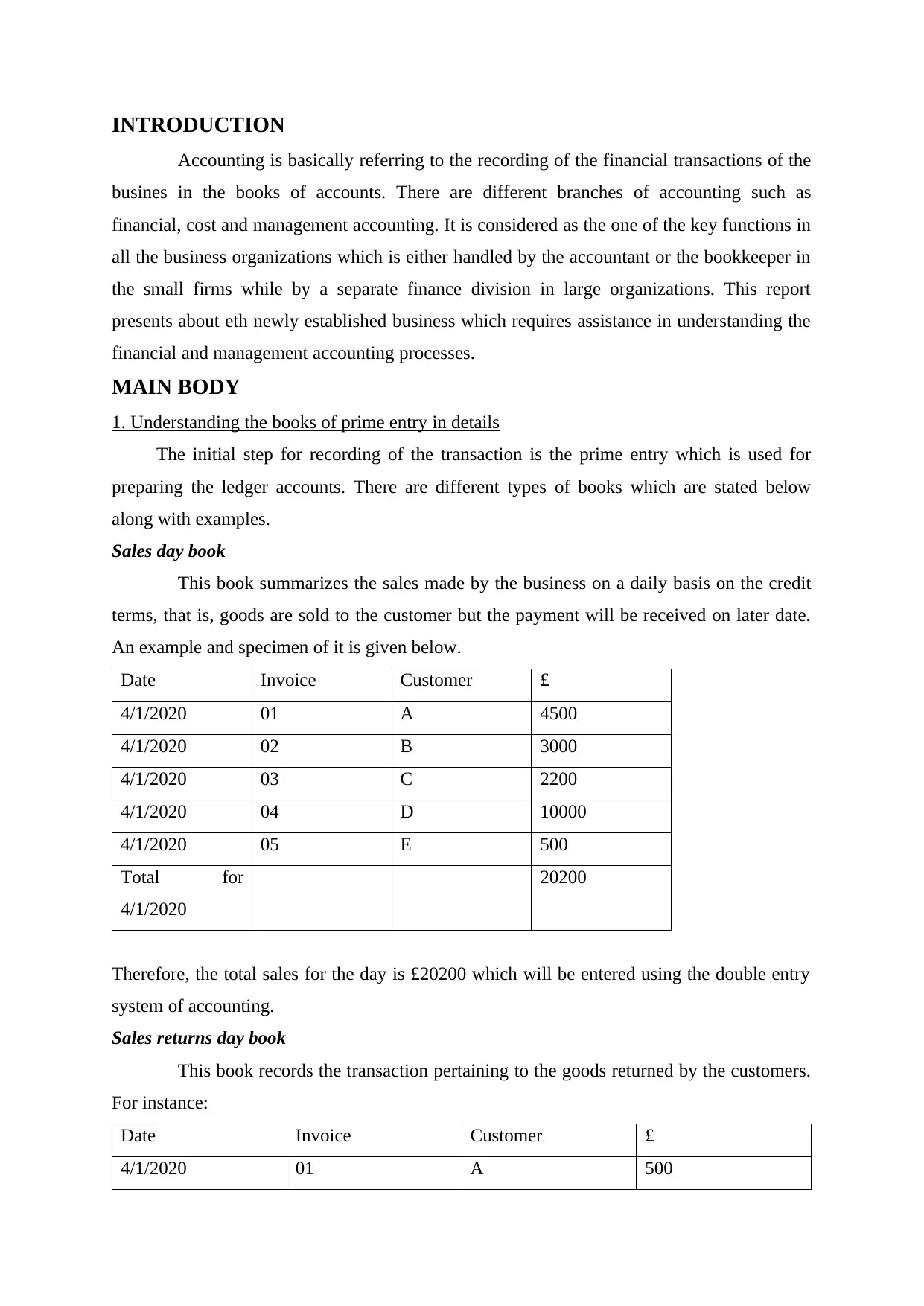

INTRODUCTION

Accounting is basically referring to the recording of the financial transactions of the

busines in the books of accounts. There are different branches of accounting such as

financial, cost and management accounting. It is considered as the one of the key functions in

all the business organizations which is either handled by the accountant or the bookkeeper in

the small firms while by a separate finance division in large organizations. This report

presents about eth newly established business which requires assistance in understanding the

financial and management accounting processes.

MAIN BODY

1. Understanding the books of prime entry in details

The initial step for recording of the transaction is the prime entry which is used for

preparing the ledger accounts. There are different types of books which are stated below

along with examples.

Sales day book

This book summarizes the sales made by the business on a daily basis on the credit

terms, that is, goods are sold to the customer but the payment will be received on later date.

An example and specimen of it is given below.

Date Invoice Customer £

4/1/2020 01 A 4500

4/1/2020 02 B 3000

4/1/2020 03 C 2200

4/1/2020 04 D 10000

4/1/2020 05 E 500

Total for

4/1/2020

20200

Therefore, the total sales for the day is £20200 which will be entered using the double entry

system of accounting.

Sales returns day book

This book records the transaction pertaining to the goods returned by the customers.

For instance:

Date Invoice Customer £

4/1/2020 01 A 500

Accounting is basically referring to the recording of the financial transactions of the

busines in the books of accounts. There are different branches of accounting such as

financial, cost and management accounting. It is considered as the one of the key functions in

all the business organizations which is either handled by the accountant or the bookkeeper in

the small firms while by a separate finance division in large organizations. This report

presents about eth newly established business which requires assistance in understanding the

financial and management accounting processes.

MAIN BODY

1. Understanding the books of prime entry in details

The initial step for recording of the transaction is the prime entry which is used for

preparing the ledger accounts. There are different types of books which are stated below

along with examples.

Sales day book

This book summarizes the sales made by the business on a daily basis on the credit

terms, that is, goods are sold to the customer but the payment will be received on later date.

An example and specimen of it is given below.

Date Invoice Customer £

4/1/2020 01 A 4500

4/1/2020 02 B 3000

4/1/2020 03 C 2200

4/1/2020 04 D 10000

4/1/2020 05 E 500

Total for

4/1/2020

20200

Therefore, the total sales for the day is £20200 which will be entered using the double entry

system of accounting.

Sales returns day book

This book records the transaction pertaining to the goods returned by the customers.

For instance:

Date Invoice Customer £

4/1/2020 01 A 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

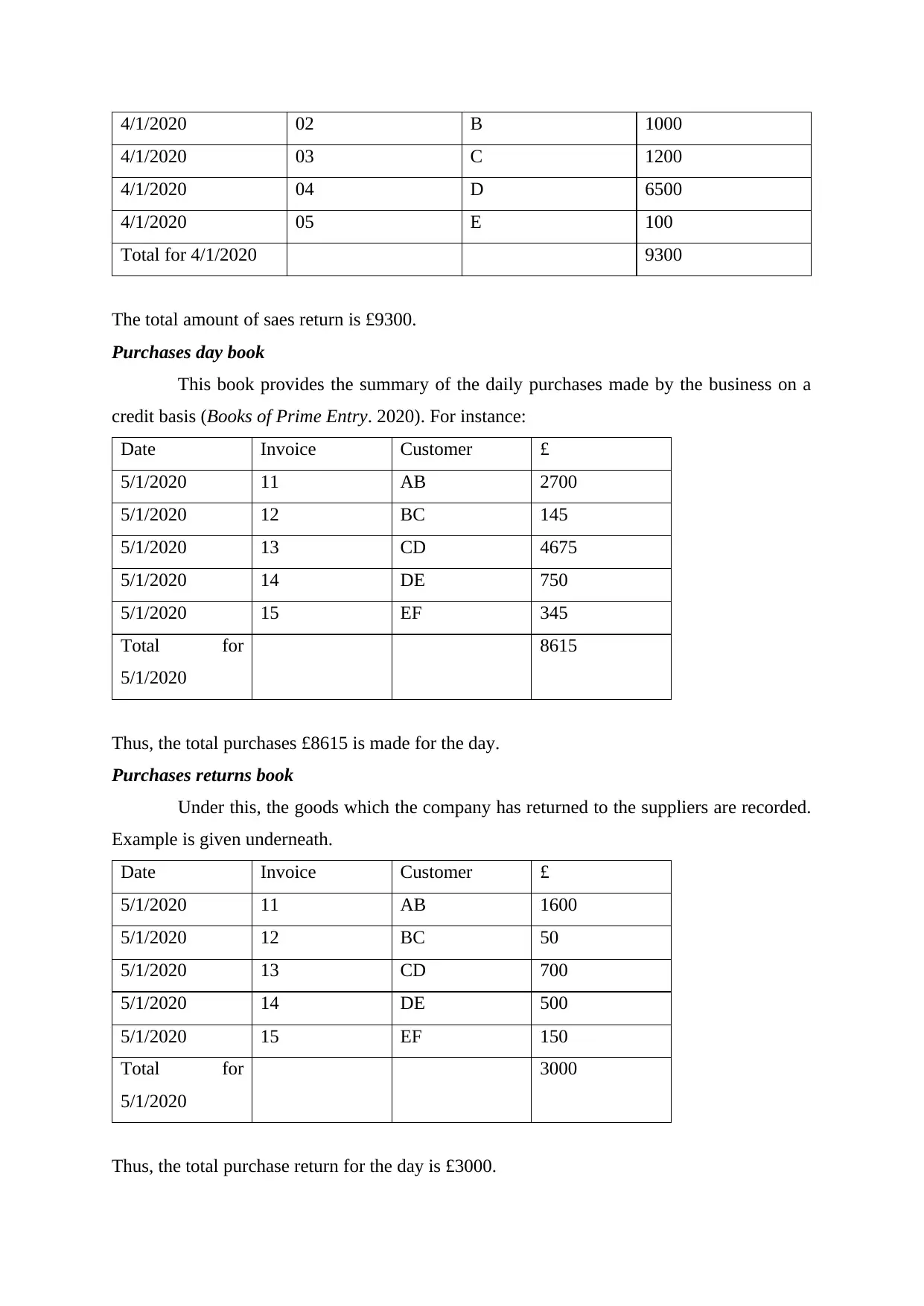

4/1/2020 02 B 1000

4/1/2020 03 C 1200

4/1/2020 04 D 6500

4/1/2020 05 E 100

Total for 4/1/2020 9300

The total amount of saes return is £9300.

Purchases day book

This book provides the summary of the daily purchases made by the business on a

credit basis (Books of Prime Entry. 2020). For instance:

Date Invoice Customer £

5/1/2020 11 AB 2700

5/1/2020 12 BC 145

5/1/2020 13 CD 4675

5/1/2020 14 DE 750

5/1/2020 15 EF 345

Total for

5/1/2020

8615

Thus, the total purchases £8615 is made for the day.

Purchases returns book

Under this, the goods which the company has returned to the suppliers are recorded.

Example is given underneath.

Date Invoice Customer £

5/1/2020 11 AB 1600

5/1/2020 12 BC 50

5/1/2020 13 CD 700

5/1/2020 14 DE 500

5/1/2020 15 EF 150

Total for

5/1/2020

3000

Thus, the total purchase return for the day is £3000.

4/1/2020 03 C 1200

4/1/2020 04 D 6500

4/1/2020 05 E 100

Total for 4/1/2020 9300

The total amount of saes return is £9300.

Purchases day book

This book provides the summary of the daily purchases made by the business on a

credit basis (Books of Prime Entry. 2020). For instance:

Date Invoice Customer £

5/1/2020 11 AB 2700

5/1/2020 12 BC 145

5/1/2020 13 CD 4675

5/1/2020 14 DE 750

5/1/2020 15 EF 345

Total for

5/1/2020

8615

Thus, the total purchases £8615 is made for the day.

Purchases returns book

Under this, the goods which the company has returned to the suppliers are recorded.

Example is given underneath.

Date Invoice Customer £

5/1/2020 11 AB 1600

5/1/2020 12 BC 50

5/1/2020 13 CD 700

5/1/2020 14 DE 500

5/1/2020 15 EF 150

Total for

5/1/2020

3000

Thus, the total purchase return for the day is £3000.

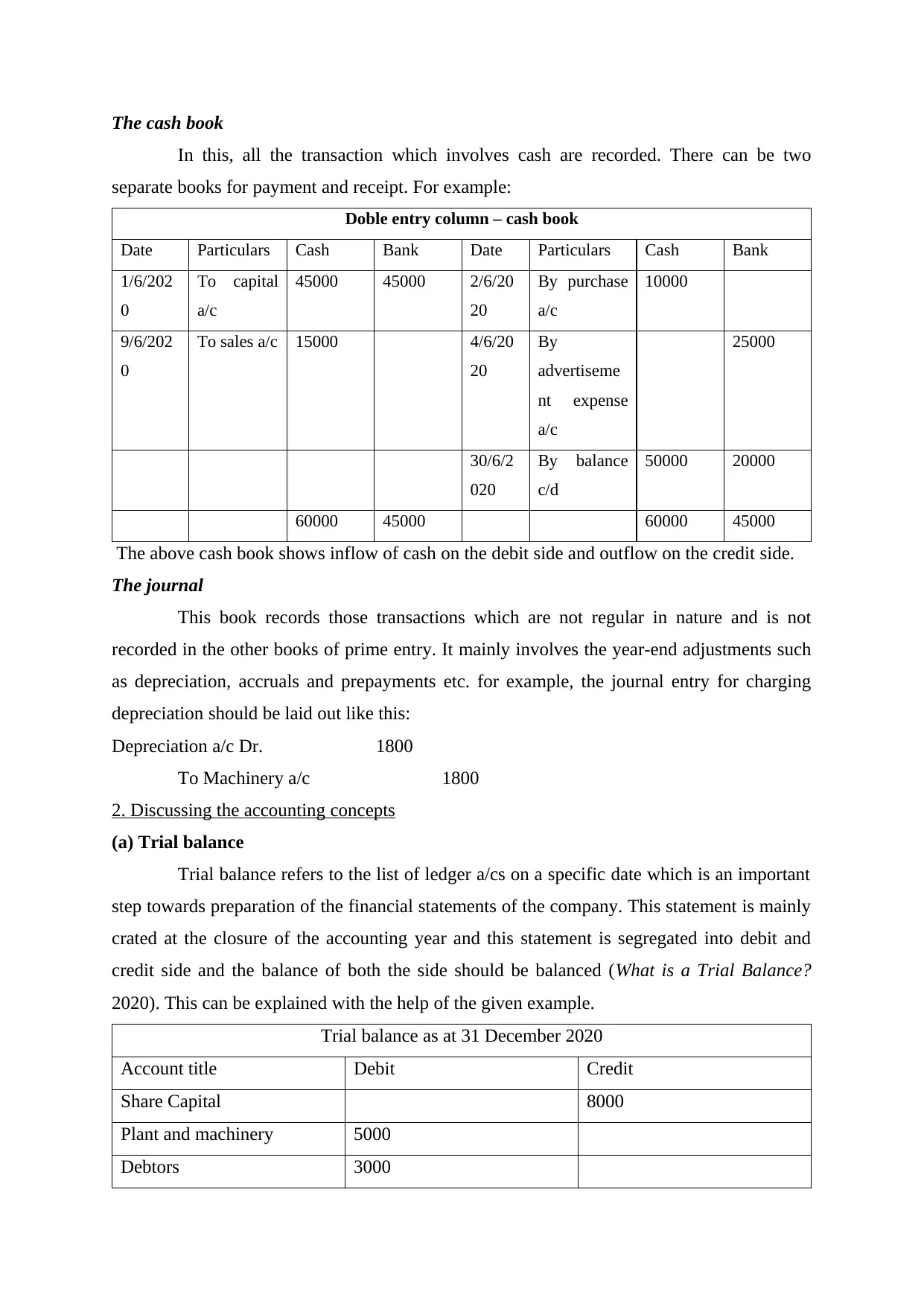

The cash book

In this, all the transaction which involves cash are recorded. There can be two

separate books for payment and receipt. For example:

Doble entry column – cash book

Date Particulars Cash Bank Date Particulars Cash Bank

1/6/202

0

To capital

a/c

45000 45000 2/6/20

20

By purchase

a/c

10000

9/6/202

0

To sales a/c 15000 4/6/20

20

By

advertiseme

nt expense

a/c

25000

30/6/2

020

By balance

c/d

50000 20000

60000 45000 60000 45000

The above cash book shows inflow of cash on the debit side and outflow on the credit side.

The journal

This book records those transactions which are not regular in nature and is not

recorded in the other books of prime entry. It mainly involves the year-end adjustments such

as depreciation, accruals and prepayments etc. for example, the journal entry for charging

depreciation should be laid out like this:

Depreciation a/c Dr. 1800

To Machinery a/c 1800

2. Discussing the accounting concepts

(a) Trial balance

Trial balance refers to the list of ledger a/cs on a specific date which is an important

step towards preparation of the financial statements of the company. This statement is mainly

crated at the closure of the accounting year and this statement is segregated into debit and

credit side and the balance of both the side should be balanced (What is a Trial Balance?

2020). This can be explained with the help of the given example.

Trial balance as at 31 December 2020

Account title Debit Credit

Share Capital 8000

Plant and machinery 5000

Debtors 3000

In this, all the transaction which involves cash are recorded. There can be two

separate books for payment and receipt. For example:

Doble entry column – cash book

Date Particulars Cash Bank Date Particulars Cash Bank

1/6/202

0

To capital

a/c

45000 45000 2/6/20

20

By purchase

a/c

10000

9/6/202

0

To sales a/c 15000 4/6/20

20

By

advertiseme

nt expense

a/c

25000

30/6/2

020

By balance

c/d

50000 20000

60000 45000 60000 45000

The above cash book shows inflow of cash on the debit side and outflow on the credit side.

The journal

This book records those transactions which are not regular in nature and is not

recorded in the other books of prime entry. It mainly involves the year-end adjustments such

as depreciation, accruals and prepayments etc. for example, the journal entry for charging

depreciation should be laid out like this:

Depreciation a/c Dr. 1800

To Machinery a/c 1800

2. Discussing the accounting concepts

(a) Trial balance

Trial balance refers to the list of ledger a/cs on a specific date which is an important

step towards preparation of the financial statements of the company. This statement is mainly

crated at the closure of the accounting year and this statement is segregated into debit and

credit side and the balance of both the side should be balanced (What is a Trial Balance?

2020). This can be explained with the help of the given example.

Trial balance as at 31 December 2020

Account title Debit Credit

Share Capital 8000

Plant and machinery 5000

Debtors 3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

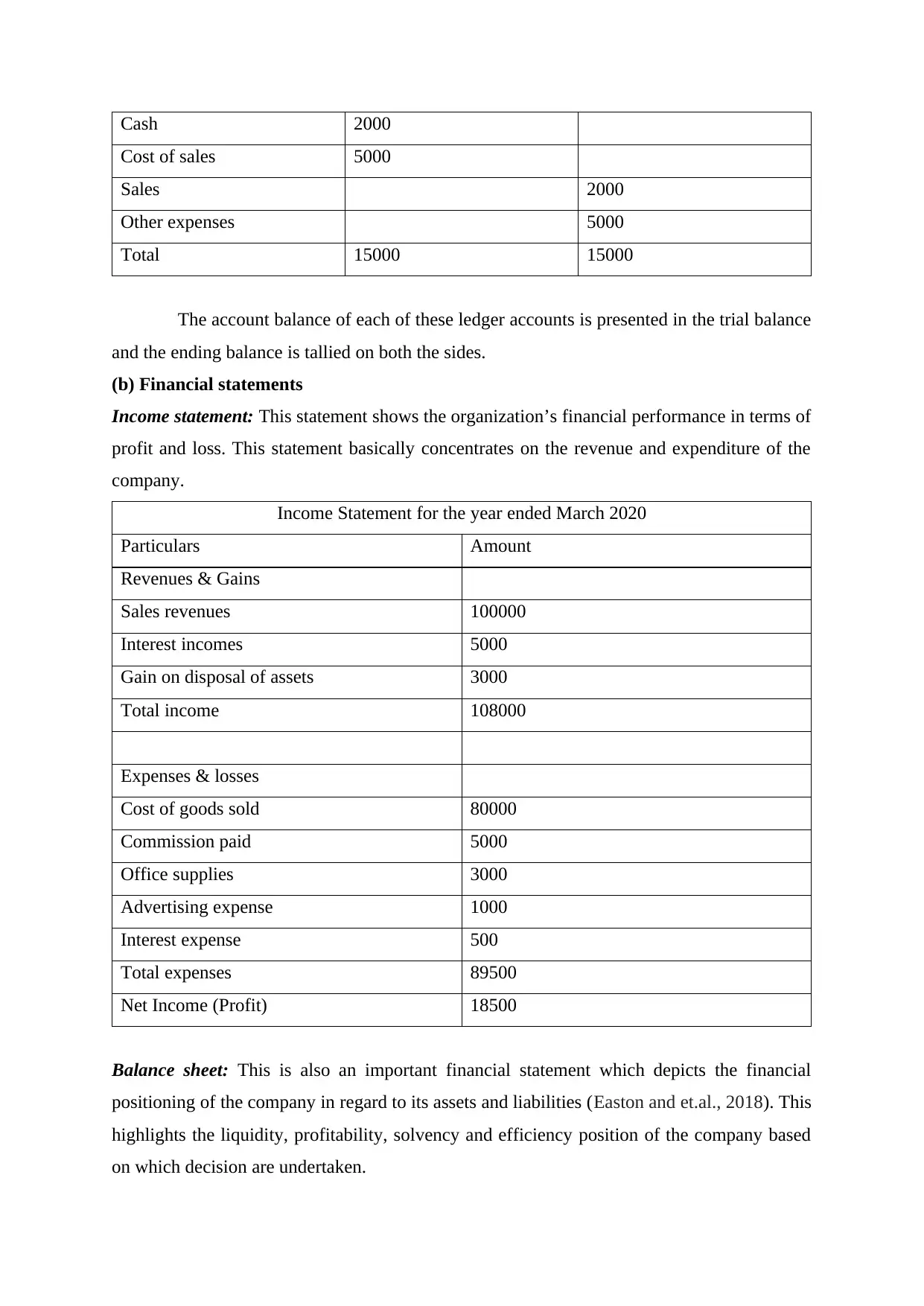

Cash 2000

Cost of sales 5000

Sales 2000

Other expenses 5000

Total 15000 15000

The account balance of each of these ledger accounts is presented in the trial balance

and the ending balance is tallied on both the sides.

(b) Financial statements

Income statement: This statement shows the organization’s financial performance in terms of

profit and loss. This statement basically concentrates on the revenue and expenditure of the

company.

Income Statement for the year ended March 2020

Particulars Amount

Revenues & Gains

Sales revenues 100000

Interest incomes 5000

Gain on disposal of assets 3000

Total income 108000

Expenses & losses

Cost of goods sold 80000

Commission paid 5000

Office supplies 3000

Advertising expense 1000

Interest expense 500

Total expenses 89500

Net Income (Profit) 18500

Balance sheet: This is also an important financial statement which depicts the financial

positioning of the company in regard to its assets and liabilities (Easton and et.al., 2018). This

highlights the liquidity, profitability, solvency and efficiency position of the company based

on which decision are undertaken.

Cost of sales 5000

Sales 2000

Other expenses 5000

Total 15000 15000

The account balance of each of these ledger accounts is presented in the trial balance

and the ending balance is tallied on both the sides.

(b) Financial statements

Income statement: This statement shows the organization’s financial performance in terms of

profit and loss. This statement basically concentrates on the revenue and expenditure of the

company.

Income Statement for the year ended March 2020

Particulars Amount

Revenues & Gains

Sales revenues 100000

Interest incomes 5000

Gain on disposal of assets 3000

Total income 108000

Expenses & losses

Cost of goods sold 80000

Commission paid 5000

Office supplies 3000

Advertising expense 1000

Interest expense 500

Total expenses 89500

Net Income (Profit) 18500

Balance sheet: This is also an important financial statement which depicts the financial

positioning of the company in regard to its assets and liabilities (Easton and et.al., 2018). This

highlights the liquidity, profitability, solvency and efficiency position of the company based

on which decision are undertaken.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

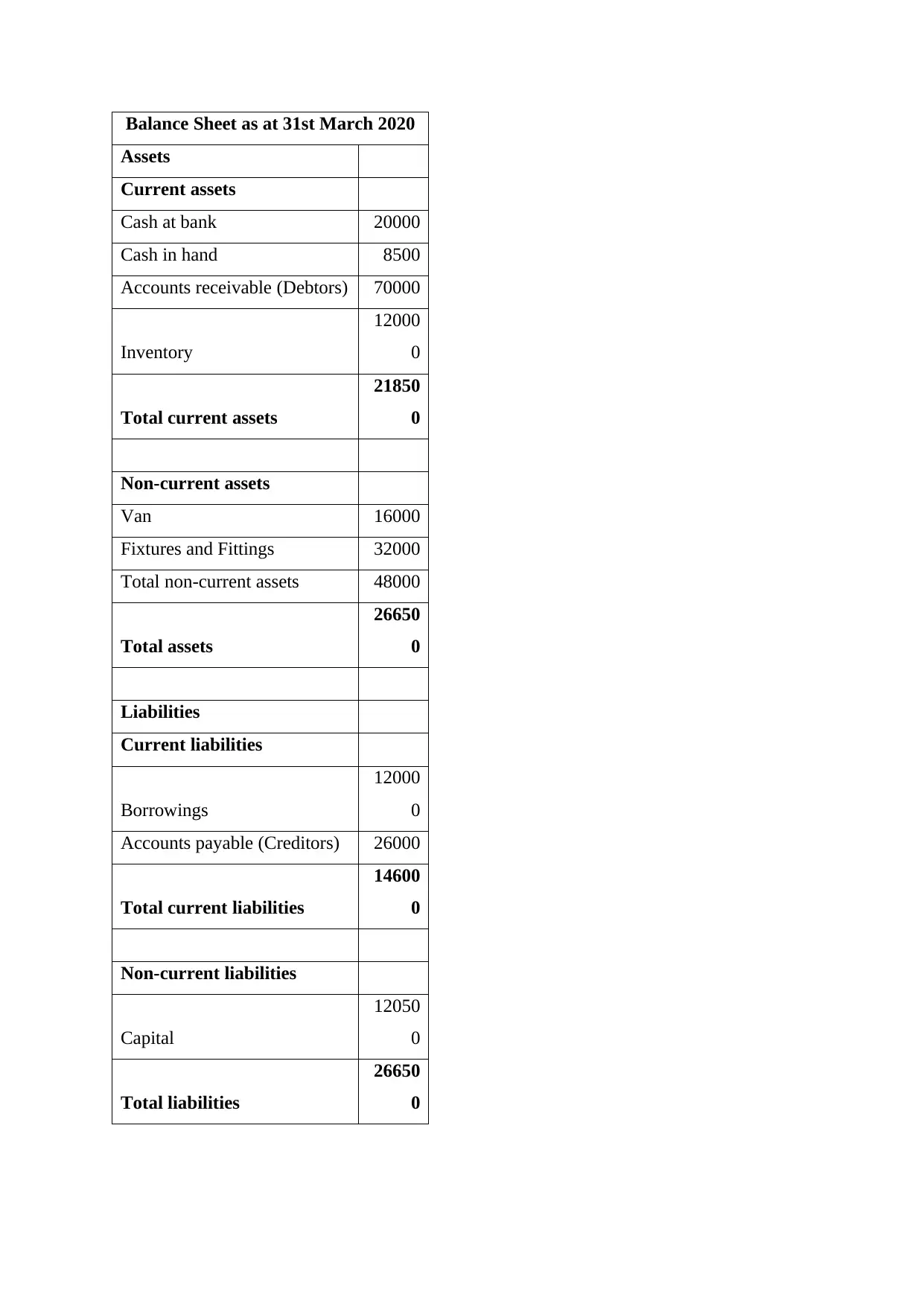

Balance Sheet as at 31st March 2020

Assets

Current assets

Cash at bank 20000

Cash in hand 8500

Accounts receivable (Debtors) 70000

Inventory

12000

0

Total current assets

21850

0

Non-current assets

Van 16000

Fixtures and Fittings 32000

Total non-current assets 48000

Total assets

26650

0

Liabilities

Current liabilities

Borrowings

12000

0

Accounts payable (Creditors) 26000

Total current liabilities

14600

0

Non-current liabilities

Capital

12050

0

Total liabilities

26650

0

Assets

Current assets

Cash at bank 20000

Cash in hand 8500

Accounts receivable (Debtors) 70000

Inventory

12000

0

Total current assets

21850

0

Non-current assets

Van 16000

Fixtures and Fittings 32000

Total non-current assets 48000

Total assets

26650

0

Liabilities

Current liabilities

Borrowings

12000

0

Accounts payable (Creditors) 26000

Total current liabilities

14600

0

Non-current liabilities

Capital

12050

0

Total liabilities

26650

0

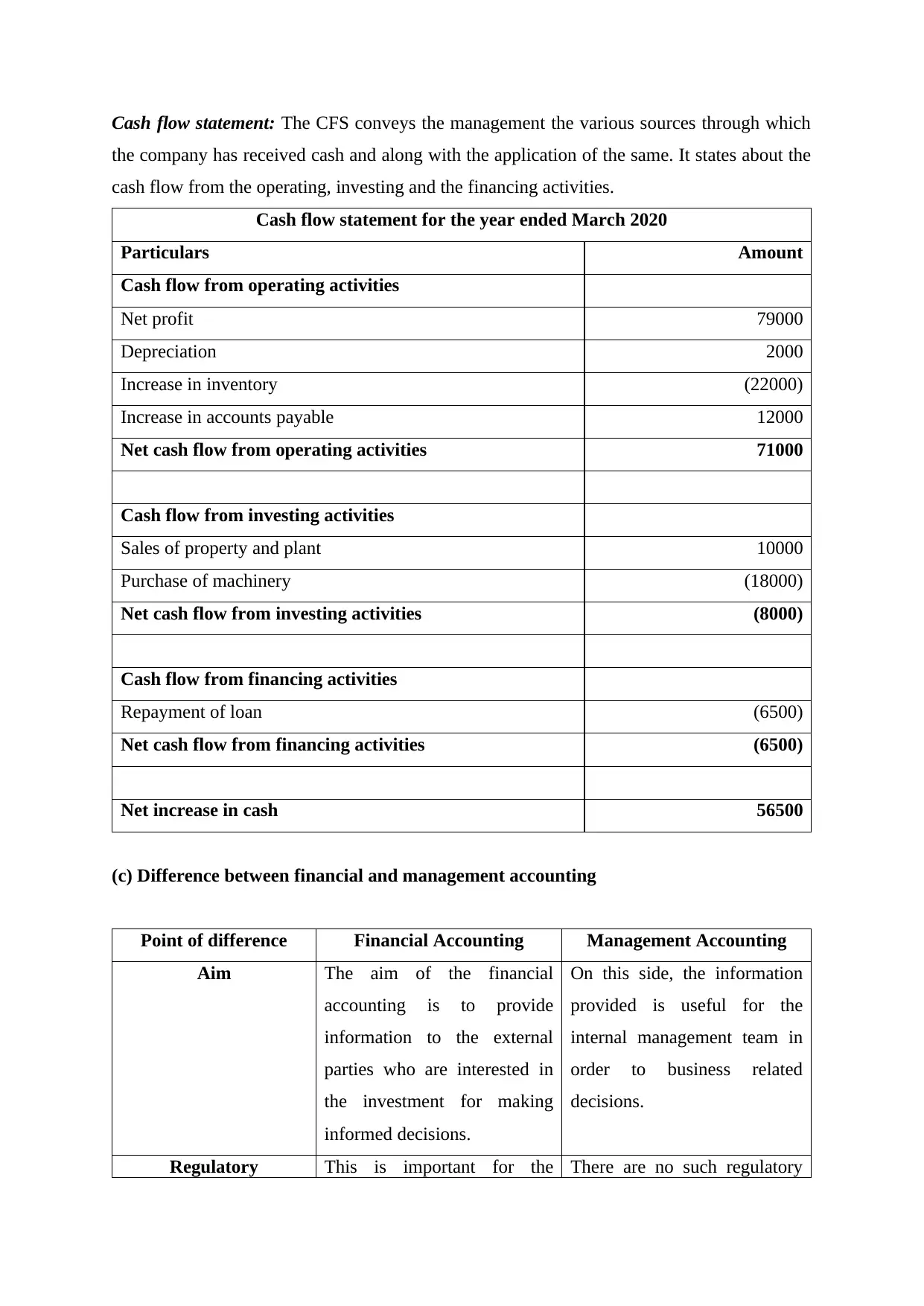

Cash flow statement: The CFS conveys the management the various sources through which

the company has received cash and along with the application of the same. It states about the

cash flow from the operating, investing and the financing activities.

Cash flow statement for the year ended March 2020

Particulars Amount

Cash flow from operating activities

Net profit 79000

Depreciation 2000

Increase in inventory (22000)

Increase in accounts payable 12000

Net cash flow from operating activities 71000

Cash flow from investing activities

Sales of property and plant 10000

Purchase of machinery (18000)

Net cash flow from investing activities (8000)

Cash flow from financing activities

Repayment of loan (6500)

Net cash flow from financing activities (6500)

Net increase in cash 56500

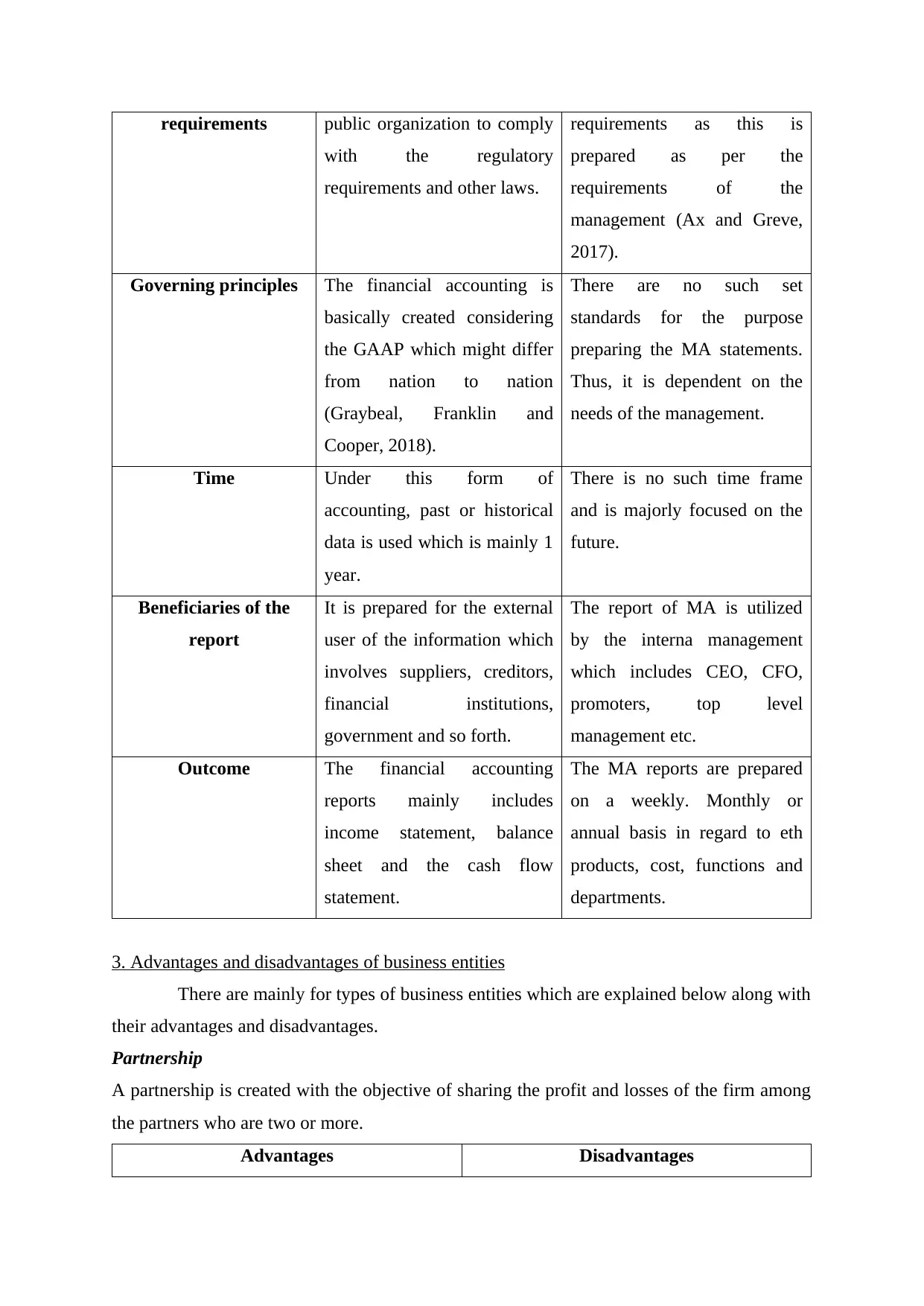

(c) Difference between financial and management accounting

Point of difference Financial Accounting Management Accounting

Aim The aim of the financial

accounting is to provide

information to the external

parties who are interested in

the investment for making

informed decisions.

On this side, the information

provided is useful for the

internal management team in

order to business related

decisions.

Regulatory This is important for the There are no such regulatory

the company has received cash and along with the application of the same. It states about the

cash flow from the operating, investing and the financing activities.

Cash flow statement for the year ended March 2020

Particulars Amount

Cash flow from operating activities

Net profit 79000

Depreciation 2000

Increase in inventory (22000)

Increase in accounts payable 12000

Net cash flow from operating activities 71000

Cash flow from investing activities

Sales of property and plant 10000

Purchase of machinery (18000)

Net cash flow from investing activities (8000)

Cash flow from financing activities

Repayment of loan (6500)

Net cash flow from financing activities (6500)

Net increase in cash 56500

(c) Difference between financial and management accounting

Point of difference Financial Accounting Management Accounting

Aim The aim of the financial

accounting is to provide

information to the external

parties who are interested in

the investment for making

informed decisions.

On this side, the information

provided is useful for the

internal management team in

order to business related

decisions.

Regulatory This is important for the There are no such regulatory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

requirements public organization to comply

with the regulatory

requirements and other laws.

requirements as this is

prepared as per the

requirements of the

management (Ax and Greve,

2017).

Governing principles The financial accounting is

basically created considering

the GAAP which might differ

from nation to nation

(Graybeal, Franklin and

Cooper, 2018).

There are no such set

standards for the purpose

preparing the MA statements.

Thus, it is dependent on the

needs of the management.

Time Under this form of

accounting, past or historical

data is used which is mainly 1

year.

There is no such time frame

and is majorly focused on the

future.

Beneficiaries of the

report

It is prepared for the external

user of the information which

involves suppliers, creditors,

financial institutions,

government and so forth.

The report of MA is utilized

by the interna management

which includes CEO, CFO,

promoters, top level

management etc.

Outcome The financial accounting

reports mainly includes

income statement, balance

sheet and the cash flow

statement.

The MA reports are prepared

on a weekly. Monthly or

annual basis in regard to eth

products, cost, functions and

departments.

3. Advantages and disadvantages of business entities

There are mainly for types of business entities which are explained below along with

their advantages and disadvantages.

Partnership

A partnership is created with the objective of sharing the profit and losses of the firm among

the partners who are two or more.

Advantages Disadvantages

with the regulatory

requirements and other laws.

requirements as this is

prepared as per the

requirements of the

management (Ax and Greve,

2017).

Governing principles The financial accounting is

basically created considering

the GAAP which might differ

from nation to nation

(Graybeal, Franklin and

Cooper, 2018).

There are no such set

standards for the purpose

preparing the MA statements.

Thus, it is dependent on the

needs of the management.

Time Under this form of

accounting, past or historical

data is used which is mainly 1

year.

There is no such time frame

and is majorly focused on the

future.

Beneficiaries of the

report

It is prepared for the external

user of the information which

involves suppliers, creditors,

financial institutions,

government and so forth.

The report of MA is utilized

by the interna management

which includes CEO, CFO,

promoters, top level

management etc.

Outcome The financial accounting

reports mainly includes

income statement, balance

sheet and the cash flow

statement.

The MA reports are prepared

on a weekly. Monthly or

annual basis in regard to eth

products, cost, functions and

departments.

3. Advantages and disadvantages of business entities

There are mainly for types of business entities which are explained below along with

their advantages and disadvantages.

Partnership

A partnership is created with the objective of sharing the profit and losses of the firm among

the partners who are two or more.

Advantages Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is very easy to establish as it

requires very less paper work and

other documents.

Can take the advantage of competent

skills of each of the partner for

attaining goals and objectives.

The responsibility is shared among

the partners in respect to the

partnership deed after receiving the

consent of all the partners.

There are chances of disagreement

among the partners in terms of

decision making.

Situation where there is no

agreement, it might result into

halting of the business because of

disagreement among the partners.

Partners are personally liable for

paying off the business debts and

can be sued.

Corporation

A corporation acts as a separate entity apart from its shareholders.

Advantages Disadvantages

Normally, the shareholders of the

corporation ae not liable for the

debts.

Corporation can avail deduction of

eth expenses such as health

insurance premium, equipment etc

(Types of Business Organizations –

Advantages and Disadvantages.

2019).

For the purpose of raining money,

corporation can sell the stocks.

The corporation is required to pay

tax before distributing profits to

shareholders and then shareholders

pays the tax on an individual level.

It involves a huge amount of

paperwork.

Under the situation of several

investors and no clarity about the

majority of interest, the management

team may manage the operation

instead of owner.

Sole proprietorship

Under this, there is only one owner and there is not difference between owner and the

business.

Advantages Disadvantages

Owner can exercise full control over

the business activities.

There is no requirement for making

The liability of the sole proprietor is

unlimited and thus, private assets of

the owner can be used to pay off the

requires very less paper work and

other documents.

Can take the advantage of competent

skills of each of the partner for

attaining goals and objectives.

The responsibility is shared among

the partners in respect to the

partnership deed after receiving the

consent of all the partners.

There are chances of disagreement

among the partners in terms of

decision making.

Situation where there is no

agreement, it might result into

halting of the business because of

disagreement among the partners.

Partners are personally liable for

paying off the business debts and

can be sued.

Corporation

A corporation acts as a separate entity apart from its shareholders.

Advantages Disadvantages

Normally, the shareholders of the

corporation ae not liable for the

debts.

Corporation can avail deduction of

eth expenses such as health

insurance premium, equipment etc

(Types of Business Organizations –

Advantages and Disadvantages.

2019).

For the purpose of raining money,

corporation can sell the stocks.

The corporation is required to pay

tax before distributing profits to

shareholders and then shareholders

pays the tax on an individual level.

It involves a huge amount of

paperwork.

Under the situation of several

investors and no clarity about the

majority of interest, the management

team may manage the operation

instead of owner.

Sole proprietorship

Under this, there is only one owner and there is not difference between owner and the

business.

Advantages Disadvantages

Owner can exercise full control over

the business activities.

There is no requirement for making

The liability of the sole proprietor is

unlimited and thus, private assets of

the owner can be used to pay off the

public disclosure of financial

activities like publishing financial

statements.

There is very less cost attached to

the formation of the sole proprietor

business along with less

documentation.

debts of the business.

Lack of proper structure pertaining

to managing of the financial records

might result into risk of

inappropriate management of

money.

It might face difficulty in raising

funds.

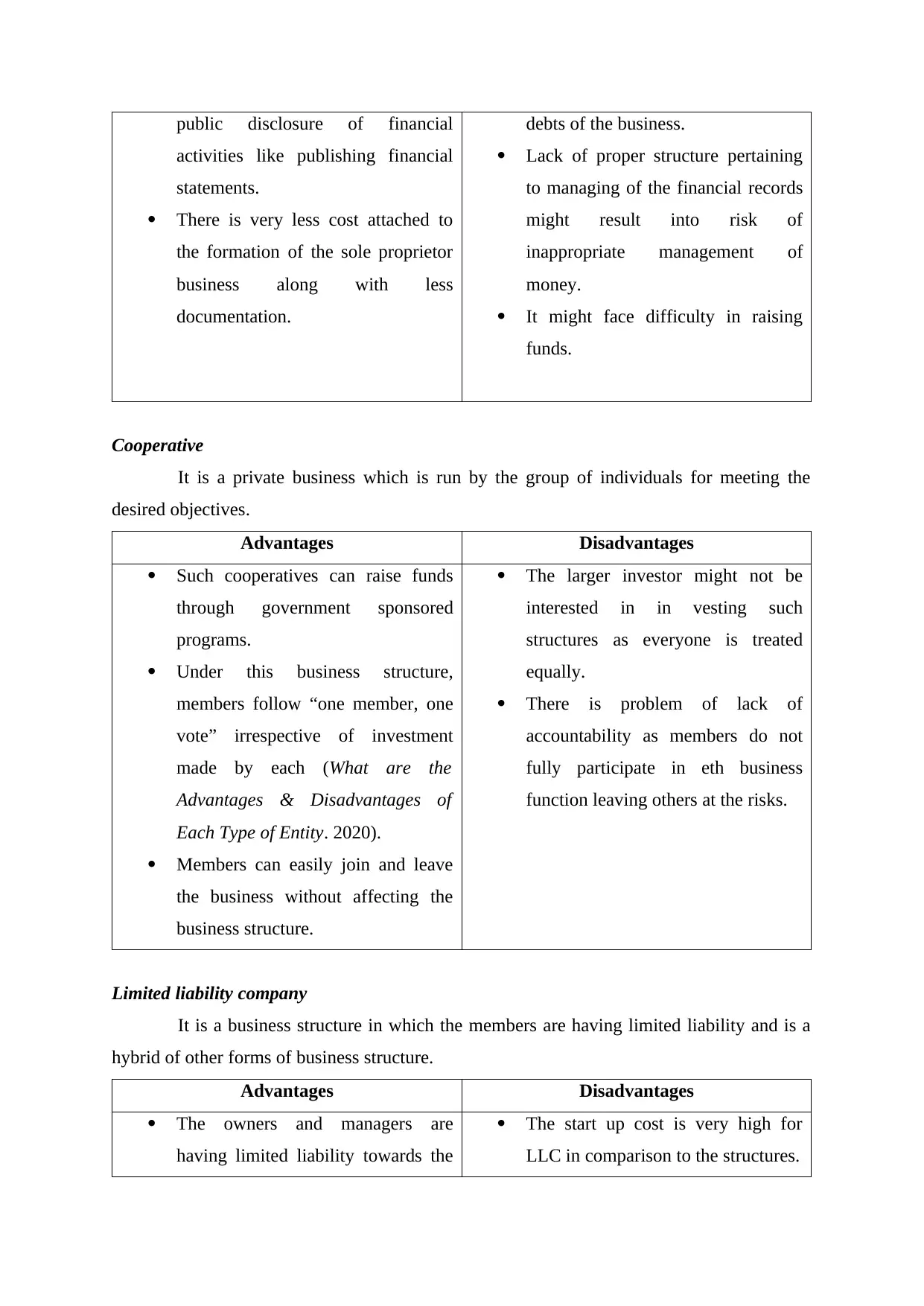

Cooperative

It is a private business which is run by the group of individuals for meeting the

desired objectives.

Advantages Disadvantages

Such cooperatives can raise funds

through government sponsored

programs.

Under this business structure,

members follow “one member, one

vote” irrespective of investment

made by each (What are the

Advantages & Disadvantages of

Each Type of Entity. 2020).

Members can easily join and leave

the business without affecting the

business structure.

The larger investor might not be

interested in in vesting such

structures as everyone is treated

equally.

There is problem of lack of

accountability as members do not

fully participate in eth business

function leaving others at the risks.

Limited liability company

It is a business structure in which the members are having limited liability and is a

hybrid of other forms of business structure.

Advantages Disadvantages

The owners and managers are

having limited liability towards the

The start up cost is very high for

LLC in comparison to the structures.

activities like publishing financial

statements.

There is very less cost attached to

the formation of the sole proprietor

business along with less

documentation.

debts of the business.

Lack of proper structure pertaining

to managing of the financial records

might result into risk of

inappropriate management of

money.

It might face difficulty in raising

funds.

Cooperative

It is a private business which is run by the group of individuals for meeting the

desired objectives.

Advantages Disadvantages

Such cooperatives can raise funds

through government sponsored

programs.

Under this business structure,

members follow “one member, one

vote” irrespective of investment

made by each (What are the

Advantages & Disadvantages of

Each Type of Entity. 2020).

Members can easily join and leave

the business without affecting the

business structure.

The larger investor might not be

interested in in vesting such

structures as everyone is treated

equally.

There is problem of lack of

accountability as members do not

fully participate in eth business

function leaving others at the risks.

Limited liability company

It is a business structure in which the members are having limited liability and is a

hybrid of other forms of business structure.

Advantages Disadvantages

The owners and managers are

having limited liability towards the

The start up cost is very high for

LLC in comparison to the structures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.