HI6025 Accounting theory and current issues | Coca Cola Assignment

Added on 2019-11-14

17 Pages4212 Words285 Views

Running head: ACCOUNTING PHENOMENA- COCA COLA AMATIL 1Accounting Phenomena- Coca Cola Amatil Limited CompanyNameInstitution

ACCOUNTING PHENOMENA- COCA COLA AMATIL 2Accounting Phenomena- Coca-Cola AmatilThe primary purpose of the paper is to evaluate accounting quality for Coca-Cola Amatil through accessing its accounting policies as well as estimates and also preparing an in-depth report on managers’ accounting and reporting strategy choice. The report has been formulated bythe ASX Listing Rule of 4.2A. 3. Coca-cola Amatil is operational in six countries, that is: New Zealand, Australia, Samoa, Fiji, Papua New Guinea and Indonesia. The company positioned as amoung the best and principal manufacturers, and most competitive suppliers of ready to drink alcohol as well as non-alcoholic beverages is an important institution in the Asia Pacific regions. Coca-Cola owns the brands and manufacturers the concentrates of several non-alcoholic beverages that are locally manufactured by Amatil. Subsequently, this is an inclusion of Coca-Cola, Fanta, Powerade, and Sprite. Coca-Cola Amatil directly employs a rough estimation of over 14000 people as well as indirectly offer jobs to so many other individuals (Abwanzo, 2016). The supply chain in the company’s operation is comprised of partnerships with the principal suppliers that work in manufacturing, packaging, and selling as well as distributing the vast range of products. Accounting policies are general principles, rules, and procedures that are implemented by a company’s core management team and is used in the preparation of the company’s financial statement. The process comprises of any methods, measurement systems as well as the procedureinvolved in presenting disclosures. The following section will extensively examine accounting policies and estimates used by CCA and a comparison of accounting policies and estimations used by its prime competitors.Segment Reporting

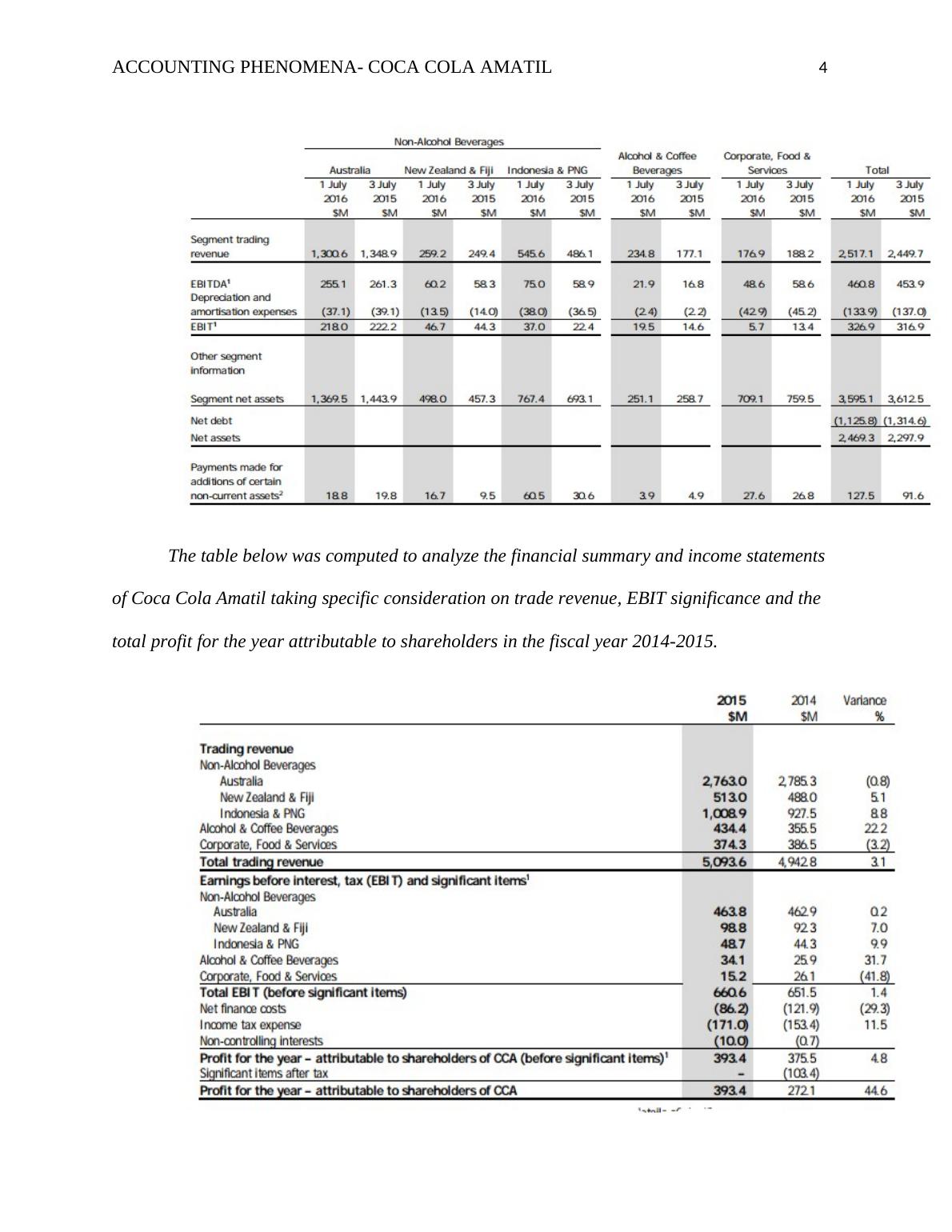

ACCOUNTING PHENOMENA- COCA COLA AMATIL 3The company operates in several segments which are grounded on results conveyed to the managing director of the group. Technically, the New Zealand and Fiji, Australia, and Indonesia, as well as PNG Non-Alcoholic Beverage segments, obtain their revenues from manufactures as well as marketing of some of the non-alcoholic beverages. Relatively, the financial statement of the group is seasonally affected by the timing of certain festivities in the respective countries most specifically within the CCA operational zones. The average trend is that revenue earnings and operating cash flows of CCA and the New Zealand based one are stronger in the second half of the financial year (Chance, 2017). This is attributed to the fact that the Christmas holiday is a trading period which automatically leads to associated effects on the working capital components. Also, the Ramadan period just like Christmas impacts the general timing of the Indonesian market within the financial year. The results in segment criteria are based on remunerations before interest and substantial item basis. The net segment assets comprise of assets in operating and investing assets as well as the liabilities involved. However, this is exclusive of amounts in net debt. Net debt amounts are comprised of long-term deposits, cash assets and debt-related assets as well as legal liabilities. The net debts, income taxes, and net finance costs are handled at a group level and hence not reported internally specifically as a segmented level. The table below is a segment report based on the year 2015-2016. The table also takes into account net debts and assets for all subsidiaries of Coca Cola Amatil and the potential impact the statistics has on profitability

ACCOUNTING PHENOMENA- COCA COLA AMATIL 4The table below was computed to analyze the financial summary and income statements of Coca Cola Amatil taking specific consideration on trade revenue, EBIT significance and the total profit for the year attributable to shareholders in the fiscal year 2014-2015.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Analysis of Coca-Cola Amatil Limitedlg...

|12

|2523

|66

Financial Statements of Coca Cola Assignmentlg...

|12

|3117

|105

Analysis and Evaluation of Coca-Cola Amatil Limitedlg...

|17

|4240

|460

Analysis of the Coca-cola Amatil Limited Annual Reportlg...

|9

|1491

|19

Accounting System and Processes PowerPoint Presentation 2022lg...

|19

|1374

|14

Marketing Management: Segmentation, Targeting and Positioning Strategies of Coca Cola Amatillg...

|14

|3591

|91