Accounting Principles, Financial Statements, and Ratio Analysis Report

VerifiedAdded on 2023/06/04

|14

|3996

|149

Report

AI Summary

This report provides a comprehensive overview of accounting principles, focusing on their application within a business context. It begins by analyzing the accounting function within an enterprise, emphasizing its role in identifying, recording, and assessing financial transactions. The report then evaluates regulatory and ethical constraints, followed by the preparation of financial statements, including an income statement and balance sheet for the Village-Wide Catering Company. The report explores the differences between sole traders, partnerships, and companies. Furthermore, it delves into financial ratio analysis, calculating and interpreting profitability, liquidity, investment, and asset usage ratios. The limitations of financial ratios are also discussed. A cash budget for the company is presented, and the benefits and limitations of budgets and budgetary planning are evaluated. The report concludes with an overview of the key concepts and findings.

5 – Accounting

principles

principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Analysis the accounting function within an enterprises..........................................................3

2. Evaluate the regulatory and ethical constraints within the organisation.................................4

3.From a given trail balance preparation of financial statements...............................................5

a) Income statement of Village- wide catering Company for the year ended 30th June 2022. .5

b) Difference between sole traders, partnership firm and company...........................................6

4. Present and calculate the financial ratios................................................................................7

a) calculate the financial ratios of the company..........................................................................7

b) Limitation of financial ratios..................................................................................................9

5. Evaluate the financial performance by using financial ratios................................................9

6. Cash budget...........................................................................................................................10

a) Cash Budget of the Village – Wide catering company.........................................................10

7.Discuss the benefits and limitations of budgets and budgetary planning and control of an

organisation. .............................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Analysis the accounting function within an enterprises..........................................................3

2. Evaluate the regulatory and ethical constraints within the organisation.................................4

3.From a given trail balance preparation of financial statements...............................................5

a) Income statement of Village- wide catering Company for the year ended 30th June 2022. .5

b) Difference between sole traders, partnership firm and company...........................................6

4. Present and calculate the financial ratios................................................................................7

a) calculate the financial ratios of the company..........................................................................7

b) Limitation of financial ratios..................................................................................................9

5. Evaluate the financial performance by using financial ratios................................................9

6. Cash budget...........................................................................................................................10

a) Cash Budget of the Village – Wide catering company.........................................................10

7.Discuss the benefits and limitations of budgets and budgetary planning and control of an

organisation. .............................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting principles mean those guidelines that are followed by company to prepare

and presentation of financial statements. It is also known as Generally Accepted Accounting

Principles. It is needed because it brings consistency in the financial statements. It should be

simple and easy understandable that the investors can understand the financial statements.

Accounting concepts and accounting conventions are included in accounting principles. There

are many accounting concepts that are needed to follow by the company such as entity business

concept, principle of going concern and money measurement principle (Aggarwal, 2022). This

report includes, the concept and scope of accounting principles of Moore Kingston Smith that is

situated in UK. They provide various activities of their clients such as finance, audit and tax.

Further this report includes preparation and presentation of financial statements for

unincorporated business and advantages and disadvantages of budgetary control. With the help

of Financial ratios company evaluates the financial performance

MAIN BODY

1. Analysis the accounting function within an enterprises

Accounting functions are the set of the financial activities which helps in identifying, assessing

and recording the transactions that are in the financial form. The prime objective of accounting

function is to maintain the records and the book keeping. It helps in the collection and storing of

the information that are related to the activities which are in the financial terms. It helps in

creation and keeping the accounts from the day company was incorporated to the current day.

This is to reconcile the information from the various sources. It also helps in projecting the future

financial requirement and the formation of the budgets. The financial statement provides the

information about the profit and loss incurred during the year. It shows the income statement of

the concerned period. It helps in keeping the track records of the expenses, profit margin and the

debts. It ensures the compliance of the statutory regulations and rules. The accountant assures

that the various taxes, claims, salaries, dividends, interests, depreciation, etc. are calculated

according to the laws. This accounting is used for both internal as well as external purpose. It

clears the company about its productivity, profitability, sustainability and monitoring its growth

in the next year (Azretbergenova, 2021). It analyses the trends followed by the organisations in

Accounting principles mean those guidelines that are followed by company to prepare

and presentation of financial statements. It is also known as Generally Accepted Accounting

Principles. It is needed because it brings consistency in the financial statements. It should be

simple and easy understandable that the investors can understand the financial statements.

Accounting concepts and accounting conventions are included in accounting principles. There

are many accounting concepts that are needed to follow by the company such as entity business

concept, principle of going concern and money measurement principle (Aggarwal, 2022). This

report includes, the concept and scope of accounting principles of Moore Kingston Smith that is

situated in UK. They provide various activities of their clients such as finance, audit and tax.

Further this report includes preparation and presentation of financial statements for

unincorporated business and advantages and disadvantages of budgetary control. With the help

of Financial ratios company evaluates the financial performance

MAIN BODY

1. Analysis the accounting function within an enterprises

Accounting functions are the set of the financial activities which helps in identifying, assessing

and recording the transactions that are in the financial form. The prime objective of accounting

function is to maintain the records and the book keeping. It helps in the collection and storing of

the information that are related to the activities which are in the financial terms. It helps in

creation and keeping the accounts from the day company was incorporated to the current day.

This is to reconcile the information from the various sources. It also helps in projecting the future

financial requirement and the formation of the budgets. The financial statement provides the

information about the profit and loss incurred during the year. It shows the income statement of

the concerned period. It helps in keeping the track records of the expenses, profit margin and the

debts. It ensures the compliance of the statutory regulations and rules. The accountant assures

that the various taxes, claims, salaries, dividends, interests, depreciation, etc. are calculated

according to the laws. This accounting is used for both internal as well as external purpose. It

clears the company about its productivity, profitability, sustainability and monitoring its growth

in the next year (Azretbergenova, 2021). It analyses the trends followed by the organisations in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the previous years and making recommendations for the improvement in the financial state of the

company .

2. Evaluate the regulatory and ethical constraints within the organisation

The accounting department of the organisation performs various functions. It maintains the

various reports, creates the budgets for the various departments and maintains the data related to

the costing. It also helps in the planning for the increment in the profits, reduction in the cost,

assessing the future requirement and delivering the important information. The functions are

discussed below-

1. Preparation of the financial reports- the accountant prepares the different financial

statements. It includes the detailed information related to the assets, liabilities, debts and

equities. It also give information about the company 's current profitable state (Gotti and

Fasan, 2020).

2. Payment of salaries and wages- Accounting department keeps the records of the salaries,

wages, provident funds, employee welfare funds ,etc. It also manages the bonuses or any

extra payment being paid to the employees.

3. Monitoring the finance related transactions- In this the proper monitoring is done. It is to

check that the transactions are updated and accurate. These transactions includes the

purchases, payments and sales made during the period.

4. Payment of the utility bill- The accounting department ensures the timely payment of the

various due bills.

5. Comply with the statutory and legal obligations- an accountant should comply with the

industrial and government rules. These rules are related to the taxation policies, payment

of the wages,etc. Such rules are made to prevent the company from the payment of the

penalties for not complying (Grimm, 2021).

6. Performance review of various departments- It includes the regular check of the financial

performances and make amendments while evaluation if it founds any need. As this

performance results in the increase of the productivity and smooth running of the

operations. It also compares the current performance of the company with the current

year 's financial statements. .

7. To avail the records to the auditor- An accountant should available all the financial

records before the auditor. So that the auditing of the enterprise will be done smoothly.

company .

2. Evaluate the regulatory and ethical constraints within the organisation

The accounting department of the organisation performs various functions. It maintains the

various reports, creates the budgets for the various departments and maintains the data related to

the costing. It also helps in the planning for the increment in the profits, reduction in the cost,

assessing the future requirement and delivering the important information. The functions are

discussed below-

1. Preparation of the financial reports- the accountant prepares the different financial

statements. It includes the detailed information related to the assets, liabilities, debts and

equities. It also give information about the company 's current profitable state (Gotti and

Fasan, 2020).

2. Payment of salaries and wages- Accounting department keeps the records of the salaries,

wages, provident funds, employee welfare funds ,etc. It also manages the bonuses or any

extra payment being paid to the employees.

3. Monitoring the finance related transactions- In this the proper monitoring is done. It is to

check that the transactions are updated and accurate. These transactions includes the

purchases, payments and sales made during the period.

4. Payment of the utility bill- The accounting department ensures the timely payment of the

various due bills.

5. Comply with the statutory and legal obligations- an accountant should comply with the

industrial and government rules. These rules are related to the taxation policies, payment

of the wages,etc. Such rules are made to prevent the company from the payment of the

penalties for not complying (Grimm, 2021).

6. Performance review of various departments- It includes the regular check of the financial

performances and make amendments while evaluation if it founds any need. As this

performance results in the increase of the productivity and smooth running of the

operations. It also compares the current performance of the company with the current

year 's financial statements. .

7. To avail the records to the auditor- An accountant should available all the financial

records before the auditor. So that the auditing of the enterprise will be done smoothly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8. Monitoring the financial transactions- The account manager maintains the records of the

financial transactions which are related to the receipts ,payments, incomes and expenses.

9. Maintaining the records in electronic form- Nowadays, the accounting involves the

updating, maintaining and creating the accounting in the digital form . This helps in

maintaining the data for the long time (Khot, 2020).

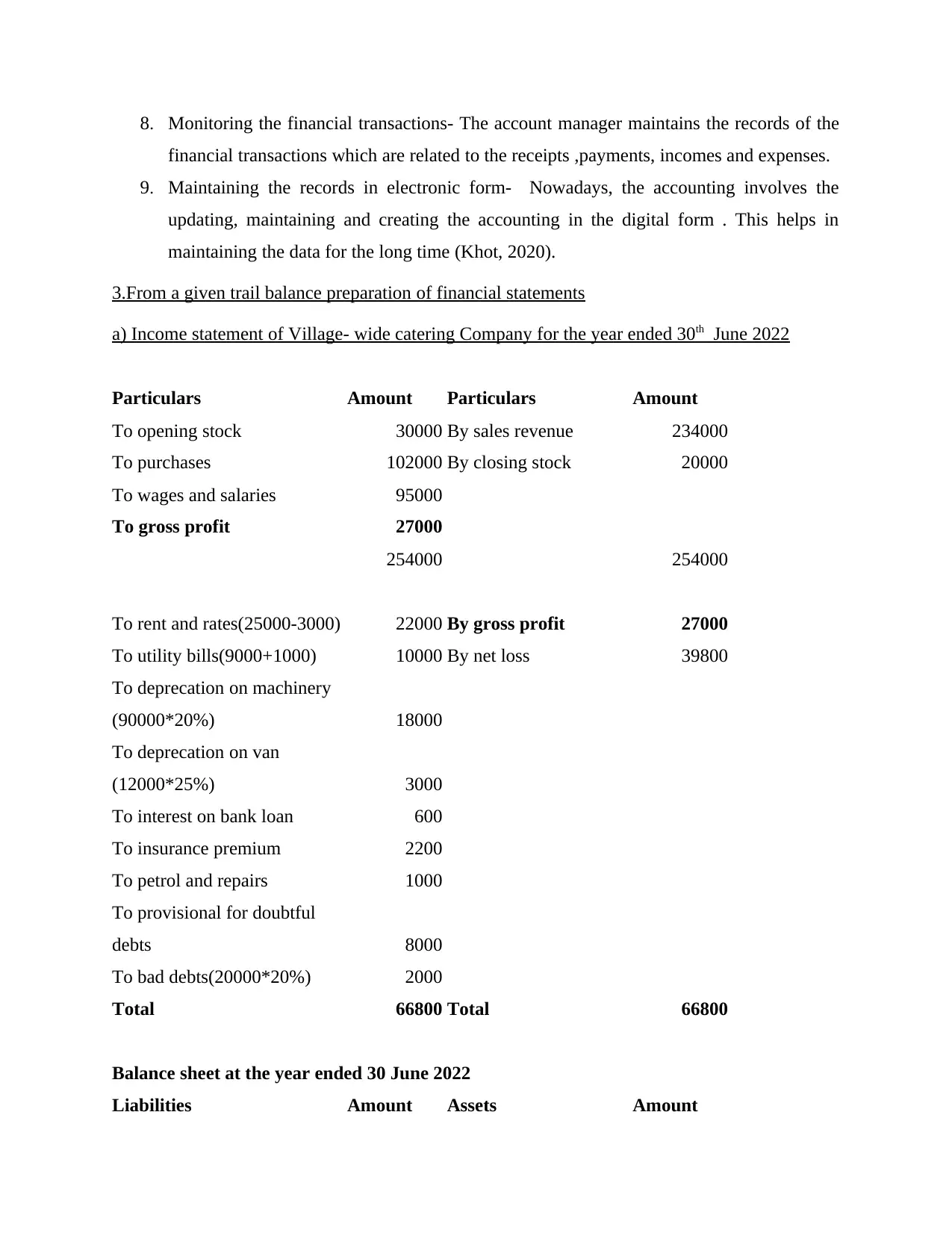

3.From a given trail balance preparation of financial statements

a) Income statement of Village- wide catering Company for the year ended 30th June 2022

Particulars Amount Particulars Amount

To opening stock 30000 By sales revenue 234000

To purchases 102000 By closing stock 20000

To wages and salaries 95000

To gross profit 27000

254000 254000

To rent and rates(25000-3000) 22000 By gross profit 27000

To utility bills(9000+1000) 10000 By net loss 39800

To deprecation on machinery

(90000*20%) 18000

To deprecation on van

(12000*25%) 3000

To interest on bank loan 600

To insurance premium 2200

To petrol and repairs 1000

To provisional for doubtful

debts 8000

To bad debts(20000*20%) 2000

Total 66800 Total 66800

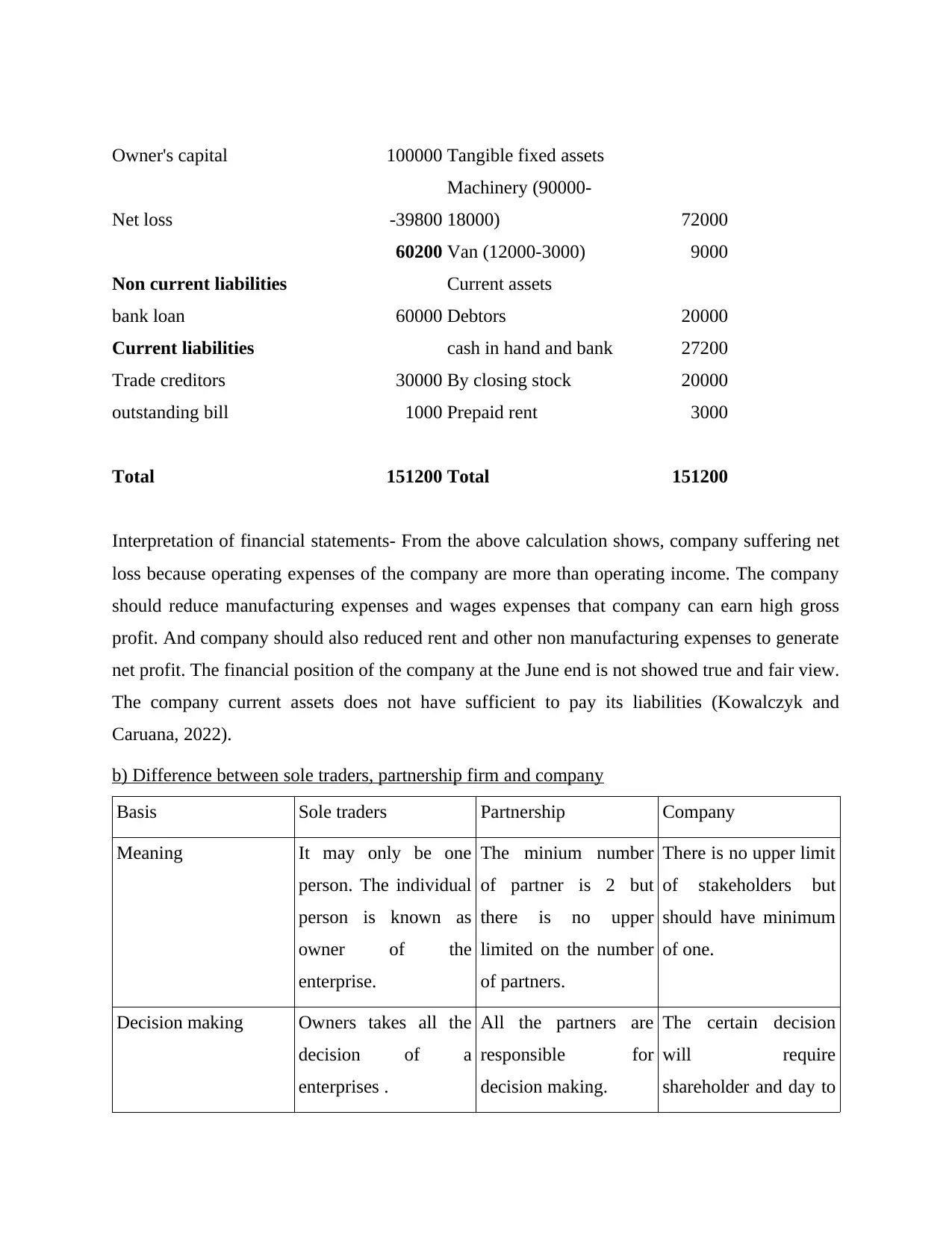

Balance sheet at the year ended 30 June 2022

Liabilities Amount Assets Amount

financial transactions which are related to the receipts ,payments, incomes and expenses.

9. Maintaining the records in electronic form- Nowadays, the accounting involves the

updating, maintaining and creating the accounting in the digital form . This helps in

maintaining the data for the long time (Khot, 2020).

3.From a given trail balance preparation of financial statements

a) Income statement of Village- wide catering Company for the year ended 30th June 2022

Particulars Amount Particulars Amount

To opening stock 30000 By sales revenue 234000

To purchases 102000 By closing stock 20000

To wages and salaries 95000

To gross profit 27000

254000 254000

To rent and rates(25000-3000) 22000 By gross profit 27000

To utility bills(9000+1000) 10000 By net loss 39800

To deprecation on machinery

(90000*20%) 18000

To deprecation on van

(12000*25%) 3000

To interest on bank loan 600

To insurance premium 2200

To petrol and repairs 1000

To provisional for doubtful

debts 8000

To bad debts(20000*20%) 2000

Total 66800 Total 66800

Balance sheet at the year ended 30 June 2022

Liabilities Amount Assets Amount

Owner's capital 100000 Tangible fixed assets

Net loss -39800

Machinery (90000-

18000) 72000

60200 Van (12000-3000) 9000

Non current liabilities Current assets

bank loan 60000 Debtors 20000

Current liabilities cash in hand and bank 27200

Trade creditors 30000 By closing stock 20000

outstanding bill 1000 Prepaid rent 3000

Total 151200 Total 151200

Interpretation of financial statements- From the above calculation shows, company suffering net

loss because operating expenses of the company are more than operating income. The company

should reduce manufacturing expenses and wages expenses that company can earn high gross

profit. And company should also reduced rent and other non manufacturing expenses to generate

net profit. The financial position of the company at the June end is not showed true and fair view.

The company current assets does not have sufficient to pay its liabilities (Kowalczyk and

Caruana, 2022).

b) Difference between sole traders, partnership firm and company

Basis Sole traders Partnership Company

Meaning It may only be one

person. The individual

person is known as

owner of the

enterprise.

The minium number

of partner is 2 but

there is no upper

limited on the number

of partners.

There is no upper limit

of stakeholders but

should have minimum

of one.

Decision making Owners takes all the

decision of a

enterprises .

All the partners are

responsible for

decision making.

The certain decision

will require

shareholder and day to

Net loss -39800

Machinery (90000-

18000) 72000

60200 Van (12000-3000) 9000

Non current liabilities Current assets

bank loan 60000 Debtors 20000

Current liabilities cash in hand and bank 27200

Trade creditors 30000 By closing stock 20000

outstanding bill 1000 Prepaid rent 3000

Total 151200 Total 151200

Interpretation of financial statements- From the above calculation shows, company suffering net

loss because operating expenses of the company are more than operating income. The company

should reduce manufacturing expenses and wages expenses that company can earn high gross

profit. And company should also reduced rent and other non manufacturing expenses to generate

net profit. The financial position of the company at the June end is not showed true and fair view.

The company current assets does not have sufficient to pay its liabilities (Kowalczyk and

Caruana, 2022).

b) Difference between sole traders, partnership firm and company

Basis Sole traders Partnership Company

Meaning It may only be one

person. The individual

person is known as

owner of the

enterprise.

The minium number

of partner is 2 but

there is no upper

limited on the number

of partners.

There is no upper limit

of stakeholders but

should have minimum

of one.

Decision making Owners takes all the

decision of a

enterprises .

All the partners are

responsible for

decision making.

The certain decision

will require

shareholder and day to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

day decision are taken

by the directors of the

company.

Liability Individual is

responsible for all

liabilities of the

business. If business

does not have

sufficient assets to pay

its debt then personal

assets of the owner can

be used.

If business does not

have enough funds to

pay its liabilities then

individual partner is

responsible to pay the

debts from their own

capital.

The company is

separate legal entity

therefore no

shareholders are

responsible to pay any

debts owed to the

company.

Tax incentives and tax Individual pay tax on

their business profits.

Taxes of the firm is

paid on their profits.

Company can seek tax

benefits although there

are many schemes

available.

Transparency and

accounts

There is no need to file

the annual accounts

but it is needed to

maintain the business

expenses.

Partners are

responsible to

maintain the records of

income and expenses.

Company must

prepare the final

accounts at the end of

the financial year.

The financial statements of individual depends on the book accounting concept which

means liabilities and shareholder equity equal assets. In according to this manner enterprise's

liabilities, stakeholder equity and assets, that is alluded to as business owner's equity on account

of a sole individual (Li, Li and Wang, 2019).

The partnership firms prepares balance sheet with the cash and cash equivalents at the

starting followed by fixed assets and current and then liabilities. The profit and loss account is

prepared as similar to sole proprietor but in additionally prepares Profit and loss appropriation

and partner's capital account.

by the directors of the

company.

Liability Individual is

responsible for all

liabilities of the

business. If business

does not have

sufficient assets to pay

its debt then personal

assets of the owner can

be used.

If business does not

have enough funds to

pay its liabilities then

individual partner is

responsible to pay the

debts from their own

capital.

The company is

separate legal entity

therefore no

shareholders are

responsible to pay any

debts owed to the

company.

Tax incentives and tax Individual pay tax on

their business profits.

Taxes of the firm is

paid on their profits.

Company can seek tax

benefits although there

are many schemes

available.

Transparency and

accounts

There is no need to file

the annual accounts

but it is needed to

maintain the business

expenses.

Partners are

responsible to

maintain the records of

income and expenses.

Company must

prepare the final

accounts at the end of

the financial year.

The financial statements of individual depends on the book accounting concept which

means liabilities and shareholder equity equal assets. In according to this manner enterprise's

liabilities, stakeholder equity and assets, that is alluded to as business owner's equity on account

of a sole individual (Li, Li and Wang, 2019).

The partnership firms prepares balance sheet with the cash and cash equivalents at the

starting followed by fixed assets and current and then liabilities. The profit and loss account is

prepared as similar to sole proprietor but in additionally prepares Profit and loss appropriation

and partner's capital account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The financial statements of company is prepared in according to companies act. The

shareholder funds shows the equity share capital, preference hare capital and net profit

(Mathews, 2020).

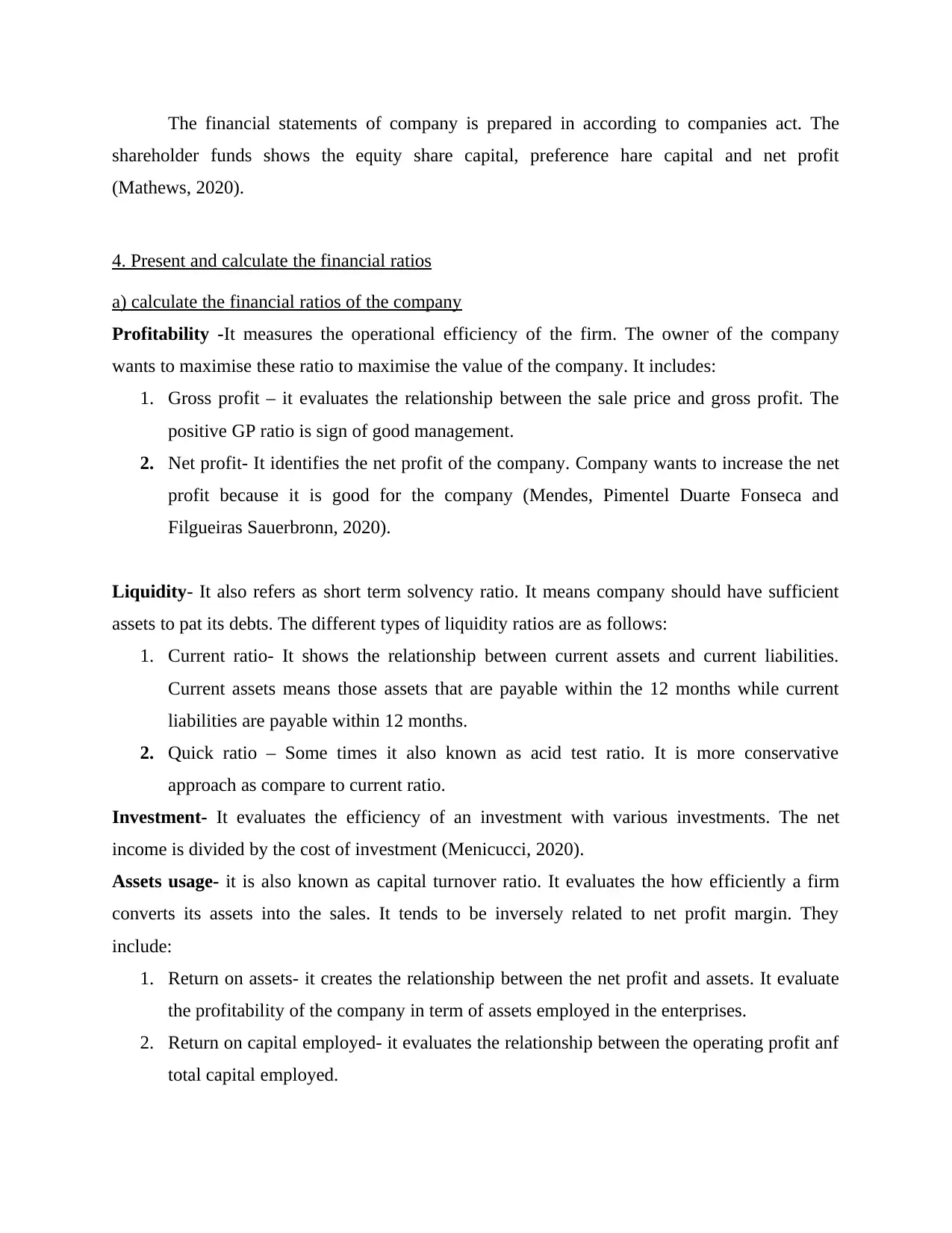

4. Present and calculate the financial ratios

a) calculate the financial ratios of the company

Profitability -It measures the operational efficiency of the firm. The owner of the company

wants to maximise these ratio to maximise the value of the company. It includes:

1. Gross profit – it evaluates the relationship between the sale price and gross profit. The

positive GP ratio is sign of good management.

2. Net profit- It identifies the net profit of the company. Company wants to increase the net

profit because it is good for the company (Mendes, Pimentel Duarte Fonseca and

Filgueiras Sauerbronn, 2020).

Liquidity- It also refers as short term solvency ratio. It means company should have sufficient

assets to pat its debts. The different types of liquidity ratios are as follows:

1. Current ratio- It shows the relationship between current assets and current liabilities.

Current assets means those assets that are payable within the 12 months while current

liabilities are payable within 12 months.

2. Quick ratio – Some times it also known as acid test ratio. It is more conservative

approach as compare to current ratio.

Investment- It evaluates the efficiency of an investment with various investments. The net

income is divided by the cost of investment (Menicucci, 2020).

Assets usage- it is also known as capital turnover ratio. It evaluates the how efficiently a firm

converts its assets into the sales. It tends to be inversely related to net profit margin. They

include:

1. Return on assets- it creates the relationship between the net profit and assets. It evaluate

the profitability of the company in term of assets employed in the enterprises.

2. Return on capital employed- it evaluates the relationship between the operating profit anf

total capital employed.

shareholder funds shows the equity share capital, preference hare capital and net profit

(Mathews, 2020).

4. Present and calculate the financial ratios

a) calculate the financial ratios of the company

Profitability -It measures the operational efficiency of the firm. The owner of the company

wants to maximise these ratio to maximise the value of the company. It includes:

1. Gross profit – it evaluates the relationship between the sale price and gross profit. The

positive GP ratio is sign of good management.

2. Net profit- It identifies the net profit of the company. Company wants to increase the net

profit because it is good for the company (Mendes, Pimentel Duarte Fonseca and

Filgueiras Sauerbronn, 2020).

Liquidity- It also refers as short term solvency ratio. It means company should have sufficient

assets to pat its debts. The different types of liquidity ratios are as follows:

1. Current ratio- It shows the relationship between current assets and current liabilities.

Current assets means those assets that are payable within the 12 months while current

liabilities are payable within 12 months.

2. Quick ratio – Some times it also known as acid test ratio. It is more conservative

approach as compare to current ratio.

Investment- It evaluates the efficiency of an investment with various investments. The net

income is divided by the cost of investment (Menicucci, 2020).

Assets usage- it is also known as capital turnover ratio. It evaluates the how efficiently a firm

converts its assets into the sales. It tends to be inversely related to net profit margin. They

include:

1. Return on assets- it creates the relationship between the net profit and assets. It evaluate

the profitability of the company in term of assets employed in the enterprises.

2. Return on capital employed- it evaluates the relationship between the operating profit anf

total capital employed.

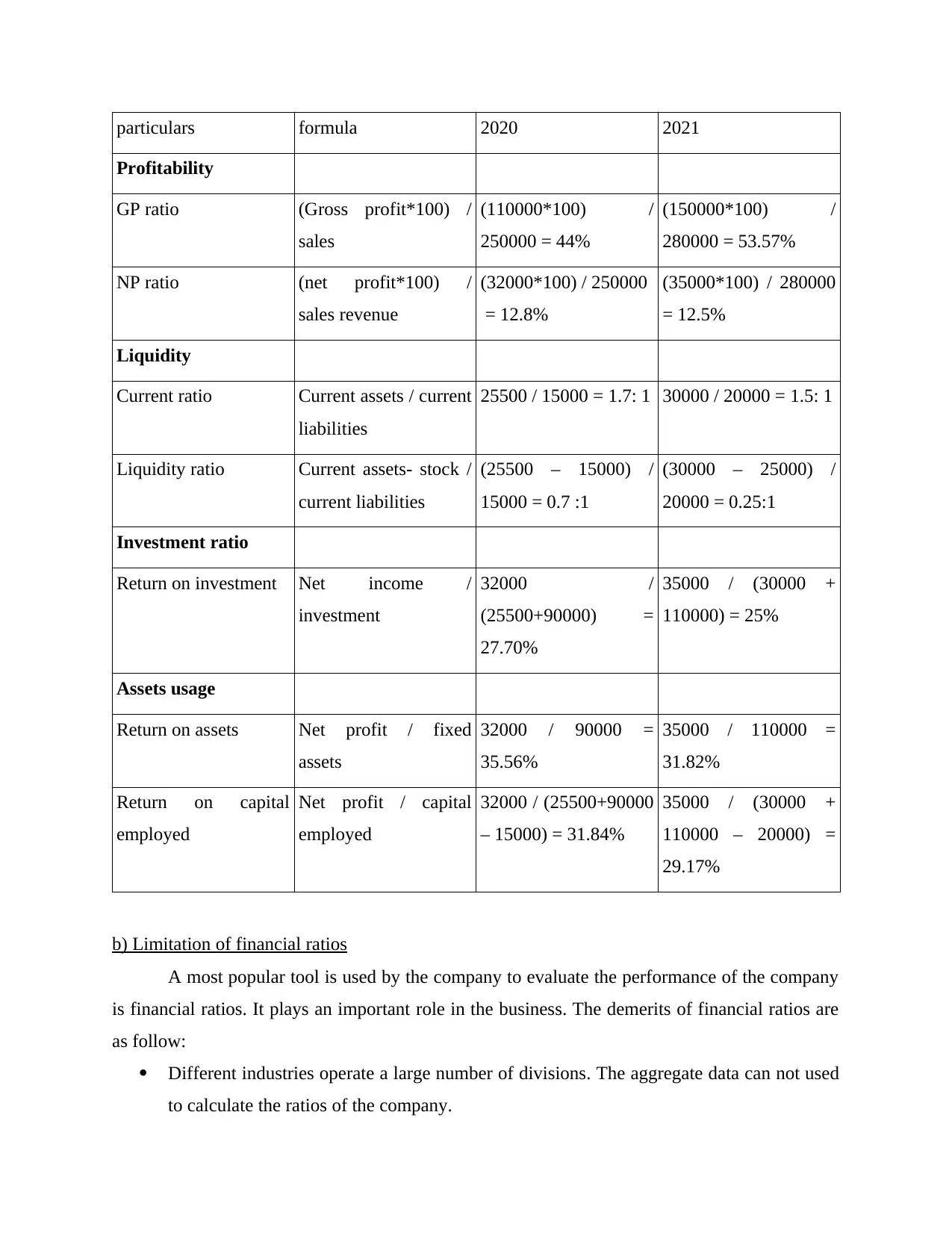

particulars formula 2020 2021

Profitability

GP ratio (Gross profit*100) /

sales

(110000*100) /

250000 = 44%

(150000*100) /

280000 = 53.57%

NP ratio (net profit*100) /

sales revenue

(32000*100) / 250000

= 12.8%

(35000*100) / 280000

= 12.5%

Liquidity

Current ratio Current assets / current

liabilities

25500 / 15000 = 1.7: 1 30000 / 20000 = 1.5: 1

Liquidity ratio Current assets- stock /

current liabilities

(25500 – 15000) /

15000 = 0.7 :1

(30000 – 25000) /

20000 = 0.25:1

Investment ratio

Return on investment Net income /

investment

32000 /

(25500+90000) =

27.70%

35000 / (30000 +

110000) = 25%

Assets usage

Return on assets Net profit / fixed

assets

32000 / 90000 =

35.56%

35000 / 110000 =

31.82%

Return on capital

employed

Net profit / capital

employed

32000 / (25500+90000

– 15000) = 31.84%

35000 / (30000 +

110000 – 20000) =

29.17%

b) Limitation of financial ratios

A most popular tool is used by the company to evaluate the performance of the company

is financial ratios. It plays an important role in the business. The demerits of financial ratios are

as follow:

Different industries operate a large number of divisions. The aggregate data can not used

to calculate the ratios of the company.

Profitability

GP ratio (Gross profit*100) /

sales

(110000*100) /

250000 = 44%

(150000*100) /

280000 = 53.57%

NP ratio (net profit*100) /

sales revenue

(32000*100) / 250000

= 12.8%

(35000*100) / 280000

= 12.5%

Liquidity

Current ratio Current assets / current

liabilities

25500 / 15000 = 1.7: 1 30000 / 20000 = 1.5: 1

Liquidity ratio Current assets- stock /

current liabilities

(25500 – 15000) /

15000 = 0.7 :1

(30000 – 25000) /

20000 = 0.25:1

Investment ratio

Return on investment Net income /

investment

32000 /

(25500+90000) =

27.70%

35000 / (30000 +

110000) = 25%

Assets usage

Return on assets Net profit / fixed

assets

32000 / 90000 =

35.56%

35000 / 110000 =

31.82%

Return on capital

employed

Net profit / capital

employed

32000 / (25500+90000

– 15000) = 31.84%

35000 / (30000 +

110000 – 20000) =

29.17%

b) Limitation of financial ratios

A most popular tool is used by the company to evaluate the performance of the company

is financial ratios. It plays an important role in the business. The demerits of financial ratios are

as follow:

Different industries operate a large number of divisions. The aggregate data can not used

to calculate the ratios of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The true values may be substantially different from historical value. It may influence the

financial data (Olomskaya, Tkhagapso and Khot, 2020).

Two firms non comparable can make the accounting data.

High current ratio may not be good as this may results from insufficient working capital

management.

5. Evaluate the financial performance by using financial ratios

In the above calculation shows, in 2021 the GP ratio is better than as compare to 2020. In

2020 the GP ratio shows 44% whether 2021 is showed 53.75%. But net profit in 2020 is better

than as compare to 2021. The company should reduce its non operating expenses. The solvency

ratio of the company is better in 2020 because in 2020 company have more assets to pay its short

term debt but the current ratio and acid test ratio are less than ideal ratio. Company must

maintain enough current assets. In 2020 the return on investment is good because company earn

more profit to utilise its fixed assets (Puri and Singh, 2021).

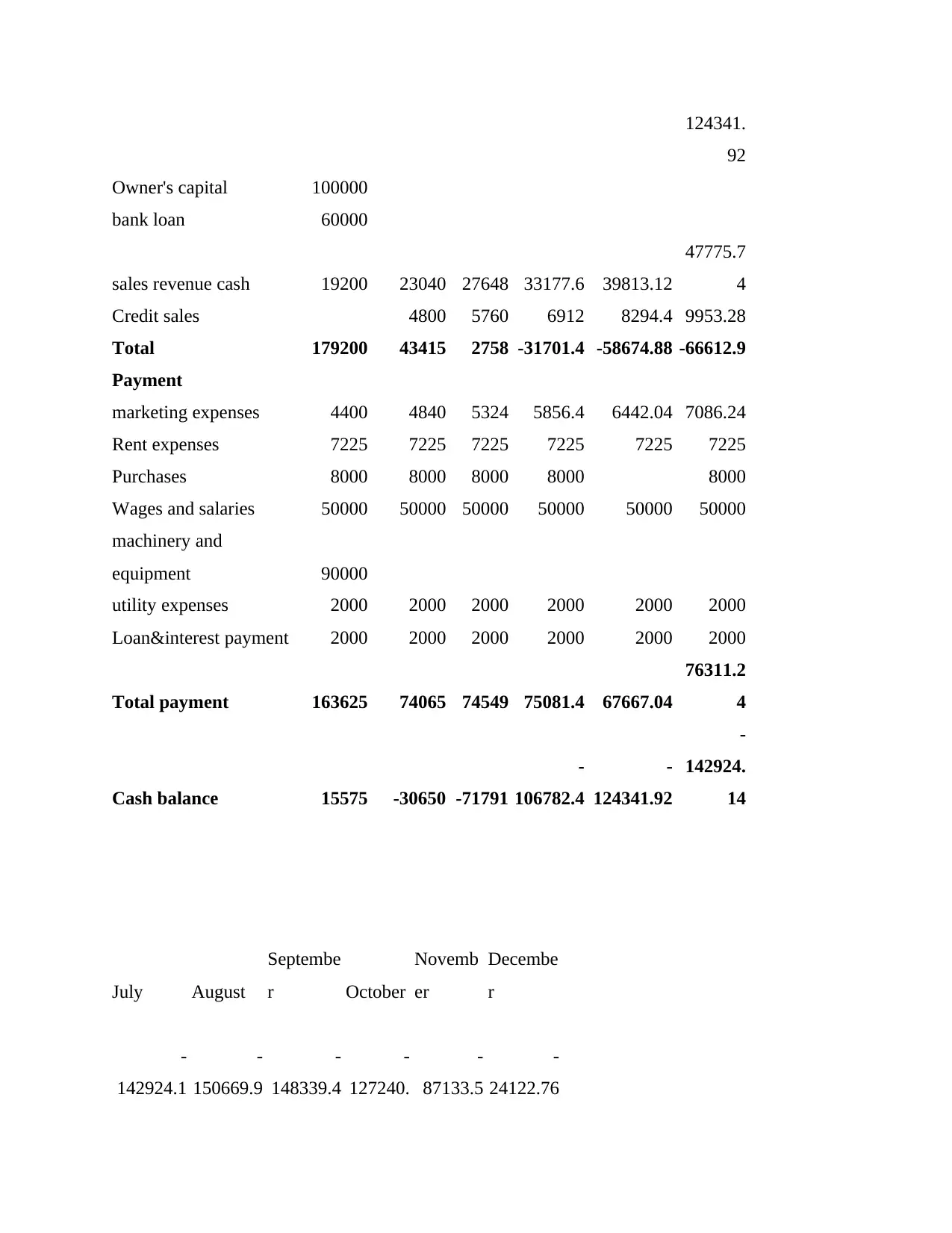

6. Cash budget

a) Cash Budget of the Village – Wide catering company

The cash budget is the pre prediction of the outflows and the inflows of the cash in the

next fiscal year or in the future. This budget is prepared to determine whether the organisation

has sufficient funds to continue the operations over the period of time. It could be weekly,

monthly, yearly or quarterly. In this the company manges its expenses and sales to attain the

optimum level. For the efficient budget the company predicts the production, sales, profits,

expenses and incomes. The assumptions are also made in the formation of the budget. The

company also takes different ways to raise the capital if there is scarcity or insufficient liquidity

with the company. This amount can be raised by increasing the capital by selling the stock or

taking loan or increasing the debts. The long term budget includes the detailed examination or

prudent planning. As it needs to focus in the long term investments, lease payments, annual

payments of the taxes, etc (White, 2019).

Particulars January February March April May June

Receipt

opening cash balance 0 15575 -30650 -71791 -106782.4 -

financial data (Olomskaya, Tkhagapso and Khot, 2020).

Two firms non comparable can make the accounting data.

High current ratio may not be good as this may results from insufficient working capital

management.

5. Evaluate the financial performance by using financial ratios

In the above calculation shows, in 2021 the GP ratio is better than as compare to 2020. In

2020 the GP ratio shows 44% whether 2021 is showed 53.75%. But net profit in 2020 is better

than as compare to 2021. The company should reduce its non operating expenses. The solvency

ratio of the company is better in 2020 because in 2020 company have more assets to pay its short

term debt but the current ratio and acid test ratio are less than ideal ratio. Company must

maintain enough current assets. In 2020 the return on investment is good because company earn

more profit to utilise its fixed assets (Puri and Singh, 2021).

6. Cash budget

a) Cash Budget of the Village – Wide catering company

The cash budget is the pre prediction of the outflows and the inflows of the cash in the

next fiscal year or in the future. This budget is prepared to determine whether the organisation

has sufficient funds to continue the operations over the period of time. It could be weekly,

monthly, yearly or quarterly. In this the company manges its expenses and sales to attain the

optimum level. For the efficient budget the company predicts the production, sales, profits,

expenses and incomes. The assumptions are also made in the formation of the budget. The

company also takes different ways to raise the capital if there is scarcity or insufficient liquidity

with the company. This amount can be raised by increasing the capital by selling the stock or

taking loan or increasing the debts. The long term budget includes the detailed examination or

prudent planning. As it needs to focus in the long term investments, lease payments, annual

payments of the taxes, etc (White, 2019).

Particulars January February March April May June

Receipt

opening cash balance 0 15575 -30650 -71791 -106782.4 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

124341.

92

Owner's capital 100000

bank loan 60000

sales revenue cash 19200 23040 27648 33177.6 39813.12

47775.7

4

Credit sales 4800 5760 6912 8294.4 9953.28

Total 179200 43415 2758 -31701.4 -58674.88 -66612.9

Payment

marketing expenses 4400 4840 5324 5856.4 6442.04 7086.24

Rent expenses 7225 7225 7225 7225 7225 7225

Purchases 8000 8000 8000 8000 8000

Wages and salaries 50000 50000 50000 50000 50000 50000

machinery and

equipment 90000

utility expenses 2000 2000 2000 2000 2000 2000

Loan&interest payment 2000 2000 2000 2000 2000 2000

Total payment 163625 74065 74549 75081.4 67667.04

76311.2

4

Cash balance 15575 -30650 -71791

-

106782.4

-

124341.92

-

142924.

14

July August

Septembe

r October

Novemb

er

Decembe

r

-

142924.1

-

150669.9

-

148339.4

-

127240.

-

87133.5

-

24122.76

92

Owner's capital 100000

bank loan 60000

sales revenue cash 19200 23040 27648 33177.6 39813.12

47775.7

4

Credit sales 4800 5760 6912 8294.4 9953.28

Total 179200 43415 2758 -31701.4 -58674.88 -66612.9

Payment

marketing expenses 4400 4840 5324 5856.4 6442.04 7086.24

Rent expenses 7225 7225 7225 7225 7225 7225

Purchases 8000 8000 8000 8000 8000

Wages and salaries 50000 50000 50000 50000 50000 50000

machinery and

equipment 90000

utility expenses 2000 2000 2000 2000 2000 2000

Loan&interest payment 2000 2000 2000 2000 2000 2000

Total payment 163625 74065 74549 75081.4 67667.04

76311.2

4

Cash balance 15575 -30650 -71791

-

106782.4

-

124341.92

-

142924.

14

July August

Septembe

r October

Novemb

er

Decembe

r

-

142924.1

-

150669.9

-

148339.4

-

127240.

-

87133.5

-

24122.76

4 7 51 7

57330.9 65797.07 82556.48

99067.7

8

118881.

34 142657.6

11943.94 14332.72 17199.27

20639.1

2

24766.9

4 29720.33

-73649.3

-

70540.11

-

48583.72

-

7533.61

56514.7

1

148255.1

7

7794.87 8574.36 9431.79

10374.9

6

11412.4

7 12553.71

7225 7225 7225 7225 7225 7225

8000 8000 8000 8000 8000 8000

50000 50000 50000 50000 50000 50000

2000 2000 2000 2000 2000 2000

2000 2000 2000 2000 2000 2000

77019.87 77799.36 78656.79

79599.9

6

80637.4

7 81778.71

-

150669.9

-

148339.4

7

-

127240.5

1

-

87133.5

7

-

24122.7

6 66476.46

7.Discuss the benefits and limitations of budgets and budgetary planning and control of an

organisation.

Budget is a plan which is based on the expenses and the incomes. It determines that how much

money will be needed for the smooth running of the business. It examines that that the company

will have sufficient funds to fulfil the needs of the company. It plans the road map of the budget

for the next 6 months or for a year. It coordinates all the activities of the various segments of the

organisation. For the efficient budget, there will thorough study for the previous years financial

57330.9 65797.07 82556.48

99067.7

8

118881.

34 142657.6

11943.94 14332.72 17199.27

20639.1

2

24766.9

4 29720.33

-73649.3

-

70540.11

-

48583.72

-

7533.61

56514.7

1

148255.1

7

7794.87 8574.36 9431.79

10374.9

6

11412.4

7 12553.71

7225 7225 7225 7225 7225 7225

8000 8000 8000 8000 8000 8000

50000 50000 50000 50000 50000 50000

2000 2000 2000 2000 2000 2000

2000 2000 2000 2000 2000 2000

77019.87 77799.36 78656.79

79599.9

6

80637.4

7 81778.71

-

150669.9

-

148339.4

7

-

127240.5

1

-

87133.5

7

-

24122.7

6 66476.46

7.Discuss the benefits and limitations of budgets and budgetary planning and control of an

organisation.

Budget is a plan which is based on the expenses and the incomes. It determines that how much

money will be needed for the smooth running of the business. It examines that that the company

will have sufficient funds to fulfil the needs of the company. It plans the road map of the budget

for the next 6 months or for a year. It coordinates all the activities of the various segments of the

organisation. For the efficient budget, there will thorough study for the previous years financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.